Household Finance Session: Annette Vissing-Jorgensen, Northwestern University

|

|

|

- Jade Webster

- 5 years ago

- Views:

Transcription

1 Household Finance Session: Annette Vissing-Jorgensen, Northwestern University This session is about household default, with a focus on: (1) Credit supply to individuals who have defaulted: Brevoort and Cooper: Credit score recovery after foreclosure Han, Keys and Li: Credit card offers after bankruptcy (2) Determinants of default: Ergungor and Moulton: Why do mortgages originated by banks have lower default rates?

2 Why do we care how much credit is extended post-default? Households care -- it affects their decision on whether to default It teaches us something about what drives default If there are long-lasting adverse effects, then default signals a ``risk type'' (preferences, resources, ability to plan) or shocks with more permanent effects, as opposed to e.g. exogenous house price declines. It affects optimal policy: Optimal policy balances: (White, JEP, 2007) - Need for consumption insurance --> Default should be easy. - Need to reduce moral hazard on the part of borrowers (defaulting has a negative externality on other borrowers via higher interest rates/reduced credit) --> Default should be hard. The stricter credit access/terms are post-default, the more proborrower legal rules for default should be.

3 Brevoort and Cooper: ``Foreclosure s Wake: the Credit Experiences of Individuals Following Foreclosure Objective: To understand ``how access to credit, as reflected in individual credit scores, is affected by foreclosure and whether these effects persist over time. Data: Enormous panel of US individual credit records from Equifax, quarterly from Q1. 345,360 individuals who had a foreclosure at some point between 2000 and ``Historical'' cohorts: Foreclosure in ``Recent'' cohorts: Foreclosure in

4 Findings: (1) Credit scores in the foreclosure quarter are much lower than predelinquency scores Down an average of 110 to 210 points. More for higher pre-delinquency scores and for recent cohorts. (2) Credit score recovery is quite slow -- and slower for higher predelinquency scores and for recent cohorts. - After 2 years, historically, over 60% of pre-delinquency subprime borrowers scores are back to their initial level. Only 10% of pre-delinquency prime borrowers scores are back to initial level. - For recent cohorts, about 5 to 10 pct points fewer have recovered by 2 years (depending on pre-delinquency score).

5 (3) Slow recovery is likely due to credit card and auto loan delinquencies remaining above pre-foreclosure levels as long as 5 years after foreclosure. (4) Attempt to argue that effect of foreclosure on subsequent delinquencies are causal: - Individuals with major mortgage delinquencies but no foreclosure have lower delinquency rates going forward than those with a foreclosure. - High post-foreclosure delinquency rates even for a sample with no delinquencies for 12 quarters before six months prior to the foreclosure period. (5) Strategic defaulters (due do house price declines) have higher delinquency rates post-foreclosure than others with foreclosures in the same time period.

6 Comment 1: The paper is struggling with causality At the end of the paper, the authors suggest three interpretations of their finding that credit scores recover slowly due to persistently high postforeclosure delinquencies: a) A causal impact of foreclosures on credit access/credit cost/wealth making subsequent delinquencies more likely b) A causal impact of foreclosures on borrower repayment incentive (why pay, low score anyway) or on non-payment stigma c) Effects of foreclosure are not causal but due to a trigger event such as job loss, divorce, health shock. And effects of these shocks may be persistent.

7 Authors conclude that: ``With the data available, we are unable to identify the reasons for this change in behavior.'' ``It is difficult to determine to what extent (if any) the effects documented in this paper are the result of the foreclosure process itself or other causes." This should be discussed more upfront. If the authors don't really like their own causality tests, then maybe don't show them. (Comparison to a sample of delinquent borrowers who did not enter foreclosure is not convincing -- as the authors recognize, those who did not have foreclosure may just have smaller underlying shocks.)

8 Suggestion: Use judicial foreclosure instrument from Pence (2006) and Mian, Sufi and Trebbi (2010) to show causal effects of foreclosures. 21 states require a judicial foreclosure: A lender must sue a borrower in court before conducting an auction to sell the property. In states without this requirement, lenders have the right to sell the house after providing only a notice of sale to the borrower (a non-judicial foreclosure). States with non-judicial foreclosure have substantially higher rates of foreclosures per home owner and per mortgage delinquency. To my knowledge, credit score formulas do not differ by state. If not, then this is a useful instrument.

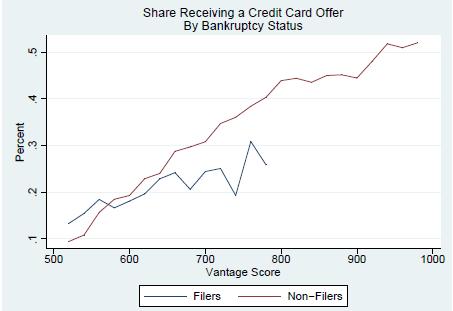

9 Comment 2: Credit scores are not a sufficient statistic for credit supply and credit terms Bankruptcy lowers credit supply dramatically, even controlling for credit score: Han, Keys and Li (2011). Makes sense in that bankruptcy increases default-probabilities (on new debt post-bankruptcy), even controlling for credit score: Cohen-Cole, Duygan-Bump and Montoriol-Garriga (2010). The same may be true for foreclosures. Importantly, recovery in credits scores may substantially overstate recovery in credit supply and terms. Graphs from Han, Keys and Li (2011). As credit scores recover, the improvement in credit supply and terms is much weaker for bankruptcy filers than non-filers.

10

11 Suggestion: Ask Han, Keys and Li (2011) to check how these graph look for foreclosures (as opposed to bankruptcies).

12 Comment 3: Suggestion -- show how fast credit scores recover for people with no further delinquencies Currently the paper cites credit bureaus for saying that scores could recover quickly. Why not just look at the data! This would clearly show whether slow credit score recovery is due to further delinquencies or not. Would also be interesting to do this for strategic defaulters to see if scores recover faster or slower for strategic defaulters with no further delinquencies. Comment 4: Suggestion -- merge in better demographic and economic controls at census tract level As Cohen-Cole, Duygan-Bump and Montoriol-Garriga (2010) and Ergungor and Moulton (2011).

