Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages

|

|

|

- Anne Ryan

- 5 years ago

- Views:

Transcription

1 Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj The Vanguard Group Rajdeep Sengupta Federal Reserve Bank of St. Louis ECB CFS Research Conference Einaudi Institute for Economics and Finance, Rome, Italy November 2009

2 Motivation and Related Literature Evidence of Weak Underwriting standards Increasingly high proportion of Low Doc and High LTV Loans Foote et al. (2008); Demyanyk and van Hemert (2008) Originate to Distribute hypothesis Securitization and Cheap Credit Weak Underwriting standards Keys et al. (2009) Gorton (2008); Elul (2009); Bubb and Kaufman (2009)

3 Dominant explanation: Decline in Underwriting Standards The President s Working Group on Financial Markets (March, 2008): The turmoil in financial markets was triggered by a dramatic weakening of underwriting standards for U.S. subprime mortgages, beginning in late 2004, and extending into early (Emphasis in the original) Implications: 1. Something went wrong within the subprime market after Subprime mortgages of earlier vintages had relatively robust underwriting

4 Hard Information? Decline in underwriting shown with hard information: Demyanyk and van Hemert (2008) Stein (2002):

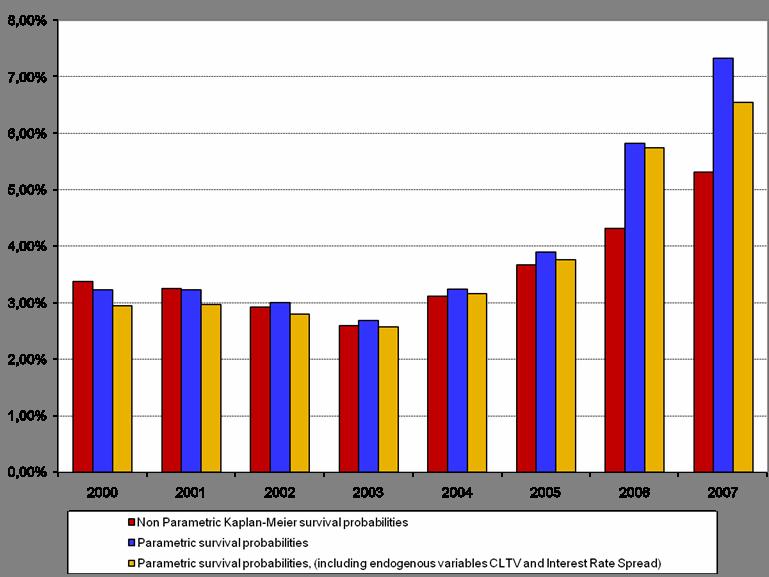

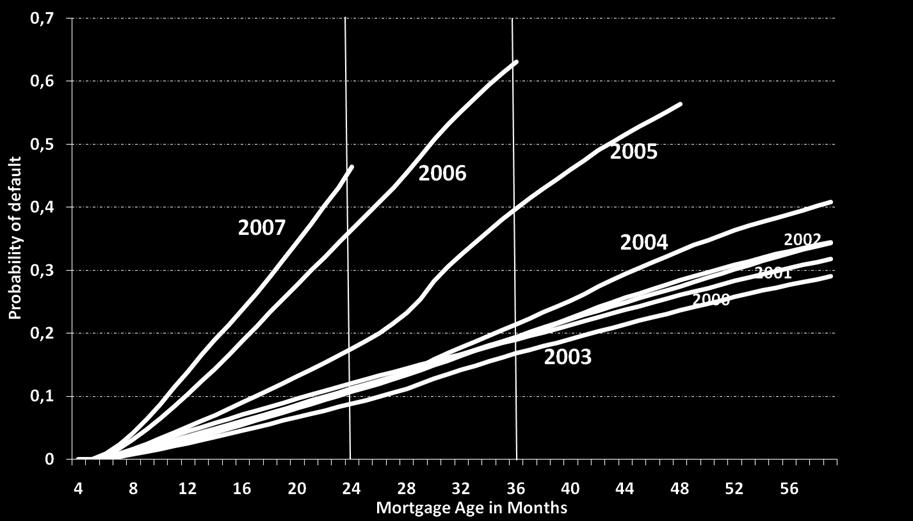

5 Subprime Default Probabilities

6 Post delinquency Behavior of Owner Occupied (up to two years after origination)

7 Post delinquency Behavior of Owner Occupied (up to two years after origination)

8 Pre delinquency Behavior for FRMs (up to loan age of 18 months)

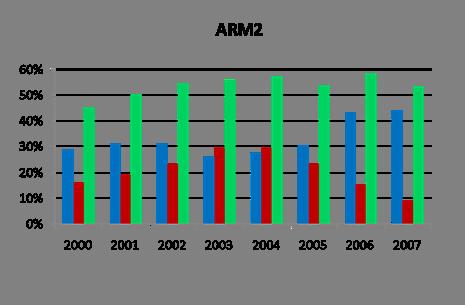

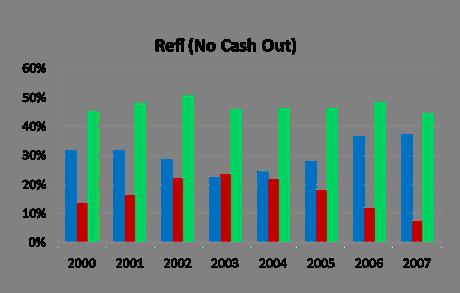

9 Pre delinquency Behavior by Product Type (up to loan age of 18 months)

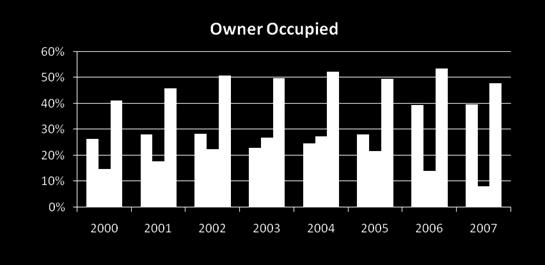

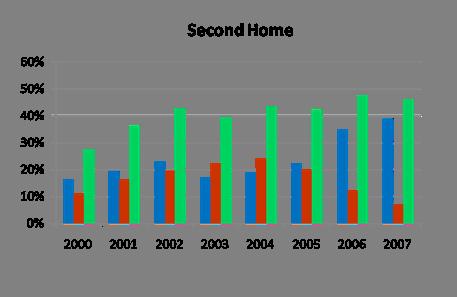

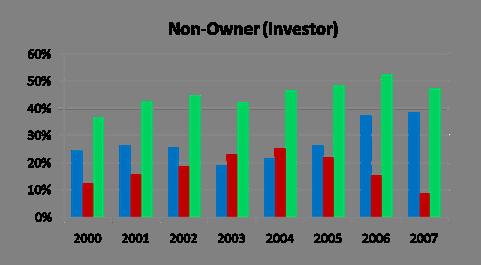

10 Pre delinquency Behavior by Occupancy (up to loan age of 18 months)

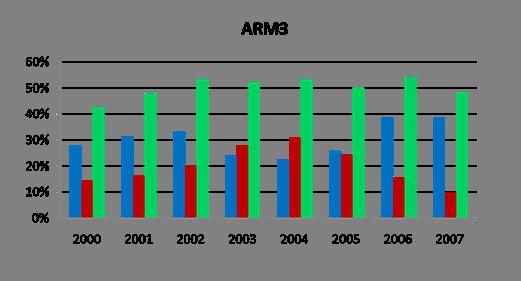

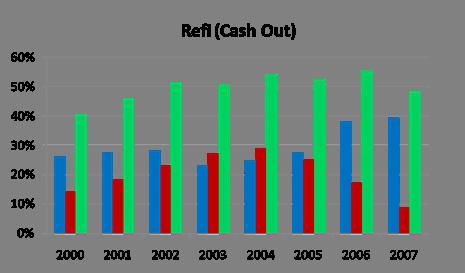

11 Pre delinquency Behavior by Purpose (up to loan age of 18 months)

12 Results Difficult to argue in favor of a secular dramatic weakening of lending standards within the subprime market. Credit score is a good predictor of ex post default specially for latter vintages Deterioration in underwriting post 2004 cannot be the dominant explanation for collapse of subprime mortgage market

13 Data and Coverage We use the data from LoanPerformance Securitized subprime mortgages only More than 9 million originations securitized as subprime Covers almost the entire market for subprime mortgages that have been securitized, especially the later vintages

14 Summary Trends: Increase in the proportion of ARMs Increase in the proportion of Low doc loans Increase in the proportion of high LTV loans Increase in average FICO scores.

15 Multivariate Nature of Underwriting Standards Despite exposing themselves to more credit risk on some borrower attributes (for example, by lowering documentation requirements) lenders seem to have attempted to offset this by increasing the average quality of borrowers (by raising credit score requirements) to whom such loans were made. Similar trend observed for other characteristics, Like Occupancy Type, LTV etc.

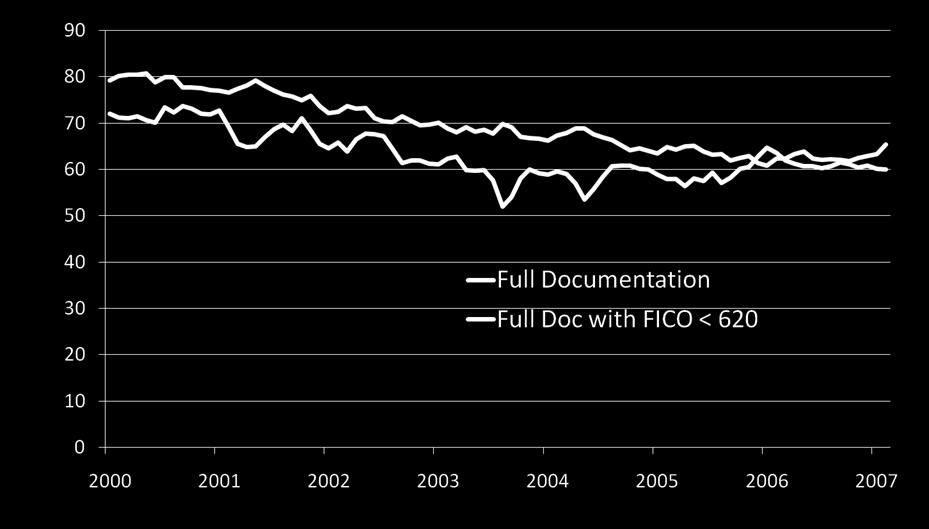

16 FICO and Full Documentation

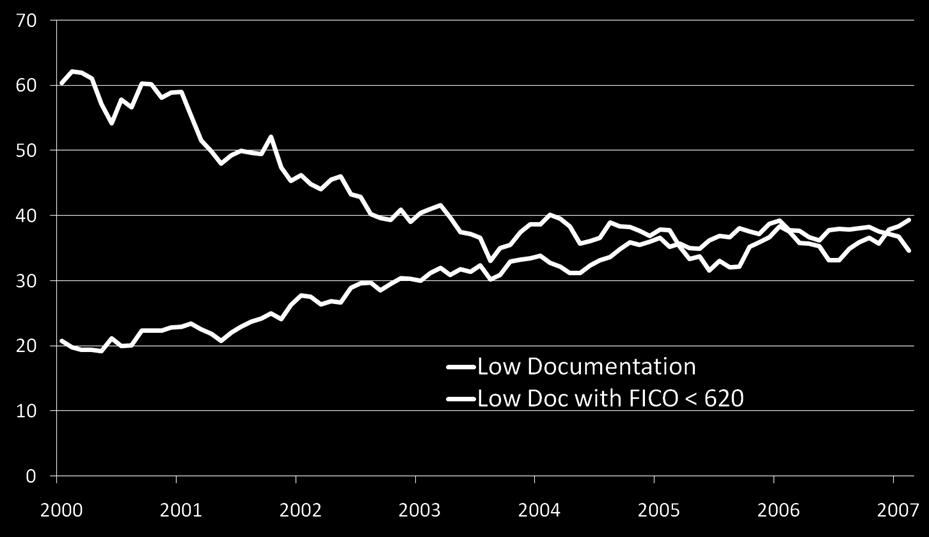

17 FICO and Low Documentation

18 FICO and Default Why did lenders choose higher FICO Scores? Ex post, some industry experts have even faulted originators on this account:... the crucial mistake many lenders made was relying on FICO credit scores to gauge default risk, regardless of the size of the down payment or the type of loan. Aug. 4, 2008 The woman who called Wall Street's meltdown Fortune Magazine,

19 FICO as a predictor of default Average Impact of Improvement in FICO on ex post probability of surviving delinquency event 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% FICO BINS < = > = 740

20 FICO as a predictor of default Average Impact of Improvement in FICO on ex post probability of surviving delinquency event 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% FICO BINS < = > = 741

21 Determinants of Default We show that a higher FICO score at origination significantly lowers the probability of (ex post) default. What Explains our Contrarian Results? Do not account for the endogeneity bias introduced by including mortgage terms in a default regression

22 Endogeneity of Mortgage Terms: Asymmetric Information Theory Adverse Selection: High risk agents are more likely to opt for the mortgage contract with the lower downpayment but a higher interest rate (Brueckner, 2000) Moral Hazard: Borrowers buying into mortgages with higher LTV for any unspecified or exogenous reasons are likely to exert less effort to repay the loan and therefore become riskier Advances in empirical contract theory: Chiappori and Salanie, (2000); Chiappori et al. (2006) Testable Implication: Under both adverse selection and moral hazard, one should observe a positive correlation conditional on observables between risk (ex post default) and coverage (LTV)

23 Endogeneity: Anecdotal Evidence Mortgage Pricing Sheet, Option One Mortgage Corp.

24 Mortgage Pricing Sheet: Cutts and Van Order (2005)

25 Positive Correlation: Endogeneity Bias Chiappori and Salanie, (2000)

26 Impact of Endogeneity Bias On the Interpretation of Structural relationship between Underwriting and Default Estimated Hazard Ratios FICO Full-Doc Dummy With Closing Rate Spread Bias With Interest Rate Spread Bias

27 0.30 Magnitude of Bias in FICO Hazard Ratios

28 Performance of FICO

29 Performance of FICO: Lower FICO scores

30 Performance of FICO: Higher FICO scores

31 Credit risk is multidimensional Lenders compensate for the increase in the ex ante risk of one borrower attribute by raising the requirement standards along another dimension Need to "aggregate" each borrower characteristic to build a summary measure that fulfils a variety of desirable conditions Solution to this aggregation problem has proved elusive

32 Counterfactual Analysis Getting around the aggregation problem How would ex post default rates change if a mortgage originated to a "representative borrower" in 2005 were to be given a loan in 2001?

33 1 0.9 Counterfactual Analysis: Survival Plots, Base Year Survivor Function Survival Time in Months

34 1 0.9 Counterfactual Analysis: Robustness: Including mortgage terms, Base Year Survivor Function Survival Time in Months

35 1 0.9 Counterfactual Analysis: Survival Plots, Base Year Survivor Function Survival Time in Months

36 1 0.9 Counterfactual Analysis: Robustness: Including mortgage terms, Base Year Survivor Function Survival Time in Months

37 Counterfactual Analysis: Survival Plots, Base Year Survivor Function Survival Time in Months

38 Counterfactual Analysis: Robustness: Including mortgage terms, Base Year Survivor Function Survival Time in Months

39 Conclusion of Counterfactual A representative borrower in 2006 (likewise for 2005 and 2007) had originated mortgages in 2001 and 2002, she would have performed significantly better than representative borrowers of vintages 2001 and 2002 respectively We fail to reject the null hypothesis for 2003 vintages: No statistically significant differences in the loan performances between the representative borrowers of 2005 or 2006 vintages and that of the 2003 vintage

40 Conclusion Difficult to argue that deterioration in underwriting for subprime mortgages led to the collapse of this market One cannot rule out that underwriting standards for subprime loans were poor to begin with. Flaw in subprime mortgage design

41 Subprime Default Probabilities

42 Additional Slides

43 DTI: Missing Values on early vintages <= Informatio n Missing % 52.40% 34.70% 0.30% 0.00% 50.30% % 48.30% 42.00% 0.10% 0.00% 40.80% % 45.40% 46.40% 0.10% 0.00% 36.90% % 44.70% 47.40% 0.10% 0.00% 34.90% % 43.80% 49.90% 0.10% 0.00% 34.80% % 44.20% 50.60% 0.00% 0.00% 29.00% % 42.20% 53.20% 0.00% 0.00% 26.30% % 39.60% 56.60% 0.00% 0.00% 30.20% % 35.50% 61.10% 0.00% 0.00% 20.30% % 35.00% 61.60% 0.00% 0.00% 31.80%

44 Prepayment Probabilities

45 Growth rate of House Prices

46 Sustainable?

47 1 0.9 Counterfactual Analysis: Robustness: Reverse Counterfactual, Base Year Survivor Function Survival Time in Months

48 1 0.8 Counterfactual Analysis: Robustness: Reverse Counterfactual, Base Year Survivor Function Survival Time in Months

49 1 0.9 Counterfactual Analysis: Robustness: Reverse Counterfactual, Base Year Survivor Function Survival Time in Months

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St. Louis Working Paper Series Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj and Rajdeep Sengupta Working

Research Division Federal Reserve Bank of St. Louis Working Paper Series Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj and Rajdeep Sengupta Working

MBS ratings and the mortgage credit boom

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

An Empirical Study on Default Factors for US Sub-prime Residential Loans

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

A Fistful of Dollars: Lobbying and the Financial Crisis

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Policy Evaluation: Methods for Testing Household Programs & Interventions

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Asymmetric information and the securitisation of SME loans

Asymmetric information and the securitisation of SME loans Ugo Albertazzi (ECB), Margherita Bottero (Bank of Italy), Leonardo Gambacorta (BIS) and Steven Ongena (U. of Zurich) 1st Annual Workshop of the

Asymmetric information and the securitisation of SME loans Ugo Albertazzi (ECB), Margherita Bottero (Bank of Italy), Leonardo Gambacorta (BIS) and Steven Ongena (U. of Zurich) 1st Annual Workshop of the

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market Lan Shi lshi@urban.org Yan (Jenny) Zhang Yan.Zhang@occ.treas.gov Presentation Sept.

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market Lan Shi lshi@urban.org Yan (Jenny) Zhang Yan.Zhang@occ.treas.gov Presentation Sept.

Sponsor-Underwriter Affiliation and Performance in Non-Agency Mortgage-Backed Securities

Sponsor-Underwriter Affiliation and Performance in Non-Agency Mortgage-Backed Securities Peng (Peter) Liu 1 Lan Shi 2 1 Cornell University 2 Office of the Comptroller of the Currency Weimer School of Advanced

Sponsor-Underwriter Affiliation and Performance in Non-Agency Mortgage-Backed Securities Peng (Peter) Liu 1 Lan Shi 2 1 Cornell University 2 Office of the Comptroller of the Currency Weimer School of Advanced

Differences Across Originators in CMBS Loan Underwriting

Differences Across Originators in CMBS Loan Underwriting Bank Structure Conference Federal Reserve Bank of Chicago, 4 May 2011 Lamont Black, Sean Chu, Andrew Cohen, and Joseph Nichols The opinions expresses

Differences Across Originators in CMBS Loan Underwriting Bank Structure Conference Federal Reserve Bank of Chicago, 4 May 2011 Lamont Black, Sean Chu, Andrew Cohen, and Joseph Nichols The opinions expresses

620 FICO, Take II: Securitization and Screening in the Subprime Mortgage Market

620, Take II: Securitization and Screening in the Subprime Mortgage Market Benjamin J. Keys Federal Reserve Board of Governors Tanmoy Mukherjee Sorin Capital Management Amit Seru Chicago Booth School of

620, Take II: Securitization and Screening in the Subprime Mortgage Market Benjamin J. Keys Federal Reserve Board of Governors Tanmoy Mukherjee Sorin Capital Management Amit Seru Chicago Booth School of

Self-reporting under SEC Reg AB and transparency in securitization: evidence from loan-level disclosure of risk factors in RMBS deals

Self-reporting under SEC Reg AB and transparency in securitization: evidence from loan-level disclosure of risk factors in RMBS deals by Joseph R. Mason, Louisiana State University Michael B. Imerman,

Self-reporting under SEC Reg AB and transparency in securitization: evidence from loan-level disclosure of risk factors in RMBS deals by Joseph R. Mason, Louisiana State University Michael B. Imerman,

Paul Gompers EMCF 2009 March 5, 2009

Paul Gompers EMCF 2009 March 5, 2009 Examine two papers that use interesting cross sectional variation to identify their tests. Find a discontinuity in the data. In how much you have to fund your pension

Paul Gompers EMCF 2009 March 5, 2009 Examine two papers that use interesting cross sectional variation to identify their tests. Find a discontinuity in the data. In how much you have to fund your pension

Loan Product Steering in Mortgage Markets

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

WORKING PAPER NO SECURITIZATION AND MORTGAGE DEFAULT: REPUTATION VS. ADVERSE SELECTION. Ronel Elul Federal Reserve Bank of Philadelphia

WORKING PAPER NO. 09-21 SECURITIZATION AND MORTGAGE DEFAULT: REPUTATION VS. ADVERSE SELECTION Ronel Elul Federal Reserve Bank of Philadelphia First version: April 29, 2009 This version: September 22, 2009

WORKING PAPER NO. 09-21 SECURITIZATION AND MORTGAGE DEFAULT: REPUTATION VS. ADVERSE SELECTION Ronel Elul Federal Reserve Bank of Philadelphia First version: April 29, 2009 This version: September 22, 2009

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013 JOSHUA WHITE AND SCOTT BAUGUESS 2 Division of Economic and Risk Analysis (DERA) U.S. Securities and Exchange

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013 JOSHUA WHITE AND SCOTT BAUGUESS 2 Division of Economic and Risk Analysis (DERA) U.S. Securities and Exchange

Pecuniary Mistakes? Payday Borrowing by Credit Union Members

Chapter 8 Pecuniary Mistakes? Payday Borrowing by Credit Union Members Susan P. Carter, Paige M. Skiba, and Jeremy Tobacman This chapter examines how households choose between financial products. We build

Chapter 8 Pecuniary Mistakes? Payday Borrowing by Credit Union Members Susan P. Carter, Paige M. Skiba, and Jeremy Tobacman This chapter examines how households choose between financial products. We build

Mortgage Delinquency and Default: A Tale of Two Options

Mortgage Delinquency and Default: A Tale of Two Options Min Hwang Song Song Robert A. Van Order George Washington University George Washington University George Washington University min@gwu.edu songsong@gwmail.gwu.edu

Mortgage Delinquency and Default: A Tale of Two Options Min Hwang Song Song Robert A. Van Order George Washington University George Washington University George Washington University min@gwu.edu songsong@gwmail.gwu.edu

Macroeconomic Adverse Selection: How Consumer Demand Drives Credit Quality

Macroeconomic Adverse Selection: How Consumer Demand Drives Credit Quality Joseph L. Breeden, CEO breeden@strategicanalytics.com 1999-2010, Strategic Analytics Inc. Preview Using Dual-time Dynamics, we

Macroeconomic Adverse Selection: How Consumer Demand Drives Credit Quality Joseph L. Breeden, CEO breeden@strategicanalytics.com 1999-2010, Strategic Analytics Inc. Preview Using Dual-time Dynamics, we

An Empirical Model of Subprime Mortgage Default from 2000 to 2007

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

What Fueled the Financial Crisis?

What Fueled the Financial Crisis? An Analysis of the Performance of Purchase and Refinance Loans Laurie S. Goodman Urban Institute Jun Zhu Urban Institute April 2018 This article will appear in a forthcoming

What Fueled the Financial Crisis? An Analysis of the Performance of Purchase and Refinance Loans Laurie S. Goodman Urban Institute Jun Zhu Urban Institute April 2018 This article will appear in a forthcoming

Household Debt and Defaults from 2000 to 2010: The Credit Supply View

Household Debt and Defaults from 2000 to 2010: The Credit Supply View Atif Mian Princeton Amir Sufi Chicago Booth July 2016 What are we trying to explain? 14000 U.S. Household Debt 12 U.S. Household Debt

Household Debt and Defaults from 2000 to 2010: The Credit Supply View Atif Mian Princeton Amir Sufi Chicago Booth July 2016 What are we trying to explain? 14000 U.S. Household Debt 12 U.S. Household Debt

The Role of Soft Information in a Dynamic Contract Setting:

The Role of Soft Information in a Dynamic Contract Setting: Evidence from the Home Equity Credit Market Sumit Agarwal Brent W. Ambrose Souphala Chomsisengphet Chunlin Liu Federal Reserve Bank of Chicago

The Role of Soft Information in a Dynamic Contract Setting: Evidence from the Home Equity Credit Market Sumit Agarwal Brent W. Ambrose Souphala Chomsisengphet Chunlin Liu Federal Reserve Bank of Chicago

Mortgage Modeling: Topics in Robustness. Robert Reeves September 2012 Bank of America

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

Transmission Mechanisms of Monetary Policy

Transmission Mechanisms of Monetary Policy Reference : Mishkin, Money, Banking and Financial Markets Chapter 26 Transmission Mechanism of Monetary Policy Transmission Mechanisms of Monetary Policy Examines

Transmission Mechanisms of Monetary Policy Reference : Mishkin, Money, Banking and Financial Markets Chapter 26 Transmission Mechanism of Monetary Policy Transmission Mechanisms of Monetary Policy Examines

The impact of the originate-to-distribute model on banks before and during the financial crisis

The impact of the originate-to-distribute model on banks before and during the financial crisis Richard J. Rosen Federal Reserve Bank of Chicago Chicago, IL 60604 rrosen@frbchi.org November 2010 Abstract:

The impact of the originate-to-distribute model on banks before and during the financial crisis Richard J. Rosen Federal Reserve Bank of Chicago Chicago, IL 60604 rrosen@frbchi.org November 2010 Abstract:

ADVERSE SELECTION IN MORTGAGE SECURITIZATION *

ADVERSE SELECTION IN MORTGAGE SECURITIZATION * Sumit Agarwal 1, Yan Chang 2, and Abdullah Yavas 3 Abstract We investigate lenders choice of loans to securitize and whether the loans they sell into the

ADVERSE SELECTION IN MORTGAGE SECURITIZATION * Sumit Agarwal 1, Yan Chang 2, and Abdullah Yavas 3 Abstract We investigate lenders choice of loans to securitize and whether the loans they sell into the

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market. Online Appendix

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

The usual disclaimer applies. The opinions are those of the discussant only and in no way involve the responsibility of the Bank of Italy.

Business Models in Banking: Is There a Best Practice? Conference Centre for Applied Research in Finance Università Bocconi September 21, 2009, Milan Tests of Ex Ante versus Ex Post Theories of Collateral

Business Models in Banking: Is There a Best Practice? Conference Centre for Applied Research in Finance Università Bocconi September 21, 2009, Milan Tests of Ex Ante versus Ex Post Theories of Collateral

Subprime Mortgage Defaults and Credit Default Swaps

THE JOURNAL OF FINANCE VOL. LXX, NO. 2 APRIL 2015 Subprime Mortgage Defaults and Credit Default Swaps ERIC ARENTSEN, DAVID C. MAUER, BRIAN ROSENLUND, HAROLD H. ZHANG, and FENG ZHAO ABSTRACT We offer the

THE JOURNAL OF FINANCE VOL. LXX, NO. 2 APRIL 2015 Subprime Mortgage Defaults and Credit Default Swaps ERIC ARENTSEN, DAVID C. MAUER, BRIAN ROSENLUND, HAROLD H. ZHANG, and FENG ZHAO ABSTRACT We offer the

The Great Surge in Mortgage Defaults : The Comparative Roles of Economic Conditions, Underwriting and Moral Hazard

The Great Surge in Mortgage Defaults 2006-2009: The Comparative Roles of Economic Conditions, Underwriting and Moral Hazard Dennis R. Capozza* and Robert Van Order** June 2010 Abstract In this paper we

The Great Surge in Mortgage Defaults 2006-2009: The Comparative Roles of Economic Conditions, Underwriting and Moral Hazard Dennis R. Capozza* and Robert Van Order** June 2010 Abstract In this paper we

New Developments in Housing Policy

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

MBS ratings and the mortgage credit boom. Adam Ashcraft Paul Goldsmith-Pinkham James Vickery * Preliminary Draft: Comments Welcome

MBS ratings and the mortgage credit boom Adam Ashcraft Paul Goldsmith-Pinkham James Vickery * Preliminary Draft: Comments Welcome First version: January 25, 2009 This version: June 30, 2009 Abstract This

MBS ratings and the mortgage credit boom Adam Ashcraft Paul Goldsmith-Pinkham James Vickery * Preliminary Draft: Comments Welcome First version: January 25, 2009 This version: June 30, 2009 Abstract This

DID PREPAYMENTS SUSTAIN THE SUBPRIME MARKET?

DID PREPAYMENTS SUSTAIN THE SUBPRIME MARKET? By Geetesh Bhardwaj, Rajdeep Sengupta November 2008 European Banking Center Discussion Paper No. 2009 09S This is also a CentER Discussion Paper No. 2009 38S

DID PREPAYMENTS SUSTAIN THE SUBPRIME MARKET? By Geetesh Bhardwaj, Rajdeep Sengupta November 2008 European Banking Center Discussion Paper No. 2009 09S This is also a CentER Discussion Paper No. 2009 38S

CRIF Lending Solutions WHITE PAPER

CRIF Lending Solutions WHITE PAPER IDENTIFYING THE OPTIMAL DTI DEFINITION THROUGH ANALYTICS CONTENTS 1 EXECUTIVE SUMMARY...3 1.1 THE TEAM... 3 1.2 OUR MISSION AND OUR APPROACH... 3 2 WHAT IS THE DTI?...4

CRIF Lending Solutions WHITE PAPER IDENTIFYING THE OPTIMAL DTI DEFINITION THROUGH ANALYTICS CONTENTS 1 EXECUTIVE SUMMARY...3 1.1 THE TEAM... 3 1.2 OUR MISSION AND OUR APPROACH... 3 2 WHAT IS THE DTI?...4

What is the micro-elasticity of mortgage demand to interest rates?

What is the micro-elasticity of mortgage demand to interest rates? Stephanie Lo 1 December 2, 2016 1 Part of this work has been performed at the Federal Reserve Bank of Boston. The views expressed in this

What is the micro-elasticity of mortgage demand to interest rates? Stephanie Lo 1 December 2, 2016 1 Part of this work has been performed at the Federal Reserve Bank of Boston. The views expressed in this

Understanding the Subprime Mortgage Crisis

Understanding the Subprime Mortgage Crisis Yuliya Demyanyk, Otto Van Hemert This Draft: August 19, 2 First Draft: October 9, 27 Abstract Using loan-level data, we analyze the quality of subprime mortgage

Understanding the Subprime Mortgage Crisis Yuliya Demyanyk, Otto Van Hemert This Draft: August 19, 2 First Draft: October 9, 27 Abstract Using loan-level data, we analyze the quality of subprime mortgage

Did Bankruptcy Reform Cause Mortgage Defaults to Rise? 1

Did Bankruptcy Reform Cause Mortgage Defaults to Rise? 1 Wenli Li, Federal Reserve Bank of Philadelphia Michelle J. White, UC San Diego and NBER and Ning Zhu, University of California, Davis Original draft:

Did Bankruptcy Reform Cause Mortgage Defaults to Rise? 1 Wenli Li, Federal Reserve Bank of Philadelphia Michelle J. White, UC San Diego and NBER and Ning Zhu, University of California, Davis Original draft:

The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations Augustin Landier Toulouse School of Economics David Sraer Princeton

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations Augustin Landier Toulouse School of Economics David Sraer Princeton

Deconstructing the Subprime Debacle Using New Indices of Underwriting Quality and Economic Conditions: A First Look 1. July 2008.

Deconstructing the Subprime Debacle Using New Indices of Underwriting Quality and Economic Conditions: A First Look 1 (Formerly titled: Subprime Mortgage Defaults, Loan Underwriting and Local Economic

Deconstructing the Subprime Debacle Using New Indices of Underwriting Quality and Economic Conditions: A First Look 1 (Formerly titled: Subprime Mortgage Defaults, Loan Underwriting and Local Economic

Challenges and Opportunities for Low Downpayment Lending

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Wells Fargo Bank, N.A. General Information Statement

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

A Look Behind the Numbers: Subprime Loan Report for Youngstown

Page1 A Look Behind the Numbers is a publication of the Federal Reserve Bank of Cleveland s Community Development group. Through data analysis, these reports examine issues relating to access to credit

Page1 A Look Behind the Numbers is a publication of the Federal Reserve Bank of Cleveland s Community Development group. Through data analysis, these reports examine issues relating to access to credit

Complex Mortgages. May 2014

Complex Mortgages Gene Amromin, Federal Reserve Bank of Chicago Jennifer Huang, Cheung Kong Graduate School of Business Clemens Sialm, University of Texas-Austin and NBER Edward Zhong, University of Wisconsin

Complex Mortgages Gene Amromin, Federal Reserve Bank of Chicago Jennifer Huang, Cheung Kong Graduate School of Business Clemens Sialm, University of Texas-Austin and NBER Edward Zhong, University of Wisconsin

Subprime Loan Performance

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao October 2, 2014 Abstract Regulation AB (Reg AB) enacted in 2006 mandates

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao October 2, 2014 Abstract Regulation AB (Reg AB) enacted in 2006 mandates

How Do Financial Frictions Shape the Product Market? Evidence from Mortgage Originations

How Do Financial Frictions Shape the Product Market? Evidence from Mortgage Originations James Vickery Federal Reserve Bank of New York and NYU Stern This Version: October 2007 Abstract: I present evidence

How Do Financial Frictions Shape the Product Market? Evidence from Mortgage Originations James Vickery Federal Reserve Bank of New York and NYU Stern This Version: October 2007 Abstract: I present evidence

The Effects of Mortgage Credit Availability: Evidence from Minimum Credit Score Lending Rules

The Effects of Mortgage Credit Availability: Evidence from Minimum Credit Score Lending Rules Steven Laufer and Andrew Paciorek Board of Governors of the Federal Reserve System December 8, 2016 Abstract

The Effects of Mortgage Credit Availability: Evidence from Minimum Credit Score Lending Rules Steven Laufer and Andrew Paciorek Board of Governors of the Federal Reserve System December 8, 2016 Abstract

Challenges to E ective Renegotiation of Residential Mortgages

Challenges to E ective Renegotiation of Residential Mortgages Tomek Piskorski Edward S. Gordon Associate Professor of Real Estate and Finance Columbia Business School July 2012 (Columbia Business School)

Challenges to E ective Renegotiation of Residential Mortgages Tomek Piskorski Edward S. Gordon Associate Professor of Real Estate and Finance Columbia Business School July 2012 (Columbia Business School)

Discussion of Relationship and Transaction Lending in a Crisis

Discussion of Relationship and Transaction Lending in a Crisis Philipp Schnabl NYU Stern, CEPR, and NBER USC Conference December 14, 2013 Summary 1 Research Question How does relationship lending vary

Discussion of Relationship and Transaction Lending in a Crisis Philipp Schnabl NYU Stern, CEPR, and NBER USC Conference December 14, 2013 Summary 1 Research Question How does relationship lending vary

Deconstructing the Subprime Debacle Using New Indices of Underwriting Quality and Economic Conditions: A First Look 1. July 2008.

Deconstructing the Subprime Debacle Using New Indices of Underwriting Quality and Economic Conditions: A First Look 1 (Formerly titled: Subprime Mortgage Defaults, Loan Underwriting and Local Economic

Deconstructing the Subprime Debacle Using New Indices of Underwriting Quality and Economic Conditions: A First Look 1 (Formerly titled: Subprime Mortgage Defaults, Loan Underwriting and Local Economic

Risky Borrowers or Risky Mortgages?

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Adverse Selection on Maturity: Evidence from On-Line Consumer Credit

Adverse Selection on Maturity: Evidence from On-Line Consumer Credit Andrew Hertzberg (Columbia) with Andrés Liberman (NYU) and Daniel Paravisini (LSE) Credit and Payments Markets Oct 2 2015 The role of

Adverse Selection on Maturity: Evidence from On-Line Consumer Credit Andrew Hertzberg (Columbia) with Andrés Liberman (NYU) and Daniel Paravisini (LSE) Credit and Payments Markets Oct 2 2015 The role of

Underwriting versus economy: a new approach to decomposing mortgage losses

The Journal of Credit Risk (19 41) Volume 5/Number 2, Summer 2009 Underwriting versus economy: a new approach to decomposing mortgage losses Ashish Das Moody s Investors Service, 250 Greenwich Street,

The Journal of Credit Risk (19 41) Volume 5/Number 2, Summer 2009 Underwriting versus economy: a new approach to decomposing mortgage losses Ashish Das Moody s Investors Service, 250 Greenwich Street,

Securitization and the Fixed-Rate Mortgage

Securitization and the Fixed-Rate Mortgage Andreas Fuster and James Vickery August 28, 2012 Preliminary and incomplete: please do not circulate without permission Abstract Fixed-rate mortgages (FRMs) dominate

Securitization and the Fixed-Rate Mortgage Andreas Fuster and James Vickery August 28, 2012 Preliminary and incomplete: please do not circulate without permission Abstract Fixed-rate mortgages (FRMs) dominate

Individual and Neighborhood Effects on FHA Mortgage Activity: Evidence from HMDA Data

JOURNAL OF HOUSING ECONOMICS 7, 343 376 (1998) ARTICLE NO. HE980238 Individual and Neighborhood Effects on FHA Mortgage Activity: Evidence from HMDA Data Zeynep Önder* Faculty of Business Administration,

JOURNAL OF HOUSING ECONOMICS 7, 343 376 (1998) ARTICLE NO. HE980238 Individual and Neighborhood Effects on FHA Mortgage Activity: Evidence from HMDA Data Zeynep Önder* Faculty of Business Administration,

Banks Incentives and the Quality of Internal Risk Models

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

Wells Fargo Bank, N.A. General Information Statement

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

The Untold Costs of Subprime Lending: Communities of Color in California. Carolina Reid. Federal Reserve Bank of San Francisco.

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

How Do Financial Frictions Shape the Product Market? Evidence from Mortgage Originations

How Do Financial Frictions Shape the Product Market? Evidence from Mortgage Originations James Vickery Federal Reserve Bank of New York and NYU Stern This Version: October 2007 Abstract: I present evidence

How Do Financial Frictions Shape the Product Market? Evidence from Mortgage Originations James Vickery Federal Reserve Bank of New York and NYU Stern This Version: October 2007 Abstract: I present evidence

The Interest Rate Elasticity of Mortgage Demand: Evidence from Bunching at the Conforming Loan Limit (Online Appendix)

") The Interest Rate Elasticity of Mortgage Demand: Evidence from Bunching at the Conforming Loan Limit (Online Appendix) Anthony A. DeFusco Kellogg School of Management Northwestern University Andrew Paciorek

The Interest Rate Elasticity of Mortgage Demand: Evidence from Bunching at the Conforming Loan Limit (Online Appendix) Anthony A. DeFusco Kellogg School of Management Northwestern University Andrew Paciorek

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

How CECL Will Impact Your Credit Union & What You Can Do to Prepare For It. Randy C Thompson, Ph.D. TCT Risk Solutions, LLC

Attitude The longer I live, the more I realize the impact of attitude on life. Attitude to me, is more important than facts. It is more important than the past, than education, than money, than circumstances,

Attitude The longer I live, the more I realize the impact of attitude on life. Attitude to me, is more important than facts. It is more important than the past, than education, than money, than circumstances,

NBER WORKING PAPER SERIES IS THE FHA CREATING SUSTAINABLE HOMEOWNERSHIP? Andrew Caplin Anna Cororaton Joseph Tracy

NBER WORKING PAPER SERIES IS THE FHA CREATING SUSTAINABLE HOMEOWNERSHIP? Andrew Caplin Anna Cororaton Joseph Tracy Working Paper 18190 http://www.nber.org/papers/w18190 NATIONAL BUREAU OF ECONOMIC RESEARCH

NBER WORKING PAPER SERIES IS THE FHA CREATING SUSTAINABLE HOMEOWNERSHIP? Andrew Caplin Anna Cororaton Joseph Tracy Working Paper 18190 http://www.nber.org/papers/w18190 NATIONAL BUREAU OF ECONOMIC RESEARCH

P2.T6. Credit Risk Measurement & Management. Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit

P2.T6. Credit Risk Measurement & Management Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Reading 48 By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T6. Credit Risk Measurement & Management Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Reading 48 By David Harper, CFA FRM CIPM www.bionicturtle.com

Asymmetric information and the securitization of SME loans

Ugo Albertazzi (Bank of Italy) Margherita Bottero (Bank of Italy) Leonardo Gambacorta (Bank for International Settlements and CEPR) Steven Ongena (University of Zurich, Swiss Finance Institute, KU Leuven

Ugo Albertazzi (Bank of Italy) Margherita Bottero (Bank of Italy) Leonardo Gambacorta (Bank for International Settlements and CEPR) Steven Ongena (University of Zurich, Swiss Finance Institute, KU Leuven

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments. Morgan J. Rose. March 2011

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

When in a hole stop digging.

When in a hole stop digging. The Commission s application of the Principles of Restructuring Aid to Banks during the Financial Crisis Christian Ahlborn and Daniel Piccinin Brussels, 5 November 2009 Overview.

When in a hole stop digging. The Commission s application of the Principles of Restructuring Aid to Banks during the Financial Crisis Christian Ahlborn and Daniel Piccinin Brussels, 5 November 2009 Overview.

DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST. Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth)

Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth)") 1 DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth) 2 Motivation Lasting impact of the 2008 mortgage crisis on

1 DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth) 2 Motivation Lasting impact of the 2008 mortgage crisis on

Backloaded Mortgages and House Price Appreciation

1 / 33 Backloaded Mortgages and House Price Appreciation Gadi Barlevy Jonas D. M. Fisher Chicago Fed Wisconsin-Fed HULM Conference April 9-10, 2010 2 / 33 Introduction: Motivation Widespread house price

1 / 33 Backloaded Mortgages and House Price Appreciation Gadi Barlevy Jonas D. M. Fisher Chicago Fed Wisconsin-Fed HULM Conference April 9-10, 2010 2 / 33 Introduction: Motivation Widespread house price

The Impact of Second Loans on Subprime Mortgage Defaults

The Impact of Second Loans on Subprime Mortgage Defaults by Michael D. Eriksen 1, James B. Kau 2, and Donald C. Keenan 3 Abstract An estimated 12.6% of primary mortgage loans were simultaneously originated

The Impact of Second Loans on Subprime Mortgage Defaults by Michael D. Eriksen 1, James B. Kau 2, and Donald C. Keenan 3 Abstract An estimated 12.6% of primary mortgage loans were simultaneously originated

Strategic Default in joint liability groups: Evidence from a natural experiment in India

Strategic Default in joint liability groups: Evidence from a natural experiment in India Xavier Gine World Bank Karuna Krishnaswamy IFMR Alejandro Ponce World Justice Project CIRANO, November 9-10, 2012

Strategic Default in joint liability groups: Evidence from a natural experiment in India Xavier Gine World Bank Karuna Krishnaswamy IFMR Alejandro Ponce World Justice Project CIRANO, November 9-10, 2012

ASYMMETRIC INFORMATION IN THE ADJUSTABLE-RATE MORTGAGE MARKET

ASYMMETRIC INFORMATION IN THE ADJUSTABLE-RATE MORTGAGE MARKET Arpit Gupta Columbia Business School Christopher Hansman Columbia University January 31, 2015 PRELIMINARY AND INCOMPLETE, PLEASE DO NOT CITE

ASYMMETRIC INFORMATION IN THE ADJUSTABLE-RATE MORTGAGE MARKET Arpit Gupta Columbia Business School Christopher Hansman Columbia University January 31, 2015 PRELIMINARY AND INCOMPLETE, PLEASE DO NOT CITE

Prediction errors in credit loss forecasting models based on macroeconomic data

Prediction errors in credit loss forecasting models based on macroeconomic data Eric McVittie Experian Decision Analytics Credit Scoring & Credit Control XIII August 2013 University of Edinburgh Business

Prediction errors in credit loss forecasting models based on macroeconomic data Eric McVittie Experian Decision Analytics Credit Scoring & Credit Control XIII August 2013 University of Edinburgh Business

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Understanding the Subprime Crisis

Chapter 1 Understanding the Subprime Crisis In collaboration with Thomas Sullivan and Jeremy Scheer It is often said that, hindsight is 20/20, a saying which rings especially true when considering an event

Chapter 1 Understanding the Subprime Crisis In collaboration with Thomas Sullivan and Jeremy Scheer It is often said that, hindsight is 20/20, a saying which rings especially true when considering an event

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO CASH FLOW ANALYSIS

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO CASH FLOW ANALYSIS Kyle S. Mrotek, FCAS, MAAA Neal Dihora, ASA, CFA CAS Spring Meeting 1 Disclaimer This presentation contains our views and these views

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO CASH FLOW ANALYSIS Kyle S. Mrotek, FCAS, MAAA Neal Dihora, ASA, CFA CAS Spring Meeting 1 Disclaimer This presentation contains our views and these views

Further Investigations into the Origin of Credit Score Cutoff Rules

Further Investigations into the Origin of Credit Score Cutoff Rules Ryan Bubb and Alex Kaufman No. 11-12 Abstract: Keys, Mukherjee, and Vig (2010a) argue that the evidence presented in Bubb and Kaufman

Further Investigations into the Origin of Credit Score Cutoff Rules Ryan Bubb and Alex Kaufman No. 11-12 Abstract: Keys, Mukherjee, and Vig (2010a) argue that the evidence presented in Bubb and Kaufman

Predatory Lending Laws and the Cost of Credit

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2008 Predatory Lending Laws and the Cost of Credit Anthony Pennington-Cross Marquette

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2008 Predatory Lending Laws and the Cost of Credit Anthony Pennington-Cross Marquette

The Benefits of Pre-Purchase Homeownership Counseling

Gabriela Avila Hoa Nguyen Peter Zorn The Benefits of Pre-Purchase Homeownership Counseling February 20, 2013 Introduction Motivation:» First-time home buyer programs are a valuable public policy vehicle

Gabriela Avila Hoa Nguyen Peter Zorn The Benefits of Pre-Purchase Homeownership Counseling February 20, 2013 Introduction Motivation:» First-time home buyer programs are a valuable public policy vehicle

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom?

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Study on the costs and benefits of the different policy options for mortgage credit. Annex D

Study on the costs and benefits of the different policy options for mortgage credit Annex D Description of early repayment and responsible lending and borrowing model European Commission, Internal Markets

Study on the costs and benefits of the different policy options for mortgage credit Annex D Description of early repayment and responsible lending and borrowing model European Commission, Internal Markets

Loan Contracting in the Presence of Usury Limits: Evidence from Auto Lending

Loan Contracting in the Presence of Usury Limits: Evidence from Auto Lending Brian T. Melzer Kellogg School of Management Northwestern University Aaron Schroeder Consumer Financial Protection Bureau GWU-FRB

Loan Contracting in the Presence of Usury Limits: Evidence from Auto Lending Brian T. Melzer Kellogg School of Management Northwestern University Aaron Schroeder Consumer Financial Protection Bureau GWU-FRB

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2010-38 December 20, 2010 Risky Mortgages and Mortgage Default Premiums BY JOHN KRAINER AND STEPHEN LEROY Mortgage lenders impose a default premium on the loans they originate to

FRBSF ECONOMIC LETTER 2010-38 December 20, 2010 Risky Mortgages and Mortgage Default Premiums BY JOHN KRAINER AND STEPHEN LEROY Mortgage lenders impose a default premium on the loans they originate to

Market Variables and Financial Distress. Giovanni Fernandez Stetson University

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

Fannie Mae Raises the DTI Limit

H O U S I N G F I N A N C E P O L I C Y C E N T E R Fannie Mae Raises the DTI Limit A Win for Expanding Access to Credit Edward Golding, Laurie Goodman, and Jun Zhu July 2017 In a May 30, 2017, notice,

H O U S I N G F I N A N C E P O L I C Y C E N T E R Fannie Mae Raises the DTI Limit A Win for Expanding Access to Credit Edward Golding, Laurie Goodman, and Jun Zhu July 2017 In a May 30, 2017, notice,

ARMs: An Overview. Fin 4713 ARM Notes. ARMs: Mechanics. Some ARM Indexes

Slide 1 ARMs: An Overview Slide 2 Fin 4713 ARM Notes The interest rate charged on the note is indexed to other market interest rates The loan payment is adjusted at specified periods. The interest rate

Slide 1 ARMs: An Overview Slide 2 Fin 4713 ARM Notes The interest rate charged on the note is indexed to other market interest rates The loan payment is adjusted at specified periods. The interest rate

High-Cost Debt and Borrower Reputation: Evidence. from the U.K.

High-Cost Debt and Borrower Reputation: Evidence from the U.K. Andres Liberman Daniel Paravisini Vikram Pathania October 2016 Abstract When taking up high-cost debt signals poor credit risk to lenders,

High-Cost Debt and Borrower Reputation: Evidence from the U.K. Andres Liberman Daniel Paravisini Vikram Pathania October 2016 Abstract When taking up high-cost debt signals poor credit risk to lenders,

We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal, (X2)

to estimate the optimal, (X2)") Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Low Income Homeownership and the Role of State Subsidies: A Comparative Analysis of Mortgage Outcomes. Stephanie Moulton 1 The Ohio State University

Low Income Homeownership and the Role of State Subsidies: A Comparative Analysis of Mortgage Outcomes Stephanie Moulton 1 The Ohio State University Matthew Record 2 The Ohio State University and San Jose

Low Income Homeownership and the Role of State Subsidies: A Comparative Analysis of Mortgage Outcomes Stephanie Moulton 1 The Ohio State University Matthew Record 2 The Ohio State University and San Jose

Household Finance Session: Annette Vissing-Jorgensen, Northwestern University

Household Finance Session: Annette Vissing-Jorgensen, Northwestern University This session is about household default, with a focus on: (1) Credit supply to individuals who have defaulted: Brevoort and

Household Finance Session: Annette Vissing-Jorgensen, Northwestern University This session is about household default, with a focus on: (1) Credit supply to individuals who have defaulted: Brevoort and

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

The Subprime Crisis: Lessons about Market Discipline

The Subprime Crisis: Lessons about Market Discipline Mark J. Flannery University of Florida Eleventh International Banking Conference, The Credit Market Turmoil of 2007 08: Implications for Public Policy,

The Subprime Crisis: Lessons about Market Discipline Mark J. Flannery University of Florida Eleventh International Banking Conference, The Credit Market Turmoil of 2007 08: Implications for Public Policy,

Federal Reserve Bank of Chicago

Federal Reserve Bank of Chicago The Mortgage Rate Conundrum Alejandro Justiniano, Giorgio E. Primiceri, and Andrea Tambalotti August 2017 WP 2017-23 * Working papers are not edited, and all opinions and

Federal Reserve Bank of Chicago The Mortgage Rate Conundrum Alejandro Justiniano, Giorgio E. Primiceri, and Andrea Tambalotti August 2017 WP 2017-23 * Working papers are not edited, and all opinions and

Announcement March 5, Updates and Clarifications for Streamlined Refinance Products

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices?

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

The Economic Power of Uncertainty: The Role of Consumer Credit Bureaus

The Economic Power of Uncertainty: The Role of Consumer Credit Bureaus Federal Reserve Forum on Credit Scores December 14, 2007 Matt Fellowes, Fellow The Economic Power of Uncertainty: The Role of Consumer

The Economic Power of Uncertainty: The Role of Consumer Credit Bureaus Federal Reserve Forum on Credit Scores December 14, 2007 Matt Fellowes, Fellow The Economic Power of Uncertainty: The Role of Consumer

Written Testimony By Anthony M. Yezer Professor of Economics George Washington University

Written Testimony By Anthony M. Yezer Professor of Economics George Washington University U.S. House of Representatives Committee on Financial Services Subcommittee on Housing and Community Opportunity

Written Testimony By Anthony M. Yezer Professor of Economics George Washington University U.S. House of Representatives Committee on Financial Services Subcommittee on Housing and Community Opportunity

The Subprime Market Meltdown: Crisis or Opportunity?

The Subprime Market Meltdown: Crisis or Opportunity? Jonathan Beinner CIO and Co-Head, US and Global Fixed Income, GSM Tom Teles Head, Mortgage Backed Securities, GSM July 10, 2007 Discussion outline.

The Subprime Market Meltdown: Crisis or Opportunity? Jonathan Beinner CIO and Co-Head, US and Global Fixed Income, GSM Tom Teles Head, Mortgage Backed Securities, GSM July 10, 2007 Discussion outline.

Credit-Induced Boom and Bust

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great