BANKING PROCEDURE AND CONTROL OF CASH

|

|

|

- Stephany Harper

- 6 years ago

- Views:

Transcription

1 BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6

2 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing a petty cash fund; setting up an auxiliary petty cash record. 4. Establishing and replenishing a change fund. 5. Handling transactions involving cash short and over. 6-2

3 Cash Most easily stolen, lost, or mishandled Need to protect all cash receipts and to control cash payments 6-3 Establish good internal control, a system of procedures and methods to safeguard cash and monitor operations

4 Internal Control Examples Responsibilities and duties of employees are divided All cash receipts are deposited into the bank on a daily basis All cash payments are made by check Employees are rotated All checks are authorized for payment Bank accounts are reconciled monthly 6-4

5 Learning Objective 1 Depositing, writing, and endorsing checks for a checking account 6-5

6 Checking Account: Getting Started Signature Card - verifies the authenticity of the signature on all checks Deposit Slip - form used when making deposits Lists each check individually Lists total amount of currency, coins & checks being deposited Debit Card - carries MasterCard/Visa logo Use anywhere MasterCard/Visa are accepted Amount of purchase is deducted directly from the checking account 6-6

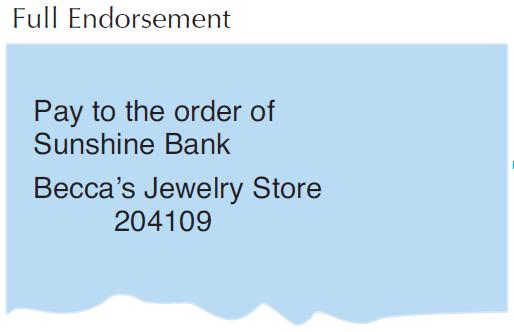

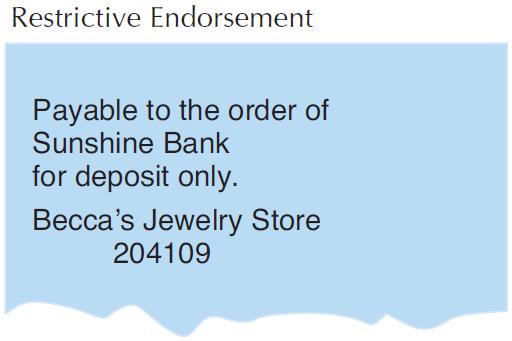

7 Checking Account: Check Endorsement Endorsement signing or stamping of one s name on back of check Payee has transferred the right to deposit or cash the check to someone else 6-7

8 Checking Account: Check Endorsement Types Blank endorsement does not specify that a particular entity must endorse it Full endorsement entity signing the back of the check indicates the name of the entity to whom the check is to be paid Restrictive endorsement stamped for deposit only 6-8

9 Checking Account: Check Endorsement 6-9

10 Journal Entries to Record Deposits Proceeds of cash sales Proceeds of collections of company accounts receivable 6-10

11 Other Sources of Revenue Credit cards, which are issued by financial institutions and by credit card companies MasterCard, VISA, and Discover American Express A drawback is that merchants typically must pay a service fee 6-11

12 Other Sources of Revenue Debit cards are issued by banks, savings and loan institutions, and credit unions on behalf of depositors Card is not an extension of credit Holder cannot spend more than the balance currently in his or her account With minor exceptions, it is the same as a credit card 6-12

13 The Checkbook When checking account is first opened, checks are issued Check written order signed by drawer instructing a drawee to pay specific sum of money to payee Cancelled Checks - have been processed by the bank and are no longer negotiable 6-13

14 FIGURE

15 Amount mismatch If the written amount on the check does not match the amount expressed in figures, the bank may: Pay the amount written in words Return the check unpaid, or Contact the drawer to see what was intended 6-15

16 In-Company Records Records must be kept for all transactions Bank deposits Checks written 6-16

17 Bank Statement Reflects all activity in the account during that period Starts off with the beginning balance The checks that the bank has paid are subtracted Any deposits received are added to the account Other charges or additions are indicated by special codes 6-17

18 A Bank Statement 6-18

19 Learning Objective 2 Reconciling a bank statement 6-19

20 Bank Reconciliation Process Process of reconciling the checkbook balance with the bank balance given on the bank statement Steps: Calculate deposits in transit and outstanding checks Recognize service charges and fees 6-20

21 Bank Reconciliation Process 6-21

22 Additional Transactions NSF (nonsufficient funds) - a check that has been returned because the drawer did not have enough money in its account to pay the check Debit memorandum - a deduction from the account holder s balance Credit memorandum - an increase in the account holder s balance 6-22

23 Step-by-step Instructions for Preparing a Bank Reconciliation Prepare a list of deposits in transit. Prepare a list of outstanding checks. Record any bank charges or credits. Compute the cash balance per your books. Enter bank balance on the reconciliation. Total the deposits in transit. Total the outstanding checks. Compute the balance per the reconciliation. The result should equal the balance shown in your general ledger. 6-23

24 Trends in Banking Electronic funds transfer (EFT) is a way to transfer funds electronically without the use of paper checks. Automatic teller machines (ATMs) allow customers to make deposits, withdraw money, and obtain account balances without having to stand in line when the bank is open. 6-24

25 Advantages of Online Banking 6-25 Convenience: Unlike your corner site, online banks never close. Availability: You can log on instantly to your online bank and take care of business 24/7. Transaction speed: Online bank sites generally execute and confirm transactions as quickly or even faster than ATM processing speeds. Efficiency: You can access and manage all of your bank accounts from one secure site. Effectiveness: Many online banking sites now offer sophisticated tools to help you manage all of your assets more effectively.