13 Han, Keys and Li: ``Credit Supply to Bankrupt Consumers: Evidence from Credit Card Mailings'' Question: Are bankrupt consumers excluded from the unsecured credit market? Methodology: Analyze credit supply using novel data set on credit card mail offers. Data: Mintel Comperemedia proprietory survey on credit offers to U.S. consumers. Includes detailed demographics. 3,000 consumers per month, repeated cross-sections, August 2009 to July Merged with credit history information from TransUnion.

14 Findings: (1) Bankruptcy filers receive a lot of credit card offers, though less than observationally similar non-filers: 22 (40) percent of filers (non-filers) receive >=1 offer in a given month. With controls: Filers have a 7 pct point lower prob. of receiving at least one credit card offer in a given month. Driven by those >2 years past filing. (2) But offers to filers are much less attractive than offers to non-filers. Controlling for observables, including credit scores, filers have: 80 bps higher interest rate. 30 percent lower credit limit 50 percent lower probability of receiving any rewards (e.g. miles), yet are 50 percent more likely to pay annual fee. More ``shrouded costs'' than non-filers (worse terms for balance transfers, worse cash-back rates, higher minimum finance charges etc.) (3) Filers benefit less from improving their credit scores (credit limits, terms).

15 Comment 1: The authors understate how bad filing for bankruptcy is for credit supply for two reasons Reason A: Not meaningful to ignore indirect effects via credit scores It is highly misleading when the authors conclude that ``consumers that file for bankruptcy within the previous two years are at least as likely to receive credit card offers as comparable non-filers'' We care about the total effect of bankruptcy on credit supply, including the indirect effect via bankruptcy's effect on credit scores. If credit score happened to be a sufficient statistic for credit risk, and bankruptcy massively lowers the credit score, the current methodology would say that bankruptcy has no effect on credit supply even if it has a huge effect.

16 Of course, if you don't control for credit score, you may worry that some unobservable (to us but not lenders) is driving both credit supply and bankruptcy. So keep credit scores in regressions, but add rows reporting the total effect. In particular, ask Brevoort and Cooper to estimate the immediate effect of a bankruptcy filing on credit scores in their panel data. Then use this to calculate the total effect of bankruptcy on the outcome variables as: Total effect of bankruptcy on outcome variable =Direct effect of being filer +(Immediate effect of a bankruptcy filing on credit score) *Effect of that credit score change on outcome variable (This will be more accurate for people filing recently.)

17 Suppose bankruptcy lowers credit score by 150 points from 850 to 700. Then the effect of bankruptcy on the various outcome variables in Table 5 is: And total effects are large even for those who filed within the previous two years.

18 Comment 1: The authors understate how bad filing for bankruptcy is for credit supply for two reasons Reason B: New credit offers are not equal to total credit supply. Authors emphasize that they are the first to measure credit supply rather than equilibrium amounts of debt (quantities) and equilibrium interest rates (prices). However, this is not exactly right: They are the first to measure NEW supply, not TOTAL supply. When the authors find that ``consumers that file for bankruptcy within the previous two years are at least as likely to receive credit card offers as comparable non-filers''

19 This doesn't mean that they face the same credit supply as non-filers, since non-filers already have lots of cards compared to people who just had theirs cancelled due to bankruptcy. You could in principle observe that filers receive more offers than non-files without this implying any difference in total credit supply! Extreme example: - Suppose people have very high (time) costs of switching cards. - Non-filers already have lots of credit cards. Filers have none or not many (at first). - Then it's more profitable to send offers to people who have no cards, i.e. people who just went bankrupt (and 20 year olds). - Non-filers could get less offers because they have plentiful credit supply from their current lenders.

20 So what can we learn from studying offers: - Something about who it is profitable to send cards to (perhaps less interesting) - A lot about terms of credit (interesting) - Not as much about total supply of credit. Comment 2: Suggestion -- deemphasize analysis of effects by time since filing. This is not a good data set for analyzing that Everyone in the data are surveyed within 1 calendar year (August 2009 to July 2010) Therefore, those who filed longer ago will mechanically have filed in an earlier calendar year. So not clear which effect is being picked up.

21 For example: Those who filed 6-9 years ago are people who filed in , i.e. before the 2005 bankruptcy reform. They tend to get fewer offers with lower credit limits, but this may not mean that credit supply changes as you get closer to the 8 year cutoff for being able to file again. Instead, it may mean that those who filed back when filing was easier are different than those who filed after it got harder.

22 Ergungor and Moulton: ``Beyond the Transaction: Depository Institutions and Reduced mortgage Default for Low Income Homebuyers'' Question: Why are default rates on mortgages originated by banks lower, even controlling for credit scores, borrower characteristics and loan terms? Authors test for presence of an information effect: Local banks have soft information about borrower default risk. The alternative is some type of institution effect (e.g. banks don't want to take on as much risk for various regulatory reasons, but no specific test). Predictions: Within banks, localness matters (more so for borrowers with low credit for which soft information likely matters more). Under the alternative bank vs. non-bank matters, localness does not.

23 Methodology: Estimate effect of lender on delinquency or default Interested in actual lender effect Control for predicted probability of picking particular lender. Instruments: Convenience (measured based on geographic proximity) and approval probability (measured as last year's denial rate of institution type). Data: 18,370 loans to low and middle income borrowers made under Ohio's mortgage revenue bond program from All loans have same terms and servicer at a given point in time. Servicing data from January, 2005-February 2011.

