The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

|

|

|

- Virgil Lamb

- 5 years ago

- Views:

Transcription

1 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1

2 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record purchases of merchandise on credit in a three-column purchases journal. 2. Post from the three-column purchases journal to the general ledger accounts. 8 2

3 Purchasing Procedures The Sales Department sends an authorized purchase requisition to the Purchasing Department The Purchasing Department issues an authorized purchase order and sends it to the selected supplier A receiving report is prepared when the merchandise is received The Accounting Department receives the invoice and copies of the purchase order and receiving report 8 3

4 This is a purchase invoice for the customer This is a sales invoice for the seller 8 4

5 QUESTION: What is the Purchases account? Wow! I need to order more inventory! ANSWER: The Purchases account is an account used to record cost of goods bought for resale during a period. 8 5

6 Assets Liabilities Account Classifications Recall the major account classifications from earlier chapters: Owner s Equity Revenue Expenses The Purchases account is under a different classification: Cost of Goods Sold 8 6

7 QUESTION: What is the Freight In account? ANSWER: The Freight In account is an account showing transportation charges for items purchased. It is also called Transportation In account. 8 7

8 Cost of Goods Sold Price of goods (debit Purchases) $ Freight charge (debit Freight In) Total invoice (credit Accounts Payable) $ Purchases + Freight In = Accounts Payable Dr. Cr. Dr. Cr. Dr. Cr The cost of goods sold accounts have normal debit balances 8 8

9 These four general journal entries require twelve separate postings to general ledger accounts. It takes a great deal of time and effort to post them 8 9

10 8 10

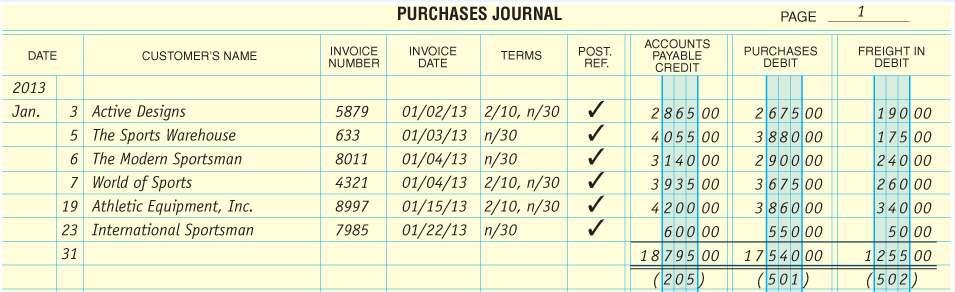

11 Objective 1 Record purchases of merchandise on credit in a three-column purchases journal 1. Enter the date, supplier s name, invoice number, invoice date, and credit terms. 2. In the Accounts Payable Credit column, enter the total owed to the supplier. 8 11

12 3. In the Purchases Debit column, enter the price of the goods purchased. 4. In the Freight In Debit column, enter the freight amount. 8 12

13 Examples of Credit Terms Net 30 days or n/30: Payment in full is due 30 days after the date of the invoice. Net 10 days EOM, or n/10 EOM: Payment in full is due 10 days after the end of the month in which the invoice was issued. 2% 10 days, net 30 days; or 2/10, n/30: If payment is made within 10 days of the invoice date, the customer can take a 2 percent discount. Otherwise, payment in full is due in 30 days. 8 13

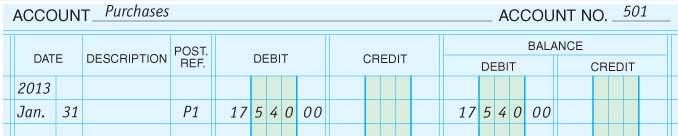

14 Objective 2 Post from the three-column purchases journal to the general ledger accounts The purchases journal simplifies the posting process Summary amounts are posted at the end of the month 8 14