26 Disadvantages of Online Banking 6-26 Although online banking has many advantages, it also has some disadvantages: Start-up may take time: In order to register, you will probably have to provide some personal identification and sign a form at a branch bank. Learning curve: Banking sites can be difficult to navigate at first. Bank site changes: Even the largest banks periodically upgrade their online programs, adding new features in unfamiliar places. Trust: For many people, the biggest hurdle to online banking is learning to trust it.

27 Fraudulent practices Phishing involves fake s that attempt to obtain information about online banking customers. Skimming is the theft of credit card information used in an otherwise legitimate debit card or credit card transaction. 6-27

28 Tips to Help You Avoid Becoming a Skimming Victim Keep your PIN safe. Don t give it to anyone. Watch out for people who try to help you at an ATM. Look at the ATM before using it. If it doesn't t look right, don t use it. If an ATM has any unusual signage, don t use it. If your card is not returned after the transaction or after pressing cancel, immediately contact the institution that issued the card. Check your statement to be sure that no unusual withdrawals appear on it. 6-28

29 Learning Objective 3 Establishing and replenishing a petty cash fund; setting up an auxiliary petty cash record 6-29

30 Petty Cash Fund Account dedicated to paying small day-to-day expenses Recorded in an auxiliary record Later summarized, journalized, and posted Asset account, normal debit balance Custodian oversees the fund 6-30

31 Setting Up the Petty Cash Fund A new asset, called Petty Cash, is created by writing a check and reducing the asset Cash 6-31

32 Operating the Petty Cash Fund Petty Cash account is debited or credited if size of fund is changed Vouchers used when money is removed from the fund Filled out each time a payment is made Vouchers are sequentially numbered Voucher totals plus cash on hand should equal the original petty cash balance 6-32

33 Petty Cash Vouchers Contains: The voucher number (which will be in sequence) The date To whom the payment was made The amount of payment The reason for payment The signature of the person approving The signature of the person receiving The account to which the item will be charged 6-33

34 Petty Cash Voucher Example 6-34

35 Auxiliary Petty Cash Record At the end of May, the following items are documented by vouchers: 6-35

36 Auxiliary Petty Cash Record Voucher information is transferred to this record: 6-36

37 Replenish The Petty Cash Fund No postings are done from the auxiliary record The compiled information is used as a basis for the formal journal entry A check is issued for the expense total and cashed; the cash is replaced in the petty cash box 6-37 Debits are a summary of the totals of expenses

38 Replenish The Petty Cash Fund 6-38

39 Learning Objective 4 Establishing and replenishing a change fund 6-39

40 Setting Up a Change Fund Change Fund is made up of various denominations Fund is placed in the cash register drawer and used to make change 6-40

41 Learning Objective 5 Handling transactions involving cash short and over 6-41

42 Cash Short and Over Account Errors often happen in making change Must record both overages and shortages A shortage is considered a miscellaneous expense An overage is considered as other-income 6-42

43 Example 1: Shortages and Overages in Sales On December 5, a pizza shop rang up sales of $560 for the day but only had $530 in cash 6-43

44 Example 1: Shortages and Overages in Sales On December 5 a pizza shop rang up sales of $560 for the day but had $610 in cash. 6-44

45 Example 2: Cash Short and Over in Petty Cash A local computer company established petty cash for $200. On November 30, the petty cash box had $160 in vouchers as well as $32 in coin and currency. 6-45

46 Example 2: Cash Short and Over in Petty Cash In the case of an overage, the Cash Short and Over would be a credit as other income. 6-46

47 Questions 6-55

48 Copyright All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America. 6-56

Ch.6 Internal Control and Accounting for Cash

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

CHAPTER 5-THE BANKING SYSTEM. Section 1- Checking Accounts

CHAPTER 5-THE BANKING SYSTEM Section 1- Checking Accounts CHECKING ACCOUNTS Checking Account: A demand deposit account on which checks are drawn. Advantages of a checking account Safe place to keep money

CHAPTER 5-THE BANKING SYSTEM Section 1- Checking Accounts CHECKING ACCOUNTS Checking Account: A demand deposit account on which checks are drawn. Advantages of a checking account Safe place to keep money

College Accounting. Heintz & Parry. 20 th Edition

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

Checking Account Simulation. Understanding Checking Accounts

Checking Account Simulation Understanding Checking Accounts What is a Checking Account? 1.7.1.G1 Tool used to transfer funds deposited into the account to make a cash purchase Could also be named a transaction

Checking Account Simulation Understanding Checking Accounts What is a Checking Account? 1.7.1.G1 Tool used to transfer funds deposited into the account to make a cash purchase Could also be named a transaction

Checking 101 Checking Out Checking Accounts

Checking 101 Checking Out Checking Accounts Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share

Checking 101 Checking Out Checking Accounts Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share

Banking Basics 101. How to Manage Your Finances and Still Have Money Left Over For a Night Out. Course objectives learn about:

Banking Basics 101 Course objectives learn about: Using a checking account Various types of payment vehicles Benefits of a savings account How to Manage Your Finances and Still Have Money Left Over For

Banking Basics 101 Course objectives learn about: Using a checking account Various types of payment vehicles Benefits of a savings account How to Manage Your Finances and Still Have Money Left Over For

Share Draft/Checking Account Basics

Share Draft/Checking Account Basics A check is a written order that represents cash. Credit union checking accounts are called share draft accounts. Share drafts, like checks, are accepted almost everywhere.

