Can the Euro Survive?

|

|

|

- Vernon Butler

- 5 years ago

- Views:

Transcription

1 Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon

2 Sovereign Debt Crisis Market participants tend to focus on yield spread between country s bonds and German Bund as indicator of stress in market for sovereign debt Prior to 1999, yields on 10 year bonds offered by PIIGS typically much higher Reflected expectations of financial markets about risks associated with inflation and exchange rate depreciation in PIIGS None of PIIGS had independent central banks committed to targeting inflation, and all had currencies that could be allowed to depreciate

3 Europhoria Between 2001 and onset of financial crisis, 10- year bond yields of the PIIGS relative to the Bund often less than 20 basis points Either markets believed fiscally-responsible members of euro area would discipline less fiscally-responsible Or there were expectations that risk-pooling would work via cross-border bailouts or sovereign bailouts by ECB With onset of financial crisis, yield spreads for PIIGS opened up, i.e., expectation of default

4 PIGS can t fly! Figure 1: 10-Year Sovereign Bond Yields in Euro Area, Source: Eurostat

5 Euro crisis: a drama with 4 actors Mismanagement and deception by Greek authorities October 2009, budget deficit revealed to be 12.7% of GDP not 6% Having failed to forecast Dubai sovereign debt crisis, ratings agencies focused not only on Greece, but other Eurozone countries downgrading led to increased yield spreads Hesitation among Eurozone governments in giving clear signal of support to Greece ECB generated uncertainty about willingness to accept Greek bonds as collateral

6 Was it all about public debt? Other than Greece, root cause of debt problem was unsustainable accumulation of private compared to public debt Triggered debt-deflation dynamic, forcing governments to take over private debt Prior to 2008, debt/gdp ratios of several Eurozone countries were actually declining notably Ireland and Spain As austerity measures have been implemented, deleveraging of private sector has become harder, with potential for further deflation

")

7 Eurozone debt Government debt in selected Eurozone countries (% of GDP) FRANCE GERMANY GREECE IRELAND ITALY PORTUGAL SPAIN 20 0 Source: IMF (2011)

8 A paradox After start of financial crisis, government debt ratio in UK increased by more than in Spain, i.e., 89% vs. 72% of GDP Yet yield on Spanish bonds increased strongly relative to UK bonds Why such difference in evaluation of sovereign default risks between Spain and UK? Achilles heel of monetary union such as Eurozone: Spain has no control over currency in which it issues its debt

9 Spain vs. UK

10 Pain and misery If investors have concerns over default in Spain, interest rates rise as bonds are sold Euros leave Spanish banking system, and liquidity crisis occurs as cost of rolling over Spanish debt increases sudden stop Also, Spanish economy cannot get boost from currency depreciation Fear of default in Spain becomes self-fulfilling prophecy as liquidity crisis turns into solvency crisis - risk of contagion elsewhere

Cost of not acting as lender of last resort in EU bond markets was potential for more costly bailout of its")

11 Avoiding bad equilibria ECB should have acted as lender of last resort Prevents solvent countries such as Spain being pushed into bad equilibrium, i.e., resolves coordination failure Coordination failure due to rational expectations, i.e., fear of insufficient liquidity results in insufficient liquidity for country(ies) Cost of not acting as lender of last resort in EU bond markets was potential for more costly bailout of its banking system

12 EU bank liabilities EU bank liabilities as % of GDP Source: IMF (2008)

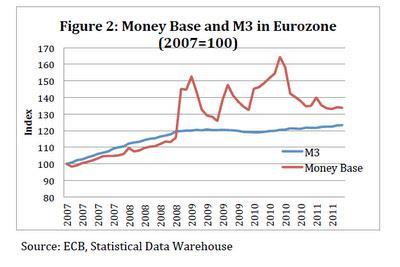

13 Arguments against ECB Risk of inflation? Money base vs. stock Fiscal consequences? Risk should be taken to ensure financial stability in EU Moral hazard? Need to separate role of insurance from fiscal supervision Bagehot doctrine? Only lend in case of illiquidity not insolvency but with uncertainty ECB is necessary Legal? ECB allowed to purchase bonds in secondary market, i.e., it can provide liquidity