15 Post from the Purchases Journal to the general ledger in seven steps. 1. Locate the Accounts Payable ledger account. 2. Enter the date. 3. Enter the posting reference. 4. Enter the amount from the Accounts Payable Credit column in the purchases journal in the Credit column of the Accounts Payable ledger account. 5. Compute the new balance and enter it into Balance Credit column. 6. In the purchases journal, enter the accounts payable ledger account number under the column total. 7. Repeat the steps for the Purchases Debit and Freight In Debit columns 8 15

16 8 16

17 8 17

18 Advantages of a Purchases Journal Allows for the division of accounting work among different employees Strengthens the audit trail Records all credit purchases in one place 8 18

19 Chapter 8 Accounting for Purchases and Accounts Payable Section 2: Accounts Payable Section Objectives 3. Post credit purchases from the purchases journal to the accounts payable subsidiary ledger. 4. Record purchases returns and allowances in the general journal and post them to the accounts payable subsidiary ledger. 5. Prepare a schedule of accounts payable. 6. Compute the net delivered cost of purchases. 7. Demonstrate a knowledge of the procedures for effective internal control of purchases. 8 19

20 The Accounts Payable Ledger The accounts payable ledger has three money columns. The Balance column is presumed to contain credit amounts. 8 20

21 Objective 3 Post credit purchases from the purchases journal to the accounts payable subsidiary ledger To keep the accounting records up to date, invoices are posted to the accounts payable subsidiary ledger every day. 8 21

22 Steps to post to the accounts payable ledger Enter the date, invoice number and date, and the page number from the purchases journal

23 8 23

24 From the purchases journal, write the dollar amount of the purchase in the credit column of the subsidiary ledger. Recalculate the current balance in the ledger. Enter the check mark in the Post. Ref. column back in the journal to indicate that the transaction is posted in the ledger

25 Cash Payments are posted as debits in the A/P Ledger. The cash payment is then posted to the individual creditor s account in the accounts payable ledger Posted from page 1 of the cash payments journal 8 25

26 Objective 4 Record purchases returns and allowances in the general journal and post them to the accounts payable subsidiary ledger Sorry, I didn t like the color. A purchase return is a return of unsatisfactory Goods previously purchased for resale. 8 26

27 A credit to the Purchase Returns and Allowances account is made when a vendor returns something to a supplier Purchases Returns and Allowances Returns and Allowances A complete record of returns and allowances A contra cost of goods sold account Normal credit balance 8 27

28 Business Transaction On January 30 Maxx-Out Sporting Goods received a credit memorandum for $100 from International Sportsman as an allowance for damaged merchandise. 8 28

29 Purchase Allowance Accounts Payable 100 Purchases Returns and Allowances

30 Posting from the General Journal Enter the amount of the return or allowance in the Debit column of the creditor s account. Update the balance. Enter the date, the credit memorandum number, and the general journal page number. 8 30

31 Objective 5 Prepare a schedule of accounts payable The total of the individual creditor accounts in the subsidiary ledger must equal the balance of the Accounts Payable control account. To prove that the control account and the subsidiary ledger are equal, businesses prepare a schedule of accounts payable. 8 31

32 A comparison of the total of the schedule of accounts payable and the balance of the Accounts Payable account shows that the two figures are the same. 8 32

33 Objective 6 Compute the net delivered cost of purchases The income statement of a merchandising business contains a section showing the total cost of purchases. This section combines information about Cost of the purchases Freight in Purchases returns and allowances 8 33

34 The net delivered cost of purchases for Maxx-Out Sporting Goods for January is calculated as follows. Purchases $ 17,540 Freight In 1,255 Delivered Cost of Purchases $ 18,795 Less Purchases Returns and Allowances 100 Net Delivered Cost of Purchases $18,

35 Objective 7 Demonstrate a knowledge of the procedures for effective internal control of purchases The objectives of the controls are to: create written proof that purchases and payments are authorized, and ensure that different people are involved in the process of buying goods, receiving goods, and making payments. 8 35

