Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed.

|

|

|

- Mabel Hood

- 5 years ago

- Views:

Transcription

1 ACCT 101 Chapter 6 Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed. Three Objectives of Internal Control Assets are safeguarded and used only for business purposes Business information is accurate Employees comply with laws and regulations Employee fraud is the intentional act of deceiving an employer for personal gain. It is very difficult to detect collusion between 2 or more employees Internal Controls protect the company and the employee by limiting temptation and taking away suspicion Sarbanes Oxley Act of 2002 Law that requires publicly traded companies to maintain adequate systems of internal control. Outside, independent auditors must attest to the adequacy of the internal control system Failure results in fines or imprisonment Five Elements of Internal Control 1. The Control Environment management philosophy and operating style (if management does not seem to care, employees will get the idea that it is okay to misuse company assets; if management sends the message that it is not okay, employees less likely to misuse company assets) 2. Risk Assessment all business have risk, the more risk a business has, the more stringent the internal controls should be. 3. Control Procedures What procedures can we follow to help accomplish the objectives of internal control? Competent Personnel make sure we screen applicants to make sure they understand how to do their job. Rotating Duties don t leave the same person in charge of the same tasks all the time. Rotate employees through the different job responsibilities within their department. Mandatory Vacations make employees take their vacation time. When someone else performs their job while they are on vacation, any discrepancies will be found. 1

2 Separation of Duties separate the tasks required to complete the job so the employees are checking each others work and one person does not have complete control. Custody of Assets separate from Accounting Operations have different people responsible for the warehouse than those that are responsible for tracking inventory in the computer. Proofs and Security Measures have checks and balances to verify the completeness and accuracy of employee s work, such as having a supervisor review work once completed 4. Monitoring- warning signals/clues indicating dishonesty or fraud 5. Information and Communication- gather information to assess and monitor internal controls Preventative vs. Detective Controls Preventative seek to prevent the fraud from occurring in the first place. Such as: separation of duties, cameras, mandatory vacations Detective to detect theft or misuse of assets if it should get past the preventative controls Such as: supervisor review, bank reconciliations Limitations of Internal Controls Designed to provide reasonable assurance of proper safeguarding of assets and reliability of the accounting records Human Error Human Fraud Effectiveness reduced by collusions Cost for establishing should not exceed the benefits Size of business limits ability to establish Cash the asset most susceptible to fraudulent activities readily convertible to other assets easily concealed and transported highly desired Cash Equivalents = Short-term, highly liquid investment asses that are readily convertible to known cash amount and sufficiently close to their due date so that their market value is not sensitive to interest rate changes. 2

3 Use of a Bank Bank reconciliation - The process of comparing the bank's account balance with the company's balance, and explaining the differences to make them agree. Differences are usually due to info that one party has that the other doesn t. Bank statement - A statement received monthly from the bank that shows the depositor's bank transactions and balances. Includes: Beginning of period balance Checks paid and other debits decreasing the account Deposits and other credits increasing the account End of period balance Bank statements are prepared from the bank's perspective therefore every deposit the bank receives is an increase in the bank's liabilities (a credit) NSF check - A check that is not paid by a bank because of insufficient funds in a bank account. - creates an accounts receivable for the depositor and reduces cash in the bank account Reconciling the bank account Bank balance and book balance seldom agree because 1. Time lags 2. Errors Steps to reveal all the reconciling items that cause the difference between the balances PUT IT WHERE IT ISN T 1. Deposits in transit - Deposits recorded by the depositor that have not been recorded by the bank. - to balance per bank 2. Outstanding checks - Checks issued and recorded by a company that have not been paid by the bank. - from balance per bank 3. Errors -All errors made by the depositor are reconciling items on cash per books -All errors made by bank are reconciling items on cash per bank 4. Bank memoranda -Bank service charges 5. Note and interest collections -Collected by bank on behalf of company Bal. Per Bank : : Adjusted Bal. Per Bank Date like Balance Sheet Bal. Per General Ledger : : Adjusted Bal. Per General Ledger 3

4 Balance per Bank XXXX Balance per Books XXXX : Deposits in Transit : Notes collected by bank (wire transfers) : Outstanding Checks : service charges NSF checks Adjusted Balance XXXX Adjusted Balance XXXX These two balances must agree Errors could go in any of the four reconciling areas depending on who made the error (the company or the bank) and whether we get more money in our account or have to pay more money. A. Adjustments needed for the additions (DR to Cash) and deductions (CR to Cash) on the Balance per Books side of the bank reconciliation. All reconciling items on the Balance per Bank side will take care of themselves. If the bank made an error the company should call them and inform them to correct it. B. After adjustments, cash balance per books should equal the adjusted balance per the bank reconciliation. Place an x in the appropriate column to indicate whether the item should be added to or deducted from the book or bank balance, or whether it should not appear on the reconciliation. If the book balance is to be adjusted, place a Dr. or Cr. in the Adjust column to indicate whether the Cash balance should be debited or credited. 1. NSF check from customer is returned on September 25 but not yet recorded by this company. 2. Interest earned on the September cash balance in the bank. 3. Deposit made on September 5 and processed by the bank on September Checks written by another depositor but charged against this company s account. 5. Bank service charge for September. 6. Checks outstanding on August 31 that cleared the bank in September. 7. Check written against the company s account and cleared by the bank; erroneously not recorded by the company s recordkeeper. 8. Principal and interest on a note receivable to this company is collected by the bank but not yet recorded by the company. 9. Checks written and mailed to payees on October Checks written by the company and mailed to payees on September Night deposit made on September 30 after the bank closed. 12. Special bank charge for collection of note in part 8 on this company s behalf. 4

