The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

|

|

|

- Paul Golden

- 6 years ago

- Views:

Transcription

1 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1

2 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s Equity Section Objectives 1. Set up T accounts for assets, liabilities, and owner s equity. 2. Analyze business transactions and enter them in the accounts. 3. Determine the balance of an account. Chapter 3 3 2

3 The Accounting Equation ASSETS The property a business owns = LIABILITIES The debts of the business + OWNER S EQUITY The owner s financial interest in the business 3 3

4 Classification of Accounts Asset Accounts Asset accounts show the property a business owns. Liability Accounts Liability accounts show the debts of the business. Owner s Equity Accounts Owner s equity accounts show the owner s financial interest in the business. 3 4

5 Objective 1 Set up T accounts for assets, liabilities and owner s equity T Accounts ASSETS = + LIABILITIES OWNER S EQUITY + Record Increases - Record Decreases - Record Decreases + Record Increases - Record Decreases + Record Increases LEFT SIDE RIGHT SIDE LEFT SIDE RIGHT SIDE LEFT SIDE RIGHT SIDE 3 5

6 Objective 2 Analyze business transactions and enter them in the accounts Effects of Business Transactions Steps to analyze the effects of the business transactions: 1. Analyze the financial event. Identify the accounts affected. Classify the accounts affected. Determine the amount of increase or decrease for each account. 2. Apply the left-side-right side rules for each account affected. 3. Make the entry in T-account form. 3 6

7 Initial Investment Carolyn Wells withdrew $100,000 from personal savings and deposited it in the new business checking account for Wells Consulting Services. LEFT Increases to asset accounts are recorded on the left side of the T account. RIGHT Increases to owner s equity accounts are recorded on the right side of the T account. Cash Carolyn Wells, Capital (a) 100,000 (a) 100,

8 Business Transaction Wells Consulting Services issued a $5,000 check to purchase a computer and other equipment. Analysis: (b) The asset account, Equipment, is increased by $5,000. (b) The asset account, Cash, is decreased by $5,000. Equipment Cash (b) 5,000 (b) 5,

9 Purchase of Equipment on Account The firm bought office equipment for $6,000 on account from Office Plus. Analysis: (c) The asset account, Equipment, is increased by $6,000. (c) The liability account, Accounts Payable, is increased by $6,000. Equipment Accounts Payable (c) 6,000 (c) 6,

10 Purchase of Supplies for Cash Wells Consulting Services issued a check for $1,500 to Office Delux Inc. to purchase office supplies. Analysis: (d) The asset account, Supplies, is increased by $1,500. (d) The asset account, Cash, is decreased by $1,500. Supplies Cash (d) 1,500 (d) 1,

11 Payment of a Liability Wells Consulting Services issued a check in the amount of $2,500 to Office Plus. Analysis: (e) The asset account, Cash, is decreased by $2,500. (e) The liability account, Accounts Payable, is decreased by $2,500. Accounts Payable Cash (e) 2,500 (e) 2,

12 Prepayment of Rent Wells Consulting Services issued a check for $8,000 to pay rent for the months of December and January. Analysis: (f) The asset account, Prepaid Rent, is increased by $8,000. (f) The asset account, Cash, is decreased by $8,000. Prepaid Rent (f) 8,000 Cash (f) 8,

13 Objective 3 Determine the balance of an account An account balance is the difference between the amounts recorded on the two sides of an account. A footing is a small pencil figure written at the base of an amount column showing the sum of the entries in the column. 3 13

14 Recording Account Balances IF the total on the right side is larger than the total on the left side, the total on the left side is larger, an account shows only one amount, THEN the balance is recorded on the right side. the balance is recorded on the left side. that amount is the balance. an account contains entries on only one side, the total of those entries is the account balance. 3 14

15 Computing the Account Balance Cash (a) 100,000 (b) 5,000 Bal. 83,000 (d) 1,500 (e) 2,500 (f) 8, ,000 Footing (100,000 17,000) 3 15

16 Summary of Account Balances ASSETS = LIABILITIES + OWNER S EQUITY Cash Accounts Payable Carolyn Wells, Capital Account balances for Carter Consulting (d) 1,500 Bal. 3,500 Services (e) 2,500 (a) 100,000 (b) 5,000 ( e) 2,500 (c) 6,000 (b) 100,000 (f) 8,000 Bal. 83,000 17,000 (d) 1,500 Supplies SUMMARY OF ACCOUNT BALANCES ASSETS = LIABILITIES + OWNER S EQUITY Prepaid Rent 83,000 3, ,000 1,500 (f) 8,000 8,000 11,000 Equipment 103,500 = 3, ,000 (b) 5,000 (c) 6,000 Bal. 11,

