The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market

|

|

|

- Lester Hall

- 5 years ago

- Views:

Transcription

1 The Effect of Mortgage Broker Licensing On Loan Origination Standards and Defaults: Evidence from U.S. Mortgage Market Lan Shi Yan (Jenny) Zhang Presentation Sept at FRB Cleveland Policy Summit The views in this paper are those of the authors and may not reflect those of the Office of the Comptroller of the Currency or the Department of Treasury. 1

2 Information asymmetry in the originate-to-distribute model The benefit of having secondary loan markets: Allows better risk-sharing by placing risk in hands of those most willing and able to bear it. Allows specialization: origination, servicing, etc. With better risk-sharing comes potentially worse incentives and adverse selection in the presence of information asymmetry Lenders have less incentives to collect soft information on borrowers (Keys et al., 2010). They exploit a discontinuity loans with FICO score greater than 620 are more likely to be selected for securitization, to illustrate the effect of securitization on loan origination quality. This paper: What are the roles of mortgage loan brokers in the originate-to-distribute financing model?

3 Relation Between Lenders and Brokers Lenders use their own employees and independent brokers to originate loans. The latter originate 68% of all residential loans in the U.S. leading up to the crisis (Wholesale Access Mortgage Research & Consulting, Inc.) Compared with lender employees, brokers are independent parties and have access to several lenders. have lower overhead costs. brokers were paid origination fee and a percentage of the loan amount. Lenders paid brokers based on the interest rate charged (Yield Spread Premium): the higher the interest rate, the greater the rebate (compensation) from lenders to brokers (Woodward & Hall, 2010).

4 Brokers Incentives The pay to brokers is not based on long-term performance of the loans originated. Rather, pay varies with Quantity and amount of loans closed. Interest rates of the loan. Given the compensation structure, brokers have incentives to generate fees by originating as many loans as possible. Expand the loan origination to subprime borrowers, those with impaired credit history. Borrowers often are not as sophiscated about mortgage terms as brokers. steer borrowers into loans with higher interest rates.

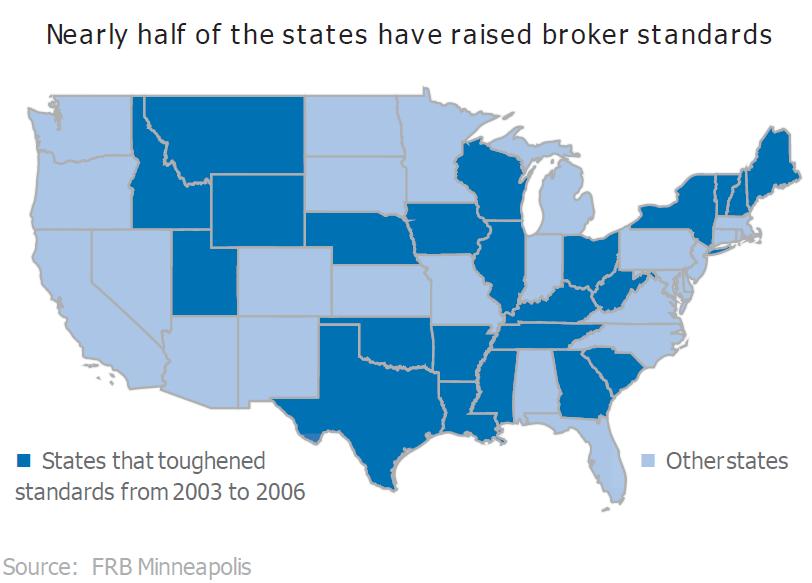

5 State Regulation of Brokers: Prior to 2008 Mortgage brokers are regulated by states. It takes the form of licensing and registration. Financial requirements (of the entity) Minimum net worth Surety bonds. Usually between $25,000 and $50,000. Some require the bond amount proportional to the number of mortgage applications, or number of loan originators, or the aggregate principal amount of loans. Registration/license requirement Specific competency requirements (for control persons/employees/both): Work Experience Education: degree or hours of classroom-training Continuing Education: Courses; classroom instructions. Exams on mortgage banking knowledge and federal and state laws and regulations. Having a physical office in the state 5

6 Hypothesis: Effect of Mortgage Broker Licensing on Loan Origination Quality Mechanism: licensing of brokers in the presence of info. asymmetry Selection effect: blocks entry of brokers who had criminal history. admits brokers who have higher ability, who value their reputation with borrowers more, and are less likely to exploit borrowers. Incentive effect: raises the cost of becoming a broker, which gives them incentives to not squander their investments by way of license revocation as a result of wrongdoings: surety bond, in particular. reduces the number of brokers and thus generates greater equilibrium profits, which raises the value of upholding reputation with borrowers (Kelley, 1990; Hellmann et al., 2000). Testable predictions: States with more stringent broker licensing requirements will have higher origination standards and better loan performance. Effect of licensing is greater when information asymmetry is greater.

7 Identification Strategies Focus on PLS loans originated during Large cross-state variation in licensing, yet it could be due to unobserved state heterogeneity that also affects the dependent variable. Strategy: within-state over-time variation in broker licensing. Effectively exploiting over time changes to identify the effect of licensing on loan origination standards. Rely on the assumption that states that change (changers) have similar over time trend than states that do not change (stayers), which we check. Also use propensity score method. 7

8

9

10 Data Data on licensing requirements: Pahl (2007) provides detailed coding of licensing requirements. Data on loan performance & terms: CoreLogic data on originated loans securitized by private label issuers (PLS) Include ABS (subprime and Alt-A), MBS (jumbo loans) Not portfolio loans nor GSE loans; will address possible selection issues. 10

11 Variable Definitions Dependent variables. whether the loan has risky features whether the originated loan is 60+ days delinquent, in foreclosure, or real estate owned (REO) 3 years after origination. Licensing variables. Bond/networth requirement: bond over $50,000=3; bond $25,000-$50,000=2; bond under $25,000=1; None=0. Registration/license (required=1; none=0). competency requirement is the specific requirement for licensing/registration (required=1; none=0). We group licensing requirements by types: specific req. for all parties -- the licensee (applicant; owner), managing directors, and employees. Also group across all parties for each specific requirement. Control variables: loan and borrower characteristics; HPI & unemployment change.

12 Summary Statistics on Performance Var. and License Variables

13

14 Summary Statistics on Loan Characteristics

15 Loan Characteristics as a Function of Broker Licensing The specification: X ist = β l lic ist + HPI_change st + α s + α t + ε ist

16 Econometric Specification for Loan Performance Regressions The specification: Y ist = β l lic ist + β X X ist + α s + α t + ε ist where -- i: loan, -- s: state, -- t: year, -- Y: 60+ days delinquent, in foreclosure, or real estate owned (REO) three years after origination. -- X: i) loan and borrower characteristics, ii) MSA quarterly HPI and state monthly unemployment change in the origination year over the last year. -- α s : state fixed effects, -- α t : year fixed effects. Standard errors are clustered at the zip-code level. 16

17

18

19

20 Economic Magnitude The significance of the licensing variables in a loan performance regression with loan characteristics included suggests that there are factors not captured by loan characteristics that are affected by broker licensing Their effort in screening the loan Some loan characteristics might be noisy: home appraisal value might be inflated (resulting in lower LTV than the true value), income might be inflated (resulting in lower DTI than the true value), etc. A one standard deviation in the following variables is associated with economically large reduction from the mean default rate: Networth/surety bond: 13 percent Experience: 11 percent Education: 11 percent Experience or education: 16 percent Exam: 19 percent Continuing education: 7 percent Licensee requirement: 39 percent Employee requirement: 26 percent. 20

21 Effect of Licensing Varies with Being Subprime or not 21

22 Effect of Licensing on Loan Performance by Documentation

23 Effect of Licensing on Loan Performance by Percent of Minority

24 Selection Issue?

25 State Anti-predatory Lending Laws (APL) With the exception of high-cost mortgages covered under Home Ownership and Equity Protection Act of 1994 (HOEPA), before the subprime crisis there were no federal statutes that expressly prohibit making a loan that a borrower will likely be unable to repay (GAO ). In response to the lack of protection of consumers in mortgage lending, many states adopted anti-predatory lending laws. In 1999, North Carolina passed the first comprehensive state law that was modeled after the federal HOEPA (mini-hoepa law). Prompted by growing concerns over the explosion in subprime lending, many other states also enacted anti-predatory lending laws. As of 2007, 29 states and the District of Columbia had mini-hoepa laws in effect and another 14 states had some types of older anti-predatory lending laws that were still in effect which were adopted prior to 2000 APLs restricted prepayment penalties, balloon payments, or negative amortization for all mortgages (Bostic et al., 2008a). Federal pre-emption of APLs. OTS: since 1996 OCC: since 2004

26 Alternative Explanation I: Effect of APL? 26

27 Further Analyses and discussion Sensitivity analyses: Robust to inclusion of originator FE Robust to inclusion of servicer FE Robust to use of lagged license variables Robust to use of 2-yr default after origination Robust to inclusion of fingerprint as a way of broker licensing The risky features were not priced in the interest rate. The effect of licensing is also stronger for ARM, IO, Negam, and loans with investment purpose. Standard economic theory predict that restriction on entry reduces efficiency But this is only true in an environment with full information. There are empirical work documenting that occupational license increases price (Kleiner, 2000) There is also literature showing that deregulation leads to excessive risktaking by banks (Keeley, 1990), entry of a third credit-rating agency reduces rating quality (Becker and Milbourn, 2011).

28 Conclusion We argue that in the originate-to-distribute model, the broker licensing raises loan underwriting standards because it raises the quality of mortgage brokers, who value their reputation more, raises the stake of being a licensed broker, reduces the number of brokers who feed the lending frenzy. We find evidence that in the originate-and-distribute mortgage financing model, states that toughened mortgage brokers licensing requirements had a lower proportion of loans with risky features and thus had better loan performance. The magnitude is percent reduction from the mean for a one sd increase in various licensing requirements. The effect is larger where information asymmetry and the role of broker is larger. Recent federal regulatory moves (SAFE Act, Dodd-Frank Act on abilityto-repay, risk retention, and broker pay ) are attempts to raise efficiency in mortgage origination and securitization market.

Sponsor-Underwriter Affiliation and Performance in Non-Agency Mortgage-Backed Securities

Sponsor-Underwriter Affiliation and Performance in Non-Agency Mortgage-Backed Securities Peng (Peter) Liu 1 Lan Shi 2 1 Cornell University 2 Office of the Comptroller of the Currency Weimer School of Advanced

Sponsor-Underwriter Affiliation and Performance in Non-Agency Mortgage-Backed Securities Peng (Peter) Liu 1 Lan Shi 2 1 Cornell University 2 Office of the Comptroller of the Currency Weimer School of Advanced

Credit-Induced Boom and Bust

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom?

