Consequences of present Euro area monetary policy on savings and capital wealth formation. 14 November Parliamentary evening in Brussels

|

|

|

- Martin Reynolds

- 5 years ago

- Views:

Transcription

1 Jacques de Larosière Consequences of present Euro area monetary policy on savings and capital wealth formation 14 November 2016 Parliamentary evening in Brussels As we all know, the ECB has engaged in a very bold expansionary monetary policy, particularly since the beginning of My purpose is not to discuss the QE policy of the ECB. My mandate this evening is to try and understand the impact of this policy on savings and on investment. I Consequences of QE on European savings A) The balance between savings and consumption. Yields - very close to 0 or even lesser on riskless investments should, normally, dissuade economic agents from saving and induce them into more consumption, which would support growth. But, contrary to the hopes of many, financial repression 1, especially in Europe, does not always result into an increase in consumption. Households savings in countries like France and Germany are structurally high (respectively 15% and 17% of incomes) and have remained stable. They ensure more than 80% of the financing of the European economies. The financial part of those savings is mostly of a precautionary nature (to face life uncertainties, unemployment, old age ) and is also constituted for transmission purposes. The majority of such funds are placed in savings accounts, insurance and pension funds which are themselves invested in safe assets. 1 Some banks in Germany are beginning to charge their household clients a negative rate on their current accounts (higher than 100,000 ). Some French banks are applying such rates on enterprises. 1

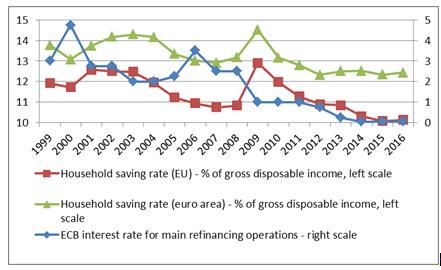

2 When the yields fall or, sometimes even disappear, as a result of monetary policy, it would be logical to see savings switch to equity instruments that can provide, over the longer term, more satisfactory returns, all the more so if investors believe in an upturn of the economy. In fact, it is that process that took place in the US as a consequence of Quantitative Easing (QE). With lower long term rates, equity markets rebounded exactly in line with the creation of liquidity by the Fed. That upturn in equity markets triggered a wealth effect which contributed to more consumption. But in the Eurozone, as I will show later, this process doesn t seem to work : no shift to equities, no wealth-effect. Indeed European savers are not the same as those in the US. They are basically risk-averse, and are not inclined to buy shares (which anyway would be, most often, penalized by the tax system). Perhaps more worryingly, for policy makers, the shift of repressed financial savings to consumption doesn t seem to work either. Indeed, one observes that a significant number of savers are trying to offset lower returns by more savings. B) Savings, consumption and low interest rates. Let us look into this crucial issue in more detail 2. Ø Gross household saving rate in the Eurozone has been hovering around the high level of 12,5% of disposable income for the last 5 years (see Graphs 1 and 2) in spite of QE ; Ø Germany s household savings ratio remains high and stable over the last 15 years : around 17% of disposable income. And this rate has not been materially influenced by the fall in German Bond yields which have tumbled (from 10% to 0,5%) over the period ; Ø France s household savings also show much resilience at around the - very high - level of 15% of disposable income. There is little correlation between bond yields and household savings behavior ; 2 See : «ECB and Europe s oversaving problems» by Paul Jackson Les cahiers de l OEE May

3 Ø Switzerland is an interesting case in point : households savings rate has increased dramatically from 21% in 1999 to 26% since 2015 during the years of monetary expansion and ultra low interest rates ; Ø The corresponding figures mark an evolution of 5% to 19% in Sweden and 1% to 11% in Denmark over the same period ; Ø In the United Kingdom, the household saving rate surged from 6% to 12% after the Bank of England dramatically lowered its intervention rate from 11% in 2007 to 0.5% in 2009 ; Ø Even in the US it now appears that lower interest rates are associated with higher savings (while it was not clear before QE). I know that we should be careful not to jump from these figures to too simple conclusions. Some saving behavior may indeed have been impacted (boosted) by the uncertainties stemming from the financial crisis. One can add that in some countries higher financial and non-financial investment may be associated with larger borrowing, a combination that would not result in a fall in consumption. Be it as it may, it remains that : 1- When studying the interest rate savings behavior, we see that the income effect (which requires a higher level of savings to offset the consequences of lower or negative interest rates) has been manifest in most European countries, while the substitution effect (saving less to spend more) seems difficult to establish (except for the UK and Italy although the picture is unclear in the latter case) ; 2 this income effect is one of the factors that explains the resilience of household savings in Europe during the last years of low interest rates ; 3 the UK is the only significant case where the substitution effect dominates (more spending when rates fall), which also explains the current account deterioration of that country ; 3

4 4 This tendency for large Eurozone countries to maintain or even increase household savings is in line with the increase of the current account surplus of the region : Source : ECB Eurozone current account surplus (as a percentage of GDP) Eurozone + 2,2% + 2,5% + 3,2% The interesting fact (but worrisome for monetary policy makers) is that the QE years in Europe have been globally accompanied by larger national savings and higher current account surpluses. All in all, the European experience does not suggest that extremely low interest rates (or negative ones) are a recipe for economic growth and the revival of consumption, let alone of investment. II Consequences of QE on investment in Europe A) The behavior of investment in the Eurozone is lackluster. The gross fixed capital formation trend has been disappointing in the Eurozone as compared with the whole group of advanced countries. Annual average growth rates of Gross Fixed Capital formation from 2008 to 2017 All advanced countries + 0,4% Eurozone - 0,8% Source : IMF World Economic Outlook

