Second Quarter 2016 Volume 9, number 2 colorado.edu/business/brd

|

|

|

- Julian Neal

- 5 years ago

- Views:

Transcription

reported steady optimism ahead of Q2 2016, but expectations were")

1 Second Quarter 2016 Volume 9, number 2 colorado.edu/business/brd Summary Stable Expectations The panel of business leaders surveyed in the Leeds Business Confidence Index (LBCI) reported steady optimism ahead of Q2 2016, but expectations were lower for Q The index is in positive territory (above 50) for all metrics in the index save for the national outlook. Sales expectations topped the outlook, and national expectations were least optimistic. According to the Bureau of Economic Analysis (BEA), the United States recorded real GDP growth of 2.4% (seasonally adjusted annual rate) in Quarterly growth peaked in Q (3.9%), followed by 2% and 1.4% in Q3 and Q4, respectively. Colorado recorded GDP growth of 2.4% in Q3 2015, ranking the state 18th-fastest growth nationally. The Rocky Mountain region grew at 2.6%. Business leaders discussed their greatest concerns two quarters out. The top concerns identified by respondents included the pending election, the impact of commodity prices (notably, oil and gas prices), the global economy, the political climate, interest rates and Fed policy, the U.S. business cycle, government regulation, and slower job growth. Examining the top three concerns, respondents most frequently noted the pending election, the impact of commodity prices, and the global economy as their greatest concerns (see appendix). Additionally, a little more than half of respondents (52%) indicated the presence of a talent shortage in Colorado. Most often, panelists described the shortage as leading to higher salaries/wages, lower retention, slower business growth, and higher project costs. As well, panelists described a longer recruiting process and the need to recruit from out-of-state. The LBCI, which captures Colorado business leaders expectations for the national economy, state economy, industry sales, profits, hiring plans, and capital expenditures, is at 55.4 for Q (unchanged from Q1) and 54.4 for Q Expectations fell compared to a year ago for both Q2 (-6.3 points) and Q3 (-3.9 points). A total of 327 panelists responded to the survey. 1

2 Business Leaders Concerns about a Talent Shortage Note: The larger the word, the more responses the concerns garnered. n=142 National and State Economies Declining Outlook Expectations about the national economy and the state economy both decreased ahead of Q2 and Q3. In particular, national expectations slipped below neutral, falling from 50.5 to 49.5 ahead of Q2 and 49.2 ahead of Q3. Expectations about the state fell 2 points, and the national economy declined 1 point. Business leaders remained more positive about the state economy than the national economy. Overall expectations for the state economy decreased from 59.3 in Q to 57.3 in Q and 56.5 in Q3. Nearly 40% of panelists expect the state economy to expand, and 47% of respondents are neutral. Three percent of respondents expect a strong increase in the state economy, and less than 1% of respondents anticipate a strong decrease. Confidence in the national economy decreased ahead of Q2 and Q3, from 50.5 in Q1 to 49.5 in Q and 49.2 in Q Pessimists outnumbered optimists 28% to 26%. According to the third estimate from the BEA, U.S. GDP in Q experienced a 1.4% increase and expanded 2.4% for the year. The BEA reported: The deceleration in real GDP in the fourth quarter primarily reflected downturns in nonresidential fixed investment and in state and local government spending, a deceleration in PCE, and a downturn in exports that were partly offset by a smaller 2

3 decrease in private inventory investment, a downturn in imports, and an acceleration in federal government spending. National employment growth exhibited strength, averaging 252,000 jobs over the five months ending in February, and the unemployment rate remained at 4.9% for the second-consecutive month in February. Total year-over-year employment growth has continued to slow in Colorado for the second consecutive month in February, with the pace of growth at 2.5%. After 21 uninterrupted months of +3% job growth from November 2013 through July 2015, job growth has expanded in the 2% range for 7 months. The state recorded 52 consecutive months of job growth. Yearover-year, the state added 63,000 jobs. Sales and Profits Expectations Stabilize Ahead of Q1 Profits and sales expectations rose ahead of Q2 2016, but sales expectations decelerated for Q3. The profits index recorded a 1.4-point increase, from 55.3 in Q to 56.7 in the Q survey. Profits expectations increased to 56.8 for Q Sales expectations increased from 58.4 to 59.5 in Q2 2016, but decreased to 58.6 in Q

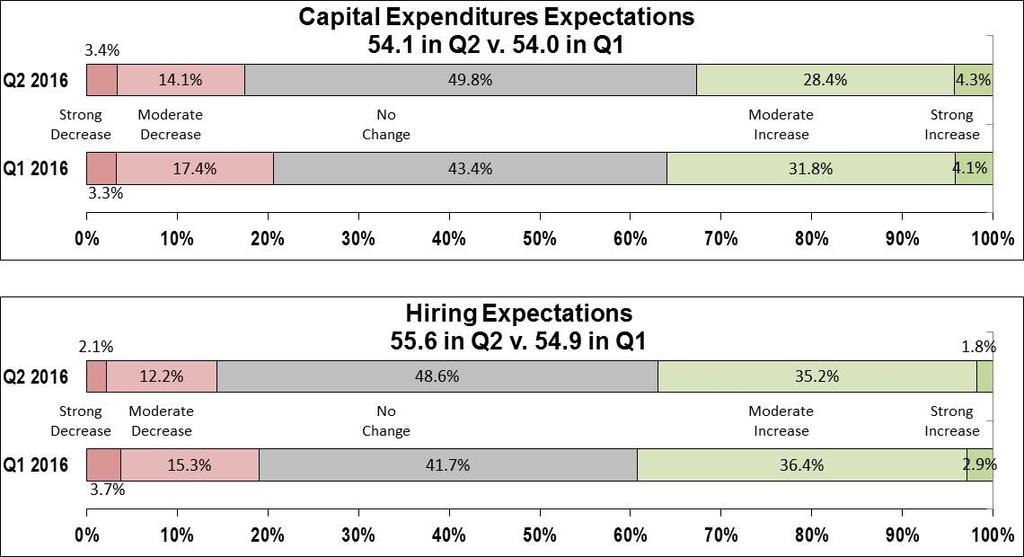

4 The positive profits index was sustained by 42% of respondents who anticipate an increase in sales in Q2 versus 17% who expect a decline; 41% are neutral. Of the respondents on the extreme tails, 4% expect a strong increase and 2% anticipate a strong decrease. The sales index increased to 59.5 in Q2 2016, with those expecting growth in sales (49%) outweighing those anticipating declines (14%). More than one-third remain neutral. According to the BEA, state personal income rose 1% from the preceding quarter in Q and 4.2% year-over-year, ranking the state 6th and 15th, respectively, for these metrics. Per capita personal income rose 2.2% year-over-year in Q4. Inflation in the second half of the year (all items index) increased 1.4% year-over-year in the Denver-Boulder-Greeley MSA. Core inflation increased 3.5% year-over-year, and shelter increased 5.8%. According to the Federal Housing Finance Agency (FHFA) purchase only home price index, between the fourth quarter of 2014 and the fourth quarter of 2015, home prices rose in every state. Colorado ranked second in the nation behind Nevada in home price appreciation in Q4 2015, with a year-over-year increase of 10.9% and a 1.3% gain over the previous quarter. According to the Institute for Supply Management, the manufacturing index increased to 49.5 in February 2016, an increase from January, but below the neutral (50) threshold. Capital Expenditures and Hiring Plans Realignment Hiring expectations increased ahead of Q2, but the capital expenditures outlook remained flat; both decreased ahead of Q3. 4

5 While half of respondents are neutral, 33% expect a boost in capital expenditures, with the overall index increasing slightly to 54.1 in Q Capital expenditure expectations decrease for Q3, to A total of 4.3% respondents expect a strong increase compared to 3.4% who anticipate a strong decrease in capital expenditures. Hiring expectations increased as well in the Q survey, from 54.9 to 55.6, but decreased, to 53, for Q3. About 49% of respondents are neutral on hiring, and another 37% of panelists note positive expectations, indicating employment in Colorado continues to have upward growth potential. The unemployment rate in Colorado decreased to 3% in February 2016, which compares to the national unemployment rate of 4.9%. Employment growth was recorded year-over-year in most metropolitan areas around the state, with the Fort Collins-Loveland MSA and the Colorado Springs MSA recording the fastest growth, 3.8% and 2.7% year-over-year, respectively. The Denver-Aurora-Broomfield (2.5%), Boulder (1.8%), Pueblo (1.5%), and Grand Junction (0.2%) MSAs also recorded employment growth, while the Greeley MSA recorded a sixth-consecutive month of year-over-year declines (-0.6%). Across the state, the greatest year-over-year percentage gains in employment were in Leisure and Hospitality (6.3%), Construction (4.3%), and Education and Health Services (4%). The weakest sector for growth was Mining and Logging (-19.1%). 5

6 About the Panel Company Size and Length of Time in Business Panelists were asked two additional questions, one about the size of their company and the other about how long their company has been in business. About half (49.5%) of survey respondents work for companies with fewer than 50 employees. The four largest groups were represented by companies with 1 4 employees (19.6%), employees (18%), 1,000 or more employees (13.8%), and 5 9 employees (12.2%). Small employers expectations increased 1.2 points ahead of Q2 while large employers expectations decreased 0.8 points. While remaining above the neutral threshold, small employers (fewer than 50 employees) were notably less optimistic than large employers. The 6

7 overall index for small employers increased to 54.1 versus 57.2 for large employers. Large employers were more bullish than small employers in every category. The greatest differential (6.5 points) was in hiring plans, with small employers recording a reading of 52.7 compared to large employers reading of More than 87% of survey respondents work at a long-standing company that has been in business for more than 10 years. Newer companies were more bullish than long-standing companies. The index by firm tenure (how long it has been in business) was higher for firms in business less than 10 years (58.1) than for firms in business more than 10 years (55.1). While responding panelists represent nearly every industry in the state, the largest percentage of respondents to the Q2 survey work in three private sectors: Professional and Technical Services (20.7%), Finance and Insurance (19.8%), and Real Estate and Rental and Leasing (11.1%). 7

8 Distribution of Expectations 8

9 9

10 Appendix: Overall Concerns Looking Ahead to Q Concern Election Commodity/Energy Prices Global Economy Political Climate Interest Rates/Fed Policy Recession/Business Cycle Government Regulation Job growth Government Spending/Debt Other Labor Shortage Skilled/Talented Workforce Affordable Housing Housing Bubble/Plateau Wage Pressure Stock Market Inflation Capital Spending Cost of Health Care Taxes National Security Strength of Dollar Consumer Confidence Deteriorating Infrastructure Demand Slowdown Low Wages Eurozone Demographics Labor Costs Decline in Retail Sales TABOR Unemployed Minimum Wage Consumer Spending Geopolitics Productivity Trade Deficits Student Loans Corruption Market Uncertainty Corporate Profits N=291 # # # For more information about the LBCI and to become a panelist, go to: 10

Summary Pessimism Abates Ahead of Q1

First Quarter 2016 Volume 9, number 1 colorado.edu/business/brd Summary Pessimism Abates Ahead of Q1 The panel of business leaders surveyed in the Leeds Business Confidence Index (LBCI) reported modestly

First Quarter 2016 Volume 9, number 1 colorado.edu/business/brd Summary Pessimism Abates Ahead of Q1 The panel of business leaders surveyed in the Leeds Business Confidence Index (LBCI) reported modestly

Leeds Business Confidence Index

Third Quarter 2018 Volume 11, number 3 colorado.edu/business/brd Leeds Business Confidence Steady Ahead of Q3 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Third Quarter 2018 Volume 11, number 3 colorado.edu/business/brd Leeds Business Confidence Steady Ahead of Q3 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Leeds Business Confidence Index

Second Quarter 2018 Volume 11, number 2 colorado.edu/business/brd Leeds Business Confidence Steady Ahead of Q2 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Second Quarter 2018 Volume 11, number 2 colorado.edu/business/brd Leeds Business Confidence Steady Ahead of Q2 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Leeds Business Confidence Index

Fourth Quarter 2017 Volume 10, number 4 colorado.edu/business/brd Leeds Business Confidence Index Cools Ahead of Q4 2017 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Fourth Quarter 2017 Volume 10, number 4 colorado.edu/business/brd Leeds Business Confidence Index Cools Ahead of Q4 2017 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Leeds Business Confidence Index

First Quarter 2018 Volume 11, number 1 colorado.edu/business/brd Leeds Business Confidence Rebounds Ahead of Q1 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

First Quarter 2018 Volume 11, number 1 colorado.edu/business/brd Leeds Business Confidence Rebounds Ahead of Q1 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Secretary of State Business Filings Q Data Analysis Summary

QUARTERLY BUSINESS & ECONOMIC INDICATORS Fourth Quarter 2017 Secretary of State Business Filings Q4 2017 Data Analysis Summary New entity filings continued to gain in Q4 2017. State employment projections