14 Money base vs. stock

first year at 40-50% of GDP, 15%/annum thereafter - core country (Germany): first-year at 20-25% of GDP, 11%/annum thereafter Costs")

15 What if Euro collapses? UBS have estimated costs of collapse: - peripheral country (Greece) first year at 40-50% of GDP, 15%/annum thereafter - core country (Germany): first-year at 20-25% of GDP, 11%/annum thereafter Costs of a rescue seem a bargain by comparison but German taxpayers would prefer to punish spendthrift Italians and Portuguese However, breakup of Eurozone, and possibly European Union, would be much worse

16 Can the Euro survive? Concern in Northern Europe is to not provide incentive for more irresponsible behavior by Club-Med countries This view treats crisis as series of individual problems as opposed to a systemic problem Illiquidity of single country becomes problem for whole Eurozone especially with financial market integration Reluctance of ECB to be lender of last resort in sovereign bond market has probably been key reason for contagion not being stopped earlier

17 Thoughts of Krugman.What s needed, clearly, is for Europe and ultimately that probably means the ECB to provide for Spain and Italy the kind of backstop countries with their own currencies can provide for themselves. Without that, the whole euro system is at risk of unraveling. (New York Times, September 11, 2011)

18 ECB finally does its job? In September 2012, ECB committed itself to unlimited support of bond markets Resulted in strong decline in spreads, e.g., January 2013, interest rate on Spanish 10- year bonds fell bellow 5% for first time in a year ECB never actually intervened, i.e., announcement reduced bond market sentiments of fear and panic Interestingly, bond spreads declined despite continued increase in debt/gdp ratios

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics A short history of capitalism Capitalism is wonderful human invention steering individual initiative and creativity

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics A short history of capitalism Capitalism is wonderful human invention steering individual initiative and creativity

Managing the Fragility of the Eurozone. Paul De Grauwe London School of Economics

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

What Governance for the Eurozone? Paul De Grauwe London School of Economics

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

Europe in crisis. George Gelauff. ECU 92 Lustrum Conference Utrecht. 23 February 2012

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Overcoming the crisis

Princeton, Oct 24 th, 2011 Overcoming the crisis backwards induction approach: 1. Diagnosis how did we get there? Run-up phase Crisis phase 2. Give long-run perspective Banking landscape (ESBies, European

Princeton, Oct 24 th, 2011 Overcoming the crisis backwards induction approach: 1. Diagnosis how did we get there? Run-up phase Crisis phase 2. Give long-run perspective Banking landscape (ESBies, European

How the Eurozone will be resolving its crisis

How the Eurozone will be resolving its crisis Wolfgang MÜNCHAU Eurointelligence ASBL The political economy of the Eurozone is based on three pillars: lies, loopholes and fudges. Back in the 1990s, its

How the Eurozone will be resolving its crisis Wolfgang MÜNCHAU Eurointelligence ASBL The political economy of the Eurozone is based on three pillars: lies, loopholes and fudges. Back in the 1990s, its

For the Eurozone, much hinges on self-discipline and self-interest

For the Eurozone, much hinges on self-discipline and self-interest Author: Jonathan Lemco, Ph.D. Will the Eurozone survive its severe financial challenges? Vanguard believes it is in the interests of both

For the Eurozone, much hinges on self-discipline and self-interest Author: Jonathan Lemco, Ph.D. Will the Eurozone survive its severe financial challenges? Vanguard believes it is in the interests of both

The European Economic Crisis

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

The Euro Zone Sovereign Debt Crisis: Testing the Limits of Solidarity. Presentation to the IA BE

IA BE The Euro Zone Sovereign Debt Crisis: Testing the Limits of Solidarity Presentation to the IA BE Jean Deboutte 14 June 2011 Table of Contents Section 1 Introduction Section 2 Diagnosis Section 3 Remedies