36 Effective systems have the following controls in place: 1. All purchases should be made only after proper authorization has been given in writing. 2. Goods should be carefully checked when received. They should then be compared with the purchase order and with the invoice received from the supplier. 3. The purchase order, receiving report, and invoice should be checked to confirm that the information reflected on the documents are in agreement. 8 36

37 4. The computations on the invoice should be checked for accuracy. 5. Authorization for payment should be made by someone other than the person who ordered the goods, and this authorization should be given only after all the verifications have been made. 6. Another person should write the check for payment. 7. Prenumbered forms should be used for purchase requisitions, purchase orders, and checks. Periodically the numbers of the documents issued should be verified to make sure that all forms can be accounted for. 8 37

38 Thank You for using College Accounting, 13th Edition Price Haddock Farina 8 38

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Heintz & Parry. 20 th Edition. College Accounting 10-1

Heintz & Parry 20 th Edition College Accounting 10-1 Chapter 11 Accounting for Purchases and Cash Payments 1 Define merchandise purchases transactions. Merchandise acquired for resale Must be items for

Heintz & Parry 20 th Edition College Accounting 10-1 Chapter 11 Accounting for Purchases and Cash Payments 1 Define merchandise purchases transactions. Merchandise acquired for resale Must be items for

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

ACCOUNTING I Chapter 10 Reading Guide. 1. What are the two major activities of merchandising businesses?

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

MERCHANDISING OPERATIONS

MERCHANDISING OPERATIONS Key Topics to Know Merchandising Businesses The revenue account is Sales, not Fees Earned New expense account, Cost of Goods Sold (COGS), records the cost of merchandise inventory

MERCHANDISING OPERATIONS Key Topics to Know Merchandising Businesses The revenue account is Sales, not Fees Earned New expense account, Cost of Goods Sold (COGS), records the cost of merchandise inventory

Accounting 1. Lesson Plan. Topic: Recording Sales and Cash Receipts Using Special Journals Unit: 4 Chapter 20

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Recording Sales and Cash Receipts Using Special Journals Unit: 4 Chapter 20 I. Objective(s): By the end of today s lesson, the student will

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Recording Sales and Cash Receipts Using Special Journals Unit: 4 Chapter 20 I. Objective(s): By the end of today s lesson, the student will

LESSON 2-1. Departmental Sales on Account and Sales Returns and Allowances. CENTURY 21 ACCOUNTING 2009 South-Western, Cengage Learning

LESSON 2-1 Departmental Sales on Account and Sales Returns and Allowances 2 Departmental Sales on Account Sales on account are recorded by department in order to help management make decisions Sales on

LESSON 2-1 Departmental Sales on Account and Sales Returns and Allowances 2 Departmental Sales on Account Sales on account are recorded by department in order to help management make decisions Sales on

LESSON Journalizing Purchases Using a Purchases Journal

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Journalizing Sales and Cash Receipts Using Special Journals. Friday, February 25, :53:53 AM ET

Journalizing Sales and Cash Receipts Using Special Journals Customer A person or business to whom merchandise or services are sold. Sales Tax A tax on a sale of merchandise or services. Businesses must

Journalizing Sales and Cash Receipts Using Special Journals Customer A person or business to whom merchandise or services are sold. Sales Tax A tax on a sale of merchandise or services. Businesses must

Payroll Taxes, Deposits, and Reports

11-1 McGraw-Hill Payroll Taxes, Deposits, and Reports Section 1: Social Security, Medicare, and Employee Income Tax Section Objectives Chapter 1. Explain how and when payroll taxes are paid to the government.

11-1 McGraw-Hill Payroll Taxes, Deposits, and Reports Section 1: Social Security, Medicare, and Employee Income Tax Section Objectives Chapter 1. Explain how and when payroll taxes are paid to the government.

