Complex Mortgages. Gene Amromin Federal Reserve Bank of Chicago. Jennifer Huang University of Texas at Austin and Cheung Kong GSB

|

|

|

- Gordon Garrett

- 5 years ago

- Views:

Transcription

1 Gene Amromin Federal Reserve Bank of Chicago Jennifer Huang University of Texas at Austin and Cheung Kong GSB Clemens Sialm University of Texas at Austin and NBER Edward Zhong University of Wisconsin-Madison January, 2012

2 Motivation Over the last decade the residential mortgage market has experienced a significant increase in product complexity. Most of the product innovation focused on products with deferred amortization schedules. Whereas mortgage securitization and the extension of credit to subprime borrowers have received a lot of attention recently, the contract design of mortgages remains largely unexplored.

3 Mortgage Types Fixed Rate Mortgages (FRM) Adjustable Rate Mortgages (ARM) (CM)

4 Mortgage Types Fixed Rate Mortgages (FRM) Adjustable Rate Mortgages (ARM) (CM) Interest Only Mortgages (IO) Option ARMs and Negative Amortization Mortgages (NEGAM)

5 Composition of Mortgages over Time FRM Cumulative Proportion ARM CM

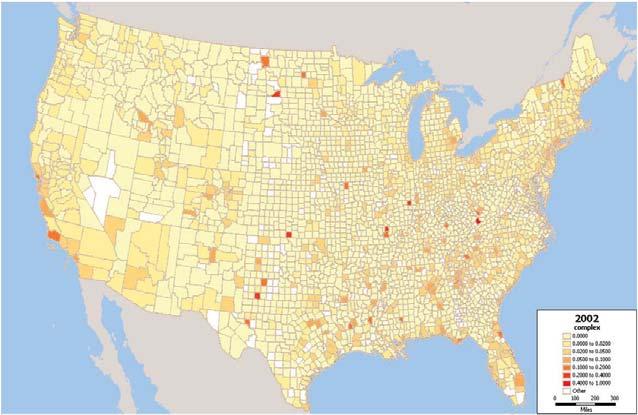

6 in 2002

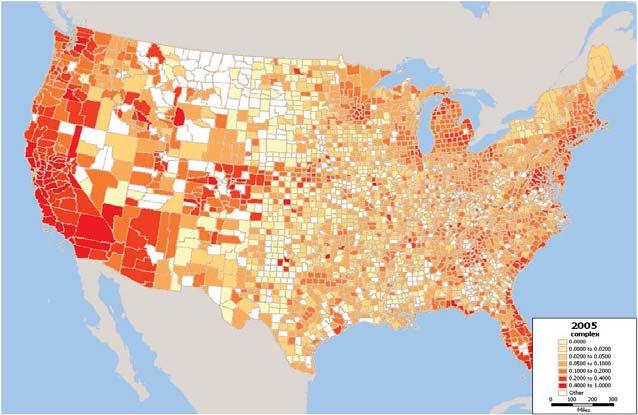

7 in 2005

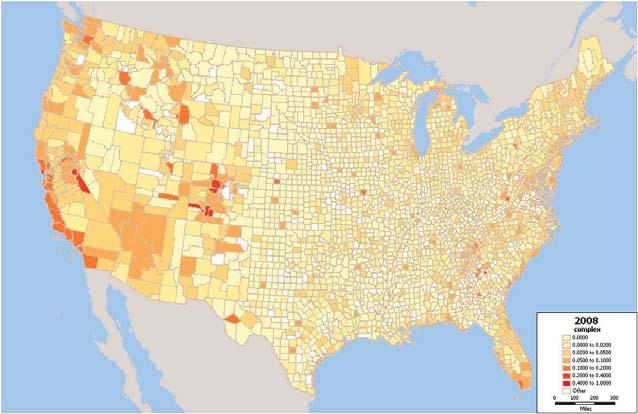

8 in 2008

9 Related Literature on Recent Mortgage Crisis Extension of Credit to Subprime Borrowers Mian and Sufi (2010); Goetzmann, Peng, and Yen (2010) Mortgage Securitization Keys, Mukherjee, Seru, and Vig (2010); Jiang, Nelson, and Vytlacil (2010a, 2010b); Purnanandam (2011) Agency Problems Berndt, Hollifield, Sandas (2010); Woodward and Hall (2010) Regulation Li, White, and Zhu (2010); Favilukis, Ludvigson, and Van Nieuwerburgh (2011)

10 Rationales for Obfuscation: Gabaix and Laibson (2006); Carlin (2009); Carlin and Manso (2009)

11 Rationales for Obfuscation: Gabaix and Laibson (2006); Carlin (2009); Carlin and Manso (2009) Consumption Smoothing: Gerardi, Rosen, and Willen (2010); Piskorski and Tchistyi (2010); Barlevy and Fisher (2010); Cocco (2010); Corbae and Quintin (2010)

12 Rationales for Obfuscation: Gabaix and Laibson (2006); Carlin (2009); Carlin and Manso (2009) Consumption Smoothing: Gerardi, Rosen, and Willen (2010); Piskorski and Tchistyi (2010); Barlevy and Fisher (2010); Cocco (2010); Corbae and Quintin (2010) Option to Default: Amromin, Huang, and Sialm (2007); Guiso, Sapienza, and Zingales (2009)

13 Main Results Obfuscation: Complex mortgages are chosen by relatively sophisticated households with high income levels and prime credit scores.

14 Main Results Obfuscation: Complex mortgages are chosen by relatively sophisticated households with high income levels and prime credit scores. Consumption Smoothing: Complex mortgages are more prevalent in areas of higher expected house price growth (i.e., population growth, prior house price appreciation).

15 Main Results Obfuscation: Complex mortgages are chosen by relatively sophisticated households with high income levels and prime credit scores. Consumption Smoothing: Complex mortgages are more prevalent in areas of higher expected house price growth (i.e., population growth, prior house price appreciation). Option to Default: Complex mortgages are more prevalent in non-recourse states. The difference in the delinquency rates between complex and traditional borrowers increases both with measures of financial sophistication (like income or credit scores) and measures of strategic default (like the LTV ratio). Complex borrowers exhibit a smaller increase in the probability of declaring bankruptcy after defaulting on their mortgages than traditional borrowers.

16 Data Sample of more than 10 million mortgage loans originated in the U.S. from 2003 to 2007 from LPS Analytics. MSA-level data on house price appreciation from the Federal Housing Finance Agency (FHFA). Local macro-economic variables from HMDA, U.S. Census, the BLS, and the BEA.