17 Chapter Analyzing Business Transactions Using T Accounts 3 Section 2: Transactions That Affect Revenue, Expenses, and Withdrawals Section Objectives 4. Set up T accounts for revenue and expenses. 5. Prepare a trial balance from T accounts. 6. Prepare an income statement, a statement of owner s equity, and a balance sheet. 7. Develop a chart of accounts. 3 17

18 Owner s Equity T-Account for Revenue Decrease Side Increase Side Revenue Decrease Increase Side Side Revenues increase owner s equity. Increases in owner s equity appear on the right side of the T account. Therefore, increases in revenue appear on the right side of revenue T accounts. 3 18

19 Revenue Decrease Side Increase Side The right side of the revenue account shows increases and the left side shows decreases. Decreases in revenue accounts are rare but might occur because of corrections or transfers. 3 19

20 Objective 4 Set up T accounts for revenue and expenses Recording Revenue from Services Sold for Cash Bal. 83,000 (g) 36,000 Cash Fees Income (g) 36,000 $36,000 (m) is entered on the left (increase) side of the asset account Cash. $36,000 (n) is entered on the right side of the Fees Income account. 3 20

21 Recording Revenue from Services Sold on Credit In December Wells Consulting Services earned $11,000 from various charge account clients. Analysis: (h) The asset account, Accounts Receivable, is increased by $11,000. (h) The revenue account, Fees Income, is increased by $11,000. Accounts Receivable (h) 11,000 Fees Income (h) 11,

22 Analysis: Receipt of Payments on Account Charge account clients paid $6,000, reducing the amount owed to Wells Consulting Services. (i) The asset account, Cash, is increased by $6,000. (i) The asset account, Accounts Receivable, is decreased by $6,000. Cash Accounts Receivable (i) 6,000 (i) 6,

23 Owner s Equity Decrease Side Increase Side Expense Revenue Increase Side Decrease Side Decrease Side Increase Side Expenses decrease owner s equity. Decreases in owner s equity appear on the left side of the T accounts. 3 23

24 Payment of Salaries In December Wells Consulting Services paid $8,000 in salaries. Analysis: (j) The asset account, Cash, is decreased by $8,000. (j) The expense account, Salaries Expense, is increased by $8,000. Salaries Expense Cash (j) 8,000 (j) 8,

25 Payment of Utilities Wells Consulting Services issued a check for $650 to pay the utilities bill. Analysis: (k) The asset account, Cash, is decreased by $650. (k) The expense account, Utilities Expense, is increased by $650. Utilities Expense Cash (k)650 (k)

26 Owner Withdrawals Owner s Equity Decrease Side Increase Side Increase Side Expense Decrease Side Decrease Side Revenue Increase Side Owner Drawing Increase Side Decrease Side Drawing decreases owner s equity. Decreases in owner s equity appear on the left side of the T accounts. 3 26

27 Carolyn Wells wrote a check to withdraw $5,000 cash for personal use. Analysis: The Owner Withdraws Funds (l) The asset account, Cash, is decreased by $5,000. (l) The owner s equity account, Carolyn Wells, Drawing, is increased by $5,000. Carolyn Wells, Drawing Cash (l) 5,000 (l) 5,

28 The Rules of Debit and Credit A debit is an entry on the left side of an account. A credit is an entry on the right side of an account. A double-entry system is an accounting system that involves recording the effects of each transaction as debits and credits in separate accounts. Every transaction in a Double entry accounting system has at least one debit and one credit. Every transaction must have at least one debit and one credit. The total of the debits and credits recorded in the separate accounts must be EQUAL. 3 28

29 Any Account Left Side Right Side Accountants refer to the left side of an account as the debit side instead of saying the left side. The right side of the account is called the credit side. 3 29