5 Bank Balance Book Balance Not Shown on Adjust Reconciliation 1) 2) 3) 4) 5) 6) 7) 8) 9) 10) 11) 12) Del Gato Clinic deposits all cash receipts on the day when they are received and it makes all cash payments by check. At the close of business on June 30, 2017, its Cash account shows an $11,589 debit balance. Del Gato Clinic s June 30 bank statement shows $10,555 on deposit in the bank. Prepare a bank reconciliation and the adjusting entries for Del Gato Clinic using the following information: a. Outstanding checks as of June 30 total $1,829. b. The June 30 bank statement lists a $16 bank service charge. c. Check No. 919, listed with the canceled checks, was correctly drawn for $467 in payment of a utility bill on June 15. Del Gato Clinic mistakenly recorded it with a debit to Utilities Expense and a credit to Cash in the amount of $476. d. The June 30 cash receipts of $2,856 were placed in the bank s night depository after banking hours and were not recorded on the June 30 bank statement. Bank statement balance... Book balance 5

6 Adjusted bank balance... Adjusted book balance... GENERAL JOURNAL Page Date Description Post ref Debit Credit Wright Company deposits all cash receipts on the day when they are received and it makes all cash payments by check. At the close of business on May 31, 2017, its Cash account shows a $27,500 debit balance. The company s May 31 bank statement shows $25,800 on deposit in the bank. Prepare a bank reconciliation for the company using the following information. a. The May 31 bank statement lists $100 in bank service charges; the company has not yet recorded the cost of these services. b. Outstanding checks as of May 31 total $5,600. c. May 31 cash receipts of $6,200 were placed in the bank s night depository after banking hours and were not recorded on the May 31 bank statement. d. In reviewing the bank statement, a $400 check written by Smith Company was mistakenly drawn against Wright s account. e. The bank statement shows a $600 NSF check from a customer; the company has not yet recorded this NSF check. Bank statement balance... Book balance 6

7 Adjusted bank balance... Adjusted book balance... The following information is available to reconcile Severino Co. s book balance of cash with its bank statement cash balance as of December 31, a. The December 31 cash balance according to the accounting records is $32,878.30, and the bank statement cash balance for that date is $46, b. Check No for $4, and Check No for $400, both written and entered in the accounting records in December, are not among the canceled checks. Two checks, No for $2,289 and No for $410.40, were outstanding on the most recent November 30 reconciliation. Check No is listed with the December canceled checks, but Check No is not. c. When the December checks are compared with entries in the accounting records, it is found that Check No had been correctly drawn for $3,456 to pay for office supplies but was erroneously entered in the accounting records as $3,465. d. Two memoranda are enclosed with the statement and are unrecorded at the time of the reconciliation. The first is for a $ charge that dealt with an NSF check for $745 received from a customer, Titus Industries, in payment of its account. The bank assessed a $17.50 fee for processing it. The second is $99 in miscellaneous expenses for check printing. e. The bank statement shows that the bank collected $19,000 cash on a note receivable for the company, deducted a $20 collection expense, and credited the balance to the company s Cash account. Severino did not record this transaction before receiving the statement. f. Severino s December 31 daily cash receipts of $9, were placed in the bank s night depository on that date but do not appear on the December 31 bank statement. Required 1. Prepare the bank reconciliation for this company as of December 31, Prepare the journal entries (in dollars and cents) necessary to bring the company s book balance of cash into conformity with the reconciled cash balance as of December 31, Explain the nature of the communications conveyed by a bank when the bank sends the depositor (a) a debit memorandum and (b) a credit memorandum. Bank statement balance... Book balance 7