Share Draft/Checking Account Basics A check is a written order that represents cash. Credit union checking accounts are called share draft accounts. Share drafts, like checks, are accepted almost everywhere.

Checking Account Simulation. Understanding Checking Accounts

Checking Account Simulation Understanding Checking Accounts What is a Checking Account? 1.7.1.G1 Tool used to transfer funds deposited into the account to make a cash purchase Could also be named a transaction

Checking Account Simulation Understanding Checking Accounts What is a Checking Account? 1.7.1.G1 Tool used to transfer funds deposited into the account to make a cash purchase Could also be named a transaction

Checking 101. Property of Penn State Federal Credit Union

Checking 101 Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is equivalent to a check,

Checking 101 Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is equivalent to a check,

PFIN 5: Banking Procedures 24

PFIN 5: Banking Procedures 24 5 1 Checking Accounts OBJECTIVES Explain the purpose and use of a checking account. Prepare a checkbook register. Write a check and prepare a deposit slip. Prepare a bank

PFIN 5: Banking Procedures 24 5 1 Checking Accounts OBJECTIVES Explain the purpose and use of a checking account. Prepare a checkbook register. Write a check and prepare a deposit slip. Prepare a bank

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check.

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

FINANCIAL SERVICES GETTING TO KNOW YOUR FINANCIAL INSTITUTION

FINANCIAL SERVICES GETTING TO KNOW YOUR FINANCIAL INSTITUTION History of financial institutions Federal Reserve Act 12 Federal Reserve Districts Non-Banking Financial Institutions -Credit Unions -Savings

FINANCIAL SERVICES GETTING TO KNOW YOUR FINANCIAL INSTITUTION History of financial institutions Federal Reserve Act 12 Federal Reserve Districts Non-Banking Financial Institutions -Credit Unions -Savings

Recognizing Credit Card Fraud

1 Recognizing Credit Card Fraud Credit card fraud happens when consumers give their credit card number to unfamiliar individuals, when cards are lost or stolen, when mail is diverted from the intended

1 Recognizing Credit Card Fraud Credit card fraud happens when consumers give their credit card number to unfamiliar individuals, when cards are lost or stolen, when mail is diverted from the intended

Welcome to Money Essentials SM!

Money Essentials SM Welcome to Money Essentials SM! Money Essentials provides you with a valuable, easy to understand introduction to financial services and is designed to give you realistic choices in

Money Essentials SM Welcome to Money Essentials SM! Money Essentials provides you with a valuable, easy to understand introduction to financial services and is designed to give you realistic choices in

Checking Account & Debit Card Simulation. Understanding Checking Accounts and Debit Card Transactions

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

Checking Account & Debit Card Simulation. Understanding Checking Accounts and Debit Card Transactions

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions Why Do People Use Checking Accounts? Reduces the need to carry large amounts of cash Convenience useful

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions Why Do People Use Checking Accounts? Reduces the need to carry large amounts of cash Convenience useful

Using Banking Services

Presentation Slides $ Lesson Six Using Banking Services 04/09 banking terms you should know Account ATM Bank Checking account Credit union Interest Joint account Minimum deposit Savings account Teller

Presentation Slides $ Lesson Six Using Banking Services 04/09 banking terms you should know Account ATM Bank Checking account Credit union Interest Joint account Minimum deposit Savings account Teller

Checking Account & Debit Card Simulation. Understanding Checking Accounts and Debit Card Transactions

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

Checking Account & Debit Card Simulation Understanding Checking Accounts and Debit Card Transactions What is a Checking Account? Common financial service used by many consumers Funds are easily accessed

the CHECKBOOK issue CHECKBOOK ISSUE BOOK.indb 3 3/28/09 6:25:51 PM

1 2 3 4 5 6 7 8 9 10 11 12 the CHECKBOOK issue Things that make you go hmmm... Transpose What???? Transposed numbers = TROUBLE BALANCE GOOOOOOD! - Balancing your checkbook accurately should bring a sense

1 2 3 4 5 6 7 8 9 10 11 12 the CHECKBOOK issue Things that make you go hmmm... Transpose What???? Transposed numbers = TROUBLE BALANCE GOOOOOOD! - Balancing your checkbook accurately should bring a sense

HOW TO USE A FINANCIAL INSTITUTION. BUILDING A better FUTURE

HOW TO USE A FINANCIAL INSTITUTION BUILDING A better FUTURE HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER Copyright 2011 Latino Community Credit

HOW TO USE A FINANCIAL INSTITUTION BUILDING A better FUTURE HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER Copyright 2011 Latino Community Credit

Chapter 5: Cash Control Systems

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

Chapter 5. Cash Control Systems

Chapter 5 Cash Control Systems 5-1 Terms checking account: a bank account from which payments can be ordered by a depositor code of conduct: a statement that guides the ethical behavior of a company and

Chapter 5 Cash Control Systems 5-1 Terms checking account: a bank account from which payments can be ordered by a depositor code of conduct: a statement that guides the ethical behavior of a company and

check debit card overdraw deposit slip endorse bank statement certified check cashier s check money order traveler s check

How can a checking account help me to manage my money? Chapter 25 Key Terms check debit card overdraw deposit slip endorse bank statement certified check cashier s check money order traveler s check Chapter

How can a checking account help me to manage my money? Chapter 25 Key Terms check debit card overdraw deposit slip endorse bank statement certified check cashier s check money order traveler s check Chapter

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES

GUIDELINES AND PROCEDURES") FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

TABLE OF CONTENTS. Introduction 3. General Guidelines for Successful Account Management 3. Managing Your Checking Account. 1.