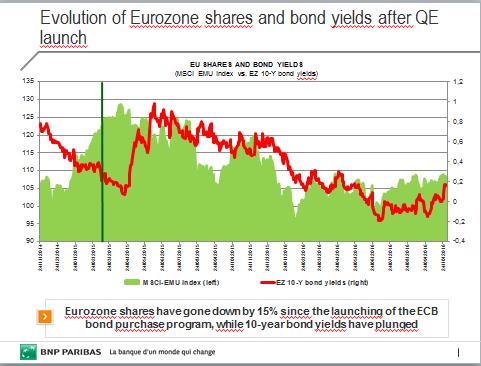

5 B) Productive investment (carried out by non financial enterprises) appears quite insensitive to changes in interest rates. Recent studies 3 have found that only 8% of firms in a September 2012 survey declared that they would increase investment if borrowing costs declined significantly. By contrast, 68% did not expect that any decline of interest rates would lead to more investments. This is all the more striking that interest rates were much higher in 2012 than they are today. These observations are consistent with the more recent ECB surveys. The determining factors cited by enterprises in business surveys regarding their decision to invest are always : Expected sales, Future growth, Confidence. Interest rates changes are hardly mentioned in the list of significant factors. C) Low interest rates do not seem to boost equity in the Eurozone. One of the assumed advantages of QE (which reduces long term interest rates) was to dissuade savers from investing in 0 yield riskless assets and to divert them into equity. This does not seem to take place. Since the ECB launched its bond purchase program in 2015, the MSCI-EMU Index actually has gone down by 15% which is in contrast with the US experience (see Graph 3). The reasons behind this bearish performance of Eurozone equities are not related to monetary policy, but to the weakness of expectations on economic growth and profitability of non financial corporations It is clear that low interest rates, if anything, have not boosted the stock market in the Eurozone. 3 See Sharpe and Suarez (2014) referred to in William de Vijlder article in Conjoncture - BNP Paribas sept/oct 2016 : What is driving corporate investment?. 5

6 D) In a region where banks account for the overwhelming part of the financing of the economy, it is essential to keep the banking channel open and active. Extremely low interest rates compound the difficulties of that problem. In the Eurozone, banks represent 70% of total financing of the economy (the reverse in the US where financial markets play the predominant role). But banks in the Eurozone have been deleveraging over the past years. Ø For 4 years ( ) the outstanding amounts of bank credit to enterprises has been reduced by 2% to 3% per year. There has been a revival of bank credit since 2015 (albeit only 1,8% increase). But Spain and Italy continue to be in negative territory. Ø On top of demand driven factors that explain part of the dampening of bank credit, there has been a sharp increase in banking regulation constraints which limits the ability of European banks to expand their business ; Ø The low interest rate environment of today compounds this evolution and contributes to erode the average profitability of banks (ROE : 4% in 2015 in EU against 9% in the US) ; Ø The envisaged additional constraints on risk weighting ( Basel 4 ) could amplify this phenomenon and make deleveraging a bigger threat. While it would be logical - and essential - to preserve the transmission channel of Monetary Policy (i.e. banks ability to lend) we see a continuous move towards more and more procyclical regulatory rules on the banking sector. 6

7 Contrary to what is often pretended, the more monetary policy is well intended and increases its ease, the less investors seem to be tempted to take advantage of it. If actualization (discount) rates, as they are set by private investors today, are high and conservative in spite of the low interest rate environment, and if savings are resilient, it is perhaps because the extreme consequences of lasting monetary laxity are seen as additional factors increasing uncertainty as well as undermining confidence in future growth. In such an environment, it is vital that central banks instill confidence and reinforce long term stability signals. Conclusion The risks incurred by too prolonged an accommodative monetary policy could be huge not only for the future of the economy but also for our society. Even if it s obvious that the natural equilibrium interest rate tends to diminish in an environment of weak growth and high savings, this does not mean that it must become negative. The interest rate will always remain the price that savers are entitled to expect for having accepted, for a given period of time, to postpone their immediate consumption. To say that such a price should become negative goes against common sense (time would be abolished!) and could bear grave consequences for the future. How could one calculate with negative rates the returns expected on an investment? What would be, in a market economy, the future of long term investment projects that would involve high fixed costs and high risks? who would finance them without adequate remuneration 4? Resource allocation tends to lose its efficiency when interest rates get very low. Indeed, the only projects that can be financed at current prevailing rates are the ones which are viable with very low rates. Less profitable and more risky investments (but perhaps socially more beneficial) could be left aside. 4 More a project is risky and more its profitability is uncertain, more its discount rate (used to determine its present value) must be high, if private markets are to finance it. 7

8 It is a fact that the present European monetary policy is hurting insurance companies and pension funds. These institutions have long term liabilities vis-à-vis their clients. But the yields produced by their assets are edging towards 0. How can those institutions solve this discrepancy 5? Let s not forget that insurance companies and pension funds used to play an essential role in the buying and holding of long term investment securities as well as in ensuring market liquidity. To make things worse, this fundamental mismatch stemming from extremely low rates, is compounded by regulatory constraint (Basel, Solvency II). The current preoccupation with the inflation goal should not overlook the dangers of asset bubbles. Negative nominal interest rates are hurting households, insurers and pension funds and are historically unprecedented. Let us not forget that a similar process was at work in the running to the credit crisis. Truth is unfortunately simple : It is not through lasting and massive liquidity creation - or even monetary policy devaluations - that growth issues can be tackled. Too much debt always leads to bubbles, to search for yield, to higher risks (insufficiently priced) and, ultimately, to crises. Jacques de Larosière See Graphs Page 9 5 US defined benefits pension plans have moved from fully funded in 2000 to 74% funded (end 2015). 8

9 Graph 1 Graph 2 Graph 3 9

Negative Yields in the Eurozone: Rationale and Repercussions

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not

The sharp accumulation in government debt can t go on forever

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

Quantitative easing in the Euro area

Quantitative easing in the Euro area Rationale, impact and some considerations for Malta 11 February 2015 Rationale for quantitative easing Quantitative easing (QE) refers to the purchase of government

Quantitative easing in the Euro area Rationale, impact and some considerations for Malta 11 February 2015 Rationale for quantitative easing Quantitative easing (QE) refers to the purchase of government

APPENDIX: Country analyses

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

EUROPEAN BANKS: NEITHER A BORROWER NOR LENDER BE

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY August 8 2016 EUROPEAN BANKS: NEITHER A BORROWER NOR LENDER BE Matthew Peterson Chief Wealth Strategist, LPL Financial KEY TAKEAWAYS Banks everywhere are under pressure

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY August 8 2016 EUROPEAN BANKS: NEITHER A BORROWER NOR LENDER BE Matthew Peterson Chief Wealth Strategist, LPL Financial KEY TAKEAWAYS Banks everywhere are under pressure

OEE Insights N 3. November In this issue. Long-run saving and monetary policy Peter Praet, Member of the Executive Board of the ECB

OEE Insights N 3 November 2016 In this issue Long-run saving and monetary policy Peter Praet, Member of the Executive Board of the ECB Consequences of present Euro area monetary policy on savings and capital

OEE Insights N 3 November 2016 In this issue Long-run saving and monetary policy Peter Praet, Member of the Executive Board of the ECB Consequences of present Euro area monetary policy on savings and capital

FINANCE & DEVELOPMENT

CLIMBI OUT OF DEBT 6 FINANCE & DEVELOPMENT March 2018 NG A new study offers more evidence that cutting spending is less harmful to growth than raising taxes Alberto Alesina, Carlo A. Favero, and Francesco

CLIMBI OUT OF DEBT 6 FINANCE & DEVELOPMENT March 2018 NG A new study offers more evidence that cutting spending is less harmful to growth than raising taxes Alberto Alesina, Carlo A. Favero, and Francesco

remain the same until the end of 2018.

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Global MT outlook: Will the crisis in emerging markets derail the recovery?

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Germany: Thrifty and risk averse

ECONOMIC RESEARCH DEPARTMENT Germany: Thrifty and risk averse High savings by households and enterprises pushed the current account surplus to 8.6% of GDP in 2015, a new historical high. The rise in household

ECONOMIC RESEARCH DEPARTMENT Germany: Thrifty and risk averse High savings by households and enterprises pushed the current account surplus to 8.6% of GDP in 2015, a new historical high. The rise in household

2Q16. Don t Be So Negative. June Uncharted territory

2Q16 TOPICS OF INTEREST Don t Be So Negative June 2016 ANDREW AKERS Analyst Following the financial crisis of 2008, slow global growth and low inflation have prompted a number of central banks to implement

2Q16 TOPICS OF INTEREST Don t Be So Negative June 2016 ANDREW AKERS Analyst Following the financial crisis of 2008, slow global growth and low inflation have prompted a number of central banks to implement

Macro vulnerabilities, regulatory reforms and financial stability issues IIF Spring Meeting

25.05.2016 Macro vulnerabilities, regulatory reforms and financial stability issues IIF Spring Meeting Luis M. Linde Governor I would like to thank Tim Adams, President and Chief Executive Officer of

25.05.2016 Macro vulnerabilities, regulatory reforms and financial stability issues IIF Spring Meeting Luis M. Linde Governor I would like to thank Tim Adams, President and Chief Executive Officer of

A prolonged period of low real interest rates? 1

A prolonged period of low real interest rates? 1 Olivier J Blanchard, Davide Furceri and Andrea Pescatori International Monetary Fund From a peak of about 5% in 1986, the world real interest rate fell

A prolonged period of low real interest rates? 1 Olivier J Blanchard, Davide Furceri and Andrea Pescatori International Monetary Fund From a peak of about 5% in 1986, the world real interest rate fell

II. Underlying domestic macroeconomic imbalances fuelled current account deficits

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

PRIVATE BANK INVESTMENT LETTER 1 ST QUARTER 2015 EDMOND DE ROTHSCHILD (MONACO)

") PRIVATE BANK INVESTMENT LETTER 1 ST QUARTER 2015 Monaco, 30th March, 2015 Lenin was right «By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of

PRIVATE BANK INVESTMENT LETTER 1 ST QUARTER 2015 Monaco, 30th March, 2015 Lenin was right «By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of

EXCHANGE RATES AMONG KEY CURRENCIES (Prague IIF September 2000)

") 24/9/2000 EXCHANGE RATES AMONG KEY CURRENCIES (Prague IIF September 2000) INTRODUCTION Under the Bretton Woods System, the assessment of the «right» bilateral exchange rates was, in principle, made relatively

24/9/2000 EXCHANGE RATES AMONG KEY CURRENCIES (Prague IIF September 2000) INTRODUCTION Under the Bretton Woods System, the assessment of the «right» bilateral exchange rates was, in principle, made relatively

THE FUTURE OF THE EUROPEAN BANKING SYSTEM

THE FUTURE OF THE EUROPEAN BANKING SYSTEM I am particularly happy to be invited by the ESM to give my thoughts on the future of the European banking system. The creation of the ESM is in itself a major

THE FUTURE OF THE EUROPEAN BANKING SYSTEM I am particularly happy to be invited by the ESM to give my thoughts on the future of the European banking system. The creation of the ESM is in itself a major

The future of the euro zone

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

Negative Rates: Staying Comfortable Below Zero

Below is the latest commentary from Pacific Life Fund Advisors LLC, the investment adviser to Pacific Funds SM. Negative Rates: Staying Comfortable Below Zero Negative interest rates are a new and untested

Below is the latest commentary from Pacific Life Fund Advisors LLC, the investment adviser to Pacific Funds SM. Negative Rates: Staying Comfortable Below Zero Negative interest rates are a new and untested

The strength of the Euro

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY The strength of the Euro IN-DEPTH ANALYSIS Abstract This paper discusses the challenges of euro-area monetary

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY The strength of the Euro IN-DEPTH ANALYSIS Abstract This paper discusses the challenges of euro-area monetary

International Money and Banking: 14. Real Interest Rates, Lower Bounds and Quantitative Easing

International Money and Banking: 14. Real Interest Rates, Lower Bounds and Quantitative Easing Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Real Interest Rates Spring 2018 1 / 23

International Money and Banking: 14. Real Interest Rates, Lower Bounds and Quantitative Easing Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Real Interest Rates Spring 2018 1 / 23

Bretton Woods and the IMS in a Multipolar World? Keynote Speech

Jacques de Larosière Former Managing Director International Monetary Fund I would like to thank the organizers of this conference for having asked so many eminent experts to focus on a subject the International

Jacques de Larosière Former Managing Director International Monetary Fund I would like to thank the organizers of this conference for having asked so many eminent experts to focus on a subject the International

Eurozone Economy Update

MACRO REPORT Eurozone Economy Update September 2015 Key Insights Monica Defend Head of Global Asset Allocation Research Andrea Brasili Senior Economist Global Asset Allocation Research Also contributing

MACRO REPORT Eurozone Economy Update September 2015 Key Insights Monica Defend Head of Global Asset Allocation Research Andrea Brasili Senior Economist Global Asset Allocation Research Also contributing

Bruno Desgardins 22 December 2018

Bruno Desgardins 22 December 2018 "If you don't take change by the hand, it will take you by the throat", Churchill. Before publishing our 2019 outlook for the global economy and markets in a few days'

Bruno Desgardins 22 December 2018 "If you don't take change by the hand, it will take you by the throat", Churchill. Before publishing our 2019 outlook for the global economy and markets in a few days'

Implications of Negative Interest Rates on Retirement Plans Tracey M. Manzi, CFA Vice President, Investment Services, Cammack Retirement Group

Implications of Negative Interest Rates on Retirement Plans Tracey M. Manzi, CFA Vice President, Investment Services, Cammack Retirement Group A few short years ago, the idea of a country having negative

Implications of Negative Interest Rates on Retirement Plans Tracey M. Manzi, CFA Vice President, Investment Services, Cammack Retirement Group A few short years ago, the idea of a country having negative

What s Holding Back the World Economy?

ECONOMICS JOSEPH E. STIGLITZ Joseph E. Stiglitz, recipient of the Nobel Memorial Prize in Economic Sciences in 2001 and the John Bates Clark Medal in 1979, is University Professor at Columbia University,

ECONOMICS JOSEPH E. STIGLITZ Joseph E. Stiglitz, recipient of the Nobel Memorial Prize in Economic Sciences in 2001 and the John Bates Clark Medal in 1979, is University Professor at Columbia University,

Managing the Fragility of the Eurozone. Paul De Grauwe London School of Economics

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

ILO World of Work Report 2013: EU Snapshot

Greece Spain Ireland Poland Belgium Portugal Eurozone France Slovenia EU-27 Cyprus Denmark Netherlands Italy Bulgaria Slovakia Romania Lithuania Latvia Czech Republic Estonia Finland United Kingdom Sweden

Greece Spain Ireland Poland Belgium Portugal Eurozone France Slovenia EU-27 Cyprus Denmark Netherlands Italy Bulgaria Slovakia Romania Lithuania Latvia Czech Republic Estonia Finland United Kingdom Sweden

Haruhiko Kuroda: How to overcome deflation

Haruhiko Kuroda: How to overcome deflation Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a conference, held by the London School of Economics and Political Science, London, 21 March 2014.

Haruhiko Kuroda: How to overcome deflation Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a conference, held by the London School of Economics and Political Science, London, 21 March 2014.

How costly is for Spain to be in the EURO?

How costly is for to be in the EURO? Are members of a monetary Union fatally handicapped to recover from recessions and solve financial crisis? By Domingo Cavallo 1 Countries with a long history of low

How costly is for to be in the EURO? Are members of a monetary Union fatally handicapped to recover from recessions and solve financial crisis? By Domingo Cavallo 1 Countries with a long history of low

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

Economic Outlook August 2017

Economic Outlook August 2017 Philippe WAECHTER Directeur de la Recherche Economique Compte Twitter: @phil_waechter ou http://twitter.com/phil_waechter SoundCloud http://soundcloud.com/phil_waechter Blog:

Economic Outlook August 2017 Philippe WAECHTER Directeur de la Recherche Economique Compte Twitter: @phil_waechter ou http://twitter.com/phil_waechter SoundCloud http://soundcloud.com/phil_waechter Blog:

Economic and financial outlook

Economic and financial outlook SEPTEMBER 2014 LAZARD FRÈRES GESTION SAS 25, rue de Courcelles 75008 Paris Sales department: +33 (0)1 44 13 01 94 - www.lazardfreresgestion.es ECONOMIC OUTLOOK 3 10 19 23

Economic and financial outlook SEPTEMBER 2014 LAZARD FRÈRES GESTION SAS 25, rue de Courcelles 75008 Paris Sales department: +33 (0)1 44 13 01 94 - www.lazardfreresgestion.es ECONOMIC OUTLOOK 3 10 19 23

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

European Public Debt: A Solution to Fragility

Workshop Discussion Material European Public Debt: A Solution to Fragility 1. Moral Hazard within EUM The establishment of an economic and monetary union generates benefits in terms of microeconomic efficiencies,

Workshop Discussion Material European Public Debt: A Solution to Fragility 1. Moral Hazard within EUM The establishment of an economic and monetary union generates benefits in terms of microeconomic efficiencies,

Negative interest rates: outcomes and consequences

Negative interest rates: outcomes and consequences Pavel Štěpánek Eva Zamrazilová Czech Banking Association Fiscal and monetary policy: between Scylla and Charybdis? Prague, May 20, 2016 Presentation framework

Negative interest rates: outcomes and consequences Pavel Štěpánek Eva Zamrazilová Czech Banking Association Fiscal and monetary policy: between Scylla and Charybdis? Prague, May 20, 2016 Presentation framework

The Celtic Tiger Roars

To: The Central Bank of Ireland From: Jeffrey Aronoff, Madeleine Findley, Sharon Dolente, and Steph Wasson Date: 4/17/02 Re: The Economic Outlook of Ireland In recent years, Ireland acquired the distinction

To: The Central Bank of Ireland From: Jeffrey Aronoff, Madeleine Findley, Sharon Dolente, and Steph Wasson Date: 4/17/02 Re: The Economic Outlook of Ireland In recent years, Ireland acquired the distinction

Global Imbalances, Currency Wars and the Euro

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICIES ECONOMIC AND MONETARY AFFAIRS Global Imbalances, Currency Wars and the Euro NOTE Abstract Global current

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICIES ECONOMIC AND MONETARY AFFAIRS Global Imbalances, Currency Wars and the Euro NOTE Abstract Global current

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

Hong Kong s Fiscal Issues

(Reprinted from HKCER Letters, Vol. 64, March/April 2001) Hong Kong s Fiscal Issues Y.C. Richard Wong Is There a Structural Budget Deficit in Hong Kong? Government officials have expressed concerns about

(Reprinted from HKCER Letters, Vol. 64, March/April 2001) Hong Kong s Fiscal Issues Y.C. Richard Wong Is There a Structural Budget Deficit in Hong Kong? Government officials have expressed concerns about

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Household Balance Sheets and Debt an International Country Study

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

Gold vs. Bonds: Another Look

PRECIOUS METALS INVESTING BMG ARTICLES Real Gold vs. A Promise of Gold 1 Gold vs. Bonds: Another Look July 2015 By Nick Barisheff I n the past, we have highlighted the advantages of using gold rather than

PRECIOUS METALS INVESTING BMG ARTICLES Real Gold vs. A Promise of Gold 1 Gold vs. Bonds: Another Look July 2015 By Nick Barisheff I n the past, we have highlighted the advantages of using gold rather than

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

The challenges to the Spanish banking industry

05.10.2018 The challenges to the Spanish banking industry Conference on banking, profitability and monetary normalisation /Universidad de Deusto, KPMG and El Correo Pablo Hernández de Cos Governor Good

05.10.2018 The challenges to the Spanish banking industry Conference on banking, profitability and monetary normalisation /Universidad de Deusto, KPMG and El Correo Pablo Hernández de Cos Governor Good

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies?

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Postponed recovery. The advanced economies posted a sluggish growth in CONJONCTURE IN FRANCE OCTOBER 2014 INSEE CONJONCTURE

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

On the Structure of EU Financial System. by S. E. G. Lolos. Contents 1

On the Structure of EU Financial System by S. E. G. Lolos Department of Economic and Regional Development Panteion University Contents 1 1. Introduction...2 2. Banks Balance Sheets...2 2.1 On the asset

On the Structure of EU Financial System by S. E. G. Lolos Department of Economic and Regional Development Panteion University Contents 1 1. Introduction...2 2. Banks Balance Sheets...2 2.1 On the asset

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

The role of central banks and governments in the crisis

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

From the financial crisis to the public debt crisis. Some considerations on the Italian Case

8th ESDN Workshop Brussels, 22-23 November 2012 From the financial crisis to the public debt crisis. Some considerations on the Italian Case Stefania P. S. Rossi Department of Economics University of Cagliari,

8th ESDN Workshop Brussels, 22-23 November 2012 From the financial crisis to the public debt crisis. Some considerations on the Italian Case Stefania P. S. Rossi Department of Economics University of Cagliari,

ANNUAL REPORT 2015 CHAPTER 2 COMPETITIVE ADJUSTMENT AND RECOVERY IN THE SPANISH ECONOMY DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

ANNUAL REPORT 215 CHAPTER 2 COMPETITIVE ADJUSTMENT AND RECOVERY IN THE SPANISH ECONOMY THE RECOVERY IN COMPETITIVENESS There has been a significant improvement in price/cost competitiveness since 28, although

ANNUAL REPORT 215 CHAPTER 2 COMPETITIVE ADJUSTMENT AND RECOVERY IN THE SPANISH ECONOMY THE RECOVERY IN COMPETITIVENESS There has been a significant improvement in price/cost competitiveness since 28, although

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

BCC UK Economic Forecast Q4 2015

BCC UK Economic Forecast Q4 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and

BCC UK Economic Forecast Q4 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and

Usable Productivity Growth in the United States

Usable Productivity Growth in the United States An International Comparison, 1980 2005 Dean Baker and David Rosnick June 2007 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite

Usable Productivity Growth in the United States An International Comparison, 1980 2005 Dean Baker and David Rosnick June 2007 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite

Immediate Gratification

In an effort to reignite world economic growth, global central banks have introduced unorthodox policies that have distorted market prices. The following discussion highlights the risks investors face.

In an effort to reignite world economic growth, global central banks have introduced unorthodox policies that have distorted market prices. The following discussion highlights the risks investors face.

Monetary Policy since the Global Financial Crisis. Philip Arestis University of Cambridge, UK, and University of the Basque Country, Spain

Monetary Policy since the Global Financial Crisis Philip Arestis University of Cambridge, UK, and University of the Basque Country, Spain Introduction The focus of this contribution is on monetary policy

Monetary Policy since the Global Financial Crisis Philip Arestis University of Cambridge, UK, and University of the Basque Country, Spain Introduction The focus of this contribution is on monetary policy

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Session 8. Business Cycles in a Closed Economy.

Session 8. Business Cycles in a Closed Economy. Building a Model of Aggregate Demand Money Market: The LM Curve Goods Market: The IS Curve A Graphical Representation of the Equilibrium: The IS/LM Model

Session 8. Business Cycles in a Closed Economy. Building a Model of Aggregate Demand Money Market: The LM Curve Goods Market: The IS Curve A Graphical Representation of the Equilibrium: The IS/LM Model

Making the Eurozone sustainable Paul De Grauwe

index 2000=100 Making the Eurozone sustainable Paul De Grauwe The election of Emmanuel Macron to the French Presidency creates new opportunities for taking initiatives that will ensure, first, that the

index 2000=100 Making the Eurozone sustainable Paul De Grauwe The election of Emmanuel Macron to the French Presidency creates new opportunities for taking initiatives that will ensure, first, that the

Policy Brief March 15, Debate on Euro Area ASTRID, 15 MARCH 2018

Policy Brief March 15, 2018 Debate on Euro Area Governance ASTRID, 15 MARCH 2018 COMMENTS ON CERP PI NO. 91 BY STEFANO MICOSSI PREMISE n.1 : the euro area suffers from a special disease entailing a continuing

Policy Brief March 15, 2018 Debate on Euro Area Governance ASTRID, 15 MARCH 2018 COMMENTS ON CERP PI NO. 91 BY STEFANO MICOSSI PREMISE n.1 : the euro area suffers from a special disease entailing a continuing

Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016.

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

Ranking Country Page. Category 1: Countries with positive CEP Default Index and positive NTE. 1 Estonia 1. 2 Luxembourg 2.

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

Chapter 10. Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics. Chapter Preview

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Financial Stability in a World of Very Low Interest Rates

43rd General Assembly of The Geneva Association Financial Stability in a World of Very Low Interest Rates Keynote speech by Ignazio Visco Governor of the Bank of Italy Rome, 9 June 2016 Since the 1980s

43rd General Assembly of The Geneva Association Financial Stability in a World of Very Low Interest Rates Keynote speech by Ignazio Visco Governor of the Bank of Italy Rome, 9 June 2016 Since the 1980s

REMARKS ON THE EVOLUTION OF THE INTERNATIONAL FINANCIAL SYSTEM. As I recall, in the sixties and seventies, one used to stress :

September 1999 REMARKS ON THE EVOLUTION OF THE INTERNATIONAL FINANCIAL SYSTEM PRESENTATION BY MR. DE LAROSIÈRE, ADVISOR TO PARIBAS, FOR THE MEETING ORGANIZED BY JONES, DAY, REAVIS & POGUE, IN WASHINGTON,

September 1999 REMARKS ON THE EVOLUTION OF THE INTERNATIONAL FINANCIAL SYSTEM PRESENTATION BY MR. DE LAROSIÈRE, ADVISOR TO PARIBAS, FOR THE MEETING ORGANIZED BY JONES, DAY, REAVIS & POGUE, IN WASHINGTON,

Yves Mersch: Monetary policy and economic inequality

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

External debt statistics of the euro area

External debt statistics of the euro area Jorge Diz Dias 1 1. Introduction Based on newly compiled data recently released by the European Central Bank (ECB), this paper reviews the latest developments

External debt statistics of the euro area Jorge Diz Dias 1 1. Introduction Based on newly compiled data recently released by the European Central Bank (ECB), this paper reviews the latest developments

Working Paper 209 M A C R O E C O N O M I C S F I N A N C I A L M A R K E T S E C O N O M I C P O L I C Y S E C T O R S

ECONOMIC RESEARCH Working Paper 209 July 4, 2017 M A C R O E C O N O M I C S F I N A N C I A L M A R K E T S E C O N O M I C P O L I C Y S E C T O R S Dr. Rolf Schneider, Jacqueline Seufert Impact of monetary

ECONOMIC RESEARCH Working Paper 209 July 4, 2017 M A C R O E C O N O M I C S F I N A N C I A L M A R K E T S E C O N O M I C P O L I C Y S E C T O R S Dr. Rolf Schneider, Jacqueline Seufert Impact of monetary

European Investment Fund Industry in 2013 p. 44. Net Assets under Management in Luxembourg Funds p. 46

statistics European Investment Fund Industry in 2013 p. 44 Net Assets under Management in Luxembourg Funds p. 46 Growth Factors in Luxembourg Investment Funds p. 47 Number of Luxembourg Investment Funds

statistics European Investment Fund Industry in 2013 p. 44 Net Assets under Management in Luxembourg Funds p. 46 Growth Factors in Luxembourg Investment Funds p. 47 Number of Luxembourg Investment Funds

The ECB and The Fed. How Did They React to the Crisis? Executive Director Monetary and Statistics Department. 11 July 2012, Prague

The ECB and The Fed How Did They React to the Crisis? Tomáš Holub Executive Director Monetary and Statistics Department 11 July 2012, Prague Outline Interest rate response to the crisis Unconventional

The ECB and The Fed How Did They React to the Crisis? Tomáš Holub Executive Director Monetary and Statistics Department 11 July 2012, Prague Outline Interest rate response to the crisis Unconventional

THE SPANISH ECONOMY: FACTS THAT CANNOT BE OVERLOOKED

THE SPANISH ECONOMY: FACTS THAT CANNOT BE OVERLOOKED Luis de Guindos Minister of Economy and Competitiveness 6 September 2012 Accumulated Imbalances of the Spanish Economy 1. Private sector indebtedness

THE SPANISH ECONOMY: FACTS THAT CANNOT BE OVERLOOKED Luis de Guindos Minister of Economy and Competitiveness 6 September 2012 Accumulated Imbalances of the Spanish Economy 1. Private sector indebtedness

Lecture 17. The Financial Markets and the Euro

Lecture 17 The Financial Markets and the Euro The Potential Role of the Euro Euro area EU USA Population in 2003 (million) 309 383 291 GDP ( billion) 7.298 9.458 11.035 Stock market capitalization 2002

Lecture 17 The Financial Markets and the Euro The Potential Role of the Euro Euro area EU USA Population in 2003 (million) 309 383 291 GDP ( billion) 7.298 9.458 11.035 Stock market capitalization 2002

Professor Claudia M Buch Vice-President of the Deutsche Bundesbank. Speech at the presentation of the Financial Stability Review

Professor Claudia M Buch Vice-President of the Deutsche Bundesbank Speech at the presentation of the 2017 Financial Stability Review of the Deutsche Bundesbank in Frankfurt am Main Wednesday, 29 November

Professor Claudia M Buch Vice-President of the Deutsche Bundesbank Speech at the presentation of the 2017 Financial Stability Review of the Deutsche Bundesbank in Frankfurt am Main Wednesday, 29 November

MCCI ECONOMIC OUTLOOK. Novembre 2017

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

1 World Economy. Value of Finnish Forest Industry Exports Fell by Almost a Quarter in 2009

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

Working Paper. A fundamental interest rate explanation and forecast. July 3, Economic Research & Corporate Development. Dr.

Spezialthemen Working Paper / Nr. 114 / 21.08.2008 Economic Research & Corporate Development Working Paper 130 July 3, 2009 MAcroeconomics Financial markets economic policy sectors Dr. Rolf Schneider A

Spezialthemen Working Paper / Nr. 114 / 21.08.2008 Economic Research & Corporate Development Working Paper 130 July 3, 2009 MAcroeconomics Financial markets economic policy sectors Dr. Rolf Schneider A

Fund Management Diary

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

International Environment Economics for Business (IEEB)

") International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

continue to foster, the deterioration of the U.S. currency in the world markets. This includes America s appetite for

consequences Americans are facing because of the dollar s free fall in value. Implications of the United State s current dollar. In addition, a potential remedy is presented and includes the formation

consequences Americans are facing because of the dollar s free fall in value. Implications of the United State s current dollar. In addition, a potential remedy is presented and includes the formation

Presentation. The Boom in Capital Flows and Financial Vulnerability in Asia

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

Gundlach: Treasuries will Rally When QE2 Ends

Gundlach: Treasuries will Rally When QE2 Ends April 19, 2011 by Robert Huebscher The bonds that PIMCO s Bill Gross sold to take a 3% short position in the Treasury market may have found a buyer in Doubleline

Gundlach: Treasuries will Rally When QE2 Ends April 19, 2011 by Robert Huebscher The bonds that PIMCO s Bill Gross sold to take a 3% short position in the Treasury market may have found a buyer in Doubleline

real B. These developments suggest two tentative conclusions. nominal

Page 1 sur 6 First ESRB annual conference 23 September 2016 Speech by François Villeroy de Galhau, Governor of the Banque de France Low interest rates and the implications for financial stability The question

Page 1 sur 6 First ESRB annual conference 23 September 2016 Speech by François Villeroy de Galhau, Governor of the Banque de France Low interest rates and the implications for financial stability The question

Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

Quarterly Macro Report

Quarterly Macro Report 3rd Quarter 218 Even though forward-looking indicators for the industrialized countries still point to an acceleration of growth, the outlook for the global economy has deteriorated

Quarterly Macro Report 3rd Quarter 218 Even though forward-looking indicators for the industrialized countries still point to an acceleration of growth, the outlook for the global economy has deteriorated

Greece and the Eurozone: Background, Context, and Prospects

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE. Paul De Grauwe (LSE) Yuemei Ji (Brunel University)

Yuemei Ji (Brunel University)") CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE Paul De Grauwe (LSE) Yuemei Ji (Brunel University) Stagnation in Eurozone Figure 1: Real GDP in Eurozone, EU10 and US (prices of 2010) 135 130 125

CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE Paul De Grauwe (LSE) Yuemei Ji (Brunel University) Stagnation in Eurozone Figure 1: Real GDP in Eurozone, EU10 and US (prices of 2010) 135 130 125

Forces and threats to Mexico s economic recovery. Remarks by. Manuel Sánchez. at the. New York, N.Y.

Forces and threats to Mexico s economic recovery Remarks by Manuel Sánchez Member of the Governing Board of the Bank of Mexico at the The United States Mexico Chamber of Commerce New York, N.Y. September

Forces and threats to Mexico s economic recovery Remarks by Manuel Sánchez Member of the Governing Board of the Bank of Mexico at the The United States Mexico Chamber of Commerce New York, N.Y. September

Petrodollars, the Savings Bust, and the U.S. Current Account Deficit

GLOBAL PERSPECTIVES Petrodollars, the Savings Bust, and the U.S. Current Account Deficit March 2007 International finance is a fascinating but challenging subject with many moving Richard H. Clarida Global

GLOBAL PERSPECTIVES Petrodollars, the Savings Bust, and the U.S. Current Account Deficit March 2007 International finance is a fascinating but challenging subject with many moving Richard H. Clarida Global

The Artificial Economic Recovery

VOLUME 2.10 JULY 23, 2010 The Artificial Economic Recovery Economic recovery in the U.S. and elsewhere has slowed rapidly and private and some public forecasts are being downgraded accordingly. The Federal

VOLUME 2.10 JULY 23, 2010 The Artificial Economic Recovery Economic recovery in the U.S. and elsewhere has slowed rapidly and private and some public forecasts are being downgraded accordingly. The Federal

Spanish economic outlook. June 2017

Spanish economic outlook June 2017 1 2 3 Spanish economy a pleasant surprise Growth drivers Forecasts once again bright One of the most dynamic economies in Europe Spain growing at a faster rate than EMU

Spanish economic outlook June 2017 1 2 3 Spanish economy a pleasant surprise Growth drivers Forecasts once again bright One of the most dynamic economies in Europe Spain growing at a faster rate than EMU

Crisis, Threats and Ways Out for the Greek Economy

Cyprus Economic Policy Review, Vol. 4, No. 1, pp. 89-96 (2010) 1450-4561 Crisis, Threats and Ways Out for the Greek Economy Nicos Christodoulakis Athens University of Economics and Business Abstract The

Cyprus Economic Policy Review, Vol. 4, No. 1, pp. 89-96 (2010) 1450-4561 Crisis, Threats and Ways Out for the Greek Economy Nicos Christodoulakis Athens University of Economics and Business Abstract The

Whatever It Takes 2.0?

Whatever It Takes 2.0? April 9, 2014 by Axel Merk of Merk Investments If you are convincingly irrational the market may expect extreme measures and front run your bluff. It s in this spirit that ECB President

Whatever It Takes 2.0? April 9, 2014 by Axel Merk of Merk Investments If you are convincingly irrational the market may expect extreme measures and front run your bluff. It s in this spirit that ECB President

Monetary policy using negative interest rates: a status report Vereinigung Basler Ökonomen

Speech Embargo 24 October 2016, 6.15 pm Monetary policy using negative interest rates: a status report Vereinigung Basler Ökonomen Thomas Jordan Chairman of the Governing Board Swiss National Bank Basel,

Speech Embargo 24 October 2016, 6.15 pm Monetary policy using negative interest rates: a status report Vereinigung Basler Ökonomen Thomas Jordan Chairman of the Governing Board Swiss National Bank Basel,

The outlook for the global economy in 2012

The Eurozone Crisis Still Threatens Global Growth Paolo Guerrieri Professor of Economics, University of Rome Sapienza; Professor, College of Europe, Bruges The outlook for the global economy in 2012 is

The Eurozone Crisis Still Threatens Global Growth Paolo Guerrieri Professor of Economics, University of Rome Sapienza; Professor, College of Europe, Bruges The outlook for the global economy in 2012 is

Panel Discussion: Europe at the Crossroads

Panel Discussion: Europe at the Crossroads Markus Brunnermeier Paul Krugman Hyun Song Shin Christopher Sims October 24th, 2011 Department of Economics and Griswold Center for Economic Policy Studies 1

Panel Discussion: Europe at the Crossroads Markus Brunnermeier Paul Krugman Hyun Song Shin Christopher Sims October 24th, 2011 Department of Economics and Griswold Center for Economic Policy Studies 1

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

1.1. Low yield environment

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public