Baseline U.S. Economic Outlook, Summary Table*

|

|

|

- Archibald Benson

- 5 years ago

- Views:

Transcription

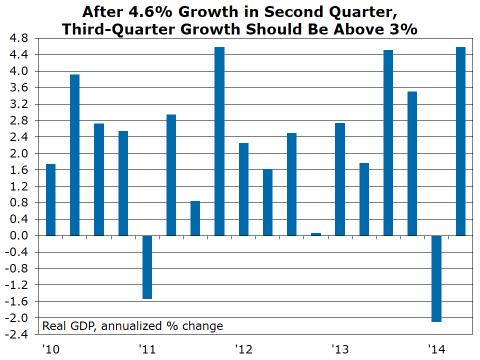

1 October 2014 Solid U.S. Economic Data Belie Market Turmoil Executive Summary September payroll job growth was above consensus with 248,000 jobs added over the month. September private-sector employment was up by 236,000, while government jobs were up by 12,000, with state and local government jobs up by 14,000 and Federal government jobs down by 2,000. As expected based on the past three years, August payroll job growth was revised up to 180,000 (from 142,000), and July job gains were revised up to 243,000 (from 212,000), for a total upward revision of 69,000, in addition to the 248,000 jobs added in September. So far in 2014 the U.S. has added an average of 227,000 jobs per month. The unemployment rate fell to 5.9 percent in September, to its lowest level since July 2008, just before the Financial Crisis. Inflation-adjusted (real) GDP growth in the second quarter was 4.6 percent at an annual rate, according to the third estimate from the Bureau of Labor Statistics. This was the second upward revision to second quarter growth; it was 4.0 percent in the advance estimate and 4.2 percent in the second estimate. The 4.6 percent second quarter gain was the biggest since the fourth quarter of In the first quarter of 2014 the economy contracted 2.1 percent. On a year-ago basis real GDP was up 2.6 percent in the second quarter. Real gross domestic income, an alternative measure of the size of the economy that looks at income going to households and firms, rose even more strongly in the second quarter. It increased an annualized 5.2 percent, an upward revision from 4.7 percent in the second estimate. GDI fell 0.8 percent in the first quarter. On a year-ago basis GDI was up 2.0 percent in the second quarter. U.S. stock prices fell sharply in mid-october, but have recovered somewhat. In addition to worries about the global economy, particularly weaker numbers from Europe, there have also been geopolitical concerns, including conflict in the Middle East and the potential spread of the Ebola virus. Falling oil prices and the potential for slower inflation have also weighed on long-term interest rates, with the yield on the 10-year Treasury briefly falling below 2.0 percent earlier this week, before recovering somewhat, to around 2.2 percent, still very low on an historical basis. But the fundamentals of the U.S. economy remain solid, with no indications of a significant slowdown in growth. The labor market continues its improvement, which will support gains in consumer spending. Businesses are boosting hiring and investment to keep up with improving demand. The housing market continues its slow recovery. And lower energy prices are a net positive for the U.S. economy. Baseline U.S. Economic Outlook, Summary Table* 1Q'14a 2Q'14a 3Q'14f 4Q'14f 1Q'15f 2Q'15f 3Q'15f 4Q'15f 2013a 2014f 2015f 2016f Output & Prices Real GDP (Chained 2009 Billions $ ) Percent Change Annualized CPI ( = 100 ) Percent Change Annualized Labor Markets Payroll Jobs (Millions ) Percent Change Annualized Unemployment Rate (Percent ) Interest Rates (Percent) Federal Funds Treasury Note, 10-year a = actual f = forecast p = preliminary * Please see the Expanded Table for more forecast series.

2 PNC Survey Finds More Small Business Owners Plan Pay Raises and Price Hikes An increasing number of U.S. small and mid-sized business owners plan to raise salaries and prices at rates higher than national trends and above the Federal Reserve s inflation trigger, according to the latest PNC Economic Outlook Survey findings. The Autumn findings of PNC s biannual survey, which began in 2003, reveal that two out of five (38 percent) business owners expect to increase employee compensation in the next six months, which is the most since This is a significant spike since Spring (32 percent) and one year ago (22 percent). Of those that plan raises, three in five (59 percent) plan wage hikes of three percent or more, which exceeds recent national wage trend growth of near two percent. Meanwhile, 38 percent plan to raise selling prices during the next year as they attempt to preserve profit margins and withstand rising supplier costs. Of those that plan hikes, 31 percent will increase prices 1-2 percent, while 40 percent intend to increase by 3-4 percent, in excess of the Federal Reserve s two percent inflation target. Business owners optimism about their own company s prospects is steady as 85 percent are optimistic, on par with 87 percent in the Spring. More than one-half (52 percent) expect sales to increase during the next six months and three of four expect growth of three percent or more. Of the 45 percent who expect profits to rise, three in five expect gains of three percent or more. Wage growth has been a missing piece of the labor market puzzle to date. With more business owners planning pay raises and higher prices for customers, these findings strongly support PNC s forecast for a faster economic and jobs expansion and also send important signals to Fed policy makers that the economic recovery is speeding up. The number of businesses that plan to hire is unchanged, but those that will aim to substantially grow their workforce. Twenty percent plan to add full-time employees compared to 22 percent six months ago and up from 16 percent one year ago. Of those hiring, the majority (61 percent) plan to add one to five employees, which is sizable, given that three-quarters of these businesses have fewer than 50 full-time employees. Of the 78 percent not hiring, over one-half (52 percent) need sales to increase at least three percent to add more employees. Two in 10 say the U.S. economy s lack of improvement is a key reason why they have not hired. Meanwhile, 28 percent of respondents said that finding qualified employees is harder than it was six months ago, up significantly from 20 percent in Autumn Nearly one in five small business owners surveyed (17 percent) will probably/definitely take out a new loan or line of credit in the next six months, up slightly from 15 percent in the Spring. One-fifth (21 percent) report that credit is easier to get relative to three months ago, compared to 17 percent who say it is more difficult. This is the first time since 2006 that the number saying easier is larger than the number saying more difficult. One factor that could hold small business back is confusion over the Affordable Care Act. Among owners with at least 50 employees, nearly two-thirds (64 percent) say they are not entirely sure how the ACA applies to their business. Nearly four in ten (42 percent) say it will impact their business in the next six months, with almost all (93 percent) saying the impact will be negative. The gradual recovery in small business sentiment is consistent with PNC s forecast for solid economic growth in the fourth quarter of 2014 and into Job growth and low interest rates will support consumer spending, the housing market recovery, and business investment. With exports benefitting from a gradually improving global economy, PNC forecasts real GDP growth of around 3 percent per annum in the fourth quarter of 2014 and throughout With growth above trend, but the labor force expanding, the unemployment rate will end this year at around 5.8 percent, and slowly decline to around 5.5 percent at the end of Visit to view the full listing of economic reports published by PNC s economists.

3 Visit to view the full listing of economic reports published by PNC s economists. 3

4 Visit to view the full listing of economic reports published by PNC s economists. Disclaimer: The material presented is of a general nature and does not constitute the provision of investment or economic advice to any person, or a recommendation to buy or sell any security or adopt any investment strategy. Opinions and forecasts expressed herein are subject to change without notice. Relevant information was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy. You should seek the advice of an investment professional to tailor a financial plan to your particular needs The PNC Financial Services Group, Inc. All rights reserved. 4