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

TABLE OF CONTENTS Introduction 3 General Guidelines for Successful Account Management 3 Managing Your Checking Account 1. Check Register 2. Planning 3. Recording Your Transactions 4. Balancing Your Account

Sarbanes-Oxley Act of 2002

Sarbanes-Oxley Act of 2002 The Sarbanes-Oxley Act of 2002 (often referred to simply as Sarbanes-Oxley) applies only to companies whose stock is traded on public exchanges. Its purpose is to restore public

Sarbanes-Oxley Act of 2002 The Sarbanes-Oxley Act of 2002 (often referred to simply as Sarbanes-Oxley) applies only to companies whose stock is traded on public exchanges. Its purpose is to restore public

Chapter 7 Student Version

Sarbanes-Oxley, Internal Control, and Cash Chapter 7 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor

Sarbanes-Oxley, Internal Control, and Cash Chapter 7 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor

Fundamental Accounting Principles, Volume 1, Fifteenth Canadian Edition

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Sarbanes-Oxley, Internal Control, and Cash

C H A P T E R 7 Sarbanes-Oxley, Internal Control, and Cash Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Sarbanes-Oxley Act (slide 1 of 2) Sarbanes-Oxley emphasizes

C H A P T E R 7 Sarbanes-Oxley, Internal Control, and Cash Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Sarbanes-Oxley Act (slide 1 of 2) Sarbanes-Oxley emphasizes

Using Banking Services

Teacher's Guide $ Lesson Six Using Banking Services 04/09 using banking services websites websites for banking services The internet is probably the most extensive and dynamic source of information in

Teacher's Guide $ Lesson Six Using Banking Services 04/09 using banking services websites websites for banking services The internet is probably the most extensive and dynamic source of information in

Debit Card User Guide

Debit Card User Guide HSBC Premier Debit Cards Access your funds and pay for your purchases wherever you are. Dear Customer, Welcome to the new era of HSBC Premier Debit Chip Cards. Your key to more convenient

Debit Card User Guide HSBC Premier Debit Cards Access your funds and pay for your purchases wherever you are. Dear Customer, Welcome to the new era of HSBC Premier Debit Chip Cards. Your key to more convenient

PAYMENT CARD INDUSTRY

DATA SECURITY POLICY Page 1 of 1 I. PURPOSE To provide guidelines and procedures to ensure that all money paid to the College in the form of cash, checks or payment cards is properly receipted, accounted

DATA SECURITY POLICY Page 1 of 1 I. PURPOSE To provide guidelines and procedures to ensure that all money paid to the College in the form of cash, checks or payment cards is properly receipted, accounted

Chapter 06 - Cash and Internal Controls. Chapter Outline

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

Arvest Bank ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE The federal Electronic Fund Transfer Act and Regulation E require financial institutions to provide certain information to consumers (i.e.,

Arvest Bank ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE The federal Electronic Fund Transfer Act and Regulation E require financial institutions to provide certain information to consumers (i.e.,

THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Name: Period: Orientation to Business Chapter 28 Notes

Name: Period: Orientation to Business Chapter 28 Notes Money Management Budget o Includes (3 key things) 5 steps 1. Set Goals 2. Estimate Income (define each) Income: Gross Pay: Deductions: Net Pay: 1

Name: Period: Orientation to Business Chapter 28 Notes Money Management Budget o Includes (3 key things) 5 steps 1. Set Goals 2. Estimate Income (define each) Income: Gross Pay: Deductions: Net Pay: 1

Chapter 4. Banking 4-1. McGraw-Hill/Irwin. Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 4 Banking 4-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Checks Written order instructing a bank, credit union, or savings and loan institution to

Chapter 4 Banking 4-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Checks Written order instructing a bank, credit union, or savings and loan institution to

Get Ready to Take Charge of Your Finances

Checking Account & Debit Card Simulation Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 180 minutes National Content Standards Family and Consumer Science Standards: 1.1.6,

Checking Account & Debit Card Simulation Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 180 minutes National Content Standards Family and Consumer Science Standards: 1.1.6,

Electronic Payment Card Program Frequently Asked Questions

1. What is the new Visa Electronic Payment Card? The Visa Electronic Payment Card (EPC) is a safe and secure method for payment of weekly Unemployment Insurance benefits. It can be used to get cash from

1. What is the new Visa Electronic Payment Card? The Visa Electronic Payment Card (EPC) is a safe and secure method for payment of weekly Unemployment Insurance benefits. It can be used to get cash from

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT. Martha's Vineyard Savings Bank 78 Main Street Edgartown, MA

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT Martha's Vineyard Savings Bank 78 Main Street 508-627-4266 For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to Martha's

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT Martha's Vineyard Savings Bank 78 Main Street 508-627-4266 For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to Martha's

HSBC Visa Credit Card User Guide

HSBC Visa Credit Card User Guide Welcome to the world full of privileges for HSBC Visa Credit Cardholders. You are about to discover the exclusive privileges brought to you by HSBC Credit Cards. You ll

HSBC Visa Credit Card User Guide Welcome to the world full of privileges for HSBC Visa Credit Cardholders. You are about to discover the exclusive privileges brought to you by HSBC Credit Cards. You ll

Basics of Banking. What Are Banks, Anyway? Types of Financial Institutions. Table of Contents

Basics of Banking This information is provided to you as a courtesy and does not constitute financial, tax or legal advice. Information provided in the financial modules may not be current and/or up to

Basics of Banking This information is provided to you as a courtesy and does not constitute financial, tax or legal advice. Information provided in the financial modules may not be current and/or up to

Step-Up Checking Program Disclosure

130 S. Main Street Fond du Lac, WI 54935 920.921.7700 Step-Up Checking Program Disclosure ELIGIBILITY REQUIREMENTS To be eligible for a Step-Up Checking Program, you must be less than 26 years of age and

130 S. Main Street Fond du Lac, WI 54935 920.921.7700 Step-Up Checking Program Disclosure ELIGIBILITY REQUIREMENTS To be eligible for a Step-Up Checking Program, you must be less than 26 years of age and

A banking service allowing a customer s money to be handled and tracked. Common bank accounts are savings and checking accounts.