24 Findings: Controlling for observables, 1 pct point lower default rate (Table 5) for bank-originated loans than non-bank originated loans. Mean default rate is 7.3 percent. There is a slight information effect overall: Relative to non-bank loans......loans originated by a local bank (branch <2 miles from borrower's new or old address) have 1 pct point lower default risk...loans originated by a non-local bank have 0.7 pct point lower default risk But local vs. non-local difference not significant. Evidence for an information effect is stronger when focusing on local vs. non-local branches of large banks (-1.3 pct point local vs pct point non-local) or when focusing on subprime borrowers (-3 pct point local vs. -1 pct point non-local).

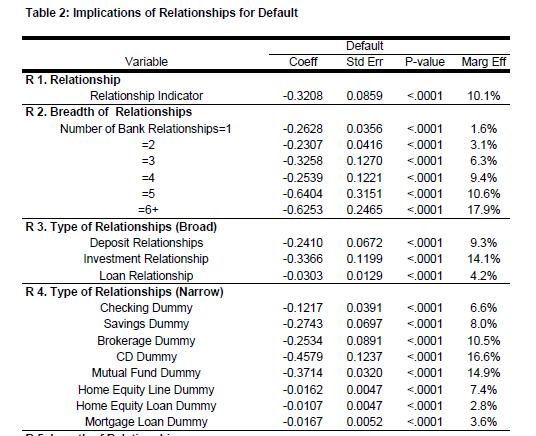

25 Comment 1: It seems likely that an information effect should be present in bank mortgage lending Evidence from Agarwal, Chomsisengphet, Liu, and Souleles (2009) shows strong reduction in default rate on credit cards the more involved the customer is with the lender: (Avg default rate is 5.6% if no relationship. Marginals are in pct, not pct points.)

26

27 Comment 2: But the current setting is not straightforward to analyze Complication: Loans are all sold to a party that does not have the soft info. Theory: o Need to generalize standard models of soft information to setting with securitization. Do prices reflect soft information in equilibrium? o How do things differ as a function of whether lenders are allowed to compete on loan terms or not (here the are not). Empirical work: o Can prices at which loans are sold to the master-servicer be obtained. Do prices in fact reflect soft information? o Does the regulatory setup say anything about pricing? In general, clarify exactly how this mortgage revenue bond program works. o How are price patterns affected by the master-servicer having monopoly power?

28 Pricing matters for how much incentive local banks have to use their soft information and for how results generalize to unregulated setting If soft information is not reflected in pricing, then all lenders should just approve everyone who qualifies (they receive a 1% origination fee). Authors argue that local banks would always use the soft information because they view themselves as having a long-term relationship with the borrower and it is not in the borrower's interest to borrow if he cannot repay. But is it in the bank's profit maximizing interest to reject?

29 Comment 3: Direct evidence that local banks act on soft information would be great Borrowers differ in credit risk based on observables: Borrowed from: Non-bank: 676. Non-local bank: 686. Local bank: 694 Can we rule out that they don't simply differ in the same way based on unobservables and that this drives the results, with no active role played by originators? We need to show that local banks act on their soft information: (1) Sometimes reject despite favorable hard information: Does data on rejections exist? Complication: Borrower behavior adjusts. (2) Sometimes don't reject despite unfavorable hard information Related soft information tests in Hochberg, Ljungqvist and Vissing- Jorgensen (2010) in venture capital setting.

ECONOMIC COMMENTARY. Americans Cut Their Debt Yuliya Demyanyk and Matthew Koepke

ECONOMIC COMMENTARY Number 2012-11 August 8, 2012 Americans Cut Their Debt Yuliya Demyanyk and Matthew Koepke The Great Recession brought an end to a 20-year expansion of consumer debt. In its wake is

ECONOMIC COMMENTARY Number 2012-11 August 8, 2012 Americans Cut Their Debt Yuliya Demyanyk and Matthew Koepke The Great Recession brought an end to a 20-year expansion of consumer debt. In its wake is

Fresh Start in Bankruptcy

Renuka Sane 29 July 2016 Fresh start The opportunity to begin a new financial chapter The term is used in the context of discharge how many years does an individual have to wait before being discharged

Renuka Sane 29 July 2016 Fresh start The opportunity to begin a new financial chapter The term is used in the context of discharge how many years does an individual have to wait before being discharged

CRIF Lending Solutions WHITE PAPER

CRIF Lending Solutions WHITE PAPER IDENTIFYING THE OPTIMAL DTI DEFINITION THROUGH ANALYTICS CONTENTS 1 EXECUTIVE SUMMARY...3 1.1 THE TEAM... 3 1.2 OUR MISSION AND OUR APPROACH... 3 2 WHAT IS THE DTI?...4

CRIF Lending Solutions WHITE PAPER IDENTIFYING THE OPTIMAL DTI DEFINITION THROUGH ANALYTICS CONTENTS 1 EXECUTIVE SUMMARY...3 1.1 THE TEAM... 3 1.2 OUR MISSION AND OUR APPROACH... 3 2 WHAT IS THE DTI?...4

ECONOMIC COMMENTARY. Three Myths about Peer-to-Peer Loans. Yuliya Demyanyk, Elena Loutskina, and Daniel Kolliner

ECONOMIC COMMENTARY Number 2017-18 November 9, 2017 Three Myths about Peer-to-Peer Loans Yuliya Demyanyk, Elena Loutskina, and Daniel Kolliner Peer-to-peer lending platforms, which provide a way for individuals

ECONOMIC COMMENTARY Number 2017-18 November 9, 2017 Three Myths about Peer-to-Peer Loans Yuliya Demyanyk, Elena Loutskina, and Daniel Kolliner Peer-to-peer lending platforms, which provide a way for individuals

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

An Evaluation of Research on the Performance of Loans with Down Payment Assistance

George Mason University School of Public Policy Center for Regional Analysis An Evaluation of Research on the Performance of Loans with Down Payment Assistance by Lisa A. Fowler, PhD Stephen S. Fuller,

George Mason University School of Public Policy Center for Regional Analysis An Evaluation of Research on the Performance of Loans with Down Payment Assistance by Lisa A. Fowler, PhD Stephen S. Fuller,

Credit-Induced Boom and Bust

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

CFPB Data Point: Becoming Credit Visible

June 2017 CFPB Data Point: Becoming Credit Visible The CFPB Office of Research p Kenneth P. Brevoort p Michelle Kambara This is another in an occasional series of publications from the Consumer Financial

June 2017 CFPB Data Point: Becoming Credit Visible The CFPB Office of Research p Kenneth P. Brevoort p Michelle Kambara This is another in an occasional series of publications from the Consumer Financial

CHART 4.1 THE SEVEN BASIC FUNCTIONS FOR EXTENDING CREDIT

CHART 4.1 THE SEVEN BASIC FUNCTIONS FOR EXTENDING CREDIT What are the seven essential functions in the extension of credit that all lenders must perform or cause to have performed? The configuration of

CHART 4.1 THE SEVEN BASIC FUNCTIONS FOR EXTENDING CREDIT What are the seven essential functions in the extension of credit that all lenders must perform or cause to have performed? The configuration of

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about FICO Scores

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

Submission to Test 2 Practice

Submission to Test 2 Practice Student: Gosselin, Richard (33969) Score: 9 4 (23%) Date: /9/25 9:2 Workstation: 72.9.66.8. The optimal mix of output may not be produced by an economy because of the existence

Submission to Test 2 Practice Student: Gosselin, Richard (33969) Score: 9 4 (23%) Date: /9/25 9:2 Workstation: 72.9.66.8. The optimal mix of output may not be produced by an economy because of the existence

Household Debt in America: A Look Across Generations Over Time

Household Debt in America: A Look Across Generations Over Time Carlos Garriga Bryan Noeth Don E. Schlagenhauf Federal Reserve Bank of St. Louis The Center for Household Financial Stability and Research

Household Debt in America: A Look Across Generations Over Time Carlos Garriga Bryan Noeth Don E. Schlagenhauf Federal Reserve Bank of St. Louis The Center for Household Financial Stability and Research

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

Credit score ratings chart 2017

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

Monetary Policy and Reaching for Income by Daniel, Garlappi and Xiao. Discussant: Annette Vissing-Jorgensen, UC Berkeley.

Monetary Policy and Reaching for Income by Daniel, Garlappi and Xiao Discussant: Annette Vissing-Jorgensen, UC Berkeley April 28, 2018 Findings: Following lower Fed funds rate (over 3 years). 1) Mutual

Monetary Policy and Reaching for Income by Daniel, Garlappi and Xiao Discussant: Annette Vissing-Jorgensen, UC Berkeley April 28, 2018 Findings: Following lower Fed funds rate (over 3 years). 1) Mutual

A Look Behind the Numbers: FHA Lending in Ohio

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

10 Errors to Avoid When Refinancing

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

Underwriting, Metrics, and Credit Scoring That Reduce Losses

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT!

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: 4 Big Reasons You Can t Afford To Ignore Business Credit Copyright 2012 All rights reserved. No part of

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: 4 Big Reasons You Can t Afford To Ignore Business Credit Copyright 2012 All rights reserved. No part of

Do Bank Branches Matter Anymore?

ECONOMIC COMMENTARY Number 211-13 August 4, 211 Do Bank Branches Matter Anymore? O. Emre Ergungor and Stephanie Moulton Bank branches have been disappearing in some major metropolitan areas, as their populations

ECONOMIC COMMENTARY Number 211-13 August 4, 211 Do Bank Branches Matter Anymore? O. Emre Ergungor and Stephanie Moulton Bank branches have been disappearing in some major metropolitan areas, as their populations

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

P2.T6. Credit Risk Measurement & Management. Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition

P2.T6. Credit Risk Measurement & Management Bionic Turtle FRM Practice Questions Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition By David Harper, CFA FRM CIPM

P2.T6. Credit Risk Measurement & Management Bionic Turtle FRM Practice Questions Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition By David Harper, CFA FRM CIPM

``Wealth and Stock Market Participation: Estimating the Causal Effect from Swedish Lotteries by Briggs, Cesarini, Lindqvist and Ostling

``Wealth and Stock Market Participation: Estimating the Causal Effect from Swedish Lotteries by Briggs, Cesarini, Lindqvist and Ostling Discussant: Annette Vissing-Jorgensen, UC Berkeley Main finding:

``Wealth and Stock Market Participation: Estimating the Causal Effect from Swedish Lotteries by Briggs, Cesarini, Lindqvist and Ostling Discussant: Annette Vissing-Jorgensen, UC Berkeley Main finding:

Policy Evaluation: Methods for Testing Household Programs & Interventions

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

The Evolution of Household Leverage During the Recovery

ECONOMIC COMMENTARY Number 2014-17 September 2, 2014 The Evolution of Household Leverage During the Recovery Stephan Whitaker Recent research has shown that geographic areas that experienced greater household

ECONOMIC COMMENTARY Number 2014-17 September 2, 2014 The Evolution of Household Leverage During the Recovery Stephan Whitaker Recent research has shown that geographic areas that experienced greater household

Credit Growth and the Financial Crisis: A New Narrative

Credit Growth and the Financial Crisis: A New Narrative Stefania Albanesi, University of Pittsburgh Giacomo De Giorgi, University of Geneva Jaromir Nosal, Boston College Fifth Conference on Household Finance

Credit Growth and the Financial Crisis: A New Narrative Stefania Albanesi, University of Pittsburgh Giacomo De Giorgi, University of Geneva Jaromir Nosal, Boston College Fifth Conference on Household Finance

Simple Notes on the ISLM Model (The Mundell-Fleming Model)

") Simple Notes on the ISLM Model (The Mundell-Fleming Model) This is a model that describes the dynamics of economies in the short run. It has million of critiques, and rightfully so. However, even though

Simple Notes on the ISLM Model (The Mundell-Fleming Model) This is a model that describes the dynamics of economies in the short run. It has million of critiques, and rightfully so. However, even though

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes)

") IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

Understanding. What you need to know about the most widely used credit scores

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

12 CREDIT LINES & CARDS YOU CAN GET FOR YOUR BUSINESS

12 CREDIT LINES & CARDS YOU CAN GET FOR YOUR BUSINESS 12 Credit Lines and Cards You Can Get for Your Business A credit line, or line of credit (LOC), is an agreement between a financial institution or

12 CREDIT LINES & CARDS YOU CAN GET FOR YOUR BUSINESS 12 Credit Lines and Cards You Can Get for Your Business A credit line, or line of credit (LOC), is an agreement between a financial institution or

Financial markets in developing countries (rough notes, use only as guidance; more details provided in lecture) The role of the financial system

The role of the financial system") Financial markets in developing countries (rough notes, use only as guidance; more details provided in lecture) The role of the financial system matching savers and investors (otherwise each person needs

Financial markets in developing countries (rough notes, use only as guidance; more details provided in lecture) The role of the financial system matching savers and investors (otherwise each person needs

A Model of the Reserve Asset

A Model of the Reserve Asset Zhiguo He (Chicago Booth and NBER) Arvind Krishnamurthy (Stanford GSB and NBER) Konstantin Milbradt (Northwestern Kellogg and NBER) July 2015 ECB 1 / 40 Motivation US Treasury

A Model of the Reserve Asset Zhiguo He (Chicago Booth and NBER) Arvind Krishnamurthy (Stanford GSB and NBER) Konstantin Milbradt (Northwestern Kellogg and NBER) July 2015 ECB 1 / 40 Motivation US Treasury

Short-term debt and financial crises: What we can learn from U.S. Treasury supply

Short-term debt and financial crises: What we can learn from U.S. Treasury supply Arvind Krishnamurthy Northwestern-Kellogg and NBER Annette Vissing-Jorgensen Berkeley-Haas, NBER and CEPR 1. Motivation

Short-term debt and financial crises: What we can learn from U.S. Treasury supply Arvind Krishnamurthy Northwestern-Kellogg and NBER Annette Vissing-Jorgensen Berkeley-Haas, NBER and CEPR 1. Motivation

JOB SITUATION INCOME. 3 rd Quarter 2015 PITTSBURGH

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

Fannie Mae National Housing Survey

Fannie Mae National Housing Survey What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from recent Fannie Mae acquisitions Topic Analysis 4/13/2015 Fannie Mae 2015 Table of Contents

Fannie Mae National Housing Survey What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from recent Fannie Mae acquisitions Topic Analysis 4/13/2015 Fannie Mae 2015 Table of Contents

Turning the tide. Managing troubled portfolios

Managing troubled portfolios Executive summary The economy may be recovering and the credit picture improving, but lending institutions still find themselves coping with some troubled portfolios. Plus,

Managing troubled portfolios Executive summary The economy may be recovering and the credit picture improving, but lending institutions still find themselves coping with some troubled portfolios. Plus,

Why is the Country Facing a Financial Crisis?

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Consumer Credit: Learning Your Customer's Default Risk from What (S)he Buys

he Buys") Consumer Credit: Learning Your Customer's Default Risk from What (S)he Buys Annette Vissing-Jorgensen Haas School of Business, University of California Berkeley, NBER and CEPR April 26, 2016 Abstract Using

Consumer Credit: Learning Your Customer's Default Risk from What (S)he Buys Annette Vissing-Jorgensen Haas School of Business, University of California Berkeley, NBER and CEPR April 26, 2016 Abstract Using

Ch In other countries the replacement rate is often higher. In the Netherlands it is over 90%. This means that after taxes Dutch workers receive

Ch. 13 1 About Social Security o Social Security is formally called the Federal Old-Age, Survivors, Disability Insurance Trust Fund (OASDI). o It was created as part of the New Deal and was designed in

Ch. 13 1 About Social Security o Social Security is formally called the Federal Old-Age, Survivors, Disability Insurance Trust Fund (OASDI). o It was created as part of the New Deal and was designed in

AND INVESTMENT * Chapt er. Key Concepts

Chapt er 7 FINANCE, SAVING, AND INVESTMENT * Key Concepts Financial Institutions and Financial Markets Finance and money are different: Finance refers to raising the funds used for investment in physical

Chapt er 7 FINANCE, SAVING, AND INVESTMENT * Key Concepts Financial Institutions and Financial Markets Finance and money are different: Finance refers to raising the funds used for investment in physical

Household Debt and Defaults from 2000 to 2010: The Credit Supply View Online Appendix

Household Debt and Defaults from 2000 to 2010: The Credit Supply View Online Appendix Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business and NBER May 2, 2016

Household Debt and Defaults from 2000 to 2010: The Credit Supply View Online Appendix Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business and NBER May 2, 2016

Taking Control of Your Money. Using Credit Wisely

Taking Control of Your Money Using Credit Wisely Session 4: Using Credit Wisely To help you stay financially healthy you need to understand credit. Credit is access to money that belongs to lenders (e.g.

Taking Control of Your Money Using Credit Wisely Session 4: Using Credit Wisely To help you stay financially healthy you need to understand credit. Credit is access to money that belongs to lenders (e.g.

Top Things To Know KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT ECONOMICS - PERSONAL FINANCE WORKSHOPS # 4 - CONTROLLING DEBT

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT ECONOMICS - PERSONAL FINANCE WORKSHOPS # 4 - CONTROLLING DEBT Vocabulary Keys : Words that are in bold = are terms that appear in one of the chapters, Words

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT ECONOMICS - PERSONAL FINANCE WORKSHOPS # 4 - CONTROLLING DEBT Vocabulary Keys : Words that are in bold = are terms that appear in one of the chapters, Words

Purchase Price Allocation, Goodwill and Other Intangibles Creation & Asset Write-ups

Purchase Price Allocation, Goodwill and Other Intangibles Creation & Asset Write-ups In this lesson we're going to move into the next stage of our merger model, which is looking at the purchase price allocation

Purchase Price Allocation, Goodwill and Other Intangibles Creation & Asset Write-ups In this lesson we're going to move into the next stage of our merger model, which is looking at the purchase price allocation

Data Point: The Geography of Credit Invisibility

September 2018 Data Point: The Geography of Credit Invisibility The Bureau of Consumer Financial Protection s Offce of Research This is another in an occasional series of publications from the Bureau of

September 2018 Data Point: The Geography of Credit Invisibility The Bureau of Consumer Financial Protection s Offce of Research This is another in an occasional series of publications from the Bureau of

Things you should know about inflation

Things you should know about inflation February 23, 2015 Inflation is a general increase in prices. Equivalently, it is a fall in the purchasing power of money. The opposite of inflation is deflation a

Things you should know about inflation February 23, 2015 Inflation is a general increase in prices. Equivalently, it is a fall in the purchasing power of money. The opposite of inflation is deflation a

Discussion of A Pigovian Approach to Liquidity Regulation

Discussion of A Pigovian Approach to Liquidity Regulation Ernst-Ludwig von Thadden University of Mannheim The regulation of bank liquidity has been one of the most controversial topics in the recent debate

Discussion of A Pigovian Approach to Liquidity Regulation Ernst-Ludwig von Thadden University of Mannheim The regulation of bank liquidity has been one of the most controversial topics in the recent debate

WJEC (Wales) Economics A-level

Economics A-level") WJEC (Wales) Economics A-level Macroeconomics Topic 2: Macroeconomic Objectives 2.3 Inflation and deflation Notes Inflation is the sustained rise in the general price level over time. This means that the

WJEC (Wales) Economics A-level Macroeconomics Topic 2: Macroeconomic Objectives 2.3 Inflation and deflation Notes Inflation is the sustained rise in the general price level over time. This means that the

Understanding Debt Problems & Solutions

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Understanding Credit. Lisa Mitchell, Sallie Mae April 6, Champions of Financial Aid ILASFAA Conference

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Financial Regulation and the Economic Security of Low-Income Households

Financial Regulation and the Economic Security of Low-Income Households Karen Dynan Brookings Institution October 14, 2010 Note. This presentation was prepared for the Institute for Research on Poverty

Financial Regulation and the Economic Security of Low-Income Households Karen Dynan Brookings Institution October 14, 2010 Note. This presentation was prepared for the Institute for Research on Poverty

To lower auto insurance rate premium we should put a stake on each steering wheel

Risk and the market for insurance Armen Alchian: To lower auto insurance rate premium we should put a stake on each steering wheel 1 Outline Risk and Risk attitudes Kinds of risk Mitigating ii i risk ik

Risk and the market for insurance Armen Alchian: To lower auto insurance rate premium we should put a stake on each steering wheel 1 Outline Risk and Risk attitudes Kinds of risk Mitigating ii i risk ik

Fannie Mae National Housing Survey. July - September 2010 Quarterly Wave

Fannie Mae National Housing Survey July - ember 2010 Quarterly Wave Copyright 2010 by Fannie Mae Release Date: November 23, 2010 Consumer attitudes: measure current and track change Attitudinal Questions

Fannie Mae National Housing Survey July - ember 2010 Quarterly Wave Copyright 2010 by Fannie Mae Release Date: November 23, 2010 Consumer attitudes: measure current and track change Attitudinal Questions

Valuation Models are based on earnings growth forecasts. Need to understand: what earnings are, their importance, & how to forecast.

1 E&G, Ch. 19: Earnings Estimation Valuation Models are based on earnings growth forecasts. Need to understand: what earnings are, their importance, & how to forecast. I. What are Earnings? A. Economist

1 E&G, Ch. 19: Earnings Estimation Valuation Models are based on earnings growth forecasts. Need to understand: what earnings are, their importance, & how to forecast. I. What are Earnings? A. Economist

An Empirical Study on Default Factors for US Sub-prime Residential Loans

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

The Lehman Shock Financial Disaster the Effects on Japan. found out an attractive and interesting article, which showed the world economic

1 The Lehman Shock Financial Disaster the Effects on Japan Introduction In the third cycle, I researched about Greece s financial crisis. In the research process, I found out an attractive and interesting

1 The Lehman Shock Financial Disaster the Effects on Japan Introduction In the third cycle, I researched about Greece s financial crisis. In the research process, I found out an attractive and interesting

How Much House Can You Afford?

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

How Do You Calculate Cash Flow in Real Life for a Real Company?

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

Do Student Loan Borrowers Opportunistically Default? Evidence from Bankruptcy Reform

Do Student Loan Borrowers Opportunistically Default? Evidence from Bankruptcy Reform Rajeev Darolia, University of Missouri Dubravka Ritter, Federal Reserve Bank of Philadelphia 2015 Policy Summit on Housing,

Do Student Loan Borrowers Opportunistically Default? Evidence from Bankruptcy Reform Rajeev Darolia, University of Missouri Dubravka Ritter, Federal Reserve Bank of Philadelphia 2015 Policy Summit on Housing,

Topic 11: Disability Insurance

Topic 11: Disability Insurance Nathaniel Hendren Harvard Spring, 2018 Nathaniel Hendren (Harvard) Disability Insurance Spring, 2018 1 / 63 Disability Insurance Disability insurance in the US is one of

Topic 11: Disability Insurance Nathaniel Hendren Harvard Spring, 2018 Nathaniel Hendren (Harvard) Disability Insurance Spring, 2018 1 / 63 Disability Insurance Disability insurance in the US is one of

Secured and Unsecured (1)

") LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

Summary. The importance of accessing formal credit markets

Policy Brief: The Effect of the Community Reinvestment Act on Consumers Contact with Formal Credit Markets by Ana Patricia Muñoz and Kristin F. Butcher* 1 3, 2013 November 2013 Summary Data on consumer

Policy Brief: The Effect of the Community Reinvestment Act on Consumers Contact with Formal Credit Markets by Ana Patricia Muñoz and Kristin F. Butcher* 1 3, 2013 November 2013 Summary Data on consumer

A Credit Smart Start. Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

SEVEN LIFE-DEFINING FINANCIAL DECISIONS

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

TEN PRICE CAP RESEARCH Summary Report

TEN-16-075. PRICE CAP RESEARCH Summary Report Prepared for: Financial Conduct Authority 25 The North Colonnade Canary wharf London E14 16 June 2017 Table of Contents 1. Introduction... 2 1.1 Background...

TEN-16-075. PRICE CAP RESEARCH Summary Report Prepared for: Financial Conduct Authority 25 The North Colonnade Canary wharf London E14 16 June 2017 Table of Contents 1. Introduction... 2 1.1 Background...

RURAL LOAN RECOVERY CONCEPTS AND MEASURES. Richard L. Meyer. Paper Prepared for the Seminar on Issues in Rural Loan Recovery in Bangladesh

ECONOMICS AND SOCIOLOGY OCCASIONAL PAPER NO. 1321 RURAL LOAN RECOVERY CONCEPTS AND MEASURES by Richard L. Meyer Paper Prepared for the Seminar on Issues in Rural Loan Recovery in Bangladesh Sponsored by

ECONOMICS AND SOCIOLOGY OCCASIONAL PAPER NO. 1321 RURAL LOAN RECOVERY CONCEPTS AND MEASURES by Richard L. Meyer Paper Prepared for the Seminar on Issues in Rural Loan Recovery in Bangladesh Sponsored by

Maturity, Indebtedness and Default Risk 1

Maturity, Indebtedness and Default Risk 1 Satyajit Chatterjee Burcu Eyigungor Federal Reserve Bank of Philadelphia February 15, 2008 1 Corresponding Author: Satyajit Chatterjee, Research Dept., 10 Independence

Maturity, Indebtedness and Default Risk 1 Satyajit Chatterjee Burcu Eyigungor Federal Reserve Bank of Philadelphia February 15, 2008 1 Corresponding Author: Satyajit Chatterjee, Research Dept., 10 Independence

How much use of home equity? LOTS. Econ 113: April 21, Boom in borrowing. There are real effects of financial changes 4/19/2015 6:09 PM

Econ 113: April 21, 2015 How much use of home equity? LOTS Subprime Lending Crisis, 2000s, continued Housing Boom & Bust HELOCs and consumer spending (Mian & Sufi) Demographic Changes Women in the Labor

Econ 113: April 21, 2015 How much use of home equity? LOTS Subprime Lending Crisis, 2000s, continued Housing Boom & Bust HELOCs and consumer spending (Mian & Sufi) Demographic Changes Women in the Labor

Market for Lemons. Market Failure Asymmetric Information. Problem Setup

Market for Lemons Market Failure Asymmetric Information Nice simple mathematical example of how asymmetric information (AI) can force markets to unravel Attributed to George Akeloff, Nobel Prize a few

Market for Lemons Market Failure Asymmetric Information Nice simple mathematical example of how asymmetric information (AI) can force markets to unravel Attributed to George Akeloff, Nobel Prize a few

Econ 1101 Spring Radek Paluszynski 5/8/2013

Econ 1101 Spring 2013 Radek Paluszynski 5/8/2013 Announcements Final exam: Tuesday, May 14 th, 6.30-8.30pm If you have exam conflict, there is a makeup final on Thursday, May 16 th, 10am-12pm Registration

Econ 1101 Spring 2013 Radek Paluszynski 5/8/2013 Announcements Final exam: Tuesday, May 14 th, 6.30-8.30pm If you have exam conflict, there is a makeup final on Thursday, May 16 th, 10am-12pm Registration

SEGMENTATION FOR CREDIT-BASED DELINQUENCY MODELS. May 2006

SEGMENTATION FOR CREDIT-BASED DELINQUENCY MODELS May 006 Overview The objective of segmentation is to define a set of sub-populations that, when modeled individually and then combined, rank risk more effectively

SEGMENTATION FOR CREDIT-BASED DELINQUENCY MODELS May 006 Overview The objective of segmentation is to define a set of sub-populations that, when modeled individually and then combined, rank risk more effectively

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Pindyck and Rubinfeld, Chapter 17 Sections 17.1 and 17.2 Asymmetric information can cause a competitive equilibrium allocation to be inefficient.

Pindyck and Rubinfeld, Chapter 17 Sections 17.1 and 17.2 Asymmetric information can cause a competitive equilibrium allocation to be inefficient. A market has asymmetric information when some agents know

Pindyck and Rubinfeld, Chapter 17 Sections 17.1 and 17.2 Asymmetric information can cause a competitive equilibrium allocation to be inefficient. A market has asymmetric information when some agents know

Credit Market Consequences of Credit Flag Removals *

Credit Market Consequences of Credit Flag Removals * Will Dobbie Benjamin J. Keys Neale Mahoney July 7, 2017 Abstract This paper estimates the impact of a credit report with derogatory marks on financial

Credit Market Consequences of Credit Flag Removals * Will Dobbie Benjamin J. Keys Neale Mahoney July 7, 2017 Abstract This paper estimates the impact of a credit report with derogatory marks on financial

Gen. Pop Hispanics African Americans Base: All Respondents (n=1,005) (n=105) (n=105) Rent 27% 38% 49% Own 68% 59% 43% Other 6% 3% 9%

(n=105) (n=105) Rent 27% 38% 49% Own 68% 59% 43% Other 6% 3% 9%") 2016 How America Views Homeownership - Study for Public Release Topline Results May 2016 Arrows ( / ) indicate significant differences across demographic groups Current Living/Home Purchasing Situation

2016 How America Views Homeownership - Study for Public Release Topline Results May 2016 Arrows ( / ) indicate significant differences across demographic groups Current Living/Home Purchasing Situation

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

The Mortgage Guide. Helping you find the right mortgage for you. Brought to you by. V a

The Mortgage Guide Helping you find the right mortgage for you Brought to you by V0050713a Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us

The Mortgage Guide Helping you find the right mortgage for you Brought to you by V0050713a Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us

Credit Market Consequences of Credit Flag Removals *

Credit Market Consequences of Credit Flag Removals * Will Dobbie Benjamin J. Keys Neale Mahoney June 5, 2017 Abstract This paper estimates the impact of a bad credit report on financial outcomes by exploiting

Credit Market Consequences of Credit Flag Removals * Will Dobbie Benjamin J. Keys Neale Mahoney June 5, 2017 Abstract This paper estimates the impact of a bad credit report on financial outcomes by exploiting

Optimize RRSP Contribution Strategy Summary

Optimize RRSP Contribution Strategy Summary Prepared by Trusted Advisor, ABC Financial Inc. Assumptions $8,000 to invest now, and $2,000 per year of long-term investable cashflow $86,000 taxable income,

Optimize RRSP Contribution Strategy Summary Prepared by Trusted Advisor, ABC Financial Inc. Assumptions $8,000 to invest now, and $2,000 per year of long-term investable cashflow $86,000 taxable income,

UNDERSTANDING CREDIT. WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2012 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2012 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

Boost Your Credit Score By Yourself! How to get the house or car you want

Boost Your Credit Score By Yourself! How to get the house or car you want TIP 1. STEP-BY-STEP GAME PLAN This is what you have to know to fix your credit in a hurry: You must know your three credit scores

Boost Your Credit Score By Yourself! How to get the house or car you want TIP 1. STEP-BY-STEP GAME PLAN This is what you have to know to fix your credit in a hurry: You must know your three credit scores

Chapter 18: The Correlational Procedures

Introduction: In this chapter we are going to tackle about two kinds of relationship, positive relationship and negative relationship. Positive Relationship Let's say we have two values, votes and campaign

Introduction: In this chapter we are going to tackle about two kinds of relationship, positive relationship and negative relationship. Positive Relationship Let's say we have two values, votes and campaign

The Mortgage Guide Helping you find the right mortgage for you

The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make. And it can be stressful.

The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make. And it can be stressful.

A Real Estate Agent s Guide to Successful Short Sales

A Real Estate Agent s Guide to Successful Short Sales INTRODUCTION Many homebuyers have heard that short sales offer excellent opportunities for investment, but few of them understand what s behind buying

A Real Estate Agent s Guide to Successful Short Sales INTRODUCTION Many homebuyers have heard that short sales offer excellent opportunities for investment, but few of them understand what s behind buying

12 Steps to Improved Credit Steven K. Shapiro

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

GUIDELINES FOR THE AVERAGE MORTGAGE

GUIDELINES FOR THE AVERAGE MORTGAGE A mortgage lender reviews a loan applicant s financial history to determine the likelihood of receiving on-time payments. The primary items reviewed are: * Income *

GUIDELINES FOR THE AVERAGE MORTGAGE A mortgage lender reviews a loan applicant s financial history to determine the likelihood of receiving on-time payments. The primary items reviewed are: * Income *

Improving Your Credit Score

Improving Your Credit Score From my experience working with many potential home buyers looking to improve their credit, they are frustrated! They are frustrated because they receive conflicting information

Improving Your Credit Score From my experience working with many potential home buyers looking to improve their credit, they are frustrated! They are frustrated because they receive conflicting information

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Winter 2017 Poverty. - 27% identified as Liberal or Very Liberal; 43% identified as Moderate; 29% identified Conservative or Very Conservative.

Winter 2017 Poverty This year, is partnering with the Baldwin Wallace University Community Research Institute ( CRI ) to augment the quarterly Listening Project surveys. The CRI will field four surveys

Winter 2017 Poverty This year, is partnering with the Baldwin Wallace University Community Research Institute ( CRI ) to augment the quarterly Listening Project surveys. The CRI will field four surveys

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

THE 2018 ECONOMY: A BIT BETTER THAN IN 2017

THE 2018 ECONOMY: A BIT BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC November 9, 2017 Detroit, MI The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market

THE 2018 ECONOMY: A BIT BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC November 9, 2017 Detroit, MI The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market

The Unique Credit Characteristics of Healthcare Patients. An Equifax Predictive Sciences Research Paper December 2003

The Unique Credit Characteristics of Healthcare Patients An Equifax Predictive Sciences Research Paper December 2003 Executive Summary As today s healthcare payment trends shift toward an ever increasing

The Unique Credit Characteristics of Healthcare Patients An Equifax Predictive Sciences Research Paper December 2003 Executive Summary As today s healthcare payment trends shift toward an ever increasing

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU?

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Commentary on 'Exchange Rate Volatility and Misalignment: Evaluating Some Proposals for Reform'

Commentary on 'Exchange Rate Volatility and Misalignment: Evaluating Some Proposals for Reform' Robert D. Hormats I will first address the character of the individual currency markets and then describe

Commentary on 'Exchange Rate Volatility and Misalignment: Evaluating Some Proposals for Reform' Robert D. Hormats I will first address the character of the individual currency markets and then describe

Residential Mortgage Default and Consumer Bankruptcy: Theory and Empirical Evidence*

Residential Mortgage Default and Consumer Bankruptcy: Theory and Empirical Evidence* Wenli Li, Philadelphia Federal Reserve and Michelle J. White, UC San Diego and NBER February 2011 *Preliminary draft,

Residential Mortgage Default and Consumer Bankruptcy: Theory and Empirical Evidence* Wenli Li, Philadelphia Federal Reserve and Michelle J. White, UC San Diego and NBER February 2011 *Preliminary draft,

Teaching the Realities of Small Business Financing

Pace University DigitalCommons@Pace Faculty Working Papers Lubin School of Business 12-1-2002 Teaching the Realities of Small Business Financing Peter M. Edelstein Pace University Follow this and additional

Pace University DigitalCommons@Pace Faculty Working Papers Lubin School of Business 12-1-2002 Teaching the Realities of Small Business Financing Peter M. Edelstein Pace University Follow this and additional