30 Rules for Debits and Credits 3 30

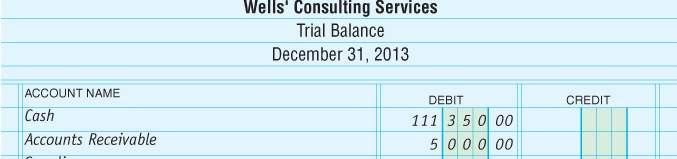

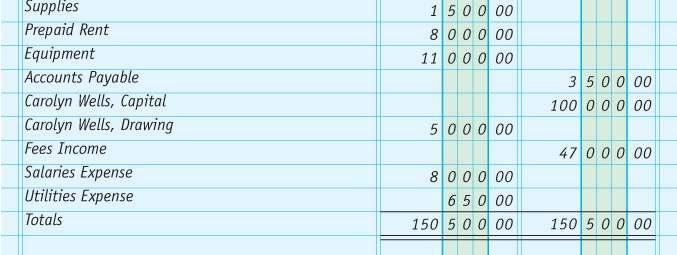

31 Objective 5 Objective 5 Prepare a trial balance from T accounts 1. Use the proper heading to include who, what, and when information. 2. List the accounts in chart of account order or in the same order as they appear in the financial statement. 3. Enter the ending balance of each account in the appropriate Debit or Credit column. 4. Total the Debit column. 5. Total the Credit column. 6. Compare the column totals. They should be equal. 3 31

32 3 32

33 Some common errors in a trial balance are: Adding trial balance columns incorrectly Recording only half a transaction for example, recording a debit but not recording a credit, or vice versa Recording both halves of a transaction as debits or credits rather than recording one debit and one credit Recording the incorrect amount for a transaction Recording a debit for one amount and a credit for a different amount Mathematical errors in calculating account balances Forgetting to carry over an account balance to the Trial Balance 3 33

34 Objective 6 Prepare an income statement, a statement of owner s equity, and a balance sheet After the trial balance is prepared, the financial statements are prepared. Net income from the income statement is used on the statement of owner s equity. The ending balance of the Carolyn Wells, Capital account, computed on the statement of owner s equity, is used on the balance sheet. 3 34

35 Wells CONSULTING SERVICES Income Statement Month Ended December 31, 2013 Revenue Fees Income 47, Expenses Salaries Expense 8, Utilities Expense Total Expenses 8, Net Income 38, Wells CONSULTING SERVICES Statement Of Owner s Equity Month Ended December 31, 2013 Carolyn Wells, Capital, Dec. 1, , Net Income for December 38, Less Withdrawals for December 5, Increase in Capital 33, Carolyn Wells, Capital, Dec. 31, , Wells CONSULTING SERVICES Balance Sheet December 31, 2013 ASSETS LIABILITIES Cash 111, Accounts Payable 3, Accounts Receivable 5, Supplies 1, Prepaid Rent 8, OWNER S EQUITY Equipment 11, Carolyn Wells, Capital 133, Total Assets 136, Total Liabilities and Owner s Equity 136,

36 Objective 7 Develop a chart of accounts Each account has a number and a name. The balance sheet accounts are listed first, followed by the income statement accounts. The account number is assigned based on the type of account. Each account should have a number assigned to it s title (name) Balance Sheet accounts are listed before income statement accounts. 3 36

37 3 37

38 Permanent and Temporary Accounts A permanent account is an account that is kept open from one accounting period to the next. A temporary account is an account whose balance is transferred to another account at the end of an accounting period. A temporary account is zeroed out at the end of the accounting period. 3 38

39 Thank You for using College Accounting, 13th Edition Price Haddock Farina 3 39

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Analyzing Business Transactions

2-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 2 Analyzing Business Transactions Section 1: Property and Financial Interest Section Objectives 1. Record in equation form

2-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 2 Analyzing Business Transactions Section 1: Property and Financial Interest Section Objectives 1. Record in equation form

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Heintz & Parry. 20 th Edition. College Accounting

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

Week 5, Chap 4 Part 1

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

The General Journal and the General Ledger

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

Chapter 2 Analyzing Business Transactions

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

Chapter 02 Analyzing Business Transactions

College Accounting A Contemporary Approach 4th Edition Haddock TEST BANK Full download at: https://testbankreal.com/download/college-accounting-contemporary-approach-4thedition-haddock-test-bank/ College

College Accounting A Contemporary Approach 4th Edition Haddock TEST BANK Full download at: https://testbankreal.com/download/college-accounting-contemporary-approach-4thedition-haddock-test-bank/ College

Analyzing the Accounting Equation

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

When to Debit and Credit in Accounting

When to Debit and Credit in Accounting Journal entries show a firm s transactions throughout a period of time; for example, when a company purchases supplies a journal entry will show the amount of supplies

When to Debit and Credit in Accounting Journal entries show a firm s transactions throughout a period of time; for example, when a company purchases supplies a journal entry will show the amount of supplies

Price, Haddock, Farina College Accounting, 15e

Price, Haddock, Farina College Accounting, 15e College Accounting Chapters 1 30 15th Edition Price SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/college-accounting-chapters-1-30-15th-edi

Price, Haddock, Farina College Accounting, 15e College Accounting Chapters 1 30 15th Edition Price SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/college-accounting-chapters-1-30-15th-edi

Name Date Class. Concept Assessment. Business Transactions and the Accounting Equation

Concept Assessment PART A Accounting Vocabulary (15 points) Directions: Using terms from the following list, complete the sentences below. Write the letter of the term you have chosen in the space provided.

