Complex Mortgages. May 2014

|

|

|

- Milton Simpson

- 5 years ago

- Views:

Transcription

1 Complex Mortgages Gene Amromin, Federal Reserve Bank of Chicago Jennifer Huang, Cheung Kong Graduate School of Business Clemens Sialm, University of Texas-Austin and NBER Edward Zhong, University of Wisconsin May 2014 The views expressed are those of the authors and are not necessarily those of the Federal Reserve Bank of Chicago or the Federal Reserve System

2 Complex mortgages and the housing crisis The availability of these alternative mortgage products [interestonly ARMs, negative amortization ARMs, pay-option ARMs] proved to be quite important and, as many have recognized, is likely a key explanation of the housing bubble. Ben S. Bernanke AEA Meetings, January 3rd, 2010

3 Motivation Over the last decade the residential mortgage market has experienced a significant increase in product complexity (followed by reversion to vanilla products) Much of the product innovation focused on products with deferred amortization schedules Complex b/c they add an extra element of uncertainty; lower monthly servicing costs at the expense of higher leverage Mortgage securitization and the extension of credit to subprime borrowers have received a lot of attention; the contract design of mortgages remains largely unexplored

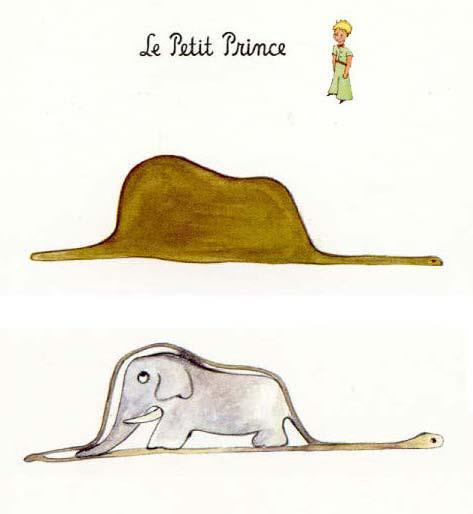

4 Cumulative Proportion Composition of mortgages over time 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% FRM ARM CM 0% A welfare-improving innovation (e.g. hat)? or something that may be difficult to digest later on?

5

6 Rationales for complex mortgages CMs as non-transparent contracts obfuscate the true borrowing costs and fool unsophisticated borrowers into suboptimal contracts Carlin (2009); Carlin and Manso (2009) CMs as optimal contracts for borrowers and lenders that expect higher growth rate or higher volatility in house prices and incomes for borrowers who maximize the value of their default option Barlevy and Fisher (2010), Piskorski and Tchistyi (2010), Corbae and Quintin (2010), Cocco (2013), Garmaise (2013)

7 Who took out such contracts? Households with high (stated) incomes and prime credit scores To purchase more expensive homes relative to income Where? Which theory is consistent with this? Areas with higher proportion of young households, higher house price appreciation, and higher population growth In non-recourse states, investment properties, incomplete docs What followed? Main questions Higher default rates: payment resets and greater leverage Unobservable borrower characteristics appear to play a role too CM borrowers more sensitive to the value of the default option Less sensitive to income and credit scores More likely to stop payments abruptly

8 What are these mortgages? Fixed-rate mortgages (FRM): fixed interest rate, principal amortized over a pre-specified term (usually 30 years) Adjustable-rate mortgages (ARM): interest rate resets at prespecified frequency; also amortize principal Complex mortgages (CM) are (mostly) ARMs: the principal does not amortize over a pre-specified horizon or is allowed to increase Interest only (IO): fixed interest over n years, then ARM that amortizes over 30-n OptionARM (NegAm): Required minimum payment < IO payment Minimum payment can only increase by 7.5% a year unless a loan reverts to an amortizing ARM if one of two conditions is met: after n months elapse (n is usually 60) LTV ratio breaches the pre-specified limit (110 to 125 )

9 An illustration of CM CM payments are much more likely to jump because of amortization kick-in CM lead to greater leverage ratios for any path of housing prices $100,000 balance, 30-year amortization; FRM rate fixed at 5%, initial ARM rate at 4.5%, spread to T-bill is 150bp, floor of 2% and cap of 7%. Simulated Treasury rate follows an AR(1) estimated for Option ARM pays 50% of the interest payment over the first 5 years, becomes an ARM with a 25-year amortization schedule thereafter

10 Data Representative sample of U.S. mortgage loans originated between 2003 and 2007 from LPS Analytics Income data from HMDA Quarterly MSA-level HPI data from the Federal Housing Finance Agency (FHFA) Quarterly county level unemployment rate data from the BLS Annual county-level population data from the BEA Local demographic characteristics from the 2000 U.S. Census

11 Summary statistics by mortgage type

12 Mortgage choice c multinomial logit model: CM v. FRM v. ARM Not poor & naïve Help with affordability More optimistic Self-selected (less averse to strategic defaults?)

13 Mortgage choice: robustness These results are robust to limiting the sample to loans with full documentation, portfolio loans Investment properties, subprime borrowers Purchase transactions, non-california loans Stronger for contracts that are more complex, i.e. for NegAm loans as compared to IOs

14 Hazard Rate Contract choice and delinquency: hazard rate CM ARM FRM Months After Origination Share becoming 60+dpd in month t conditional on being performing in t-1 From about 15 months on, CM hazard rates are uniformly the highest Funny peaks following 2 and 3 year anniversaries

15 Contract choice and delinquency: regressions Cox proportional hazard model of first time default (60+dpd), allow baseline hazard to vary by state and year of origination Why might we expect CMs to default more? additional payment shocks higher LTV possible self-selection: attract households that may be more risk-seeking, subject to greater background risk, more willing to default Include time-varying loan and macro characteristics Change in required payments, change in house value and loan amount, MSA-level unemployment and income growth McHMDA originations, performance observed through 2009

16 Hazard regression results VARIABLES MSA-Level Covariates CM 0.698** (0.012) IO 0.659** (0.013) NEGAM 0.938** (0.020) Payment resets 0.031** 0.025** (0.002) (0.002) House Price Growth ** ** (0.020) (0.020) Loan Balance Growth (0.012) (0.012) Income growth ** ** (0.024) (0.024) Unemployment (0.013) (0.012) ARM 0.456** 0.460** (0.010) (0.010) Log (income) ** ** (0.010) (0.010) FICO ** ** (0.012) (0.012) Payment resets are associated with higher delinquency hazard rates as are decreases in house prices or incomes Yet, CMs have higher delinquency rates with all of these controls in place The impact of having a CM on delinquency status is similar to that of a 1 std decrease in FICO score About twice as high as for a similar FRM borrower (e =2)

17 What could explain higher CM delinquencies? CM 0.697** (0.013) CM x LTV 0.108** (0.020) CM x Log(income) 0.083** (0.009) CM x FICO 0.078** (0.012) ARM 0.452** (0.010) Log (income) ** (0.010) FICO ** (0.010) LTV 0.472** (0.010) State-year baselines Yes Other controls Yes N 23,151,288 Suggestive evidence that CM borrowers differ in their risk taking and willingness to default. How can we test this? Interact CM with measures of gains from default and sophistication Defaults by CM borrowers are more sensitive to gain from default The default gap between CM and FRM borrowers is largest for the more affluent and more creditworthy households i.e. more sophisticated CM borrowers are the ones to default more

18 Payment patterns following initial delinquency No additional payments given delinquency CM 0.629** (0.019) ARM 0.435** (0.013) Log (income) 0.197** (0.017) FICO 0.375** (0.006) LTV 0.281** (0.011) VTI 0.120** (0.018) Low doc 0.054** (0.013) Jumbo (0.036) Condo 0.287** (0.042) Investor 0.511** (0.030) Refinance (0.013) Initial delinquency less likely to be strategic for households who try to get back on track CM borrowers are more likely to not make any additional payments after first becoming 60+ days past due Observations 1,525,404

19 Summary and conclusions Complex mortgages are chosen by creditworthy households seeking to purchase more expensive homes relative to their incomes There is little evidence consistent with the notion that CM borrowers are naïve households bamboozled by unscrupulous lenders CM borrowers experience substantially higher ex post default rates after controlling for a number of borrower, loan, and macro factors These rates cannot be explained by payment resets or higher LTVs associated with non-amortizing loans Highest sensitivity to gains from default, higher default gap for more sophisticated CM borrowers, and higher propensity to default abruptly are consistent with CMs attracting borrowers who are more strategic in the default decisions

20 Geographic distribution of CM: 2002

21 Geographic distribution of CM: 2005

22 Geographic distribution of CM: 2008

Complex Mortgages. Gene Amromin Federal Reserve Bank of Chicago. Jennifer Huang University of Texas at Austin and Cheung Kong GSB

Gene Amromin Federal Reserve Bank of Chicago Jennifer Huang University of Texas at Austin and Cheung Kong GSB Clemens Sialm University of Texas at Austin and NBER Edward Zhong University of Wisconsin-Madison

Gene Amromin Federal Reserve Bank of Chicago Jennifer Huang University of Texas at Austin and Cheung Kong GSB Clemens Sialm University of Texas at Austin and NBER Edward Zhong University of Wisconsin-Madison

Loan Product Steering in Mortgage Markets

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Backloaded Mortgages and House Price Appreciation

1 / 33 Backloaded Mortgages and House Price Appreciation Gadi Barlevy Jonas D. M. Fisher Chicago Fed Wisconsin-Fed HULM Conference April 9-10, 2010 2 / 33 Introduction: Motivation Widespread house price

1 / 33 Backloaded Mortgages and House Price Appreciation Gadi Barlevy Jonas D. M. Fisher Chicago Fed Wisconsin-Fed HULM Conference April 9-10, 2010 2 / 33 Introduction: Motivation Widespread house price

Mortgage Rates, Household Balance Sheets, and Real Economy

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Loan Level Mortgage Modeling

Loan Level Mortgage Modeling Modeling and Data Challenges Shirish Chinchalkar October 2015 Agenda 1. The complexity of loan level modeling 2. Our approach for modeling mortgages 3. Data Challenges 4. Conclusion

Loan Level Mortgage Modeling Modeling and Data Challenges Shirish Chinchalkar October 2015 Agenda 1. The complexity of loan level modeling 2. Our approach for modeling mortgages 3. Data Challenges 4. Conclusion

Mortgage Modeling: Topics in Robustness. Robert Reeves September 2012 Bank of America

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market Lan Shi lshi@urban.org Yan (Jenny) Zhang Yan.Zhang@occ.treas.gov Presentation Sept.

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market Lan Shi lshi@urban.org Yan (Jenny) Zhang Yan.Zhang@occ.treas.gov Presentation Sept.

An Empirical Model of Subprime Mortgage Default from 2000 to 2007

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

1. Modification algorithm

Internet Appendix for: "The Effect of Mortgage Securitization on Foreclosure and Modification" 1. Modification algorithm The LPS data set lacks an explicit modification flag but contains enough detailed

Internet Appendix for: "The Effect of Mortgage Securitization on Foreclosure and Modification" 1. Modification algorithm The LPS data set lacks an explicit modification flag but contains enough detailed

New Developments in Housing Policy

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging. Online Appendix

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging Marco Di Maggio, Amir Kermani, Benjamin J. Keys, Tomasz Piskorski, Rodney Ramcharan, Amit Seru, Vincent Yao

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging Marco Di Maggio, Amir Kermani, Benjamin J. Keys, Tomasz Piskorski, Rodney Ramcharan, Amit Seru, Vincent Yao

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments. Morgan J. Rose. March 2011

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

The subprime lending boom increased the ability of many Americans to get

ANDREW HAUGHWOUT Federal Reserve Bank of New York CHRISTOPHER MAYER Columbia Business School National Bureau of Economic Research Federal Reserve Bank of New York JOSEPH TRACY Federal Reserve Bank of New

ANDREW HAUGHWOUT Federal Reserve Bank of New York CHRISTOPHER MAYER Columbia Business School National Bureau of Economic Research Federal Reserve Bank of New York JOSEPH TRACY Federal Reserve Bank of New

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom?

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Credit-Induced Boom and Bust

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal, (X2)

to estimate the optimal, (X2)") Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks

Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks Greg Buchak, University of Chicago Gregor Matvos, Chicago Booth and NBER Tomek Piskorski, Columbia GSB and NBER Amit Seru, Stanford University

Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks Greg Buchak, University of Chicago Gregor Matvos, Chicago Booth and NBER Tomek Piskorski, Columbia GSB and NBER Amit Seru, Stanford University

The Untold Costs of Subprime Lending: Communities of Color in California. Carolina Reid. Federal Reserve Bank of San Francisco.

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

Announcement March 5, Updates and Clarifications for Streamlined Refinance Products

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

An Empirical Study on Default Factors for US Sub-prime Residential Loans

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations Augustin Landier Toulouse School of Economics David Sraer Princeton

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations Augustin Landier Toulouse School of Economics David Sraer Princeton

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

The new Prudential treatment for residential real estate

The new Prudential treatment for residential real estate 04/09/2009 Pag. 1 di 7 The new Prudential treatment for residential real estate This paper describes the CRIF position about a specific question

The new Prudential treatment for residential real estate 04/09/2009 Pag. 1 di 7 The new Prudential treatment for residential real estate This paper describes the CRIF position about a specific question

Issue No. 80 July 2009

Issue No. 80 July 2009 Welcome to the Pipeline! AD&Co s monthly newsletter focused on recent trends, changes and advances in the mortgage investor s market. CREDIT COMMENTARY New Severity Projections in

Issue No. 80 July 2009 Welcome to the Pipeline! AD&Co s monthly newsletter focused on recent trends, changes and advances in the mortgage investor s market. CREDIT COMMENTARY New Severity Projections in

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market. Online Appendix

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST. Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth)

Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth)") 1 DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth) 2 Motivation Lasting impact of the 2008 mortgage crisis on

1 DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth) 2 Motivation Lasting impact of the 2008 mortgage crisis on

AGENCY CONFORMING & HIGH BALANCE (Fannie Mae DU) BORROWER PAID

BORROWER PAID") AGENCY CONFORMING & HIGH BALANCE (Fannie Mae DU) BORROWER PAID 30 & 25 Year Fixed Agency DU (DU30, DU25) 20 Year Fixed Agency DU (DU20) 15 & 10 Year Fixed Agency DU (DU15, DU10) 4.750 107.140 107.029 106.957

AGENCY CONFORMING & HIGH BALANCE (Fannie Mae DU) BORROWER PAID 30 & 25 Year Fixed Agency DU (DU30, DU25) 20 Year Fixed Agency DU (DU20) 15 & 10 Year Fixed Agency DU (DU15, DU10) 4.750 107.140 107.029 106.957

Homeownership and Nontraditional and Subprime Mortgages

Housing Policy Debate ISSN: 1051-1482 (Print) 2152-050X (Online) Journal homepage: http://www.tandfonline.com/loi/rhpd20 Homeownership and Nontraditional and Subprime Mortgages Arthur Acolin, Xudong An,

Housing Policy Debate ISSN: 1051-1482 (Print) 2152-050X (Online) Journal homepage: http://www.tandfonline.com/loi/rhpd20 Homeownership and Nontraditional and Subprime Mortgages Arthur Acolin, Xudong An,

Risky Borrowers or Risky Mortgages?

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

A Look Behind the Numbers: FHA Lending in Ohio

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

Structuring Mortgages for Macroeconomic Stability

Structuring Mortgages for Macroeconomic Stability John Y. Campbell, Nuno Clara, and Joao Cocco Harvard University and London Business School CEAR-RSI Household Finance Workshop Montréal November 16, 2018

Structuring Mortgages for Macroeconomic Stability John Y. Campbell, Nuno Clara, and Joao Cocco Harvard University and London Business School CEAR-RSI Household Finance Workshop Montréal November 16, 2018

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices?

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

THE WEALTH BUILDING HOME LOAN. AEI s Housing Center

THE WEALTH BUILDING HOME LOAN Presented by Stephen Oliner and Edward Pinto stephen.oliner@aei.org, pintoedward1@gmail.com American Enterprise Institute Center on Housing Markets and Finance http://www.aei.org/housing/

THE WEALTH BUILDING HOME LOAN Presented by Stephen Oliner and Edward Pinto stephen.oliner@aei.org, pintoedward1@gmail.com American Enterprise Institute Center on Housing Markets and Finance http://www.aei.org/housing/

The Rise and Fall of Securitization

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class. Internet Appendix. Manuel Adelino, Duke University

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class Internet Appendix Manuel Adelino, Duke University Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth College

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class Internet Appendix Manuel Adelino, Duke University Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth College

Foreclosure Delay and Consumer Credit Performance

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

The Hidden Peril: The Role of the Condo Loan Market in the Recent Financial Crisis *

The Hidden Peril: The Role of the Condo Loan Market in the Recent Financial Crisis * Sumit Agarwal, Yongheng Deng, Chenxi Luo, and Wenlan Qian National University of Singapore October 2012 * Acknowledgements:

The Hidden Peril: The Role of the Condo Loan Market in the Recent Financial Crisis * Sumit Agarwal, Yongheng Deng, Chenxi Luo, and Wenlan Qian National University of Singapore October 2012 * Acknowledgements:

Lessons to Learn from CRA Lending

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

A Fistful of Dollars: Lobbying and the Financial Crisis

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

Quantitative Perspectives

Quantitative Perspectives LOANDYNAMICS : AD&CO S APPROACH TO MODELING CREDIT RISK by Anne Ching OCTOBER 2008 2008 andrew davidson & co., inc. QP Contents Executive Summary 01 The Data 02 Model Structure

Quantitative Perspectives LOANDYNAMICS : AD&CO S APPROACH TO MODELING CREDIT RISK by Anne Ching OCTOBER 2008 2008 andrew davidson & co., inc. QP Contents Executive Summary 01 The Data 02 Model Structure

Learning to Cope: Voluntary Financial Education and Loan Performance during a Housing Crisis

Learning to Cope: Voluntary Financial Education and Loan Performance during a Housing Crisis By SUMIT AGARWAL, GENE AMROMIN, ITZHAK BEN-DAVID, SOUPHALA CHOMSISENGPHET AND DOUGLAS D. EVANOFF 1 As we write

Learning to Cope: Voluntary Financial Education and Loan Performance during a Housing Crisis By SUMIT AGARWAL, GENE AMROMIN, ITZHAK BEN-DAVID, SOUPHALA CHOMSISENGPHET AND DOUGLAS D. EVANOFF 1 As we write

Economic Shocks: the Great Depression and Great Recession. Andy Bauer Senior Regional Economist October 19, 2017

Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist October 19, 2017 Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist

Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist October 19, 2017 Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist

Borrower Behavior, Mortgage Terminations, and The Pricing of Residential Mortgages

Borrower Behavior, Mortgage Terminations, and The Pricing of Residential Mortgages John M. Quigley University of California, Berkeley Reserve Bank of New Zealand, Wellington, September 2006 Motivation

Borrower Behavior, Mortgage Terminations, and The Pricing of Residential Mortgages John M. Quigley University of California, Berkeley Reserve Bank of New Zealand, Wellington, September 2006 Motivation

Main Points: Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 n For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 n For the quarterly period ended

Lunchtime Data Talk. Housing Finance Policy Center. Mortgage Origination Pricing and Volume: More than You Ever Wanted to Know

Housing Finance Policy Center Lunchtime Data Talk Mortgage Origination Pricing and Volume: More than You Ever Wanted to Know Frank Nothaft, Freddie Mac Mike Fratantoni, Mortgage Bankers Association October

Housing Finance Policy Center Lunchtime Data Talk Mortgage Origination Pricing and Volume: More than You Ever Wanted to Know Frank Nothaft, Freddie Mac Mike Fratantoni, Mortgage Bankers Association October

Challenges and Opportunities for Low Downpayment Lending

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Mortgage Financing in the Housing Boom and Bust

Mortgage Financing in the Housing Boom and Bust Benjamin J. Keys University of Chicago Tomasz Piskorski Columbia GSB Amit Seru University of Chicago and NBER Vikrant Vig London Business School ABSTRACT:

Mortgage Financing in the Housing Boom and Bust Benjamin J. Keys University of Chicago Tomasz Piskorski Columbia GSB Amit Seru University of Chicago and NBER Vikrant Vig London Business School ABSTRACT:

Home Affordable Refinance FAQs May 12, 2009

Home Affordable Refinance FAQs May 12, 2009 The Making Home Affordable Program includes a new initiative Home Affordable Refinance to assist homeowners in refinancing their mortgages. The primary expectation

Home Affordable Refinance FAQs May 12, 2009 The Making Home Affordable Program includes a new initiative Home Affordable Refinance to assist homeowners in refinancing their mortgages. The primary expectation

PORTFOLIO ARM BORROWER PAID RATE SHEET For Lender Paid Comp Plan see below

PORTFOLIO ARM BORROWER PAID RATE SHEET For Lender Paid Comp Plan see below 5/1 LIBOR (Portfolio 6/2/6) ARM (JP51, JP51IO) 7/1 LIBOR (Portfolio 6/2/6) ARM (JP71) 10/1 LIBOR (Portfolio 6/2/6) ARM (JP101)

PORTFOLIO ARM BORROWER PAID RATE SHEET For Lender Paid Comp Plan see below 5/1 LIBOR (Portfolio 6/2/6) ARM (JP51, JP51IO) 7/1 LIBOR (Portfolio 6/2/6) ARM (JP71) 10/1 LIBOR (Portfolio 6/2/6) ARM (JP101)

Differences Across Originators in CMBS Loan Underwriting

Differences Across Originators in CMBS Loan Underwriting Bank Structure Conference Federal Reserve Bank of Chicago, 4 May 2011 Lamont Black, Sean Chu, Andrew Cohen, and Joseph Nichols The opinions expresses

Differences Across Originators in CMBS Loan Underwriting Bank Structure Conference Federal Reserve Bank of Chicago, 4 May 2011 Lamont Black, Sean Chu, Andrew Cohen, and Joseph Nichols The opinions expresses

Housing Finance Policy Center Lunchtime Data Talk Mortgage Modifications Using Principal Reduction: How Effective Are They?

Housing Finance Policy Center Lunchtime Data Talk Mortgage Modifications Using Principal Reduction: How Effective Are They? Ben Keys, University of Chicago Tess Scharlesmann, Office of Financial Research,

Housing Finance Policy Center Lunchtime Data Talk Mortgage Modifications Using Principal Reduction: How Effective Are They? Ben Keys, University of Chicago Tess Scharlesmann, Office of Financial Research,

Investor Presentation. February 11, 2014

Investor Presentation February 11, 2014 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

Investor Presentation February 11, 2014 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

Structured Finance. U.S. RMBS Loan Loss Model Criteria. Residential Mortgage / U.S.A. Sector-Specific Criteria. Scope. Key Rating Drivers

U.S. RMBS Loan Loss Model Criteria Sector-Specific Criteria Residential Mortgage / U.S.A. Inside This Report Page Scope 1 Key Rating Drivers 1 Model Overview 2 Role of the Model in the Rating Process 3

U.S. RMBS Loan Loss Model Criteria Sector-Specific Criteria Residential Mortgage / U.S.A. Inside This Report Page Scope 1 Key Rating Drivers 1 Model Overview 2 Role of the Model in the Rating Process 3

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj The Vanguard Group Rajdeep Sengupta Federal Reserve Bank of St. Louis ECB CFS Research Conference Einaudi

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj The Vanguard Group Rajdeep Sengupta Federal Reserve Bank of St. Louis ECB CFS Research Conference Einaudi

35% 26% 57% 51% PROFILE. CIty of durham: Assets & opportunity ProfILe. key highlights. ABoUt the ProfILe ASSETS & OPPORTUNITY

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

Housing Markets and the Macroeconomy During the 2000s. Erik Hurst July 2016

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

Subprime Bond Case Study Two Harbors Investment Corp. August 6, 2014

Two Harbors Investment Corp. Two Harbors Investment Corp. is proud to present:. The company believes periodic webinars will provide an opportunity to share more in-depth insights on various topics which

Two Harbors Investment Corp. Two Harbors Investment Corp. is proud to present:. The company believes periodic webinars will provide an opportunity to share more in-depth insights on various topics which

Denver Subprime Loan Report

FOR IMMEDIATE RELEASE CONTACT: Stacee Montague March 4, 2008 303-572-2385 stacee.montague@kc.frb.org Denver Subprime Loan Report Mark Schweitzer, Vice President, Branch Executive and Economist, Federal

FOR IMMEDIATE RELEASE CONTACT: Stacee Montague March 4, 2008 303-572-2385 stacee.montague@kc.frb.org Denver Subprime Loan Report Mark Schweitzer, Vice President, Branch Executive and Economist, Federal

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Financial Stability and the Mortgage Market: Canada s Policy Framework. Allan Crawford, Bank of Canada

Financial Stability and the Mortgage Market: Canada s Policy Framework Allan Crawford, Bank of Canada This paper was presented at Housing, Stability and the Macroeconomy: International Perspectives conference,

Financial Stability and the Mortgage Market: Canada s Policy Framework Allan Crawford, Bank of Canada This paper was presented at Housing, Stability and the Macroeconomy: International Perspectives conference,

Mortgage terminology.

Mortgage terminology. Adjustable Rate Mortgage (ARM). A mortgage on which the interest rate, after an initial period, can be changed by the lender. While ARMs in many countries abroad allow rate changes

Mortgage terminology. Adjustable Rate Mortgage (ARM). A mortgage on which the interest rate, after an initial period, can be changed by the lender. While ARMs in many countries abroad allow rate changes

Internet Appendix for A Model of Mortgage Default

Internet Appendix for A Model of Mortgage Default John Y. Campbell 1 João F. Cocco 2 This version: February 2014 1 Department of Economics, Harvard University, Littauer Center, Cambridge, MA 02138, US

Internet Appendix for A Model of Mortgage Default John Y. Campbell 1 João F. Cocco 2 This version: February 2014 1 Department of Economics, Harvard University, Littauer Center, Cambridge, MA 02138, US

Hayne Leland Professor of the Graduate School, Haas School of Business, UC Berkeley Principal, Home Equity Securities (HES)

") 1 Beyond Mortgages: Equity Financing for Homes Hayne Leland Professor of the Graduate School, Haas School of Business, UC Berkeley Principal, Home Equity Securities (HES) FIRS Conference, Lisbon June 2016

1 Beyond Mortgages: Equity Financing for Homes Hayne Leland Professor of the Graduate School, Haas School of Business, UC Berkeley Principal, Home Equity Securities (HES) FIRS Conference, Lisbon June 2016

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Vol 2017, No. 16. Abstract

Mortgage modification in Ireland: a recent history Fergal McCann 1 Economic Letter Series Vol 2017, No. 16 Abstract Mortgage modification has played a central role in the policy response to the mortgage

Mortgage modification in Ireland: a recent history Fergal McCann 1 Economic Letter Series Vol 2017, No. 16 Abstract Mortgage modification has played a central role in the policy response to the mortgage

Strategic Default, Loan Modification and Foreclosure

Strategic Default, Loan Modification and Foreclosure Ben Klopack and Nicola Pierri January 17, 2017 Abstract We study borrower strategic default in the residential mortgage market. We exploit a discontinuity

Strategic Default, Loan Modification and Foreclosure Ben Klopack and Nicola Pierri January 17, 2017 Abstract We study borrower strategic default in the residential mortgage market. We exploit a discontinuity

State Dependency of Monetary Policy: The Refinancing Channel

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

The Influence of Foreclosure Delays on Borrower s Default Behavior

The Influence of Foreclosure Delays on Borrower s Default Behavior Shuang Zhu Department of Finance E.J. Ourso College of Business Administration Louisiana State University Baton Rouge, LA 70803-6308 OFF:

The Influence of Foreclosure Delays on Borrower s Default Behavior Shuang Zhu Department of Finance E.J. Ourso College of Business Administration Louisiana State University Baton Rouge, LA 70803-6308 OFF:

Mortgage Delinquency and Default: A Tale of Two Options

Mortgage Delinquency and Default: A Tale of Two Options Min Hwang Song Song Robert A. Van Order George Washington University George Washington University George Washington University min@gwu.edu songsong@gwmail.gwu.edu

Mortgage Delinquency and Default: A Tale of Two Options Min Hwang Song Song Robert A. Van Order George Washington University George Washington University George Washington University min@gwu.edu songsong@gwmail.gwu.edu

PIMCO Advisory s Approach to RMBS Valuation. December 8, 2010

PIMCO Advisory s Approach to RMBS Valuation December 8, 2010 0 The reports contain modeling based on hypothetical information which has been provided for informational purposes only. No representation

PIMCO Advisory s Approach to RMBS Valuation December 8, 2010 0 The reports contain modeling based on hypothetical information which has been provided for informational purposes only. No representation

Second Quarter 2018 Earnings Call AUGUST 8, 2018

Second Quarter 2018 Earnings Call AUGUST 8, 2018 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

Second Quarter 2018 Earnings Call AUGUST 8, 2018 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

1. Sustained increases in population and job growth. According to US Census information, the

Financial Crisis Inquiry Commission Phil Angelides, Chairman Sacramento Field Hearing September 23, 2010 Thomas C. Putnam, President Putnam Housing Finance Consulting Mr. Chairman and Commissioners Thank

Financial Crisis Inquiry Commission Phil Angelides, Chairman Sacramento Field Hearing September 23, 2010 Thomas C. Putnam, President Putnam Housing Finance Consulting Mr. Chairman and Commissioners Thank

Policy Evaluation: Methods for Testing Household Programs & Interventions

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

during the Financial Crisis

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

RMBS Price Discovery & Transparency

RMBS Price Discovery & Transparency Case Study on the Key Aspects of Pricing UK Non-Conforming RMBS Hikmet Sevdican Mike Li Contents Brief Introduction to RMBS UK Mortgage Market Macroeconomic Factors

RMBS Price Discovery & Transparency Case Study on the Key Aspects of Pricing UK Non-Conforming RMBS Hikmet Sevdican Mike Li Contents Brief Introduction to RMBS UK Mortgage Market Macroeconomic Factors

New Construction and Mortgage Default

New Construction and Mortgage Default ASSA/AREUEA Conference January 6 th, 2019 Tom Mayock UNC Charlotte Office of the Comptroller of the Currency tmayock@uncc.edu Konstantinos Tzioumis ALBA Business School

New Construction and Mortgage Default ASSA/AREUEA Conference January 6 th, 2019 Tom Mayock UNC Charlotte Office of the Comptroller of the Currency tmayock@uncc.edu Konstantinos Tzioumis ALBA Business School

First Quarter 2017 Earnings Call MAY 4, 2017

First Quarter 2017 Earnings Call MAY 4, 2017 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

First Quarter 2017 Earnings Call MAY 4, 2017 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

Homeownership Preservation in Maryland

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

NOVEMBER 16, As Required by the Dodd-Frank Wall Street Reform and Consumer Protection Act

Federal Home Loan Bank of New York 2017 Annual Stress Test Disclosure Results of the Federal Housing Finance Agency Supervisory Severely Adverse Scenario NOVEMBER 16, 2017 As Required by the Dodd-Frank

Federal Home Loan Bank of New York 2017 Annual Stress Test Disclosure Results of the Federal Housing Finance Agency Supervisory Severely Adverse Scenario NOVEMBER 16, 2017 As Required by the Dodd-Frank

Economic and Housing Outlook

Economic and Housing Outlook Volusia Building Industry Association July 18, 218 Robert Dietz, Ph.D. NAHB Chief Economist Housing Market Growing; Single-Family Lags Tax reform changes Macroeconomics post-tax

Economic and Housing Outlook Volusia Building Industry Association July 18, 218 Robert Dietz, Ph.D. NAHB Chief Economist Housing Market Growing; Single-Family Lags Tax reform changes Macroeconomics post-tax

Mortgage Default Option Mispricing and Procyclicality

Mortgage Default Option Mispricing and Procyclicality Andrew Davidson, Andrew Davidson and Co., Inc. Alex Levin, Andrew Davidson and Co., Inc. Susan Wachter, University of Pennsylvania June 19, 2013 Abstract:

Mortgage Default Option Mispricing and Procyclicality Andrew Davidson, Andrew Davidson and Co., Inc. Alex Levin, Andrew Davidson and Co., Inc. Susan Wachter, University of Pennsylvania June 19, 2013 Abstract:

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

Learning to Cope: Voluntary Financial Education and Loan Performance during a Housing Crisis

American Economic Review: Papers & Proceedings 2010, 100:2, 1 10 http://www.aeaweb.org/articles.php?doi=10.1257/aer.100.2.1 Learning to Cope: Voluntary Financial Education and Loan Performance during a

American Economic Review: Papers & Proceedings 2010, 100:2, 1 10 http://www.aeaweb.org/articles.php?doi=10.1257/aer.100.2.1 Learning to Cope: Voluntary Financial Education and Loan Performance during a

An Evaluation of Research on the Performance of Loans with Down Payment Assistance

George Mason University School of Public Policy Center for Regional Analysis An Evaluation of Research on the Performance of Loans with Down Payment Assistance by Lisa A. Fowler, PhD Stephen S. Fuller,

George Mason University School of Public Policy Center for Regional Analysis An Evaluation of Research on the Performance of Loans with Down Payment Assistance by Lisa A. Fowler, PhD Stephen S. Fuller,

Residential Mortgage Credit Model

Residential Mortgage Credit Model June 2016 data made beautiful Four Major Components to the Credit Model 1. Transition Model: An idealized roll-rate model with three states: i. Performing (Current, 30-DPD)

Residential Mortgage Credit Model June 2016 data made beautiful Four Major Components to the Credit Model 1. Transition Model: An idealized roll-rate model with three states: i. Performing (Current, 30-DPD)

MGIC Investment Corporation Bear Stearns Mortgage Finance & Housing Markets Conference May 18, 2006

MGIC Investment Corporation Bear Stearns Mortgage Finance & Housing Markets Conference May 18, 2006 Patrick Sinks President and Chief Operating Officer Safe Harbor Statement During the course of this presentation,

MGIC Investment Corporation Bear Stearns Mortgage Finance & Housing Markets Conference May 18, 2006 Patrick Sinks President and Chief Operating Officer Safe Harbor Statement During the course of this presentation,

Illiquidity and Interest Rate Policy

Illiquidity and Interest Rate Policy Douglas Diamond and Raghuram Rajan University of Chicago Booth School of Business and NBER 2 Motivation Illiquidity and insolvency are likely when long term assets

Illiquidity and Interest Rate Policy Douglas Diamond and Raghuram Rajan University of Chicago Booth School of Business and NBER 2 Motivation Illiquidity and insolvency are likely when long term assets

ARMs: An Overview. Fin 4713 ARM Notes. ARMs: Mechanics. Some ARM Indexes

Slide 1 ARMs: An Overview Slide 2 Fin 4713 ARM Notes The interest rate charged on the note is indexed to other market interest rates The loan payment is adjusted at specified periods. The interest rate

Slide 1 ARMs: An Overview Slide 2 Fin 4713 ARM Notes The interest rate charged on the note is indexed to other market interest rates The loan payment is adjusted at specified periods. The interest rate

The nature of the default risk

Hedging mortgage default risk with mortgage guaranty insurance: A model for Europe? Presentation for the European Mortgage Federation / European Network of Housing Research Joint Seminar on European Mortgage

Hedging mortgage default risk with mortgage guaranty insurance: A model for Europe? Presentation for the European Mortgage Federation / European Network of Housing Research Joint Seminar on European Mortgage

A+ HYBRID PROGRAM. 1 Year (5,3) 5% Months % Months 13-24

5% Months % Months 13-24") LOAN AMOUNT Loan Terms Maximum Amortization A+ HYBRID PROGRAM INCOME PRODUCING REAL ESTATE INCOME QUALIFYING BUSINESS LOAN Minimum: $125,000 Maximum: $1,000,000 Fixed-rate terms of 1, 3 or 5 years with

LOAN AMOUNT Loan Terms Maximum Amortization A+ HYBRID PROGRAM INCOME PRODUCING REAL ESTATE INCOME QUALIFYING BUSINESS LOAN Minimum: $125,000 Maximum: $1,000,000 Fixed-rate terms of 1, 3 or 5 years with

Real gross domestic product

Real gross domestic product United States Compound annual growth rate 10 5 0-5 -10 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 Sources: Bureau of Economic Analysis, IHS Global Insight. Employment by sector

Real gross domestic product United States Compound annual growth rate 10 5 0-5 -10 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 Sources: Bureau of Economic Analysis, IHS Global Insight. Employment by sector

High Default Risk on Down Payment Assistance Program: Adverse Selection Vs. Program Characteristics?

High Default Risk on Down Payment Assistance Program: Adverse Selection Vs. Program Characteristics? Yuanjie Zhang December 22, 2010 Abstract Various government programs have been developed in the United

High Default Risk on Down Payment Assistance Program: Adverse Selection Vs. Program Characteristics? Yuanjie Zhang December 22, 2010 Abstract Various government programs have been developed in the United

Import Competition and Household Debt

Import Competition and Household Debt Barrot (MIT) Plosser (NY Fed) Loualiche (MIT) Sauvagnat (Bocconi) USC Spring 2017 The views expressed in this paper are those of the authors and do not necessarily

Import Competition and Household Debt Barrot (MIT) Plosser (NY Fed) Loualiche (MIT) Sauvagnat (Bocconi) USC Spring 2017 The views expressed in this paper are those of the authors and do not necessarily

Fourth Quarter 2014 Financial Results Supplement

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

Federal Home Loan Bank of Atlanta 2017 Annual Stress Test Disclosure

Federal Home Loan Bank of Atlanta 2017 Annual Stress Test Disclosure Results of the Federal Housing Finance Agency Supervisory Severely Adverse Scenario November 16, 2017 As Required by the Dodd-Frank

Federal Home Loan Bank of Atlanta 2017 Annual Stress Test Disclosure Results of the Federal Housing Finance Agency Supervisory Severely Adverse Scenario November 16, 2017 As Required by the Dodd-Frank

Mortgage Insurance What Have We Learned? (Part 2)

") Mortgage Insurance What Have We Learned? (Part 2) Prepared for: Prepared by: Date: CAS Special Interest Seminar Chicago, IL Michael A. Henk, FCAS, MAAA Consulting Actuary October 1, 2013 Anti-Trust Notice

Mortgage Insurance What Have We Learned? (Part 2) Prepared for: Prepared by: Date: CAS Special Interest Seminar Chicago, IL Michael A. Henk, FCAS, MAAA Consulting Actuary October 1, 2013 Anti-Trust Notice

Subprime Lending in Tennessee

Subprime Lending in Tennessee July 19, 2007 Hulya Arik, Ph.D. Research Coordinator Graphic Design by Paul Henkel, A.B.D. Asst. Director for Research, Planning & Technical Services Presentation Overview

Subprime Lending in Tennessee July 19, 2007 Hulya Arik, Ph.D. Research Coordinator Graphic Design by Paul Henkel, A.B.D. Asst. Director for Research, Planning & Technical Services Presentation Overview