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT KENNETH BENTON SENIOR CONSUMER REGULATIONS SPECIALIST FEDERAL RESERVE BANK OF PHILADELPHIA MAY 10, 2012 Disclaimer: the

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT KENNETH BENTON SENIOR CONSUMER REGULATIONS SPECIALIST FEDERAL RESERVE BANK OF PHILADELPHIA MAY 10, 2012 Disclaimer: the

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments. Morgan J. Rose. March 2011

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

Supplementary Results for Geographic Variation in Subprime Loan Features, Foreclosures and Prepayments Morgan J. Rose Office of the Comptroller of the Currency 250 E Street, SW Washington, DC 20219 University

Mortgage Reform Under the Dodd-Frank Act

Mortgage Reform Under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist September 20, 2013 FEDERAL RESERVE BANK OF PHILADELPHIA DISCLAIMER: The views expressed are the presenters

Mortgage Reform Under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist September 20, 2013 FEDERAL RESERVE BANK OF PHILADELPHIA DISCLAIMER: The views expressed are the presenters

Loan Product Steering in Mortgage Markets

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Risky Borrowers or Risky Mortgages?

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Overview of Mortgage Lending

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

CREDIT RISK MANAGEMENT GUIDANCE FOR HOME EQUITY LENDING

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market. Online Appendix

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

Are Lemon s Sold First? Dynamic Signaling in the Mortgage Market Online Appendix Manuel Adelino, Kristopher Gerardi and Barney Hartman-Glaser This appendix supplements the empirical analysis and provides

Loan Originator Compensation and Steering Prohibitions. Branch Originations March 2011

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

Any person, who for direct or indirect compensation, assists a consumer in obtaining or applying to obtain a residential mortgage loan; or

Mortgage Reform and Anti-Predatory Lending Act Although it has received far less attention than other titles of the Dodd-Frank Act (the Act or Dodd-Frank ), such as those addressing derivatives, too big

Mortgage Reform and Anti-Predatory Lending Act Although it has received far less attention than other titles of the Dodd-Frank Act (the Act or Dodd-Frank ), such as those addressing derivatives, too big

MORTGAGE REFORM AND ANTI-PREDATORY LENDING ACT of 2009

MORTGAGE REFORM AND ANTI-PREDATORY LENDING ACT of 2009 (As Passed by House of Representatives) Laurence E. Platt 202.778.9034 larry.platt@klgates.com K&L Gates 1601 K St., NW Washington, DC 20006 fax:

MORTGAGE REFORM AND ANTI-PREDATORY LENDING ACT of 2009 (As Passed by House of Representatives) Laurence E. Platt 202.778.9034 larry.platt@klgates.com K&L Gates 1601 K St., NW Washington, DC 20006 fax:

Consumer Regulatory Changes

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj The Vanguard Group Rajdeep Sengupta Federal Reserve Bank of St. Louis ECB CFS Research Conference Einaudi

Where s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages Geetesh Bhardwaj The Vanguard Group Rajdeep Sengupta Federal Reserve Bank of St. Louis ECB CFS Research Conference Einaudi

Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act. August 6, 2010

Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act August 6, 2010 BACKGROUND This summary describes key points in the Dodd-Frank Wall Street Reform

Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act August 6, 2010 BACKGROUND This summary describes key points in the Dodd-Frank Wall Street Reform

Credit-Induced Boom and Bust

Credit-Induced Boom and Bust Marco Di Maggio Columbia Business School mdimaggio@columbia.edu Amir Kermani University of California - Berkeley amir@haas.berkeley.edu First Draft Abstract Can an increase

Credit-Induced Boom and Bust Marco Di Maggio Columbia Business School mdimaggio@columbia.edu Amir Kermani University of California - Berkeley amir@haas.berkeley.edu First Draft Abstract Can an increase

The Untold Costs of Subprime Lending: Communities of Color in California. Carolina Reid. Federal Reserve Bank of San Francisco.

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

Second Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173) July 13, 2010

July 13, 2010") Second Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173) July 13, 2010 As signed by the Conference of the House and Senate on June 29,

Second Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173) July 13, 2010 As signed by the Conference of the House and Senate on June 29,

Announcement March 5, Updates and Clarifications for Streamlined Refinance Products

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013 JOSHUA WHITE AND SCOTT BAUGUESS 2 Division of Economic and Risk Analysis (DERA) U.S. Securities and Exchange

Qualified Residential Mortgage: Background Data Analysis on Credit Risk Retention 1 AUGUST 2013 JOSHUA WHITE AND SCOTT BAUGUESS 2 Division of Economic and Risk Analysis (DERA) U.S. Securities and Exchange

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

Complex Mortgages. May 2014

Complex Mortgages Gene Amromin, Federal Reserve Bank of Chicago Jennifer Huang, Cheung Kong Graduate School of Business Clemens Sialm, University of Texas-Austin and NBER Edward Zhong, University of Wisconsin

Complex Mortgages Gene Amromin, Federal Reserve Bank of Chicago Jennifer Huang, Cheung Kong Graduate School of Business Clemens Sialm, University of Texas-Austin and NBER Edward Zhong, University of Wisconsin