IA BE The Euro Zone Sovereign Debt Crisis: Testing the Limits of Solidarity Presentation to the IA BE Jean Deboutte 14 June 2011 Table of Contents Section 1 Introduction Section 2 Diagnosis Section 3 Remedies

Economic and Financial Affairs Committee. The EMU: challenges and the way forward

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Europe s Response to the Sovereign Debt Crisis. Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Member of

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

A Two-Handed Economist s Presentation on The Treaty. Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

Europe s Response to the Sovereign Debt Crisis. Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Banks and sovereign debt in Europe

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Eurozone Focus The Ongoing Saga Of Sovereign Debt

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 THE DEBT CRISIS IN GREECE AND THE EURO ZONE

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 April 2010 Prepared by: Sema Gençay ÇAPANOĞLU (scapanoglu@ikv.org.tr) THE DEBT CRISIS IN GREECE AND THE EURO ZONE Greece is struggling with the most serious

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 April 2010 Prepared by: Sema Gençay ÇAPANOĞLU (scapanoglu@ikv.org.tr) THE DEBT CRISIS IN GREECE AND THE EURO ZONE Greece is struggling with the most serious

Greece Facing an Uncertain Future

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

International financial crises

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

Eighth UNCTAD Debt Management Conference

Eighth UNCTAD Debt Management Conference Geneva, 14-16 November 2011 Debt Resolution Mechanisms: Should there be a Statutory Mechanism for Resolving Debt Crises? by Mr. Frank Moss Director General, International

Eighth UNCTAD Debt Management Conference Geneva, 14-16 November 2011 Debt Resolution Mechanisms: Should there be a Statutory Mechanism for Resolving Debt Crises? by Mr. Frank Moss Director General, International

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

CONDITIONAL EUROBONDS AND EUROZONE REFORM

CONDITIONAL EUROBONDS AND EUROZONE REFORM John Muellbauer, INET at Oxford OENB workshop Towards a genuine economic and monetary union, Vienna, 10-11 September, 2015 OBJECTIVES Reduce the Euro-area policy

CONDITIONAL EUROBONDS AND EUROZONE REFORM John Muellbauer, INET at Oxford OENB workshop Towards a genuine economic and monetary union, Vienna, 10-11 September, 2015 OBJECTIVES Reduce the Euro-area policy

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.

During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.") Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

The EU is running out of choices to tame the crisis

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

TOWARDS A MORE INTEGRATED AND STABLE EUROPE? National Bank of Poland

TOWARDS A MORE INTEGRATED AND STABLE EUROPE? National Bank of Poland by Daniel Gros Warsaw; October 2011 Key points 1. Background: global credit boom and excess leverage. 2. EMU system not designed to

TOWARDS A MORE INTEGRATED AND STABLE EUROPE? National Bank of Poland by Daniel Gros Warsaw; October 2011 Key points 1. Background: global credit boom and excess leverage. 2. EMU system not designed to

António Afonso, Jorge Silva Debt crisis and 10-year sovereign yields in Ireland and in Portugal

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

The European Central Bank as Lender of Last Resort in the Government Bond Markets

CESifo Economic Studies, Vol. 59, 3/2013, 520 535 doi:10.1093/cesifo/ift012 The European Central Bank as Lender of Last Resort in the Government Bond Markets Paul De Grauwe*,y *London School of Economics,

CESifo Economic Studies, Vol. 59, 3/2013, 520 535 doi:10.1093/cesifo/ift012 The European Central Bank as Lender of Last Resort in the Government Bond Markets Paul De Grauwe*,y *London School of Economics,

Can the Eurozone Reform?

Can the Eurozone Reform? by Economist Conference on: Governance and regional arteries for Growth: Europe s momentum Greece s impetus, Wyndham Loutraki Poseidon Resort, Greece, May 10-11, 2018 The Greek

Can the Eurozone Reform? by Economist Conference on: Governance and regional arteries for Growth: Europe s momentum Greece s impetus, Wyndham Loutraki Poseidon Resort, Greece, May 10-11, 2018 The Greek

The Lender of Last Resort in the Euro Area: Where Do We Stand?