Concept Assessment PART A Accounting Vocabulary (15 points) Directions: Using terms from the following list, complete the sentences below. Write the letter of the term you have chosen in the space provided.

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

ACCT 151A WEEK 2, CHAP 2. Instructor: Michael Booth Cabrillo College

ACCT 151A WEEK 2, CHAP 2 Instructor: Michael Booth Cabrillo College ANALYZING BUSINESS TRANSACTIONS Property and Financial Objectives Interest 1. Record in equation form the financial effects of a business

ACCT 151A WEEK 2, CHAP 2 Instructor: Michael Booth Cabrillo College ANALYZING BUSINESS TRANSACTIONS Property and Financial Objectives Interest 1. Record in equation form the financial effects of a business

Debits and Credits CHAPTER

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

COMPLETING THE ACCOUNTING CYCLE

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Chapter Outline Notes. Transactions That Affect Revenue, Expenses, and Withdrawals

Chapter Outline Notes Transactions That Affect Revenue, Expenses, and Withdrawals Section 1: Relationship of Revenue, Expenses, and Withdrawals to Owner s Equity The revenue, expense, and owner s withdrawals

Chapter Outline Notes Transactions That Affect Revenue, Expenses, and Withdrawals Section 1: Relationship of Revenue, Expenses, and Withdrawals to Owner s Equity The revenue, expense, and owner s withdrawals

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Chapter 3: The Ledger and Double-Entry Accounting System. 3. How to record in Assets, Liabilities & Owner s Equity account:

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

Dec. 4: Paid $ 750 cash for office supplies. Date Accounts Debit Credit Dec. 4 Office Supplies 750 Cash 750

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Reporting and Analyzing Cash Flows

Chapter 17 Reporting and Analyzing Cash Flows QUICK STUDY SOLUTIONS Quick Study 17-1 (10 minutes) 1. Operating 6. Operating 2. Operating 7. Investing 3. Financing 8 Operating 4. Financing 9. Operating

Chapter 17 Reporting and Analyzing Cash Flows QUICK STUDY SOLUTIONS Quick Study 17-1 (10 minutes) 1. Operating 6. Operating 2. Operating 7. Investing 3. Financing 8 Operating 4. Financing 9. Operating

Chapter Outline Notes. Business Transactions and the Accounting Equation

Chapter Outline Notes Section 1: Property and Financial Claims A. Property property anything of value that a person or business owns and therefore controls When you own an item of property, you have a

Chapter Outline Notes Section 1: Property and Financial Claims A. Property property anything of value that a person or business owns and therefore controls When you own an item of property, you have a

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Full file at Chapter 2: Analyzing Business Transactions

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

9 Payments, and Banking Procedures. Cash Receipts, Cash

9-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Cash Receipts, Cash 9 Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts

9-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Cash Receipts, Cash 9 Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts

Chapter 4 Completing the Accounting Cyclt 163

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Chapter 13. Annuities and Sinking Funds McGraw-Hill/Irwin. Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 13 Annuities and Sinking Funds 13-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Compounding Interest (Future Value) Annuity - A series of payments--can

Chapter 13 Annuities and Sinking Funds 13-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Compounding Interest (Future Value) Annuity - A series of payments--can

4/9/2012. Recording Transactions. Learning Objectives (LO) LO 1 Double-Entry System. LO 1 Double-Entry System. LO 1 Double-Entry System

LO 1 Double-Entry System. LO 1 Double-Entry System. LO 1 Double-Entry System") 4/9/212 Recording Transactions CHAPTER 3 Learning Objectives (LO) After studying this chapter, you should be able to 1. Use double-entry accounting 2. Describe the five steps in the recording process 3.

4/9/212 Recording Transactions CHAPTER 3 Learning Objectives (LO) After studying this chapter, you should be able to 1. Use double-entry accounting 2. Describe the five steps in the recording process 3.