9 Payments, and Banking Procedures. Cash Receipts, Cash

9-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Cash Receipts, Cash 9 Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts

9-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Cash Receipts, Cash 9 Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts

Recording Departmental Sales and Cash Receipts

Recording Departmental Sales and Cash Receipts Departmental Sales on Account and Sales Returns and Allowances MasterSport records all departmental sales on account in a Sales Journal. The Sales Journal

Recording Departmental Sales and Cash Receipts Departmental Sales on Account and Sales Returns and Allowances MasterSport records all departmental sales on account in a Sales Journal. The Sales Journal

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Posting from a General Journal to a General Ledger. Tuesday, October 26, :48:47 PM ET

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS. Assign Students to Read Ch. 9 and complete the terms p. 234

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS Assign Students to Read Ch. 9 and complete the terms p. 234 (Students may hand-write them on handout or do on word processor) Discuss Section

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS Assign Students to Read Ch. 9 and complete the terms p. 234 (Students may hand-write them on handout or do on word processor) Discuss Section

Accounting Fundamentals: Journals

Directions: Fill in the blanks. 1. Journals Are a form for recording transactions in chronological order journal entries include the transaction amounts, which accounts are affected and how the accounts

Directions: Fill in the blanks. 1. Journals Are a form for recording transactions in chronological order journal entries include the transaction amounts, which accounts are affected and how the accounts

Ch.8 Accounting for a Merchandising Business: Sales and Cash Receipts

Ch.8 Accounting for a Merchandising Business: Sales and Cash Receipts Procedures and forms used in selling merchandise Credit sales Sales Journal Sales returns and allowances Sales discounts Posting procedure

Ch.8 Accounting for a Merchandising Business: Sales and Cash Receipts Procedures and forms used in selling merchandise Credit sales Sales Journal Sales returns and allowances Sales discounts Posting procedure

Analyzing Business Transactions

2-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 2 Analyzing Business Transactions Section 1: Property and Financial Interest Section Objectives 1. Record in equation form

2-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 2 Analyzing Business Transactions Section 1: Property and Financial Interest Section Objectives 1. Record in equation form

Chapter 2: Measurement Concepts: Recording Business Transactions

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

Chapter 2: Measurement Concepts: Recording Business Transactions Student: 1. The valuation issue deals with how the components of a transaction should be categorized. 2. Business transactions are economic

Merchandising Activities

COMPILED BY AL KHADASH Merchandising Activities Chapter 6 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Operating Cycle of a Merchandising Company Cash Accounts

COMPILED BY AL KHADASH Merchandising Activities Chapter 6 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Operating Cycle of a Merchandising Company Cash Accounts

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Accounting I. Lesson Plan. Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Cash Payments Unit: 3 Chapter 11

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

The General Journal and the General Ledger

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

Bookkeepers are the accountant s eyes and ears. Few accountants actually take the time

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Chapter 20 Notes Uncollectible Accounts Expense

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

ACCT 652 Accounting. Review of last week. Review of last week (2) 12/29/15. Week 2 Charts of accounts, Journals, T-accounts, and special journals

12/29/15. Week 2 Charts of accounts, Journals, T-accounts, and special journals") ACCT 652 Accounting Week 2 Charts of accounts, Journals, T-accounts, and special journals Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of

ACCT 652 Accounting Week 2 Charts of accounts, Journals, T-accounts, and special journals Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Chapter 4: The Simple Ledger

Chapter 4: The Simple Ledger 4.1: Ledger Accounts Pages 88 92 account a record that documents each change to items in the accounting equation. There is one account for each asset, each liability, and each

Chapter 4: The Simple Ledger 4.1: Ledger Accounts Pages 88 92 account a record that documents each change to items in the accounting equation. There is one account for each asset, each liability, and each

Work4Me. Algorithmic Version. Aging Accounts Receivable. Problem Eleven. 1 st Web-Based Edition

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Eleven Aging Accounts Receivable Page 1 INTRODUCTION Log on to Algorithmic Work4Me II and from the Problems Menu Bar, select Problem 11, Aging

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Eleven Aging Accounts Receivable Page 1 INTRODUCTION Log on to Algorithmic Work4Me II and from the Problems Menu Bar, select Problem 11, Aging

How to Journalize using Data Entry

Steps Essential to Success 1. Print a copy of the Problem you intend to complete. To do so, go to the software log-in page and click on Download Student Manual button, click on the Problem to open it.

