Fraud, Internal Control, and Cash

|

|

|

- Cecil Banks

- 5 years ago

- Views:

Transcription

1 7-1

2 Chapter 7 Fraud, Internal Control, and Cash Learning Objectives After studying this chapter, you should be able to: 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal control principles to cash receipts. 4. Explain the applications of internal control principles to cash disbursements. 5. Describe the operation of a petty cash fund. 6. Indicate the control features of a bank account. 7. Prepare a bank reconciliation. 8. Explain the reporting of cash. 7-2

3 Preview of Chapter Financial Accounting IFRS Second Edition Weygandt Kimmel Kieso

4 Fraud and Internal Control Fraud Dishonest act by an employee that results in personal benefit to the employee at a cost to the employer. Three factors that contribute to fraudulent activity. Illustration LO 1 Define fraud and internal control.

5 Fraud and Internal Control Internal Control Methods and measures adopted to: 1. Safeguard assets. 2. Enhance accuracy and reliability of accounting records. 3. Increase efficiency of operations. 4. Ensure compliance with laws and regulations. 7-5 LO 1 Define fraud and internal control.

6 Fraud and Internal Control Internal Control Five Primary Components: 1. Control environment. 2. Risk assessment. 3. Control activities. 4. Information and communication. 5. Monitoring. 7-6 LO 1 Define fraud and internal control.

7 7-7

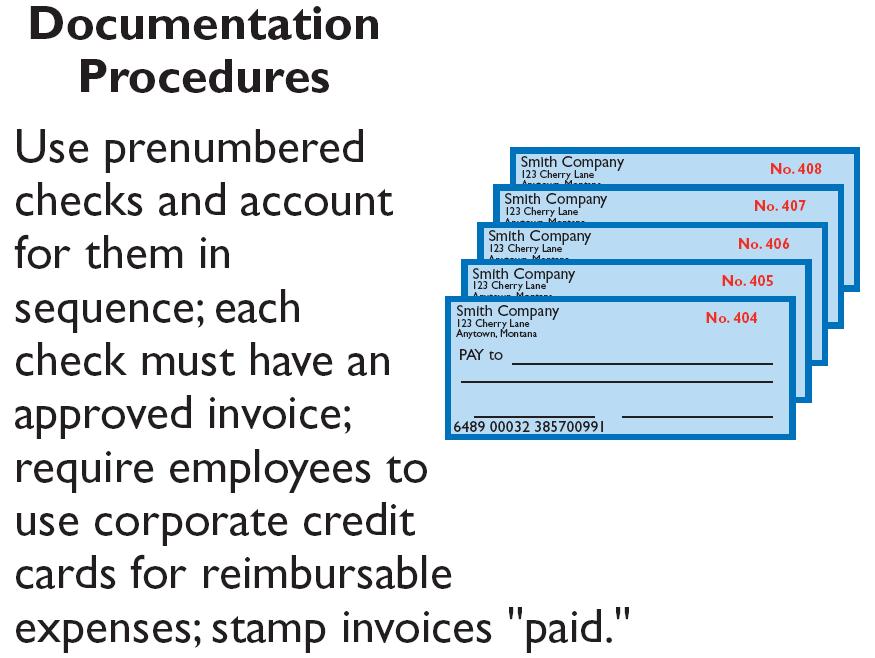

8 Fraud and Internal Control Principles of Internal Control Activities Establishment of Responsibility Control is most effective when only one person is responsible for a given task. Segregation of Duties Related duties should be assigned to different individuals. Documentation Procedures Companies should use prenumbered documents and all documents should be accounted for. 7-8 LO 2 Identify the principles of internal control activities.

9 Fraud and Internal Control Principles of Internal Control Activities Illustration 7-2 Physical Controls 7-9 LO 2 Identify the principles of internal control activities.

10 Fraud and Internal Control Principles of Internal Control Activities Independent Internal Verification 1. Records periodically verified by an employee who is independent. Illustration Discrepancies reported to management LO 2 Identify the principles of internal control activities.

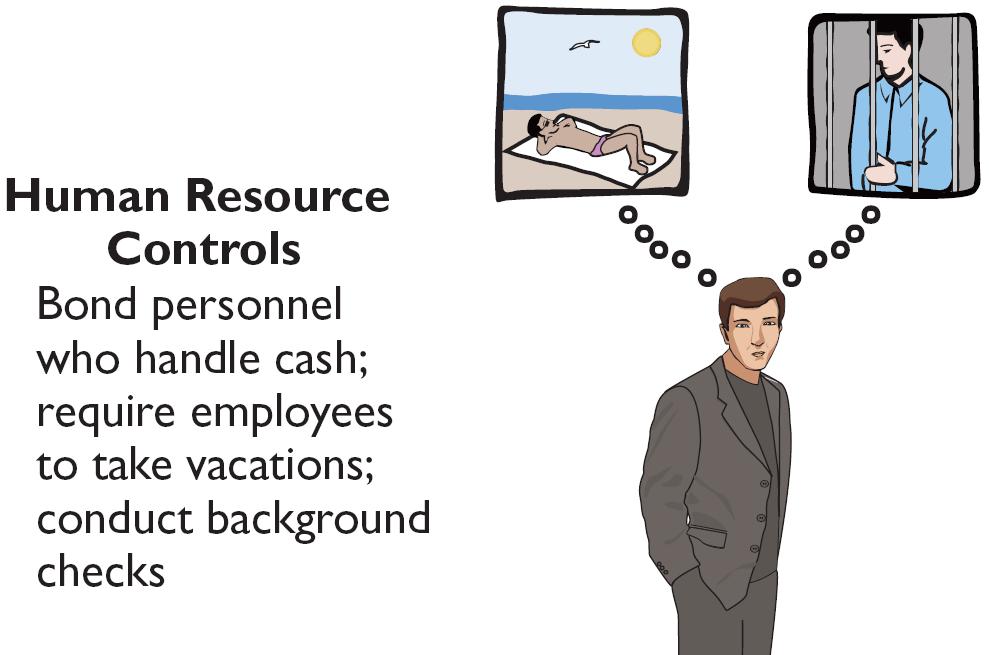

11 Fraud and Internal Control Principles of Internal Control Activities Human Resource Controls 1. Bond employees. 2. Rotate employees duties and require vacations. 3. Conduct background checks LO 2 Identify the principles of internal control activities.