5 PNC Economics Group October, 2014 Baseline U.S. Economic Outlook, Expanded Table 1Q'14a 2Q'14a 3Q'14f 4Q'14f 1Q'15f 2Q'15f 3Q'15f 4Q'15f 2013a 2014f 2015f 2016f Output Nominal GDP (Billions $ ) Percent Change Annualized Real GDP (Chained 2009 Billions $ ) Percent Change Annualized Pers. Consumption Expenditures Percent Change Annualized Nonresidential Fixed Investment Percent Change Annualized Residential Investment Percent Change Annualized Change in Private Inventories Net Exports Government Expenditures Percent Change Annualized Industrial Prod. Index (2007 = 100 ) Percent Change Annualized Capacity Utilization (Percent ) Prices CPI ( = 100 ) Percent Change Annualized Core CPI Index ( = 100) Percent Change Annualized PCE Price Index (2009 = 100 ) Percent Change Annualized Core PCE Price Index (2009 = 100 ) Percent Change Annualized GDP Price Index (2009 = 100 ) Percent Change Annualized Crude Oil, WTI ($/Barrel ) Labor Markets Payroll Jobs (Millions ) Percent Change Annualized Unemployment Rate (Percent ) Average Weekly Hours, Prod. Works Personal Income Average Hourly Earnings ($ ) Percent Change Annualized Real Disp. Income (2009 Billions $ ) Percent Change Annualized Housing Housing Starts (Ths., Ann. Rate ) Ext. Home Sales (Ths., Ann Rate ) New SF Home Sales (Ths., Ann Rate ) Case/Shiller HPI (Jan = 100 ) Percent Change Year Ago Consumer Household Economic Stress Index Auto Sales (Millions ) Consumer Credit (Billions $ ) Percent Change Annualized Interest Rates (Percent) Prime Rate Federal Funds Month Treasury Bill Year Treasury Note Year Fixed Mortgage a = actual f = forecast p = preliminary Visit to view the full listing of economic reports published by PNC s economists. Disclaimer: The material presented is of a general nature and does not constitute the provision of investment or economic advice to any person, or a recommendation to buy or sell any security or adopt any investment strategy. Opinions and forecasts expressed herein are subject to change without notice. Relevant information was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy. You should seek the advice of an investment professional to tailor a financial plan to your particular needs The PNC Financial Services Group, Inc. All rights reserved.

Baseline U.S. Economic Outlook, Summary Table*

January 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Great December Jobs Report;

January 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Great December Jobs Report;

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist.

January 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Another Fed Rate Hike in December, Inflation Remains

January 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Another Fed Rate Hike in December, Inflation Remains

Baseline U.S. Economic Outlook, Summary Table*

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

November 2014 Solid October Jobs Report Boosts Workers Incomes real Baseline U.S. Economic Outlook, Summary Table*

November 21 Executive Summary Solid October Jobs Report Boosts Workers Incomes October payroll jobs growth was a "soft" 21, jobs. Private-sector employment was up by 2, jobs, while state and local government

November 21 Executive Summary Solid October Jobs Report Boosts Workers Incomes October payroll jobs growth was a "soft" 21, jobs. Private-sector employment was up by 2, jobs, while state and local government

Baseline U.S. Economic Outlook, Summary Table*

December 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Continued Solid Job Growth;

December 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Continued Solid Job Growth;

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

August 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Excellent Second Quarter Growth as Labor Market Continues

August 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Excellent Second Quarter Growth as Labor Market Continues

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

March 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Job Growth Picks Up in 218, Inflation Pressures Are Building

March 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Job Growth Picks Up in 218, Inflation Pressures Are Building

Baseline U.S. Economic Outlook, Summary Table*

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

May 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary With Job Market in Good Shape,

May 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary With Job Market in Good Shape,

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

May 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Slower but Still Solid Economic Growth in the First Quarter;

May 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Slower but Still Solid Economic Growth in the First Quarter;

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

September 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Slows in August,

September 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Slows in August,

NATIONAL ECONOMIC OUTLOOK

May 218 NATIONAL ECONOMIC OUTLOOK Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist THE PNC FINANCIAL SERVICES GROUP The Tower at PNC

May 218 NATIONAL ECONOMIC OUTLOOK Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist THE PNC FINANCIAL SERVICES GROUP The Tower at PNC

NATIONAL ECONOMIC OUTLOOK

November 2017 NATIONAL ECONOMIC OUTLOOK Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist THE PNC FINANCIAL

November 2017 NATIONAL ECONOMIC OUTLOOK Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist THE PNC FINANCIAL

2015: FINALLY, A STRONG YEAR

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

il 27, 2018 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist The U.S. economy expanded 2.3 percent at a seasonally-adjusted annualized

il 27, 2018 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist The U.S. economy expanded 2.3 percent at a seasonally-adjusted annualized

The President s Report to the Board of Directors

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

JOB SITUATION INCOME. 3 rd Quarter 2015 PITTSBURGH

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

Modest Economic Growth and Falling GDP Gap

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

Economic Growth Expected to Slow and Housing to Stabilize in 2019

Consumer Confidence Expectations in the Next Six Months (%) Economic Developments December 218 Economic Growth Expected to Slow and Housing to Stabilize in 219 The U.S. economy is expected to grow 2.6

Consumer Confidence Expectations in the Next Six Months (%) Economic Developments December 218 Economic Growth Expected to Slow and Housing to Stabilize in 219 The U.S. economy is expected to grow 2.6

Economic and Housing Outlook 1. William Strauss, Senior Economist and Economic Advisor Federal Reserve Bank of Chicago. Economic and Housing Outlook

Economic and Housing Outlook Builder Chicago, IL May, William Strauss Senior Economist and Economic Advisor The Great Recession ended in June, but the economy expanded by just.% over the past year Real

Economic and Housing Outlook Builder Chicago, IL May, William Strauss Senior Economist and Economic Advisor The Great Recession ended in June, but the economy expanded by just.% over the past year Real

Consolidated Investment Report

Consolidated Investment Report September 2015 As Palm Beach County s Chief Financial Officer, the Clerk & Comptroller is charged with safeguarding and investing all County funds. The Clerk s management

Consolidated Investment Report September 2015 As Palm Beach County s Chief Financial Officer, the Clerk & Comptroller is charged with safeguarding and investing all County funds. The Clerk s management

MACROECONOMIC INSIGHTS

MACROECONOMIC INSIGHTS U.S. ECONOMIC OUTLOOK 13 July 2018 On the Banking System, Monetary Policy & Regulation Since the recession ended in June 2009, the growth rate for loans and leases extended by all

MACROECONOMIC INSIGHTS U.S. ECONOMIC OUTLOOK 13 July 2018 On the Banking System, Monetary Policy & Regulation Since the recession ended in June 2009, the growth rate for loans and leases extended by all

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist The government shutdown that began at the end of 2018 and

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist The government shutdown that began at the end of 2018 and

Provided to you by Lee McLain

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of October 22, 2018 Economic Calendar - week of October

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of October 22, 2018 Economic Calendar - week of October

Economic Review Fourth Quarter 2017

Economic Review Fourth Quarter 2017 The state of the general economy can help or hinder a business prospects by influencing the demand for its goods and services and the availability and price of inputs

Economic Review Fourth Quarter 2017 The state of the general economy can help or hinder a business prospects by influencing the demand for its goods and services and the availability and price of inputs

In fiscal year 2016, for the first time since 2009, the

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

US Economy Update May 2014

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

file:///c:/users/cathy/appdata/local/microsoft/windows/temporary Int...

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

21, 2017 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Housing starts rose 8.3 percent in to 1.215 million

21, 2017 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Housing starts rose 8.3 percent in to 1.215 million

Consensus Forecast for 2011

Consensus Forecast for 2011 William Strauss Senior Economist and Economic Advisor Review of past performance 1 The growth in real GDP came in initially at a faster pace than was anticipated quarterly forecasts

Consensus Forecast for 2011 William Strauss Senior Economist and Economic Advisor Review of past performance 1 The growth in real GDP came in initially at a faster pace than was anticipated quarterly forecasts

Consensus Forecast 2010 and 2011

Consensus Forecast 2010 and 2011 Seventeenth Annual Automotive Outlook Symposium Detroit, Michigan June 4, 2010 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Review

Consensus Forecast 2010 and 2011 Seventeenth Annual Automotive Outlook Symposium Detroit, Michigan June 4, 2010 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Review

Danske Bank October 2015 Economic Update,

Monthly update: 5 October 2015 Danske Bank Chief Economist, Twitter: angela_mcgowan www.danskebank.co.uk/ec Local job and investment announcements during September 2015 Over the month of September there

Monthly update: 5 October 2015 Danske Bank Chief Economist, Twitter: angela_mcgowan www.danskebank.co.uk/ec Local job and investment announcements during September 2015 Over the month of September there

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Second Quarter 2016 Volume 9, number 2 colorado.edu/business/brd

Second Quarter 2016 Volume 9, number 2 colorado.edu/business/brd Summary Stable Expectations The panel of business leaders surveyed in the Leeds Business Confidence Index (LBCI) reported steady optimism

Second Quarter 2016 Volume 9, number 2 colorado.edu/business/brd Summary Stable Expectations The panel of business leaders surveyed in the Leeds Business Confidence Index (LBCI) reported steady optimism

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 2018

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Stronger Q2, Less Drag from Energy, Labor Stutter Freezes Fed

Economic Outlook: C Balance of Risk: Stronger Q, Less Drag from Energy, Labor Stutter Freezes Fed Recent economic data has generally been positive. The very weak first quarter real GDP growth has been

Economic Outlook: C Balance of Risk: Stronger Q, Less Drag from Energy, Labor Stutter Freezes Fed Recent economic data has generally been positive. The very weak first quarter real GDP growth has been

Boost from Fiscal Policy to Fade in 2019

Real PCE: Motor Vehicles & Parts (SAAR, 29$, Annualized % Change) Regular Grade, Avg Dollars per Gallon Economic Developments May 28 Boost from Fiscal Policy to Fade in 29 First quarter economic growth

Real PCE: Motor Vehicles & Parts (SAAR, 29$, Annualized % Change) Regular Grade, Avg Dollars per Gallon Economic Developments May 28 Boost from Fiscal Policy to Fade in 29 First quarter economic growth

LETTER. economic. Explaining price variances between Canada and the United States MARCH bdc.ca

economic LETTER MARCH 212 Explaining price variances between Canada and the United States With an exchange rate at par with the U.S. dollar, it s easy for Canadian consumers to compare prices for similar

economic LETTER MARCH 212 Explaining price variances between Canada and the United States With an exchange rate at par with the U.S. dollar, it s easy for Canadian consumers to compare prices for similar

Smith Leonard PLLC Kenneth D. Smith, CPA Mark S. Laferriere, CPA

Smith Leonard PLLC s Industry Newsletter January 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A ccording to our latest survey of residential furniture manufacturers and distributors, new orders in November 2017

Smith Leonard PLLC s Industry Newsletter January 2018 HIGHLIGHTS - EXECUTIVE SUMMARY A ccording to our latest survey of residential furniture manufacturers and distributors, new orders in November 2017

Growth May Slow to End 2016 But Sentiment Brightens

Economic Developments December 2016 Growth May Slow to End 2016 But Sentiment Brightens We expect economic growth to moderate to less than two percent this quarter, with full-year 2016 growth at 1.8 percent.

Economic Developments December 2016 Growth May Slow to End 2016 But Sentiment Brightens We expect economic growth to moderate to less than two percent this quarter, with full-year 2016 growth at 1.8 percent.

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

Outlook and Market Review Fourth Quarter 2013

Outlook and Market Review Fourth Quarter 2013 Economic growth remains sluggish and inflation is not on the radar screen. The Bureau of Economic Analysis revised fourth quarter GDP growth to a 2.4% rate

Outlook and Market Review Fourth Quarter 2013 Economic growth remains sluggish and inflation is not on the radar screen. The Bureau of Economic Analysis revised fourth quarter GDP growth to a 2.4% rate

Interest Rate Forecast

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Ontario Economic Accounts

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

Market Month: July 2017

Market Month: July 2017 The Markets (as of market close July 31, 2017) The last day of July saw each of the indexes listed here post gains over their June closing values. Despite slumping tech stocks at

Market Month: July 2017 The Markets (as of market close July 31, 2017) The last day of July saw each of the indexes listed here post gains over their June closing values. Despite slumping tech stocks at

NFIB SMALL BUSINESS. William C. Dunkelberg Holly Wade SMALL BUSINESS OPTIMISM INDEX COMPONENTS. Seasonally Adjusted Level

NFIB SMALL BUSINESS ECONOMIC TRENDS William C. Dunkelberg Holly Wade April 218 Based on a Survey of Small and Independent Business Owners SMALL BUSINESS OPTIMISM INDEX COMPONENTS Index Component Seasonally

NFIB SMALL BUSINESS ECONOMIC TRENDS William C. Dunkelberg Holly Wade April 218 Based on a Survey of Small and Independent Business Owners SMALL BUSINESS OPTIMISM INDEX COMPONENTS Index Component Seasonally

Minutes of the Monetary Policy Committee meeting November 2010

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting November 2010 Published: 17 November 2010 The Act on the Central Bank of Iceland stipulates

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting November 2010 Published: 17 November 2010 The Act on the Central Bank of Iceland stipulates

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS Comptroller Kevin Lembo today said that there are reasons for cautious optimism that the state could end Fiscal

COMPTROLLER LEMBO REPORTS EARLY INDICATIONS THAT STATE COULD END FISCAL YEAR 2019 IN SURPLUS Comptroller Kevin Lembo today said that there are reasons for cautious optimism that the state could end Fiscal

Monthly Economic Indicators And Charts

Monthly Economic Indicators And Charts June Richard F. Moody- Chief Economist Steve Pfitzer Investor Relations Information contained herein is based on data obtained from recognized sources believed to

Monthly Economic Indicators And Charts June Richard F. Moody- Chief Economist Steve Pfitzer Investor Relations Information contained herein is based on data obtained from recognized sources believed to

Main Economic & Financial Indicators Poland

Main Economic & Financial Indicators Poland. 6 OCTOBER 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Main Economic & Financial Indicators Poland. 6 OCTOBER 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Market Month: April 2017

Market Month: April 2017 The Markets (as of market close April 28, 2017) Equities continued their positive trend in April, spurred by favorable corporate earnings reports, proposed federal tax cuts, and

Market Month: April 2017 The Markets (as of market close April 28, 2017) Equities continued their positive trend in April, spurred by favorable corporate earnings reports, proposed federal tax cuts, and

The Outlook for the U.S. Economy March Summary View. The Current State of the Economy

The Outlook for the U.S. Economy March 2010 Summary View The Current State of the Economy 8% 6% Quarterly Change (SAAR) Chart 1. The Economic Outlook History Forecast The December 2007-2009 recession is

The Outlook for the U.S. Economy March 2010 Summary View The Current State of the Economy 8% 6% Quarterly Change (SAAR) Chart 1. The Economic Outlook History Forecast The December 2007-2009 recession is

Consensus Forecast 2004 and 2005

Consensus Forecast 2004 and 2005 Eleventh Annual Auto Outlook Symposium Detroit, Michigan June 4, 2004 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Review of past

Consensus Forecast 2004 and 2005 Eleventh Annual Auto Outlook Symposium Detroit, Michigan June 4, 2004 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Review of past

Growth Picks Up as Expected, No Thanks to Housing

Q1-2008 Q3-2008 Q1-2009 Q3-2009 Q1-2010 Q3-2010 Q1-2011 Q3-2011 Q1-2012 Q3-2012 Q1-2013 Q3-2013 Q1-2014 Q3-2014 Q1-2015 Q3-2015 Q1-2016 Q3-2016 Q1-2017 Q3-2017 Q1-2018 Personal Saving Rate (SA) Personal

Q1-2008 Q3-2008 Q1-2009 Q3-2009 Q1-2010 Q3-2010 Q1-2011 Q3-2011 Q1-2012 Q3-2012 Q1-2013 Q3-2013 Q1-2014 Q3-2014 Q1-2015 Q3-2015 Q1-2016 Q3-2016 Q1-2017 Q3-2017 Q1-2018 Personal Saving Rate (SA) Personal

Growth to accelerate. A quarterly analysis of trends in the Irish economy

Produced by the Economic Research Unit July 2014 A quarterly analysis of trends in the Irish economy Growth to accelerate Strong start to 2014 Recovery becoming more broad-based GDP growth revised up for

Produced by the Economic Research Unit July 2014 A quarterly analysis of trends in the Irish economy Growth to accelerate Strong start to 2014 Recovery becoming more broad-based GDP growth revised up for

World Economic outlook

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom Michael Dolega Senior Economist, TD Economics 15 Annual MEREDA Forecast Conference Portland, Maine January, 15 Key Themes Global economic

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom Michael Dolega Senior Economist, TD Economics 15 Annual MEREDA Forecast Conference Portland, Maine January, 15 Key Themes Global economic

LETTER. economic. Canada and the global financial crisis SEPTEMBER bdc.ca

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

MACROECONOMIC FORECAST

MACROECONOMIC FORECAST Spring 17 Ministry of Finance of the Republic of Bulgaria Bulgarian economy is expected to expand by 3% in 17 driven by domestic demand. As compared to 16, the external sector will

MACROECONOMIC FORECAST Spring 17 Ministry of Finance of the Republic of Bulgaria Bulgarian economy is expected to expand by 3% in 17 driven by domestic demand. As compared to 16, the external sector will