Steps Essential to Success 1. Print a copy of the Problem you intend to complete. To do so, go to the software log-in page and click on Download Student Manual button, click on the Problem to open it.

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Chapter 5. Solution 5.1. Donncha O Donoghue 1

Chapter 5 Solution 5.1 Distinguish between books of original entry and ledger accounts The books of original entry ( day books or journals ) are the books in which transactions are first recorded and are

Chapter 5 Solution 5.1 Distinguish between books of original entry and ledger accounts The books of original entry ( day books or journals ) are the books in which transactions are first recorded and are

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Auditing and Assurance Services, 15e

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

ACCT1115. Review Package - Quiz 2. Fall 2013

ACCT1115 Review Package - Quiz 2 Fall 2013 Page 1 of 16 Part I Multiple Choice 1) A company has a $48,000 loan to be paid off over 24 months. Principal payments are $2,000 per month. The current and non-current

ACCT1115 Review Package - Quiz 2 Fall 2013 Page 1 of 16 Part I Multiple Choice 1) A company has a $48,000 loan to be paid off over 24 months. Principal payments are $2,000 per month. The current and non-current

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting 1. Lesson Plan. Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

COMSATS Institute of Information Technology Abbottabad

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Accounting for Merchandising Businesses

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

Accounting for Business Transactions QUESTIONS

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

Advantage Multiple Currency Support Current Procedures

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate

Statement of Cash Flows

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Accounting Vocabulary

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

IAB LEVEL 2 CERTIFICATE IN MANUAL AND COMPUTERISED BOOKKEEPING (QCF)

") CONTENTS IAB LEVEL 2 CERTIFICATE IN MANUAL AND COMPUTERISED BOOKKEEPING (QCF) Qualification Accreditation Number 601/3789/7 (Accreditation review date 31 st December 2016) QUALIFICATION SPECIFICATION Introduction

CONTENTS IAB LEVEL 2 CERTIFICATE IN MANUAL AND COMPUTERISED BOOKKEEPING (QCF) Qualification Accreditation Number 601/3789/7 (Accreditation review date 31 st December 2016) QUALIFICATION SPECIFICATION Introduction

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

Accounting with MYOB Accounting Plus v18. Chapter Four Accounts Payable

Accounting with MYOB Accounting Plus v18 Chapter Four Accounts Payable Recording a Purchase Important Points A Purchase is obtaining goods for re-sale. Purchases are obtained from Suppliers. Amounts owed

Accounting with MYOB Accounting Plus v18 Chapter Four Accounts Payable Recording a Purchase Important Points A Purchase is obtaining goods for re-sale. Purchases are obtained from Suppliers. Amounts owed

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Journalizing Sales and Cash Receipt Using Special Journals

Chapter 10 Journalizing Sales and Cash Receipt Using Special Journals Objectives 1. Define accounting terms related to sales and cash receipts for a merchandising business. 2. Identify accounting concepts

Chapter 10 Journalizing Sales and Cash Receipt Using Special Journals Objectives 1. Define accounting terms related to sales and cash receipts for a merchandising business. 2. Identify accounting concepts

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 10 1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin Chapter 10 Payroll Computations, Records, and Payment Section 1: Payroll Laws and Taxes Section Objectives 1. Explain

1-1 10 1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin Chapter 10 Payroll Computations, Records, and Payment Section 1: Payroll Laws and Taxes Section Objectives 1. Explain

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Before reading these additional examples, make sure you have read Cathy Sibley s article on Control Accounts, published in June 2012 Velocity.

C02 Financial Accounting Fundamentals Control Accounts Before reading these additional examples, make sure you have read Cathy Sibley s article on Control Accounts, published in June 2012 Velocity. Let

C02 Financial Accounting Fundamentals Control Accounts Before reading these additional examples, make sure you have read Cathy Sibley s article on Control Accounts, published in June 2012 Velocity. Let

1

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed.