QUARTERLY BUSINESS & ECONOMIC INDICATORS Fourth Quarter 2017 Secretary of State Business Filings Q4 2017 Data Analysis Summary New entity filings continued to gain in Q4 2017. State employment projections

Secretary of State Business Filings Q Data Analysis Summary

QUARTERLY BUSINESS & ECONOMIC INDICATORS First Quarter 2016 Secretary of State Business Filings Q1 2016 Data Analysis Summary Employment projected to continue expanding in Q2 2016 and Q3 2016, but at a

QUARTERLY BUSINESS & ECONOMIC INDICATORS First Quarter 2016 Secretary of State Business Filings Q1 2016 Data Analysis Summary Employment projected to continue expanding in Q2 2016 and Q3 2016, but at a

Secretary of State Business Filings Q Data Analysis Summary

QUARTERLY BUSINESS & ECONOMIC INDICATORS First Quarter 2018 Secretary of State Business Filings Q1 2018 Data Analysis Summary New entity filings recorded strong growth in Q1 2018. State employment projections

QUARTERLY BUSINESS & ECONOMIC INDICATORS First Quarter 2018 Secretary of State Business Filings Q1 2018 Data Analysis Summary New entity filings recorded strong growth in Q1 2018. State employment projections

Analysis & Background

1 Values shown are June estimates. # # # Analysis & Background Expected Revisions to Colorado Second quarter 2017 Quarterly Census of Employment and Wages (QCEW) results indicate Colorado total nonfarm

1 Values shown are June estimates. # # # Analysis & Background Expected Revisions to Colorado Second quarter 2017 Quarterly Census of Employment and Wages (QCEW) results indicate Colorado total nonfarm

Secretary of State Business Filings Q Data Analysis Summary

QUARTERLY BUSINESS & ECONOMIC INDICATORS Fourth Quarter 2016 Secretary of State Business Filings Q4 2016 Data Analysis Summary New entity filings exhibit unrelenting growth in Q4 2016. Employment growth

QUARTERLY BUSINESS & ECONOMIC INDICATORS Fourth Quarter 2016 Secretary of State Business Filings Q4 2016 Data Analysis Summary New entity filings exhibit unrelenting growth in Q4 2016. Employment growth

Secretary of State Business Filings Q Data Analysis Summary

C O L O R A D O S E C R E TA R Y O F S TAT E QUARTERLY BUSINESS & ECONOMIC INDICATORS Secretary of State Jena Griswold Fourth Quarter 2018 Secretary of State Business Filings Q4 2018 Data Analysis Summary

C O L O R A D O S E C R E TA R Y O F S TAT E QUARTERLY BUSINESS & ECONOMIC INDICATORS Secretary of State Jena Griswold Fourth Quarter 2018 Secretary of State Business Filings Q4 2018 Data Analysis Summary

Secretary of State Business Filings Q Data Analysis Summary

QUARTERLY BUSINESS & ECONOMIC INDICATORS Third Quarter 2016 Secretary of State Business Filings Q3 2016 Data Analysis Summary Employment is projected to continue expanding in Q3 2016 and Q4 2016, but at

QUARTERLY BUSINESS & ECONOMIC INDICATORS Third Quarter 2016 Secretary of State Business Filings Q3 2016 Data Analysis Summary Employment is projected to continue expanding in Q3 2016 and Q4 2016, but at

The Colorado Outlook March 17, Follow the Governor s Office of State Planning and Budgeting on

sourc e Table of Contents Summary... 3 The Economy: Issues, Trends, and Forecast... 4 Summary of Key Economic Indicators... 29 General Fund and State Education Fund Revenue Forecast... 35 General Fund

sourc e Table of Contents Summary... 3 The Economy: Issues, Trends, and Forecast... 4 Summary of Key Economic Indicators... 29 General Fund and State Education Fund Revenue Forecast... 35 General Fund

Business Growth in Colorado

QUARTERLY BUSINESS & ECONOMIC INDICATORS First Quarter 2013 PUBLISHED BY BUSINESS RESEARCH DIVISION, LEEDS SCHOOL OF BUSINESS, UNIVERSITY OF COLORADO BOULDER I N D I C AT O R S Employment (SA) New Entity

QUARTERLY BUSINESS & ECONOMIC INDICATORS First Quarter 2013 PUBLISHED BY BUSINESS RESEARCH DIVISION, LEEDS SCHOOL OF BUSINESS, UNIVERSITY OF COLORADO BOULDER I N D I C AT O R S Employment (SA) New Entity

Economy on Stronger Footing

QUARTERLY BUSINESS & ECONOMIC INDICATORS Second Quarter 2013 PUBLISHED BY BUSINESS RESEARCH DIVISION, LEEDS SCHOOL OF BUSINESS, UNIVERSITY OF COLORADO BOULDER I N D I C AT O R S Employment (SA) New Entity

QUARTERLY BUSINESS & ECONOMIC INDICATORS Second Quarter 2013 PUBLISHED BY BUSINESS RESEARCH DIVISION, LEEDS SCHOOL OF BUSINESS, UNIVERSITY OF COLORADO BOULDER I N D I C AT O R S Employment (SA) New Entity

Economic Highlights. ISM Purchasing Managers Index 1. Sixth District Payroll Employment by Industry 2. Contributions to Real GDP Growth 3

December 1, 2010 Economic Highlights Manufacturing ISM Purchasing Managers Index 1 Employment Sixth District Payroll Employment by Industry 2 Economic Activity Contributions to Real GDP Growth 3 Prices

December 1, 2010 Economic Highlights Manufacturing ISM Purchasing Managers Index 1 Employment Sixth District Payroll Employment by Industry 2 Economic Activity Contributions to Real GDP Growth 3 Prices

The Colorado Outlook September 20, Follow the Governor s Office of State Planning and Budgeting on

source Table of Contents Summary... 3 The Economy: Issues, Trends, and Forecast... 4 Summary of Key Economic Indicators... 17 General Fund and State Education Fund Revenue Forecast... 23 General Fund and

source Table of Contents Summary... 3 The Economy: Issues, Trends, and Forecast... 4 Summary of Key Economic Indicators... 17 General Fund and State Education Fund Revenue Forecast... 23 General Fund and

Will the Recovery Ever End? Boulder Economic Forecast

Will the Recovery Ever End? Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 219 #COBizOutlook Real

Will the Recovery Ever End? Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 219 #COBizOutlook Real

ECONOMIC FORECAST BREAKFAST

ECONOMIC FORECAST BREAKFAST LEADERSHIP IN A STARTUP ECONOMY FRIDAY, JANUARY 15, 2016 www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME

ECONOMIC FORECAST BREAKFAST LEADERSHIP IN A STARTUP ECONOMY FRIDAY, JANUARY 15, 2016 www.colorado.edu/leeds/brd CAREER ADVANCING DEGREES FROM LEEDS EVENING MBA PROGRAM FOR WORKING PROFESSIONALS #1 PART-TIME

Will the Recovery Ever End? Certified Financial Planners

Will the Recovery Ever End? Certified Financial Planners Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 25, 219 Attention: This

Will the Recovery Ever End? Certified Financial Planners Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 25, 219 Attention: This

More of the Same? Southwest Business Forum

More of the Same? Southwest Business Forum Place cover image here Richard Wobbekind Senior Associate Dean, Leeds School of Business Executive Director, Business Research Division January 4, 2017 Colorado

More of the Same? Southwest Business Forum Place cover image here Richard Wobbekind Senior Associate Dean, Leeds School of Business Executive Director, Business Research Division January 4, 2017 Colorado

Manufacturing Barometer

Special topic: Year 2016 major challenges Manufacturing Barometer Business outlook report January 2016 Contents 1 Quarterly highlights 1.1 Key indicators for the business outlook 7 1.2 PwC global manufacturing

Special topic: Year 2016 major challenges Manufacturing Barometer Business outlook report January 2016 Contents 1 Quarterly highlights 1.1 Key indicators for the business outlook 7 1.2 PwC global manufacturing

QUARTERLY INDICATORS Southern Nevada Business Confidence Index

Third Quarter 2018 Economic Outlook: Global, National, and Local U.S. real gross domestic product (GDP) for the first quarter of 2018 expanded at an annualized rate of 2.0 percent, after three consecutive

Third Quarter 2018 Economic Outlook: Global, National, and Local U.S. real gross domestic product (GDP) for the first quarter of 2018 expanded at an annualized rate of 2.0 percent, after three consecutive

Secretary of State Business Filings Q Data Analysis Summary

C O L O R A D O S E C R E TA R Y O F S TAT E QUARTERLY BUSINESS & ECONOMIC INDICATORS Fourth Quarter 2014 Secretary of State Business Filings Q4 2014 Data Analysis Summary New business filings increase

C O L O R A D O S E C R E TA R Y O F S TAT E QUARTERLY BUSINESS & ECONOMIC INDICATORS Fourth Quarter 2014 Secretary of State Business Filings Q4 2014 Data Analysis Summary New business filings increase

Valentyn Povroznyuk, Edilberto L. Segura

National real GDP grew by 2.3% quarter-over-quarter (qoq) in Q2 2015. Average real GDP growth for Q4 2011-Q1 2015 was revised downwards by 0.2% from the previously published 2.2%. US industrial output

National real GDP grew by 2.3% quarter-over-quarter (qoq) in Q2 2015. Average real GDP growth for Q4 2011-Q1 2015 was revised downwards by 0.2% from the previously published 2.2%. US industrial output

Baseline U.S. Economic Outlook, Summary Table*

October 2014 Solid U.S. Economic Data Belie Market Turmoil Executive Summary September payroll job growth was above consensus with 248,000 jobs added over the month. September private-sector employment

October 2014 Solid U.S. Economic Data Belie Market Turmoil Executive Summary September payroll job growth was above consensus with 248,000 jobs added over the month. September private-sector employment

MORGANTOWN METROPOLITAN STATISTICAL AREA OUTLOOK COLLEGE OF BUSINESS AND ECONOMICS. Bureau of Business and Economic Research

2013 MORGANTOWN METROPOLITAN STATISTICAL AREA OUTLOOK COLLEGE OF BUSINESS AND ECONOMICS Bureau of Business and Economic Research 1 MORGANTOWN METROPOLITAN STATISTICAL AREA OUtlook 2013 EXECUTIVE SUMMARY

2013 MORGANTOWN METROPOLITAN STATISTICAL AREA OUTLOOK COLLEGE OF BUSINESS AND ECONOMICS Bureau of Business and Economic Research 1 MORGANTOWN METROPOLITAN STATISTICAL AREA OUtlook 2013 EXECUTIVE SUMMARY

Florida Economic Outlook State Gross Domestic Product

Florida Economic Outlook The Florida Economic Estimating Conference met in July 2017 to revise the forecast for the state s economy. As further updated by the Legislative Office of Economic and Demographic

Florida Economic Outlook The Florida Economic Estimating Conference met in July 2017 to revise the forecast for the state s economy. As further updated by the Legislative Office of Economic and Demographic

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS Comptroller Kevin Lembo today said that there are reasons for cautious optimism that the state could end Fiscal

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS Comptroller Kevin Lembo today said that there are reasons for cautious optimism that the state could end Fiscal

QUARTERLY INDICATORS Southern Nevada Business Confidence Index

Second Quarter 2018 Economic Outlook: Global, National, and Local U.S. real gross domestic product (GDP) for the fourth quarter of 2017 expanded at an annualized rate of 2.9 percent, after two consecutive

Second Quarter 2018 Economic Outlook: Global, National, and Local U.S. real gross domestic product (GDP) for the fourth quarter of 2017 expanded at an annualized rate of 2.9 percent, after two consecutive

Colorado Economic Forecast Just the Facts!

Colorado Economic Forecast 2017 Just the Facts! Larimer County Workforce Development Board February 8, 2017 Gary Horvath 1 If the Recession is Over Where is the Talent? February 2012 Presentation 222,831

Colorado Economic Forecast 2017 Just the Facts! Larimer County Workforce Development Board February 8, 2017 Gary Horvath 1 If the Recession is Over Where is the Talent? February 2012 Presentation 222,831

2015 Mid-Year Economic Update

BROOMFIELD Economic Development 2015 Mid-Year Economic Update Provided by: Broomfield Economic Development One Descombes Drive Broomfield, CO 80020 303-464-5579 www.investbroomfield.com Prepared by: Development

BROOMFIELD Economic Development 2015 Mid-Year Economic Update Provided by: Broomfield Economic Development One Descombes Drive Broomfield, CO 80020 303-464-5579 www.investbroomfield.com Prepared by: Development

MonthlyEconomicIndicators. MarchUpdate: 2017Benchmark EmploymentRevision. EnergeticBodies.EnergeticMinds. ResearchSponsor.

MonthlyEconomicIndicators EnergeticBodies.EnergeticMinds. www.metrodenver.org MarchUpdate: 2017Benchmark EmploymentRevision ResearchSponsor www.pinnacol.com www.developmentresearch.net 2016 and 2017 Employment

MonthlyEconomicIndicators EnergeticBodies.EnergeticMinds. www.metrodenver.org MarchUpdate: 2017Benchmark EmploymentRevision ResearchSponsor www.pinnacol.com www.developmentresearch.net 2016 and 2017 Employment

Outlook for the Hawai'i Economy

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Smith Leonard PLLC Kenneth D. Smith, CPA Mark S. Laferriere, CPA

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter August 2018 N HIGHLIGHTS - EXECUTIVE SUMMARY ew orders in June 2018 were up 5% over June 2017, according to our recent survey of residential

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter August 2018 N HIGHLIGHTS - EXECUTIVE SUMMARY ew orders in June 2018 were up 5% over June 2017, according to our recent survey of residential

2016 End of Year Economic Update

BROOMFIELD Economic Development End of Year Economic Update RELEASED: MARCH 2017 Provided by: Broomfield Economic Development One Descombes Drive Broomfield, CO 80020 303-464-5579 www.investbroomfield.com

BROOMFIELD Economic Development End of Year Economic Update RELEASED: MARCH 2017 Provided by: Broomfield Economic Development One Descombes Drive Broomfield, CO 80020 303-464-5579 www.investbroomfield.com

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

May 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary With Job Market in Good Shape,

May 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary With Job Market in Good Shape,

Southwest Business Forum. Business Research Division Leeds School of Business University of Colorado

Southwest Business Forum Colorado Population, Employment, Income and Prices Change in Population Change in Colorado Population Thousands 2004-2014 100 90 80 70 60 50 40 30 20 10 Among top 7 states for

Southwest Business Forum Colorado Population, Employment, Income and Prices Change in Population Change in Colorado Population Thousands 2004-2014 100 90 80 70 60 50 40 30 20 10 Among top 7 states for

VECTRA BANK 23 RD ANNUAL ECONOMIC FORECAST BREAKFAST START SMART IN 2016! Member FDIC VectraBank.com

VECTRA BANK 23 RD ANNUAL ECONOMIC FORECAST BREAKFAST START SMART IN 2016! Member FDIC VectraBank.com Colorado s Economy and State Budget Office of State Planning and Budgeting April 26, 2016 Jason Schrock,

VECTRA BANK 23 RD ANNUAL ECONOMIC FORECAST BREAKFAST START SMART IN 2016! Member FDIC VectraBank.com Colorado s Economy and State Budget Office of State Planning and Budgeting April 26, 2016 Jason Schrock,

QUARTERLY INDICATORS Southern Nevada Business Confidence Index

Fourth Quarter 2017 Economic Outlook: Global, National, and Local U.S. real gross domestic product (GDP) for the second quarter of 2017 rebounded robustly, increasing at a 3.1 percent annualized rate.

Fourth Quarter 2017 Economic Outlook: Global, National, and Local U.S. real gross domestic product (GDP) for the second quarter of 2017 rebounded robustly, increasing at a 3.1 percent annualized rate.

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

Consolidated Investment Report

Consolidated Investment Report September 2015 As Palm Beach County s Chief Financial Officer, the Clerk & Comptroller is charged with safeguarding and investing all County funds. The Clerk s management

Consolidated Investment Report September 2015 As Palm Beach County s Chief Financial Officer, the Clerk & Comptroller is charged with safeguarding and investing all County funds. The Clerk s management

SEMA INDUSTRY INDICATORS

SEMA INDUSTRY INDICATORS JULY 2018 The first half of 2018 is now in the books and the economy has shown resilience in the face of a myriad of concerns. These fears have included low overall economic growth

SEMA INDUSTRY INDICATORS JULY 2018 The first half of 2018 is now in the books and the economy has shown resilience in the face of a myriad of concerns. These fears have included low overall economic growth

RÉMUNÉRATION DES SALARIÉS. ÉTAT ET ÉVOLUTION COMPARÉS 2010 MAIN FINDINGS

RÉMUNÉRATION DES SALARIÉS. ÉTAT ET ÉVOLUTION COMPARÉS 2010 MAIN FINDINGS PART I SALARIES AND TOTAL COMPENSATION All other Quebec employees In 2010, the average salaries of Quebec government employees 1

RÉMUNÉRATION DES SALARIÉS. ÉTAT ET ÉVOLUTION COMPARÉS 2010 MAIN FINDINGS PART I SALARIES AND TOTAL COMPENSATION All other Quebec employees In 2010, the average salaries of Quebec government employees 1

Empire State Manufacturing Survey

November 216 Empire State Manufacturing Survey Business activity stabilized in New York State, according to firms responding to the November 216 Empire State Manufacturing Survey. The headline general

November 216 Empire State Manufacturing Survey Business activity stabilized in New York State, according to firms responding to the November 216 Empire State Manufacturing Survey. The headline general

Smith Leonard PLLC Kenneth D. Smith, CPA Mark S. Laferriere, CPA

Smith Leonard PLLC s Industry Newsletter January 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A ccording to our latest survey of residential furniture manufacturers and distributors, new orders in November 2017

Smith Leonard PLLC s Industry Newsletter January 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A ccording to our latest survey of residential furniture manufacturers and distributors, new orders in November 2017

MBA Forecast Commentary Joel Kan

MBA Forecast Commentary Joel Kan Economy & Labor Markets Strong Enough, First Rate Hike Expected in December MBA Economic and Mortgage Finance Commentary: November 2015 This month s outlook largely mirrors

MBA Forecast Commentary Joel Kan Economy & Labor Markets Strong Enough, First Rate Hike Expected in December MBA Economic and Mortgage Finance Commentary: November 2015 This month s outlook largely mirrors

JOB SITUATION INCOME. 3 rd Quarter 2015 PITTSBURGH

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

The Beige Book. Summary of Economic Activity

The Beige Book Eighth District August 2017 Summary of Economic Activity Economic conditions have improved at a modest pace since our previous report. District labor market conditions continue to improve,

The Beige Book Eighth District August 2017 Summary of Economic Activity Economic conditions have improved at a modest pace since our previous report. District labor market conditions continue to improve,

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University The economy continues to grow at a steady rate, with slight increases in global and national GDP, a lower national unemployment rate, and

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University The economy continues to grow at a steady rate, with slight increases in global and national GDP, a lower national unemployment rate, and

Michigan Economic Update

Michigan Economic Update Federal Reserve Bank of Chicago Detroit Branch October 30, 2015 Paul Traub Senior Business Economist The Midwest Economy declined to -0.15 in September while Michigan s contribution

Michigan Economic Update Federal Reserve Bank of Chicago Detroit Branch October 30, 2015 Paul Traub Senior Business Economist The Midwest Economy declined to -0.15 in September while Michigan s contribution

Third Quarter 2015 An independent economic analysis of Arkansas three largest metro areas: Central Arkansas Northwest Arkansas The Fort Smith region

Third Quarter 2015 An independent economic analysis of Arkansas three largest metro areas: Central Arkansas Northwest Arkansas The Fort Smith region About The Compass The Compass Report is managed by Talk

Third Quarter 2015 An independent economic analysis of Arkansas three largest metro areas: Central Arkansas Northwest Arkansas The Fort Smith region About The Compass The Compass Report is managed by Talk

2015 End of Year Economic Update

BROOMFIELD Economic Development 2015 End of Year Economic Update RELEASED: FEBRUARY 2016 Provided by: Broomfield Economic Development One Descombes Drive Broomfield, CO 80020 303-464-5579 www.investbroomfield.com

BROOMFIELD Economic Development 2015 End of Year Economic Update RELEASED: FEBRUARY 2016 Provided by: Broomfield Economic Development One Descombes Drive Broomfield, CO 80020 303-464-5579 www.investbroomfield.com

Economic Activity Report. October 2016

Economic Activity Report October 2016 The current economic activity report for Commerce City economy reported mixed trends across many indicators. The employment situation improved, with overall employment

Economic Activity Report October 2016 The current economic activity report for Commerce City economy reported mixed trends across many indicators. The employment situation improved, with overall employment

The President s Report to the Board of Directors

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

Manufacturing Barometer

www.pwc.com Manufacturing Barometer Business outlook report April 2013 Special topic: Fiscal policy uncertainties Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 1.1

www.pwc.com Manufacturing Barometer Business outlook report April 2013 Special topic: Fiscal policy uncertainties Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 1.1

State of Ohio Workforce. 2 nd Quarter

To Strengthen Ohio s Families through the Delivery of Integrated Solutions to Temporary Challenges State of Ohio Workforce 2 nd Quarter 2 0 1 2 Quarterly Report on the State of Ohio s Workforce Reference

To Strengthen Ohio s Families through the Delivery of Integrated Solutions to Temporary Challenges State of Ohio Workforce 2 nd Quarter 2 0 1 2 Quarterly Report on the State of Ohio s Workforce Reference

O HIGHLIGHTS - EXECUTIVE SUMMARY

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter February 2018 O HIGHLIGHTS - EXECUTIVE SUMMARY ur latest survey of residential furniture manufacturers and distributors revealed some disappointing

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter February 2018 O HIGHLIGHTS - EXECUTIVE SUMMARY ur latest survey of residential furniture manufacturers and distributors revealed some disappointing

Arvest Consumer Sentiment Survey April 2016

Arvest Consumer Sentiment Survey April Produced for Arvest Bank by a multi-university collaboration including: Center for Business and Economic Research Sam M. Walton College of Business University of

Arvest Consumer Sentiment Survey April Produced for Arvest Bank by a multi-university collaboration including: Center for Business and Economic Research Sam M. Walton College of Business University of

ECONOMIC PROSPECTS FOR HONG KONG IN Win Lin Chou, ACE Centre for Business and Economic Research, Hong Kong

ECONOMIC PROSPECTS FOR HONG KONG IN 2014-15 Win Lin Chou, ACE Centre for Business and Economic Research, Hong Kong I. The Current Trends Real gross domestic product (GDP) in Hong Kong slowed to 1.8 percent

ECONOMIC PROSPECTS FOR HONG KONG IN 2014-15 Win Lin Chou, ACE Centre for Business and Economic Research, Hong Kong I. The Current Trends Real gross domestic product (GDP) in Hong Kong slowed to 1.8 percent

REGIONAL SUMMARIES. Nonfarm employment grew in the second quarter. Non-farm jobs totaled 56,900 in June, up from 55,500 in June 2016.

Second Quarter 2017 Quarterly narrative An independent economic analysis of four Arkansas metro areas: Central Arkansas Northwest Arkansas The Fort Smith region Jonesboro metro REGIONAL SUMMARIES Fort

Second Quarter 2017 Quarterly narrative An independent economic analysis of four Arkansas metro areas: Central Arkansas Northwest Arkansas The Fort Smith region Jonesboro metro REGIONAL SUMMARIES Fort

2018 Kansas City Economic Forecast. Mid-Year Update Greater Kansas City Chamber of Commerce June 15, 2018

2018 Kansas City Economic Forecast Mid-Year Update Greater Kansas City Chamber of Commerce June 15, 2018 Status of the U.S. Economy By many measures the economy is approaching maximum capacity. 160,000

2018 Kansas City Economic Forecast Mid-Year Update Greater Kansas City Chamber of Commerce June 15, 2018 Status of the U.S. Economy By many measures the economy is approaching maximum capacity. 160,000

Modest Economic Growth and Falling GDP Gap

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

61.9 (June: 63.6 all-time high, revised)

") NAM MANUFACTURERS OUTLOOK SURVEY THIRD QUARTER 2018 OCTOBER 5, 2018 Percentage of Respondents Positive About Their Own Company s Outlook 92.5% (June: 95.1% all-time high) Four-Quarter Average: 93.9% *

NAM MANUFACTURERS OUTLOOK SURVEY THIRD QUARTER 2018 OCTOBER 5, 2018 Percentage of Respondents Positive About Their Own Company s Outlook 92.5% (June: 95.1% all-time high) Four-Quarter Average: 93.9% *

March 19, Employment. Benchmark Jobs Data Proved More Accurate in Real Time

March 19, 2019 Growth in employment and the business-cycle index slowed for Houston at the start of the year. Leading indicators were mixed but largely painted a softer outlook for 2019. Revisions to 2018

March 19, 2019 Growth in employment and the business-cycle index slowed for Houston at the start of the year. Leading indicators were mixed but largely painted a softer outlook for 2019. Revisions to 2018

Phoenix Management Services Lending Climate in America Survey

Phoenix Management Services Lending Climate in America Survey 2 nd Quarter 2016 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA 2 nd Quarter 2016 SUMMARY, TRENDS AND IMPLICATIONS 1.

Phoenix Management Services Lending Climate in America Survey 2 nd Quarter 2016 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA 2 nd Quarter 2016 SUMMARY, TRENDS AND IMPLICATIONS 1.

Empire State Manufacturing Survey

January 216 Empire State Manufacturing Survey The January 216 Empire State Manufacturing Survey indicates that business activity declined for New York manufacturers at the fastest pace since the Great

January 216 Empire State Manufacturing Survey The January 216 Empire State Manufacturing Survey indicates that business activity declined for New York manufacturers at the fastest pace since the Great

THE PURCHASING ECONOMY SURVEY REPORT

Welcome to our July Newsletter covering June survey results. Creighton s monthly survey of supply managers and procurement experts in nine Mid-America states indicates that economic growth remains in a

Welcome to our July Newsletter covering June survey results. Creighton s monthly survey of supply managers and procurement experts in nine Mid-America states indicates that economic growth remains in a

Manufacturing Barometer Business outlook report July 2014

www.pwc.com Manufacturing Barometer Business outlook report July 2014 Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 1.1 Manufacturing current assessment and outlook

www.pwc.com Manufacturing Barometer Business outlook report July 2014 Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 1.1 Manufacturing current assessment and outlook

Monetary and financial trends in the fourth quarter of 2014

Monetary and financial trends in the fourth quarter of 2014 Oil prices have significantly contracted in the third and fourth quarters of 2014, in an international economic environment marked by fragile

Monetary and financial trends in the fourth quarter of 2014 Oil prices have significantly contracted in the third and fourth quarters of 2014, in an international economic environment marked by fragile

SIP Aggressive Portfolio

SIP LIFESTYLE PORTFOLIOS FACT SHEET (NOV 2015) SIP Aggressive Portfolio SIP Aggressive Portfolio is a unitized fund, which is designed to provide long term capital growth. It is designed for those who

SIP LIFESTYLE PORTFOLIOS FACT SHEET (NOV 2015) SIP Aggressive Portfolio SIP Aggressive Portfolio is a unitized fund, which is designed to provide long term capital growth. It is designed for those who

Outlook and Market Review First Quarter 2016

Outlook and Market Review First Quarter 2016 The U.S. economy grew at a 0.8% annual rate in the first quarter according to thesecond estimate of the Bureau of Economic Analysis. U.S. economic growth in

Outlook and Market Review First Quarter 2016 The U.S. economy grew at a 0.8% annual rate in the first quarter according to thesecond estimate of the Bureau of Economic Analysis. U.S. economic growth in

Manufacturing Barometer

www.pwc.com Manufacturing Barometer Business outlook report April 2014 Special topic: Energy costs Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 6 1.1 Manufacturing current

www.pwc.com Manufacturing Barometer Business outlook report April 2014 Special topic: Energy costs Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 6 1.1 Manufacturing current

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

Global PMI. Global economy buoyed by rising US strength. June 12 th IHS Markit. All Rights Reserved.

Global PMI Global economy buoyed by rising US strength June 12 th 2018 2 Global PMI rises but also brings signs of slower future growth At 54.0 in May, the headline JPMorgan Global Composite PMI, compiled

Global PMI Global economy buoyed by rising US strength June 12 th 2018 2 Global PMI rises but also brings signs of slower future growth At 54.0 in May, the headline JPMorgan Global Composite PMI, compiled

PFSi Historical Measurement

Personal Financial Satisfaction Index (PFSi) Defined The Personal Financial Satisfaction Index (PFSi) is the result of two component sub-indexes. It is calculated as the difference between the Personal

Personal Financial Satisfaction Index (PFSi) Defined The Personal Financial Satisfaction Index (PFSi) is the result of two component sub-indexes. It is calculated as the difference between the Personal

The Arkansas Economic Outlook

The Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Arkansas Economic Development Institute, UALR December 1, 2017 Overview Review of Economic Conditions: Output

The Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Arkansas Economic Development Institute, UALR December 1, 2017 Overview Review of Economic Conditions: Output

The Election Economy. November 29, City of Georgetown

The Election Economy November 29, 2016 City of Georgetown More Growth Coming Why are people moving here? Citizens Quality of Life Planning for Growth 100% Renewable Energy by 2018 Transportation Investments

The Election Economy November 29, 2016 City of Georgetown More Growth Coming Why are people moving here? Citizens Quality of Life Planning for Growth 100% Renewable Energy by 2018 Transportation Investments

Charting a New (Economy) Course

Course") Charting a New (Economy) Course Metro Denver 2009 Economic Forecast January 2009 Colorado Outperforms the U.S. 2009 forecast values Colorado United States Job losses less severe -0.4% -1.1% Unemployment

Charting a New (Economy) Course Metro Denver 2009 Economic Forecast January 2009 Colorado Outperforms the U.S. 2009 forecast values Colorado United States Job losses less severe -0.4% -1.1% Unemployment

AICPA Business & Industry U.S. Economic Outlook Survey 4Q 2014

AICPA Business & Industry U.S. Economic Outlook Survey 4Q 2014 The CPA Outlook Index The CPA Outlook Index (CPAOI) is a broad-based indicator of the strength of US business activity and economic direction

AICPA Business & Industry U.S. Economic Outlook Survey 4Q 2014 The CPA Outlook Index The CPA Outlook Index (CPAOI) is a broad-based indicator of the strength of US business activity and economic direction

Manufacturing Barometer

Special topic: Robotics systems Manufacturing Barometer Business outlook report April 2015 Contents 1 Quarterly highlights 1.1 Key indicators for the business outlook 7 1.2 Manufacturing current assessment

Special topic: Robotics systems Manufacturing Barometer Business outlook report April 2015 Contents 1 Quarterly highlights 1.1 Key indicators for the business outlook 7 1.2 Manufacturing current assessment

Southwest Colorado Business Forum Business Research Division Leeds School of Business

Southwest Colorado Business Forum 2008 Dr. Richard L. Wobbekind Associate Dean of MBA and Enterprise Programs and Executive Director of the Business Research Division, Leeds School of Business Colorado

Southwest Colorado Business Forum 2008 Dr. Richard L. Wobbekind Associate Dean of MBA and Enterprise Programs and Executive Director of the Business Research Division, Leeds School of Business Colorado

2012 Owasso Economic Outlook

Center for Applied Economic Research Center for Applied Economic Research 2012 Owasso Economic Outlook Prepared by Mouhcine Guettabi Research Economist Dan S. Rickman Regents Professor of Economics Oklahoma

Center for Applied Economic Research Center for Applied Economic Research 2012 Owasso Economic Outlook Prepared by Mouhcine Guettabi Research Economist Dan S. Rickman Regents Professor of Economics Oklahoma

A Closer Look at Gross Domestic Product by MSA. Spartanburg. Charleston. Greenville. South Carolina. Hilton Head Island. Columbia.

December Summary s economy improved somewhat, according to recent reports. Payroll employment grew substantially and housing market reports were generally positive while household conditions were mostly

December Summary s economy improved somewhat, according to recent reports. Payroll employment grew substantially and housing market reports were generally positive while household conditions were mostly

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

A More Dovish Fed Helps Improve Economic and Housing Market Conditions

Light Vehicle Retail Sales [Imported+Domestic] (SAAR, Mil. Units) Economic Developments February 2018 A More Dovish Fed Helps Improve Economic and Housing Market Conditions Over the full year of 2019 we

Light Vehicle Retail Sales [Imported+Domestic] (SAAR, Mil. Units) Economic Developments February 2018 A More Dovish Fed Helps Improve Economic and Housing Market Conditions Over the full year of 2019 we

U.S. Economic Update and Outlook. Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 2013

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

U.S. Equipment & Software Investment Momentum Monitor

U.S. Equipment & Software Investment Momentum Monitor June 2018 CONTACT INFORMATION: Kelli Nienaber, Executive Director Equipment Leasing & Finance Foundation knienaber@elfaonline.org www.leasefoundation.org

U.S. Equipment & Software Investment Momentum Monitor June 2018 CONTACT INFORMATION: Kelli Nienaber, Executive Director Equipment Leasing & Finance Foundation knienaber@elfaonline.org www.leasefoundation.org

U.S. Economic Slowdown Expected through 1999

!" #$$% !" U.S. Economic Slowdown Expected through 1999 U.S. FORECAST Current Economic Conditions The strong expansion enjoyed by the U.S. economy since 1991 has now slowed considerably, and in light of

!" #$$% !" U.S. Economic Slowdown Expected through 1999 U.S. FORECAST Current Economic Conditions The strong expansion enjoyed by the U.S. economy since 1991 has now slowed considerably, and in light of

Manufacturing Barometer Business outlook report January 2012

www.pwc.com Manufacturing Barometer Business outlook report January 2012 Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 2 Economic views 2.1 View of US economy, this

www.pwc.com Manufacturing Barometer Business outlook report January 2012 Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 2 Economic views 2.1 View of US economy, this

The Beige Book. Summary of Economic Activity

The Beige Book Eighth District January 2018 Summary of Economic Activity Reports from contacts indicate that economic conditions have continued to improve at a modest pace since our previous report. Labor

The Beige Book Eighth District January 2018 Summary of Economic Activity Reports from contacts indicate that economic conditions have continued to improve at a modest pace since our previous report. Labor

NFIB SMALL BUSINESS. William C. Dunkelberg Holly Wade SMALL BUSINESS OPTIMISM INDEX COMPONENTS. Seasonally Adjusted Level

NFIB SMALL BUSINESS ECONOMIC TRENDS William C. Dunkelberg Holly Wade April 218 Based on a Survey of Small and Independent Business Owners SMALL BUSINESS OPTIMISM INDEX COMPONENTS Index Component Seasonally

NFIB SMALL BUSINESS ECONOMIC TRENDS William C. Dunkelberg Holly Wade April 218 Based on a Survey of Small and Independent Business Owners SMALL BUSINESS OPTIMISM INDEX COMPONENTS Index Component Seasonally

Global PMI. Global economic growth kicks higher at start of fourth quarter but outlook darkens. November 14 th 2016

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

Manufacturing Barometer Business outlook report October 2012

www.pwc.com Manufacturing Barometer Business outlook report October 2012 Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 1.1 Manufacturing current assessment and outlook

www.pwc.com Manufacturing Barometer Business outlook report October 2012 Contents 1 Quarterly highlights Page 1.1 Key indicators for the business outlook 5 1.1 Manufacturing current assessment and outlook

New England Economic Partnership May 2013: Massachusetts

Executive Summary and Highlights MASSACHUSETTS ECONOMIC OUTLOOK The Massachusetts economy is in the fourth year of the expansion that began in the summer of 2009. During this expansion, real gross state

Executive Summary and Highlights MASSACHUSETTS ECONOMIC OUTLOOK The Massachusetts economy is in the fourth year of the expansion that began in the summer of 2009. During this expansion, real gross state

Banks at a Glance: Economic and Banking Highlights by State 2Q 2018

Economic and Banking Highlights by State 2Q 2018 These semi-annual reports highlight key indicators of economic and banking conditions within each of the nine states comprising the 12th Federal Reserve

Economic and Banking Highlights by State 2Q 2018 These semi-annual reports highlight key indicators of economic and banking conditions within each of the nine states comprising the 12th Federal Reserve

Housingmarket. Tennessee. 2nd Quarter Business and Economic Research Center David Penn, Ph.D., Associate Professor, Economics

Tennessee Housingmarket 2nd Quarter 214 Business and Economic Research Center David Penn, Ph.D., Associate Professor, Economics Supported by Tennessee Housing Development Agency Economic Overview ennessee

Tennessee Housingmarket 2nd Quarter 214 Business and Economic Research Center David Penn, Ph.D., Associate Professor, Economics Supported by Tennessee Housing Development Agency Economic Overview ennessee

SEMA INDUSTRY INDICATORS

SEMA INDUSTRY INDICATORS SEPTEMBER 2018 The U.S. economy is looking good as we head into September. August brought another solid month of job gains - adding 201,000 new jobs during the month. The economy

SEMA INDUSTRY INDICATORS SEPTEMBER 2018 The U.S. economy is looking good as we head into September. August brought another solid month of job gains - adding 201,000 new jobs during the month. The economy

Boost from Fiscal Policy to Fade in 2019

Real PCE: Motor Vehicles & Parts (SAAR, 29$, Annualized % Change) Regular Grade, Avg Dollars per Gallon Economic Developments May 28 Boost from Fiscal Policy to Fade in 29 First quarter economic growth

Real PCE: Motor Vehicles & Parts (SAAR, 29$, Annualized % Change) Regular Grade, Avg Dollars per Gallon Economic Developments May 28 Boost from Fiscal Policy to Fade in 29 First quarter economic growth

DALLAS-FORT WORTH METRO

METRO FOURTH QUARTER 2017 Economic Growth Beats Expectations More jobs added than any other metro According to the Texas Workforce Commission, the Dallas-Fort Worth (DFW) economy led the nation by adding

METRO FOURTH QUARTER 2017 Economic Growth Beats Expectations More jobs added than any other metro According to the Texas Workforce Commission, the Dallas-Fort Worth (DFW) economy led the nation by adding