Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

|

|

|

- Logan Marsh

- 5 years ago

- Views:

Transcription

1 Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

2 A short history of capitalism Capitalism is wonderful human invention steering individual initiative and creativity towards capital accumulation and ever more material progress It is also inherently unstable, however. Periods of optimism and pessimism alternate, creating booms and busts in economic activity. The booms are wonderful; the busts create great hardship for many people.

3 Booms and busts are endemic in capitalism Many economic decisions are forward looking. Investors and consumers look into the future to decide to invest or to consume. But the future is dark. Nobody knows it. As a result, when making forecasts, consumers and investors look at each other. This makes it possible for optimism of one individual to be transmitted to others creating a self-fulfilling movement in optimism.

4 Animal spirits and self-fulfilling dynamics Optimism induces consumers to consume more and investors to invest more, thereby validating their optimism. The reverse is also true. When pessimism sets in, the same contagion mechanism leads to a self-fulfilling decline in economic activity. Animal spirits prevail.

5 Role of banking sector During euphoria and booms households and firms cheerfully take on debt to profit from perceived high rates of return Banks jump on this and provide credit Excessive debt accumulation made possible by excessive bank credit Until crash Deleveraging becomes necessary both by banks and non-banks Deep recession

6 Stabilizing an unstable system The involvement of financial institutions in booms and bust dynamics makes capitalism particularly unstable Since Great Depression we have learned to bring in some stabilizers that have softened the instability Two stabilizers: Central Bank as a Lender of Last Resort Government budget as an automatic shock absorber

7 Lender of Last Resort Central Banks were originally created to deal with inherent instability of capitalism Were given double task: Lender of last resort for banks: backstop to counter panic and run on banks Lender of last resort of governments: to counter run in government bond markets Why this double task?

8 Deadly embrace Banks and governments face same problem: unbalanced maturity structure of assets and liabilities Making both banks and governments vulnerable for movements of distrust Which will lead to liquidity crisis And can degenerate into solvency crisis I will develop this point further Banks and governments hold each other in deadly embrace: When banks collapse sovereign is in trouble When government collapses banks are in trouble

9 Government budget as shock absorber The need to have government budget is shock absorber is based on Keynes savings paradox paradox When after crash private sector has to reduce debt it does two things It tries to save more It sells assets Private sector can only save more if government sector borrows more (i.e. higher budget deficit) If government also tries to save more, attempts to save more by private sector are self-defeating and economy is pulled into deflationary spiral

10 Stabilizers are organized at national levels These stabilizing features relatively well organized at the level of countries (US, UK, France, Germany) Not at international level nor at the level of a monetary union like the Eurozone These design failures were only recognized after the financial crisis. And even then in many countries, especially in Northern Europe still not recognized because of dramatic diagnostic failure, focusing on government profligacy

11 Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts continued to work at national level and monetary union in no way disciplined these into a union-wide dynamics. On the contrary the monetary union probably exacerbated these national booms and busts. 2. Stabilizers that existed at national level were stripped away from the member-states without being transposed at the monetary union level. This left the member states naked and fragile, unable to deal with the coming disturbances. 3. Let me expand on these two points.

12 Design failure I Booms and bust dynamics: national In Eurozone money is fully centralized All the rest of macroeconomic policies is organized at national level Thus booms and busts are not constrained by the fact that a monetary union exists. As a result, these booms and busts originate at the national level, not at the Eurozone level, and can have a life of their own for quite some time. At some point though when the boom turns into a bust, the implications for the rest of the union become acute

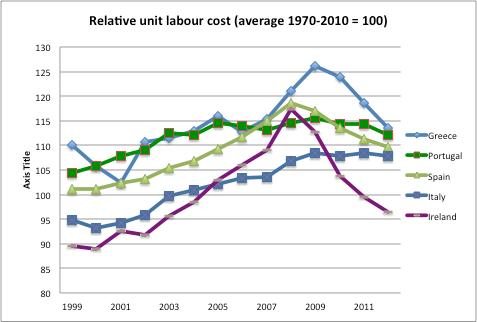

13 Monetary union can exacerbate national booms and busts In fact the existence of the monetary union can exacerbate booms and busts at the national level. This has to do with the existence of only one policy interest rate when underlying macroeconomic conditions are very different. The fact that only one interest rate exists for the union exacerbates these differences, i.e. it leads to a stronger boom in the booming countries and a stronger recession in the recession countries than if there had been no monetary union.

ECB, Monthly Bulletin, Nov.")

14 Average yearly inflation differential (y-axis) and average change in relative unit labour cost (x-axis) ECB, Monthly Bulletin, Nov. 2012

15 Increasing current account imbalances Source: Citigroup, Empirical and Thematic Perspectives, 27 January, 2012

16 Design failure II: no stabilizers left in place Absence of lender of last resort in government bond market exposed fragility of government bond market in a monetary union

17 Fragility of government bond market in monetary union Governments of member states cannot guarantee to bond holders that cash would always be there to pay them out at maturity Contrast with stand-alone countries that give this implicit guarantee because they can and will force central bank to provide liquidity There is no limit to money creating capacity

18 Self-fulfilling crises This lack of guarantee can trigger liquidity crises Distrust leads to bond sales Interest rate increases Liquidity is withdrawn from national markets Government unable to rollover debt Is forced to introduce immediate and intense austerity Producing deep recession and Debt/GDP ratio increases This leads to default crisis Countries are pushed into bad equilibrium

19 This happened in Ireland, Portugal and Spain Greece is different problem: it was a solvency problem from the start Thus absence of LoLR tends to eliminate other stabilizer: automatic budget stabilizer Once in bad equilibrium countries are forced to introduce sharp austerity pushing them in recession and aggravating the solvency problem Budget stabilizer is forcefully swithched off Back to pre-1930s conditions

20

21

22

23 Design Failure III Deadly embrace between banks and sovereign Once in bad equilibrium a third design failure was exposed Countries in bad equilibrium also experience banking crisis due to deadly embrace noted earlier When sovereign is pushed in default so are banks

24 Summary The Eurozone was left unprepared to deal with endemic booms and busts in capitalism Probably these were even enhanced because of the existence of the monetary union While nothing was in place to stabilize an unstable system that pushed some countries into bad equilibria and others in good equilibria In fact some of the pre-existing stabilizing forces were switched off

25 How to redesign the Eurozone Short run: ECB is key Medium run: Macroeconomic policies in the Eurozone Long run: Consolidating national budgets and debt levels

26 The common central bank as lender of last resort Liquidity crises are avoided in stand-alone countries that issue debt in their own currencies mainly because central bank will provide all the necessary liquidity to sovereign. This outcome can also be achieved in a monetary union if the common central bank is willing to buy the different sovereigns debt in times of crisis. In doing this central bank prevents panic from triggering a self-fulfilling liquidity crisis that can degenerate into solvency crisis And pushing countries into bad equilibria

27 ECB has finally acted On September 6, ECB announced it will buy unlimited amounts of government bonds. Program is called Outright Monetary Transactions (OMT) In defending OMT, Mr Draghi argued that you have large parts of the euro area in a bad equilibrium in which you may have self-fulfilling expectations that feed on themselves.. So, there is a case for intervening... to break these expectations, which... do not concern only the specific countries, but the euro area as a whole. And this would justify the intervention of the central bank

28

29

30

31 This is the right step: only the ECB can now save the Eurozone There is danger though that its effectiveness will be reduced by politically inspired limitations Bonds with maturity less than 3 years will be bought Conditions of even more austerity may be imposed Note also that while necessary, OMT is insufficient

32 ECB should act today Spreads increase again in periphery Making recovery impossible Quantitative easing in Eurozone: ECB buys government bonds of periphery This will improve monetary transmission process And reduce degree of segmentation in financial markets of Eurozone

33 What is the criticism? Inflation risk Moral hazard Fiscal implications

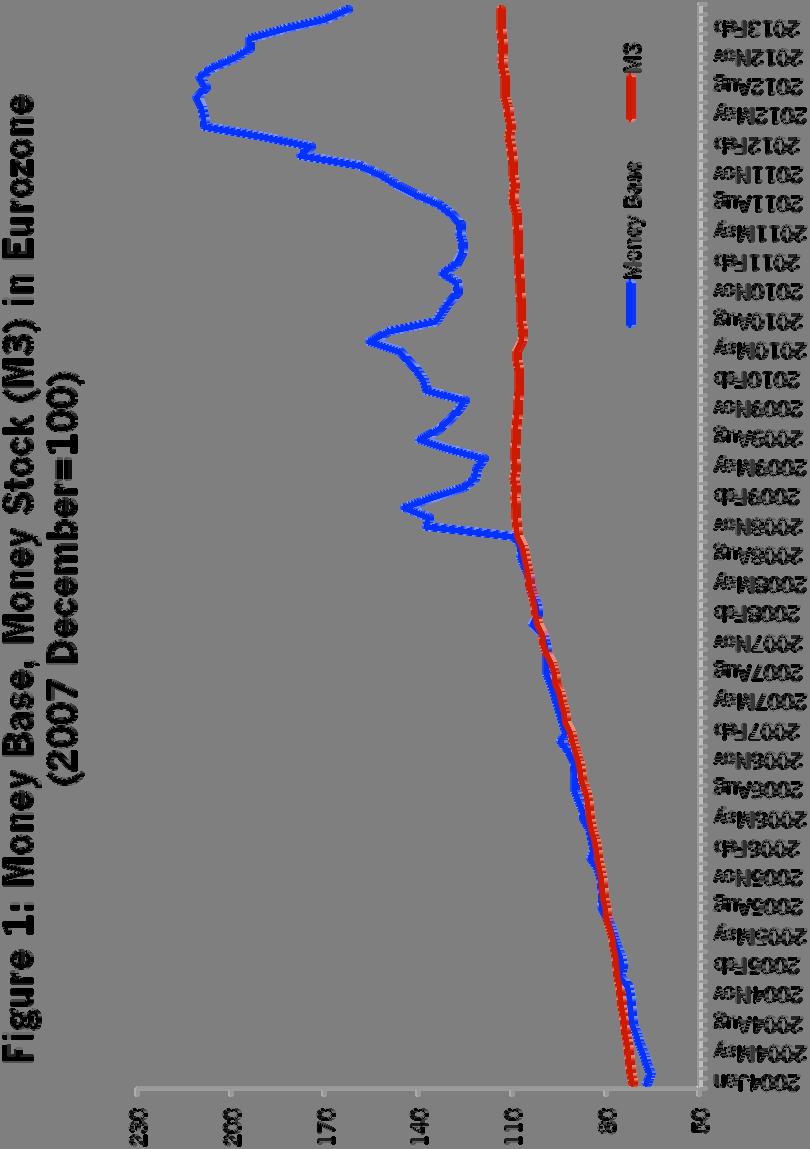

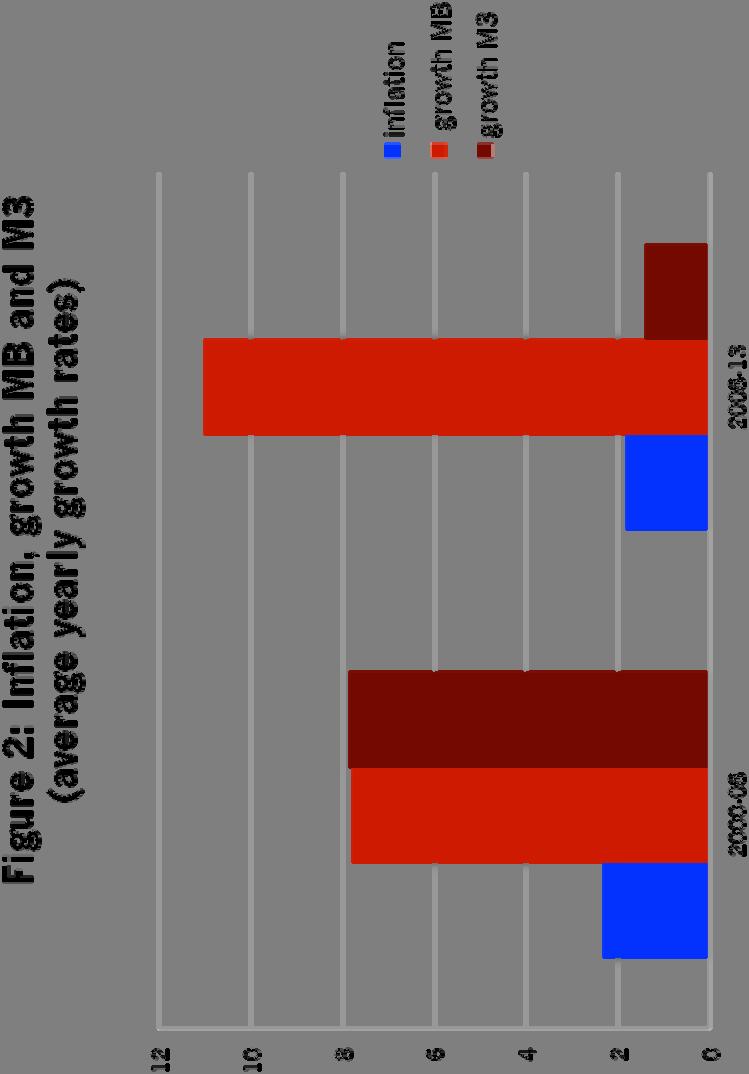

34 Inflation risk Distinction should be made between money base and money stock When central bank provides liquidity as a lender of last resort money base and money stock move in different direction In general when debt crisis erupts, investors want to be liquid

35

36

37 Thus during debt crisis banks accumulate liquidity provided by central bank This liquidity is hoarded, i.e. not used to extend credit As a result, money stock does not increase; it can even decline No risk of inflation Same as in the 1930s (cfr. Friedman)

38 Moral hazard Like with all insurance mechanisms there is a risk of moral hazard. By providing a lender of last resort insurance the ECB gives an incentive to governments to issue too much debt. This is indeed a serious risk. But this risk of moral hazard is no different from the risk of moral hazard in the banking system. It would be a mistake if the central bank were to abandon its role of lender of last resort in the banking sector because there is a risk of moral hazard. In the same way it is wrong for the ECB to abandon its role of lender of last resort in the government bond market because there is a risk of moral hazard

39 Separation of liquidity provision from supervision The way to deal with moral hazard is to impose rules that will constrain governments in issuing debt, very much like moral hazard in the banking sector is tackled by imposing limits on risk taking by banks. In general, it is better to separate liquidity provision from moral hazard concerns. Liquidity provision should be performed by a central bank; the governance of moral hazard by another institution, the supervisor.

40 This should also be the design of the governance within the Eurozone. The ECB assumes the responsibility of lender of last resort in the sovereign bond markets. A different and independent authority (European Commission) takes over the responsibility of regulating and supervising the creation of debt by national governments. This leads to the need for mutual control on debt positions, i.e. some form of political union

41 Metaphor of burning house To use a metaphor: When a house is burning the fire department is responsible for extinguishing the fire. Another department (police and justice) is responsible for investigating wrongdoing and applying punishment if necessary. Both functions should be kept separate. A fire department that is responsible both for fire extinguishing and punishment is unlikely to be a good fire department. The same is true for the ECB. If the latter tries to solve a moral hazard problem, it will fail in its duty to be a lender of last resort.

42 Fiscal consequences Third criticism: lender of last resort operations in the government bond markets can have fiscal consequences. Reason: if governments fail to service their debts, the ECB will make losses. These will have to be borne by taxpayers. Thus by intervening in the government bond markets, the ECB is committing future taxpayers. The ECB should avoid operations that mix monetary and fiscal policies

43 Is this valid criticism? No All open market operations (including foreign exchange market operations) carry risk of losses and thus have fiscal implications. When a central bank buys private paper in the context of its open market operation, there is a risk involved, because the issuer of the paper can default. This will then lead to losses for the central bank. These losses are in no way different from the losses the central bank can incur when buying government bonds. Thus, the argument really implies that a central bank should abstain from any open market operation. It should stop being a central bank.