New Lending Opportunities in the Changed Mortgage Market: Dodd-Frank Act Mortgage Regulations

New Lending Opportunities in the Changed Mortgage Market: Dodd-Frank Act Mortgage Regulations Kenneth Benton Senior Consumer Regulations Specialist May 14, 2014 FEDERAL RESERVE BANK OF PHILADELPHIA Disclaimer:

New Lending Opportunities in the Changed Mortgage Market: Dodd-Frank Act Mortgage Regulations Kenneth Benton Senior Consumer Regulations Specialist May 14, 2014 FEDERAL RESERVE BANK OF PHILADELPHIA Disclaimer:

Deregulation, Competition and the Race to the Bottom

Deregulation, Competition and the Race to the Bottom Marco Di Maggio Amir Kermani Sanket Korgaonkar February 28, 2015 The latest version can be found here. Abstract We take advantage of the pre-emption

Deregulation, Competition and the Race to the Bottom Marco Di Maggio Amir Kermani Sanket Korgaonkar February 28, 2015 The latest version can be found here. Abstract We take advantage of the pre-emption

New Construction and Mortgage Default

New Construction and Mortgage Default ASSA/AREUEA Conference January 6 th, 2019 Tom Mayock UNC Charlotte Office of the Comptroller of the Currency tmayock@uncc.edu Konstantinos Tzioumis ALBA Business School

New Construction and Mortgage Default ASSA/AREUEA Conference January 6 th, 2019 Tom Mayock UNC Charlotte Office of the Comptroller of the Currency tmayock@uncc.edu Konstantinos Tzioumis ALBA Business School

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL33930 Subprime Mortgages: Primer on Current Lending and Foreclosure Issues Edward Vincent Murphy, Government and Finance

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL33930 Subprime Mortgages: Primer on Current Lending and Foreclosure Issues Edward Vincent Murphy, Government and Finance

NMLS Mortgage Call Report Field Definitions & Instructions

NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q1 2020 Reporting This document provides field definitions, instructions and data formatting requirements for completing the NMLS

NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q1 2020 Reporting This document provides field definitions, instructions and data formatting requirements for completing the NMLS

Information Asymmetry in Private-Label Mortgage Securitization: Evidence from Allocations to Aliated Funds.

Information Asymmetry in Private-Label Mortgage Securitization: Evidence from Allocations to Aliated Funds. Brent W. Ambrose 1 Moussa Diop 2 Walter D'Lima 3 Mark Thibodeau 1 1 The Pennsylvania State University

Information Asymmetry in Private-Label Mortgage Securitization: Evidence from Allocations to Aliated Funds. Brent W. Ambrose 1 Moussa Diop 2 Walter D'Lima 3 Mark Thibodeau 1 1 The Pennsylvania State University

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices?

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

Qualified Mortgages and Qualified Residential Mortgages under the Dodd-Frank Act

Qualified Mortgages and Qualified Residential Mortgages under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist Greg Bell Banking Supervisor Consumer Compliance Risk Team FEDERAL

Qualified Mortgages and Qualified Residential Mortgages under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist Greg Bell Banking Supervisor Consumer Compliance Risk Team FEDERAL

Fed Loan Originator Compensation Changes

Fed Loan Originator Compensation Changes Federal Reserve System 12 CFR Part 226 Regulation Z; Docket No. R-1366 Truth in Lending Agency: Board of Governors of the Federal Reserve System. Action: Final

Fed Loan Originator Compensation Changes Federal Reserve System 12 CFR Part 226 Regulation Z; Docket No. R-1366 Truth in Lending Agency: Board of Governors of the Federal Reserve System. Action: Final

MBS ratings and the mortgage credit boom

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

Lessons to Learn from CRA Lending

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

1. Modification algorithm

Internet Appendix for: "The Effect of Mortgage Securitization on Foreclosure and Modification" 1. Modification algorithm The LPS data set lacks an explicit modification flag but contains enough detailed

Internet Appendix for: "The Effect of Mortgage Securitization on Foreclosure and Modification" 1. Modification algorithm The LPS data set lacks an explicit modification flag but contains enough detailed

Things My Mortgage Broker Never Told Me: Escrow, Property Taxes, and Mortgage Delinquency

Things My Mortgage Broker Never Told Me: Escrow, Property Taxes, and Mortgage Delinquency Nathan B. Anderson UIC & Institute of Govt and Public Affairs Jane K. Dokko Federal Reserve Board May 2009 Two

Things My Mortgage Broker Never Told Me: Escrow, Property Taxes, and Mortgage Delinquency Nathan B. Anderson UIC & Institute of Govt and Public Affairs Jane K. Dokko Federal Reserve Board May 2009 Two

7th Session: International trends in the regulation of mortgage markets. Masahiro Kobayashi

IUHF 30th World Congress June 27, 2017 7th Session: International trends in the regulation of mortgage markets Masahiro Kobayashi Director General, Research and Survey Department, and Director General,

IUHF 30th World Congress June 27, 2017 7th Session: International trends in the regulation of mortgage markets Masahiro Kobayashi Director General, Research and Survey Department, and Director General,

New Developments in Housing Policy

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

New Developments in Housing Policy Andrew Haughwout Research FRBNY The views and opinions presented here are those of the authors, and do not necessarily reflect those of the Federal Reserve Bank of New

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

State of North Carolina

Beverly E. Perdue Governor State of North Carolina Office of the Commissioner of Banks Joseph A. Smith, Jr. Commissioner of Banks DELIVERED VIA CERTIFIED MAIL ELECTRONIC MAIL Contact Name Company Name

Beverly E. Perdue Governor State of North Carolina Office of the Commissioner of Banks Joseph A. Smith, Jr. Commissioner of Banks DELIVERED VIA CERTIFIED MAIL ELECTRONIC MAIL Contact Name Company Name

Credit Access and Consumer Protection: Searching for the Right Balance

Credit Access and Consumer Protection: Searching for the Right Balance North Carolina Banking Institute March 26, 2013 Charlotte, NC Michael D. Calhoun Impact On Consumer Finances Already New Rapidly Appreciating

Credit Access and Consumer Protection: Searching for the Right Balance North Carolina Banking Institute March 26, 2013 Charlotte, NC Michael D. Calhoun Impact On Consumer Finances Already New Rapidly Appreciating

Expanded NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q Reporting

Expanded NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q1 2016 Reporting This document provides field definitions, instructions and data formatting requirements for completing

Expanded NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q1 2016 Reporting This document provides field definitions, instructions and data formatting requirements for completing

Fannie Mae Updates Compliance with Laws and Responsible Lending

June 24, 2014 Fannie Mae Updates Compliance with Laws and Responsible Lending By Anna DeSimone June 24, 2014, Fannie Mae published Ann. SEL-2014-07: Selling Guide Updates. The Selling Guide has been updated

June 24, 2014 Fannie Mae Updates Compliance with Laws and Responsible Lending By Anna DeSimone June 24, 2014, Fannie Mae published Ann. SEL-2014-07: Selling Guide Updates. The Selling Guide has been updated

A Look Behind the Numbers: FHA Lending in Ohio

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

First Quarter 2017 Earnings Call MAY 4, 2017

First Quarter 2017 Earnings Call MAY 4, 2017 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

First Quarter 2017 Earnings Call MAY 4, 2017 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

The Federal Reserve s HOEPA Proposal and Subprime Related Legislation by. Locke Lord Bissell & Liddell LLP Barnett Sivon & Natter P.C.

The Federal Reserve s HOEPA Proposal and Subprime Related Legislation by Charlotte M. Bahin Raymond Natter Locke Lord Bissell & Liddell LLP Barnett Sivon & Natter P.C. After receiving significant pressure

The Federal Reserve s HOEPA Proposal and Subprime Related Legislation by Charlotte M. Bahin Raymond Natter Locke Lord Bissell & Liddell LLP Barnett Sivon & Natter P.C. After receiving significant pressure

NC Mortgage Trends Matthew Martin, Ph.D. Regional Economist Federal Reserve Bank of Richmond

NC Mortgage Trends Matthew Martin, Ph.D. Regional Economist Federal Reserve Bank of Richmond The National Picture: 2007 Foreclosures Source: Realtytrac Confidential Information 2 The National Picture:

NC Mortgage Trends Matthew Martin, Ph.D. Regional Economist Federal Reserve Bank of Richmond The National Picture: 2007 Foreclosures Source: Realtytrac Confidential Information 2 The National Picture:

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Title 5: Banking and Consumer Finance. Part 2: Mortgage Company Activities. Part 2 Chapter 1: Mississippi S.A.F.E. Mortgage Act. Rule 1.1 Purpose.

Title 5: Banking and Consumer Finance Part 2: Mortgage Company Activities Part 2 Chapter 1: Mississippi S.A.F.E. Mortgage Act Rule 1.1 Purpose. This regulation was adopted as an amendment to the Regulations

Title 5: Banking and Consumer Finance Part 2: Mortgage Company Activities Part 2 Chapter 1: Mississippi S.A.F.E. Mortgage Act Rule 1.1 Purpose. This regulation was adopted as an amendment to the Regulations

Mortgage Loan Originator SAFE TN Comprehensive Course Mortgage Loan Originator Prelicensing / National Topics 20-Hour Course Syllabus

Mortgage Loan Originator SAFE TN Comprehensive Course Mortgage Loan Originator Prelicensing / National 20-Hour Course Syllabus Course Provider School Name: Tennessee Association of Mortgage Professionals

Mortgage Loan Originator SAFE TN Comprehensive Course Mortgage Loan Originator Prelicensing / National 20-Hour Course Syllabus Course Provider School Name: Tennessee Association of Mortgage Professionals

CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number ) August 2, 2010

August 2, 2010") CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number 111-203) August 2, 2010 Here is a short summary highlighting the provisions of the Dodd-Frank

CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number 111-203) August 2, 2010 Here is a short summary highlighting the provisions of the Dodd-Frank

Dodd-Frank Implementation Checklist

Dodd-Frank Implementation Checklist Project Initiation Determine the nature and scope of the project 1. Determine who will be responsible for implementing Dodd-Frank Act compliance requirements, and how

Dodd-Frank Implementation Checklist Project Initiation Determine the nature and scope of the project 1. Determine who will be responsible for implementing Dodd-Frank Act compliance requirements, and how

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Non-QM. Qualified Mortgages General QMs. GSE QMs. Agency QMs. Points & Fees 5%

Subprime 2006 No down payment required (80/20) or 100% LTV Average 580 credit score Income stated No reserves Negative Amortization and balloon payments No appraisal requirements Prepayment penalties Exceptions

Subprime 2006 No down payment required (80/20) or 100% LTV Average 580 credit score Income stated No reserves Negative Amortization and balloon payments No appraisal requirements Prepayment penalties Exceptions

Memorandum. Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Mortgage Modeling: Topics in Robustness. Robert Reeves September 2012 Bank of America

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

Mortgage Modeling: Topics in Robustness Robert Reeves September 2012 Bank of America Evaluating Model Robustness Essentially, all models are wrong, but some are useful. - George Box Assessing model robustness:

Subprime Loan Performance

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao October 2, 2014 Abstract Regulation AB (Reg AB) enacted in 2006 mandates

Disclosure Regulation on Mortgage Securitization and Subprime Loan Performance Lantian Liang Harold H. Zhang Feng Zhao Xiaofei Zhao October 2, 2014 Abstract Regulation AB (Reg AB) enacted in 2006 mandates

Strategic Default, Loan Modification and Foreclosure

Strategic Default, Loan Modification and Foreclosure Ben Klopack and Nicola Pierri January 17, 2017 Abstract We study borrower strategic default in the residential mortgage market. We exploit a discontinuity

Strategic Default, Loan Modification and Foreclosure Ben Klopack and Nicola Pierri January 17, 2017 Abstract We study borrower strategic default in the residential mortgage market. We exploit a discontinuity

Residential Mortgage Credit Model

Residential Mortgage Credit Model June 2016 data made beautiful Four Major Components to the Credit Model 1. Transition Model: An idealized roll-rate model with three states: i. Performing (Current, 30-DPD)

Residential Mortgage Credit Model June 2016 data made beautiful Four Major Components to the Credit Model 1. Transition Model: An idealized roll-rate model with three states: i. Performing (Current, 30-DPD)

APPENDIX A: GLOSSARY

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

Paul Gompers EMCF 2009 March 5, 2009

Paul Gompers EMCF 2009 March 5, 2009 Examine two papers that use interesting cross sectional variation to identify their tests. Find a discontinuity in the data. In how much you have to fund your pension

Paul Gompers EMCF 2009 March 5, 2009 Examine two papers that use interesting cross sectional variation to identify their tests. Find a discontinuity in the data. In how much you have to fund your pension

The New World of Mortgage Regulation A Look Back - A Look Around and a Look Forward. Barry D. Johnson Shareholder SettlePou

The New World of Mortgage Regulation A Look Back - A Look Around and a Look Forward By Barry D. Johnson Shareholder SettlePou 3333 Lee Parkway, 8 th Floor Dallas, Texas 75219 (214) 520-3300 bjohnson@settlepou.com

The New World of Mortgage Regulation A Look Back - A Look Around and a Look Forward By Barry D. Johnson Shareholder SettlePou 3333 Lee Parkway, 8 th Floor Dallas, Texas 75219 (214) 520-3300 bjohnson@settlepou.com

Foreclosure Delay and Consumer Credit Performance

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

Housing Finance Policy Center Lunchtime Data Talk Mortgage Modifications Using Principal Reduction: How Effective Are They?

Housing Finance Policy Center Lunchtime Data Talk Mortgage Modifications Using Principal Reduction: How Effective Are They? Ben Keys, University of Chicago Tess Scharlesmann, Office of Financial Research,

Housing Finance Policy Center Lunchtime Data Talk Mortgage Modifications Using Principal Reduction: How Effective Are They? Ben Keys, University of Chicago Tess Scharlesmann, Office of Financial Research,

Request For Comment: Methodology And Assumptions For Rating U.S. RMBS Issued 2009 And Later

Criteria Structured Finance Request for Comment: Request For Comment: Methodology And Assumptions For Rating U.S. RMBS Issued 2009 And Later Analytical Contacts: Farooq Omer, CFA, New York (1) 212-438-1129;

Criteria Structured Finance Request for Comment: Request For Comment: Methodology And Assumptions For Rating U.S. RMBS Issued 2009 And Later Analytical Contacts: Farooq Omer, CFA, New York (1) 212-438-1129;

Consumer Financial Protection Bureau. March 15, Draft, Sensitive and Pre-Decisional Not for External Distribution

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Bank of America Merrill Lynch Leveraged Finance Conference. November 29, 2016 NYSE: RDN

Bank of America Merrill Lynch Leveraged Finance Conference November 29, 2016 NYSE: RDN www.radian.biz 1 AGENDA Post Crisis U.S. Housing Market What is Private Mortgage Insurance? Strong Business Fundamentals

Bank of America Merrill Lynch Leveraged Finance Conference November 29, 2016 NYSE: RDN www.radian.biz 1 AGENDA Post Crisis U.S. Housing Market What is Private Mortgage Insurance? Strong Business Fundamentals

Predatory Lending Laws and the Cost of Credit

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2008 Predatory Lending Laws and the Cost of Credit Anthony Pennington-Cross Marquette

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2008 Predatory Lending Laws and the Cost of Credit Anthony Pennington-Cross Marquette

Lending and Collateral Q&A

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

Mortgage Bankers and Brokers Association of New Hampshire

Mortgage Bankers and Brokers Association of New Hampshire March 24, 2014 Ken Markison, MBA Regulatory Counsel Presented by David H. Stevens President, Mortgage Bankers Association Introduction Seven weeks

Mortgage Bankers and Brokers Association of New Hampshire March 24, 2014 Ken Markison, MBA Regulatory Counsel Presented by David H. Stevens President, Mortgage Bankers Association Introduction Seven weeks

Home Affordable Refinance (DU Refi Plus and Refi Plus) FAQs

FAQs") Home Affordable Refinance (DU Refi Plus and Refi Plus) FAQs February 3, 2015 The Home Affordable Refinance Program (HARP) is designed to assist homeowners in refinancing their mortgages even if they owe

Home Affordable Refinance (DU Refi Plus and Refi Plus) FAQs February 3, 2015 The Home Affordable Refinance Program (HARP) is designed to assist homeowners in refinancing their mortgages even if they owe

by Sankar De and Manpreet Singh

Comments on: Credit Rationing in Informal Markets: The case of small firms in India by Sankar De and Manpreet Singh Discussant: Johanna Francis (Fordham University and UCSC) CAFIN Workshop 25-26 April

Comments on: Credit Rationing in Informal Markets: The case of small firms in India by Sankar De and Manpreet Singh Discussant: Johanna Francis (Fordham University and UCSC) CAFIN Workshop 25-26 April

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Regulation AB II September 19, 2014 Presented By: Kenneth E. Kohler Jerry R. Marlatt

Regulation AB II September 19, 2014 Presented By: Kenneth E. Kohler Jerry R. Marlatt 2014 Morrison & Foerster LLP All Rights Reserved mofo.com Regulation AB II On August 27, 2014, the SEC adopted changes

Regulation AB II September 19, 2014 Presented By: Kenneth E. Kohler Jerry R. Marlatt 2014 Morrison & Foerster LLP All Rights Reserved mofo.com Regulation AB II On August 27, 2014, the SEC adopted changes

Risk and Performance of Mutual Funds Securitized Mortgage Investments

Risk and Performance of Mutual Funds Securitized Mortgage Investments Brent W. Ambrose Moussa Diop Walter D Lima Mark Thibodeau October 30, 2018 Abstract We expand the debate on incentives embedded in

Risk and Performance of Mutual Funds Securitized Mortgage Investments Brent W. Ambrose Moussa Diop Walter D Lima Mark Thibodeau October 30, 2018 Abstract We expand the debate on incentives embedded in

TILA Mortgage Coverage Categories Closed-End Mortgages Secured by Dwelling (DF)

") New Mortgage Rules NCLC Summer Mortgage Conference 2012 Alys Cohen with Peter Carroll, CFPB July 18, 2012 Washington, D.C. TILA Mortgage Coverage Categories Closed-End Mortgages Secured by Dwelling (DF)

New Mortgage Rules NCLC Summer Mortgage Conference 2012 Alys Cohen with Peter Carroll, CFPB July 18, 2012 Washington, D.C. TILA Mortgage Coverage Categories Closed-End Mortgages Secured by Dwelling (DF)

6/18/2015. Residential Mortgage Types and Borrower Decisions. Role of the secondary market Mortgage types:

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Subprime Mortgage Defaults and Credit Default Swaps

THE JOURNAL OF FINANCE VOL. LXX, NO. 2 APRIL 2015 Subprime Mortgage Defaults and Credit Default Swaps ERIC ARENTSEN, DAVID C. MAUER, BRIAN ROSENLUND, HAROLD H. ZHANG, and FENG ZHAO ABSTRACT We offer the

THE JOURNAL OF FINANCE VOL. LXX, NO. 2 APRIL 2015 Subprime Mortgage Defaults and Credit Default Swaps ERIC ARENTSEN, DAVID C. MAUER, BRIAN ROSENLUND, HAROLD H. ZHANG, and FENG ZHAO ABSTRACT We offer the

A Fistful of Dollars: Lobbying and the Financial Crisis

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

A Fistful of Dollars: Lobbying and the Financial Crisis by Deniz Igan, Prachi Mishra, and Thierry Tressel Research Department, IMF The views expressed in this paper are those of the authors and do not

Dodd-Frank Wall Street Reform and Consumer Protection Act: Key Issues for Savings Associations

1 Dodd-Frank Wall Street Reform and Consumer Protection Act: Key Issues for Savings Associations Financial Institutions Team Kilpatrick Stockton LLP July 27, 2010 Joseph P. Daly Christina M. Gattuso Aaron

1 Dodd-Frank Wall Street Reform and Consumer Protection Act: Key Issues for Savings Associations Financial Institutions Team Kilpatrick Stockton LLP July 27, 2010 Joseph P. Daly Christina M. Gattuso Aaron

Conforming limits - Purchase - Rate and Term Refinances (Loans must have been purchase money A quality mortgage at origination)

") DREAM MAKER FIXED RATE LOW INCOME / LOW FICO WHOLESALE PRODUCT GUIDELINES PRODUCT CODES: C30XO C20XO C15XO C10XO Several states and local municipalities have enacted legislation which define High Cost

DREAM MAKER FIXED RATE LOW INCOME / LOW FICO WHOLESALE PRODUCT GUIDELINES PRODUCT CODES: C30XO C20XO C15XO C10XO Several states and local municipalities have enacted legislation which define High Cost

The Influence of Foreclosure Delays on Borrower s Default Behavior

The Influence of Foreclosure Delays on Borrower s Default Behavior Shuang Zhu Department of Finance E.J. Ourso College of Business Administration Louisiana State University Baton Rouge, LA 70803-6308 OFF:

The Influence of Foreclosure Delays on Borrower s Default Behavior Shuang Zhu Department of Finance E.J. Ourso College of Business Administration Louisiana State University Baton Rouge, LA 70803-6308 OFF:

Mortgage Rates, Household Balance Sheets, and Real Economy

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Ability-to-Repay and Qualified Mortgage Rule (ATR/QM Rule)- Effective 1/10/14

- Effective 1/10/14") Ability-to-Repay and Qualified Mortgage Rule (ATR/QM Rule)- Effective 1/10/14 1) Dodd Frank requires that lenders make a reasonable, good-faith determination that the loan applicant has a reasonable ability

Ability-to-Repay and Qualified Mortgage Rule (ATR/QM Rule)- Effective 1/10/14 1) Dodd Frank requires that lenders make a reasonable, good-faith determination that the loan applicant has a reasonable ability

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-K. For the transition period from to.

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

Fannie Mae Reports Net Income of $4.6 Billion and Comprehensive Income of $4.4 Billion for Second Quarter 2015

Resource Center: 1-800-732-6643 Contact: Date: Pete Bakel 202-752-2034 August 6, 2015 Fannie Mae Reports Net Income of 4.6 Billion and Comprehensive Income of 4.4 Billion for Second Quarter 2015 Fannie

Resource Center: 1-800-732-6643 Contact: Date: Pete Bakel 202-752-2034 August 6, 2015 Fannie Mae Reports Net Income of 4.6 Billion and Comprehensive Income of 4.4 Billion for Second Quarter 2015 Fannie

Expanded NMLS Mortgage Call Report Field Definitions & Instructions

Expanded NMLS Mortgage Call Report Field Definitions & Instructions This document provides field definitions, instructions and data formatting requirements for completing the Expanded NMLS Mortgage Call

Expanded NMLS Mortgage Call Report Field Definitions & Instructions This document provides field definitions, instructions and data formatting requirements for completing the Expanded NMLS Mortgage Call

Fannie Mae 2010 First Quarter Credit Supplement. May 10, 2010

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Board of Governors of the Federal Reserve System; Truth in Lending

Board of Governors of the Federal Reserve System; Truth in Lending ABA Contact: Bob Davis (202) 663-5588 rdavis@aba.com Joe Pigg (202) 663-5480 jpigg@aba.com Rod Alba (202) 663-5592 ralba@aba.com Krista

Board of Governors of the Federal Reserve System; Truth in Lending ABA Contact: Bob Davis (202) 663-5588 rdavis@aba.com Joe Pigg (202) 663-5480 jpigg@aba.com Rod Alba (202) 663-5592 ralba@aba.com Krista

THIS IS NOT LEGAL ADVICE

I. Ability to Repay (ATR) Qualified Mortgage (QM) Overview In 2008 the Board of Governors of the Federal Reserve System adopted a rule under the Truth in Lending Act prohibiting creditors from making higher-priced

I. Ability to Repay (ATR) Qualified Mortgage (QM) Overview In 2008 the Board of Governors of the Federal Reserve System adopted a rule under the Truth in Lending Act prohibiting creditors from making higher-priced

BANKING REPORT! D espite wide agreement among members of Congress. A BNA s. Three Approaches for FHA Refinancing of Subprime Mortgages.

A BNA s BANKING REPORT! Housing Three Approaches for FHA Refinancing of Subprime Mortgages The attached chart, prepared by attorney Raymond Natter, compares the House, Senate, and Bush administration s

A BNA s BANKING REPORT! Housing Three Approaches for FHA Refinancing of Subprime Mortgages The attached chart, prepared by attorney Raymond Natter, compares the House, Senate, and Bush administration s

Housing Finance in the Aftermath of the Crisis

Housing Finance in the Aftermath of the Crisis Dr. Michael Lea San Diego State University Presentation to the Homer Hoyt Institute May 16-17, 2014 Outline of Presentation Causes of the US Mortgage Market

Housing Finance in the Aftermath of the Crisis Dr. Michael Lea San Diego State University Presentation to the Homer Hoyt Institute May 16-17, 2014 Outline of Presentation Causes of the US Mortgage Market

Regulation of Subprime and Predatory Lending (forthcoming)

") Brooklyn Law School BrooklynWorks Faculty Scholarship 1-2010 (forthcoming) David Reiss Follow this and additional works at: http://brooklynworks.brooklaw.edu/faculty Part of the Law Commons Recommended

Brooklyn Law School BrooklynWorks Faculty Scholarship 1-2010 (forthcoming) David Reiss Follow this and additional works at: http://brooklynworks.brooklaw.edu/faculty Part of the Law Commons Recommended

What is the micro-elasticity of mortgage demand to interest rates?

What is the micro-elasticity of mortgage demand to interest rates? Stephanie Lo 1 December 2, 2016 1 Part of this work has been performed at the Federal Reserve Bank of Boston. The views expressed in this

What is the micro-elasticity of mortgage demand to interest rates? Stephanie Lo 1 December 2, 2016 1 Part of this work has been performed at the Federal Reserve Bank of Boston. The views expressed in this