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Solution Manual for College Accounting 12th Edition by Jeffrey Slater 2 Debits and Credits: Analyzing and Recording Business Transactions

Solution Manual for College Accounting 12th Edition by Jeffrey Slater 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter 2: Debits and Credits: Analyzing and Recording Business

Solution Manual for College Accounting 12th Edition by Jeffrey Slater 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter 2: Debits and Credits: Analyzing and Recording Business

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Chapter 4: The Simple Ledger

Chapter 4: The Simple Ledger 4.1: Ledger Accounts Pages 88 92 account a record that documents each change to items in the accounting equation. There is one account for each asset, each liability, and each

Chapter 4: The Simple Ledger 4.1: Ledger Accounts Pages 88 92 account a record that documents each change to items in the accounting equation. There is one account for each asset, each liability, and each

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 11 Contestant Number: Time: Rank: FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2016 CONCEPT KNOWLEDGE: True/False (20 @ 2 points each) Multiple Choice (25 @ 2 points each) APPLICATION KNOWLEDGE:

Page 1 of 11 Contestant Number: Time: Rank: FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2016 CONCEPT KNOWLEDGE: True/False (20 @ 2 points each) Multiple Choice (25 @ 2 points each) APPLICATION KNOWLEDGE:

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Examination Booklet Version 1. Bookkeeping

Examination Booklet Version 1 Bookkeeping The Accounting Equation When you feel confident that you have mastered the material in The Accounting Equation, go to and submit your answers online EXAMINATION

Examination Booklet Version 1 Bookkeeping The Accounting Equation When you feel confident that you have mastered the material in The Accounting Equation, go to and submit your answers online EXAMINATION

Week 5, Chap 4 Part 2

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Accounting I. StraighterLine does not apply letter grades. Students earn a score as a percentage of 100%. A passing percentage is 70% or higher.

Accounting I Course Text Wild, John J., Kermit D. Larson, and Barbara Chiapetta. Fundamental Accounting Principles, Volume 1, 18th edition. McGraw-Hill/Irwin, 2007. ISBN 0-07-328661-3 Course Description

Accounting I Course Text Wild, John J., Kermit D. Larson, and Barbara Chiapetta. Fundamental Accounting Principles, Volume 1, 18th edition. McGraw-Hill/Irwin, 2007. ISBN 0-07-328661-3 Course Description

Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176)

") NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

Chapter 2 MULTIPLE CHOICE

Objectives: 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to the rules of debit and credit. 3. Preparing a trial balance. 4. Preparing financial statements

Objectives: 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to the rules of debit and credit. 3. Preparing a trial balance. 4. Preparing financial statements

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Fundamental Accounting Principles

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 14 th Canadian Edition by Larson/Jensen Prepared by: Tilly Jensen, Athabasca University Wendy Popowich, Northern Alberta Institute of Technology

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 14 th Canadian Edition by Larson/Jensen Prepared by: Tilly Jensen, Athabasca University Wendy Popowich, Northern Alberta Institute of Technology

Payroll Taxes, Deposits, and Reports

11-1 McGraw-Hill Payroll Taxes, Deposits, and Reports Section 1: Social Security, Medicare, and Employee Income Tax Section Objectives Chapter 1. Explain how and when payroll taxes are paid to the government.

11-1 McGraw-Hill Payroll Taxes, Deposits, and Reports Section 1: Social Security, Medicare, and Employee Income Tax Section Objectives Chapter 1. Explain how and when payroll taxes are paid to the government.

Business Accounts. That sounds a little confusing. All the accounts of a business are grouped together in a ledger.

Business Accounts An account is a location within an accounting system in which the increases and decreases in a specific asset, liability, or owner s equity are recorded and stored. That sounds a little

Business Accounts An account is a location within an accounting system in which the increases and decreases in a specific asset, liability, or owner s equity are recorded and stored. That sounds a little

Accounting I. Lesson Plan. Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Cash Payments Unit: 3 Chapter 11

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Accounting for Business Transactions QUESTIONS

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Chapter 2 Recording Business Transactions

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

on the land. be treated as an expense of the business. company should credit an unearned revenues account for the amount charged to the customer.

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) The first step in the accounting cycle is transaction analysis. 2) An account is a detailed record of increases and

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) The first step in the accounting cycle is transaction analysis. 2) An account is a detailed record of increases and

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

CHAPTER 2 Solutions ANALYZING AND RECORDING BUSINESS TRANSACTIONS

Principles of Financial Accounting 12th Edition Needles Solutions Manual Full Download: http://testbanklive.com/download/principles-of-financial-accounting-12th-edition-needles-solutions-manual/ CHAPTER

Principles of Financial Accounting 12th Edition Needles Solutions Manual Full Download: http://testbanklive.com/download/principles-of-financial-accounting-12th-edition-needles-solutions-manual/ CHAPTER

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

Property is anything of value that is owned or controlled. Financial Claim is the legal right to an item or property.