The Lender of Last Resort in the Euro Area: Where Do We Stand? Karl Whelan University College Dublin Presentation at University College Cork March 9, 2018 Plan for this Talk Lender of last resort Rationale

The Lender of Last Resort in the Euro Area: Where Do We Stand? Karl Whelan University College Dublin Presentation at University College Cork March 9, 2018 Plan for this Talk Lender of last resort Rationale

Eurozone. Outlook for. Ernst & Young Eurozone Forecast. Summer edition 2012

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

Global Safe Assets. Pierre-Olivier Gourinchas (UC Berkeley, Sciences-Po) Olivier Jeanne (JHU, PIIE)

Olivier Jeanne (JHU, PIIE)") Pierre-Olivier Gourinchas (UC Berkeley, Sciences-Po) Olivier Jeanne (JHU, PIIE) International Conference on Capital Flows and Safe Assets May 26-27, 2013 Introduction Widespread concern that the global

Pierre-Olivier Gourinchas (UC Berkeley, Sciences-Po) Olivier Jeanne (JHU, PIIE) International Conference on Capital Flows and Safe Assets May 26-27, 2013 Introduction Widespread concern that the global

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA Ulrich Volz, German Development Institute 8 August 2012, United Nations Economic and Social Commission for Asia

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA Ulrich Volz, German Development Institute 8 August 2012, United Nations Economic and Social Commission for Asia

Deposit Flight From Europe Banks Eroding Common Currency

Deposit Flight From Europe Banks Eroding Common Currency An accelerating flight of deposits from banks in four European countries is jeopardizing the renewal of economic growth and undermining a main tenet

Deposit Flight From Europe Banks Eroding Common Currency An accelerating flight of deposits from banks in four European countries is jeopardizing the renewal of economic growth and undermining a main tenet

The Turbulent EMS in the 1990s: What Lessons for Today? Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel

The Turbulent in the 1990s: What Lessons for Today? André Sapir Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel 2 The turbulent 1990s: the incompatible trio July 1990: Full

The Turbulent in the 1990s: What Lessons for Today? André Sapir Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel 2 The turbulent 1990s: the incompatible trio July 1990: Full

EUROPE LEADS FLIGHT TO QUALITY

EUROPE LEADS FLIGHT TO QUALITY Our cautious stance has paid off this quarter as many of the risks we were concerned about have begun to play out. This has led to a flight to quality, which is where we

EUROPE LEADS FLIGHT TO QUALITY Our cautious stance has paid off this quarter as many of the risks we were concerned about have begun to play out. This has led to a flight to quality, which is where we

The Greek. Hans-Werner Sinn

CESifo, a Munich-based, globe-spanning economic research and policy advice institution Forum june 215 Special Issue - Update The Greek Tragedy Hans-Werner Sinn This document contains updated graphs and

CESifo, a Munich-based, globe-spanning economic research and policy advice institution Forum june 215 Special Issue - Update The Greek Tragedy Hans-Werner Sinn This document contains updated graphs and

Falling Short of Expectations? Stress-Testing the European Banking System

Falling Short of Expectations? Stress-Testing the European Banking System Viral V. Acharya (NYU Stern, CEPR and NBER) and Sascha Steffen (ESMT) January 2014 1 Falling Short of Expectations? Stress-Testing

Falling Short of Expectations? Stress-Testing the European Banking System Viral V. Acharya (NYU Stern, CEPR and NBER) and Sascha Steffen (ESMT) January 2014 1 Falling Short of Expectations? Stress-Testing

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

ECB LTRO Dec Greece program

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

In search of symmetry in the eurozone

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

From the financial crisis to the public debt crisis. Some considerations on the Italian Case

8th ESDN Workshop Brussels, 22-23 November 2012 From the financial crisis to the public debt crisis. Some considerations on the Italian Case Stefania P. S. Rossi Department of Economics University of Cagliari,

8th ESDN Workshop Brussels, 22-23 November 2012 From the financial crisis to the public debt crisis. Some considerations on the Italian Case Stefania P. S. Rossi Department of Economics University of Cagliari,

