Piotr Danisewicz Lancaster University Danny McGowan University of Nottingham Enrico Onali Aston University Klaus Schaeck Lancaster University

|

|

|

- Alvin Green

- 5 years ago

- Views:

Transcription

1 2nd ACPR conference Paris, December 2, 2015 Piotr Danisewicz Lancaster University Danny McGowan University of Nottingham Enrico Onali Aston University Klaus Schaeck Lancaster University

2 Debt priority has implications for monitoring incentives. If junior claimants are exposed to greater losses in the event of bankruptcy, they should have greater incentives to increase ex ante monitoring efforts. Exploiting an unexplored natural experiment in the U.S. banking industry, we provide novel insights into market discipline in banking. Market discipline: Cornerstone of the financial safety net Monitoring dimension: Typically reflected in risk pricing of bank debt. Influencing dimension: Changes in bank conduct. We investigate if changes to the priority structure of claims on bank assets affect junior-debtholders (i.e., non-depositors) incentive to monitor and influence conduct. 2

3 Staggered introduction of depositor preference laws (DPLs) in 15 U.S. states between 1983 and Assets of failed bank are paid out to creditors based on a claims structure. DPLs change the claim structure on a failed bank s assets by assigning a priority claim to all depositors by subordinating non-depositors. DPLs only apply to state-chartered but not to nationally-chartered banks. The Banking Act of 1935 specified a claims structure 1. Receiver without DPLs 2. Secured creditors 3. Insured depositors 4. Uninsured depositors & general creditors 5. Shareholders 1. Receiver with DPLs 2. Secured creditors 3. Insured & uninsured depositors 4. General creditors 5. Shareholders 3

.")

4 Subordinating claims of general creditors to those of depositors eradicates costly duplication of monitoring. DPLs reallocate monitoring to more efficient monitors, which have more efficient monitoring technologies (Birchler 2000 RFS). Empirical predictions: (Uninsured) depositors require a lower interest rate which reduces funding costs and translates into higher bank profits (pricing effect). Monitoring dimension o Shift in liability structure towards increased deposit funding (quantity effect). Non-depositors seek compensation for higher risk. (pricing effect). o Shift in liability structure away from non-deposit funding (quantity effect). Influencing dimension Increase in monitoring incentivizes banks to reduce risk. o Reductions in bank risk taking. 4

5 Proponents from the policy community argue this will: 1. Prevent bank runs 2. Engender more stable banking through increased market discipline But the banking industry is sceptical arguing DPL will: 1. Raise costs of funding for banks 2. Raise costs for customers 5

; Bliss and Flannery (2000 WP); Martinez Peria and Schmukler (2001 JF); Goldberg and Hudgins (2002 JFE); Krishnan, Ritchken, and Thomson (2005 JF); Ashcraft (2008 JFI).")

6 Jury is still out on whether private sector agents reliably engage in risk monitoring and preventative influence of bank behavior. Flannery and Sorescu (1996 JF); Bliss and Flannery (2000 WP); Martinez Peria and Schmukler (2001 JF); Goldberg and Hudgins (2002 JFE); Krishnan, Ritchken, and Thomson (2005 JF); Ashcraft (2008 JFI). Crisis raised counter concerns that market discipline has lost much of its appeal in the years. Acharya, Anginer, and Warburton (2014 WP) New insights for policy and regulation. DPLs as a policy tool received little attention in the past few decades. Debate about such legislation in EU after the crisis with policymakers and academics advocating the use of bail-in provisions where debtholders contribute to bank resolutions (Flannery 2010 WP). ECB called for the introduction of depositor preference laws in all member states of the EU in the aftermath of the crisis in Cyprus (implemented by the end of 2014 in EU member countries). Independent Commission on Banking in the UK recommended the introduction of such laws. Implications in a broader corporate finance context. Loan contracts need to be structured in a way to provide incentives for the lender to monitor the borrower (Rajan and Winton 1995 JF). Assigning priority claims to depositors: alternative to contractual devices to motivate monitoring in context of banking regulation. 6

7 Ideal experiment to establish causality arising from seniority of debt claims. Exploit variation across states over time in the introduction of depositor preference laws allows a valid counterfactual. Successive adoption of DPLs states constitutes a plausibly exogenous change in the monitoring incentives of non-depositors. Difference-in-difference estimations to compare key dependent variables among state-chartered banks with observationally similar control group of nationally-chartered banks from same state unaffected by DPLs. Panel data with quarterly frequency allow bank-fixed effects and state-quarter fixed effects. 30 states opted to implement DPLs between 1909 and In 1993, Clinton administration introduced DPLs for all banks, irrespective of the charter. 7

8 Quarterly Call Report data for commercial and savings banks in the U.S. Sample covers 1983Q1 to 1993Q2 for banks in 15 enacting states and includes 199,698 observations for 5,506 banks 8

9 Representativeness: Comparing banks in 15-state sample with average bank in the U.S. using the population suggests no significant differences in asset size and profits. Weakly significant difference at the ten percent level for soundness. Exogeneity: We survey state legislative councils legislative council s digests concurrencies of the state amendments assembly laws, and Lexis/Nexis, Factiva, and American Banker: Sources do not suggest banking sector conditions or lobbying by interest groups drive implementation of DPLs. Linear probability models and Cox proportional hazard models empirically refute adoption of DPLs is endogenous with respect to the outcomes we study. 9

10 We exploit plausibly exogenous variation in DPL enactment across states and time using a difference-in-difference estimator We estimate y ist = α + β DPL st Charter i + δx ist + γ i + γ st + ε ist Dependent variables measure cost of funds [Total interest expenses, deposit interest expenses, non-deposit interest expenses to total liabilities] liability structure [market shares for insured, uninsured deposits, and non-deposits] Soundness [Z-score (ln), non-performing loans ratio, leverage], Profitability [ROE, Total interest income to total income]. X ist is a vector of bank-time varying controls; γ i bank fixed effects; γ st are state-quarter fixed effects. Dummy variables rule out all unobservable time-invariant bank-specific factors, and state-time-varying forces at the state and national levels, and Clean identification of the average treatment effect - we exploit cross-charter variation within the state-quarter dimension of the data set, i.e.. we compare banks in the same macro environment. Errors clustered at the bank level. 10

11 Pricing effects funding costs Dependent variable Total interest expenses Interest on deposits Interest on non-deposits Charter (1.38) (1.52) (-1.39) Charter*DPL *** *** *** (-4.06) (-4.56) (6.31) Bank size *** *** *** (12.29) (13.14) (3.47) Capital ratio Total interest *** *** ** expenses and interest (-11.33) (-10.83) (2.31) Bank FE YES YES YES on deposits decline State*Quarter FE YES YES YES Observations as deposits priority 199, , ,731 R 2 increases! Number of banks Economically significant 5,509 5,509 5,509 These effects persist in the long run! Heightened exposure to losses causes an increase in non-deposit costs Evidence of monitoring! 11

12 Dependent variable Insured deposits Uninsured deposits Non-deposits Charter*DPL ** (-0.35) (2.26) (0.27) Bank size (-1.51) (-1.14) (1.75) Capital ratio (-0.31) (-0.48) (-0.32) State-charter FE YES YES YES State*Quarter FE YES YES YES Observations R 2 Number of state-charters 1,286 1,286 1,286 Uninsured deposits market shares increase! No effect on state-chartered banks market share of insured deposits. Insured depositors position is unaffected by DPLs. Economically large (13 percent) increase in state-chartered banks market share of uninsured deposits. Risk-averse uninsured depositors increase supply to state-chartered banks. 12

13 Panel A: Banks risk and decomposed Z-Score (ln) Panel B: Banks profitability Dependent variable ZSCORE(ln) ROASD(ln) ROA(ln) ETA(ln) NPL LEV ROE(ln) TIINC(ln) Charter ** * ** *** *** (2.45) (-1.72) (2.42) (2.87) (-0.37) (0.35) (1.04) (-2.77) Charter * DPL *** *** *** * * ** ** (5.26) (-1.58) (3.20) (7.12) (-1.78) (-1.78) (1.99) (2.51) - Bank size *** *** *** *** ** ** *** (2.58) (-7.76) (11.91) (-12.08) (-6.00) (14.04) (12.48) (-1.28) Bank FE YES YES YES YES YES YES YES YES State*Quarter FE YES YES YES YES YES YES YES YES Observations 199, , , , , , , ,731 R-squared Number of banks 5,509 5,509 5,509 5,509 5,509 5,509 5,509 5,509 Improved health: Z- scores (ln), nonperforming loans, and leverage improve! Evidence of influencing! Improved profitability! Evidence of influencing! Results are consistent with Birchler (2000 RFS) and Hardy (2013 WP) Non-depositors have stronger incentives to monitor banks risk exposure due to their junior claim. More skin in the game. These actions put constraints on the risk-taking behavior of banks asset allocation choices. 13

14 Potential confounds and omitted variables 15 difference-in-differences estimates in the paper staggered nature. Omitted variable has to coincide temporarily with all 15 treatments and has to only affect state-chartered banks. Nevertheless, a set of plausible factors warrant investigation. 1. Bank size correlates with funding structure and funding costs Triple interaction terms between size, DPL, and state-chartered bank dummy remains insignificant. 2. Banks may want to avoid being subject to DPLs and switch charter. Only 3.8 percent of banks switch charters Charter switches are not significantly associated with DPL adoption. Omitting banks that switch charters has no effect on our results. 14

15 Potential confounds and omitted variables 3. The U.S. experienced a string of banking problems in the 1980s and 1990s. Texas banking crisis New England banking crisis (Connecticut, Maine, New Hampshire, and Rhode Island) Omitting Texas and the New England States has no effect on our findings. S&L crisis Triple interaction terms that consider the intensity of the S&L crisis leaves our results unchanged. 4. Regulators react to the banking turmoil. FIRREA (1989): More resources to deal with failing banks. Removing observations 1989Q4 to 1993Q2 during which FIRREA has no effect on key coefficients. FDICIA (1991): Introduces least cost resolution provision - suggests effect on key coefficients because purchase and assumption transactions which tend to be associated with lower resolution costs are easier in states with depositor preference. If no FDICIA, key coefficients should be smaller in magnitude. Omitting observations 1991Q4 to 1993Q2 yields indeed smaller key coefficients. 5. Deregulation: Lifting of inter- and intrastate branching restrictions. Triple interaction terms to consider inter- and intrastate deregulation with the charter dummy and the dummy for depositor preference. Interaction terms remain insignificant, and our main results are unaffected, although the magnitude of the coefficients declines. 15

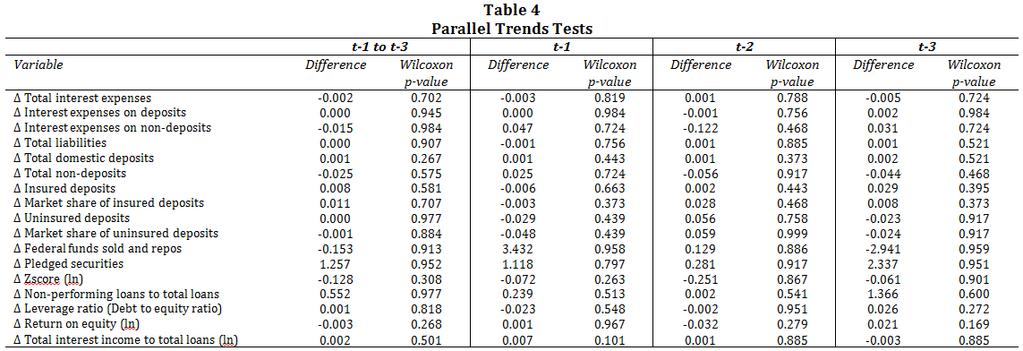

16 Placebo tests to examine the validity of the parallel trends assumption. Changes in conduct should only be observed when DPLs affects state-chartered banks but can neither be observed at other points in time, nor in other types of banks which are not subject to treatment. Random assignment of placebo treatments to nationally-chartered banks. Anticipation effects are ruled out by assigning treatment randomly to state-chartered banks prior to the treatment. All placebo tests remain insignificant! Magnitudes of the coefficients should remain unaffected irrespective of control variables. Main tests excluding time-varying bank-specific control variables indeed show very similar coefficient magnitudes. Clustering of standard errors. Collapsing observations before and following enactment of DPLs does not affect inferences. Double-clustering of the standard errors at bank and year level has no effect. Other tests show that including all 50 states, accounting for a charter time trend, and survivorship bias also leave the inferences unchanged. 16

17 Falsification test Monte Carlo simulations with 1,000 replications to check whether state- chartered banks were affected by federal DPL in Sample consists of state-chartered banks from the 15 states because a suitable control group does not exist. Random assignment of banks to placebo treatment in 1993Q3 and all subsequent quarters or zero otherwise. Specification estimates how much higher/lower the dependent variable was within the same bank following the introduction of federal DPL. Null of zero effect is true. This analysis confirms that state-chartered banks affected by state depositor preference law remained unaffected by the subsequent introduction of national depositor preference. External validity State-chartered banks in states with DPLs are ideal control group for an alternative setup. Extend sample period to 1997Q3. group are all banks in states that had not implemented DPLs prior to 1993Q3 and nationally-chartered banks in states that had introduced depositor preference legislation. We obtain the same effect now on the newly treated banks. Test highlights the external validity of our inferences. 17

18 Unexplored natural experiment to inform the debate about market discipline. Timely importance for policy and regulation. Australia, Argentina, Hong Kong, Malaysia, and the U.S. already have some form of DPL in place. EU policy makers introduced priority to depositors claims in a bank failure in 2014 after intensive debates with the industry. Key findings illustrate that non-depositors are a credible source of market discipline. We document both pricing and quantity effects. We not only find evidence of monitoring but also show creditors influence conduct in terms of risk taking. As treatement is plausibly exogenous, results are highly robust. From a policy perspective, findings justify proposals put forward in policy community and implemented in EU to introduce DPLs. Notes of caution: Bank business models have undergone changes over the past few decades and the nature of our experimental setting renders it infeasible to use more recent data. Results may not extend to banks that are subject to the SSM due to different liability composition. We do not claim that depositor preference is a panacea to constrain bank risk taking. Step-by-step adoption of DPLs can be considered a useful source of exogenous variation in the monitoring incentives of debtholders for further empirical work. 18

19 19

20 Political economy of enacting depositor preference laws (Linear probability models) Dependent variable: Depositor preference law dummy State-chartered assets (-0.47) (-0.53) S&L crisis (1.25) (1.18) Assets in all failed banks (1.15) (1.10) Bank profitability Democrat governor (0.61) (0.53) (-0.82) (-0.77) State FE YES YES YES YES Quarter FE YES YES YES YES Observations R 2 2,056 2,056 2,056 2, and control group in quarter prior to depositor preference Difference t-statistic Total interest expenses Interest on deposits Interest on non-deposits Bank size Equity Neither state-level banking conditions nor the political environment nor the collective importance of state-chartered banks predict the adoption of depositor preference. 20

21 Exogeneity Tests: Cox Proportional Hazards Model Total liabilities expenses Expenses on deposits Expenses on non-deposits Insured deposits market Uninsured deposits Non-deposits market share market share share Coefficient Z-stat (0.99) (1.27) (0.34) (0.86) (0.93) (0.35) s YES YES YES YES YES YES State FE YES YES YES YES YES YES Year FE YES YES YES YES YES YES Observations 1,196 1,196 1,196 1,196 1,196 1,196 Z-score (ln) Non-performing loans Leverage Ratio Return on assets (ln) Return on equity (ln) Interest income (ln) Coefficient Z-stat (1.37) (1.64) (0.89) (0.39) (-0.37) (1.19) s YES YES YES YES YES YES State FE YES YES YES YES YES YES Year FE YES YES YES YES YES YES Observations 1,196 1,196 1,196 1,196 1,196 1,196 Adoption of depositor preference is exogenous with respect to the outcomes we study. No reverse causality. 21

.018 Non-performing loans.4.3.2.1.45.4.35 2 0-2 T-tests confirm these results empirically!.017.016.015.014.013 11.4 Leverage ratio -5.")

22 .017 Total interest expenses.017 Expenses on deposits.009 Expenses on non-deposits.75 Insured deposits market share Uninsured deposits market share.5 Non-deposits market share 4 Zscore (ln).018 Non-performing loans T-tests confirm these results empirically! Leverage ratio -5.8 Return on assets (ln) -3.5 Return on equity (ln) -3 Interest income/total loans (ln)

23 23

Debt Priority Structure, Market Discipline and Bank Conduct

Debt Priority Structure, Market Discipline and Bank Conduct Piotr Danisewicz University of Bristol School of Economics, Finance, and Management Tyndall Avenue Bristol BS8 1TH, UK Danny McGowan University

Debt Priority Structure, Market Discipline and Bank Conduct Piotr Danisewicz University of Bristol School of Economics, Finance, and Management Tyndall Avenue Bristol BS8 1TH, UK Danny McGowan University

Bail-ins: Does Assigning Priority to Deposits Affect Bank Conduct?

Bail-ins: Does Assigning Priority to Deposits Affect Bank Conduct? Piotr Danisewicz, Danny McGowan, Enrico Onali and Klaus Schaeck * Abstract We exploit plausibly exogenous variation in the priority of

Bail-ins: Does Assigning Priority to Deposits Affect Bank Conduct? Piotr Danisewicz, Danny McGowan, Enrico Onali and Klaus Schaeck * Abstract We exploit plausibly exogenous variation in the priority of

Debt Priority Structure and Bank Earnings Opacity

Debt Priority Structure and Bank Earnings Opacity Abstract We examine how changes in debt priority structure that expose junior creditors to greater risk in the event of bankruptcy and thereby give them

Debt Priority Structure and Bank Earnings Opacity Abstract We examine how changes in debt priority structure that expose junior creditors to greater risk in the event of bankruptcy and thereby give them

Depositor Runs and Financial Literacy by Kim

Depositor Runs and Financial Literacy by Kim Discussant: Andres Liberman (NYU) FRS 2016 June 3, 2016 Summary of the paper Question: does depositor behavior during a bank run vary with financial literacy?

Depositor Runs and Financial Literacy by Kim Discussant: Andres Liberman (NYU) FRS 2016 June 3, 2016 Summary of the paper Question: does depositor behavior during a bank run vary with financial literacy?

The relation between bank losses & loan supply an analysis using panel data

The relation between bank losses & loan supply an analysis using panel data Monika Turyna & Thomas Hrdina Department of Economics, University of Vienna June 2009 Topic IMF Working Paper 232 (2008) by Erlend

The relation between bank losses & loan supply an analysis using panel data Monika Turyna & Thomas Hrdina Department of Economics, University of Vienna June 2009 Topic IMF Working Paper 232 (2008) by Erlend

The End of Market Discipline? Investor Expectations of Implicit State Guarantees

The Investor Expectations of Implicit State Guarantees Viral Acharya New York University World Bank, Virginia Tech A. Joseph Warburton Syracuse University Motivation Federal Reserve Chairman Bernanke (2013):

The Investor Expectations of Implicit State Guarantees Viral Acharya New York University World Bank, Virginia Tech A. Joseph Warburton Syracuse University Motivation Federal Reserve Chairman Bernanke (2013):

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking?

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Banks as Patient Lenders: Evidence from a Tax Reform

Banks as Patient Lenders: Evidence from a Tax Reform Elena Carletti Filippo De Marco Vasso Ioannidou Enrico Sette Bocconi University Bocconi University Lancaster University Banca d Italia Investment in

Banks as Patient Lenders: Evidence from a Tax Reform Elena Carletti Filippo De Marco Vasso Ioannidou Enrico Sette Bocconi University Bocconi University Lancaster University Banca d Italia Investment in

Trading and Enforcing Patent Rights. Carlos J. Serrano University of Toronto and NBER

Trading and Enforcing Patent Rights Alberto Galasso University of Toronto Mark Schankerman London School of Economics and CEPR Carlos J. Serrano University of Toronto and NBER OECD-KNOWINNO Workshop @

Trading and Enforcing Patent Rights Alberto Galasso University of Toronto Mark Schankerman London School of Economics and CEPR Carlos J. Serrano University of Toronto and NBER OECD-KNOWINNO Workshop @

The Effects of Supervision on Bank Performance: Evidence from Discontinuous Examination Frequencies

The Effects of Supervision on Bank Performance: Evidence from Discontinuous Examination Frequencies Marcelo Rezende and Jason Wu 1 Federal Reserve Board 1 The views expressed herein are my own and do not

The Effects of Supervision on Bank Performance: Evidence from Discontinuous Examination Frequencies Marcelo Rezende and Jason Wu 1 Federal Reserve Board 1 The views expressed herein are my own and do not

Financial institutions after the crisis: facing new challenges and new regulatory frameworks

Financial institutions after the crisis: facing new challenges and new regulatory frameworks Paris, December 2, 2015 Banque de France, Conference Center, Auditorium 31 rue Croix des Petits Champs, 75001

Financial institutions after the crisis: facing new challenges and new regulatory frameworks Paris, December 2, 2015 Banque de France, Conference Center, Auditorium 31 rue Croix des Petits Champs, 75001

Depositor Discipline of Mutual Savings Banks in Korea

Depositor Discipline of Mutual Savings Banks in Korea Abstract MinHwan Lee College of Business Administration, Inha University, Incheon, Korea, 402-751, E-mail: skymh@inha.ac.kr This paper verified whether

Depositor Discipline of Mutual Savings Banks in Korea Abstract MinHwan Lee College of Business Administration, Inha University, Incheon, Korea, 402-751, E-mail: skymh@inha.ac.kr This paper verified whether

International Spillovers and Local Credit Cycles

International Spillovers and Local Credit Cycles Yusuf Soner Baskaya Julian di Giovanni Şebnem Kalemli-Özcan Mehmet Fatih Ulu Comments by Sole Martinez Peria Macro-Financial Division IMF Prepared for the

International Spillovers and Local Credit Cycles Yusuf Soner Baskaya Julian di Giovanni Şebnem Kalemli-Özcan Mehmet Fatih Ulu Comments by Sole Martinez Peria Macro-Financial Division IMF Prepared for the

Borrower Distress and Debt Relief: Evidence From A Natural Experiment

Borrower Distress and Debt Relief: Evidence From A Natural Experiment Krishnamurthy Subramanian a Prasanna Tantri a Saptarshi Mukherjee b (a) Indian School of Business (b) Stern School of Business, NYU

Borrower Distress and Debt Relief: Evidence From A Natural Experiment Krishnamurthy Subramanian a Prasanna Tantri a Saptarshi Mukherjee b (a) Indian School of Business (b) Stern School of Business, NYU

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1 Valentina Bruno, Ilhyock Shim and Hyun Song Shin 2 Abstract We assess the effectiveness of macroprudential policies

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1 Valentina Bruno, Ilhyock Shim and Hyun Song Shin 2 Abstract We assess the effectiveness of macroprudential policies

Mortgage Rates, Household Balance Sheets, and Real Economy

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Investment of financially distressed firms: the role of trade credit

Investment of financially distressed firms: the role of trade credit Annalisa Ferrando ECB Marcin Wolski EIB ECB, 11 July 2018 The opinions expressed herein are those of the authors and do not necessarily

Investment of financially distressed firms: the role of trade credit Annalisa Ferrando ECB Marcin Wolski EIB ECB, 11 July 2018 The opinions expressed herein are those of the authors and do not necessarily

Wholesale funding runs

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris The Development of Securities Markets. Trends, risks and policies Bocconi - Consob Feb. 2016 Motivation Wholesale funding growing source

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris The Development of Securities Markets. Trends, risks and policies Bocconi - Consob Feb. 2016 Motivation Wholesale funding growing source

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Firing Costs, Employment and Misallocation

Firing Costs, Employment and Misallocation Evidence from Randomly Assigned Judges Omar Bamieh University of Vienna November 13th 2018 1 / 27 Why should we care about firing costs? Firing costs make it

Firing Costs, Employment and Misallocation Evidence from Randomly Assigned Judges Omar Bamieh University of Vienna November 13th 2018 1 / 27 Why should we care about firing costs? Firing costs make it

Discussion of: Banks Incentives and Quality of Internal Risk Models

Discussion of: Banks Incentives and Quality of Internal Risk Models by Matthew C. Plosser and Joao A. C. Santos Philipp Schnabl 1 1 NYU Stern, NBER and CEPR Chicago University October 2, 2015 Motivation

Discussion of: Banks Incentives and Quality of Internal Risk Models by Matthew C. Plosser and Joao A. C. Santos Philipp Schnabl 1 1 NYU Stern, NBER and CEPR Chicago University October 2, 2015 Motivation

Providing Protection or Encouraging Holdup? The Effects of Labor Unions on Innovation

Providing Protection or Encouraging Holdup? The Effects of Labor Unions on Innovation Daniel Bradley, University of South Florida Incheol Kim, University of South Florida Xuan Tian, Indiana University

Providing Protection or Encouraging Holdup? The Effects of Labor Unions on Innovation Daniel Bradley, University of South Florida Incheol Kim, University of South Florida Xuan Tian, Indiana University

Financial Liberalization and Neighbor Coordination

Financial Liberalization and Neighbor Coordination Arvind Magesan and Jordi Mondria January 31, 2011 Abstract In this paper we study the economic and strategic incentives for a country to financially liberalize

Financial Liberalization and Neighbor Coordination Arvind Magesan and Jordi Mondria January 31, 2011 Abstract In this paper we study the economic and strategic incentives for a country to financially liberalize

Bank Leverage and Monetary Policy s Risk-Taking Channel: Evidence from the United States

Bank Leverage and Monetary Policy s Risk-Taking Channel: Evidence from the United States by Giovanni Dell Ariccia (IMF and CEPR) Luc Laeven (IMF and CEPR) Gustavo Suarez (Federal Reserve Board) CSEF Unicredit

Bank Leverage and Monetary Policy s Risk-Taking Channel: Evidence from the United States by Giovanni Dell Ariccia (IMF and CEPR) Luc Laeven (IMF and CEPR) Gustavo Suarez (Federal Reserve Board) CSEF Unicredit

The impact of accounting standards on the allocation of pension assets

Christian Barthelme, Siemens Group Vicky Kiosse, University of Exeter Thorsten Sellhorn, LMU Munich christian.barthelme@whu.edu p.kiosse@exeter.ac.uk sellhorn@bwl.lmu.de The impact of accounting standards

Christian Barthelme, Siemens Group Vicky Kiosse, University of Exeter Thorsten Sellhorn, LMU Munich christian.barthelme@whu.edu p.kiosse@exeter.ac.uk sellhorn@bwl.lmu.de The impact of accounting standards

Empirical Methods for Corporate Finance

Empirical Methods for Corporate Finance Difference in Differences Note: This set of slides is inspired by that of Michael R. Roberts at Wharton Basics (As said earlier) one of the most causes of endogeneity

Empirical Methods for Corporate Finance Difference in Differences Note: This set of slides is inspired by that of Michael R. Roberts at Wharton Basics (As said earlier) one of the most causes of endogeneity

CORPORATE TAX INCENTIVES AND CAPITAL STRUCTURE: EVIDENCE FROM UK TAX RETURN DATA

CORPORATE TAX INCENTIVES AND CAPITAL STRUCTURE: EVIDENCE FROM UK TAX RETURN DATA Jing Xing, Giorgia Maffini, and Michael Devereux Centre for Business Taxation Saïd Business School University of Oxford

CORPORATE TAX INCENTIVES AND CAPITAL STRUCTURE: EVIDENCE FROM UK TAX RETURN DATA Jing Xing, Giorgia Maffini, and Michael Devereux Centre for Business Taxation Saïd Business School University of Oxford

Unconventional Monetary Policy and Bank Lending Relationships

Unconventional Monetary Policy and Bank Lending Relationships Christophe Cahn 1 Anne Duquerroy 1 William Mullins 2 1 Banque de France 2 University of Maryland BdF-BdI Workshop - June 9, 2017 1 / 43 Motivation

Unconventional Monetary Policy and Bank Lending Relationships Christophe Cahn 1 Anne Duquerroy 1 William Mullins 2 1 Banque de France 2 University of Maryland BdF-BdI Workshop - June 9, 2017 1 / 43 Motivation

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1 Sumit Agarwal Georgetown University Amit Bubna Cornerstone Research Molly Lipscomb University of Virginia Abstract The within-month

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1 Sumit Agarwal Georgetown University Amit Bubna Cornerstone Research Molly Lipscomb University of Virginia Abstract The within-month

A Fistful of Dollars: Lobbying and the Financial Crisis

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

The Role of Foreign Banks in Trade

The Role of Foreign Banks in Trade Stijn Claessens (Federal Reserve Board & CEPR) Omar Hassib (Maastricht University) Neeltje van Horen (De Nederlandsche Bank & CEPR) RIETI-MoFiR-Hitotsubashi-JFC International

The Role of Foreign Banks in Trade Stijn Claessens (Federal Reserve Board & CEPR) Omar Hassib (Maastricht University) Neeltje van Horen (De Nederlandsche Bank & CEPR) RIETI-MoFiR-Hitotsubashi-JFC International

The Labor Market Consequences of Adverse Financial Shocks

The Labor Market Consequences of Adverse Financial Shocks November 2012 Unemployment rate on the two sides of the Atlantic Credit to the private sector over GDP Credit to private sector as a percentage

The Labor Market Consequences of Adverse Financial Shocks November 2012 Unemployment rate on the two sides of the Atlantic Credit to the private sector over GDP Credit to private sector as a percentage

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

ADEMU WORKING PAPER SERIES. Deposit Insurance and Bank Risk-Taking

ADEMU WORKING PAPER SERIES Deposit Insurance and Bank Risk-Taking Carolina López-Quiles Centeno ʈ Matic Petricek April 2018 WP 2018/101 www.ademu-project.eu/publications/working-papers Abstract This paper

ADEMU WORKING PAPER SERIES Deposit Insurance and Bank Risk-Taking Carolina López-Quiles Centeno ʈ Matic Petricek April 2018 WP 2018/101 www.ademu-project.eu/publications/working-papers Abstract This paper

Measuring Impact. Impact Evaluation Methods for Policymakers. Sebastian Martinez. The World Bank

Impact Evaluation Measuring Impact Impact Evaluation Methods for Policymakers Sebastian Martinez The World Bank Note: slides by Sebastian Martinez. The content of this presentation reflects the views of

Impact Evaluation Measuring Impact Impact Evaluation Methods for Policymakers Sebastian Martinez The World Bank Note: slides by Sebastian Martinez. The content of this presentation reflects the views of

Asymmetric information and the securitisation of SME loans

Asymmetric information and the securitisation of SME loans Ugo Albertazzi (ECB), Margherita Bottero (Bank of Italy), Leonardo Gambacorta (BIS) and Steven Ongena (U. of Zurich) 1st Annual Workshop of the

Asymmetric information and the securitisation of SME loans Ugo Albertazzi (ECB), Margherita Bottero (Bank of Italy), Leonardo Gambacorta (BIS) and Steven Ongena (U. of Zurich) 1st Annual Workshop of the

Empirical Methods for Corporate Finance. Panel Data, Fixed Effects, and Standard Errors

Empirical Methods for Corporate Finance Panel Data, Fixed Effects, and Standard Errors The use of panel datasets Source: Bowen, Fresard, and Taillard (2014) 4/20/2015 2 The use of panel datasets Source:

Empirical Methods for Corporate Finance Panel Data, Fixed Effects, and Standard Errors The use of panel datasets Source: Bowen, Fresard, and Taillard (2014) 4/20/2015 2 The use of panel datasets Source:

WHAT HAPPENED TO LONG TERM EMPLOYMENT? ONLINE APPENDIX

WHAT HAPPENED TO LONG TERM EMPLOYMENT? ONLINE APPENDIX This appendix contains additional analyses that are mentioned in the paper but not reported in full due to space constraints. I also provide more

WHAT HAPPENED TO LONG TERM EMPLOYMENT? ONLINE APPENDIX This appendix contains additional analyses that are mentioned in the paper but not reported in full due to space constraints. I also provide more

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil. International Monetary Fund

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil International Monetary Fund September, 2008 Motivation Goal of the Paper Outline Systemic

How Do Exchange Rate Regimes A ect the Corporate Sector s Incentives to Hedge Exchange Rate Risk? Herman Kamil International Monetary Fund September, 2008 Motivation Goal of the Paper Outline Systemic

Managing Trade: Evidence from China and the US

Managing Trade: Evidence from China and the US Nick Bloom, Stanford & NBER Kalina Manova, Stanford, Oxford, NBER & CEPR John Van Reenen, London School of Economics & CEP Zhihong Yu, Nottingham National

Managing Trade: Evidence from China and the US Nick Bloom, Stanford & NBER Kalina Manova, Stanford, Oxford, NBER & CEPR John Van Reenen, London School of Economics & CEP Zhihong Yu, Nottingham National

Howard Bodenhorn Clemson University and NBER FRB-Atlanta May 2015

DOUBLE LIABILITY AT EARLY AMERICAN BANKS Howard Bodenhorn Clemson University and NBER FRB-Atlanta May 2015 LIMITED AND EXTENDED LIABILITY Limited liability is one of the defining characteristics of modern

DOUBLE LIABILITY AT EARLY AMERICAN BANKS Howard Bodenhorn Clemson University and NBER FRB-Atlanta May 2015 LIMITED AND EXTENDED LIABILITY Limited liability is one of the defining characteristics of modern

The Time Cost of Documents to Trade

The Time Cost of Documents to Trade Mohammad Amin* May, 2011 The paper shows that the number of documents required to export and import tend to increase the time cost of shipments. However, this relationship

The Time Cost of Documents to Trade Mohammad Amin* May, 2011 The paper shows that the number of documents required to export and import tend to increase the time cost of shipments. However, this relationship

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables

Appendix A: Appendix Figures and Tables") ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

Internet Appendix for Does Banking Competition Affect Innovation? 1. Additional robustness checks

Internet Appendix for Does Banking Competition Affect Innovation? This internet appendix provides robustness tests and supplemental analyses to the main results presented in Does Banking Competition Affect

Internet Appendix for Does Banking Competition Affect Innovation? This internet appendix provides robustness tests and supplemental analyses to the main results presented in Does Banking Competition Affect

Peer Effects in Retirement Decisions

Peer Effects in Retirement Decisions Mario Meier 1 & Andrea Weber 2 1 University of Mannheim 2 Vienna University of Economics and Business, CEPR, IZA Meier & Weber (2016) Peers in Retirement 1 / 35 Motivation

Peer Effects in Retirement Decisions Mario Meier 1 & Andrea Weber 2 1 University of Mannheim 2 Vienna University of Economics and Business, CEPR, IZA Meier & Weber (2016) Peers in Retirement 1 / 35 Motivation

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects Manju Puri (Duke) Jörg Rocholl (ESMT) Sascha Steffen (Mannheim) 3rd Unicredit Group Conference

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects Manju Puri (Duke) Jörg Rocholl (ESMT) Sascha Steffen (Mannheim) 3rd Unicredit Group Conference

Migration Responses to Household Income Shocks: Evidence from Kyrgyzstan

Migration Responses to Household Income Shocks: Evidence from Kyrgyzstan Katrina Kosec Senior Research Fellow International Food Policy Research Institute Development Strategy and Governance Division Joint

Migration Responses to Household Income Shocks: Evidence from Kyrgyzstan Katrina Kosec Senior Research Fellow International Food Policy Research Institute Development Strategy and Governance Division Joint

Bank Capital and Lending: Evidence from Syndicated Loans

Bank Capital and Lending: Evidence from Syndicated Loans Yongqiang Chu, Donghang Zhang, and Yijia Zhao This Version: June, 2014 Abstract Using a large sample of bank-loan-borrower matched dataset of individual

Bank Capital and Lending: Evidence from Syndicated Loans Yongqiang Chu, Donghang Zhang, and Yijia Zhao This Version: June, 2014 Abstract Using a large sample of bank-loan-borrower matched dataset of individual

Policy Evaluation: Methods for Testing Household Programs & Interventions

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

The Labor Market Consequences of Adverse Financial Shocks

13TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 8 9, 2012 The Labor Market Consequences of Adverse Financial Shocks Tito Boeri Bocconi University and frdb Pietro Garibaldi University of Torino and

13TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 8 9, 2012 The Labor Market Consequences of Adverse Financial Shocks Tito Boeri Bocconi University and frdb Pietro Garibaldi University of Torino and

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

Small Bank Comparative Advantages in Alleviating Financial Constraints and Providing Liquidity Insurance over Time

Small Bank Comparative Advantages in Alleviating Financial Constraints and Providing Liquidity Insurance over Time Allen N. Berger University of South Carolina Wharton Financial Institutions Center European

Small Bank Comparative Advantages in Alleviating Financial Constraints and Providing Liquidity Insurance over Time Allen N. Berger University of South Carolina Wharton Financial Institutions Center European

Banks Incentives and the Quality of Internal Risk Models

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics

Henrik Jacobsen Kleven London School of Economics") LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

The Origins of Italian NPLs

The Origins of Italian NPLs by Paolo Angelini, Marcello Bofondi, and Luigi Zingales Discussion at the BIS Annual Conference in Lucerne, June 23 2017 By Viral V. Acharya Reserve Bank of India [Views reflected

The Origins of Italian NPLs by Paolo Angelini, Marcello Bofondi, and Luigi Zingales Discussion at the BIS Annual Conference in Lucerne, June 23 2017 By Viral V. Acharya Reserve Bank of India [Views reflected

Interstate Banking Deregulation and Bank Loan Commitments

Interstate Banking Deregulation and Bank Loan Commitments FRBSF/BEJM Conference on Empirical Macroeconomics Using Geographical Data Ki Young Park School of Economics Yonsei University March 18, 2011 Ki

Interstate Banking Deregulation and Bank Loan Commitments FRBSF/BEJM Conference on Empirical Macroeconomics Using Geographical Data Ki Young Park School of Economics Yonsei University March 18, 2011 Ki

TRADE COLLAPSE DURING THE 2009 CRISIS: HOW DID EUROPEAN COMPANIES FARE? LESSONS FROM

TRADE COLLAPSE DURING THE 2009 CRISIS: HOW DID EUROPEAN COMPANIES FARE? LESSONS FROM SEVEN COUNTRIES Gábor Békés, Miklós Koren, Balázs Muraközy & László Halpern (Institute of Economics, Hungarian Academy

TRADE COLLAPSE DURING THE 2009 CRISIS: HOW DID EUROPEAN COMPANIES FARE? LESSONS FROM SEVEN COUNTRIES Gábor Békés, Miklós Koren, Balázs Muraközy & László Halpern (Institute of Economics, Hungarian Academy

* CONTACT AUTHOR: (T) , (F) , -

, (F) , -") Agricultural Bank Efficiency and the Role of Managerial Risk Preferences Bernard Armah * Timothy A. Park Department of Agricultural & Applied Economics 306 Conner Hall University of Georgia Athens, GA

Agricultural Bank Efficiency and the Role of Managerial Risk Preferences Bernard Armah * Timothy A. Park Department of Agricultural & Applied Economics 306 Conner Hall University of Georgia Athens, GA

MA Advanced Macroeconomics 3. Examples of VAR Studies

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

Non-Performing Loans and the Supply of Bank Credit: Evidence from Italy

Non-Performing Loans and the Supply of Bank Credit: Evidence from Italy M Accornero P Alessandri L Carpinelli A M Sorrentino First ESCB Workshop on Financial Stability November 2 th - 3 rd, 2017 Disclaimer:

Non-Performing Loans and the Supply of Bank Credit: Evidence from Italy M Accornero P Alessandri L Carpinelli A M Sorrentino First ESCB Workshop on Financial Stability November 2 th - 3 rd, 2017 Disclaimer:

Does the interest rate for business loans respond asymmetrically to changes in the cash rate?

University of Wollongong Research Online Faculty of Commerce - Papers (Archive) Faculty of Business 2013 Does the interest rate for business loans respond asymmetrically to changes in the cash rate? Abbas

University of Wollongong Research Online Faculty of Commerce - Papers (Archive) Faculty of Business 2013 Does the interest rate for business loans respond asymmetrically to changes in the cash rate? Abbas

Why Do Firms Evade Taxes? The Role of Information Sharing and Financial Sector Outreach The Journal of Finance. Thorsten Beck Chen Lin Yue Ma

Why Do Firms Evade Taxes? The Role of Information Sharing and Financial Sector Outreach The Journal of Finance Thorsten Beck Chen Lin Yue Ma Motivation Financial deepening is pro-growth This literature

Why Do Firms Evade Taxes? The Role of Information Sharing and Financial Sector Outreach The Journal of Finance Thorsten Beck Chen Lin Yue Ma Motivation Financial deepening is pro-growth This literature

Stronger Risk Controls, Lower Risk: Evidence from U.S. Bank Holding Companies

Stronger Risk Controls, Lower Risk: Evidence from U.S. Bank Holding Companies Andrew Ellul 1 Vijay Yerramilli 2 1 Kelley School of Business, Indiana University 2 C. T. Bauer College of Business, University

Stronger Risk Controls, Lower Risk: Evidence from U.S. Bank Holding Companies Andrew Ellul 1 Vijay Yerramilli 2 1 Kelley School of Business, Indiana University 2 C. T. Bauer College of Business, University

Trinity College and Darwin College. University of Cambridge. Taking the Art out of Smart Beta. Ed Fishwick, Cherry Muijsson and Steve Satchell

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

In Debt and Approaching Retirement: Claim Social Security or Work Longer?

AEA Papers and Proceedings 2018, 108: 401 406 https://doi.org/10.1257/pandp.20181116 In Debt and Approaching Retirement: Claim Social Security or Work Longer? By Barbara A. Butrica and Nadia S. Karamcheva*

AEA Papers and Proceedings 2018, 108: 401 406 https://doi.org/10.1257/pandp.20181116 In Debt and Approaching Retirement: Claim Social Security or Work Longer? By Barbara A. Butrica and Nadia S. Karamcheva*

PRE CONFERENCE WORKSHOP 3

PRE CONFERENCE WORKSHOP 3 Stress testing operational risk for capital planning and capital adequacy PART 2: Monday, March 18th, 2013, New York Presenter: Alexander Cavallo, NORTHERN TRUST 1 Disclaimer

PRE CONFERENCE WORKSHOP 3 Stress testing operational risk for capital planning and capital adequacy PART 2: Monday, March 18th, 2013, New York Presenter: Alexander Cavallo, NORTHERN TRUST 1 Disclaimer

Financial liberalization and the relationship-specificity of exports *

Financial and the relationship-specificity of exports * Fabrice Defever Jens Suedekum a) University of Nottingham Center of Economic Performance (LSE) GEP and CESifo Mercator School of Management University

Financial and the relationship-specificity of exports * Fabrice Defever Jens Suedekum a) University of Nottingham Center of Economic Performance (LSE) GEP and CESifo Mercator School of Management University

Deposit Insurance and Banks Deposit Rates: Evidence From a EU Policy

Deposit Insurance and Banks Deposit Rates: Evidence From a EU Policy Matteo Gatti Tommaso Oliviero EUI University of Naples and CEF May 1, 2017 Motivation In 2009 EU raised deposit insurance limit to e100,

Deposit Insurance and Banks Deposit Rates: Evidence From a EU Policy Matteo Gatti Tommaso Oliviero EUI University of Naples and CEF May 1, 2017 Motivation In 2009 EU raised deposit insurance limit to e100,

CHAPTER 2 LITERATURE REVIEW. Modigliani and Miller (1958) in their original work prove that under a restrictive set

in their original work prove that under a restrictive set") CHAPTER 2 LITERATURE REVIEW 2.1 Background on capital structure Modigliani and Miller (1958) in their original work prove that under a restrictive set of assumptions, capital structure is irrelevant. This

CHAPTER 2 LITERATURE REVIEW 2.1 Background on capital structure Modigliani and Miller (1958) in their original work prove that under a restrictive set of assumptions, capital structure is irrelevant. This

COMMENTS ON SESSION 1 AUTOMATIC STABILISERS AND DISCRETIONARY FISCAL POLICY. Adi Brender *

COMMENTS ON SESSION 1 AUTOMATIC STABILISERS AND DISCRETIONARY FISCAL POLICY Adi Brender * 1 Key analytical issues for policy choice and design A basic question facing policy makers at the outset of a crisis

COMMENTS ON SESSION 1 AUTOMATIC STABILISERS AND DISCRETIONARY FISCAL POLICY Adi Brender * 1 Key analytical issues for policy choice and design A basic question facing policy makers at the outset of a crisis

The real effects of regulatory enforcement actions: Evidence from U.S. counties

The real effects of regulatory enforcement actions: Evidence from U.S. counties Piotr Danisewicz Bangor Business School, Bangor University Danny McGowan Bangor Business School, Bangor University Enrico

The real effects of regulatory enforcement actions: Evidence from U.S. counties Piotr Danisewicz Bangor Business School, Bangor University Danny McGowan Bangor Business School, Bangor University Enrico

Corporate Investment and the Real Exchange Rate

Corporate Investment and the Real Exchange Rate Mai Dao Camelia Minoiu Jonathan D. Ostry Research Department, IMF* 21-22 April, 2016 *The views expressed herein are those of the authors and should not

Corporate Investment and the Real Exchange Rate Mai Dao Camelia Minoiu Jonathan D. Ostry Research Department, IMF* 21-22 April, 2016 *The views expressed herein are those of the authors and should not

RESPONSE EMPIRICALLY VALIDATING THE POLICE LIABILITY INSURANCE CLAIM. Andrea Cann Chandrasekher

RESPONSE EMPIRICALLY VALIDATING THE POLICE LIABILITY INSURANCE CLAIM Andrea Cann Chandrasekher INTRODUCTION Professor John Rappaport s paper is an innovative study of police misconduct and the possible

RESPONSE EMPIRICALLY VALIDATING THE POLICE LIABILITY INSURANCE CLAIM Andrea Cann Chandrasekher INTRODUCTION Professor John Rappaport s paper is an innovative study of police misconduct and the possible

Sovereign Distress, Bank Strength and Performance:

Sovereign Distress, Bank Strength and Performance: Evidence from the European Debt Crisis Yifei Cao, Francesc Rodriguez-Tous and Matthew Willison 29 November 2016, Sheffield *The views expressed in this

Sovereign Distress, Bank Strength and Performance: Evidence from the European Debt Crisis Yifei Cao, Francesc Rodriguez-Tous and Matthew Willison 29 November 2016, Sheffield *The views expressed in this

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj The Vanguard Group Rajdeep Sengupta Federal Reserve Bank of St. Louis ECB CFS Research Conference Einaudi

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj The Vanguard Group Rajdeep Sengupta Federal Reserve Bank of St. Louis ECB CFS Research Conference Einaudi

Center for the Study of Financial Regulation

The at the University of Notre Dame has as its mission to promote sound economic analysis of current and proposed financial regulation. Poorly conceived financial regulations can impose large costs on

The at the University of Notre Dame has as its mission to promote sound economic analysis of current and proposed financial regulation. Poorly conceived financial regulations can impose large costs on

Motivation Literature overview Constructing public capital stocks Stylized facts Empirical model and estimation strategy Estimation results Policy

Efficiency-Adjusted Public Capital and Growth IMF-WB Conference on Fiscal Policy, Equity, and Long-Term Growth in Developing Countries Sanjeev Gupta April 21, 2013 1 Outline of Presentation Motivation

Efficiency-Adjusted Public Capital and Growth IMF-WB Conference on Fiscal Policy, Equity, and Long-Term Growth in Developing Countries Sanjeev Gupta April 21, 2013 1 Outline of Presentation Motivation

The Persistent Effect of Temporary Affirmative Action: Online Appendix

The Persistent Effect of Temporary Affirmative Action: Online Appendix Conrad Miller Contents A Extensions and Robustness Checks 2 A. Heterogeneity by Employer Size.............................. 2 A.2

The Persistent Effect of Temporary Affirmative Action: Online Appendix Conrad Miller Contents A Extensions and Robustness Checks 2 A. Heterogeneity by Employer Size.............................. 2 A.2

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY Daniel Dejuan and Corinna Ghirelli Bank of Spain European Network for Research on Investment EIB - Luxemburg 9 April 018 DG ECONOMICS,

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY Daniel Dejuan and Corinna Ghirelli Bank of Spain European Network for Research on Investment EIB - Luxemburg 9 April 018 DG ECONOMICS,

Liquidity Risk and U.S. Bank Lending at Home and Abroad Ricardo Correa, Linda Goldberg, and Tara Rice

Liquidity Risk and U.S. Bank Lending at Home and Abroad Ricardo Correa, Linda Goldberg, and Tara Rice June 2014 Views expressed are those of the author and do not necessarily reflect the position of the

Liquidity Risk and U.S. Bank Lending at Home and Abroad Ricardo Correa, Linda Goldberg, and Tara Rice June 2014 Views expressed are those of the author and do not necessarily reflect the position of the

The lender of last resort: liquidity provision versus the possibility of bail-out

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

BANK RISK-TAKING AND CAPITAL REQUIREMENTS

BANK RISK-TAKING AND CAPITAL REQUIREMENTS Rebeca Anguren Gabriel Jiménez * February 2017 Abstract In this paper we empirically investigate the effect of the increase in regulatory capital requirements

BANK RISK-TAKING AND CAPITAL REQUIREMENTS Rebeca Anguren Gabriel Jiménez * February 2017 Abstract In this paper we empirically investigate the effect of the increase in regulatory capital requirements

Empirical Approaches in Public Finance. Hilary Hoynes EC230. Outline of Lecture:

Lecture: Empirical Approaches in Public Finance Hilary Hoynes hwhoynes@ucdavis.edu EC230 Outline of Lecture: 1. Statement of canonical problem a. Challenges for causal identification 2. Non-experimental

Lecture: Empirical Approaches in Public Finance Hilary Hoynes hwhoynes@ucdavis.edu EC230 Outline of Lecture: 1. Statement of canonical problem a. Challenges for causal identification 2. Non-experimental

Capital structure and profitability of firms in the corporate sector of Pakistan

Business Review: (2017) 12(1):50-58 Original Paper Capital structure and profitability of firms in the corporate sector of Pakistan Sana Tauseef Heman D. Lohano Abstract We examine the impact of debt ratios

Business Review: (2017) 12(1):50-58 Original Paper Capital structure and profitability of firms in the corporate sector of Pakistan Sana Tauseef Heman D. Lohano Abstract We examine the impact of debt ratios

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals Stockholm School of Economics Dilip Mookherjee Boston University Sujata Visaria Boston University

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals Stockholm School of Economics Dilip Mookherjee Boston University Sujata Visaria Boston University

How exogenous is exogenous income? A longitudinal study of lottery winners in the UK

How exogenous is exogenous income? A longitudinal study of lottery winners in the UK Dita Eckardt London School of Economics Nattavudh Powdthavee CEP, London School of Economics and MIASER, University

How exogenous is exogenous income? A longitudinal study of lottery winners in the UK Dita Eckardt London School of Economics Nattavudh Powdthavee CEP, London School of Economics and MIASER, University

Wholesale funding dry-ups

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris MIT HEC Paris 12th Annual Central Bank Microstructure Workshop Banque de France September 2016 Motivation Wholesale funding: A growing source

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris MIT HEC Paris 12th Annual Central Bank Microstructure Workshop Banque de France September 2016 Motivation Wholesale funding: A growing source

Exam. ECON 4624 Empirical Public Economics. (a) Consider the budget contraint in Figure 1 below. What are the expected effects on

Consider the budget contraint in Figure 1 below. What are the expected effects on") Exam ECON 4624 Empirical Public Economics This exercise set consists of five (5) pages. Exercise 1 (50%) Kostøl and Mogstad (2014, American Economic Review) study the impact of financial incentives on

Exam ECON 4624 Empirical Public Economics This exercise set consists of five (5) pages. Exercise 1 (50%) Kostøl and Mogstad (2014, American Economic Review) study the impact of financial incentives on

Investment and Employment Responses to State Adoption of Federal Accelerated Depreciation Policies

Investment and Employment Responses to State Adoption of Federal Accelerated Depreciation Policies Eric Ohrn Grinnell College 72nd Annual Congress of the IIPF August 10, 2016 Introduction During the 2000s,

Investment and Employment Responses to State Adoption of Federal Accelerated Depreciation Policies Eric Ohrn Grinnell College 72nd Annual Congress of the IIPF August 10, 2016 Introduction During the 2000s,

Additional Evidence and Replication Code for Analyzing the Effects of Minimum Wage Increases Enacted During the Great Recession

ESSPRI Working Paper Series Paper #20173 Additional Evidence and Replication Code for Analyzing the Effects of Minimum Wage Increases Enacted During the Great Recession Economic Self-Sufficiency Policy

ESSPRI Working Paper Series Paper #20173 Additional Evidence and Replication Code for Analyzing the Effects of Minimum Wage Increases Enacted During the Great Recession Economic Self-Sufficiency Policy

May 19, Abstract

LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Boston College gatev@bc.edu Philip E. Strahan Boston College, Wharton Financial Institutions Center & NBER philip.strahan@bc.edu May 19, 2008 Abstract

LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Boston College gatev@bc.edu Philip E. Strahan Boston College, Wharton Financial Institutions Center & NBER philip.strahan@bc.edu May 19, 2008 Abstract

Credit Constraints and Search Frictions in Consumer Credit Markets

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

Appendices. A Simple Model of Contagion in Venture Capital

Appendices A A Simple Model of Contagion in Venture Capital Given the structure of venture capital financing just described, the potential mechanisms by which shocks might propagate across companies in

Appendices A A Simple Model of Contagion in Venture Capital Given the structure of venture capital financing just described, the potential mechanisms by which shocks might propagate across companies in

US real interest rates and default risk in emerging economies

US real interest rates and default risk in emerging economies Nathan Foley-Fisher Bernardo Guimaraes August 2009 Abstract We empirically analyse the appropriateness of indexing emerging market sovereign

US real interest rates and default risk in emerging economies Nathan Foley-Fisher Bernardo Guimaraes August 2009 Abstract We empirically analyse the appropriateness of indexing emerging market sovereign

Regulating Household Leverage

Regulating Household Leverage Anthony A. DeFusco Stephanie Johnson John Mondragon Northwestern University December 2016 DeFusco, Johnson, Mondragon Regulating Household Leverage 1 / 31 Household Leverage

Regulating Household Leverage Anthony A. DeFusco Stephanie Johnson John Mondragon Northwestern University December 2016 DeFusco, Johnson, Mondragon Regulating Household Leverage 1 / 31 Household Leverage

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Skin in the game, wealth and risk-taking: Evidence from private equity funds

Skin in the game, wealth and risk-taking: Evidence from private equity funds Carsten Bienz, Norwegian School of Economics Karin Thorburn, Norwegian School of Economics, CEPR, ECGI Uwe Walz, Goethe University

Skin in the game, wealth and risk-taking: Evidence from private equity funds Carsten Bienz, Norwegian School of Economics Karin Thorburn, Norwegian School of Economics, CEPR, ECGI Uwe Walz, Goethe University

Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Fabian Brunner & Nicolas Boob

![Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Fabian Brunner & Nicolas Boob](/thumbs/85/92264989.jpg "Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Fabian Brunner & Nicolas Boob") Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Background and Motivation Rauh (2006): Financial constraints and real investment Endogeneity: Investment

Bakke & Whited [JF 2012] Threshold Events and Identification: A Study of Cash Shortfalls Discussion by Background and Motivation Rauh (2006): Financial constraints and real investment Endogeneity: Investment

14.471: Fall 2012: Recitation 3: Labor Supply: Blundell, Duncan and Meghir EMA (1998)

") 14.471: Fall 2012: Recitation 3: Labor Supply: Blundell, Duncan and Meghir EMA (1998) Daan Struyven September 29, 2012 Questions: How big is the labor supply elasticitiy? How should estimation deal whith

14.471: Fall 2012: Recitation 3: Labor Supply: Blundell, Duncan and Meghir EMA (1998) Daan Struyven September 29, 2012 Questions: How big is the labor supply elasticitiy? How should estimation deal whith