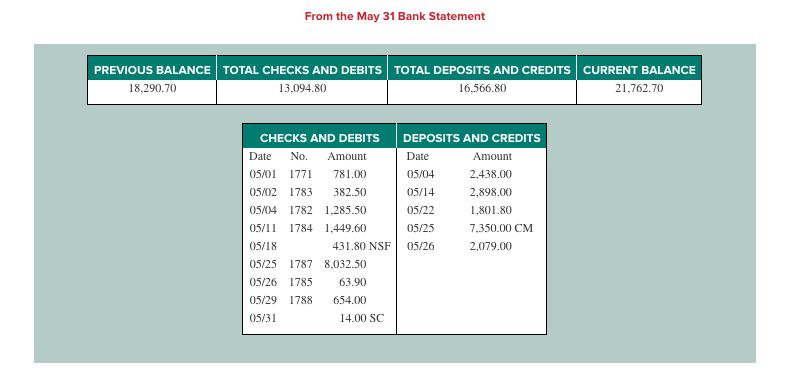

8 Adjusted bank balance... Adjusted book balance... GENERAL JOURNAL Page Date Description Post ref Debit Credit Shamara Systems most recently reconciled its bank balance on April 30 and reported two checks outstanding at that time, No for $781 and No for $1, The following information is available for its May 31, 2017, reconciliation. Check No is correctly drawn for $654 to pay for May utilities; however, the recordkeeper misread the amount and entered it in the accounting records with a debit to Utilities Expense and a credit to Cash for $644. The bank paid and deducted the correct amount. The NSF check shown in the statement originally received from a customer, W. Sox, in payment of her account. The company has not yet recorded its return. The credit memorandum (CM) is from a $7,400 note that the bank collected for the company. The bank deducted a $50 collection expense and deposited the remainder in the company s account. The collection and expense have not yet been recorded. Required 1. Prepare the May 31, 2017, bank reconciliation for Shamara Systems. 2. Prepare the journal entries (in dollars and cents) to adjust the book balance of cash to the reconciled balance. 3. The bank statement reveals that some of the prenumbered checks in the sequence are missing. Describe three possible situations to explain this. 8

9 9

10 Bank statement balance... Book balance Adjusted bank balance... Adjusted book balance... GENERAL JOURNAL Date Description Post ref Debit Page Credit Petty Cash small amount of cash kept on hand for incidental purchases. A. The only time the petty cash account is affected is when the fund is established or the amount of the fund is increased or decreased. Check is cashed and proceeds given to petty cashier. Entry to establish Petty Cash Fund DR Petty Cash XXX CR Cash XXX 10

11 B. Patty cash payments report and all receipts are given to the company cashier in exchange for a check to reimburse the fund. The petty cashier cashes the check and puts the cash in the petty cashbox. Entry to replenish petty cash. DR Expenses XXX CR Cash XXX Waupaca Company establishes a $350 petty cash fund on September 9. On September 30, the fund shows $104 in cash along with receipts for the following expenditures: transportation-in, $40; postage expenses, $123; and miscellaneous expenses, $80. The petty cashier could not account for a $3 shortage in the fund. The company uses the perpetual system in accounting for merchandise inventory. Prepare (1) the September 9 entry to establish the fund, (2) the September 30 entry to reimburse the fund, and (3) an October 1 entry to increase the fund to $400. GENERAL JOURNAL Page Date Description Post ref Debit Credit Cash Over and Short Ups and downs are expected. Should monitor for employees who are consistently Short and never Over. If it is too large, you may have a problem. Typically a debit balance since customers will dispute being short changed rather than over Combined with miscellaneous expense Book it: DR: Cash 395 DR: Cash Over and Short 5 CR: Sales

Chapter 06 - Cash and Internal Controls. Chapter Outline

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

2013 年 会计学原理 期中考试 1 / 6

2013 年 会计学原理 期中考试 Part I True or False (0.5 mark each, 21 marks in total) 1. The primary objective of financial accounting is to provide general purpose financial statements to help external users analyze

2013 年 会计学原理 期中考试 Part I True or False (0.5 mark each, 21 marks in total) 1. The primary objective of financial accounting is to provide general purpose financial statements to help external users analyze

Fundamental Accounting Principles, Volume 1, Fifteenth Canadian Edition

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Chapter 6. Accounting For Cash and Internal Controls

Chapter 6 Accounting For Cash and Internal Controls C 2 Cash, Cash Equivalents, and Liquidity Cash Currency, coins and amounts on deposit in bank accounts, checking accounts, and many savings accounts.

Chapter 6 Accounting For Cash and Internal Controls C 2 Cash, Cash Equivalents, and Liquidity Cash Currency, coins and amounts on deposit in bank accounts, checking accounts, and many savings accounts.

Chapter 7 Student Version

Sarbanes-Oxley, Internal Control, and Cash Chapter 7 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor

Sarbanes-Oxley, Internal Control, and Cash Chapter 7 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor

Fraud, Internal Control, and Cash

7-1 Chapter 7 Fraud, Internal Control, and Cash Learning Objectives After studying this chapter, you should be able to: 1. Define fraud and internal control. 2. Identify the principles of internal control

7-1 Chapter 7 Fraud, Internal Control, and Cash Learning Objectives After studying this chapter, you should be able to: 1. Define fraud and internal control. 2. Identify the principles of internal control

CHAPTER 8 INTERNAL CONTROL AND CASH SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY

CHAPTER 8 INTERNAL CONTROL AND CASH SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 C 17. 3 C 25.

CHAPTER 8 INTERNAL CONTROL AND CASH SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 C 17. 3 C 25.

Chapter 7 Question Review 1

Chapter 7 Question Review 1 Chapter 7 Questions Multiple Choice 1. The entry to replenish a petty cash fund includes a credit to a. Petty Cash. b. Cash. c. Freight-In. d. Postage Expense. 2. A $300 petty

Chapter 7 Question Review 1 Chapter 7 Questions Multiple Choice 1. The entry to replenish a petty cash fund includes a credit to a. Petty Cash. b. Cash. c. Freight-In. d. Postage Expense. 2. A $300 petty

Ch.6 Internal Control and Accounting for Cash

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Cash and Internal Control C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Auditing and Assurance Services, 15e

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Fill-in-the-Blank Equations. Exercises

Chapter 8 Sarbanes-Oxley, Internal Control, and Cash Study Guide Solutions 1. Liability 2. Increase; debit 3. Monthly cash expenses 4. Cash as of year-end Fill-in-the-Blank Equations Exercises 1. In Poletti