The IMF. Benjamin Graham

The IMF Benjamin Graham The IMF Benjamin Graham Housekeeping Brief Note: Why I assigned readings that are generally pro-imf Reading Quiz (1) Which of the following are true? a. The IMF stands for the International

The IMF Benjamin Graham The IMF Benjamin Graham Housekeeping Brief Note: Why I assigned readings that are generally pro-imf Reading Quiz (1) Which of the following are true? a. The IMF stands for the International

The Financial Crisis of ? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

Monetary Policy Responses to the Eurozone Crisis i

MONETARY POLICY RESPONSES TO THE EUROZONE CRISIS 1 Monetary Policy Responses to the Eurozone Crisis i Jihëd MEJRISSI Philipps-Universität Marburg Contents Abstract... 1 1. Introduction... 1 2. Monetary

MONETARY POLICY RESPONSES TO THE EUROZONE CRISIS 1 Monetary Policy Responses to the Eurozone Crisis i Jihëd MEJRISSI Philipps-Universität Marburg Contents Abstract... 1 1. Introduction... 1 2. Monetary

Global Debt Crisis & Impact on India. October 2011

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

Divergence and Adjustment in the Euro Area

MINISTÉRIO DAS FINANÇAS Divergence and Adjustment in the Euro Area Vítor Gaspar Frankfurt June 15, 2012 MINISTÉRIO DAS FINANÇAS 1 Outline 1. Credit Boom 2. Eliminating excessive debt 3. Challenges ahead

MINISTÉRIO DAS FINANÇAS Divergence and Adjustment in the Euro Area Vítor Gaspar Frankfurt June 15, 2012 MINISTÉRIO DAS FINANÇAS 1 Outline 1. Credit Boom 2. Eliminating excessive debt 3. Challenges ahead

Its dimensions and implications. MR Anand GL Gupta Ranjan Dash

Its dimensions and implications MR Anand GL Gupta Ranjan Dash Optimism and enthusiasm (1999-2007) soon replaced by pessimism and distrust (2009-11) General origins. 2 main causes, 1 anomaly. 2 causes:

Its dimensions and implications MR Anand GL Gupta Ranjan Dash Optimism and enthusiasm (1999-2007) soon replaced by pessimism and distrust (2009-11) General origins. 2 main causes, 1 anomaly. 2 causes:

Banking Union in Europe Glass Half Full or Glass Half Empty. Thorsten Beck

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

EURECA project. Hellenic Recovery Fund a solution for Greece and Europe

EURECA project Hellenic Recovery Fund a solution for Greece and Europe Frankfurt, September 2011 Preface The Greek solvency crisis in combination with speculative attacks on several euro zone countries

EURECA project Hellenic Recovery Fund a solution for Greece and Europe Frankfurt, September 2011 Preface The Greek solvency crisis in combination with speculative attacks on several euro zone countries

Wolfgang Münchau Associate Editor Financial Times and President of Eurointelligence

Associate Editor Financial Times and President of Eurointelligence How Much Risk Can a Central Bank Assume? I will not answer this question because it is essentially unanswerable in abstract. The more

Associate Editor Financial Times and President of Eurointelligence How Much Risk Can a Central Bank Assume? I will not answer this question because it is essentially unanswerable in abstract. The more

The Economics of the European Union

Fletcher School, Tufts University The Economics of the European Union Prof. George Alogoskoufis Lecture 21: The Eurozone Crisis, Why it Happened and Lessons for the Future Two Important Recent Reports

Fletcher School, Tufts University The Economics of the European Union Prof. George Alogoskoufis Lecture 21: The Eurozone Crisis, Why it Happened and Lessons for the Future Two Important Recent Reports

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011 Anthony B. Sanders Distinguished Professor of Real Estate Finance, George Mason University, and Senior Scholar, Mercatus

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011 Anthony B. Sanders Distinguished Professor of Real Estate Finance, George Mason University, and Senior Scholar, Mercatus

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Eurozone Ernst & Young Eurozone Forecast Summer edition June 2011

Eurozone Ernst & Young Eurozone Forecast Summer edition June 2011 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Eurozone Ernst & Young Eurozone Forecast Summer edition June 2011 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2012

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2012 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2012 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

The future of the euro zone

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

How Europe is Overcoming the Euro Crisis?