ACCT 101 Chapter 6 Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed. Three Objectives of Internal Control Assets are safeguarded

ACCT 101 Chapter 6 Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed. Three Objectives of Internal Control Assets are safeguarded

CA CPT Accpunt Sale of Goods Approval Or Return Basis

CA CPT Accpunt Sale of Goods Approval Or Return Basis Test ID :199 Date : 12-11-2016 Time :00:48:00 Instruction for Qusetion 1 To 40 MCQ Qn.1) A trader has credited certain items of sales on approval aggregating

CA CPT Accpunt Sale of Goods Approval Or Return Basis Test ID :199 Date : 12-11-2016 Time :00:48:00 Instruction for Qusetion 1 To 40 MCQ Qn.1) A trader has credited certain items of sales on approval aggregating

Chapter 02 Analyzing and Recording Transactions

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

Accounting 3 4. Course Outline. Board Approved: October 10, I. Course Information. A. Course Title: Accounting 3-4. B. Course Code Number: BU143

Accounting 3 4 Course Outline Board Approved: October 10, 1995 I. Course Information A. Course Title: Accounting 3-4 B. Course Code Number: BU143 C. Course Length: One Year D. Grade Level: 12 E. Units

Accounting 3 4 Course Outline Board Approved: October 10, 1995 I. Course Information A. Course Title: Accounting 3-4 B. Course Code Number: BU143 C. Course Length: One Year D. Grade Level: 12 E. Units

COMSATS Institute of Information Technology Abbottabad

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Trial Balance. Format of Trial Balance. The under mention points may be noted for preparing a trial balance.

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Work4Me I Accounting Simulations. Demonstration Problem

Work4Me I Accounting Simulations 3 rd Web-Based Edition Demonstration Problem Classic Accounting Services, Incorporated Page 1 Problem 1 Demonstration Problem The Work4Me problems begin with a hands-on,

Work4Me I Accounting Simulations 3 rd Web-Based Edition Demonstration Problem Classic Accounting Services, Incorporated Page 1 Problem 1 Demonstration Problem The Work4Me problems begin with a hands-on,

Work4Me I Accounting Simulations. Problem Seven

Work4Me I Accounting Simulations 3 rd Web-Based Edition Problem Seven Uptight Tools, Inc. Accounting for Accounts Receivable and Merchandise Inventory using a Perpetual Inventory System Page 1 UPTIGHT

Work4Me I Accounting Simulations 3 rd Web-Based Edition Problem Seven Uptight Tools, Inc. Accounting for Accounts Receivable and Merchandise Inventory using a Perpetual Inventory System Page 1 UPTIGHT

Assessment Schedule 2009 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224)

") NCEA Level 2 Accounting (90224) 2009 Page 1 of 8 Assessment Schedule 2009 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Evidence Statement ONE (a)

NCEA Level 2 Accounting (90224) 2009 Page 1 of 8 Assessment Schedule 2009 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Evidence Statement ONE (a)

Full file at Chapter 2: Analyzing Business Transactions

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Chapter 2: Analyzing Business Transactions TRUE/FALSE 1. When a company receives a product previously ordered, a recordable transaction has occurred. T PTS: 1 OBJ: LO1 KEY: business transactions 2. When

Week 5, Chap 4 Part 2

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

FUNDAMENTAL ACCOUNTING (01)

") 13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2009 Multiple Choice (30 @ 2 points each) Account Identification (39 @ 1 point each) Production Portion Problem 1: Journalizing

13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2009 Multiple Choice (30 @ 2 points each) Account Identification (39 @ 1 point each) Production Portion Problem 1: Journalizing

1 General journal entries for purchases returns and sales returns

Introduction The re-accredited VCE Accounting course (2003 2006) has certainly evolved over the last couple of years. Having witnessed two sets of examinations (2003 and 2004), teachers have now been given

Introduction The re-accredited VCE Accounting course (2003 2006) has certainly evolved over the last couple of years. Having witnessed two sets of examinations (2003 and 2004), teachers have now been given

VisionVPM General Ledger Module User Guide

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

- A resource - Controlled by the entity - As a result of a past event - From economic benefits are expected to flow to the entity.