12 Total take: $11 million The Missing Control ANATOMY OF A FRAUD Maureen Frugali was a training supervisor for claims processing at Colossal Healthcare. As a standard part of the claims processing training program, Maureen created fictitious claims for use by trainees. These fictitious claims were then sent to the accounts payable department. After the training claims had been processed, she was to notify Accounts Payable of all fictitious claims, so that they would not be paid. However, she did not inform Accounts Payable about every fictitious claim. She created some fictitious claims for entities that she controlled (that is, she would receive the payment), and she let Accounts Payable pay her. Establishment of responsibility. The healthcare company did not adequately restrict the responsibility for authoring and approving claims transactions. The training supervisor should not have been authorized to create claims in the company s live system. 7-12

13 Total take: $475,000 The Missing Control ANATOMY OF A FRAUD Lawrence Fairbanks, the assistant vice-chancellor of communications at Aesop University, was allowed to make purchases of under $2,500 for his department without external approval. Unfortunately, he also sometimes bought items for himself, such as expensive antiques and other collectibles. How did he do it? He replaced the vendor invoices he received with fake vendor invoices that he created. The fake invoices had descriptions that were more consistent with the communications department s purchases. He submitted these fake invoices to the accounting department as the basis for their journal entries and to the accounts payable department as the basis for payment. Segregation of duties. The university had not properly segregated related purchasing activities. Lawrence was ordering items, receiving the items, and receiving the invoice. By receiving the invoice, he had control over the documents that were used to account for the purchase and thus was able to substitute a fake invoice. 7-13

14 Total take: $570,000 The Missing Control ANATOMY OF A FRAUD Angela Bauer was an accounts payable clerk for Aggasiz Construction Company. She prepared and issued checks to vendors and reconciled bank statements. She perpetrated a fraud in this way: She wrote checks for costs that the company had not actually incurred (e.g., fake taxes). A supervisor then approved and signed the checks. Before issuing the check, though, she would white-out the payee line on the check and change it to personal accounts that she controlled. She was able to conceal the theft because she also reconciled the bank account. That is, nobody else ever saw that the checks had been altered. Segregation of duties. Aggasiz Construction Company did not properly segregate record-keeping from physical custody. Angela had physical custody of the checks, which essentially was control of the cash. She also had recordkeeping responsibility because she prepared the bank reconciliation. 7-14

15 ANATOMY OF A FRAUD To support their reimbursement requests for travel costs incurred, employees at Mod Fashions Corporation s design center were required to submit receipts. The receipts could include the detailed bill provided for a meal, or the credit card receipt provided when the credit card payment is made, or a copy of the employee s monthly credit card bill that listed the item. A number of the designers who frequently traveled together came up with a fraud scheme: They submitted claims for the same expenses. For example, if they had a meal together that cost $200, one person submitted the detailed meal bill, another submitted the credit card receipt, and a third submitted a monthly credit card bill showing the meal as a line item. Thus, all three received a $200 reimbursement Total take: $75,000 The Missing Control Documentation procedures. Mod Fashions should require the original, detailed receipt. It should not accept photocopies, and it should not accept credit card statements. In addition, documentation procedures could be further improved by requiring the use of a corporate credit card (rather than a personal credit card) for all business expenses.

16 Total take: $240,000 The Missing Control ANATOMY OF A FRAUD At Centerstone Health, a large insurance company, the mailroom each day received insurance applications from prospective customers. Mailroom employees scanned the applications into electronic documents before the applications were processed. Once the applications are scanned they can be accessed online by authorized employees. Insurance agents at Centerstone Health earn commissions based upon successful applications. The sales agent s name is listed on the application. However, roughly 15% of the applications are from customers who did not work with a sales agent. Two friends Alex, an employee in record keeping, and Parviz, a sales agent thought up a way to perpetrate a fraud. Alex identified scanned applications that did not list a sales agent. After business hours, he entered the mailroom and found the hardcopy applications that did not show a sales agent. He wrote in Parviz s name as the sales agent and then rescanned the application for processing. Parviz received the commission, which the friends then split. 7-16

17 Total take: $240,000 The Missing Control Physical controls. Centerstone Health lacked two basic physical controls that could have prevented this fraud. First, the mailroom should have been locked during nonbusiness hours, and access during business hours should have been tightly controlled. Second, the scanned applications supposedly could be accessed only by authorized employees using their passwords. However, the password for each employee was the same as the employee s user ID. Since employee user-id numbers were available to all other employees, all employees knew all other employees passwords. Unauthorized employees could access the scanned applications. Thus, Alex could enter the system using another employee s password and access the scanned applications. 7-17

18 7-18 Total take: $275,000 The Missing Control ANATOMY OF A FRAUD Bobbi Jean Donnelly, the office manager for Mod Fashions Corporations design center, was responsible for preparing the design center budget and reviewing expense reports submitted by design center employees. Her desire to upgrade her wardrobe got the better of her, and she enacted a fraud that involved filing expense-reimbursement requests for her own personal clothing purchases. She was able to conceal the fraud because she was responsible for reviewing all expense reports, including her own. In addition, she sometimes was given ultimate responsibility for signing off on the expense reports when her boss was too busy. Also, because she controlled the budget, when she submitted her expenses, she coded them to budget items that she knew were running under budget, so that they would not catch anyone s attention. Independent internal verification. Bobbi Jean s boss should have verified her expense reports. When asked what he thought her expenses were, the boss said about $10,000. At $115,000 per year, her actual expenses were more than ten times what would have been expected. However, because he was too busy to verify her expense reports or to review the budget, he never noticed.

19 7-19 Total take: $95,000 The Missing Control ANATOMY OF A FRAUD Ellen Lowry was the desk manager and Josephine Rodriquez was the head of housekeeping at the Excelsior Inn, a luxury hotel. The two best friends were so dedicated to their jobs that they never took vacations, and they frequently filled in for other employees. In fact, Ms. Rodriquez, whose job as head of housekeeping did not include cleaning rooms, often cleaned rooms herself, just to help the staff keep up. Ellen, the desk manager, provided significant discounts to guests who paid with cash. She kept the cash and did not register the guest in the hotel s computerized system. Instead, she took the room out of circulation due to routine maintenance. Because the room did not show up as being used, it did not receive a normal housekeeping assignment. Instead, Josephine, the head of housekeeping, cleaned the rooms during the guests stay. Human resource controls. Ellen, the desk manager, had been fired by a previous employer. If the Excelsior Inn had conducted a background check, it would not have hired her. The fraud was detected when Ellen missed work due to illness. A system of mandatory vacations and rotating days off would have increased the chances of detecting the fraud before it became so large.

20 7-20

21 Fraud and Internal Control Limitations of Internal Control Costs should not exceed benefit. Human element. Size of the business LO 2 Identify the principles of internal control activities.

22 7-22

23 Cash Controls Cash Receipts Controls Illustration LO 3

24 Cash Controls Cash Receipts Controls Illustration LO 3

25 Cash Controls Cash Receipts Controls Over-the-Counter Receipts Important internal control principle segregation of recordkeeping from physical custody. Illustration LO 3

26 Cash Controls Cash Receipts Controls Mail Receipts Mail receipts should be opened by two people, a list prepared, and each check endorsed. Each mail clerk signs the list to establish responsibility for the data. Original copy of the list, along with the checks, is sent to the cashier s department. Copy of the list is sent to the accounting department for recording. Clerks also keep a copy LO 3 Explain the applications of internal control principles to cash receipts.

27 Cash Controls Cash Disbursements Controls Generally, internal control over cash disbursements is more effective when companies pay by check, rather than by cash. Applications: Voucher system Petty cash fund 7-27 LO 4 Explain the applications of internal control principles to cash disbursements.

28 Cash Controls Cash Disbursements Controls Illustration LO 4

29 Cash Controls Cash Disbursements Controls Illustration LO 4

30 Cash Controls Cash Disbursements Controls Voucher System Network of approvals, by authorized individuals, to ensure all disbursements by check are proper. A voucher is an authorization form prepared for each expenditure LO 4 Explain the applications of internal control principles to cash disbursements.

31 Cash Controls Cash Disbursements Controls Petty Cash Fund - Used to pay small amounts. Involves: 1. establishing the fund, 2. making payments from the fund, and 3. replenishing the fund LO 5 Describe the operation of a petty cash fund.

32 Cash Controls Illustration: If Zhu Company decides to establish a NT$3,000 fund on March 1, the journal entry is: Mar. 1 Petty cash 3,000 Cash 3, LO 5 Describe the operation of a petty cash fund.

33 Cash Controls Illustration: Assume that on March 15 Zhu s petty cash custodian requests a check for NT$2,610. The fund contains NT$390 cash and petty cash receipts for postage NT$1,320, freight-out NT$1,140, and miscellaneous expenses NT$150. The general journal entry to record the check is: Mar. 15 Postage expense 1,320 Freight-out expense 1,140 Miscellaneous expense 150 Cash 2, LO 5 Describe the operation of a petty cash fund.

34 Cash Controls Illustration: Occasionally, the company may need to recognize a cash shortage or overage. Assume that Zhu s petty cash custodian has only NT$360 in cash in the fund plus the receipts as listed. The request for reimbursement would, therefore, be for NT$2,640, and Zhu would make the following entry: Mar. 15 Postage expense 1,320 Freight-out expense 1,140 Miscellaneous expense 150 Cash over and short 30 Cash 2, LO 5 Describe the operation of a petty cash fund.

35 7-35

36 Control Features: Use of a Bank Contributes to good internal control over cash. Minimizes the amount of currency on hand. Creates a double record of bank transactions. Bank reconciliation LO 6 Indicate the control features of a bank account.

37 Control Features: Use of a Bank Making Bank Deposits Authorized employee should make deposit. Illustration 7-8 Bank Code Numbers Front Side Reverse Side 7-37 LO 6 Indicate the control features of a bank account.

38 Control Features: Use of a Bank Writing Checks Written order signed by depositor directing bank to pay a specified sum of money to a designated recipient. Illustration 7-9 Maker Payee Payer 7-38 LO 6 Indicate the control features of a bank account.

. Credit Memorandum Collect notes receivable. Interest earned.")

39 Control Features: Use of a Bank Bank Statements Illustration 7-10 Debit Memorandum Bank service charge. NSF (not sufficient funds). Credit Memorandum Collect notes receivable. Interest earned. 7-39

40 Control Features: Use of a Bank Reconciling the Bank Account Reconcile balance per books and balance per bank to their adjusted (corrected) cash balances. Reconciling Items: 1. Deposits in transit. 2. Outstanding checks. Time Lags 3. Bank memoranda. 4. Errors LO 7 Prepare a bank reconciliation.

41 Control Features: Use of a Bank Reconciliation Procedures Illustration Deposit in Transit - Outstanding Checks +/- Bank Errors CORRECT BALANCE + Notes collected by bank - NSF (bounced) checks - Check printing or other service charges +/- Book Errors CORRECT BALANCE 7-41 LO 7 Prepare a bank reconciliation.