Chapter 8 Sarbanes-Oxley, Internal Control, and Cash Study Guide Solutions 1. Liability 2. Increase; debit 3. Monthly cash expenses 4. Cash as of year-end Fill-in-the-Blank Equations Exercises 1. In Poletti

BANKING PROCEDURE AND CONTROL OF CASH

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

Sarbanes-Oxley, Internal Control, and Cash

C H A P T E R 7 Sarbanes-Oxley, Internal Control, and Cash Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Sarbanes-Oxley Act (slide 1 of 2) Sarbanes-Oxley emphasizes

C H A P T E R 7 Sarbanes-Oxley, Internal Control, and Cash Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Sarbanes-Oxley Act (slide 1 of 2) Sarbanes-Oxley emphasizes

Exercises: Set B. 28 B-Exercises

28 B-Exercises Identify the principles of internal control. (LO 2), C weaknesses over cash receipts and suggest (LO 2, 3) weaknesses for cash disbursements and suggest (LO 2, 4) (LO 5) Exercises: Set B

28 B-Exercises Identify the principles of internal control. (LO 2), C weaknesses over cash receipts and suggest (LO 2, 3) weaknesses for cash disbursements and suggest (LO 2, 4) (LO 5) Exercises: Set B

Sarbanes-Oxley Act of 2002

Sarbanes-Oxley Act of 2002 The Sarbanes-Oxley Act of 2002 (often referred to simply as Sarbanes-Oxley) applies only to companies whose stock is traded on public exchanges. Its purpose is to restore public

Sarbanes-Oxley Act of 2002 The Sarbanes-Oxley Act of 2002 (often referred to simply as Sarbanes-Oxley) applies only to companies whose stock is traded on public exchanges. Its purpose is to restore public

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

FINANCE COMMITTEE PROCEDURES. Committee Responsibilities. Audit Process

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

SPECIFIC PRACTICES Cash Management Page 1

SPEIFI PRATIES 4510 ash Management Page 1 SUBJET: Petty ash and hange Fund Accounts PURPOSE: To describe a procedure for the creation and management of a petty cash or change fund account. DISUSSION: This

SPEIFI PRATIES 4510 ash Management Page 1 SUBJET: Petty ash and hange Fund Accounts PURPOSE: To describe a procedure for the creation and management of a petty cash or change fund account. DISUSSION: This

Chapter 3 Cash And Cash Equivalent

Chapter 3 Cash And Cash Equivalent Cash Learning Objectives 1. Establish and account for a Change Fund. 2. Establish and account for a Petty Cash Fund. 3. Describe the use of commercial banking services

Chapter 3 Cash And Cash Equivalent Cash Learning Objectives 1. Establish and account for a Change Fund. 2. Establish and account for a Petty Cash Fund. 3. Describe the use of commercial banking services

Accounting Building Business Skills. Learning Objectives. Learning Objectives. Paul D. Kimmel. Chapter Seven: Internal Control, Cash and Receivables

Accounting Building Business Skills Paul D. Kimmel Chapter Seven: Internal Control, Cash and Receivables PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003

Accounting Building Business Skills Paul D. Kimmel Chapter Seven: Internal Control, Cash and Receivables PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES

GUIDELINES AND PROCEDURES") FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

SOLUTIONS TO BRIEF EXERCISES

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 8-1 1. Financial Pressure 2. Rationalization 3. Financial Pressure 4. Opportunity BRIEF EXERCISE 8-2 1. True. 2. True. 3. False. The Sarbanes-Oxley Act requires

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 8-1 1. Financial Pressure 2. Rationalization 3. Financial Pressure 4. Opportunity BRIEF EXERCISE 8-2 1. True. 2. True. 3. False. The Sarbanes-Oxley Act requires

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 8 1 Chapter Accounting for Purchases and Accounts Payable 8 Section 1: Merchandise Purchases Section Objectives 1. Record

College Accounting. Heintz & Parry. 20 th Edition

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check.

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

ASSIGNMENT CLASSIFICATION TABLE

CHAPTER 8 Internal Control and Cash ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Describe internal control. 1 1 2. Explain the principles

CHAPTER 8 Internal Control and Cash ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Describe internal control. 1 1 2. Explain the principles

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Assets Define Assets? Assets Financial Reporting Standard (FRS) defines assets as resources controlled by an entity

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Assets Define Assets? Assets Financial Reporting Standard (FRS) defines assets as resources controlled by an entity

COUNTY OF HENRICO, VIRGINIA PETTY CASH FUND POLICIES AND PROCEDURES

COUNTY OF HENRICO, VIRGINIA PETTY CASH FUND POLICIES AND PROCEDURES Approved by the County Manager And Effective August 1, 2007 (Updated July 1, 2017) PETTY CASH FUNDS Purpose: The availability of petty

COUNTY OF HENRICO, VIRGINIA PETTY CASH FUND POLICIES AND PROCEDURES Approved by the County Manager And Effective August 1, 2007 (Updated July 1, 2017) PETTY CASH FUNDS Purpose: The availability of petty

LOSS PREVENTION AND INTERNAL CONTROLS SUPPLEMENTAL APPLICATION FOR FINANCIAL INSTITUTIONS

Name of Insurance Company to which application is made LOSS PREVENTION AND INTERNAL CONTROLS SUPPLEMENTAL APPLICATION FOR FINANCIAL INSTITUTIONS NAME OF INSURED: ADDRESS: A. GENERAL INFORMATION 1. During

Name of Insurance Company to which application is made LOSS PREVENTION AND INTERNAL CONTROLS SUPPLEMENTAL APPLICATION FOR FINANCIAL INSTITUTIONS NAME OF INSURED: ADDRESS: A. GENERAL INFORMATION 1. During

Chapter II: Internal Controls II-10

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Citywide Cash Handling Procedures Performance Audit

Citywide Cash Handling Procedures Performance Audit March 2010 Office of the Auditor Audit Services Division City and County of Denver Dennis J. Gallagher Auditor The Auditor of the City and County of

Citywide Cash Handling Procedures Performance Audit March 2010 Office of the Auditor Audit Services Division City and County of Denver Dennis J. Gallagher Auditor The Auditor of the City and County of

TITLE: FISCAL MANAGEMENT

TITLE: FISCAL MANAGEMENT PURPOSE AND SCOPE: This policy outlines the procedures Kokua uses to ensure sound financial management. POLICY 4.0 Rev. September 2017 A. RESPONSIBILITY FOR FINANCIAL OVERSIGHT

TITLE: FISCAL MANAGEMENT PURPOSE AND SCOPE: This policy outlines the procedures Kokua uses to ensure sound financial management. POLICY 4.0 Rev. September 2017 A. RESPONSIBILITY FOR FINANCIAL OVERSIGHT

Cash and Financial Investments

CHAPTER 10 Cash and Financial Investments Review Questions 10 1 The following circumstances might cause a client to understate assets: (1) Management of a privately held company may be motivated to understate

CHAPTER 10 Cash and Financial Investments Review Questions 10 1 The following circumstances might cause a client to understate assets: (1) Management of a privately held company may be motivated to understate

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

Do not turn this page until the start signal is given!

UNIVERSITY INTERSCHOLASTIC LEAGUE ACCOUNTING EXAM Invitational 2015-A Contestant # Team # Do not turn this page until the start signal is given! All answers MUST be written on your answer sheet. Either

UNIVERSITY INTERSCHOLASTIC LEAGUE ACCOUNTING EXAM Invitational 2015-A Contestant # Team # Do not turn this page until the start signal is given! All answers MUST be written on your answer sheet. Either

Solutions. I. Auditing Cash and Cash Equivalents. A. Learning Question Answers

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

CITY OF RICHARDSON INTERDEPARTMENTAL POLICY AND PROCEDURES

Revised May 1, 2018 CITY OF RICHARDSON INTERDEPARTMENTAL POLICY AND PROCEDURES PETTY CASH/CHANGE FUNDS POLICY Petty cash funds are established to reimburse City employees for small cash expenditures. Petty

Revised May 1, 2018 CITY OF RICHARDSON INTERDEPARTMENTAL POLICY AND PROCEDURES PETTY CASH/CHANGE FUNDS POLICY Petty cash funds are established to reimburse City employees for small cash expenditures. Petty

CASH ACCOUNTING MANUAL

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

The University of Montana Treasury Area (Treasury) maintains a cashiering function for the purpose of receiving monies due The University.

maintains a cashiering function for the purpose of receiving monies due The University.") Business Services The University of Montana Missoula, Montana 59812-1254 Procedure: 120001 Revision Date: 5/4/16 Revision Number: 7 PROCEDURE: Department Cashier Procedures OVERVIEW... 1 STATUTES AND GUIDELINES...

Business Services The University of Montana Missoula, Montana 59812-1254 Procedure: 120001 Revision Date: 5/4/16 Revision Number: 7 PROCEDURE: Department Cashier Procedures OVERVIEW... 1 STATUTES AND GUIDELINES...

PART 3 Financial Planning, Control and Decision Making

PART 3 Financial Planning, Control and Decision Making Cash management and control 10 Cost volume profit analysis for decision making Budgeting for planning and control Performance evaluation for managers

PART 3 Financial Planning, Control and Decision Making Cash management and control 10 Cost volume profit analysis for decision making Budgeting for planning and control Performance evaluation for managers

Chapter 7 Cash and Receivables

Chapter 7 Cash and Receivables Questions for Review of Key Topics Question 7 1 Cash equivalents usually include negotiable instruments as well as highly liquid investments that have a maturity date no

Chapter 7 Cash and Receivables Questions for Review of Key Topics Question 7 1 Cash equivalents usually include negotiable instruments as well as highly liquid investments that have a maturity date no

INTERNAL CONTROL AND LOSS PREVENTION SUPPLEMENTAL APPLICATION FOR INVESTMENT FIRMS

Name of Insurance Company to which application is made INTERNAL CONTROL AND LOSS PREVENTION SUPPLEMENTAL APPLICATION FOR INVESTMENT FIRMS A. AUDITS NAME OF INSTITUTION: PRINCIPAL ADDRESS: DATE: 1. Are

Name of Insurance Company to which application is made INTERNAL CONTROL AND LOSS PREVENTION SUPPLEMENTAL APPLICATION FOR INVESTMENT FIRMS A. AUDITS NAME OF INSTITUTION: PRINCIPAL ADDRESS: DATE: 1. Are

1. Cash includes coin, currency, checks, money orders, and credit card transactions.

1.0 Purpose BEREA COLLEGE Cash Handling Policy Document Document No. No. FIN032 FIN006 Revision Effective Date Date 3/2018 7/2008 Review Revision Date Date 3/2018 Next Pages Review Date 3/2019 1-3 Pages

1.0 Purpose BEREA COLLEGE Cash Handling Policy Document Document No. No. FIN032 FIN006 Revision Effective Date Date 3/2018 7/2008 Review Revision Date Date 3/2018 Next Pages Review Date 3/2019 1-3 Pages

Guidelines for Church Financial Review

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

3/11/2016. Student Activity Funds. Basic Facts about Student Activity Funds

Student Activity Funds Presented by: Natalie Rew, CPA Basic Facts about Student Activity Funds WI Stats, s. 120.16(2) authorizes a school district treasurer to receive money raised in extra-curricular

Student Activity Funds Presented by: Natalie Rew, CPA Basic Facts about Student Activity Funds WI Stats, s. 120.16(2) authorizes a school district treasurer to receive money raised in extra-curricular

BULLETIN NO.: BUS-49 DATE: 2/01/02 PAGE: 1 of 15 POLICY FOR HANDLING CASH AND CASH EQUIVALENTS. Vice President--Financial Management Anne C.

PAGE: 1 of 15 POLICY FOR HANDLING CASH AND CASH EQUIVALENTS Vice President--Financial Management Anne C. Broome Content Page I. References 2 A. Business and Finance Bulletins 2 B. Accounting Manual 2 II.

PAGE: 1 of 15 POLICY FOR HANDLING CASH AND CASH EQUIVALENTS Vice President--Financial Management Anne C. Broome Content Page I. References 2 A. Business and Finance Bulletins 2 B. Accounting Manual 2 II.

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY ORIGINALLY ADOPTED BY CITY COUNCIL: NOVEMBER 17, 2011 PREFACE The intent of the City of Kennedale s Internal Controls & Cash Handling Policy is

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY ORIGINALLY ADOPTED BY CITY COUNCIL: NOVEMBER 17, 2011 PREFACE The intent of the City of Kennedale s Internal Controls & Cash Handling Policy is

CHAPTER 7. Internal Control and Cash. Chapter Overview

CHAPTER 7 Internal Control and Cash Chapter Overview Chapter 7 discusses the purposes and characteristics of an effective system of internal control. The text describes four objectives that a company hopes

CHAPTER 7 Internal Control and Cash Chapter Overview Chapter 7 discusses the purposes and characteristics of an effective system of internal control. The text describes four objectives that a company hopes

Chapter 23 Audit of Cash and Financial Instruments. Copyright 2014 Pearson Education

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 5: Cash Control Systems

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

Department of State Treasurer. Policy Manual for Local Governments. Section 80: Internal Controls

Department of State Treasurer Policy Manual for Local Governments s Revision Issued: March 2017 Table of Contents Executive Summary... 1 Part I Objectives and Components of Internal Control... 3 A. Introduction...

Department of State Treasurer Policy Manual for Local Governments s Revision Issued: March 2017 Table of Contents Executive Summary... 1 Part I Objectives and Components of Internal Control... 3 A. Introduction...

CONT 3106 PROBLEMS AND EXERCISES OF CHAPTERS 11, 12 & 4 SECOND SEMESTER

CONT 3106 PROBLEMS AND EXERCISES OF CHAPTERS 11, 12 & 4 SECOND SEMESTER 2012-2013 CHAPTER 11 P11-1C Listed below are several transactions. For each transaction, indicate by letter whether the cash effect

CONT 3106 PROBLEMS AND EXERCISES OF CHAPTERS 11, 12 & 4 SECOND SEMESTER 2012-2013 CHAPTER 11 P11-1C Listed below are several transactions. For each transaction, indicate by letter whether the cash effect

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Sarbanes-Oxley was passed in response to which of the following? 1) A) The mounting government

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Sarbanes-Oxley was passed in response to which of the following? 1) A) The mounting government

Chapter 10. Cash and Financial Investments. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

a) Post-closing trial balance c) Income statement d) Statement of retained earnings

Post-closing trial balance c) Income statement d) Statement of retained earnings") Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTS PAYABLE POLICIES AND PROCEDURES...

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

ACCT 652 Accounting. Review of last week. Review of last week (2) 12/29/15. Week 2 Charts of accounts, Journals, T-accounts, and special journals

12/29/15. Week 2 Charts of accounts, Journals, T-accounts, and special journals") ACCT 652 Accounting Week 2 Charts of accounts, Journals, T-accounts, and special journals Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of

ACCT 652 Accounting Week 2 Charts of accounts, Journals, T-accounts, and special journals Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of

Movable and Sensitive Minor Equipment

Movable and Sensitive Minor Equipment This section applies to departmental equipment that meets the following criteria: Equipment items of a movable nature that cost $5,000 or more. Equipment items that

Movable and Sensitive Minor Equipment This section applies to departmental equipment that meets the following criteria: Equipment items of a movable nature that cost $5,000 or more. Equipment items that

SALT LAKE COUNTY AUDITOR S OFFICE

SALT LAKE COUNTY AUDITOR S OFFICE SEAN THOMAS Auditor Richard L. Chamberlain, Director Contracts and Procurement Division 2001 South State Street, Suite N4500 Salt Lake City, Utah 84190 RE: Surplus Property

SALT LAKE COUNTY AUDITOR S OFFICE SEAN THOMAS Auditor Richard L. Chamberlain, Director Contracts and Procurement Division 2001 South State Street, Suite N4500 Salt Lake City, Utah 84190 RE: Surplus Property

PTO/Booster Club Financial Guidelines

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

Bank Reconciliations

Professor Authored Problems Intermediate Accounting I Acct 541 Bank Reconciliations Problem 93 Simple Bank Reconciliation The Smith Company needs help in constructing a bank reconciliation for July 31:

Professor Authored Problems Intermediate Accounting I Acct 541 Bank Reconciliations Problem 93 Simple Bank Reconciliation The Smith Company needs help in constructing a bank reconciliation for July 31:

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL Title: Cash Handling Policy Number: 05.20.12 Issuing Authority: Office of Financial Affairs Responsible Officer: Chief Financial Officer and Treasurer Date

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL Title: Cash Handling Policy Number: 05.20.12 Issuing Authority: Office of Financial Affairs Responsible Officer: Chief Financial Officer and Treasurer Date

ProCard Policies & Procedures Training Guide

ProCard Policies & Procedures Training Guide Prepared by: Department of Procurement Sampey 4106 897-4722 1 ProCard Benefits An accelerated process for routine or small purchases Eliminates the Under $250

ProCard Policies & Procedures Training Guide Prepared by: Department of Procurement Sampey 4106 897-4722 1 ProCard Benefits An accelerated process for routine or small purchases Eliminates the Under $250

NATIONAL SENIOR CERTIFICATE GRADE 12

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING PREPARATORY EXAMINATION 2008 MEMORANDUM MARKS: 300 TIME: 3 hours This memorandum consists of 17 pages. Accounting 2 DoE/Preparatory Examination 2008 QUESTION

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING PREPARATORY EXAMINATION 2008 MEMORANDUM MARKS: 300 TIME: 3 hours This memorandum consists of 17 pages. Accounting 2 DoE/Preparatory Examination 2008 QUESTION

Diocese of Oregon. The Episcopal Church in Western Oregon. Audit Program for Parishes and Missions February 26th, 2011

Diocese of Oregon The Episcopal Church in Western Oregon Audit Program for Parishes and Missions February 26th, 2011 HOW TO USE THIS MANUAL This booklet has been prepared for use as a manual. Please do

Diocese of Oregon The Episcopal Church in Western Oregon Audit Program for Parishes and Missions February 26th, 2011 HOW TO USE THIS MANUAL This booklet has been prepared for use as a manual. Please do

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1 1. Procedure Title: Receipt and Deposit of Cash and Checks 2. Procedure Purpose and Effect: To outline procedures for proper safeguarding

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1 1. Procedure Title: Receipt and Deposit of Cash and Checks 2. Procedure Purpose and Effect: To outline procedures for proper safeguarding

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Cash Handling Policy & Procedures

Cash Handling Policy & Procedures Purpose SB 2015-2016:14 The cash handling policy and procedures outlined in this document are intended to provide guidance and appropriate segregation of duties on the

Cash Handling Policy & Procedures Purpose SB 2015-2016:14 The cash handling policy and procedures outlined in this document are intended to provide guidance and appropriate segregation of duties on the

A Key Controls Audit of the Friendly Neighborhood Senior Center

Office of the Salt Lake County Auditor Scott Tingley, CIA, CGAP Report No. 2017- MLR01 November 2017 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief

Office of the Salt Lake County Auditor Scott Tingley, CIA, CGAP Report No. 2017- MLR01 November 2017 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief

Examination Process Investment and Cash Analysis October 26, 2002

1 Examination Process Investment and Cash Analysis October 26, 2002 Credit unions continue to improve their mobilization of member savings and, in some cases, the demand by members for loans does not keep

1 Examination Process Investment and Cash Analysis October 26, 2002 Credit unions continue to improve their mobilization of member savings and, in some cases, the demand by members for loans does not keep

Debit and Credit Rules Module 2 part I. T- Accounts Assets = Liabilities + OE. T- Accounts: Basic Patterns A = L + OE

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

Salt Lake County Library Imprest Fund

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

Safeguarding the Financial Assets of Your Church. Indiana Conference of the United Methodist Church

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

XI ACCOUNTING REGULAR / PRIVATE

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES Objective: To secure public funds and to protect the staff member, as well as the District, against any type of fraud or misapproation of funds that might

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES Objective: To secure public funds and to protect the staff member, as well as the District, against any type of fraud or misapproation of funds that might

IMPREST ACCOUNTS. Policy i

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

Salt Lake County Auditor. A Key Control Audit of the Kearns Senior Center

Office of the Salt Lake County Auditor Scott Tingley, CIA, CGAP SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

Office of the Salt Lake County Auditor Scott Tingley, CIA, CGAP SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR AUTHORITY AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A AS

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR AUTHORITY AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A AS

Chapter 20 Notes Uncollectible Accounts Expense

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

Chapter 5. Cash Control Systems

Chapter 5 Cash Control Systems 5-1 Terms checking account: a bank account from which payments can be ordered by a depositor code of conduct: a statement that guides the ethical behavior of a company and

Chapter 5 Cash Control Systems 5-1 Terms checking account: a bank account from which payments can be ordered by a depositor code of conduct: a statement that guides the ethical behavior of a company and

Accounting I Lesson Plan

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Cash Control Systems Unit: Chapter 7 I. Objective(s): By the end of today s lesson, the student will be able to: define accounting terms related

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Cash Control Systems Unit: Chapter 7 I. Objective(s): By the end of today s lesson, the student will be able to: define accounting terms related

Toronto Children s Services Operating Criteria. Financial Management Criteria. January 2010

Toronto Children s Services Operating Criteria Financial Management Criteria January 00 FINANCIAL MANAGEMENT CRITERIA For all funded programs: Child Care Centres, Home Child Care Agencies, Special Needs

Toronto Children s Services Operating Criteria Financial Management Criteria January 00 FINANCIAL MANAGEMENT CRITERIA For all funded programs: Child Care Centres, Home Child Care Agencies, Special Needs

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CASH: CAMPUS CASH COLLECTION DEPOSITS C ACCOUNTING MANUAL Page 1 CASH: CAMPUS CASH COLLECTION DEPOSITS. Contents. I.

ACCOUNTING MANUAL Page 1 CASH: CAMPUS CASH COLLECTION DEPOSITS Contents Page I. Introduction 2 II. Procedures 2 A. Depositing Cash Receipts 2 B. Recording Cash Deposits 3 C. Transfer of Funds to the Treasurer's

ACCOUNTING MANUAL Page 1 CASH: CAMPUS CASH COLLECTION DEPOSITS Contents Page I. Introduction 2 II. Procedures 2 A. Depositing Cash Receipts 2 B. Recording Cash Deposits 3 C. Transfer of Funds to the Treasurer's

EXERCISES. The complete AICPA summary of Section 404 of Sarbanes-Oxley is as follows: Section 404: Management Assessment of Internal Controls.

EXERCISES Ex. 7 1 Section 404 requires management s internal control report to: (1) state the responsibility of management for establishing and maintaining an adequate internal control structure and procedures

EXERCISES Ex. 7 1 Section 404 requires management s internal control report to: (1) state the responsibility of management for establishing and maintaining an adequate internal control structure and procedures

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 8 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF RECEIVABLES PROBLEM NO. 1 In the audit of Beatles Company, the auditor had an appreciation of the following schedule and noted

Page 1 of 8 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF RECEIVABLES PROBLEM NO. 1 In the audit of Beatles Company, the auditor had an appreciation of the following schedule and noted

CASH HANDLING POLICIES

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

Multiple choice question 51 A small neighborhood barber shop that is operated by its owner would likely be organized as a Proprietorship.

FINAL EXAM Financial accounting Multiple choice question 92 The best definition of assets is the Resources belonging to a company that have future benefit to the company. Collections of resources belonging

FINAL EXAM Financial accounting Multiple choice question 92 The best definition of assets is the Resources belonging to a company that have future benefit to the company. Collections of resources belonging

Purchasing Card Pcard Procedures Manual

Purchasing Card Pcard Procedures Manual Welcome to Franklin and Marshall College s Purchasing Card (Pcard) Program. The purpose of the program is to provide authorized College personnel with an additional,

Purchasing Card Pcard Procedures Manual Welcome to Franklin and Marshall College s Purchasing Card (Pcard) Program. The purpose of the program is to provide authorized College personnel with an additional,

Accounting Cycle. Ahmad Tariq Bhatti. The Fundamentals of Accounting. FCMA, FPA, MA (Economics), BSc Dubai, United Arab Emirates

, BSc Dubai, United Arab Emirates") Accounting Cycle The Fundamentals of Accounting Ahmad Tariq Bhatti FCMA, FPA, MA (Economics), BSc Dubai, United Arab Emirates Contents UNIT 1: ACCOUNTING CYCLE 7 1.1 Assumptions of financial accounting

Accounting Cycle The Fundamentals of Accounting Ahmad Tariq Bhatti FCMA, FPA, MA (Economics), BSc Dubai, United Arab Emirates Contents UNIT 1: ACCOUNTING CYCLE 7 1.1 Assumptions of financial accounting

QUEEN S UNIVERSITY BELFAST. Cash Handling Procedures

QUEEN S UNIVERSITY BELFAST Cash Handling Procedures Version Detail Author Approval Date v1.0 Final Finance Directorate Director of Finance July 2017 1 Introduction... 2 1.1 Definitions... 3 1.2 Scope of

QUEEN S UNIVERSITY BELFAST Cash Handling Procedures Version Detail Author Approval Date v1.0 Final Finance Directorate Director of Finance July 2017 1 Introduction... 2 1.1 Definitions... 3 1.2 Scope of

The Hidden Costs of Paper-Based Payments. How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships

The Hidden Costs of Paper-Based Payments How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships The Hidden Costs of a Simple Check B2B payment methods are slow and

The Hidden Costs of Paper-Based Payments How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships The Hidden Costs of a Simple Check B2B payment methods are slow and

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities