Empirical Methods for Corporate Finance. Panel Data, Fixed Effects, and Standard Errors

|

|

|

- Anthony West

- 6 years ago

- Views:

Transcription

1 Empirical Methods for Corporate Finance Panel Data, Fixed Effects, and Standard Errors

4/20/2015 2")

2 The use of panel datasets Source: Bowen, Fresard, and Taillard (2014) 4/20/2015 2

4/20/2015 3")

3 The use of panel datasets Source: Bowen, Fresard, and Taillard (2014) 4/20/2015 3

4 Basics (As said earlier) There are three main causes of trouble (violation of E(u x) = 0 in OLS) in empirical corporate finance Endogenous explanators Mismeasured explanators Omitted factors (Refresher) Some variable(s) that the econometrician does not observe may be correlated with the dependent and explanatory variable(s) Mainly due to the considerable (unobserved) heterogeneity present in many corporate finance settings Firms can differ in so many ways! (think about it for one second) Panel data can sometimes offer a partial (neither complete nor costless) solution to this problem 4/20/2015 4

5 What is a panel dataset? In panel data, individuals (persons, firms, cities, countries, ) are observed at serveral point in time (days, year, before and after a treatment, ) Notatation: We observe N firms over T period If each firm (i) is observed in all periods (t), the panel is balanced Two main interests in the econometrics of panel data (1) Exploit panel data to control for unobserved time invariant heterogeneity in cross sectional models («fixedeffects») (2) Disentangling components of variance and estimating the transition probability among states (study the dynamics of cross sectional populations) («random effects») In most corporate finance applications, we rely on (1) and estimate fixed effects models 4/20/2015 5

6 General structure of a panel The T observations for firm i can be written as And NT observations for all firms and time periods as 4/20/2015 6

7 Econometric specification: the logic Suppose a cross sectional model of the form («the truth») yi 1 xi 1 ci ui 1 with E( ui 1 xi 1, ci ) 0 If c i is observed then β can be identified from a multiple regression of y on x and c If c i is not observed, causal identification of β requires Lack of correlation between x i1 and c i («random effect») Cov( xi1, yi1) Var( x ) i1 An instrument (z i ) uncorrelated with u i1 and c i Cov( zi Cov( z 1 i, y, x i1 i1 ) ) 4/20/2015 7

8 Econometric specification: the logic Suppose that neither of these two options is available but we observe y i2 and x i2 for the same firm in a second period (T=2) y i2 xi2 ci ui2 with E( uit xi1, xi, 2, ci ) 0 Then β is identified in the regression in first difference even if c i is not observed y y ( xi2 xi1) ( ui,2 u 1) i2 i1 i Taking the first difference eliminate the time invariant unobserved heterogeneity! And Cov( x i2 Var( x, y i2 ) i2 ) The variation that identifies β is within firm variation 4/20/2015 8

9 Illustration This is the line we would fit if we do not account for individual effects (Pooled OLS on a large cross section) This is the «true» unbiased slope (that account for the individual effects) Estimation with pooled OLS is biased and inconsistent! 4/20/2015 9

10 Why might fixed effects arise? Any time invariant individual characteristic that cannot be observed in the data at hand could contribute to the presence of fixed effects In regressions aimed at understanding firm behavior, specific sources of fixed effects depend on the application In capital structure regression (e.g. leverage) a fixed effect might be related to Unobserved technological differences across firms Unobserved ability of the CEO or people deciding on financial policies In general, a fixed effect can capture any low frequency unobserved variable 4/20/

11 Fixed effect models We focus here on static fixed effect models (no lagged dependent variables). The basic model is: ' yit xit ci uit witht 1,...,T Assumption (A1): E(ui xi,ci ) 0 (t 1,...,T) The error at any period is uncorrelated with past, present and future values of x (strict exogeneity assumption) E.g. current values of x are not influenced by past errors Assumption (A2): Var(u x i i,c i ) σ 2 I T Errors are conditionally homoskedastic and not serially correlated Treatment with heteroskedastic is relatively easy (e.g. available in Stata) 4/20/

12 Estimation with fixed effects (1) Under A1 (mean independence), we can estimate the model in first difference by OLS (convenient) OLS estimator will be unbiased and consistent (for large N) This is rarely the case (Cov( u it, u it-1 )isnot zero!) If Cov( u it, u it-1 )isnot zero, the optimal estimator is given by generalized leastsquares (GLS) Take deviation from the mean! Estimate the following (within or FE) specification ~ y it ~ x u~ ' 1 it it with ~ yit yit T T t 1 y it y it y The variation that identifies β is within firm variation Note that the firm specific effect (c i ) dissapears (constant) Time invariant hetegeneity is solved 4/20/

13 Estimation with fixed effects (2) The FE estimator is asymptotically normally distributed so that the usual OLS inference can be applied The usual tests (t, Wald, ) can be used in large and small samples In practice, the error is often likely serially correlated (T >2). This needs to be corrected (using cluster robust standard errors) Note that time invariant regressors (e.g. the constant) cancel so their effect cannot be estimated with a within estimator The FE estimator is numerically identical to pool OLS including a set of N-1 dummy variables which identifies the firms and hence N-1 parameters («Least Squares Dummy Variables Estimator» LSDV) Get estimates for c i The LSDV estimator is generally not consistent as the number of parameter goes to infinity F test for the joint significance of fixed effects (this is useful) 4/20/

14 Alternative: random effects In the FE specification, the firm specific effect (c i ) is allowed to be correlated with the explanatory variables (Note that this is the root of the problem!) If the firm specific effect (c i ) is uncorrelated with the explanatory variables (past, present and future), we have a random effect (RE) specification In RE specification, the emphasis is on the error term The error term has two components (c i +u i ) that are unrelated to the regressors No problem to identify β (identified in the cross section) but the panel structrue is used to identify the variance of c i and u i Used to separate out permanent from transitory components of variation Not many application of RE models in corporate finance 4/20/

15 Fixed or random effects? Intuitively, we should opt for a RE specification if one can be sure that the firm specific effect really is unrelated to the explanatory variables This can be tested using a (Durbin Wu ) Hausmann test Comparision of the FE and RE estimators: H ˆ ˆ ˆ( ˆ ˆ( 2 ( IV OLS )'[ V IV ) V OLS )]( IV OLS ) ~ J ˆ ˆ ˆ Where J is the number of time varying regressors The null hypothesis is that the firm specific effect (c i ) is uncorrelated with the regressors and the errors are equicorrelated 4/20/

16 Implementation in Stata (1) 4/20/

17 Implementation in Stata (2) 4/20/

18 Implementation in Stata (3) 4/20/

19 Practical issues (1) Most of the empirical corporate finance use fixed effects. Is that fine? The answer is not obvious. The use of FE deserves careful thoughts Always try estimations with fixed and random effects and check for statistical significance of the FE Check if the inclusion of fixed effects changes the magnitude of the coefficients in an economically meaningful way The inclusion of fixed effects reduces efficiency Even if the Hausman test rejects the null of random effects, if the economic significance is little changed, using OLS can still be valid E.g. Lemmon, Roberts and Zender (JoF 2008) 4/20/

20 Practical issues (2) Warning: Including fixed effects can exacerbate measurement problems If the dependent variable is a first differenced variable (e.g. investment or change in cash holdings) and if the fixed effect is related to level of the dependent variable, then the fixed effect has already been differenced out of the regression Again, using fixed effect reduces efficiency E.g. fixed effects rarely tend to make important qualitative differences in investment equations If the research question is aimed at understanding cross sectional variation in a variable, then fixed effects defeat this purpose 4/20/

")

21 Coles and Li (2011) 4/20/

22 4/20/

23 4/20/

24 4/20/

25 4/20/

26 4/20/

27 4/20/

(By")

")

28 Graham and Leary (2012) (By traditional determinants) 4/20/

29 Graham and Leary (2012) 4/20/

30 Graham and Leary (2012) 4/20/

31 Application: Managing with style Bertrand and Schoar, 2003, Managing with style: The effect of managers on firm policies (Quarterly Journal of Economics) Question: How much do individual managers matter for firm behavior and economic performance? Motivation: Previous studies focused on firm, industry, and market level characteristics to explain corporate behaviors View in the business press is that (certain) managers are key factors in corporate practices (e.g. Steve Jobs) Can add to our understanding of corporate finance Empirical challenge: Identify/measure the (marginal & causal) impact of managers on firms Empirical strategy: Use managers fixed effects to uncover their impact on various policies (no causal statement here) Results: Managers traits appear to be related to firms choices and performance 4/20/

32 Location in the field Governance Real decisions Financing Valuation Institutional framework: laws, regulations, taxes, markets, macro economy No causal effects here 4/20/

33 Why should manager matter? (in theory) No effect (Null hypothesis) In a purely neoclassical view of the firm, managers are homogenous and selfless inputs into the production process (remember your microeconomic classes ) Managers can differ (preferences, risk aversion, skills, ) but do not affect corporate policies Non zero effect (managers matter) Agency models (principal agent) allow for managers having discretion inside the firm (depend on governance practices only) Some models allow managers to differ Agency perspective (1): Managers may matter if the corporate control is poor or limited (improved) Neoclassical perspective (2): Firms (e.g. boards) select specific managers (endogenous matching) Both approaches predict that managers matter! 4/20/

34 Sample construction Construction of a manager firm matched panel dataset that tracks different managers across different firms and time (why is this key?) Data sources Forbes 800 files ( ) and Execucomp ( ) for the information about CEO (and other top executives) Focus on CEO but also CFO, COO and subdivision CEOs Restrict on the subset of firms for which at least one executive can be observed in at least one other firm (for minimum three years) The resulting sample contains about 600 firms and 500 managers 4/20/

due to data screening Executives from larger firms are more likely to move between COMPUSTAT firms (be in the sample) The effects documented in")

35 Summary statistics (representative?) Firms in the sample are somewhat special (e.g. larger) due to data screening Executives from larger firms are more likely to move between COMPUSTAT firms (be in the sample) The effects documented in the paper may not generalize to smaller (private) firms 4/20/

36 Job transition A large majority of job moves are from «other» to «other» «other» corresponds to operationally important positions 117 CEO moved to another CEO position in another firm! (fired?) 4/20/

: The objective is the get an estimate of the different λs")

They are not after causality (non random allocation of managers across")

37 Panel specification The (FE) specification is as follows (on the CEO firm matched sample): The objective is the get an estimate of the different λs for different y (policies) They use the LSDV estimator (clear why?) They are not after causality (non random allocation of managers across firms) 4/20/

38 Managers fixed effects (investment) CEO fixed effect increase the Adjusted R 2 by 3% in the investment equation This represents the average marginal contribution of CEO fixed effects CEO fixed effect are jointly significant (F Tests are large ) 4/20/

4/20/2015")

39 Managers fixed effect (financing) CEO fixed effect has a rather small effect in leverage equation CEO fixed effect are jointly not significant (F Tests are super small) 4/20/

40 Managers fixed effects (performance) CEO fixed effects are significant in performance equations Controlling for many different things, some CEOs are related to better performance 4/20/

41 Magnitude of the managers fixed effects? Retrieve the estimated managers fixed effect from the LSDV estimation (e.g. in Stata) Some CEO are negatively related to performance! Important heterogeneity across managers 4/20/

We do see consistent patterns (e.")

42 Management styles? Can we detect systematic «styles» among managers fixed effect? (Use simple OLS regression) We do see consistent patterns (e.g internal vs external investment or debt vs cash) 4/20/

43 Fixed effects and compensation Managers fixed effect appear to be related to their compensation! Firms appear to pay a premium for managers who are associated with higher rates of return on assets! 4/20/

44 Managers traits? 4/20/2015 Empircal Corporate Finance 44

45 Conclusion/comments CEO appear to matter CEO Systematically related to corporate policies This has generated a lot of research on WHY do CEO matter (some explanations) Overconfident CEO Connected CEO (political, school, investment bankers, private equity) Financial expertise Original use of fixed effects to answer an interesting question (not a causal question though) This type of approach has been used by others in the literature 4/20/

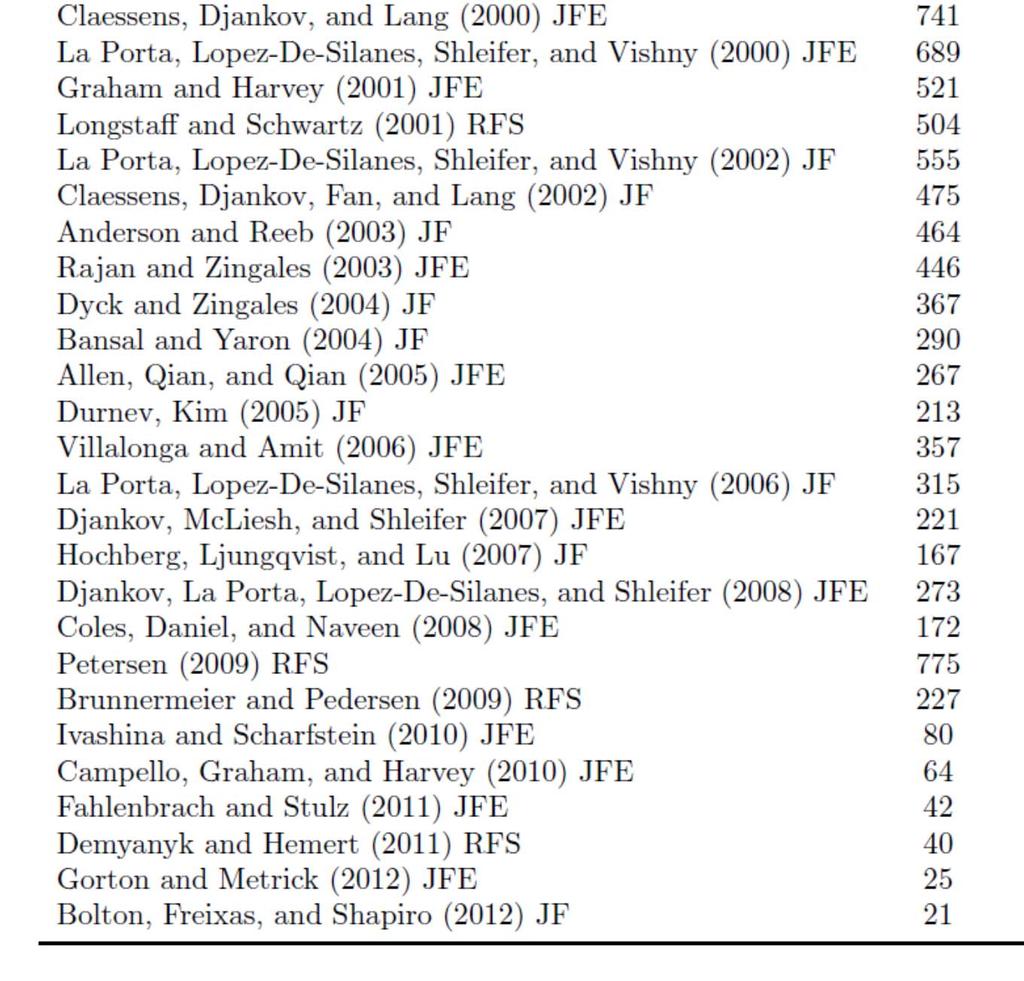

46 Think about Standard Errors! Petersen (2009)

47 Influencial Research?

48 Potential Problem? In panel data, residuals may be correlated across firms and across time (not iid) Why? Consequences? OLS standard errors (hence t stats) can be biased May lead to wrong conclusion Let s see what happens and what can de done 4/20/

49 Pooled OLS Simple panel model (firm i, time t) Assume Cov(X, ε)=0 IID 4/20/

50 Unobserved Firm Fixed Effect Residual becomes: and Correlation within firms but not between firms Continue to assume independence between X and ε

51 True Standard Errors (OLS)? OLS understates true standard errors if ρs are not zero! + Increases in T

52 True Residual Structure

53 How bad it this? Simulation of a panel dataset with a firm fixed effect Repeat this several time to observe true SE SE of y=1 and SE of ε=2 R 2 =20% Change the fraction of the variance of y that is due to the firm fixed effect (0% 75%) Change the fraction of the variance of ε that is due to the firm fixed effect (0% 75%)

54 True SE OLS SE OLS SE cluster

55 Time effect? Petersen (2009) execute a similar analysis for Time fixed effect (cross firm residual correlation) Firm and Time fixed effect Temporary Firm fixed effect (decay) Bottom line: Everything potentially create BIASES

56 Application: Capital Structure

57 Take Away In the presence of firm fixed effect OLS SE are biased SE clustered by firm are unbiased In the presence of a time fixed effect OLS SE are biased Fama McBeth SE are unbiased In the presence of both Include time dummies and cluster by firm Double cluster by time and firm Learn about the structure of the data

58 Stata and SAS code and help /htm/papers/standarderror.html

FE670 Algorithmic Trading Strategies. Stevens Institute of Technology

FE670 Algorithmic Trading Strategies Lecture 4. Cross-Sectional Models and Trading Strategies Steve Yang Stevens Institute of Technology 09/26/2013 Outline 1 Cross-Sectional Methods for Evaluation of Factor

FE670 Algorithmic Trading Strategies Lecture 4. Cross-Sectional Models and Trading Strategies Steve Yang Stevens Institute of Technology 09/26/2013 Outline 1 Cross-Sectional Methods for Evaluation of Factor

Empirical Methods for Corporate Finance. Regression Discontinuity Design

Empirical Methods for Corporate Finance Regression Discontinuity Design Basic Idea of RDD Observations (e.g. firms, individuals, ) are treated based on cutoff rules that are known ex ante For instance,

Empirical Methods for Corporate Finance Regression Discontinuity Design Basic Idea of RDD Observations (e.g. firms, individuals, ) are treated based on cutoff rules that are known ex ante For instance,

Quantitative Techniques Term 2

Quantitative Techniques Term 2 Laboratory 7 2 March 2006 Overview The objective of this lab is to: Estimate a cost function for a panel of firms; Calculate returns to scale; Introduce the command cluster

Quantitative Techniques Term 2 Laboratory 7 2 March 2006 Overview The objective of this lab is to: Estimate a cost function for a panel of firms; Calculate returns to scale; Introduce the command cluster

Econometrics and Economic Data

Econometrics and Economic Data Chapter 1 What is a regression? By using the regression model, we can evaluate the magnitude of change in one variable due to a certain change in another variable. For example,

Econometrics and Economic Data Chapter 1 What is a regression? By using the regression model, we can evaluate the magnitude of change in one variable due to a certain change in another variable. For example,

Empirical Methods for Corporate Finance

Empirical Methods for Corporate Finance Difference in Differences Note: This set of slides is inspired by that of Michael R. Roberts at Wharton Basics (As said earlier) one of the most causes of endogeneity

Empirical Methods for Corporate Finance Difference in Differences Note: This set of slides is inspired by that of Michael R. Roberts at Wharton Basics (As said earlier) one of the most causes of endogeneity

The Simple Regression Model

Chapter 2 Wooldridge: Introductory Econometrics: A Modern Approach, 5e Definition of the simple linear regression model "Explains variable in terms of variable " Intercept Slope parameter Dependent var,

Chapter 2 Wooldridge: Introductory Econometrics: A Modern Approach, 5e Definition of the simple linear regression model "Explains variable in terms of variable " Intercept Slope parameter Dependent var,

The Simple Regression Model

Chapter 2 Wooldridge: Introductory Econometrics: A Modern Approach, 5e Definition of the simple linear regression model Explains variable in terms of variable Intercept Slope parameter Dependent variable,

Chapter 2 Wooldridge: Introductory Econometrics: A Modern Approach, 5e Definition of the simple linear regression model Explains variable in terms of variable Intercept Slope parameter Dependent variable,

Presence of Stochastic Errors in the Input Demands: Are Dual and Primal Estimations Equivalent?

Presence of Stochastic Errors in the Input Demands: Are Dual and Primal Estimations Equivalent? Mauricio Bittencourt (The Ohio State University, Federal University of Parana Brazil) bittencourt.1@osu.edu

Presence of Stochastic Errors in the Input Demands: Are Dual and Primal Estimations Equivalent? Mauricio Bittencourt (The Ohio State University, Federal University of Parana Brazil) bittencourt.1@osu.edu

AN ANALYSIS OF THE DEGREE OF DIVERSIFICATION AND FIRM PERFORMANCE Zheng-Feng Guo, Vanderbilt University Lingyan Cao, University of Maryland

The International Journal of Business and Finance Research Volume 6 Number 2 2012 AN ANALYSIS OF THE DEGREE OF DIVERSIFICATION AND FIRM PERFORMANCE Zheng-Feng Guo, Vanderbilt University Lingyan Cao, University

The International Journal of Business and Finance Research Volume 6 Number 2 2012 AN ANALYSIS OF THE DEGREE OF DIVERSIFICATION AND FIRM PERFORMANCE Zheng-Feng Guo, Vanderbilt University Lingyan Cao, University

Panel Regression of Out-of-the-Money S&P 500 Index Put Options Prices

Panel Regression of Out-of-the-Money S&P 500 Index Put Options Prices Prakher Bajpai* (May 8, 2014) 1 Introduction In 1973, two economists, Myron Scholes and Fischer Black, developed a mathematical model

Panel Regression of Out-of-the-Money S&P 500 Index Put Options Prices Prakher Bajpai* (May 8, 2014) 1 Introduction In 1973, two economists, Myron Scholes and Fischer Black, developed a mathematical model

Volume 37, Issue 2. Handling Endogeneity in Stochastic Frontier Analysis

Volume 37, Issue 2 Handling Endogeneity in Stochastic Frontier Analysis Mustafa U. Karakaplan Georgetown University Levent Kutlu Georgia Institute of Technology Abstract We present a general maximum likelihood

Volume 37, Issue 2 Handling Endogeneity in Stochastic Frontier Analysis Mustafa U. Karakaplan Georgetown University Levent Kutlu Georgia Institute of Technology Abstract We present a general maximum likelihood

An Empirical Examination of Traditional Equity Valuation Models: The case of the Athens Stock Exchange

European Research Studies, Volume 7, Issue (1-) 004 An Empirical Examination of Traditional Equity Valuation Models: The case of the Athens Stock Exchange By G. A. Karathanassis*, S. N. Spilioti** Abstract

European Research Studies, Volume 7, Issue (1-) 004 An Empirical Examination of Traditional Equity Valuation Models: The case of the Athens Stock Exchange By G. A. Karathanassis*, S. N. Spilioti** Abstract

List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Factors in the returns on stock : inspiration from Fama and French asset pricing model

Lingnan Journal of Banking, Finance and Economics Volume 5 2014/2015 Academic Year Issue Article 1 January 2015 Factors in the returns on stock : inspiration from Fama and French asset pricing model Yuanzhen

Lingnan Journal of Banking, Finance and Economics Volume 5 2014/2015 Academic Year Issue Article 1 January 2015 Factors in the returns on stock : inspiration from Fama and French asset pricing model Yuanzhen

The Role of Credit Ratings in the. Dynamic Tradeoff Model. Viktoriya Staneva*

The Role of Credit Ratings in the Dynamic Tradeoff Model Viktoriya Staneva* This study examines what costs and benefits of debt are most important to the determination of the optimal capital structure.

The Role of Credit Ratings in the Dynamic Tradeoff Model Viktoriya Staneva* This study examines what costs and benefits of debt are most important to the determination of the optimal capital structure.

Your Name (Please print) Did you agree to take the optional portion of the final exam Yes No. Directions

Did you agree to take the optional portion of the final exam Yes No. Directions") Your Name (Please print) Did you agree to take the optional portion of the final exam Yes No (Your online answer will be used to verify your response.) Directions There are two parts to the final exam.

Your Name (Please print) Did you agree to take the optional portion of the final exam Yes No (Your online answer will be used to verify your response.) Directions There are two parts to the final exam.

Key Objectives. Module 2: The Logic of Statistical Inference. Z-scores. SGSB Workshop: Using Statistical Data to Make Decisions

SGSB Workshop: Using Statistical Data to Make Decisions Module 2: The Logic of Statistical Inference Dr. Tom Ilvento January 2006 Dr. Mugdim Pašić Key Objectives Understand the logic of statistical inference

SGSB Workshop: Using Statistical Data to Make Decisions Module 2: The Logic of Statistical Inference Dr. Tom Ilvento January 2006 Dr. Mugdim Pašić Key Objectives Understand the logic of statistical inference

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

UNOBSERVABLE EFFECTS AND SPEED OF ADJUSTMENT TO TARGET CAPITAL STRUCTURE

International Journal of Business and Society, Vol. 16 No. 3, 2015, 470-479 UNOBSERVABLE EFFECTS AND SPEED OF ADJUSTMENT TO TARGET CAPITAL STRUCTURE Bolaji Tunde Matemilola Universiti Putra Malaysia Bany

International Journal of Business and Society, Vol. 16 No. 3, 2015, 470-479 UNOBSERVABLE EFFECTS AND SPEED OF ADJUSTMENT TO TARGET CAPITAL STRUCTURE Bolaji Tunde Matemilola Universiti Putra Malaysia Bany

Lecture 5. Predictability. Traditional Views of Market Efficiency ( )

") Lecture 5 Predictability Traditional Views of Market Efficiency (1960-1970) CAPM is a good measure of risk Returns are close to unpredictable (a) Stock, bond and foreign exchange changes are not predictable

Lecture 5 Predictability Traditional Views of Market Efficiency (1960-1970) CAPM is a good measure of risk Returns are close to unpredictable (a) Stock, bond and foreign exchange changes are not predictable

Online Appendix to Grouped Coefficients to Reduce Bias in Heterogeneous Dynamic Panel Models with Small T

Online Appendix to Grouped Coefficients to Reduce Bias in Heterogeneous Dynamic Panel Models with Small T Nathan P. Hendricks and Aaron Smith October 2014 A1 Bias Formulas for Large T The heterogeneous

Online Appendix to Grouped Coefficients to Reduce Bias in Heterogeneous Dynamic Panel Models with Small T Nathan P. Hendricks and Aaron Smith October 2014 A1 Bias Formulas for Large T The heterogeneous

Basic Regression Analysis with Time Series Data

with Time Series Data Chapter 10 Wooldridge: Introductory Econometrics: A Modern Approach, 5e The nature of time series data Temporal ordering of observations; may not be arbitrarily reordered Typical

with Time Series Data Chapter 10 Wooldridge: Introductory Econometrics: A Modern Approach, 5e The nature of time series data Temporal ordering of observations; may not be arbitrarily reordered Typical

Determinants of Cyclical Aggregate Dividend Behavior

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

Introduction to Algorithmic Trading Strategies Lecture 9

Introduction to Algorithmic Trading Strategies Lecture 9 Quantitative Equity Portfolio Management Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Alpha Factor Models References

Introduction to Algorithmic Trading Strategies Lecture 9 Quantitative Equity Portfolio Management Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Alpha Factor Models References

The Determinants of Corporate Debt Maturity Structure

10 The Determinants of Corporate Debt Maturity Structure Ewa J. Kleczyk Custom Analytics, ImpactRx, Inc. Horsham, Pa. USA 1. Introduction According to Stiglitz (1974) and Modigliani and Miller (1958),

10 The Determinants of Corporate Debt Maturity Structure Ewa J. Kleczyk Custom Analytics, ImpactRx, Inc. Horsham, Pa. USA 1. Introduction According to Stiglitz (1974) and Modigliani and Miller (1958),

Economics 345 Applied Econometrics

Economics 345 Applied Econometrics Problem Set 4--Solutions Prof: Martin Farnham Problem sets in this course are ungraded. An answer key will be posted on the course website within a few days of the release

Economics 345 Applied Econometrics Problem Set 4--Solutions Prof: Martin Farnham Problem sets in this course are ungraded. An answer key will be posted on the course website within a few days of the release

The Evidence for Differences in Risk for Fixed vs Mobile Telecoms For the Office of Communications (Ofcom)

") The Evidence for Differences in Risk for Fixed vs Mobile Telecoms For the Office of Communications (Ofcom) November 2017 Project Team Dr. Richard Hern Marija Spasovska Aldo Motta NERA Economic Consulting

The Evidence for Differences in Risk for Fixed vs Mobile Telecoms For the Office of Communications (Ofcom) November 2017 Project Team Dr. Richard Hern Marija Spasovska Aldo Motta NERA Economic Consulting

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Abstract. Crop insurance premium subsidies affect patterns of crop acreage for two

Abstract Crop insurance premium subsidies affect patterns of crop acreage for two reasons. First, holding insurance coverage constant, premium subsidies directly increase expected profit, which encourages

Abstract Crop insurance premium subsidies affect patterns of crop acreage for two reasons. First, holding insurance coverage constant, premium subsidies directly increase expected profit, which encourages

WORKING PAPERS IN ECONOMICS & ECONOMETRICS. Bounds on the Return to Education in Australia using Ability Bias

WORKING PAPERS IN ECONOMICS & ECONOMETRICS Bounds on the Return to Education in Australia using Ability Bias Martine Mariotti Research School of Economics College of Business and Economics Australian National

WORKING PAPERS IN ECONOMICS & ECONOMETRICS Bounds on the Return to Education in Australia using Ability Bias Martine Mariotti Research School of Economics College of Business and Economics Australian National

Economics 300 Econometrics Econometric Approaches to Causal Inference: Instrumental Variables

Economics 300 Econometrics Econometric Approaches to Causal Inference: Variables Dennis C. Plott University of Illinois at Chicago Department of Economics www.dennisplott.com Fall 2014 Dennis C. Plott

Economics 300 Econometrics Econometric Approaches to Causal Inference: Variables Dennis C. Plott University of Illinois at Chicago Department of Economics www.dennisplott.com Fall 2014 Dennis C. Plott

Current Account Balances and Output Volatility

Current Account Balances and Output Volatility Ceyhun Elgin Bogazici University Tolga Umut Kuzubas Bogazici University Abstract: Using annual data from 185 countries over the period from 1950 to 2009,

Current Account Balances and Output Volatility Ceyhun Elgin Bogazici University Tolga Umut Kuzubas Bogazici University Abstract: Using annual data from 185 countries over the period from 1950 to 2009,

Appendix A (Pornprasertmanit & Little, in press) Mathematical Proof

Mathematical Proof") Appendix A (Pornprasertmanit & Little, in press) Mathematical Proof Definition We begin by defining notations that are needed for later sections. First, we define moment as the mean of a random variable

Appendix A (Pornprasertmanit & Little, in press) Mathematical Proof Definition We begin by defining notations that are needed for later sections. First, we define moment as the mean of a random variable

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Derivation of zero-beta CAPM: Efficient portfolios

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

The Relationship between Earning, Dividend, Stock Price and Stock Return: Evidence from Iranian Companies

20 International Conference on Humanities, Society and Culture IPEDR Vol.20 (20) (20) IACSIT Press, Singapore The Relationship between Earning, Dividend, Stock Price and Stock Return: Evidence from Iranian

20 International Conference on Humanities, Society and Culture IPEDR Vol.20 (20) (20) IACSIT Press, Singapore The Relationship between Earning, Dividend, Stock Price and Stock Return: Evidence from Iranian

Financial Econometrics

Financial Econometrics Volatility Gerald P. Dwyer Trinity College, Dublin January 2013 GPD (TCD) Volatility 01/13 1 / 37 Squared log returns for CRSP daily GPD (TCD) Volatility 01/13 2 / 37 Absolute value

Financial Econometrics Volatility Gerald P. Dwyer Trinity College, Dublin January 2013 GPD (TCD) Volatility 01/13 1 / 37 Squared log returns for CRSP daily GPD (TCD) Volatility 01/13 2 / 37 Absolute value

The Comovements Along the Term Structure of Oil Forwards in Periods of High and Low Volatility: How Tight Are They?

The Comovements Along the Term Structure of Oil Forwards in Periods of High and Low Volatility: How Tight Are They? Massimiliano Marzo and Paolo Zagaglia This version: January 6, 29 Preliminary: comments

The Comovements Along the Term Structure of Oil Forwards in Periods of High and Low Volatility: How Tight Are They? Massimiliano Marzo and Paolo Zagaglia This version: January 6, 29 Preliminary: comments

Management Science Letters

Management Science Letters 3 (2013) 73 80 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl Investigating different influential factors on capital

Management Science Letters 3 (2013) 73 80 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl Investigating different influential factors on capital

Firing Costs, Employment and Misallocation

Firing Costs, Employment and Misallocation Evidence from Randomly Assigned Judges Omar Bamieh University of Vienna November 13th 2018 1 / 27 Why should we care about firing costs? Firing costs make it

Firing Costs, Employment and Misallocation Evidence from Randomly Assigned Judges Omar Bamieh University of Vienna November 13th 2018 1 / 27 Why should we care about firing costs? Firing costs make it

Dividend Changes and Future Profitability

THE JOURNAL OF FINANCE VOL. LVI, NO. 6 DEC. 2001 Dividend Changes and Future Profitability DORON NISSIM and AMIR ZIV* ABSTRACT We investigate the relation between dividend changes and future profitability,

THE JOURNAL OF FINANCE VOL. LVI, NO. 6 DEC. 2001 Dividend Changes and Future Profitability DORON NISSIM and AMIR ZIV* ABSTRACT We investigate the relation between dividend changes and future profitability,

Advanced Econometrics

Advanced Econometrics Instructor: Takashi Yamano 11/14/2003 Due: 11/21/2003 Homework 5 (30 points) Sample Answers 1. (16 points) Read Example 13.4 and an AER paper by Meyer, Viscusi, and Durbin (1995).

Advanced Econometrics Instructor: Takashi Yamano 11/14/2003 Due: 11/21/2003 Homework 5 (30 points) Sample Answers 1. (16 points) Read Example 13.4 and an AER paper by Meyer, Viscusi, and Durbin (1995).

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Does a financial crisis affect operating risk? Evidence from Polish listed companies 1

Economics and Business Review, Vol. 4 (18), No. 1, 2018: 64-85 DOI: 10.18559/ebr.2018.1.5 Does a financial crisis affect operating risk? Evidence from Polish listed companies 1 Sławomir Kalinowski 2, Marcin

Economics and Business Review, Vol. 4 (18), No. 1, 2018: 64-85 DOI: 10.18559/ebr.2018.1.5 Does a financial crisis affect operating risk? Evidence from Polish listed companies 1 Sławomir Kalinowski 2, Marcin

Employer-Provided Health Insurance and Labor Supply of Married Women

Upjohn Institute Working Papers Upjohn Research home page 2011 Employer-Provided Health Insurance and Labor Supply of Married Women Merve Cebi University of Massachusetts - Dartmouth and W.E. Upjohn Institute

Upjohn Institute Working Papers Upjohn Research home page 2011 Employer-Provided Health Insurance and Labor Supply of Married Women Merve Cebi University of Massachusetts - Dartmouth and W.E. Upjohn Institute

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Spring University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Empirical Capital Structure Research: New Ideas, Recent Evidence, and Methodological Issues. Ralf Elsas and David Florysiak

Empirical Capital Structure Research: New Ideas, Recent Evidence, and Methodological Issues Ralf Elsas and David Florysiak Discussion paper 2008-10 July 2008 Munich School of Management University of Munich

Empirical Capital Structure Research: New Ideas, Recent Evidence, and Methodological Issues Ralf Elsas and David Florysiak Discussion paper 2008-10 July 2008 Munich School of Management University of Munich

Acemoglu, et al (2008) cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that

cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that") Acemoglu, et al (2008) cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that the strong positive correlation between income and democracy

Acemoglu, et al (2008) cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that the strong positive correlation between income and democracy

Does Manufacturing Matter for Economic Growth in the Era of Globalization? Online Supplement

Does Manufacturing Matter for Economic Growth in the Era of Globalization? Results from Growth Curve Models of Manufacturing Share of Employment (MSE) To formally test trends in manufacturing share of

Does Manufacturing Matter for Economic Growth in the Era of Globalization? Results from Growth Curve Models of Manufacturing Share of Employment (MSE) To formally test trends in manufacturing share of

Financial Development and Economic Growth at Different Income Levels

1 Financial Development and Economic Growth at Different Income Levels Cody Kallen Washington University in St. Louis Honors Thesis in Economics Abstract This paper examines the effects of financial development

1 Financial Development and Economic Growth at Different Income Levels Cody Kallen Washington University in St. Louis Honors Thesis in Economics Abstract This paper examines the effects of financial development

The relationship between GDP, labor force and health expenditure in European countries

Econometrics-Term paper The relationship between GDP, labor force and health expenditure in European countries Student: Nguyen Thu Ha Contents 1. Background:... 2 2. Discussion:... 2 3. Regression equation

Econometrics-Term paper The relationship between GDP, labor force and health expenditure in European countries Student: Nguyen Thu Ha Contents 1. Background:... 2 2. Discussion:... 2 3. Regression equation

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables

Appendix A: Appendix Figures and Tables") ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

The data definition file provided by the authors is reproduced below: Obs: 1500 home sales in Stockton, CA from Oct 1, 1996 to Nov 30, 1998

Economics 312 Sample Project Report Jeffrey Parker Introduction This project is based on Exercise 2.12 on page 81 of the Hill, Griffiths, and Lim text. It examines how the sale price of houses in Stockton,

Economics 312 Sample Project Report Jeffrey Parker Introduction This project is based on Exercise 2.12 on page 81 of the Hill, Griffiths, and Lim text. It examines how the sale price of houses in Stockton,

Cash holdings determinants in the Portuguese economy 1

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Variance clustering. Two motivations, volatility clustering, and implied volatility

Variance modelling The simplest assumption for time series is that variance is constant. Unfortunately that assumption is often violated in actual data. In this lecture we look at the implications of time

Variance modelling The simplest assumption for time series is that variance is constant. Unfortunately that assumption is often violated in actual data. In this lecture we look at the implications of time

Note on Cost of Capital

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

Management Science Letters

Management Science Letters 2 (2012) 2625 2630 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl The impact of working capital and financial structure

Management Science Letters 2 (2012) 2625 2630 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl The impact of working capital and financial structure

The Speed of Adjustment to the Target Market Value Leverage is Slower Than You Think

The Speed of Adjustment to the Target Market Value Leverage is Slower Than You Think Qie Ellie Yin * Department of Finance and Decision Sciences School of Business Hong Kong Baptist University qieyin@hkbu.edu.hk

The Speed of Adjustment to the Target Market Value Leverage is Slower Than You Think Qie Ellie Yin * Department of Finance and Decision Sciences School of Business Hong Kong Baptist University qieyin@hkbu.edu.hk

Online Robustness Appendix to Are Household Surveys Like Tax Forms: Evidence from the Self Employed

Online Robustness Appendix to Are Household Surveys Like Tax Forms: Evidence from the Self Employed March 01 Erik Hurst University of Chicago Geng Li Board of Governors of the Federal Reserve System Benjamin

Online Robustness Appendix to Are Household Surveys Like Tax Forms: Evidence from the Self Employed March 01 Erik Hurst University of Chicago Geng Li Board of Governors of the Federal Reserve System Benjamin

THE IMPACT OF BANKING RISKS ON THE CAPITAL OF COMMERCIAL BANKS IN LIBYA

THE IMPACT OF BANKING RISKS ON THE CAPITAL OF COMMERCIAL BANKS IN LIBYA Azeddin ARAB Kastamonu University, Turkey, Institute for Social Sciences, Department of Business Abstract: The objective of this

THE IMPACT OF BANKING RISKS ON THE CAPITAL OF COMMERCIAL BANKS IN LIBYA Azeddin ARAB Kastamonu University, Turkey, Institute for Social Sciences, Department of Business Abstract: The objective of this

14.471: Fall 2012: Recitation 3: Labor Supply: Blundell, Duncan and Meghir EMA (1998)

") 14.471: Fall 2012: Recitation 3: Labor Supply: Blundell, Duncan and Meghir EMA (1998) Daan Struyven September 29, 2012 Questions: How big is the labor supply elasticitiy? How should estimation deal whith

14.471: Fall 2012: Recitation 3: Labor Supply: Blundell, Duncan and Meghir EMA (1998) Daan Struyven September 29, 2012 Questions: How big is the labor supply elasticitiy? How should estimation deal whith

The Vasicek adjustment to beta estimates in the Capital Asset Pricing Model

The Vasicek adjustment to beta estimates in the Capital Asset Pricing Model 17 June 2013 Contents 1. Preparation of this report... 1 2. Executive summary... 2 3. Issue and evaluation approach... 4 3.1.

The Vasicek adjustment to beta estimates in the Capital Asset Pricing Model 17 June 2013 Contents 1. Preparation of this report... 1 2. Executive summary... 2 3. Issue and evaluation approach... 4 3.1.

Improving Returns-Based Style Analysis

Improving Returns-Based Style Analysis Autumn, 2007 Daniel Mostovoy Northfield Information Services Daniel@northinfo.com Main Points For Today Over the past 15 years, Returns-Based Style Analysis become

Improving Returns-Based Style Analysis Autumn, 2007 Daniel Mostovoy Northfield Information Services Daniel@northinfo.com Main Points For Today Over the past 15 years, Returns-Based Style Analysis become

Panel data techniques and accounting research

Panel data techniques and accounting research P de Jager Department of Financial Management University of Pretoria Abstract Empirical accounting research frequently makes use of data sets with a time-series

Panel data techniques and accounting research P de Jager Department of Financial Management University of Pretoria Abstract Empirical accounting research frequently makes use of data sets with a time-series

Topic 2. Productivity, technological change, and policy: macro-level analysis

Topic 2. Productivity, technological change, and policy: macro-level analysis Lecture 3 Growth econometrics Read Mankiw, Romer and Weil (1992, QJE); Durlauf et al. (2004, section 3-7) ; or Temple, J. (1999,

Topic 2. Productivity, technological change, and policy: macro-level analysis Lecture 3 Growth econometrics Read Mankiw, Romer and Weil (1992, QJE); Durlauf et al. (2004, section 3-7) ; or Temple, J. (1999,

Capital structure and profitability of firms in the corporate sector of Pakistan

Business Review: (2017) 12(1):50-58 Original Paper Capital structure and profitability of firms in the corporate sector of Pakistan Sana Tauseef Heman D. Lohano Abstract We examine the impact of debt ratios

Business Review: (2017) 12(1):50-58 Original Paper Capital structure and profitability of firms in the corporate sector of Pakistan Sana Tauseef Heman D. Lohano Abstract We examine the impact of debt ratios

Managerial incentives to increase firm volatility provided by debt, stock, and options. Joshua D. Anderson

Managerial incentives to increase firm volatility provided by debt, stock, and options Joshua D. Anderson jdanders@mit.edu (617) 253-7974 John E. Core* jcore@mit.edu (617) 715-4819 Abstract We measure

Managerial incentives to increase firm volatility provided by debt, stock, and options Joshua D. Anderson jdanders@mit.edu (617) 253-7974 John E. Core* jcore@mit.edu (617) 715-4819 Abstract We measure

CEOs Personal Portfolio and Corporate Policies

CEOs Personal Portfolio and Corporate Policies Hamid Boustanifar Dan Zhang October, 2016 Abstract Using a unique data set of personal wealth and sociodemographic characteristics for all Norwegian CEOs,

CEOs Personal Portfolio and Corporate Policies Hamid Boustanifar Dan Zhang October, 2016 Abstract Using a unique data set of personal wealth and sociodemographic characteristics for all Norwegian CEOs,

Fiscal Divergence and Business Cycle Synchronization: Irresponsibility is Idiosyncratic. Zsolt Darvas, Andrew K. Rose and György Szapáry

Fiscal Divergence and Business Cycle Synchronization: Irresponsibility is Idiosyncratic Zsolt Darvas, Andrew K. Rose and György Szapáry 1 I. Motivation Business cycle synchronization (BCS) the critical

Fiscal Divergence and Business Cycle Synchronization: Irresponsibility is Idiosyncratic Zsolt Darvas, Andrew K. Rose and György Szapáry 1 I. Motivation Business cycle synchronization (BCS) the critical

Incentives in Executive Compensation Contracts: An Examination of Pay-for-Performance

Incentives in Executive Compensation Contracts: An Examination of Pay-for-Performance Alaina George April 2003 I would like to thank my advisor, Professor Miles Cahill, for his encouragement, direction,

Incentives in Executive Compensation Contracts: An Examination of Pay-for-Performance Alaina George April 2003 I would like to thank my advisor, Professor Miles Cahill, for his encouragement, direction,

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE Eva Výrostová Abstract The paper estimates the impact of the EU budget on the economic convergence process of EU member states. Although the primary

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE Eva Výrostová Abstract The paper estimates the impact of the EU budget on the economic convergence process of EU member states. Although the primary

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Problem Set 6. I did this with figure; bar3(reshape(mean(rx),5,5) );ylabel( size ); xlabel( value ); mean mo return %

,5,5) );ylabel( size ); xlabel( value ); mean mo return %") Business 35905 John H. Cochrane Problem Set 6 We re going to replicate and extend Fama and French s basic results, using earlier and extended data. Get the 25 Fama French portfolios and factors from the

Business 35905 John H. Cochrane Problem Set 6 We re going to replicate and extend Fama and French s basic results, using earlier and extended data. Get the 25 Fama French portfolios and factors from the

Assessing Model Stability Using Recursive Estimation and Recursive Residuals

Assessing Model Stability Using Recursive Estimation and Recursive Residuals Our forecasting procedure cannot be expected to produce good forecasts if the forecasting model that we constructed was stable

Assessing Model Stability Using Recursive Estimation and Recursive Residuals Our forecasting procedure cannot be expected to produce good forecasts if the forecasting model that we constructed was stable

Financial Econometrics Notes. Kevin Sheppard University of Oxford

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

Financial Econometrics Notes Kevin Sheppard University of Oxford Monday 15 th January, 2018 2 This version: 22:52, Monday 15 th January, 2018 2018 Kevin Sheppard ii Contents 1 Probability, Random Variables

The Speed of Adjustment to the Target Market Value Leverage is Slower Than You Think

The Speed of Adjustment to the Target Market Value Leverage is Slower Than You Think Qie Ellie Yin * Department of Finance and Decision Sciences School of Business Hong Kong Baptist University qieyin@hkbu.edu.hk

The Speed of Adjustment to the Target Market Value Leverage is Slower Than You Think Qie Ellie Yin * Department of Finance and Decision Sciences School of Business Hong Kong Baptist University qieyin@hkbu.edu.hk

Introduction to Econometrics (3 rd Updated Edition) Solutions to Odd- Numbered End- of- Chapter Exercises: Chapter 6

Solutions to Odd- Numbered End- of- Chapter Exercises: Chapter 6") Introduction to Econometrics (3 rd Updated Edition) by James H. Stock and Mark W. Watson Solutions to Odd- Numbered End- of- Chapter Exercises: Chapter 6 (This version August 17, 014) 015 Pearson Education,

Introduction to Econometrics (3 rd Updated Edition) by James H. Stock and Mark W. Watson Solutions to Odd- Numbered End- of- Chapter Exercises: Chapter 6 (This version August 17, 014) 015 Pearson Education,

Example 1 of econometric analysis: the Market Model

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

An Empirical Analysis on the Relationship between Health Care Expenditures and Economic Growth in the European Union Countries

An Empirical Analysis on the Relationship between Health Care Expenditures and Economic Growth in the European Union Countries Çiğdem Börke Tunalı Associate Professor, Department of Economics, Faculty

An Empirical Analysis on the Relationship between Health Care Expenditures and Economic Growth in the European Union Countries Çiğdem Börke Tunalı Associate Professor, Department of Economics, Faculty

Lecture 8: Markov and Regime

Lecture 8: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2016 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Lecture 8: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2016 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Choice Probabilities. Logit Choice Probabilities Derivation. Choice Probabilities. Basic Econometrics in Transportation.

1/31 Choice Probabilities Basic Econometrics in Transportation Logit Models Amir Samimi Civil Engineering Department Sharif University of Technology Primary Source: Discrete Choice Methods with Simulation

1/31 Choice Probabilities Basic Econometrics in Transportation Logit Models Amir Samimi Civil Engineering Department Sharif University of Technology Primary Source: Discrete Choice Methods with Simulation

An Empirical Investigation of the Lease-Debt Relation in the Restaurant and Retail Industry

University of Massachusetts Amherst ScholarWorks@UMass Amherst International CHRIE Conference-Refereed Track 2011 ICHRIE Conference Jul 28th, 4:45 PM - 4:45 PM An Empirical Investigation of the Lease-Debt

University of Massachusetts Amherst ScholarWorks@UMass Amherst International CHRIE Conference-Refereed Track 2011 ICHRIE Conference Jul 28th, 4:45 PM - 4:45 PM An Empirical Investigation of the Lease-Debt

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES. Lucas Island Model

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

Economics 430 Handout on Rational Expectations: Part I. Review of Statistics: Notation and Definitions

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

A1. Relating Level and Slope to Expected Inflation and Output Dynamics

Appendix 1 A1. Relating Level and Slope to Expected Inflation and Output Dynamics This section provides a simple illustrative example to show how the level and slope factors incorporate expectations regarding

Appendix 1 A1. Relating Level and Slope to Expected Inflation and Output Dynamics This section provides a simple illustrative example to show how the level and slope factors incorporate expectations regarding

Public Economics. Contact Information

Public Economics K.Peren Arin Contact Information Office Hours:After class! All communication in English please! 1 Introduction The year is 1030 B.C. For decades, Israeli tribes have been living without

Public Economics K.Peren Arin Contact Information Office Hours:After class! All communication in English please! 1 Introduction The year is 1030 B.C. For decades, Israeli tribes have been living without

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Testing for efficient markets

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

DIFFERENCE DIFFERENCES

DIFFERENCE IN DIFFERENCES & PANEL DATA Technical Track Session III Céline Ferré The World Bank Structure of this session 1 When do we use Differences-in- Differences? (Diff-in-Diff or DD) 2 Estimation

DIFFERENCE IN DIFFERENCES & PANEL DATA Technical Track Session III Céline Ferré The World Bank Structure of this session 1 When do we use Differences-in- Differences? (Diff-in-Diff or DD) 2 Estimation

Lecture 9: Markov and Regime

Lecture 9: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2017 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

Lecture 9: Markov and Regime Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2017 Overview Motivation Deterministic vs. Endogeneous, Stochastic Switching Dummy Regressiom Switching

A Non-Random Walk Down Wall Street

A Non-Random Walk Down Wall Street Andrew W. Lo A. Craig MacKinlay Princeton University Press Princeton, New Jersey list of Figures List of Tables Preface xiii xv xxi 1 Introduction 3 1.1 The Random Walk

A Non-Random Walk Down Wall Street Andrew W. Lo A. Craig MacKinlay Princeton University Press Princeton, New Jersey list of Figures List of Tables Preface xiii xv xxi 1 Introduction 3 1.1 The Random Walk

Dynamic Capital Structure Adjustment and the. Impact of Fractional Dependent Variables

Dynamic Capital Structure Adjustment and the Impact of Fractional Dependent Variables Ralf Elsas David Florysiak June 2010 Abstract Capital structure research using dynamic partial adjustment models aims

Dynamic Capital Structure Adjustment and the Impact of Fractional Dependent Variables Ralf Elsas David Florysiak June 2010 Abstract Capital structure research using dynamic partial adjustment models aims

Sensex Realized Volatility Index (REALVOL)

") Sensex Realized Volatility Index (REALVOL) Introduction Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility.

Sensex Realized Volatility Index (REALVOL) Introduction Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility.

Market Timing Does Work: Evidence from the NYSE 1

Market Timing Does Work: Evidence from the NYSE 1 Devraj Basu Alexander Stremme Warwick Business School, University of Warwick November 2005 address for correspondence: Alexander Stremme Warwick Business

Market Timing Does Work: Evidence from the NYSE 1 Devraj Basu Alexander Stremme Warwick Business School, University of Warwick November 2005 address for correspondence: Alexander Stremme Warwick Business

The Divergence of Long - and Short-run Effects of Manager s Shareholding on Bank Efficiencies in Taiwan

Journal of Applied Finance & Banking, vol. 4, no. 6, 2014, 47-57 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2014 The Divergence of Long - and Short-run Effects of Manager s Shareholding

Journal of Applied Finance & Banking, vol. 4, no. 6, 2014, 47-57 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2014 The Divergence of Long - and Short-run Effects of Manager s Shareholding

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics

Henrik Jacobsen Kleven London School of Economics") LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost