Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

|

|

|

- Jesse Cobb

- 6 years ago

- Views:

Transcription

1 Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest

2 Contents Types of fraud, their modes of detection and mitigation Contract and Procurement Fraud Asset Misappropriation Financial Statement fraud

3 What is Fraud? Fraud is an intentional deception made for personal gain in order to obtain unauthorized benefits (money, property, etc.) A representation about a material fact, which is false Made intentionally, knowingly, or recklessly It is believed by the victim And acted upon by the victim To the victim s detriment

4 Why do People commit fraud The Fraud Triangle Opportunity Pressure Rationalization

5 Why do People commit fraud

6 Classifications of Fraud Asset Misappropriation- a scheme that involves the theft or misuse of an organization s assets Procurement Fraud-Unlawful manipulation of the procurement process to acquire goods or services to obtain and unfair advantage.

7 Classifications of Fraud Fraudulent statements fabrication of an organization s financial statements to make the company appear more or less profitable Corruption- a scheme in which a person uses his or her influence in a business transaction to obtain an unauthorized benefit contrary to that person s duty to his or her employer

8 Contract and Procurement Fraud The Ideal Procurement Cycle

9 Contract and Procurement Fraud Procurement Process Contracting to acquire goods or services Often based on relationships Decisions to acquire made objectively and subjectively Purchases dictated by company policies and procedures Conflicts arise between operations and financial controls Process is often challenged by various work-arounds

10 Contract and Procurement Fraud Common types of procurement fraud Collusion between employees and vendors Vendors defrauding the company Collusion among vendors within an industry Employees defrauding their employers

11 Contract and Procurement Fraud Procurement Fraud Schemes Conflicts of interest Phantom vendor Split purchase orders/split orders Kickbacks Personal purchases Duplicate payments Defective products Product substitution Fictitious invoices Bribery Bid rigging

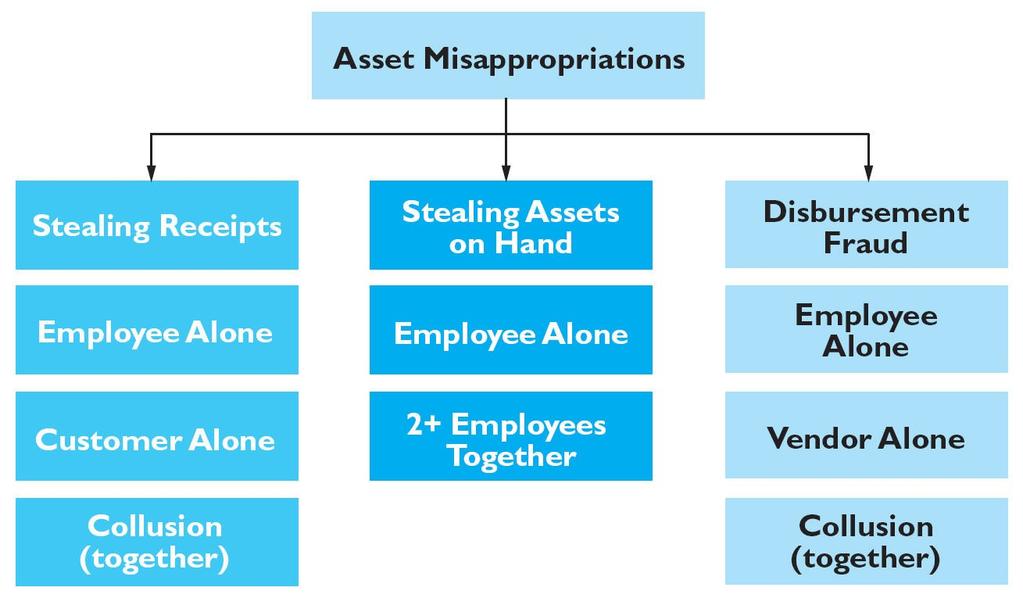

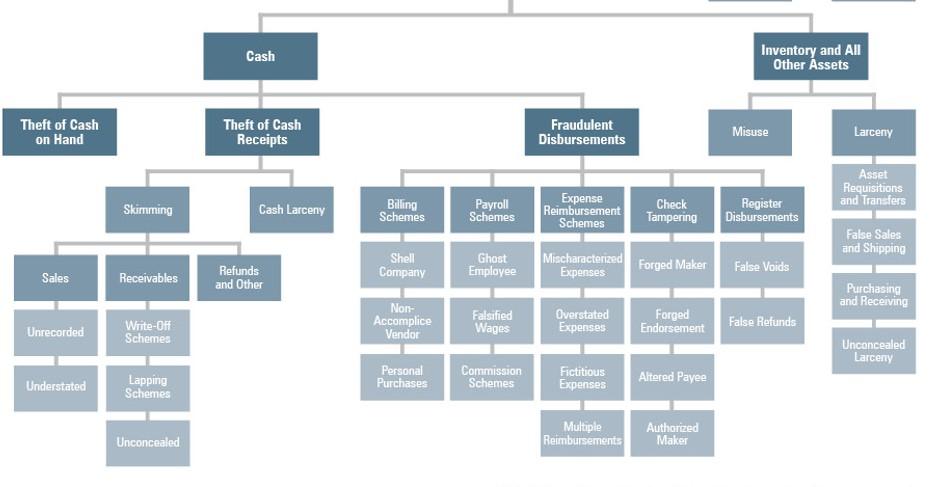

12 Asset Misappropriation Schemes Asset Misappropriation- a scheme that involves the theft or misuse of an organization s assets Cash receipts schemes Inventory and all other assets schemes

13 Asset Missapprpriation

14 Asset Misappropriation Schemes

15 Controlling risks Organization are adopting the COSO risk management and control frameworks to manage and control fraud risk. The three lines of defense framework play a key role in prevention and detection of asset misappropriation fraud.

16 Sales and Accounts Receivables Cash Receipts Schemes Two types; a) Skimming Cash not being recorded in the books of the organization (off-book fraud) b) Larceny- perpetrated when cash has already been recorded in the books of the org

17 Cash Larceny How it is perpetrated: Cash theft at cash collection points Transactions reversing. Register manipulation Altering cash counts Destroying cash register tapes. Deposit lapping. Deposit in transit.

18 Detection of cash Larceny Analysis of cash receipts Review and analysis of the cost of sales, cost of sales, returns and allowances Analysis all journal entries made to cash accounts on a periodic basis

19 Controlling Cash Larceny Enforcing Segregation of duties Assignment rotation and mandatory vacations Surprise cash counts and supervision Physical security of the cash-lockable drawers

20 Fraud Risks in Cash Disbursement How Cash reimbursement fraud is perpetrated. Fictitious expenses Overstated expenses Multiple reimbursements

21 Fraud Risks in Purchasing and Two types Accounts Payable 1. Billing Schemes 2. Cheque Tampering Schemes

22 Fraud Risks in Purchasing and Accounts Payable Billing Schemes Invoicing via shell companies Invoicing via non-accomplice vendors Personal purchases with company funds

23 Fraud Risks in Purchasing and Accounts Payable Prevention of Billing Schemes Training purchasing personnel on ethical standards Sufficient compensation for purchasing staff to reduce the motive and rationalization of fraud Proper documentation-pre-numbered and controlled purchase requisitions; purchase orders receiving reports; cheques Proper approvals-for vendor additions; Local Chart of Authority with limits

24 Fraud Risks in Purchasing and Accounts Payable Prevention of Billing Schemes Segregation of duties-purchasing separate from payment function Invest in hotlines Enforce policies on competitive bidding Purchases and inventory levels should be reviewed for completeness and accuracy Credit card statements should be reviewed periodically for any irregularities

25 Fraud Risks in Purchasing and Accounts Payable Cheque Tampering Schemes Forged maker Forged endorsements Altered payee Authorized maker

26 Fraud Risks in Purchasing and Accounts Payable Prevention of cheque Tampering Schemes Banking controls Cheque preparation/ disbursement controls Cheque custody controls Physical tampering controls

27 Fraud Risk in Payroll and Payroll Schemes HR Ghost workers Commission Schemes Falsified hours and hourly schemes

28 Fraud Risk in Payroll and HR Payroll schemes detection Analysis of deductions from payroll Review of overtime for proper authorizations Random checks on customers to confirm sales for the commission paid Comparative analysis of commissions earned by salespersons Analysis of payee addresses and accounts

29 Fraud Risk in Payroll and HR Prevention of Payroll schemes Segregation duties in payroll duties Monthly payroll reconciliation and management reviews. Outsourcing of payroll processing to a contractor

30 Fraud risk in Physical Assets Inventory and physical assets schemes Theft of inventory, equipment and other assets Misuse of company assets Larceny Asset requisition and transfers Purchasing and receiving schemes

31 Fraud risk in Physical Assets How to detect physical assets fraud schemes Review of perpetual inventory records Undertaking physical inventory counts Analytical review of cost of sales, sales, purchases and purchase prices

32 Financial Statement Fraud Financial Statement Fraud- deliberate misrepresentation of the financial condition of an enterprise accomplished through the intentional misstatement or omission of amounts or disclosures in the financial statement to deceive financial statement users- ACFE definition.

33 Financial Statement Fraud schemes Revenue/Accounts Receivable Frauds Inventory/Cost of Goods Sold Frauds Understating Liability/Expense Frauds Overstating Assets Frauds Overall Misrepresentation/ disclosures Performance schemes (Procurement schemes, contractor schemes)

34 Executive Fraud-Related Schemes Misstating Financial Statements Executive Loans and Corporate Looting Insider Trading IPO Favouritism CEO Retirement Perks

35 Incentives for financial statement Fraud Incentives to commit financial statement fraud are very strong. Investors want decreased risk and high returns. Risk is reduced when variability of earnings is decreased. Rewards are increased when income continuously improves

36 Driver of financial Fraud Why so many financial statement frauds Good economy was masking many problems Moral decay in society Executive incentives Corporate expectations rewards for short-term behavior Nature of accounting rules Behavior of CPA firms Greed by investment banks, commercial banks, and investors Educator failures

37 Way Forward Will Financial Statement Frauds occur in the future? YES: There has been an increasing number of financial statement fraud cases in the recent years Incentives still exist Corporates keep setting high targets for executives NO Governments have stepped in to regulate industries- Risk Based approaches(basel Frameworks) Requirement to have internal controls Accounting Rules for accountants (mandatory audit partner rotation; Oversight Board, limitations on services, etc.)

38 Interactive Session Isaac Mutembei Murugu

Forensics Audit Seminar- Nyeri.. Financial Statement Fraud. Isaac Mutembei Murugu. CIA, CISA 2 nd November 2017

Forensics Audit Seminar- Nyeri.. Financial Statement Fraud Isaac Mutembei Murugu CIA, CISA 2 nd November 2017 Uphold public interest Contents Financial statement, contracts and procurement fraud investigations

Forensics Audit Seminar- Nyeri.. Financial Statement Fraud Isaac Mutembei Murugu CIA, CISA 2 nd November 2017 Uphold public interest Contents Financial statement, contracts and procurement fraud investigations

FRAUD AWARENESS & PREVENTION

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

FRAUD AWARENESS & PREVENTION Nancy Wonderlich Koonce, CPA/MBA/CVA/CFE nkoonce@idahocpa.com What is occupational fraud? The use of one s occupation for personal enrichment through the deliberate misuse

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

FRAUD: A Web Of Deceit

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

FRAUD: A Web Of Deceit Presented by: Tessa Filippazzo, CPA, CFE Curtis Blakely & Co., P.C. PO Box 5486 Longview, TX 75608 (903) 758 0734 tfilippazzo@cbandco.com DEFINITION Intentional perversion of truth

1/3/2013. Months. Other $75,000. Government $81,000. Non-Profit $100,000. Dollars. Public Company $127,000. Private Company $200,000

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

In its 2008 Report to the Nation, Occupational Fraud and Abuse, the Association of Certified Fraud Examiners (ACFE) - reported losses of 7% of revenue or $994 billion of US Gross Domestic Product lost

OCCUPATIONAL FRAUD 9/20/2018

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

OCCUPATIONAL FRAUD Presented by Inv. Andrea Jacobson Alaska State Troopers Alaska Bureau of Investigation Financial Crimes Unit What does it look like? What do we do when we see it? How do we prevent it?

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

HOW TO SPOT AND MITIGATE FRAUDULENT ACTIVITIES For Government Entities and Nonprofit Organizations November 15, 2017 Presenters Bruce V. Bush Bruce is a Senior Director in RSM s Financial Investigations

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Mitigating Fraud. June 22, Sept. 21, 2014

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Mitigating Fraud June 22, 2016 Sept. 21, 2014 Agenda Overview of the 2016 Report to the Nations on Occupational Fraud and Abuse Real Life Fraud Cases Mitigation Tools Lone Star College s Ethics Hotline

Forensics Audit Seminar Fraud in Financial Sector. Isaac Mutembei Murugu. CISA, CIA 24 th November 2017

Forensics Audit Seminar Fraud in Financial Sector Isaac Mutembei Murugu CISA, CIA 24 th November 2017 Uphold public interest Contents Fraud in the financial sector Mobile money fraud ATM fraud Loan related

Forensics Audit Seminar Fraud in Financial Sector Isaac Mutembei Murugu CISA, CIA 24 th November 2017 Uphold public interest Contents Fraud in the financial sector Mobile money fraud ATM fraud Loan related

Fraud Prevention for Nonprofits

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Managing Reputational Risk for Nonprofit Organizations. Best Practices for Fraud Prevention. July 14, Christopher W. Truman, CPA, Manager

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Managing Reputational Risk for Nonprofit Organizations Best Practices for Fraud Prevention July 14, 2014 CLAconnect.com Presenters Christopher W. Truman, CPA, Manager 2 July 14, 2014 1 Things to Think

Financial Transactions and Fraud Schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Fraudulent Disbursements 2016 Association of Certified Fraud Examiners, Inc. Fraudulent Disbursement Schemes Register disbursement schemes

Fraud prevention for credit unions

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

Fraud prevention for credit unions Deposit Insurance Corporation of Ontario November 12, 2013 2 Agenda The cost of fraud Internal fraud The risks of external fraud facing credit unions Fraud prevention

ACFE CFEX. Certified Fraud Examiner (CFEX)

") ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

ACFE CFEX Certified Fraud Examiner (CFEX) http://killexams.com/exam-detail/cfex QUESTION: 167 Bank statement are diligently reviewed to ensure that amounts and signature have not been altered, is an activity

Lecture notes for: Corporate Cons

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

Lecture notes for: Corporate Cons This video covers internal fraud schemes (as opposed to management trying to defraud investors - like the other two videos) Cash Internal fraud schemes: Accounts receivable

A c f e. Report to. the Nation. on Occupational Fraud & Abuse

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

2 0 0 6 A c f e Report to the Nation on Occupational Fraud & Abuse Letter from the President On behalf of the ACFE, I am pleased to present the 2006 Report to the Nation on Occupational Fraud and Abuse,

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

An Expensive Problem. Fraud in Government A Growing Problem

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

Stuart T Stickel, CPA, CFE Deputy State Auditor West Virginia State Auditor s Office Charleston, WV An Expensive Problem Business fraud and abuse in the U.S. cost about $650 billion a year. Government

November 2017 ICPAK FORENSIC AUDIT SEMINAR

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

November 2017 ICPAK FORENSIC AUDIT SEMINAR Introduction What is Fraud? 2 1 Insert Banner Profile of a Fraudster Introduction to Fraud A false representation of a matter of fact, whether by words or by

Grant Fraud. Leslie Les Hollie Assistant Inspector General For Investigations

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Grant Fraud Leslie Les Hollie Assistant Inspector General For Investigations US Dept of Health and Human Service Office of Inspector General Office of Investigations Washington, DC HRSA: May 16, 2017 Not

Sunera Canada ULC. Effective Fraud Risk Assessment Annual Fraud Program. October 21, 2016

Sunera Canada ULC Effective Fraud Risk Assessment 2016 Annual Fraud Program October 21, 2016 Sunera LLC Snapshot Professional consultancy with core competency in Governance, SOx, NI 52-109, Internal Audit,

Sunera Canada ULC Effective Fraud Risk Assessment 2016 Annual Fraud Program October 21, 2016 Sunera LLC Snapshot Professional consultancy with core competency in Governance, SOx, NI 52-109, Internal Audit,

Fraud Examination. Prevention, Detection, and Investigation. Steven M. Bragg

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud Examination Prevention, Detection, and Investigation Steven M. Bragg Chapter 1 Introduction to Fraud... 1 Learning Objectives... 1 Introduction... 1 What is Fraud?... 1 Confidence... 1 The Effects

Fraud Risk Assessment

Fraud Risk AHIA Southeast Regional Seminar Houston Texas Friday, November 12, 2010 Today s Discussion Agenda What is fraud? Industry fraud statistics Common fraud scenarios Fraud risk assessment (FRA)

Fraud Risk AHIA Southeast Regional Seminar Houston Texas Friday, November 12, 2010 Today s Discussion Agenda What is fraud? Industry fraud statistics Common fraud scenarios Fraud risk assessment (FRA)

Lecture Notes for How to Steal $500 Million

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

Lecture Notes for How to Steal $500 Million These notes will be in the form of questions that you should try to answer while watching the video. The purpose is to make certain that you are paying attention

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

International Standard on Auditing (Ireland) 240

240") International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

Table 1: Historical Summary of Revenue Lost to Fraud. Estimate of Revenue Lost to Fraud

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

Anchin Alert: ACFE Report to the Nations 2018 The Association of Certified Fraud Examiners ( ACFE ) recently published the Report to the Nations 2018 Global Study on Occupational Fraud and Abuse (the 2018

International Standard on Auditing (UK) 240 (Revised June 2016)

240 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

IIA Fraud Conference. Case studies from recent investigations. 8 April 2015

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

IIA Fraud Conference Case studies from recent investigations 8 April 2015 Outline What is fraud and types of fraud EY s 13 th Global Fraud Survey Survey approach and participant profile Unethical behavior

The Procurement Fraud Equation. Tom Caulfield

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

The Procurement Fraud Equation Tom Caulfield Specializing in assessment and mitigation strategies for procurement integrity to reduce the risk of financial and reputation losses 2016 ACFE Law Enforcement

Fraud Prevention & Detection. Eric Conforti, CPA, CFE April 17, 2018

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud Prevention & Detection Eric Conforti, CPA, CFE April 17, 2018 1 Recent Trends Prevention and Detection Methods Common Schemes Case Studies Throughout 2 ACFE Report to the Nations 3 ACFE Report to

Fraud in Government. Mike Nolan, CPA, CFE, CGMA. CCACC & CCA&RMC Conference Monterey, CA September 2014

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

Fraud in Government Mike Nolan, CPA, CFE, CGMA CCACC & CCA&RMC Conference Monterey, CA September 2014 Headlines Former New Orleans Mayor Ray Nagin convicted of corruption City of Bell California Public

The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Chapter 2 Skimming 1

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

Chapter 2 Skimming 1 Define skimming. Chapter Objectives List and understand the two principal categories of skimming schemes. Understand how sales skimming is committed and concealed. Understand schemes

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen:

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

The Auditor s Responsibilities. Audit of Financial Statements

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Finacial Statement Fraud. Peter N Munachewa, CFE Risk Management Consultant

Finacial Statement Fraud Peter N Munachewa, CFE Risk Management Consultant What is FSF Falsification, alteration, or manipulation of material financial records, supporting documents, or business transactions

Finacial Statement Fraud Peter N Munachewa, CFE Risk Management Consultant What is FSF Falsification, alteration, or manipulation of material financial records, supporting documents, or business transactions

Fraud Detection in Public Schools

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

Fraud Detection in Public Schools Goal: To learn how to prevent and detect fraud from actual evidence uncovered during fraud investigations Format: We will discuss three of the largest fraud cases over

FRAUD TRENDS TO WATCH FOR IN Presented by: Daniel J. Mahalak

FRAUD TRENDS TO WATCH FOR IN 2018 Presented by: Daniel J. Mahalak Session Overview In recent years, fraud has seemingly been increasing in credit unions. Some of this fraud is related to the technology

FRAUD TRENDS TO WATCH FOR IN 2018 Presented by: Daniel J. Mahalak Session Overview In recent years, fraud has seemingly been increasing in credit unions. Some of this fraud is related to the technology

COVERAGE FRAUD IN EMPLOYEE BENEFIT PLANS 5/15/2014. Where employee benefit fraud is likely. Internal controls that help prevent fraud

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

FRAUD IN EMPLOYEE BENEFIT PLANS COVERAGE Where employee benefit fraud is likely Internal controls that help prevent fraud What should management have done? Schemes and war stories 1 FRAUD TRIANGLE Incentive/pressure

INTERNAL FRAUD PREVENTION:

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

INTERNAL FRAUD PREVENTION: COMMON FRAUDS AND THE ABSOLUTES OF INTERNAL CONTROL DESIGN Presented for the 2018 Telergee Alliance CFO & Controllers Conference Presented by STEVE DAWSON, CPA, CFE 1 The Not

UNDERSTANDING FINANCIAL STATEMENTS

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

UNDERSTANDING FINANCIAL STATEMENTS WHAT ARE FINANCIAL STATEMENTS? Most commonly there are 3 types of financial statements: 1. Balance Sheet 2. Income Statement 3. Cash Flows BREAKING IT DOWN: THE BALANCE

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY Letter from the President In 1996, Dr. Joseph T. Wells, CFE, CPA, founder and Chairman of the ACFE, directed the publication

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 GLOBAL FRAUD STUDY Letter from the President In 1996, Dr. Joseph T. Wells, CFE, CPA, founder and Chairman of the ACFE, directed the publication

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

PREVENTING FRAUD IN THE HOSPITALITY INDUSTRY Provided by David M. Bleser of Hospitality Safeguards, Inc. Jim Stover of Arthur J. Gallagher TABLE OF CONTENTS I. INTRODUCTION TO FRAUD...2 A. FRAUD FOUNDATION...2

Future Generali India Insurance Company Limited. Anti Fraud Policy. (Version 5.0)

") Future Generali India Insurance Company Limited Anti Fraud Policy (Version 5.0) Document Status: Field Standard Name Description Anti-Fraud Policy Company Future Generali India Insurance Company Limited

Future Generali India Insurance Company Limited Anti Fraud Policy (Version 5.0) Document Status: Field Standard Name Description Anti-Fraud Policy Company Future Generali India Insurance Company Limited

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

CRIMESTAR. commercial crime from a different angle

CRIMESTAR commercial crime from a different angle CRIMESTAR commercial crime from a different angle THE IMPORTANCE OF BROAD COVER FOR DIFFERENT TYPES OF FRAUD The motivation for fraud is triggered by a

CRIMESTAR commercial crime from a different angle CRIMESTAR commercial crime from a different angle THE IMPORTANCE OF BROAD COVER FOR DIFFERENT TYPES OF FRAUD The motivation for fraud is triggered by a

Chapter 2 Skimming. 2. To a fraudster, the principle advantage of skimming is the difficulty with which the scheme is detected. a. True b.

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Chapter 2 Skimming 1. is the theft of cash from a victim entity prior to its entry in an accounting system. a. A fictitious disbursement b. Skimming c. Larceny d. Conversion 2. To a fraudster, the principle

Chapter 10. Cash and Financial Investments. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

Fraud: How to Get Your District Free Publicity

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

APRIL 13-16, 2016 Fraud: How to Get Your District Free Publicity THESE MATERIALS HAVE BEEN PREPARED BY NIGRO & NIGRO, PC THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL, SO THEREFORE ARE NOT AN

1: ASSESSMENT OF EXPOSURE TO SPECIFIC FRAUD RISKS - SELECTION OF APPLICANTS BY MANAGING AUTHORITIES

1: ASSESSMENT OF EXPOSURE TO SPECIFIC FRAUD RISKS - SELECTION OF APPLICANTS BY MANAGING AUTHORITIES Ref Title description SR1 Conflicts of interest within the evaluation Members of the MA's evaluation

1: ASSESSMENT OF EXPOSURE TO SPECIFIC FRAUD RISKS - SELECTION OF APPLICANTS BY MANAGING AUTHORITIES Ref Title description SR1 Conflicts of interest within the evaluation Members of the MA's evaluation

The University has no tolerance of bribery and fraud and will take appropriate action to prevent it in respect of its activities.

University of Hull SUMMARY Policy: The University has no tolerance of bribery and fraud and will take appropriate action to prevent it in respect of its activities. Bribery and fraud by University employees

University of Hull SUMMARY Policy: The University has no tolerance of bribery and fraud and will take appropriate action to prevent it in respect of its activities. Bribery and fraud by University employees

Approval version. G l o b a l P o l i c y : F r a u d R e s p o n s e a n d W h i s t l e b l o w i n g P o l i c y. Board of Directors.

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

Good From The Inside Out. Saturday, April 8, 2017

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

Good From The Inside Out Saturday, April 8, 2017 What s New? Just last week Ex-CFO Accused of Embezzling $20M From Credit Union -Detroit Free Press January 9, 2016 Headlines Recent headlines Engaged CU

7/21/2015. July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT. Lessons from the Trenches. Angela Morelock Partner

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

July 22, 2015 at 1 p.m. Central time FRAUD & EMBEZZLEMENT Lessons from the Trenches Angela Morelock Partner amorelock@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

Community College Audit and Fiscal Compliance Workshop. VAVRINEK, TRINE, DAY & CO., LLP May 23, 2017

Community College Audit and Fiscal Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP May 23, 2017 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Community College Audit and Fiscal Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP May 23, 2017 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Catch Me If You Can. Fraud in Local Government. CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

Catch Me If You Can Fraud in Local Government CITY & COUNTY OF SAN FRANCISCO Office of the Controller Audits Division Steve Flaherty, Principal Investigator 10.03.2018 2 Disclaimer Any names or incidents

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE FOREWORD Bruce Dorris, J.D., CFE, CPA President and CEO, Association of Certified Fraud Examiners With the publication of the 2018

REPORT TO THE NATIONS 2018 GLOBAL STUDY ON OCCUPATIONAL FRAUD AND ABUSE FOREWORD Bruce Dorris, J.D., CFE, CPA President and CEO, Association of Certified Fraud Examiners With the publication of the 2018

Everything You Didn t Want To Know About Employee Crime

Everything You Didn t Want To Know About Employee Crime It's something employers don't want to have to think about: employee crime. Finding out that trusted, long-term employees have been stealing from

Everything You Didn t Want To Know About Employee Crime It's something employers don't want to have to think about: employee crime. Finding out that trusted, long-term employees have been stealing from

This document sets out the University s position on Fraud and Bribery and its framework for addressing the Bribery Act Scope

1 Policy/CoP title: Anti-Fraud and Bribery Policy 2 Summary description This document sets out the University s position on Fraud and Bribery and its framework for addressing the Bribery Act 2010 3 Scope

1 Policy/CoP title: Anti-Fraud and Bribery Policy 2 Summary description This document sets out the University s position on Fraud and Bribery and its framework for addressing the Bribery Act 2010 3 Scope

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Have you dealt with fraud in the past?

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

Birmingham CPE Seminar Birmingham, Alabama August 17, 2017 Fraud: Real People, Real Schemes Roy Strickland, CPA/CFF, CFE, MAFF 1 Polling Question Have you dealt with fraud in the past? 2 DHG Birmingham

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain RISK MANAGEMENT CA. Pramod Jain Risks are potential events that

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain RISK MANAGEMENT CA. Pramod Jain Risks are potential events that

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE GLObAL FrAUD STUDy

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2014 GLObAL FrAUD STUDy Letter from the President & CEO In 1988, Dr. Joseph T. Wells founded the ACFE with a stated mission to reduce the incidence

Is Your Construction Project a Victim of Fraud?

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction

Is Your Construction Project a Victim of Fraud? Guler Ann Wiefling, CFE Partner, Forensics and Litigation Services Stephen Howard, CFE Director, Forensics and Litigation Services Agenda Is Your Construction

Analyzing a Potpourri of Fraud in Higher Education. Calvin Wendelboe, CPA, CIA, CFE

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Analyzing a Potpourri of Fraud in Higher Education Calvin Wendelboe, CPA, CIA, CFE Green Dot Bank Participating with Poll Everywhere Web Voting PollEv.com/ACUA 22333 Text Voting ACUA Scheme #1 Asset

Figure 1: Occupational Frauds by Category Frequency

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Figure 1: Occupational Frauds by Category Frequency TYPE OF FRAUD Asset Misappropriation Corruption Financial Statement Fraud 12.8% 26.7% 89.5% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Figure 2: Occupational

Policy on Fraud Prevention and Detection

Status: Approved Custodian: Director: Finance and Administration Date approved: 2011-09-21 Decision number: SAQA 0893/11 Implementation date: 2011-09-21 Due for review: 2014-09-20 File Number: 1 Table

Status: Approved Custodian: Director: Finance and Administration Date approved: 2011-09-21 Decision number: SAQA 0893/11 Implementation date: 2011-09-21 Due for review: 2014-09-20 File Number: 1 Table

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

(No., Street) Present Crime Insurance Program: (Include primary AND excess, if applicable) If not applicable, please check here:

Present Crime Insurance Program: (Include primary AND excess, if applicable) If not applicable, please check here:") , a stock insurance company, herein called the Insurer THE HARTFORD CRIMESHIELD SM ADVANCED POLICY APPLICATION FOR NON-CUSTODIAL INVESTMENT ADVISERS (FIRST PARTY) Agency Name: Hartford Agency Code: Application

, a stock insurance company, herein called the Insurer THE HARTFORD CRIMESHIELD SM ADVANCED POLICY APPLICATION FOR NON-CUSTODIAL INVESTMENT ADVISERS (FIRST PARTY) Agency Name: Hartford Agency Code: Application

Cash and Internal Control C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

Cash and Internal Control E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to

ACC3FOA CHAPTER 1 THE NATURE OF FRAUD

Civil Law Customer Fraud Employee Embezzlement Evidential Matter Financial Statements Fraud Investment Scams Jurisdiction Management Fraud Miscellaneous Fraud Net Income Perpetrators Profit Margin Revenue

Civil Law Customer Fraud Employee Embezzlement Evidential Matter Financial Statements Fraud Investment Scams Jurisdiction Management Fraud Miscellaneous Fraud Net Income Perpetrators Profit Margin Revenue

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

Identifying and preventing fraud & corruption in ESI Funds. Fraud prevention: Audit and control systems; Reporting fraud; Fraud indicators.

Fraud prevention: Audit and control systems; Reporting fraud; Fraud indicators. Dermot Byrne, Head of Authority Identifying and preventing fraud & corruption in ESI Funds ERDF Audit Authority, Ireland

Fraud prevention: Audit and control systems; Reporting fraud; Fraud indicators. Dermot Byrne, Head of Authority Identifying and preventing fraud & corruption in ESI Funds ERDF Audit Authority, Ireland

Fraud Risk Assessment Awareness in Employee Benefit Plans

Fraud Risk Assessment Awareness in Employee Benefit Plans Tyler Geiman, CPA, CFE, CFF Novak Francella, LLC Phone: (443) 832-4009 Fax: (443) 393-0323 Web: www.novakfrancella.com Fraud is any intentional

Fraud Risk Assessment Awareness in Employee Benefit Plans Tyler Geiman, CPA, CFE, CFF Novak Francella, LLC Phone: (443) 832-4009 Fax: (443) 393-0323 Web: www.novakfrancella.com Fraud is any intentional

POLICY APPLICATION for COMMERCIAL and GOVERNMENTAL ENTITIES

, a stock insurance company, herein called the Insurer CrimeSHIELD SM POLICY APPLICATION for COMMERCIAL and GOVERNMENTAL ENTITIES Agency Name: Hartford Agency Code: Application is hereby made by: (First

, a stock insurance company, herein called the Insurer CrimeSHIELD SM POLICY APPLICATION for COMMERCIAL and GOVERNMENTAL ENTITIES Agency Name: Hartford Agency Code: Application is hereby made by: (First

MIS 520 Data Analytics for IT Auditors

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

MIS 520 Data Analytics for IT Auditors Week 1: Introduction to Fraud Ed Ferrara, MSIA, CISSP eferrara@temple.edu The Many Faces of Fraud Fraud Theft (Misappropriation) Deceptive Statements Corruption Fraud

APPLICATION FOR FINANCIAL INSTITUTION BOND FOR INVESTMENT FIRMS NON-CUSTODIAL INVESTMENT ADVISORS (FIRST PARTY)

") APPLICATION FOR FINANCIAL INSTITUTION BOND FOR INVESTMENT FIRMS NON-CUSTODIAL INVESTMENT ADVISORS (FIRST PARTY) Agency Name: Hartford Agency Code: Application is hereby made by (Name of Adviser): (First

APPLICATION FOR FINANCIAL INSTITUTION BOND FOR INVESTMENT FIRMS NON-CUSTODIAL INVESTMENT ADVISORS (FIRST PARTY) Agency Name: Hartford Agency Code: Application is hereby made by (Name of Adviser): (First

Delivering Confidence PAGE 1

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

PAGE 1 PAGE 2 Small Business, Big Thieves Preventing Fraud in Your Organization Presented by: Sean T. Daughton, CPA, CFE Kaitlyn Hensler, CPA, CFE 6.6.2018 3 Big Thieves PAGE 3 4 Concealing Fraud PAGE

Fraud in the Government Realm. Introduction. What is Fraud? My career began with a local government fraud in 1993

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

11/9/15. Fraud in Non-profit Organizations: What You Need to Know NOW!

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

Fraud in Non-profit Organizations: What You Need to Know NOW! The CFE Credential The Certified Fraud Examiner (CFE) credential denotes proven expertise in fraud prevention, detection and deterrence. CFEs

THE CHANGING PATTERNS OF FINANCIAL STATEMENT FRAUD

THE CHANGING PATTERNS OF FINANCIAL STATEMENT FRAUD DEFINITIONS Financial statement frauds is the deliberate misrepresentation of the financial conditions of an enterprise accomplished through the intentional

THE CHANGING PATTERNS OF FINANCIAL STATEMENT FRAUD DEFINITIONS Financial statement frauds is the deliberate misrepresentation of the financial conditions of an enterprise accomplished through the intentional

CRIMEGUARD CHOICE SM Fidelity and Crime Insurance APPLICATION. Name of Applicant: Principal Address: Date Business Established: Annual Revenues:

GENERAL INFORMATION National Union Fire Insurance Company of Pittsburgh, Pa. (a capital stock company, herein called the Company ) Executive Offices: 175 Water Street New York, NY 10038 CRIMEGUARD CHOICE

GENERAL INFORMATION National Union Fire Insurance Company of Pittsburgh, Pa. (a capital stock company, herein called the Company ) Executive Offices: 175 Water Street New York, NY 10038 CRIMEGUARD CHOICE

Illustrate by way of some example how Fraudulent Financial Reporting and Misappropriation of Asset can be done?

SA240(R) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL What is a Fraud? Intentional mistakes to get unjust advantage are commonly known as fraud. Fraud as defined by SA 240

SA240(R) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL What is a Fraud? Intentional mistakes to get unjust advantage are commonly known as fraud. Fraud as defined by SA 240

Anti-fraud and Corruption Policy

Anti-fraud and Corruption Policy Responsible Division: Finances Validated by: Board (Executive Committee) Date of approval: 17/05/2017 Date of next review: May 2019 Language versions available: English

Anti-fraud and Corruption Policy Responsible Division: Finances Validated by: Board (Executive Committee) Date of approval: 17/05/2017 Date of next review: May 2019 Language versions available: English

Chapter 9. #17 is a bad question if it is changed as follows the answer is d

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

INTERNAL AUDIT AND THE RISING CORPORATE SCANDALS

INTERNAL AUDIT AND THE RISING CORPORATE SCANDALS The Internal Audit Conference 29 th March 2017 Presenter: CPA Ronald Wanyama Outline Introduction What are Corporate Scandals? Causes of Corporate Scandals

INTERNAL AUDIT AND THE RISING CORPORATE SCANDALS The Internal Audit Conference 29 th March 2017 Presenter: CPA Ronald Wanyama Outline Introduction What are Corporate Scandals? Causes of Corporate Scandals

Internal Routine & Controls (IRC) & Fraud New York Region Directors College

& Fraud New York Region Directors College") Internal Routine & Controls (IRC) & Fraud 2015 New York Region Directors College Discussion Topics Fraud: What It Is and Why People Commit It Fundamentals of IRC and Fraud Prevention Insider Fraud Fraud

Internal Routine & Controls (IRC) & Fraud 2015 New York Region Directors College Discussion Topics Fraud: What It Is and Why People Commit It Fundamentals of IRC and Fraud Prevention Insider Fraud Fraud

Spotting Financial Distortions: A Primer for Attorneys

Spotting Financial Distortions: A Primer for Attorneys The Web Conference Series For Corporate Counsel January 17, 2007 To ask a question using the question pane Enter your question into the text area

Spotting Financial Distortions: A Primer for Attorneys The Web Conference Series For Corporate Counsel January 17, 2007 To ask a question using the question pane Enter your question into the text area

Fraud and corruption prevention and control policy of the International Federation of Red Cross and Red Crescent Societies

www.ifrc.org Saving lives, changing minds. Fraud and corruption prevention and control policy of the International Federation of Red Cross and Red Crescent Societies Document Issued On: [insert date] Approved

www.ifrc.org Saving lives, changing minds. Fraud and corruption prevention and control policy of the International Federation of Red Cross and Red Crescent Societies Document Issued On: [insert date] Approved

Protecting against check fraud perspectives and best practices

Protecting against check fraud perspectives and best practices Presenter Name Corp Title, Functional Title Date of presentation 2016 Wells Fargo Bank, N.A. All rights reserved. For public use. Agenda Check

Protecting against check fraud perspectives and best practices Presenter Name Corp Title, Functional Title Date of presentation 2016 Wells Fargo Bank, N.A. All rights reserved. For public use. Agenda Check

OAPT June 9, Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

OAPT June 9, 2015 Deterring Fraud and the Latest Fraud Schemes in Public Entities TAKE AWAY #1 Fraud can happen at any entity, at any time with the right circumstance Be Vigilant and Skeptical of what

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 2016 SOUTHERN ASIA EDITION Contents Introduction...3 How Occupational Fraud Is Committed...5 Frequency and Median Loss of Occupational Fraud Schemes...