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

Research Euro area: debt crisis set to continue for years

Investment Research General Market Conditions 13 September 20 Research Euro area: debt crisis set to continue for years At the beginning of the year, we presented three debt crisis scenarios. In this document

Investment Research General Market Conditions 13 September 20 Research Euro area: debt crisis set to continue for years At the beginning of the year, we presented three debt crisis scenarios. In this document

Kenneth Matziorinis McGill School of Continuing Studies Canbek Economic Consultants Inc. 19 th Annual Canadian Security Traders Conference

Kenneth Matziorinis McGill School of Continuing Studies Canbek Economic Consultants Inc. 19 th Annual Canadian Security Traders Conference Manoir Saint Sauveur, Saint Sauveur, Quebec August 16, 2012 Why

Kenneth Matziorinis McGill School of Continuing Studies Canbek Economic Consultants Inc. 19 th Annual Canadian Security Traders Conference Manoir Saint Sauveur, Saint Sauveur, Quebec August 16, 2012 Why

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Portugal: economic adjustment and challenges ahead

Portugal: economic adjustment and challenges ahead Carlos da Silva Costa Governor Madrid, November 10 th 2015 Forum Europa Outline I. Adjustment of the Portuguese II. Lessons to be drawn III. Challenges

Portugal: economic adjustment and challenges ahead Carlos da Silva Costa Governor Madrid, November 10 th 2015 Forum Europa Outline I. Adjustment of the Portuguese II. Lessons to be drawn III. Challenges

Emerging from the Crisis

Emerging from the Crisis i Franklin Allen University of Pennsylvania Elena Carletti European University Institute Louvain-La-Neuve May 6, 2010 What caused the crisis? The conventional wisdom used to be

Emerging from the Crisis i Franklin Allen University of Pennsylvania Elena Carletti European University Institute Louvain-La-Neuve May 6, 2010 What caused the crisis? The conventional wisdom used to be

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

The Sovereign Debt Crisis in Ireland and Southern Europe

The Sovereign Debt Crisis in Ireland and Southern Europe The Political Origins and Economic Consequences of the Eurozone Week 8 Aidan Regan Introduction This week we will examine the sovereign debt crisis

The Sovereign Debt Crisis in Ireland and Southern Europe The Political Origins and Economic Consequences of the Eurozone Week 8 Aidan Regan Introduction This week we will examine the sovereign debt crisis

Department of Economics ECONOMIC OVERVIEW

Department of Economics ECONOMIC OVERVIEW January 2012 EDITORIAL Will the Euro Survive? By joining the euro, Europe s peripheral countries gained access to cheap, easy financing. They spent beyond their

Department of Economics ECONOMIC OVERVIEW January 2012 EDITORIAL Will the Euro Survive? By joining the euro, Europe s peripheral countries gained access to cheap, easy financing. They spent beyond their

Ranking Country Page. Category 1: Countries with positive CEP Default Index and positive NTE. 1 Estonia 1. 2 Luxembourg 2.

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

Midterm: Greece Debt Crisis

I. Introduction Greece s debt crisis of 2010 was triggered by high budget deficits that reached 13.6% of GDP 4 times the amount allowed by the EU and high national debt levels reaching 300bn, representing

I. Introduction Greece s debt crisis of 2010 was triggered by high budget deficits that reached 13.6% of GDP 4 times the amount allowed by the EU and high national debt levels reaching 300bn, representing

Greece and the Eurozone: Background, Context, and Prospects

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Balance Sheet Review. Shareholders equity increased by 8.6 bn to 53.6 bn. Strong solvency ratio up by 18 percentage points to 197 %.

Balance Sheet Review Shareholders equity increased by 8.6 bn to 53.6 bn. Strong solvency ratio up by 18 percentage points to 197 %.1 Shareholders equity 2 Shareholders equity C 057 mn 70,000 + 19.2 % 60,000

Balance Sheet Review Shareholders equity increased by 8.6 bn to 53.6 bn. Strong solvency ratio up by 18 percentage points to 197 %.1 Shareholders equity 2 Shareholders equity C 057 mn 70,000 + 19.2 % 60,000

Costly Reforms and Self-Fulfilling Crises

Costly Reforms and Self-Fulfilling Crises Juan Carlos Conesa Stony Brook Unniversity, Timothy J. Kehoe University of Minnesota and Federal Reserve Bank of Minneapolis Conference on Macroeconomic Theory

Costly Reforms and Self-Fulfilling Crises Juan Carlos Conesa Stony Brook Unniversity, Timothy J. Kehoe University of Minnesota and Federal Reserve Bank of Minneapolis Conference on Macroeconomic Theory

Chapter 8. Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

European Public Debt: A Solution to Fragility

Workshop Discussion Material European Public Debt: A Solution to Fragility 1. Moral Hazard within EUM The establishment of an economic and monetary union generates benefits in terms of microeconomic efficiencies,

Workshop Discussion Material European Public Debt: A Solution to Fragility 1. Moral Hazard within EUM The establishment of an economic and monetary union generates benefits in terms of microeconomic efficiencies,

I. Economic outlook. Economic outlook, challenges and policies. Setting the right course for economic policy

Setting the right course for economic policy Annual Report - German Council of Economic Experts Volker Wieland GCEE Member and IMFS, Goethe University Frankfurt Municipal Guarantee Board, Helsinki, December

Setting the right course for economic policy Annual Report - German Council of Economic Experts Volker Wieland GCEE Member and IMFS, Goethe University Frankfurt Municipal Guarantee Board, Helsinki, December

Q Economic Outlook

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Eurozone Ernst & Young Eurozone Forecast Autumn edition September 2011

Eurozone Ernst & Young Eurozone Forecast Autumn edition September 2011 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia

Eurozone Ernst & Young Eurozone Forecast Autumn edition September 2011 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia

* I am grateful to Daniel Gros, Martin Wolf and Charles Wyplosz for comments and suggestions

THE GOVERNANCE OF A FRAGILE EUROZONE Paul De Grauwe* University of Leuven and CEPS Abstract: When entering a monetary union, member- countries change the nature of their sovereign debt in a fundamental

THE GOVERNANCE OF A FRAGILE EUROZONE Paul De Grauwe* University of Leuven and CEPS Abstract: When entering a monetary union, member- countries change the nature of their sovereign debt in a fundamental

Themes in bond investing June 2009

For professional investors only Not for public distribution January 2011 Themes in bond investing June 2009 Introduction Eurozone sovereign risk concerns are back in the spotlight following the Irish bailout.

For professional investors only Not for public distribution January 2011 Themes in bond investing June 2009 Introduction Eurozone sovereign risk concerns are back in the spotlight following the Irish bailout.

To view this PDF as a projectable presentation, save the file, click view in the top menu bar, & select full screen mode. Upon completion of the

To view this PDF as a projectable presentation, save the file, click view in the top menu bar, & select full screen mode. Upon completion of the presentation, hit ESC to exit the file. To request an editable

To view this PDF as a projectable presentation, save the file, click view in the top menu bar, & select full screen mode. Upon completion of the presentation, hit ESC to exit the file. To request an editable

MANAGING GREEK INDEBTEDNESS: How Greece can regain fiscal credibility and avoid the recessionary debt-trap

MANAGING GREEK INDEBTEDNESS: How Greece can regain fiscal credibility and avoid the recessionary debt-trap Nicos Christodoulakis Athens University of Economics and Business Public Financial Management

MANAGING GREEK INDEBTEDNESS: How Greece can regain fiscal credibility and avoid the recessionary debt-trap Nicos Christodoulakis Athens University of Economics and Business Public Financial Management

Procedia - Social and Behavioral Sciences 156 ( 2014 )

") Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 156 ( 2014 ) 398 403 19th International Scientific Conference; Economics and Management 2014, ICEM 2014,

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 156 ( 2014 ) 398 403 19th International Scientific Conference; Economics and Management 2014, ICEM 2014,

The Greek and EU crisis Athens, KEPE, June 27, 2012

The Greek and EU crisis Athens, KEPE, June 27, 2012 Nicholas Economides Stern School of Business, New York University http://www.stern.nyu.edu/networks/ NET Institute http://www.netinst.org/ mailto:economides@stern.nyu.edu

The Greek and EU crisis Athens, KEPE, June 27, 2012 Nicholas Economides Stern School of Business, New York University http://www.stern.nyu.edu/networks/ NET Institute http://www.netinst.org/ mailto:economides@stern.nyu.edu

The role of ECB in relation to the modified EFSF and the future ESM. Prof. Dr. iur. Dr. rer. pol. Peter Sester

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

Investment Report The Flexible Guarantee Bond and Flexi Guarantee Plan

Investment Report 2011 The Flexible Guarantee Bond and Flexi Guarantee Plan The Flexible Guarantee Bond and Flexi Guarantee Plan Investment Report 2011 This information does not constitute investment advice

Investment Report 2011 The Flexible Guarantee Bond and Flexi Guarantee Plan The Flexible Guarantee Bond and Flexi Guarantee Plan Investment Report 2011 This information does not constitute investment advice

Greece and the Eurozone: Background, Context, and Prospects. Stergios Skaperdas Global Peace and Conflict Studies February 12, 2015

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas Global Peace and Conflict Studies February 12, 2015 Agenda Background on Greece Context: Eurozone and the EU Four scenarios:

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas Global Peace and Conflict Studies February 12, 2015 Agenda Background on Greece Context: Eurozone and the EU Four scenarios:

Do Central Bank Interventions Limit the Market Discipline from Short-Term Debt?

Do Central Bank Interventions Limit the Market Discipline from Short-Term Debt? Viral Acharya NYU Stern School of Business Diane Pierret HEC Lausanne Sascha Steffen European School of Management and Technology

Do Central Bank Interventions Limit the Market Discipline from Short-Term Debt? Viral Acharya NYU Stern School of Business Diane Pierret HEC Lausanne Sascha Steffen European School of Management and Technology

Investment Report With Profits Fund

Investment Report 2011 With Profits Fund With Profits Fund Investment Report 2011 The information in this report should not be considered as investment advice and we recommend that you speak to a suitably

Investment Report 2011 With Profits Fund With Profits Fund Investment Report 2011 The information in this report should not be considered as investment advice and we recommend that you speak to a suitably

More evidence that financial markets imposed excessive austerity in the eurozone

More evidence that financial markets imposed excessive austerity in the eurozone Paul De Grauwe and Yuemei Ji 5 February 2013 The decision by the ECB in 2012 to commit itself to unlimited support of the

More evidence that financial markets imposed excessive austerity in the eurozone Paul De Grauwe and Yuemei Ji 5 February 2013 The decision by the ECB in 2012 to commit itself to unlimited support of the

The near-term global economic outlook

Overview The near-term global economic outlook Paul van den Noord Counsellor to the Chief Economist OECD 1 Overview World growth has slowed, including in EMEs. Trade has weakened. Unemployment is high

Overview The near-term global economic outlook Paul van den Noord Counsellor to the Chief Economist OECD 1 Overview World growth has slowed, including in EMEs. Trade has weakened. Unemployment is high

How Curb Risk In Wall Street. Luigi Zingales. University of Chicago

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

GROSS FUND PERFORMANCE 30 th April 2010

Sc pe GROSS FUND PERFORMANCE 30 th April 2010 Highlights During The Month Despite the turmoil in the Greek government bond market, global equity markets remained broadly unchanged in April. The underperformance

Sc pe GROSS FUND PERFORMANCE 30 th April 2010 Highlights During The Month Despite the turmoil in the Greek government bond market, global equity markets remained broadly unchanged in April. The underperformance