Kids Glossary Terms Account Account balance Account fee Annual fee Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank Bank account Bank statement Bounced

Kids Glossary Terms Account Account balance Account fee Annual fee Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank Bank account Bank statement Bounced

Teens Glossary Terms. (see Bank account)

") Teens Glossary Terms Account Account balance Account fee Annual fee Annual percentage rate (APR) Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank (see Bank

Teens Glossary Terms Account Account balance Account fee Annual fee Annual percentage rate (APR) Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank (see Bank

Checking Account and Debit Card Simulation

Checking Account and Debit Card Simulation Student Instructions and Worksheets Introductory Level Take Charge Today May 2006 Checking Account & Debit Card Simulation Page 1 Checking Account Student Instructions

Checking Account and Debit Card Simulation Student Instructions and Worksheets Introductory Level Take Charge Today May 2006 Checking Account & Debit Card Simulation Page 1 Checking Account Student Instructions

Quick Write. Learn About. The Advantages of Bank Services. I saw a bank that said 24 Hour Banking, but I don t have that much time.

LESSON 2 Quick Write I saw a bank that said 24 Hour Banking, but I don t have that much time. Stephen Wright, famous writer Your summer part-time job has allowed you to save $300, and your grandparents

LESSON 2 Quick Write I saw a bank that said 24 Hour Banking, but I don t have that much time. Stephen Wright, famous writer Your summer part-time job has allowed you to save $300, and your grandparents

Check It Out. FDIC Money Smart for Young Adults. Building: Knowledge, Security, Confidence

Check It Out FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Purpose Check It Out will teach you how to use a checking account responsibly 2 Objectives By the end of this course,

Check It Out FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Purpose Check It Out will teach you how to use a checking account responsibly 2 Objectives By the end of this course,

Fairport Public Library

Fairport Public Library Policies and Procedures Manual Cash Handling Table of Contents: I. Policy Statement II. Procedures III. Record Keeping IV. Appendix I. Policy Statement: This policy defines the

Fairport Public Library Policies and Procedures Manual Cash Handling Table of Contents: I. Policy Statement II. Procedures III. Record Keeping IV. Appendix I. Policy Statement: This policy defines the

Financial Services. All Classes. Vocabulary. Name Period Day

Name Period Day Financial Services All Classes Once you ve started earning money, you have to figure out the best way to spend it. Not what to spend it on necessarily you already did that with your budget,

Name Period Day Financial Services All Classes Once you ve started earning money, you have to figure out the best way to spend it. Not what to spend it on necessarily you already did that with your budget,

CASH ACCOUNTING MANUAL

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ELECTRONIC FUND TRANSFER DISCLOSURE

ELECTRONIC FUND TRANSFER DISCLOSURE www.bankfirstfs.com For purposes of this disclosure the terms "we", "us" and "our" refer to BankFirst Financial Services. The terms "you" and "your" refer to the recipient

ELECTRONIC FUND TRANSFER DISCLOSURE www.bankfirstfs.com For purposes of this disclosure the terms "we", "us" and "our" refer to BankFirst Financial Services. The terms "you" and "your" refer to the recipient

Personal Interest Bearing Checking Account-Related Disclosures

130 S. Main Street Fond du Lac, WI 54935 920.921.7700 Personal Interest Bearing Checking Account-Related Disclosures VARIABLE RATE INFORMATION Please see our online rate information for current interest

130 S. Main Street Fond du Lac, WI 54935 920.921.7700 Personal Interest Bearing Checking Account-Related Disclosures VARIABLE RATE INFORMATION Please see our online rate information for current interest

UH/Student Business Services Policies and Procedures

UH/Student Business Services Policies and Procedures CASH HANDLING Student Business Services (SBS) is the primary University of Houston department responsible for revenue collection of approved tuition,

UH/Student Business Services Policies and Procedures CASH HANDLING Student Business Services (SBS) is the primary University of Houston department responsible for revenue collection of approved tuition,

Checking Account and Debit Card Simulation

Checking Account and Debit Card Simulation Student Instructions and Worksheets Get Ready to Take Charge of Your Finances Family Economics & Financial Education May 2006 Get Ready to Take Charge of Your

Checking Account and Debit Card Simulation Student Instructions and Worksheets Get Ready to Take Charge of Your Finances Family Economics & Financial Education May 2006 Get Ready to Take Charge of Your

State Bank Financial State Bank Shelby 4020 Mormon Coulee Road La Crosse WI ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

State Bank Financial State Bank Shelby 4020 Mormon Coulee Road 608.788.0400 ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our"

State Bank Financial State Bank Shelby 4020 Mormon Coulee Road 608.788.0400 ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our"

Selected Terms & Conditions for Wells Fargo Business Debit, ATM and Deposit Cards

Selected Terms & Conditions for Wells Fargo Debit, ATM and Deposit Cards Terms and Conditions effective 04/24/2017. Introduction page 1 Using Your Card page 2 Using Your Card Through a Mobile Device page

Selected Terms & Conditions for Wells Fargo Debit, ATM and Deposit Cards Terms and Conditions effective 04/24/2017. Introduction page 1 Using Your Card page 2 Using Your Card Through a Mobile Device page