44 Sometimes central bank has to make losses Truth is that in order to stabilize the economy the central bank sometimes has to make losses. Losses can be good for a central bank if it increases financial stability Objective of central bank should be financial stability, not making profits

45 But As the central bank should only intervene to take care of liquidity crisis it is unlikely to make losses It only makes losses if it provides liquidity to an insolvent nation (e.g. Greece) Thus, ECB should follow Bagehot s rule: provide unlimited amount of cash to solvent but illiquid governments

46 Central bank does not need equity Also there is no limit to the losses a central bank can make because it creates the money that is needed to settle its debt. Only limit arises from the need to maintain control over the money supply. A central bank does not need assets to do this: central bank can literally put the assets in the shredding machine A central bank also does not need capital (equity) There is no need to recapitalize the central bank

47 Medium run: Fiscal policies that will not kill growth Macroeconomic policies exclusively geared towards austerity in the South reinforce the split between countries in bad and in good equilibria These countries have started strong internal devaluations at the cost of deep recessions

48

49 What has been the contribution of the Core countries in the adjustment?

50 Interpretation Burden of adjustments to imbalances in the eurozone between surplus and deficit countries is borne almost exclusively by deficit countries in the periphery. This asymmetric system introduces a deflationary bias in the Eurozone Explaining the double-dip recession that is now starting in the whole of the Eurozone

51

52 Towards symmetric macroeconomic policies Stimulus in the North, where spending is below production (current account surplus) Austerity in the South (but spread out over more years) This also allows to deal with current account imbalances It takes two to tango This symmetric approach should start from the different fiscal positions of the member countries of the Eurozone

53

54

55 Here is the proposed rule The creditor countries that have stabilized their debt ratios should stop trying to balance their budgets now that the Eurozone is entering a new recession. Instead they should stabilize their government debt ratios at the levels they have achieved in The implication of such a rule is that these countries can run small budget deficits and yet keep their government debt levels constant. For Germany this implies a significant stimulus

56 Note on Germany Germany can now borrow at historically low interest rates How come German government cannot find investment projects that earn a social rate of return of more than 1.5% Is this lack of imagination? Or engrained fear of DEBT?

57 Long run: Towards a fiscal union? Ideally a full fiscal union is called for A consolidation of national debts creates a common fiscal authority that can issue debt in a currency under the control of that authority. This protects member states from being forced into default by financial markets. Fiscal union also makes insurance possible to compensate countries for bad luck

58 However Full fiscal unification is so far away that one has to think of more modest approach Here are some suggestions: Partial pooling of debt aimed at reducing fragility of national bond markets (Eurobonds) We can not all the time ask ECB to step in We have to strengthen Eurozone structurally Pooling also requires disciplining mechanism Banking union (common supervision and common resolution mechanism) European authority with taxing power necessary

59 All this requires transfer of sovereignty: More political union is necessary to make Eurozone sustainable in the long run

60 Conclusion The recent decision by the ECB to act a Lender of Last Resort is a major regime change for the Eurozone It has significantly reduced existential fears that slowly but inexorably were destroying the Eurozone s foundations. The ECB s new role although necessary is not sufficient to guarantee its survival Signals must be given that the Eurozone is here to stay

61 These signals are: A partial debt pooling that ties the hands of the member countries of the Eurozone and shows that they are serious in their intentions to stick together. Symmetric macroeconomic policies to avoid a long and protracted deflation that will not be accepted by large parts of the Eurozone population In the long run a significant political union will be necessary, Euro is currency without a country To make it sustainable a European country has to be created

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

What Governance for the Eurozone? Paul De Grauwe London School of Economics

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

Managing the Fragility of the Eurozone. Paul De Grauwe London School of Economics

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Can the Euro Survive?

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

The European Central Bank as Lender of Last Resort in the Government Bond Markets

CESifo Economic Studies, Vol. 59, 3/2013, 520 535 doi:10.1093/cesifo/ift012 The European Central Bank as Lender of Last Resort in the Government Bond Markets Paul De Grauwe*,y *London School of Economics,

CESifo Economic Studies, Vol. 59, 3/2013, 520 535 doi:10.1093/cesifo/ift012 The European Central Bank as Lender of Last Resort in the Government Bond Markets Paul De Grauwe*,y *London School of Economics,

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

Closed-Door Workshop Eurozone in the Doldrums. The Legacy of the Eurocrisis ISPI-Milan, 13 March p.m.

Closed-Door Workshop Eurozone in the Doldrums. The Legacy of the Eurocrisis ISPI-Milan, 13 March 2015 4.00 5.30 p.m. Paul DE GRAUWE, London School of Economics If we look at the cumulated current accounts

Closed-Door Workshop Eurozone in the Doldrums. The Legacy of the Eurocrisis ISPI-Milan, 13 March 2015 4.00 5.30 p.m. Paul DE GRAUWE, London School of Economics If we look at the cumulated current accounts

In search of symmetry in the eurozone

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE. Paul De Grauwe (LSE) Yuemei Ji (Brunel University)

Yuemei Ji (Brunel University)") CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE Paul De Grauwe (LSE) Yuemei Ji (Brunel University) Stagnation in Eurozone Figure 1: Real GDP in Eurozone, EU10 and US (prices of 2010) 135 130 125

CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE Paul De Grauwe (LSE) Yuemei Ji (Brunel University) Stagnation in Eurozone Figure 1: Real GDP in Eurozone, EU10 and US (prices of 2010) 135 130 125

Design failures of the euro area 1

1 Paul De Grauwe London School of Economics Economists were early critics of the design of the euro area, though many of their warnings went unheeded. This column discusses some fundamental design flaws,

1 Paul De Grauwe London School of Economics Economists were early critics of the design of the euro area, though many of their warnings went unheeded. This column discusses some fundamental design flaws,

KEYNES SAVINGS PARADOX, FISHER S DEBT DEFLATION AND THE BANKING CRISIS. Paul De Grauwe University of Leuven

KEYNES SAVINGS PARADOX, FISHER S DEBT DEFLATION AND THE BANKING CRISIS Paul De Grauwe University of Leuven Abstract: The sharp fall in economic activity in the world is the result of an interaction between

KEYNES SAVINGS PARADOX, FISHER S DEBT DEFLATION AND THE BANKING CRISIS Paul De Grauwe University of Leuven Abstract: The sharp fall in economic activity in the world is the result of an interaction between

More evidence that financial markets imposed excessive austerity in the eurozone

More evidence that financial markets imposed excessive austerity in the eurozone Paul De Grauwe and Yuemei Ji 5 February 2013 The decision by the ECB in 2012 to commit itself to unlimited support of the

More evidence that financial markets imposed excessive austerity in the eurozone Paul De Grauwe and Yuemei Ji 5 February 2013 The decision by the ECB in 2012 to commit itself to unlimited support of the

How to avoid a double-dip recession in the eurozone

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Gains for all: A proposal for a common euro bond Paul De Grauwe Wim Moesen. University of Leuven

Gains for all: A proposal for a common euro bond Paul De Grauwe Wim Moesen University of Leuven Until the eruption of the credit crisis in August 2007 financial markets were gripped by a flight to risk.

Gains for all: A proposal for a common euro bond Paul De Grauwe Wim Moesen University of Leuven Until the eruption of the credit crisis in August 2007 financial markets were gripped by a flight to risk.

* I am grateful to Daniel Gros, Martin Wolf and Charles Wyplosz for comments and suggestions

THE GOVERNANCE OF A FRAGILE EUROZONE Paul De Grauwe* University of Leuven and CEPS Abstract: When entering a monetary union, member- countries change the nature of their sovereign debt in a fundamental

THE GOVERNANCE OF A FRAGILE EUROZONE Paul De Grauwe* University of Leuven and CEPS Abstract: When entering a monetary union, member- countries change the nature of their sovereign debt in a fundamental

In the absence of fiscal union, the Eurozone needs a more flexible monetary policy: A comment

PSL Quarterly Review, vol. 69 n. 278 (September 2016), 279-285 In the absence of fiscal union, the Eurozone needs a more flexible monetary policy: A comment ANDREA TERZI * In a recent article in this Review,

PSL Quarterly Review, vol. 69 n. 278 (September 2016), 279-285 In the absence of fiscal union, the Eurozone needs a more flexible monetary policy: A comment ANDREA TERZI * In a recent article in this Review,

European Public Debt: A Solution to Fragility

Workshop Discussion Material European Public Debt: A Solution to Fragility 1. Moral Hazard within EUM The establishment of an economic and monetary union generates benefits in terms of microeconomic efficiencies,

Workshop Discussion Material European Public Debt: A Solution to Fragility 1. Moral Hazard within EUM The establishment of an economic and monetary union generates benefits in terms of microeconomic efficiencies,

CONDITIONAL EUROBONDS AND EUROZONE REFORM

CONDITIONAL EUROBONDS AND EUROZONE REFORM John Muellbauer, INET at Oxford OENB workshop Towards a genuine economic and monetary union, Vienna, 10-11 September, 2015 OBJECTIVES Reduce the Euro-area policy

CONDITIONAL EUROBONDS AND EUROZONE REFORM John Muellbauer, INET at Oxford OENB workshop Towards a genuine economic and monetary union, Vienna, 10-11 September, 2015 OBJECTIVES Reduce the Euro-area policy

The future of the euro zone

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

Cross-border banking regulating according to risk. Thorsten Beck

Cross-border banking regulating according to risk Thorsten Beck Following 2008: Lots of regulatory reforms Basel 3: Higher quantity and quality of capital and liquid assets Additional capital buffers for

Cross-border banking regulating according to risk Thorsten Beck Following 2008: Lots of regulatory reforms Basel 3: Higher quantity and quality of capital and liquid assets Additional capital buffers for

Paul De Grauwe The legacy of the Eurozone crisis and how to overcome it

Paul De Grauwe The legacy of the Eurozone crisis and how to overcome it Article (Published version) (Refereed) Original citation: de Grauwe, Paul (2016) The legacy of the Eurozone crisis and how to overcome

Paul De Grauwe The legacy of the Eurozone crisis and how to overcome it Article (Published version) (Refereed) Original citation: de Grauwe, Paul (2016) The legacy of the Eurozone crisis and how to overcome

The Economic and Social Review, Vol. 43, No. 1, Spring, 2012, pp. 1 30

The Economic and Social Review, Vol. 43, No. 1, Spring, 2012, pp. 1 30 A Fragile Eurozone in Search of a Better Governance PAUL DE GRAUWE* University of Leuven Abstract: When entering a monetary union,

The Economic and Social Review, Vol. 43, No. 1, Spring, 2012, pp. 1 30 A Fragile Eurozone in Search of a Better Governance PAUL DE GRAUWE* University of Leuven Abstract: When entering a monetary union,

Banking Union in Europe Glass Half Full or Glass Half Empty. Thorsten Beck

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

International financial crises

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

Contributions from the Sherpas of the Member States to the Five Presidents' Report SPAIN. Second Contribution

Contributions from the Sherpas of the Member States to the Five Presidents' Report SPAIN Second Contribution Better Economic Governance in the Euro Area Spanish Contribution May 14 th 2015 The economic

Contributions from the Sherpas of the Member States to the Five Presidents' Report SPAIN Second Contribution Better Economic Governance in the Euro Area Spanish Contribution May 14 th 2015 The economic

Making the Eurozone sustainable Paul De Grauwe

index 2000=100 Making the Eurozone sustainable Paul De Grauwe The election of Emmanuel Macron to the French Presidency creates new opportunities for taking initiatives that will ensure, first, that the

index 2000=100 Making the Eurozone sustainable Paul De Grauwe The election of Emmanuel Macron to the French Presidency creates new opportunities for taking initiatives that will ensure, first, that the

The outlook for the global economy in 2012

The Eurozone Crisis Still Threatens Global Growth Paolo Guerrieri Professor of Economics, University of Rome Sapienza; Professor, College of Europe, Bruges The outlook for the global economy in 2012 is

The Eurozone Crisis Still Threatens Global Growth Paolo Guerrieri Professor of Economics, University of Rome Sapienza; Professor, College of Europe, Bruges The outlook for the global economy in 2012 is

Notes on Hyman Minsky s Financial Instability Hypothesis

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

The Economics of the European Union

Fletcher School, Tufts University The Economics of the European Union Prof. George Alogoskoufis Lecture 21: The Eurozone Crisis, Why it Happened and Lessons for the Future Two Important Recent Reports

Fletcher School, Tufts University The Economics of the European Union Prof. George Alogoskoufis Lecture 21: The Eurozone Crisis, Why it Happened and Lessons for the Future Two Important Recent Reports

Consequences of present Euro area monetary policy on savings and capital wealth formation. 14 November Parliamentary evening in Brussels

Jacques de Larosière Consequences of present Euro area monetary policy on savings and capital wealth formation 14 November 2016 Parliamentary evening in Brussels As we all know, the ECB has engaged in

Jacques de Larosière Consequences of present Euro area monetary policy on savings and capital wealth formation 14 November 2016 Parliamentary evening in Brussels As we all know, the ECB has engaged in

Eurozone. Outlook for. Ernst & Young Eurozone Forecast. Summer edition 2012

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

The Turbulent EMS in the 1990s: What Lessons for Today? Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel

The Turbulent in the 1990s: What Lessons for Today? André Sapir Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel 2 The turbulent 1990s: the incompatible trio July 1990: Full

The Turbulent in the 1990s: What Lessons for Today? André Sapir Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel 2 The turbulent 1990s: the incompatible trio July 1990: Full

The role of ECB in relation to the modified EFSF and the future ESM. Prof. Dr. iur. Dr. rer. pol. Peter Sester

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies?

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Banks and sovereign debt in Europe

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Global Safe Assets. Pierre-Olivier Gourinchas (UC Berkeley, Sciences-Po) Olivier Jeanne (JHU, PIIE)

Olivier Jeanne (JHU, PIIE)") Pierre-Olivier Gourinchas (UC Berkeley, Sciences-Po) Olivier Jeanne (JHU, PIIE) International Conference on Capital Flows and Safe Assets May 26-27, 2013 Introduction Widespread concern that the global

Pierre-Olivier Gourinchas (UC Berkeley, Sciences-Po) Olivier Jeanne (JHU, PIIE) International Conference on Capital Flows and Safe Assets May 26-27, 2013 Introduction Widespread concern that the global

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

II. Underlying domestic macroeconomic imbalances fuelled current account deficits

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

Greece Facing an Uncertain Future

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

For the Eurozone, much hinges on self-discipline and self-interest

For the Eurozone, much hinges on self-discipline and self-interest Author: Jonathan Lemco, Ph.D. Will the Eurozone survive its severe financial challenges? Vanguard believes it is in the interests of both

For the Eurozone, much hinges on self-discipline and self-interest Author: Jonathan Lemco, Ph.D. Will the Eurozone survive its severe financial challenges? Vanguard believes it is in the interests of both

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Interview with Klaus Regling, Managing Director, ESM. Published in Hospodárske noviny (Slovakia) on 16 September Interviewer: Tomáš Púchly

on 16 September Interviewer: Tomáš Púchly") Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Economic and Financial Affairs Committee. The EMU: challenges and the way forward

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Fund Management Diary

Fund Management Diary Meeting held on 14 June 2016 Deficit Matters In late October 2013, the US Treasury issued a report saying that the German current account surplus which at that time stood at 7% of

Fund Management Diary Meeting held on 14 June 2016 Deficit Matters In late October 2013, the US Treasury issued a report saying that the German current account surplus which at that time stood at 7% of

Fiscal Dimensions of Inflationist Monetary Policy. Marvin Goodfriend Carnegie Mellon University and National Bureau of Economic Research

Fiscal Dimensions of Inflationist Monetary Policy Marvin Goodfriend Carnegie Mellon University and National Bureau of Economic Research Shadow Open Market Committee October 21, 2011 Introduction Policymakers

Fiscal Dimensions of Inflationist Monetary Policy Marvin Goodfriend Carnegie Mellon University and National Bureau of Economic Research Shadow Open Market Committee October 21, 2011 Introduction Policymakers

MACROECONOMICS IN THE GLOBAL ECONOMY

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Professor Antonio Fatás Final Exam February 23, 2015 Instructions: (PLEASE READ) Space to answer the questions is limited. DO NOT WRITE IN THE BACK

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Professor Antonio Fatás Final Exam February 23, 2015 Instructions: (PLEASE READ) Space to answer the questions is limited. DO NOT WRITE IN THE BACK

Independent Central Banking in times of crisis

Independent Central Banking in times of crisis The Eurosystem CEMLA: XI Meeting of Central Bank Legal Advisers Santiago, Chile Content A.The Eurosystem s response to the crisis B. The Eurosystem Framework

Independent Central Banking in times of crisis The Eurosystem CEMLA: XI Meeting of Central Bank Legal Advisers Santiago, Chile Content A.The Eurosystem s response to the crisis B. The Eurosystem Framework

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Chapter 8. Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015

Instructor: Prof. Menzie Chinn UW Madison Fall 2015") Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Money and Banking ECON3303. Lecture 9: Financial Crises. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

The financial crisis challenges and new ideas Luxembourg School of Finance 28 January 2010

The financial crisis challenges and new ideas Luxembourg School of Finance 28 January 2010 I am very pleased to be here tonight and wish to thank the Luxembourg School of Finance for providing me with

The financial crisis challenges and new ideas Luxembourg School of Finance 28 January 2010 I am very pleased to be here tonight and wish to thank the Luxembourg School of Finance for providing me with

Europe in crisis. George Gelauff. ECU 92 Lustrum Conference Utrecht. 23 February 2012

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Global Imbalances, Currency Wars and the Euro

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICIES ECONOMIC AND MONETARY AFFAIRS Global Imbalances, Currency Wars and the Euro NOTE Abstract Global current

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICIES ECONOMIC AND MONETARY AFFAIRS Global Imbalances, Currency Wars and the Euro NOTE Abstract Global current

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Greece and the Euro. Harris Dellas, University of Bern. Abstract

Greece and the Euro Harris Dellas, University of Bern Abstract The recent debt crisis in the EU has revived interest in the costs and benefits of membership in a currency union for a country like Greece

Greece and the Euro Harris Dellas, University of Bern Abstract The recent debt crisis in the EU has revived interest in the costs and benefits of membership in a currency union for a country like Greece

Chapter Fourteen. Chapter 10 Regulating the Financial System 5/6/2018. Financial Crisis

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Member of

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

Links between Macro Stability and Financial Stability

Links between Macro Stability and Financial Stability Isabel Schnabel University of Bonn Conference Rethinking the Central Bank s Mandate Sveriges Riksbank, Stockholm, June 4, 2016 1/35 I. Macro stability

Links between Macro Stability and Financial Stability Isabel Schnabel University of Bonn Conference Rethinking the Central Bank s Mandate Sveriges Riksbank, Stockholm, June 4, 2016 1/35 I. Macro stability

OECD III: EMU. Gavin Cameron Lady Margaret Hall. Michaelmas Term 2004

OECD III: EMU Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 the Trinity Free Capital Mobility USA, Japan ERM, NICs, EMU Independent domestic monetary policy Stable (Fixed) Exchange Rate Bretton

OECD III: EMU Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 the Trinity Free Capital Mobility USA, Japan ERM, NICs, EMU Independent domestic monetary policy Stable (Fixed) Exchange Rate Bretton

The Financial Crisis, Global Imbalances, and the

The Financial Crisis, Global Imbalances, and the International Monetary System David Vines Oxford University, Australian National University, and CEPR ICRIER-CEPII-BRUEGEL Conference on International Cooperation

The Financial Crisis, Global Imbalances, and the International Monetary System David Vines Oxford University, Australian National University, and CEPR ICRIER-CEPII-BRUEGEL Conference on International Cooperation

What Future for the Eurozone? Paul De Grauwe London School of Economics. Yuemei Ji Brunel University

Preliminary draft What Future for the Eurozone? Paul De Grauwe London School of Economics Yuemei Ji Brunel University Abstract: We argue first that the Eurozone crisis has left a legacy of unsustainable

Preliminary draft What Future for the Eurozone? Paul De Grauwe London School of Economics Yuemei Ji Brunel University Abstract: We argue first that the Eurozone crisis has left a legacy of unsustainable

Negative Yields in the Eurozone: Rationale and Repercussions

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not

QUELS CHOCS POUR SORTIR DE LA CRISE? Prof. Dr. BRUNO COLMANT Membre de l'académie Royale de Belgique

QUELS CHOCS POUR SORTIR DE LA CRISE? Prof. Dr. BRUNO COLMANT Membre de l'académie Royale de Belgique 2 Several issues to deal with Recession and huge social issues : unemployment, digitalisation Public

QUELS CHOCS POUR SORTIR DE LA CRISE? Prof. Dr. BRUNO COLMANT Membre de l'académie Royale de Belgique 2 Several issues to deal with Recession and huge social issues : unemployment, digitalisation Public

Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

The near-term global economic outlook

Overview The near-term global economic outlook Paul van den Noord Counsellor to the Chief Economist OECD 1 Overview World growth has slowed, including in EMEs. Trade has weakened. Unemployment is high

Overview The near-term global economic outlook Paul van den Noord Counsellor to the Chief Economist OECD 1 Overview World growth has slowed, including in EMEs. Trade has weakened. Unemployment is high

Josef Bonnici: The changing nature of economic and financial governance following the euro area crisis

Josef Bonnici: The changing nature of economic and financial governance following the euro area crisis Introductory remarks by Professor Josef Bonnici, Governor of the Central Bank of Malta, at the Malta

Josef Bonnici: The changing nature of economic and financial governance following the euro area crisis Introductory remarks by Professor Josef Bonnici, Governor of the Central Bank of Malta, at the Malta

How Curb Risk In Wall Street. Luigi Zingales. University of Chicago

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

The European Economic Crisis

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for Modest

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for Modest

Quantitative Easing in the Eurozone. It s Possible without Fiscal Transfers

Quantitative Easing in the Eurozone. It s Possible without Fiscal Transfers Paul de Grauwe and Yuemei Ji QUANTITATIVE EASING IN THE EUROZONE. IT S POSSIBLE WITHOUT FISCAL TRANSFERS Paul De Grauwe London

Quantitative Easing in the Eurozone. It s Possible without Fiscal Transfers Paul de Grauwe and Yuemei Ji QUANTITATIVE EASING IN THE EUROZONE. IT S POSSIBLE WITHOUT FISCAL TRANSFERS Paul De Grauwe London

Adventures in Monetary Policy: The Case of the European Monetary Union

: The Case of the European Monetary Union V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis The ECB and Its Watchers XIX March 14, 2018 Why the Discontent? The Tell-Tale

: The Case of the European Monetary Union V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis The ECB and Its Watchers XIX March 14, 2018 Why the Discontent? The Tell-Tale

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Working Paper Research. The fragility of two monetary regimes : The European Monetary System and the Eurozone. October 2013 No 243

The fragility of two monetary regimes : The European Monetary System and the Eurozone Working Paper Research by Paul De Grauwe and Yuemei Ji October 2013 No 243 Editorial Director Jan Smets, Member of

The fragility of two monetary regimes : The European Monetary System and the Eurozone Working Paper Research by Paul De Grauwe and Yuemei Ji October 2013 No 243 Editorial Director Jan Smets, Member of

Some Thoughts on Monetary and Political Union. Paul De Grauwe

Some Thoughts on Monetary and Political Union Paul De Grauwe Introduction The question of the future of the monetary union in Europe is first and foremost the question of whether a monetary union can be

Some Thoughts on Monetary and Political Union Paul De Grauwe Introduction The question of the future of the monetary union in Europe is first and foremost the question of whether a monetary union can be

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Dr Andreas Dombret Member of the Executive Board of the Deutsche Bundesbank

Dr Andreas Dombret Member of the Executive Board of the Deutsche Bundesbank Looking to the future What comes next in terms of European financial integration? Speech at the South African Institute for International

Dr Andreas Dombret Member of the Executive Board of the Deutsche Bundesbank Looking to the future What comes next in terms of European financial integration? Speech at the South African Institute for International

From the financial crisis to the public debt crisis. Some considerations on the Italian Case

8th ESDN Workshop Brussels, 22-23 November 2012 From the financial crisis to the public debt crisis. Some considerations on the Italian Case Stefania P. S. Rossi Department of Economics University of Cagliari,

8th ESDN Workshop Brussels, 22-23 November 2012 From the financial crisis to the public debt crisis. Some considerations on the Italian Case Stefania P. S. Rossi Department of Economics University of Cagliari,

POLI 12D: International Relations Sections 1, 6

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

In addition, the sample portfolio ended the quarter with 100% invested in cash equivalent and fixed income investments.

Review: Sample Income Portfolio In the past quarter, the portfolio s value was impacted by the following changes in market values Bonds and preferred shares increased by $472.47 Deposits of interest and

Review: Sample Income Portfolio In the past quarter, the portfolio s value was impacted by the following changes in market values Bonds and preferred shares increased by $472.47 Deposits of interest and

TOWARDS A MORE INTEGRATED AND STABLE EUROPE? National Bank of Poland

TOWARDS A MORE INTEGRATED AND STABLE EUROPE? National Bank of Poland by Daniel Gros Warsaw; October 2011 Key points 1. Background: global credit boom and excess leverage. 2. EMU system not designed to

TOWARDS A MORE INTEGRATED AND STABLE EUROPE? National Bank of Poland by Daniel Gros Warsaw; October 2011 Key points 1. Background: global credit boom and excess leverage. 2. EMU system not designed to

Financial Fragility and the Lender of Last Resort

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

International Money and Banking: 17. Exchange Rate Regimes and the Euro Crisis

International Money and Banking: 17. Exchange Rate Regimes and the Euro Crisis Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Exchange Rate Regimes and the Euro Spring 2018 1 / 31 Part

International Money and Banking: 17. Exchange Rate Regimes and the Euro Crisis Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Exchange Rate Regimes and the Euro Spring 2018 1 / 31 Part

STRUCTURAL SHIFTS AND CHALLENGES IN THE GLOBAL ECONOMY M I C H A E L S P E N C E N E W D E L H I J A N U A R Y

STRUCTURAL SHIFTS AND CHALLENGES IN THE GLOBAL ECONOMY M I C H A E L S P E N C E N E W D E L H I J A N U A R Y 2 0 1 2 2 3 What is the Next Convergence? Before the Industrial Revolution 200 years of divergence

STRUCTURAL SHIFTS AND CHALLENGES IN THE GLOBAL ECONOMY M I C H A E L S P E N C E N E W D E L H I J A N U A R Y 2 0 1 2 2 3 What is the Next Convergence? Before the Industrial Revolution 200 years of divergence

ECO 403 L0301 Developmental Macroeconomics. Lecture 8 Balance-of-Payment Crises

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

Greece should restructure its debt but stay in the Euro

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

Intesa Sanpaolo S.p.A.

Intesa Sanpaolo S.p.A. IRMC 2012 The Unintended Consequences of Re-Regulation Rome, 19 June 2012 Mauro Maccarinelli Head of Market Risk and Financial Valuation Risk Management Group 1 Re-Regulation (1/2)

Intesa Sanpaolo S.p.A. IRMC 2012 The Unintended Consequences of Re-Regulation Rome, 19 June 2012 Mauro Maccarinelli Head of Market Risk and Financial Valuation Risk Management Group 1 Re-Regulation (1/2)

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

Fixed Exchange Rates and Currency Unions

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

Speech Bridging the North-South Divide in the Euro Area

Speech Bridging the North-South Divide in the Euro Area Angel Ubide D.E. Shaw & Co. and Peterson Institute for International Economics Remarks to the Euro50 Group Meeting in Brussels March 28, 2014 I will

Speech Bridging the North-South Divide in the Euro Area Angel Ubide D.E. Shaw & Co. and Peterson Institute for International Economics Remarks to the Euro50 Group Meeting in Brussels March 28, 2014 I will

New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations

New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations 8th Conference on Payment and Securities Settlement Systems, Ohrid, 11-13 May 2015

New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations 8th Conference on Payment and Securities Settlement Systems, Ohrid, 11-13 May 2015

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

ECN 106 Macroeconomics 1. Lecture 10

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the