Property and Financial Claims Property is anything of value that is owned or controlled. Financial Claim is the legal right to an item or property. Property Rights is the creditors and the owners financial

Property and Financial Claims Property is anything of value that is owned or controlled. Financial Claim is the legal right to an item or property. Property Rights is the creditors and the owners financial

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

T Accounts, Debits and Credits, Trial Balance, and Financial Statements

2 T Accounts, s and s, Trial Balance, and Financial Statements TEACHING OBJECTIVES 1. To introduce the T account form 2. To introduce debit and credit 3. To introduce the function and preparation of a

2 T Accounts, s and s, Trial Balance, and Financial Statements TEACHING OBJECTIVES 1. To introduce the T account form 2. To introduce debit and credit 3. To introduce the function and preparation of a

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY. Y. Chang Company COVER SHEET

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Chapter 3: Double-Entry Bookkeeping

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 02 Analyzing and Recording Transactions

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Fundamental Accounting Principles

Last revised: January 23, 2016. SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 15 th Canadian Edition by Larson/Jensen/Dieckmann Revised for the 15 th Edition by: Praise Ma, Kwantlen Polytechnic

Last revised: January 23, 2016. SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 15 th Canadian Edition by Larson/Jensen/Dieckmann Revised for the 15 th Edition by: Praise Ma, Kwantlen Polytechnic

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chapter 5 Transactions that Affect Revenue, Expenses, and Withdrawals

Chapter 5 Transactions that Affect Revenue, Expenses, and Withdrawals 5.1 Relationship of Revenue, Expenses and Withdrawals to Owner s Equity Temporary and Permanent Accounts Temporary Accounts Revenue,

Chapter 5 Transactions that Affect Revenue, Expenses, and Withdrawals 5.1 Relationship of Revenue, Expenses and Withdrawals to Owner s Equity Temporary and Permanent Accounts Temporary Accounts Revenue,

CHAPTER 3 ANALYZING BUSINESS TRANSACTIONS USING T ACCOUNTS

CHAPTER 3 ANALYZING BUSINESS TRANSACTIONS USING T ACCOUNTS Chapter Opener: Thinking Critically or would have increased and Equity or the Service Revenue account would have also increased. The equation

CHAPTER 3 ANALYZING BUSINESS TRANSACTIONS USING T ACCOUNTS Chapter Opener: Thinking Critically or would have increased and Equity or the Service Revenue account would have also increased. The equation

RECORDING BUSINESS TRANSACTIONS

2 RECORDING BUSINESS TRANSACTIONS CONNECTING CHAPTER 2 LEARNING OBJECTIVE Define and use key accounting terms What are the key terms used when recording transactions? The Accounting Cycle, page 60 Chart

2 RECORDING BUSINESS TRANSACTIONS CONNECTING CHAPTER 2 LEARNING OBJECTIVE Define and use key accounting terms What are the key terms used when recording transactions? The Accounting Cycle, page 60 Chart

Chapter 2 The Accounting Information System

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

Name: Date: Period: Standard 2: Students will list and identify characteristics of the three basic accounting equation elements.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

> DO IT! Chapter 2 The Recording Process. Recording Business Activities D-7

Chapter 2 The Recording Process Normal Balances Kate Browne has just rented space in a shopping mall. In this space, she will open a hair salon to be called Hair It Is. A friend has advised Kate to set

Chapter 2 The Recording Process Normal Balances Kate Browne has just rented space in a shopping mall. In this space, she will open a hair salon to be called Hair It Is. A friend has advised Kate to set

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

City of Bingham. Cumulative Problem. For use with McGraw-Hill/Irwin Accounting for Governmental and Nonprofit Entities, 13 th Edition

City of Bingham Cumulative Problem For use with McGraw-Hill/Irwin Accounting for Governmental and Nonprofit Entities, 13 th Edition By Earl R. Wilson and Susan C. Kattelus Table of Contents Foreword 1

City of Bingham Cumulative Problem For use with McGraw-Hill/Irwin Accounting for Governmental and Nonprofit Entities, 13 th Edition By Earl R. Wilson and Susan C. Kattelus Table of Contents Foreword 1