17 Summary Statistics FRM ARM CM Income 87,835 99, ,581 Income with Full Documentation 85,302 95, ,895 FICO FICO less than First Lien Loan to Value (LTV) Value to Income (VTI) Investment Property Low Documentation Government Securitized Private Securitized Above Conforming Limit College or More House Price Change Prior 5 Years Non-Recourse Mortgage Number of Observations 7,077,626 1,284,132 1,773,843

18 Dynamic Changes in Mortgage Payments Payments on complex mortgages are on average about 20% lower than the payments on fully amortizing fixed rate mortgages during the first five years after origination. Fig 3

19 Dynamic Changes in Mortgage Payments Payments on complex mortgages are on average about 20% lower than the payments on fully amortizing fixed rate mortgages during the first five years after origination. Fig 3 The payments on complex mortgages exhibit payment resets after the introductory period. The mean payment on a complex loan increases by about 10% in the fifth year after origination relative to the payment in the first year. Fig 4

20 Dynamic Changes in Mortgage Payments Payments on complex mortgages are on average about 20% lower than the payments on fully amortizing fixed rate mortgages during the first five years after origination. Fig 3 The payments on complex mortgages exhibit payment resets after the introductory period. The mean payment on a complex loan increases by about 10% in the fifth year after origination relative to the payment in the first year. Fig 4 Due to the deferred amortization, debt levels remain high for an extended time period. Borrowers of complex loans amortize on average only 4% of their loan balance after five years, whereas borrowers of fixed rate loans amortize on average 9%. Fig 5

21 Multinomial Logit Regressions Individual-level MSA-Level Covariates Covariates ARM CM ARM CM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young House Price Change Population Growth Log(BEA Income) Non-Recourse States Observations 10,135,601 8,914,795

22 Robustness Tests The results remain robust using alternative samples or specifications. Inclusion of state and lender fixed effects. Fixed Effects Decomposition of complex loans into Interest-Only (IO) and Negative Amortization Mortgages (NEGAM). Contract Detail Subsamples of full-documentation loans, purchases, non-california loans, non-securitized loans, and loans on investment properties. Subsamples Year-by-year multinomial logit estimation. Year-by-Year

23 Reasons for Mortgage Delinquency Cash Flow Default Complex mortgages exhibit increasing payments over time, as the payments reset when the loans become fully amortizing. Strategic Default Complex mortgages have higher loan-to-value ratios, increasing the option value to default. Complex borrowers exhibit different characteristics or preferences (e.g., risk aversion, income risk, ethical norms).

24 Mortgage Complexity and Delinquency CM Hazard Rate ARM FRM Months After Origination

25 Hazard Models of Mortgage Delinquency CM ARM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young Log(BEA Income) Increase in House Value Increase in Loan Balance Payment Resets Unemployment Rate Income Growth since Origination Government Securitized Private Securitized Observations 32,590,515 25,619,647 25,619,647

26 Hazard Models of Delinquency with Interaction Effects CM CM x Log(Income) CM x FICO CM x LTV ARM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young Log(BEA Income) Increase in House Value Increase in Loan Balance Payment Resets Observations 25,619,647 25,619,647 25,619,647 25,619,647 Interpretation

27 Hazard Models for Personal Bankruptcy CM Delinquency CM x Delinquency ARM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young Log(BEA Income) Increase in House Value Increase in Loan Balance Observations 34,252,339 26,778,403 26,778,403 26,778,403

28 Robustness Tests The results remain robust using alternative samples or specifications. Use of alternative baseline hazard rates (common, state, year, state-year, lender, lender-year). Fixed Effects Decomposition of complex loans into Interest-Only (IO) and Negative Amortization Mortgages (NEGAM). Detailed Contract Subsamples of purchases, full-documentation, non-california loans, investment properties, and securitized loans. Subsample Year-by-year hazard model. Year-by-Year

29 Conclusions Complex mortgages are chosen by relatively high-credit-quality households seeking to purchase more expensive houses relative to their incomes. Borrowers using complex mortgages experience substantially higher ex post default rates after controlling for their credit score and other household and neighborhood characteristics. The results indicate that the strategic default option is an important consideration for complex mortgages.

30 Additional Results

31 Income Level by Mortgage Type Cumulative Distribution FRM ARM CM , , , , ,000 Income

32 FICO Credit Score by Mortgage Type FRM Cumulative Distribution ARM CM FICO Score

33 ValuetoIncome(VTI)RatiobyMortgageType Cumulative Distribution FRM ARM CM Value-to-Income Ratio

34 Mortgage Payment Relative to FRM After 1 Year ARM Distribution CM Actual Mortgage Payment after One Year Relative to FRM Back

35 Mortgage Payment Relative to FRM After 3 Years ARM 0.04 Distribution 0.03 CM Actual Mortgage Payment after Three Years Relative to FRM Back

36 Mortgage Payment Relative to FRM After 5 Years ARM 0.06 Distribution CM Actual Mortgage Payment after Five Years Relative to FRM Back

37 Relative Mortgage Payment After 3 Years CM 0.8 ARM 0.7 Cumulative Distribution Third Year Payment Relative to First Year Payment Back

38 Relative Mortgage Payment After 5 Years CM 0.7 Cumulative Distribution ARM Fifth Year Payment Relative to First Year Payment Back

39 Remaining Mortgage Balance After 1 Year FRM 0.6 Probability Distribution ARM CM Remaining Mortgage Balance After One Year Relative to Original Balance Back

40 Remaining Mortgage Balance After 3 Years FRM CM Probability Distribution ARM Remaining Mortgage Balance After Three Years Relative to Original Balance Back

41 Remaining Mortgage Balance After 5 Years FRM CM Probability Distribution ARM Remaining Mortgage Balance After FiveYears Relative to Original Balance Back

42 Multinomial Logit Regressions: Fixed Effects State Lender Fixed Effects Fixed Effects ARM CM ARM CM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young House Price Change Population Growth Log(BEA Income) Non-Recourse States Observations 8,914,795 6,719,987 Back

43 Multinomial Logit: Detailed Mortgage Contracts Individual-level Covariates MSA-level Covariates ARM IO NEGAM ARM IO NEGAM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young House Price Change Population Growth Log(BEA Income) Non-Recourse States Observations 10,135,601 8,914,795 Back

44 Multinomial Logit (CM Equation): Subsamples Full Purchases Exclude Not Investment Documentation Only California Securitized Properties Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young House Price Change Population Growth Log(BEA Income) Non-Recourse States Observations 3,279,098 5,214,519 7,545, , ,569 Back

45 Multinomial Logit (CM Equation): Year-by-Year Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young House Price Change Population Growth Log(BEA Income) Non-Recourse States Observations 1,420,293 2,244,082 1,651,865 2,272,016 1,326,539 Back

46 Interpretation of Interaction Effects It is important to be careful when interpreting interaction effects in non-linear models (Ai and Norton 2003). The interaction effect in our hazard model can be interpreted as a semi-elasticity of the hazard function: λ(i, t) =λ(t)e (β 0+β 1 CM+β 2 FICO+β 3 CM FICO+ɛ) Taking logs and the derivative derivative gives: log(λ(i, t)) = β 2 + β 3 CM. FICO Since CM is binary, β 3 gives: log(λ(i, t)) log(λ(i, t)) FICO CM=1 FICO = β 3. CM=0 Back

47 Hazard Models: Lender-Year Baselines CM CM x Log(Income) CM x FICO CM x LTV ARM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young Log(BEA Income) Increase in House Value (0.016) (0.016) Increase in Loan Balance (0.010) (0.010) Payment Resets (0.001) (0.001) Observations 25,619,718 25,619,718 Back

48 Hazard Models: Detailed Contract Specification IO NEGAM IO x Log(Income) NEGAM x Log(Income) IO x FICO NEGAM x FICO IO x LTV NEGAM x LTV ARM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young Log(BEA Income) Increase in House Value Increase in Loan Balance Payment Resets Unemployment Rate Income Growth since Origination Observations 25,619,647 25,619,647 25,619,647 25,619,647 25,619,647 Back

49 Hazard Models: Subsamples Full Purchases Exclude Not Investment Documentation Only California Securitized Properties CM CM x Log(Income) CM x FICO CM x LTV ARM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young Log(BEA Income) Increase in House Value Increase in Loan Balance Payment Resets Unemployment Rate Income Growth since Origination Observations 9,345,354 15,116,355 21,713,131 2,330,799 2,443,944 Back

50 Hazard Model: Year-by-Year CM CM x Log(Income) CM x FICO CM x LTV ARM Log(Income) FICO LTV VTI Low Documentation Above Loan Limit Condo Investment Property Refinance College or More Young Log(BEA Income) Increase in House Value Increase in Loan Balance Payment Resets Unemployment Rate Income Growth since Origination Observations 5,482,921 7,174,441 4,895,836 5,549,944 2,516,505 Back

Complex Mortgages. May 2014

Complex Mortgages Gene Amromin, Federal Reserve Bank of Chicago Jennifer Huang, Cheung Kong Graduate School of Business Clemens Sialm, University of Texas-Austin and NBER Edward Zhong, University of Wisconsin

Complex Mortgages Gene Amromin, Federal Reserve Bank of Chicago Jennifer Huang, Cheung Kong Graduate School of Business Clemens Sialm, University of Texas-Austin and NBER Edward Zhong, University of Wisconsin

1. Modification algorithm

Internet Appendix for: "The Effect of Mortgage Securitization on Foreclosure and Modification" 1. Modification algorithm The LPS data set lacks an explicit modification flag but contains enough detailed

Internet Appendix for: "The Effect of Mortgage Securitization on Foreclosure and Modification" 1. Modification algorithm The LPS data set lacks an explicit modification flag but contains enough detailed

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging. Online Appendix

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging Marco Di Maggio, Amir Kermani, Benjamin J. Keys, Tomasz Piskorski, Rodney Ramcharan, Amit Seru, Vincent Yao

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging Marco Di Maggio, Amir Kermani, Benjamin J. Keys, Tomasz Piskorski, Rodney Ramcharan, Amit Seru, Vincent Yao

An Empirical Model of Subprime Mortgage Default from 2000 to 2007

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

Residential Mortgage Default and Consumer Bankruptcy: Theory and Empirical Evidence*

Residential Mortgage Default and Consumer Bankruptcy: Theory and Empirical Evidence* Wenli Li, Philadelphia Federal Reserve and Michelle J. White, UC San Diego and NBER February 2011 *Preliminary draft,

Residential Mortgage Default and Consumer Bankruptcy: Theory and Empirical Evidence* Wenli Li, Philadelphia Federal Reserve and Michelle J. White, UC San Diego and NBER February 2011 *Preliminary draft,

Foreclosure Delay and Consumer Credit Performance

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments. Morgan J. Rose. March 2011

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

Strategic Default, Loan Modification and Foreclosure

Strategic Default, Loan Modification and Foreclosure Ben Klopack and Nicola Pierri January 17, 2017 Abstract We study borrower strategic default in the residential mortgage market. We exploit a discontinuity

Strategic Default, Loan Modification and Foreclosure Ben Klopack and Nicola Pierri January 17, 2017 Abstract We study borrower strategic default in the residential mortgage market. We exploit a discontinuity

The Untold Costs of Subprime Lending: Communities of Color in California. Carolina Reid. Federal Reserve Bank of San Francisco.

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

Backloaded Mortgages and House Price Appreciation

1 / 33 Backloaded Mortgages and House Price Appreciation Gadi Barlevy Jonas D. M. Fisher Chicago Fed Wisconsin-Fed HULM Conference April 9-10, 2010 2 / 33 Introduction: Motivation Widespread house price

1 / 33 Backloaded Mortgages and House Price Appreciation Gadi Barlevy Jonas D. M. Fisher Chicago Fed Wisconsin-Fed HULM Conference April 9-10, 2010 2 / 33 Introduction: Motivation Widespread house price

WORKING PAPER NO SECURITIZATION AND MORTGAGE DEFAULT: REPUTATION VS. ADVERSE SELECTION. Ronel Elul Federal Reserve Bank of Philadelphia

WORKING PAPER NO. 09-21 SECURITIZATION AND MORTGAGE DEFAULT: REPUTATION VS. ADVERSE SELECTION Ronel Elul Federal Reserve Bank of Philadelphia First version: April 29, 2009 This version: September 22, 2009

WORKING PAPER NO. 09-21 SECURITIZATION AND MORTGAGE DEFAULT: REPUTATION VS. ADVERSE SELECTION Ronel Elul Federal Reserve Bank of Philadelphia First version: April 29, 2009 This version: September 22, 2009

Mortgage Financing in the Housing Boom and Bust

Mortgage Financing in the Housing Boom and Bust Benjamin J. Keys University of Chicago Tomasz Piskorski Columbia GSB Amit Seru University of Chicago and NBER Vikrant Vig London Business School ABSTRACT:

Mortgage Financing in the Housing Boom and Bust Benjamin J. Keys University of Chicago Tomasz Piskorski Columbia GSB Amit Seru University of Chicago and NBER Vikrant Vig London Business School ABSTRACT:

Homeownership and Nontraditional and Subprime Mortgages

Housing Policy Debate ISSN: 1051-1482 (Print) 2152-050X (Online) Journal homepage: http://www.tandfonline.com/loi/rhpd20 Homeownership and Nontraditional and Subprime Mortgages Arthur Acolin, Xudong An,

Housing Policy Debate ISSN: 1051-1482 (Print) 2152-050X (Online) Journal homepage: http://www.tandfonline.com/loi/rhpd20 Homeownership and Nontraditional and Subprime Mortgages Arthur Acolin, Xudong An,

Announcement March 5, Updates and Clarifications for Streamlined Refinance Products

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Self-reporting under SEC Reg AB and transparency in securitization: evidence from loan-level disclosure of risk factors in RMBS deals

Self-reporting under SEC Reg AB and transparency in securitization: evidence from loan-level disclosure of risk factors in RMBS deals by Joseph R. Mason, Louisiana State University Michael B. Imerman,

Self-reporting under SEC Reg AB and transparency in securitization: evidence from loan-level disclosure of risk factors in RMBS deals by Joseph R. Mason, Louisiana State University Michael B. Imerman,

Mortgage Rates, Household Balance Sheets, and Real Economy

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

An Empirical Study on Default Factors for US Sub-prime Residential Loans

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

An Empirical Study on Default Factors for US Sub-prime Residential Loans Kai-Jiun Chang, Ph.D. Candidate, National Taiwan University, Taiwan ABSTRACT This research aims to identify the loan characteristics

NBER WORKING PAPER SERIES DID BANKRUPTCY REFORM CAUSE MORTGAGE DEFAULT TO RISE? Wenli Li Michelle J. White Ning Zhu

NBER WORKING PAPER SERIES DID BANKRUPTCY REFORM CAUSE MORTGAGE DEFAULT TO RISE? Wenli Li Michelle J. White Ning Zhu Working Paper 15968 http://www.nber.org/papers/w15968 NATIONAL BUREAU OF ECONOMIC RESEARCH

NBER WORKING PAPER SERIES DID BANKRUPTCY REFORM CAUSE MORTGAGE DEFAULT TO RISE? Wenli Li Michelle J. White Ning Zhu Working Paper 15968 http://www.nber.org/papers/w15968 NATIONAL BUREAU OF ECONOMIC RESEARCH

Understanding the Subprime Mortgage Crisis

Understanding the Subprime Mortgage Crisis Yuliya Demyanyk, Otto Van Hemert This Draft: August 19, 2 First Draft: October 9, 27 Abstract Using loan-level data, we analyze the quality of subprime mortgage

Understanding the Subprime Mortgage Crisis Yuliya Demyanyk, Otto Van Hemert This Draft: August 19, 2 First Draft: October 9, 27 Abstract Using loan-level data, we analyze the quality of subprime mortgage

Loan Product Steering in Mortgage Markets

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Subprime Loan Performance

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao October 2, 2014 Abstract Regulation AB (Reg AB) enacted in 2006 mandates

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao October 2, 2014 Abstract Regulation AB (Reg AB) enacted in 2006 mandates

NBER WORKING PAPER SERIES THE ROLE OF MORTGAGE BROKERS IN THE SUBPRIME CRISIS. Antje Berndt Burton Hollifield Patrik Sandås

NBER WORKING PAPER SERIES THE ROLE OF MORTGAGE BROKERS IN THE SUBPRIME CRISIS Antje Berndt Burton Hollifield Patrik Sandås Working Paper 16175 http://www.nber.org/papers/w16175 NATIONAL BUREAU OF ECONOMIC

NBER WORKING PAPER SERIES THE ROLE OF MORTGAGE BROKERS IN THE SUBPRIME CRISIS Antje Berndt Burton Hollifield Patrik Sandås Working Paper 16175 http://www.nber.org/papers/w16175 NATIONAL BUREAU OF ECONOMIC

The Hidden Peril: The Role of the Condo Loan Market in the Recent Financial Crisis *

The Hidden Peril: The Role of the Condo Loan Market in the Recent Financial Crisis * Sumit Agarwal, Yongheng Deng, Chenxi Luo, and Wenlan Qian National University of Singapore October 2012 * Acknowledgements:

The Hidden Peril: The Role of the Condo Loan Market in the Recent Financial Crisis * Sumit Agarwal, Yongheng Deng, Chenxi Luo, and Wenlan Qian National University of Singapore October 2012 * Acknowledgements:

We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal, (X2)

to estimate the optimal, (X2)") Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Online appendix: Optimal refinancing rate We follow Agarwal, Driscoll, and Laibson (2012; henceforth, ADL) to estimate the optimal refinance rate or, equivalently, the optimal refi rate differential. In

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices?

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

Credit-Induced Boom and Bust

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions. Ingrid Gould Ellen

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

Did Bankruptcy Reform Cause Mortgage Defaults to Rise? 1

Did Bankruptcy Reform Cause Mortgage Defaults to Rise? 1 Wenli Li, Federal Reserve Bank of Philadelphia Michelle J. White, UC San Diego and NBER and Ning Zhu, University of California, Davis Original draft:

Did Bankruptcy Reform Cause Mortgage Defaults to Rise? 1 Wenli Li, Federal Reserve Bank of Philadelphia Michelle J. White, UC San Diego and NBER and Ning Zhu, University of California, Davis Original draft:

Default Option Exercise over the Financial Crisis and Beyond *

Default Option Exercise over the Financial Crisis and Beyond * Xudong An San Diego State University Yongheng Deng National University of Singapore Stuart A. Gabriel UCLA Abstract We provide new evidence

Default Option Exercise over the Financial Crisis and Beyond * Xudong An San Diego State University Yongheng Deng National University of Singapore Stuart A. Gabriel UCLA Abstract We provide new evidence

Pathways after Default: What Happens to Distressed Mortgage Borrowers and Their Homes?

NELLCO NELLCO Legal Scholarship Repository New York University Law and Economics Working Papers New York University School of Law 10-1-2011 Pathways after Default: What Happens to Distressed Mortgage Borrowers

NELLCO NELLCO Legal Scholarship Repository New York University Law and Economics Working Papers New York University School of Law 10-1-2011 Pathways after Default: What Happens to Distressed Mortgage Borrowers

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013 JOSHUA WHITE AND SCOTT BAUGUESS 2 Division of Economic and Risk Analysis (DERA) U.S. Securities and Exchange

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013 JOSHUA WHITE AND SCOTT BAUGUESS 2 Division of Economic and Risk Analysis (DERA) U.S. Securities and Exchange

ADVERSE SELECTION IN MORTGAGE SECURITIZATION *

ADVERSE SELECTION IN MORTGAGE SECURITIZATION * Sumit Agarwal 1, Yan Chang 2, and Abdullah Yavas 3 Abstract We investigate lenders choice of loans to securitize and whether the loans they sell into the

ADVERSE SELECTION IN MORTGAGE SECURITIZATION * Sumit Agarwal 1, Yan Chang 2, and Abdullah Yavas 3 Abstract We investigate lenders choice of loans to securitize and whether the loans they sell into the

Fannie Mae National Housing Survey

Fannie Mae National Housing Survey What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from recent Fannie Mae acquisitions Topic Analysis 4/13/2015 Fannie Mae 2015 Table of Contents

Fannie Mae National Housing Survey What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from recent Fannie Mae acquisitions Topic Analysis 4/13/2015 Fannie Mae 2015 Table of Contents

Subprime Loan Performance

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao May 22, 2015 Abstract In 2006, the US Securities and Exchange Commission

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao May 22, 2015 Abstract In 2006, the US Securities and Exchange Commission

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom?

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST. Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth)

Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth)") 1 DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth) 2 Motivation Lasting impact of the 2008 mortgage crisis on

1 DYNAMICS OF HOUSING DEBT IN THE RECENT BOOM AND BUST Manuel Adelino (Duke) Antoinette Schoar (MIT Sloan and NBER) Felipe Severino (Dartmouth) 2 Motivation Lasting impact of the 2008 mortgage crisis on

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market. Online Appendix

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class. Internet Appendix. Manuel Adelino, Duke University

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class Internet Appendix Manuel Adelino, Duke University Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth College

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class Internet Appendix Manuel Adelino, Duke University Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth College

during the Financial Crisis

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

Structuring Mortgages for Macroeconomic Stability

Structuring Mortgages for Macroeconomic Stability John Y. Campbell, Nuno Clara, and Joao Cocco Harvard University and London Business School CEAR-RSI Household Finance Workshop Montréal November 16, 2018

Structuring Mortgages for Macroeconomic Stability John Y. Campbell, Nuno Clara, and Joao Cocco Harvard University and London Business School CEAR-RSI Household Finance Workshop Montréal November 16, 2018

A Fistful of Dollars: Lobbying and the Financial Crisis

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

Long line of research on mortgage default due to its wide impact

Xudong An, Yongheng Deng and Stuart Gabriel January 15, 2015 Background y Mortgage default was emblematic of the crisis period y Caused the failure of numerous big financial institutions y Bearn Sterns,

Xudong An, Yongheng Deng and Stuart Gabriel January 15, 2015 Background y Mortgage default was emblematic of the crisis period y Caused the failure of numerous big financial institutions y Bearn Sterns,

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke. Antoinette Schoar, MIT and NBER

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: December 15 First

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: December 15 First

The subprime lending boom increased the ability of many Americans to get

ANDREW HAUGHWOUT Federal Reserve Bank of New York CHRISTOPHER MAYER Columbia Business School National Bureau of Economic Research Federal Reserve Bank of New York JOSEPH TRACY Federal Reserve Bank of New

ANDREW HAUGHWOUT Federal Reserve Bank of New York CHRISTOPHER MAYER Columbia Business School National Bureau of Economic Research Federal Reserve Bank of New York JOSEPH TRACY Federal Reserve Bank of New

Liar s Loan? Effects of Origination Channel and Information Falsification on Mortgage Delinquency 1

Liar s Loan? Effects of Origination Channel and Information Falsification on Mortgage Delinquency 1 Wei Jiang 2 Ashlyn Aiko Nelson 3 Edward Vytlacil 4 This Draft: September 2009 1 The authors thank a major

Liar s Loan? Effects of Origination Channel and Information Falsification on Mortgage Delinquency 1 Wei Jiang 2 Ashlyn Aiko Nelson 3 Edward Vytlacil 4 This Draft: September 2009 1 The authors thank a major

Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks

Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks Greg Buchak, University of Chicago Gregor Matvos, Chicago Booth and NBER Tomek Piskorski, Columbia GSB and NBER Amit Seru, Stanford University

Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks Greg Buchak, University of Chicago Gregor Matvos, Chicago Booth and NBER Tomek Piskorski, Columbia GSB and NBER Amit Seru, Stanford University

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market Lan Shi lshi@urban.org Yan (Jenny) Zhang Yan.Zhang@occ.treas.gov Presentation Sept.

The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market Lan Shi lshi@urban.org Yan (Jenny) Zhang Yan.Zhang@occ.treas.gov Presentation Sept.

State-dependent effects of monetary policy: The refinancing channel

https://voxeu.org State-dependent effects of monetary policy: The refinancing channel Martin Eichenbaum, Sérgio Rebelo, Arlene Wong 02 December 2018 Mortgage rate systems vary in practice across countries,

https://voxeu.org State-dependent effects of monetary policy: The refinancing channel Martin Eichenbaum, Sérgio Rebelo, Arlene Wong 02 December 2018 Mortgage rate systems vary in practice across countries,

Housing Markets and the Macroeconomy During the 2000s. Erik Hurst July 2016

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

Adecade-long boom in the housing market and related

The Review of Economics and Statistics VOL. XCVI MARCH 2014 NUMBER 1 LIAR S LOAN? EFFECTS OF ORIGINATION CHANNEL AND INFORMATION FALSIFICATION ON MORTGAGE DELINQUENCY Wei Jiang, Ashlyn Aiko Nelson, and

The Review of Economics and Statistics VOL. XCVI MARCH 2014 NUMBER 1 LIAR S LOAN? EFFECTS OF ORIGINATION CHANNEL AND INFORMATION FALSIFICATION ON MORTGAGE DELINQUENCY Wei Jiang, Ashlyn Aiko Nelson, and

The Dynamics of Adjustable-Rate Subprime Mortgage Default: A Structural Estimation

The Dynamics of Adjustable-Rate Subprime Mortgage Default: A Structural Estimation Hanming Fang You Suk Kim Wenli Li May 27, 2015 Abstract One important characteristic of the recent mortgage crisis is

The Dynamics of Adjustable-Rate Subprime Mortgage Default: A Structural Estimation Hanming Fang You Suk Kim Wenli Li May 27, 2015 Abstract One important characteristic of the recent mortgage crisis is

Can t Pay or Won t Pay? Unemployment, Negative Equity, and Strategic Default

Can t Pay or Won t Pay? Unemployment, Negative Equity, and Strategic Default Kristopher Gerardi, Kyle F. Herkenhoff, Lee E. Ohanian, and Paul S. Willen December 6, 2016 Abstract This paper exploits matched

Can t Pay or Won t Pay? Unemployment, Negative Equity, and Strategic Default Kristopher Gerardi, Kyle F. Herkenhoff, Lee E. Ohanian, and Paul S. Willen December 6, 2016 Abstract This paper exploits matched

NBER WORKING PAPER SERIES HOUSEHOLD DEBT AND DEFAULTS FROM 2000 TO 2010: FACTS FROM CREDIT BUREAU DATA. Atif Mian Amir Sufi

NBER WORKING PAPER SERIES HOUSEHOLD DEBT AND DEFAULTS FROM 2000 TO 2010: FACTS FROM CREDIT BUREAU DATA Atif Mian Amir Sufi Working Paper 21203 http://www.nber.org/papers/w21203 NATIONAL BUREAU OF ECONOMIC

NBER WORKING PAPER SERIES HOUSEHOLD DEBT AND DEFAULTS FROM 2000 TO 2010: FACTS FROM CREDIT BUREAU DATA Atif Mian Amir Sufi Working Paper 21203 http://www.nber.org/papers/w21203 NATIONAL BUREAU OF ECONOMIC

Not all prepayment penalties are created equal

ABSTRACT Not all prepayment penalties are created equal Kelly R. Rush Mount Vernon Nazarene University Chris Neuenschwander Anderson University The study was an examination of prepayment and default of

ABSTRACT Not all prepayment penalties are created equal Kelly R. Rush Mount Vernon Nazarene University Chris Neuenschwander Anderson University The study was an examination of prepayment and default of

Rethinking the Role of Racial Segregation in the American Foreclosure Crisis

Rethinking the Role of Racial Segregation in the American Foreclosure Crisis Jonathan P. Latner* Bremen International Graduate School of Social Science Abstract Racial segregation is an important factor

Rethinking the Role of Racial Segregation in the American Foreclosure Crisis Jonathan P. Latner* Bremen International Graduate School of Social Science Abstract Racial segregation is an important factor

New Developments in Housing Policy

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke. Antoinette Schoar, MIT and NBER

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: December 15 First

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: December 15 First

The Influence of Foreclosure Delays on Borrower s Default Behavior

The Influence of Foreclosure Delays on Borrower s Default Behavior Shuang Zhu Department of Finance E.J. Ourso College of Business Administration Louisiana State University Baton Rouge, LA 70803-6308 OFF:

The Influence of Foreclosure Delays on Borrower s Default Behavior Shuang Zhu Department of Finance E.J. Ourso College of Business Administration Louisiana State University Baton Rouge, LA 70803-6308 OFF:

Determinants of the Incidence of Loan Modifications. April 2011

DRAFT - PLEASE DO NOT CITE OR QUOTE WITHOUT PERMISSION OF THE AUTHORS Determinants of the Incidence of Loan Modifications Vicki Been and Mary Weselcouch*; Ioan Voicu and Scott Murff** April 2011 * Furman

DRAFT - PLEASE DO NOT CITE OR QUOTE WITHOUT PERMISSION OF THE AUTHORS Determinants of the Incidence of Loan Modifications Vicki Been and Mary Weselcouch*; Ioan Voicu and Scott Murff** April 2011 * Furman

The Role of Mortgage Brokers in the. Subprime Crisis

The Role of Mortgage Brokers in the Subprime Crisis Antje Berndt Burton Hollifield Patrik Sandås March 15, 2010 JEL Classifications: G12, G18, G21, G32 Keywords: Mortgage brokers; Broker compensation;

The Role of Mortgage Brokers in the Subprime Crisis Antje Berndt Burton Hollifield Patrik Sandås March 15, 2010 JEL Classifications: G12, G18, G21, G32 Keywords: Mortgage brokers; Broker compensation;

A Model of Mortgage Default

A Model of Mortgage Default John Y. Campbell 1 João F. Cocco 2 First draft: November 2010 JEL classification: G21, E21. Keywords: Household finance, loan to value ratio, loan to income ratio, negative

A Model of Mortgage Default John Y. Campbell 1 João F. Cocco 2 First draft: November 2010 JEL classification: G21, E21. Keywords: Household finance, loan to value ratio, loan to income ratio, negative

Collateral Valuation and Borrower Financial Constraints: Evidence from the Residential Real Estate Market

Collateral Valuation and Borrower Financial Constraints: Evidence from the Residential Real Estate Market Sumit Agarwal National University of Singapore, ushakri@yahoo.com Itzhak Ben-David Fisher College

Collateral Valuation and Borrower Financial Constraints: Evidence from the Residential Real Estate Market Sumit Agarwal National University of Singapore, ushakri@yahoo.com Itzhak Ben-David Fisher College

Online Appendix to: Regional Redistribution

Online Appendix to: Regional Redistribution Erik Hurst University of Chicago Booth School of Business and NBER Benjamin J. Keys University of Chicago Harris School of Public Policy Joseph S. Vavra University

Online Appendix to: Regional Redistribution Erik Hurst University of Chicago Booth School of Business and NBER Benjamin J. Keys University of Chicago Harris School of Public Policy Joseph S. Vavra University

The Rise in Mortgage Defaults

The Rise in Mortgage Defaults Chris Mayer, Karen Pence, and Shane M. Sherlund November 2008 Christopher J. Mayer is Paul Milstein Professor of Finance and Economics, Columbia Business School, New York,

The Rise in Mortgage Defaults Chris Mayer, Karen Pence, and Shane M. Sherlund November 2008 Christopher J. Mayer is Paul Milstein Professor of Finance and Economics, Columbia Business School, New York,

A New Look at the U.S. Foreclosure Crisis: Panel Data Evidence of Prime and Subprime Lending. Preliminary Draft: Feb 23, 2015

A New Look at the U.S. Foreclosure Crisis: Panel Data Evidence of Prime and Subprime Lending Preliminary Draft: Feb 23, 2015 Fernando Ferreira and Joseph Gyourko The Wharton School University of Pennsylvania

A New Look at the U.S. Foreclosure Crisis: Panel Data Evidence of Prime and Subprime Lending Preliminary Draft: Feb 23, 2015 Fernando Ferreira and Joseph Gyourko The Wharton School University of Pennsylvania

Villains or Scapegoats? The Role of Subprime Borrowers during the Housing Boom

Villains or Scapegoats? The Role of Subprime Borrowers during the Housing Boom James Conklin W. Scott Frame Kristopher Gerardi Haoyang Liu May 23, 2018 Abstract An expansion in mortgage credit to subprime

Villains or Scapegoats? The Role of Subprime Borrowers during the Housing Boom James Conklin W. Scott Frame Kristopher Gerardi Haoyang Liu May 23, 2018 Abstract An expansion in mortgage credit to subprime

The first hints of trouble in the mortgage market surfaced in mid-2005, and

Journal of Economic Perspectives Volume 23, Number 1 Winter 2009 Pages 27 50 The Rise in Mortgage Defaults Christopher Mayer, Karen Pence, and Shane M. Sherlund The first hints of trouble in the mortgage

Journal of Economic Perspectives Volume 23, Number 1 Winter 2009 Pages 27 50 The Rise in Mortgage Defaults Christopher Mayer, Karen Pence, and Shane M. Sherlund The first hints of trouble in the mortgage

NBER WORKING PAPER SERIES COLLATERAL VALUATION AND BORROWER FINANCIAL CONSTRAINTS: EVIDENCE FROM THE RESIDENTIAL REAL ESTATE MARKET

NBER WORKING PAPER SERIES COLLATERAL VALUATION AND BORROWER FINANCIAL CONSTRAINTS: EVIDENCE FROM THE RESIDENTIAL REAL ESTATE MARKET Sumit Agarwal Itzhak Ben-David Vincent Yao Working Paper 19606 http://www.nber.org/papers/w19606

NBER WORKING PAPER SERIES COLLATERAL VALUATION AND BORROWER FINANCIAL CONSTRAINTS: EVIDENCE FROM THE RESIDENTIAL REAL ESTATE MARKET Sumit Agarwal Itzhak Ben-David Vincent Yao Working Paper 19606 http://www.nber.org/papers/w19606

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom?

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent, Rubén Hernández-Murillo, and Michael T. Owyang Keywords: Mortgages, Loan Performance, Community Reinvestment

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent, Rubén Hernández-Murillo, and Michael T. Owyang Keywords: Mortgages, Loan Performance, Community Reinvestment

What Broker Charges Reveal about Mortgage Risk

What Broker Charges Reveal about Mortgage Risk Antje Berndt Burton Hollifield Patrik Sandås March 2012 Preliminary version Abstract Prior to the subprime crisis, mortgage brokers charged higher fees for

What Broker Charges Reveal about Mortgage Risk Antje Berndt Burton Hollifield Patrik Sandås March 2012 Preliminary version Abstract Prior to the subprime crisis, mortgage brokers charged higher fees for

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Benjamin J. Keys, University of Chicago* Tomasz Piskorski, Columbia Business School Amit Seru, University of Chicago and NBER Vincent Yao,

Mortgage Rates, Household Balance Sheets, and the Real Economy Benjamin J. Keys, University of Chicago* Tomasz Piskorski, Columbia Business School Amit Seru, University of Chicago and NBER Vincent Yao,

Agency Conflicts in Residential Mortgage Securitization: What Does the Empirical Literature Tell Us?

FEDERAL RESERVE BANK of ATLANTA WORKING PAPER SERIES Agency Conflicts in Residential Mortgage Securitization: What Does the Empirical Literature Tell Us? W. Scott Frame Working Paper 2017-1 March 2017

FEDERAL RESERVE BANK of ATLANTA WORKING PAPER SERIES Agency Conflicts in Residential Mortgage Securitization: What Does the Empirical Literature Tell Us? W. Scott Frame Working Paper 2017-1 March 2017

The Subprime Crisis:

The Subprime Crisis: Can problems in a small part of the mortgage market disrupt the entire economy? Paul Willen Federal Reserve Bank of Boston REFA Meeting, December 6, 27 The following reflects the views

The Subprime Crisis: Can problems in a small part of the mortgage market disrupt the entire economy? Paul Willen Federal Reserve Bank of Boston REFA Meeting, December 6, 27 The following reflects the views

Impact of Information Asymmetry and Servicer Incentives on Foreclosure of Securitized Mortgages

Impact of Information Asymmetry and Servicer Incentives on Foreclosure of Securitized Mortgages Dimuthu Ratnadiwakara March 2016 ABSTRACT In this paper I examine how servicer characteristics affect foreclosure

Impact of Information Asymmetry and Servicer Incentives on Foreclosure of Securitized Mortgages Dimuthu Ratnadiwakara March 2016 ABSTRACT In this paper I examine how servicer characteristics affect foreclosure

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

NBER WORKING PAPER SERIES THE DYNAMICS OF ADJUSTABLE-RATE SUBPRIME MORTGAGE DEFAULT: A STRUCTURAL ESTIMATION. Hanming Fang You Suk Kim Wenli Li

NBER WORKING PAPER SERIES THE DYNAMICS OF ADJUSTABLE-RATE SUBPRIME MORTGAGE DEFAULT: A STRUCTURAL ESTIMATION Hanming Fang You Suk Kim Wenli Li Working Paper 21810 http://www.nber.org/papers/w21810 NATIONAL

NBER WORKING PAPER SERIES THE DYNAMICS OF ADJUSTABLE-RATE SUBPRIME MORTGAGE DEFAULT: A STRUCTURAL ESTIMATION Hanming Fang You Suk Kim Wenli Li Working Paper 21810 http://www.nber.org/papers/w21810 NATIONAL

Mortgage Delinquency and Default: A Tale of Two Options

Mortgage Delinquency and Default: A Tale of Two Options Min Hwang Song Song Robert A. Van Order George Washington University George Washington University George Washington University min@gwu.edu songsong@gwmail.gwu.edu

Mortgage Delinquency and Default: A Tale of Two Options Min Hwang Song Song Robert A. Van Order George Washington University George Washington University George Washington University min@gwu.edu songsong@gwmail.gwu.edu

Market Structure, Credit Expansion and Mortgage Default Risks

Market Structure, Credit Expansion and Mortgage Default Risks Liu, Bo 1 Shilling, James D. 2 Sing, Tien Foo #3 Revised: May 12, 2011 1 Department of Real Estate; School of Design and Environment; National

Market Structure, Credit Expansion and Mortgage Default Risks Liu, Bo 1 Shilling, James D. 2 Sing, Tien Foo #3 Revised: May 12, 2011 1 Department of Real Estate; School of Design and Environment; National

Credit Growth and the Financial Crisis: A New Narrative

Credit Growth and the Financial Crisis: A New Narrative Stefania Albanesi, University of Pittsburgh Giacomo De Giorgi, University of Geneva Jaromir Nosal, Boston College Fifth Conference on Household Finance

Credit Growth and the Financial Crisis: A New Narrative Stefania Albanesi, University of Pittsburgh Giacomo De Giorgi, University of Geneva Jaromir Nosal, Boston College Fifth Conference on Household Finance

Lessons to Learn from CRA Lending

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

Challenges to E ective Renegotiation of Residential Mortgages

Challenges to E ective Renegotiation of Residential Mortgages Tomek Piskorski Edward S. Gordon Associate Professor of Real Estate and Finance Columbia Business School July 2012 (Columbia Business School)

Challenges to E ective Renegotiation of Residential Mortgages Tomek Piskorski Edward S. Gordon Associate Professor of Real Estate and Finance Columbia Business School July 2012 (Columbia Business School)

Loan Product Steering in Mortgage Markets

Loan Product Steering in Mortgage Markets Sumit Agarwal, Gene Amromin, Itzhak Ben-David and Douglas D. Evanoff * ABSTRACT Accusations of unscrupulous lender behavior e.g., predatory lending abounded during

Loan Product Steering in Mortgage Markets Sumit Agarwal, Gene Amromin, Itzhak Ben-David and Douglas D. Evanoff * ABSTRACT Accusations of unscrupulous lender behavior e.g., predatory lending abounded during

Loan Modifications and Redefault Risk An Examination of Short-term Impacts

Loan Modifications and Redefault Risk An Examination of Short-term Impacts Roberto G. Quercia, Lei Ding, and Janneke Ratcliffe * Abstract One promising strategy to stem the flood of home foreclosure is

Loan Modifications and Redefault Risk An Examination of Short-term Impacts Roberto G. Quercia, Lei Ding, and Janneke Ratcliffe * Abstract One promising strategy to stem the flood of home foreclosure is

Financial Stability and the Mortgage Market: Canada s Policy Framework. Allan Crawford, Bank of Canada

Financial Stability and the Mortgage Market: Canada s Policy Framework Allan Crawford, Bank of Canada This paper was presented at Housing, Stability and the Macroeconomy: International Perspectives conference,

Financial Stability and the Mortgage Market: Canada s Policy Framework Allan Crawford, Bank of Canada This paper was presented at Housing, Stability and the Macroeconomy: International Perspectives conference,

Defined Contribution Pension Plans: Sticky or Discerning Money?

Defined Contribution Pension Plans: Sticky or Discerning Money? Clemens Sialm University of Texas at Austin, Stanford University, and NBER Laura Starks University of Texas at Austin Hanjiang Zhang Nanyang

Defined Contribution Pension Plans: Sticky or Discerning Money? Clemens Sialm University of Texas at Austin, Stanford University, and NBER Laura Starks University of Texas at Austin Hanjiang Zhang Nanyang

A Tale of Two Tensions: Balancing Access to Credit and Credit Risk in Mortgage Underwriting. Marsha J. Courchane Charles River Associates

A Tale of Two Tensions: Balancing Access to Credit and Credit Risk in Mortgage Underwriting Marsha J. Courchane Charles River Associates Leonard C. Kiefer Freddie Mac Peter M. Zorn Freddie Mac January

A Tale of Two Tensions: Balancing Access to Credit and Credit Risk in Mortgage Underwriting Marsha J. Courchane Charles River Associates Leonard C. Kiefer Freddie Mac Peter M. Zorn Freddie Mac January

MBS ratings and the mortgage credit boom

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

Housing Market and Mortgage Performance in the Fifth District

QUARTERLY UPDATE Housing Market and Mortgage Performance in the Fifth District 3 rd Quarter, 2013 Jamie Feik Lisa Hearl Joseph Mengedoth An Update on Housing Market and Mortgage Performance in the Fifth

QUARTERLY UPDATE Housing Market and Mortgage Performance in the Fifth District 3 rd Quarter, 2013 Jamie Feik Lisa Hearl Joseph Mengedoth An Update on Housing Market and Mortgage Performance in the Fifth

Recent Developments in Consumer Credit and Payments*

Recent Developments in Consumer Credit and Payments* BY MITCHELL BERLIN O n September 24-25, 2009, the Research Department and the Payment Cards Center of the Federal Reserve Bank of Philadelphia held

Recent Developments in Consumer Credit and Payments* BY MITCHELL BERLIN O n September 24-25, 2009, the Research Department and the Payment Cards Center of the Federal Reserve Bank of Philadelphia held

The Attractions and Perils of Flexible Mortgage Lending

The Attractions and Perils of Flexible Mortgage Lending Mark J. Garmaise UCLA Anderson Abstract A mortgage program that offered borrowers greater flexibility in the timing of repayments increased a bank

The Attractions and Perils of Flexible Mortgage Lending Mark J. Garmaise UCLA Anderson Abstract A mortgage program that offered borrowers greater flexibility in the timing of repayments increased a bank

Mortgage Modeling: Topics in Robustness. Robert Reeves September 2012 Bank of America

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

The new Prudential treatment for residential real estate

The new Prudential treatment for residential real estate 04/09/2009 Pag. 1 di 7 The new Prudential treatment for residential real estate This paper describes the CRIF position about a specific question

The new Prudential treatment for residential real estate 04/09/2009 Pag. 1 di 7 The new Prudential treatment for residential real estate This paper describes the CRIF position about a specific question

Model Stability and the Subprime Mortgage Crisis

IRES2010-010 IRES Working Paper Series Model Stability and the Subprime Mortgage Crisis Xudong An Yongheng Deng Eric Rosenblatt Vincent W. Yao September 12, 2010 Model Stability and the Subprime Mortgage

IRES2010-010 IRES Working Paper Series Model Stability and the Subprime Mortgage Crisis Xudong An Yongheng Deng Eric Rosenblatt Vincent W. Yao September 12, 2010 Model Stability and the Subprime Mortgage

What Drives Racial and Ethnic Differences in High Cost Mortgages? The Role of High Risk Lenders

What Drives Racial and Ethnic Differences in High Cost Mortgages? The Role of High Risk Lenders Patrick Bayer Duke University Fernando Ferreira University of Pennsylvania (Wharton) Stephen L. Ross University

What Drives Racial and Ethnic Differences in High Cost Mortgages? The Role of High Risk Lenders Patrick Bayer Duke University Fernando Ferreira University of Pennsylvania (Wharton) Stephen L. Ross University

Credit Risk of Low Income Mortgages

Credit Risk of Low Income Mortgages Hamilton Fout, Grace Li, and Mark Palim Economic and Strategic Research, Fannie Mae 3900 Wisconsin Avenue NW, Washington DC 20016 May 2017 The authors thank Anthony

Credit Risk of Low Income Mortgages Hamilton Fout, Grace Li, and Mark Palim Economic and Strategic Research, Fannie Mae 3900 Wisconsin Avenue NW, Washington DC 20016 May 2017 The authors thank Anthony

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE. SUBJECT: Home Loan Program 2012 Mid-Year Report CONSENT: X ATTACHMENT(S): 1

: 1") TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

NC Mortgage Trends Matthew Martin, Ph.D. Regional Economist Federal Reserve Bank of Richmond

NC Mortgage Trends Matthew Martin, Ph.D. Regional Economist Federal Reserve Bank of Richmond The National Picture: 2007 Foreclosures Source: Realtytrac Confidential Information 2 The National Picture:

NC Mortgage Trends Matthew Martin, Ph.D. Regional Economist Federal Reserve Bank of Richmond The National Picture: 2007 Foreclosures Source: Realtytrac Confidential Information 2 The National Picture:

The Impact of Second Loans on Subprime Mortgage Defaults

The Impact of Second Loans on Subprime Mortgage Defaults by Michael D. Eriksen 1, James B. Kau 2, and Donald C. Keenan 3 Abstract An estimated 12.6% of primary mortgage loans were simultaneously originated

The Impact of Second Loans on Subprime Mortgage Defaults by Michael D. Eriksen 1, James B. Kau 2, and Donald C. Keenan 3 Abstract An estimated 12.6% of primary mortgage loans were simultaneously originated