42 Control Features: Use of a Bank The bank statement for Laird Company, in Illustration 7-10, shows a balance per bank of 15, on April 30, On this date the balance of cash per books is 11, Using the four reconciliation steps, Laird determines the following reconciling items. Step 1. Deposits in transit: April 30 deposit (received by bank on May 1). 2, Step 2. Outstanding checks: No. 453, 3,000.00; no. 457, 1,401.30; no. 460, 1, , Step 3. Errors: Laird wrote check no. 443 for 1, and the bank correctly paid that amount. However, Laird recorded the check as 1, Step 4. Bank memoranda: a. Debit NSF check from J. R. Baron for b. Debit Charge for printing company checks c. Credit Collection of note receivable for 1,000 plus interest earned 50, less bank collection fee , LO 7 Prepare a bank reconciliation.

43 Control Features: Use of a Bank Illustration: Prepare a bank reconciliation at April 30. Cash balance per bank statement 15, Deposit in transit 2, Outstanding checks (5,904.00) Adjusted cash balance per bank 12, Cash balance per books 11, Error in check No NSF check (425.60) Bank service charge (30.00) Collection of notes receivable 1, Adjusted cash balance per books 12, LO 7 Prepare a bank reconciliation.

44 Control Features: Use of a Bank Entries From Bank Reconciliation Collection of Note Receivable: Assuming interest of 50 has not been accrued and collection fee is charged to Miscellaneous Expense, the entry is: Apr. 30 Cash 1, Miscellaneous expense Notes receivable 1, Interest revenue LO 7 Prepare a bank reconciliation.

45 Control Features: Use of a Bank Book Error: The cash disbursements journal shows that check no. 443 was a payment on account to Andrea Company, a supplier. The correcting entry is: Apr. 30 Cash Accounts payable NSF Check: As indicated earlier, an NSF check becomes an account receivable to the depositor. The entry is: Apr. 30 Accounts receivable Cash LO 7 Prepare a bank reconciliation.

46 Control Features: Use of a Bank Bank Service Charges: Depositors debit check printing charges (DM) and other bank service charges (SC) to Miscellaneous Expense. The entry is: Apr. 30 Miscellaneous expense Cash Illustration LO 7 Prepare a bank reconciliation.

47 Control Features: Use of a Bank Electronic Funds Transfer (EFT) System Disbursement systems that uses wire, telephone, or computers to transfer cash balances between locations. EFT transfers normally result in better internal control since no cash or checks are handled by company employees LO 7 Prepare a bank reconciliation.

48 7-48

49 Sally Kist owns Linen Kist Fabrics. Sally asks you to explain how she should treat the following reconciling items when reconciling the company s bank account: (1) a debit memorandum for an NSF check, (2) a credit memorandum for a note collected by the bank, (3) outstanding checks, and (4) a deposit in transit. Solution: Sally should treat the reconciling items as follows. (1) NSF check: Deduct from balance per books. (2) Collection of note: Add to balance per books. (3) Outstanding checks: Deduct from balance per bank. (4) Deposit in transit: Add to balance per bank LO 7

50 Reporting Cash Cash Equivalents Cash equivalents are short-term, highly liquid investments that are both: 1. Readily convertible to cash, and 2. So near their maturity that their market value is relatively insensitive to changes in interest rates. Restricted Cash Should be reported separately on the balance sheet as restricted cash LO 8 Explain the reporting of cash.

51 Reporting Cash Illustration LO 8 Explain the reporting of cash.

52 Another Perspective Key Points The fraud triangle discussed in this chapter is applicable to all international companies. Some of the major frauds on a U.S. basis are Enron, WorldCom, and more recently the Bernie Madoff Ponzi scheme. Rising economic crime poses a growing threat to companies, with nearly one-third of all organizations worldwide being victims of fraud in a recent 12-month period. The survey data shows that the incidence of economic crime varies by territory; some countries, mainly those in emerging markets, experienced much higher levels of fraud than the average, as much as 71% in one country; by industry sector, some (notably insurance, financial services, and communications) reporting higher levels of fraud than others; and by size and type of organization. But no organization is immune (PricewaterhouseCoopers Global Economic Crime Survey, 2009). 7-52

53 Another Perspective Key Points 7-53 Accounting scandals both in the United States and internationally have re-ignited the debate over the relative merits of GAAP, which takes a rules-based approach to accounting, versus IFRS, which takes a principles-based approach. The FASB announced that it intends to introduce more principles-based standards. After numerous corporate scandals, the U.S. Congress passed the Sarbanes-Oxley Act (SOX). Under SOX, all publicly traded U.S. corporations are required to maintain an adequate system of internal control. As a result of SOX, corporate executives and boards of directors must ensure that internal controls are reliable and effective. In addition, independent outside auditors must attest to the adequacy of the internal control system.

54 Another Perspective Key Points SOX created the Public Company Oversight Board (PCAOB) to establish auditing standards and regulate auditor activity. Internal controls are a system of checks and balances designed to prevent and detect fraud and errors. While most companies have these systems in place, many have never completely documented them, nor had an independent auditor attest to their effectiveness. Both of these actions are required under SOX. Companies find that internal control review is a costly process but badly needed. One study estimates the cost of SOX compliance for U.S. companies at over $35 billion, with audit fees doubling in the first year of compliance. At the same time, examination of internal controls indicates lingering problems in the way companies operate. 7-54

55 Another Perspective Key Points As indicated earlier, SOX internal control standards apply only to companies listed on U.S. exchanges. There is continuing debate over whether foreign issuers should have to comply with this extra layer of regulation. The accounting and internal control procedures related to cash are essentially the same under both GAAP and this textbook. In addition, the definition used for cash equivalents is the same. Most companies report cash and cash equivalents together under GAAP, as shown in this textbook. In addition, GAAP follows the same accounting policies related to the reporting of restricted cash. 7-55

56 Another Perspective Key Points GAAP and IFRS define cash and cash equivalents similarly as follows. Cash is comprised of cash on hand and demand deposits. Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. 7-56

57 Another Perspective Looking to the Future Ethics has become a very important aspect of reporting. Different cultures have different perspectives on bribery and other questionable activities, and consequently penalties for engaging in such activities vary considerably across countries. High-quality international accounting requires both highquality accounting standards and high-quality auditing. Similar to the convergence of GAAP and IFRS, there is movement to improve international auditing standards. The International Auditing and Assurance Standards Board (IAASB) functions as an independent standard-setting body. It works to establish high-quality auditing and assurance and quality-control standards throughout the world. Whether the IAASB adopts internal control provisions similar to those in SOX remains to be seen. Under proposed new standards for financial statements, companies would not be allowed to combine cash equivalents with cash. 7-57

58 Copyright Copyright 2013 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein. 7-58

FRAUD, INTERNAL CONTROL, AND CASH

c07fraud,internalcontrol,andcash.qxd 8/16/10 2:19 PM Page 334 chapter 7 FRAUD, INTERNAL CONTROL, AND CASH the navigator Scan Study Objectives Read Feature Story Scan Preview Read Text and Answer Do it!

c07fraud,internalcontrol,andcash.qxd 8/16/10 2:19 PM Page 334 chapter 7 FRAUD, INTERNAL CONTROL, AND CASH the navigator Scan Study Objectives Read Feature Story Scan Preview Read Text and Answer Do it!

Chapter 06 - Cash and Internal Controls. Chapter Outline

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed.

ACCT 101 Chapter 6 Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed. Three Objectives of Internal Control Assets are safeguarded

ACCT 101 Chapter 6 Internal Control protect the assets and ensure that business information is accurate and ensure that regulations are being followed. Three Objectives of Internal Control Assets are safeguarded

Fundamental Accounting Principles, Volume 1, Fifteenth Canadian Edition

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Accounting for Receivables

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

Exercises: Set B. 28 B-Exercises

28 B-Exercises Identify the principles of internal control. (LO 2), C weaknesses over cash receipts and suggest (LO 2, 3) weaknesses for cash disbursements and suggest (LO 2, 4) (LO 5) Exercises: Set B

28 B-Exercises Identify the principles of internal control. (LO 2), C weaknesses over cash receipts and suggest (LO 2, 3) weaknesses for cash disbursements and suggest (LO 2, 4) (LO 5) Exercises: Set B

1-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

CHAPTER 8 INTERNAL CONTROL AND CASH SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY

CHAPTER 8 INTERNAL CONTROL AND CASH SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 C 17. 3 C 25.

CHAPTER 8 INTERNAL CONTROL AND CASH SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 C 17. 3 C 25.

Accounting in Action. Chapter 1. Learning Objectives. After studying this chapter, you should be able to:

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

SOLUTIONS TO BRIEF EXERCISES

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 8-1 1. Financial Pressure 2. Rationalization 3. Financial Pressure 4. Opportunity BRIEF EXERCISE 8-2 1. True. 2. True. 3. False. The Sarbanes-Oxley Act requires

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 8-1 1. Financial Pressure 2. Rationalization 3. Financial Pressure 4. Opportunity BRIEF EXERCISE 8-2 1. True. 2. True. 3. False. The Sarbanes-Oxley Act requires

Liabilities. Chapter 10. Learning Objectives. After studying this chapter, you should be able to:

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

The Recording Process

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Chapter 7 Student Version

Sarbanes-Oxley, Internal Control, and Cash Chapter 7 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor

Sarbanes-Oxley, Internal Control, and Cash Chapter 7 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor

Sarbanes-Oxley, Internal Control, and Cash

C H A P T E R 7 Sarbanes-Oxley, Internal Control, and Cash Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Sarbanes-Oxley Act (slide 1 of 2) Sarbanes-Oxley emphasizes

C H A P T E R 7 Sarbanes-Oxley, Internal Control, and Cash Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Sarbanes-Oxley Act (slide 1 of 2) Sarbanes-Oxley emphasizes

Cash Operations Training Mary H. Loomis, CPA, Comptroller

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

BANKING PROCEDURE AND CONTROL OF CASH

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

The Recording Process

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Chapter 6. Accounting For Cash and Internal Controls

Chapter 6 Accounting For Cash and Internal Controls C 2 Cash, Cash Equivalents, and Liquidity Cash Currency, coins and amounts on deposit in bank accounts, checking accounts, and many savings accounts.

Chapter 6 Accounting For Cash and Internal Controls C 2 Cash, Cash Equivalents, and Liquidity Cash Currency, coins and amounts on deposit in bank accounts, checking accounts, and many savings accounts.

Chapter 7 Question Review 1

Chapter 7 Question Review 1 Chapter 7 Questions Multiple Choice 1. The entry to replenish a petty cash fund includes a credit to a. Petty Cash. b. Cash. c. Freight-In. d. Postage Expense. 2. A $300 petty

Chapter 7 Question Review 1 Chapter 7 Questions Multiple Choice 1. The entry to replenish a petty cash fund includes a credit to a. Petty Cash. b. Cash. c. Freight-In. d. Postage Expense. 2. A $300 petty

CHAPTER1. Accounting in Action. PreviewofCHAPTER1. What is Accounting?

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

FINANCE COMMITTEE PROCEDURES. Committee Responsibilities. Audit Process

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

Ch.6 Internal Control and Accounting for Cash

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Cash and Internal Control C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

COUNTY OF HENRICO, VIRGINIA PETTY CASH FUND POLICIES AND PROCEDURES

COUNTY OF HENRICO, VIRGINIA PETTY CASH FUND POLICIES AND PROCEDURES Approved by the County Manager And Effective August 1, 2007 (Updated July 1, 2017) PETTY CASH FUNDS Purpose: The availability of petty

COUNTY OF HENRICO, VIRGINIA PETTY CASH FUND POLICIES AND PROCEDURES Approved by the County Manager And Effective August 1, 2007 (Updated July 1, 2017) PETTY CASH FUNDS Purpose: The availability of petty

ACCOUNTS PAYABLE POLICIES AND PROCEDURES...

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

Chapter II: Internal Controls II-10

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

EXERCISES. The complete AICPA summary of Section 404 of Sarbanes-Oxley is as follows: Section 404: Management Assessment of Internal Controls.

EXERCISES Ex. 7 1 Section 404 requires management s internal control report to: (1) state the responsibility of management for establishing and maintaining an adequate internal control structure and procedures

EXERCISES Ex. 7 1 Section 404 requires management s internal control report to: (1) state the responsibility of management for establishing and maintaining an adequate internal control structure and procedures

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

Auditing and Assurance Services, 15e

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

CHAPTER 7. Internal Control and Cash. Chapter Overview

CHAPTER 7 Internal Control and Cash Chapter Overview Chapter 7 discusses the purposes and characteristics of an effective system of internal control. The text describes four objectives that a company hopes

CHAPTER 7 Internal Control and Cash Chapter Overview Chapter 7 discusses the purposes and characteristics of an effective system of internal control. The text describes four objectives that a company hopes

Accounting for Receivables

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

Accounting Building Business Skills. Learning Objectives. Learning Objectives. Paul D. Kimmel. Chapter Seven: Internal Control, Cash and Receivables

Accounting Building Business Skills Paul D. Kimmel Chapter Seven: Internal Control, Cash and Receivables PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003

Accounting Building Business Skills Paul D. Kimmel Chapter Seven: Internal Control, Cash and Receivables PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003

College Accounting. Heintz & Parry. 20 th Edition

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

FAYETTEVILLE POLICIES AND PROCEDURES 306.0

FAYETTEVILLE POLICIES AND PROCEDURES 306.0 Cash Handling Procedures The handling of University monies requires that certain basic procedures be followed precisely at all times. Procedures for the handling

FAYETTEVILLE POLICIES AND PROCEDURES 306.0 Cash Handling Procedures The handling of University monies requires that certain basic procedures be followed precisely at all times. Procedures for the handling

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 7-1 7-2 PREVIEW OF CHAPTER 7 7-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 7-1 7-2 PREVIEW OF CHAPTER 7 7-3

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

ASSIGNMENT CLASSIFICATION TABLE

CHAPTER 8 Internal Control and Cash ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Describe internal control. 1 1 2. Explain the principles

CHAPTER 8 Internal Control and Cash ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Describe internal control. 1 1 2. Explain the principles

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

Peralta Community College District AP 6300

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

Business Services Cash Handling: Department Manual

Business Services Cash Handling: Department Manual Deborah Michaels Associate Director, Business Services Cash Management Tina Cripe Administrative Program Assistant, Banking Specialist http://www.sou.edu/bus_serv/bursar/index.html

Business Services Cash Handling: Department Manual Deborah Michaels Associate Director, Business Services Cash Management Tina Cripe Administrative Program Assistant, Banking Specialist http://www.sou.edu/bus_serv/bursar/index.html

Fill-in-the-Blank Equations. Exercises

Chapter 8 Sarbanes-Oxley, Internal Control, and Cash Study Guide Solutions 1. Liability 2. Increase; debit 3. Monthly cash expenses 4. Cash as of year-end Fill-in-the-Blank Equations Exercises 1. In Poletti

Chapter 8 Sarbanes-Oxley, Internal Control, and Cash Study Guide Solutions 1. Liability 2. Increase; debit 3. Monthly cash expenses 4. Cash as of year-end Fill-in-the-Blank Equations Exercises 1. In Poletti

CSU. ICSUAM Section 6000 Financing, Treasury, and Risk Management

CSU ICSUAM Section 6000 Financing, Treasury, and Risk Management Table of Contents 6320.00 Petty Cash Funds and Change Funds... 3 6330.00 Incoming Cash and Checks... 5 **DRAFT** 6320.00 Petty Cash Funds

CSU ICSUAM Section 6000 Financing, Treasury, and Risk Management Table of Contents 6320.00 Petty Cash Funds and Change Funds... 3 6330.00 Incoming Cash and Checks... 5 **DRAFT** 6320.00 Petty Cash Funds

Advances (Including Petty Cash and Accounts Receivable)

") CORNELL UNIVERSITY POLICY LIBRARY Advances (Including Petty Cash and Accounts Receivable) Chapter: 21, Advances Revised: POLICY STATEMENT Cornell University provides advances of cash or other resources

CORNELL UNIVERSITY POLICY LIBRARY Advances (Including Petty Cash and Accounts Receivable) Chapter: 21, Advances Revised: POLICY STATEMENT Cornell University provides advances of cash or other resources

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES

GUIDELINES AND PROCEDURES") FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check.

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM. SECTION: Fiscal Affairs NUMBER: 03.A.07

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM SECTION: Fiscal Affairs NUMBER: 03.A.07 AREA: General SUBJECT: Petty Cash Funds 1. PURPOSE This administrative memorandum establishes custodial, accounting

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM SECTION: Fiscal Affairs NUMBER: 03.A.07 AREA: General SUBJECT: Petty Cash Funds 1. PURPOSE This administrative memorandum establishes custodial, accounting

FISCAL MANAGEMENT (Replaces current SBCCD AP 6300)

") 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 AP 6300 AP 6300 San Bernardino Community College District Administrative Procedure

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 AP 6300 AP 6300 San Bernardino Community College District Administrative Procedure

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

Accounting Policies and Procedures Manual

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

CASH ACCOUNTING MANUAL

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

CHAPTER 5 SARBANES-OXLEY, INTERNAL CONTROL, AND CASH

CHAPTER 5 SARBANES-OXLEY, INTERNAL CONTROL, AND CASH CLASS DISCUSSION QUESTIONS 1. a. Congress passed the Sarbanes-Oxley Act of 2002 because of the Enron, WorldCom, Tyco, Adelphia, and other financial

CHAPTER 5 SARBANES-OXLEY, INTERNAL CONTROL, AND CASH CLASS DISCUSSION QUESTIONS 1. a. Congress passed the Sarbanes-Oxley Act of 2002 because of the Enron, WorldCom, Tyco, Adelphia, and other financial

Reviewed by: Chuck Roper (Treasury) Sue Potter (A/P) Bill Santiago (Purchasing)

Sue Potter (A/P) Bill Santiago (Purchasing)") Topic: s Date: 03/30/15 Prepared by: Kathy Sawtells Reviewed by: Chuck Roper (Treasury) Sue Potter (A/P) Bill Santiago (Purchasing) Title: Controller Purpose: There are times when small or emergency purchases

Topic: s Date: 03/30/15 Prepared by: Kathy Sawtells Reviewed by: Chuck Roper (Treasury) Sue Potter (A/P) Bill Santiago (Purchasing) Title: Controller Purpose: There are times when small or emergency purchases

Chapter 11. Corporations: Organization, Share Transactions, Dividends, and Retained Earnings. Learning Objectives

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

Fairport Public Library

Fairport Public Library Policies and Procedures Manual Cash Handling Table of Contents: I. Policy Statement II. Procedures III. Record Keeping IV. Appendix I. Policy Statement: This policy defines the

Fairport Public Library Policies and Procedures Manual Cash Handling Table of Contents: I. Policy Statement II. Procedures III. Record Keeping IV. Appendix I. Policy Statement: This policy defines the

Accounting I Lesson Plan

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Cash Control Systems Unit: Chapter 7 I. Objective(s): By the end of today s lesson, the student will be able to: define accounting terms related

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Cash Control Systems Unit: Chapter 7 I. Objective(s): By the end of today s lesson, the student will be able to: define accounting terms related

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

Chapter 10. Cash and Financial Investments. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

Accounting consists of three basic activities it

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

CITY OF MONT BELVIEU CITY COUNCIL POLICY

Page 1 of 14 4.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to accounts for the handling of Mont Belvieu s municipal cash and to maintain public

Page 1 of 14 4.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to accounts for the handling of Mont Belvieu s municipal cash and to maintain public

GATEWAY WATER MANAGEMENT AUTHORITY

GATEWAY WATER MANAGEMENT AUTHORITY ACCOUNTING POLICIES AND PROCEDURES MANUAL September 10, 2015 Page 1 of 12 I. Introduction The purpose of this manual is to describe all accounting policies and procedures

GATEWAY WATER MANAGEMENT AUTHORITY ACCOUNTING POLICIES AND PROCEDURES MANUAL September 10, 2015 Page 1 of 12 I. Introduction The purpose of this manual is to describe all accounting policies and procedures

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Assets Define Assets? Assets Financial Reporting Standard (FRS) defines assets as resources controlled by an entity

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Assets Define Assets? Assets Financial Reporting Standard (FRS) defines assets as resources controlled by an entity

Safeguarding the Financial Assets of Your Church. Indiana Conference of the United Methodist Church

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

AIPHS Financial Procedures

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

The Episcopal Diocese of Kansas

The Episcopal Diocese of Kansas Internal control and audit standards for parish funds and assets Adopted by the Council of Trustees May 15, 2007; revised September 18, 2007 Purpose: From the Manual of

The Episcopal Diocese of Kansas Internal control and audit standards for parish funds and assets Adopted by the Council of Trustees May 15, 2007; revised September 18, 2007 Purpose: From the Manual of

1. Cash includes coin, currency, checks, money orders, and credit card transactions.

1.0 Purpose BEREA COLLEGE Cash Handling Policy Document Document No. No. FIN032 FIN006 Revision Effective Date Date 3/2018 7/2008 Review Revision Date Date 3/2018 Next Pages Review Date 3/2019 1-3 Pages

1.0 Purpose BEREA COLLEGE Cash Handling Policy Document Document No. No. FIN032 FIN006 Revision Effective Date Date 3/2018 7/2008 Review Revision Date Date 3/2018 Next Pages Review Date 3/2019 1-3 Pages

IMPREST ACCOUNTS. Policy i

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

UH/Student Business Services Policies and Procedures

UH/Student Business Services Policies and Procedures CASH HANDLING Student Business Services (SBS) is the primary University of Houston department responsible for revenue collection of approved tuition,

UH/Student Business Services Policies and Procedures CASH HANDLING Student Business Services (SBS) is the primary University of Houston department responsible for revenue collection of approved tuition,

Employee Benefit Plan Fraud Examples

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

City of Wasco Internal Control Policy

City of Wasco Internal Control Policy 1. Introduction: The City Council of the City of Wasco and City management have a duty to be good fiscal stewards of government assets. This roll of stewardship includes

City of Wasco Internal Control Policy 1. Introduction: The City Council of the City of Wasco and City management have a duty to be good fiscal stewards of government assets. This roll of stewardship includes

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL Title: Cash Handling Policy Number: 05.20.12 Issuing Authority: Office of Financial Affairs Responsible Officer: Chief Financial Officer and Treasurer Date

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL Title: Cash Handling Policy Number: 05.20.12 Issuing Authority: Office of Financial Affairs Responsible Officer: Chief Financial Officer and Treasurer Date

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

University of Colorado Denver

University of Colorado Denver Fiscal Policy Title: Source: Prepared by: Approved by: Cash Receipts and Deposits Finance Office Controller Associate Vice Chancellor for Finance and Administration Effective

University of Colorado Denver Fiscal Policy Title: Source: Prepared by: Approved by: Cash Receipts and Deposits Finance Office Controller Associate Vice Chancellor for Finance and Administration Effective

PRESBYTERY OF CINCINNATI ACCOUNTING POLICIES AND PROCEDURES MANUAL TABLE OF CONTENTS

TABLE OF CONTENTS 1.00 Introduction 3 2.00 Chart of Accounts.. Appendix A 3.00 Division of Duties 4 3.1 Presbytery.. 4 3.2 Treasurer 4 3.3 Business Administrator. 4 3.4 Bookkeeper.. 4 3.5 Administrative

TABLE OF CONTENTS 1.00 Introduction 3 2.00 Chart of Accounts.. Appendix A 3.00 Division of Duties 4 3.1 Presbytery.. 4 3.2 Treasurer 4 3.3 Business Administrator. 4 3.4 Bookkeeper.. 4 3.5 Administrative

Investments. 1. Discuss why corporations invest in debt and share securities.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Accounting and Administrative Manual Section 100: Accounting and Finance

No.: C-06 Page: 1 of 5 General: The adequacy of internal control over cash receipts depends primarily on the business manager's ability to segregate the responsibilities for the performance of certain

No.: C-06 Page: 1 of 5 General: The adequacy of internal control over cash receipts depends primarily on the business manager's ability to segregate the responsibilities for the performance of certain

TITLE II ADMINISTRATIVE REGULATIONS

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 18 CASH HANDLING POLICY 18.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to account for the handling

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 18 CASH HANDLING POLICY 18.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to account for the handling

Diocese of Madison. Policy for Parish Cash Management. A. Bank Accounts and Their Security

Diocese of Madison Policy for Parish Cash Management The handling of cash is a primary concern of financial control in any organization. Therefore, establishing good procedures and internal controls for

Diocese of Madison Policy for Parish Cash Management The handling of cash is a primary concern of financial control in any organization. Therefore, establishing good procedures and internal controls for

Cash Management Policy Knox County Housing Authority 216 W. Simmons St. Galesburg, IL (309)

") Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

Tulane Purchasing Card Policies and Procedures

Tulane Purchasing Card Policies and Procedures I. Purpose The Purchasing Card program was established to provide a more efficient and cost-effective method for purchasing and paying for small dollar transactions,

Tulane Purchasing Card Policies and Procedures I. Purpose The Purchasing Card program was established to provide a more efficient and cost-effective method for purchasing and paying for small dollar transactions,

PREVIEW OF CHAPTER 1-2

1-1 PREVIEW OF CHAPTER 1 1-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 1 Accounting Standards Financial Reporting and LEARNING OBJECTIVES After studying this chapter, you should

1-1 PREVIEW OF CHAPTER 1 1-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 1 Accounting Standards Financial Reporting and LEARNING OBJECTIVES After studying this chapter, you should

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY ORIGINALLY ADOPTED BY CITY COUNCIL: NOVEMBER 17, 2011 PREFACE The intent of the City of Kennedale s Internal Controls & Cash Handling Policy is

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY ORIGINALLY ADOPTED BY CITY COUNCIL: NOVEMBER 17, 2011 PREFACE The intent of the City of Kennedale s Internal Controls & Cash Handling Policy is

CASH HANDLING POLICIES

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

Conrad N. Hilton College of Hotel & Restaurant Management Cash Handling Procedures For Fiscal Year 2013

Conrad N. Hilton College of Hotel & Restaurant Management Cash Handling Procedures For Fiscal Year 2013 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving

Conrad N. Hilton College of Hotel & Restaurant Management Cash Handling Procedures For Fiscal Year 2013 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving

Citywide Cash Handling Procedures Performance Audit

Citywide Cash Handling Procedures Performance Audit March 2010 Office of the Auditor Audit Services Division City and County of Denver Dennis J. Gallagher Auditor The Auditor of the City and County of

Citywide Cash Handling Procedures Performance Audit March 2010 Office of the Auditor Audit Services Division City and County of Denver Dennis J. Gallagher Auditor The Auditor of the City and County of

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1 1. Procedure Title: Receipt and Deposit of Cash and Checks 2. Procedure Purpose and Effect: To outline procedures for proper safeguarding

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1 1. Procedure Title: Receipt and Deposit of Cash and Checks 2. Procedure Purpose and Effect: To outline procedures for proper safeguarding

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

THE REACH HEALTHCARE FOUNDATION Statement of Internal Controls

THE REACH HEALTHCARE FOUNDATION Statement of Internal Controls Accounting System The REACH Healthcare Foundation uses a fund-based accounting system, utilizing Quickbooks Nonprofit Premiere Edition software.

THE REACH HEALTHCARE FOUNDATION Statement of Internal Controls Accounting System The REACH Healthcare Foundation uses a fund-based accounting system, utilizing Quickbooks Nonprofit Premiere Edition software.

WILEY IFRS EDITION. Accounting for Receivables PREVIEW OF CHAPTER 8. Financial Accounting IFRS 3rd Edition Weygandt Kimmel Kieso CHAPTER

WILEY IFRS EDITION Prepared by Coby Harmon University of California, Santa Barbara 8-1 Westmont College PREVIEW OF CHAPTER 8 8-2 Financial Accounting IFRS 3rd Edition Weygandt Kimmel Kieso 8 CHAPTER Accounting

WILEY IFRS EDITION Prepared by Coby Harmon University of California, Santa Barbara 8-1 Westmont College PREVIEW OF CHAPTER 8 8-2 Financial Accounting IFRS 3rd Edition Weygandt Kimmel Kieso 8 CHAPTER Accounting

COUNTY OF SONOMA. CAL-Card USER MANUAL

COUNTY OF SONOMA CAL-Card USER MANUAL DEPARTMENT OF GENERAL SERVICES PURCHASING DIVISION May 2012 TABLE OF CONTENTS SECTION PAGE NO. 1. General Information 1 2. Definitions 3 3. Authorized, Restricted

COUNTY OF SONOMA CAL-Card USER MANUAL DEPARTMENT OF GENERAL SERVICES PURCHASING DIVISION May 2012 TABLE OF CONTENTS SECTION PAGE NO. 1. General Information 1 2. Definitions 3 3. Authorized, Restricted

The Importance of Sound Financial Policies and Procedures

The Importance of Sound Financial Policies and Procedures Presented by Michael Holton Holton Healthcare Consulting, Inc. Raleigh, NC mholton@holtonhealthcare.com www.holtonhealthcare.com 0 Understand the

The Importance of Sound Financial Policies and Procedures Presented by Michael Holton Holton Healthcare Consulting, Inc. Raleigh, NC mholton@holtonhealthcare.com www.holtonhealthcare.com 0 Understand the