Hamilton Bank 501 Fairmount Avenue, Suite 200 Towson, MD ELECTRONIC FUND TRANSFER DISCLOSURE

Hamilton Bank 501 Fairmount Avenue, Suite 200 Towson, MD. 21286-5469 www.hamilton-bank.com ELECTRONIC FUND TRANSFER DISCLOSURE For purposes of this disclosure the terms "we", "us" and "our" refer to Hamilton

Hamilton Bank 501 Fairmount Avenue, Suite 200 Towson, MD. 21286-5469 www.hamilton-bank.com ELECTRONIC FUND TRANSFER DISCLOSURE For purposes of this disclosure the terms "we", "us" and "our" refer to Hamilton

Accounting I Lesson Plan

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Cash Control Systems Unit: Chapter 7 I. Objective(s): By the end of today s lesson, the student will be able to: define accounting terms related

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Cash Control Systems Unit: Chapter 7 I. Objective(s): By the end of today s lesson, the student will be able to: define accounting terms related

Checking Account Simulation. Understanding Checking Accounts

Checking Account Simulation Understanding Checking Accounts What is a Checking Account? 1.7.1.G1 Tool used to transfer funds deposited into the account to make a cash purchase Benefits Can help to manage

Checking Account Simulation Understanding Checking Accounts What is a Checking Account? 1.7.1.G1 Tool used to transfer funds deposited into the account to make a cash purchase Benefits Can help to manage

Chapter 5 Banking Procedures. Copyright 2007 Thomson South-Western

Chapter 5 Banking Procedures Copyright 2007 Thomson South-Western Introduction to Checking Accounts A check is a written order to pay a stated amount to a person or business Checking account Is a demand

Chapter 5 Banking Procedures Copyright 2007 Thomson South-Western Introduction to Checking Accounts A check is a written order to pay a stated amount to a person or business Checking account Is a demand

YOUR RIGHTS AND RESPONSIBILITIES

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT YOUR RIGHTS AND RESPONSIBILITIES www.morris.bank For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to Morris Bank. The

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT YOUR RIGHTS AND RESPONSIBILITIES www.morris.bank For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to Morris Bank. The

First Savings Bank of Hegewisch

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT First Savings Bank of Hegewisch For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to First Savings Bank of Hegewisch.

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT First Savings Bank of Hegewisch For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to First Savings Bank of Hegewisch.

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

Fidelity Federal Sv & Ln Association 60 N. Sandusky St. and 1940 St. Rt. 37 W PO Box 279 740-363-1284, 740-363-1233 or 740-548-4300 www.fidfedsl.com ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For

Fidelity Federal Sv & Ln Association 60 N. Sandusky St. and 1940 St. Rt. 37 W PO Box 279 740-363-1284, 740-363-1233 or 740-548-4300 www.fidfedsl.com ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For

Name: Be sure to compute the total

Name: A deposit slip contains the account holder s account number and allows money (cash or check) to be deposited into the correct account. When filling out a deposit slip, enter the following: Date of

Name: A deposit slip contains the account holder s account number and allows money (cash or check) to be deposited into the correct account. When filling out a deposit slip, enter the following: Date of

Overdraft Education Practice & Reference Materials

Overdraft Education Practice & Reference Materials 2013 IN-Focus Digital Booklet Instructions 2 This booklet is designed for use with the Overdraft Education Workshop video. Any unauthorized use is prohibited

Overdraft Education Practice & Reference Materials 2013 IN-Focus Digital Booklet Instructions 2 This booklet is designed for use with the Overdraft Education Workshop video. Any unauthorized use is prohibited

Electronic Funds Transfer - Your Rights and Responsibilities ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

Marblehead Bank 21 Atlantic Avenue - 1 Humphrey Street Marblehead MA 01945 100 Cummings Center - Suite 101-F Beverly MA 01915 781-631-5500 customercare@marblebank.com marblebank.com Electronic Funds Transfer

Marblehead Bank 21 Atlantic Avenue - 1 Humphrey Street Marblehead MA 01945 100 Cummings Center - Suite 101-F Beverly MA 01915 781-631-5500 customercare@marblebank.com marblebank.com Electronic Funds Transfer

Accounting Terms Chap 1-8

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from. Union State Bank 545 Main Street Everest, KS (785)

") IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from Union State Bank 545 Main Street Everest, KS 66424 (785)548-7521 ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types

IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from Union State Bank 545 Main Street Everest, KS 66424 (785)548-7521 ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types

Chapter 7 Question Review 1

Chapter 7 Question Review 1 Chapter 7 Questions Multiple Choice 1. The entry to replenish a petty cash fund includes a credit to a. Petty Cash. b. Cash. c. Freight-In. d. Postage Expense. 2. A $300 petty

Chapter 7 Question Review 1 Chapter 7 Questions Multiple Choice 1. The entry to replenish a petty cash fund includes a credit to a. Petty Cash. b. Cash. c. Freight-In. d. Postage Expense. 2. A $300 petty

IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from. The Tri-County Bank 106 N Main St Stuart, NE (402)

") IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from The Tri-County Bank 106 N Main St Stuart, NE 68780 (402)924-3861 ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types

IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from The Tri-County Bank 106 N Main St Stuart, NE 68780 (402)924-3861 ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types

General Information for Cardholder s on PIN & PAY

General Information for Cardholder s on PIN & PAY As part of our on-going initiative to enhance security, we are pleased to introduce the 6-digit PIN (Personal Identification Number) for validation, replacing

General Information for Cardholder s on PIN & PAY As part of our on-going initiative to enhance security, we are pleased to introduce the 6-digit PIN (Personal Identification Number) for validation, replacing

ELECTRONIC FUNDS TRANSFER DISCLOSURE ERROR RESOLUTION NOTICE DEBIT CARD AGREEMENT

ELECTRONIC FUNDS TRANSFER DISCLOSURE ERROR RESOLUTION NOTICE DEBIT CARD AGREEMENT A. Consumer Liability Tell us AT ONCE if you believe your card has been lost or stolen, or if you believe that an electronic

ELECTRONIC FUNDS TRANSFER DISCLOSURE ERROR RESOLUTION NOTICE DEBIT CARD AGREEMENT A. Consumer Liability Tell us AT ONCE if you believe your card has been lost or stolen, or if you believe that an electronic

Policy Statement. Policy Manager and Responsible Department or Office. Purpose/Reason for the Policy. Departments/Offices Affected by the Policy

OFFICIAL POLICY 2.2.3.1 Cash Receipts Policy 3/3/2016 Policy Statement The purpose of this document is to provide guidelines for departments generating funds on behalf of the College. Departments demonstrating

OFFICIAL POLICY 2.2.3.1 Cash Receipts Policy 3/3/2016 Policy Statement The purpose of this document is to provide guidelines for departments generating funds on behalf of the College. Departments demonstrating

CASH HANDLING PROCEDURES

CASH HANDLING PROCEDURES 1.0 OBJECTIVE: The primary purpose of this document is to established campus protocol and procedural guidelines for the handling of cash and cash equivalents and appropriate segregation

CASH HANDLING PROCEDURES 1.0 OBJECTIVE: The primary purpose of this document is to established campus protocol and procedural guidelines for the handling of cash and cash equivalents and appropriate segregation

BANKING SERVICES AND PROCEDURES

CHAPTER 23 VOCABULARY REVIEW 1. clearinghouses 2. maker 3. principal 4. payer, payee 5. holder BANKING SERVICES AND PROCEDURES 6. Uniform Commercial Code 7. drawee 8. negotiable 9. disbursements 10. reconciliation

CHAPTER 23 VOCABULARY REVIEW 1. clearinghouses 2. maker 3. principal 4. payer, payee 5. holder BANKING SERVICES AND PROCEDURES 6. Uniform Commercial Code 7. drawee 8. negotiable 9. disbursements 10. reconciliation

get cash withdrawals from savings account(s) with an ATM card get cash withdrawals from savings account(s) with a debit card

with an ATM card get cash withdrawals from savings account(s) with a debit card") ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types of Electronic Fund Transfers we are capable of handling, some of which may not apply to your account. Please read this

ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types of Electronic Fund Transfers we are capable of handling, some of which may not apply to your account. Please read this

Debit MasterCard. Conditions of Use. These are the conditions of use that apply to your Rabobank Debit MasterCard. You must read and retain them.

Debit MasterCard Conditions of Use These are the conditions of use that apply to your Rabobank Debit MasterCard. You must read and retain them. June 2016 Contents 1. Signing your card... 3 2. Ownership

Debit MasterCard Conditions of Use These are the conditions of use that apply to your Rabobank Debit MasterCard. You must read and retain them. June 2016 Contents 1. Signing your card... 3 2. Ownership

Date Here. Welcome University of Michigan International Students

Date Here Welcome University of Michigan International Students U.S. Banking System Overview Banking is regulated by federal and state governments Privacy Disclosure Fraud protection Protection against

Date Here Welcome University of Michigan International Students U.S. Banking System Overview Banking is regulated by federal and state governments Privacy Disclosure Fraud protection Protection against

WUPRPM. Regulations and Procedures Effective Date: May 11, 2007 L. Cash Collections and Cash Funds Revision Date: November 1, 2012.

Table of Contents 1. Purpose... 3 2. Definitions... 3 3. Security of Cash Funds... 3 4. Cash Collections General... 5 5. Cash Collections Procedures... 6 6. Procedures Common to Petty Cash and Change Funds...

Table of Contents 1. Purpose... 3 2. Definitions... 3 3. Security of Cash Funds... 3 4. Cash Collections General... 5 5. Cash Collections Procedures... 6 6. Procedures Common to Petty Cash and Change Funds...

Office of the Bursar 7/11/2018 1

These are Ohio University-wide guidelines and shall apply to all staff members of the University. The cash handling guidelines focus on preventing the mishandling or loss of cash and situations where charges

These are Ohio University-wide guidelines and shall apply to all staff members of the University. The cash handling guidelines focus on preventing the mishandling or loss of cash and situations where charges

Chapter 23 Audit of Cash and Financial Instruments. Copyright 2014 Pearson Education

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

ATM/DEBIT CARD DISCLOSURE CHECKING ACCOUNT DISCLOSURE...3 ELECTRONIC FUNDS TRANSFER ACT DISCLOSURE

DISCLOSURES INDEX ATM/DEBIT CARD DISCLOSURE... 1-2 CHECKING ACCOUNT DISCLOSURE...3 ELECTRONIC FUNDS TRANSFER ACT DISCLOSURE... 4-5 ELECTRONIC WHOLESALE CREDIT TRANSACTIONS...6 PRIVACY POLICY... 7-8 ROYAL

DISCLOSURES INDEX ATM/DEBIT CARD DISCLOSURE... 1-2 CHECKING ACCOUNT DISCLOSURE...3 ELECTRONIC FUNDS TRANSFER ACT DISCLOSURE... 4-5 ELECTRONIC WHOLESALE CREDIT TRANSACTIONS...6 PRIVACY POLICY... 7-8 ROYAL

Greenfield Savings Bank 400 Main Street Greenfield, MA (413) ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE") Greenfield Savings Bank 400 Main Street Greenfield, MA 01301 (413) 774-3191 ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our"

Greenfield Savings Bank 400 Main Street Greenfield, MA 01301 (413) 774-3191 ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our"

CHECKING 101 EDUCATION. Practice & Reference Material

CHECKING 101 EDUCATION Practice & Reference Material BOOKLET INFORMATION Thank you for your willingness to learn more about managing your checking account and how to better use the tools Armed Forces Bank

CHECKING 101 EDUCATION Practice & Reference Material BOOKLET INFORMATION Thank you for your willingness to learn more about managing your checking account and how to better use the tools Armed Forces Bank

Learning about. Checking. Accounts WHAT YOU NEED TO KNOW Deluxe Corp. All Right Reserved.

Learning about Checking Accounts WHAT YOU NEED TO KNOW 2010 Deluxe Corp. All Right Reserved. Contents Learn About Checking Accounts................................3 Write a Check....................................................4

Learning about Checking Accounts WHAT YOU NEED TO KNOW 2010 Deluxe Corp. All Right Reserved. Contents Learn About Checking Accounts................................3 Write a Check....................................................4

Selected Terms & Conditions for Wells Fargo Consumer Debit and ATM Cards

Selected Terms & Conditions for Wells Fargo Consumer Debit and ATM s Terms and Conditions effective 04/24/2017. Introduction page 1 Using Your page 2 Using Your Through a Mobile Device page 4 One-Time

Selected Terms & Conditions for Wells Fargo Consumer Debit and ATM s Terms and Conditions effective 04/24/2017. Introduction page 1 Using Your page 2 Using Your Through a Mobile Device page 4 One-Time

Purchasing and Travel Services

Purchasing and Travel Services Purchasing Card Procedures January 2015 1. PURPOSE To give direction to the administration of purchasing cards and the operational support necessary for use of purchasing

Purchasing and Travel Services Purchasing Card Procedures January 2015 1. PURPOSE To give direction to the administration of purchasing cards and the operational support necessary for use of purchasing

COUNTY OF IMPERIAL CASH CONTROL AND ACCOUNTING STANDARD PRACTICE MANUAL F O R E W A R D

CASH CONTROL AND ACCOUNTING STANDARD PRACTICE MANUAL F O R E W A R D This manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The

CASH CONTROL AND ACCOUNTING STANDARD PRACTICE MANUAL F O R E W A R D This manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The

Unemployment Insurance U.S. Bank ReliaCard. Frequently Asked Questions. What is the ReliaCard and How Does It Work?

Unemployment Insurance U.S. Bank ReliaCard What is the ReliaCard and How Does It Work? What is the ReliaCard? The ReliaCard is a reloadable, prepaid card issued by U.S. Bank. The ReliaCard is an electronic

Unemployment Insurance U.S. Bank ReliaCard What is the ReliaCard and How Does It Work? What is the ReliaCard? The ReliaCard is a reloadable, prepaid card issued by U.S. Bank. The ReliaCard is an electronic

Who Should Know This Policy 1 Definitions 2 Contacts 2 Policy Specifics and Procedures 2 Forms 6 Related Documents 6 Revision History 7 FAQ 7

Cash Receipting Policy Type: Administrative Responsible Office: Treasury Services, Office of the Vice President for Finance and Budget Initial Policy Approved: Undated Current Revision Approved: 08/21/2017

Cash Receipting Policy Type: Administrative Responsible Office: Treasury Services, Office of the Vice President for Finance and Budget Initial Policy Approved: Undated Current Revision Approved: 08/21/2017

The Southern Bank Company. Electronic Fund Transfers Your Rights and Responsibilities

The Southern Bank Company Electronic Fund Transfers Your Rights and Responsibilities Federal Law requires that consumers who make use of the Banks electronic funds transfer services receive the disclosures

The Southern Bank Company Electronic Fund Transfers Your Rights and Responsibilities Federal Law requires that consumers who make use of the Banks electronic funds transfer services receive the disclosures

BANKING & FINANCE (145)

") Page 1 of 10 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2017 Multiple Choice: (30 @ 2 points each) (60 points) Financial Word Problems: (9 @ 2 points each) (18 points) Endorsements:

Page 1 of 10 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2017 Multiple Choice: (30 @ 2 points each) (60 points) Financial Word Problems: (9 @ 2 points each) (18 points) Endorsements:

Banking YourMoneyCounts

Banking YourMoneyCounts As one of the world s leading financial services companies, HSBC is proud to support our communities. Our long history of providing financial education continues today, through

Banking YourMoneyCounts As one of the world s leading financial services companies, HSBC is proud to support our communities. Our long history of providing financial education continues today, through

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Bill Pay User Terms and Agreements

Bill Pay User Terms and Agreements First Community Bank hereby publishes the following terms and conditions for User's use of bill payment services via telephone, personal computer or any other device

Bill Pay User Terms and Agreements First Community Bank hereby publishes the following terms and conditions for User's use of bill payment services via telephone, personal computer or any other device

Mastercard BusinessCard/ PurchasingCard. Conditions of Use

Mastercard BusinessCard/ PurchasingCard Conditions of Use These are your Mastercard BusinessCard/ PurchasingCard account holder and cardholder Conditions of Use. Please read these Conditions of Use and

Mastercard BusinessCard/ PurchasingCard Conditions of Use These are your Mastercard BusinessCard/ PurchasingCard account holder and cardholder Conditions of Use. Please read these Conditions of Use and