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Multiple choice questions for Accounting for Non-Accountants 10 th edition

Accounting for Non-Accountants 10th Online Material 1 Multiple choice questions for Accounting for Non-Accountants 10 th edition Set 3 20 questions 1 At the start of the year, the balance on Kieran s capital

Accounting for Non-Accountants 10th Online Material 1 Multiple choice questions for Accounting for Non-Accountants 10 th edition Set 3 20 questions 1 At the start of the year, the balance on Kieran s capital

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an):

- Please choose one Wages outstanding given in the trial balance will be treated as a (an):") Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Fundamental Accounting Principles

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 14 th Canadian Edition by Larson/Jensen Prepared by: Tilly Jensen, Athabasca University Wendy Popowich, Northern Alberta Institute of Technology

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles 14 th Canadian Edition by Larson/Jensen Prepared by: Tilly Jensen, Athabasca University Wendy Popowich, Northern Alberta Institute of Technology

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Journalizing Transactions

LESSON Journalizing Transactions CENTURY ACCOUNTING Thomson/South-Western Objectives:. Define accounting terms related to journalizing transactions.. Identify accounting concepts and practices related

LESSON Journalizing Transactions CENTURY ACCOUNTING Thomson/South-Western Objectives:. Define accounting terms related to journalizing transactions.. Identify accounting concepts and practices related

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

ECON 3A---FALL 2007 MIDTERM #2 ANSWER QUESTIONS #1-25 ON GREEN SCANTRON AND THE REST IN THE SPACE PROVIDED-PLEASE.

ECON 3A---FALL 2007 MIDTERM #2 Name: PERM #: ANSWER QUESTIONS #1-25 ON GREEN SCANTRON AND THE REST IN THE SPACE PROVIDED-PLEASE. 1. Gross profit equals the difference between A) net sales revenues and

ECON 3A---FALL 2007 MIDTERM #2 Name: PERM #: ANSWER QUESTIONS #1-25 ON GREEN SCANTRON AND THE REST IN THE SPACE PROVIDED-PLEASE. 1. Gross profit equals the difference between A) net sales revenues and

Activity 1: Transactions

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

Accounting COURSE SYLLABUS Course Description: Course Objectives:

Accounting COURSE SYLLABUS Course Description: The objective of this class is to introduce Accounting and the Accounting equation. The students will be able to Analyze Business source documents, Journalize

Accounting COURSE SYLLABUS Course Description: The objective of this class is to introduce Accounting and the Accounting equation. The students will be able to Analyze Business source documents, Journalize

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

XI ACCOUNTING PRIVATE. Sameer Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit 2014 XI ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit 2014 XI ACCOUNTING

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Chapter 2 Analyzing Business Transactions

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

Debits and Credits. (Explanation)

") s and s (Explanation) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Introduction to s and s If the

s and s (Explanation) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Introduction to s and s If the

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Sales Returns (Returns Inwards) Day A book of original entry used by the book-keeper to enter all returns back into the firm by debtors (trader receiv

Day A book of original entry used by the book-keeper to enter all returns back into the firm by debtors (trader receiv") Return Inwards (Sales Returns) Day All Business Transactions Credit Sales Credit Purchases Sales Returns In Purchases Returns Out Cash/Bank Receipts/ Payments Small Cash Receipts/ payments Other Transactions

Return Inwards (Sales Returns) Day All Business Transactions Credit Sales Credit Purchases Sales Returns In Purchases Returns Out Cash/Bank Receipts/ Payments Small Cash Receipts/ payments Other Transactions

Basic Book-keeping Skills for Learners

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum Learning Resources Corner Course 1: Contemporary Perspectives on Accounting

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum Learning Resources Corner Course 1: Contemporary Perspectives on Accounting