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

FOMC Stresses Importance of Data-Dependent Policy in October Minutes

Economic Analysis FOMC Stresses Importance of Data-Dependent Policy in October Minutes Kim Fraser Chase The minutes from October s FOMC meeting revealed some further discussion on forward guidance and

Economic Analysis FOMC Stresses Importance of Data-Dependent Policy in October Minutes Kim Fraser Chase The minutes from October s FOMC meeting revealed some further discussion on forward guidance and

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated quarterly to reflect the current economic outlook for factors that typically impact

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated quarterly to reflect the current economic outlook for factors that typically impact

NAM MANUFACTURERS OUTLOOK SURVEY THIRD QUARTER 2017 September 29, 2017

NAM MANUFACTURERS OUTLOOK SURVEY THIRD QUARTER 2017 September 29, 2017 Percentage of Respondents Positive in Their Own Company s Outlook 89.8% (June: 89.5%) Small Manufacturers: 85.1% (June: 84.8%) Medium-Sized

NAM MANUFACTURERS OUTLOOK SURVEY THIRD QUARTER 2017 September 29, 2017 Percentage of Respondents Positive in Their Own Company s Outlook 89.8% (June: 89.5%) Small Manufacturers: 85.1% (June: 84.8%) Medium-Sized

The Mid-Year Economic Forecast. June 20, 2018

The Mid-Year Economic Forecast June 20, 2018 Agenda National Economy: On a Solid Footing Construction & Housing: Still Strong Risks: What Could Go Wrong? 2 National Economy On a Solid Footing 3 GDP Grew

The Mid-Year Economic Forecast June 20, 2018 Agenda National Economy: On a Solid Footing Construction & Housing: Still Strong Risks: What Could Go Wrong? 2 National Economy On a Solid Footing 3 GDP Grew

LETTER. economic. The price of oil and prices at the pump: why the difference? NOVEMBER bdc.ca

economic LETTER NOVEMBER 211 The price of oil and prices at the pump: why the difference? Since the end of April the price of crude oil based on the West Texas Intermediate (WTI) benchmark has dropped

economic LETTER NOVEMBER 211 The price of oil and prices at the pump: why the difference? Since the end of April the price of crude oil based on the West Texas Intermediate (WTI) benchmark has dropped

Jan F Qvigstad: Outlook for the Norwegian economy

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Monetary Policy Update December 2007

Monetary Policy Update December 7 At its meeting on 8 December, the Executive Board of the Riksbank decided to hold the repo rate unchanged at per cent. During the first half of 8 it is expected that the

Monetary Policy Update December 7 At its meeting on 8 December, the Executive Board of the Riksbank decided to hold the repo rate unchanged at per cent. During the first half of 8 it is expected that the

The real change in private inventories added 0.15 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

IMF Executive Board Concludes Article IV Consultation with United States

Tuesday 12 th July 2016 11:30 am International Prepared by: Ravi Kurjah, Analyst II, First Citizens Research and Analytics Ravi.Kurjah@firstcitizenstt.com IMF Executive Board Concludes Article IV Consultation

Tuesday 12 th July 2016 11:30 am International Prepared by: Ravi Kurjah, Analyst II, First Citizens Research and Analytics Ravi.Kurjah@firstcitizenstt.com IMF Executive Board Concludes Article IV Consultation

Outlook and Market Review First Quarter 2016

Outlook and Market Review First Quarter 2016 The U.S. economy grew at a 0.8% annual rate in the first quarter according to thesecond estimate of the Bureau of Economic Analysis. U.S. economic growth in

Outlook and Market Review First Quarter 2016 The U.S. economy grew at a 0.8% annual rate in the first quarter according to thesecond estimate of the Bureau of Economic Analysis. U.S. economic growth in

SEMA INDUSTRY INDICATORS

SEMA INDUSTRY INDICATORS Economic data strengthened over the last month. The employment report led the way, but across the board incoming economic data was firm, setting up what could be an extremely strong

SEMA INDUSTRY INDICATORS Economic data strengthened over the last month. The employment report led the way, but across the board incoming economic data was firm, setting up what could be an extremely strong

Moderating Growth Expected in the Second Half; Housing Supply Still Lagging

Corporate Profits with IVA and CCAdj (SAAR, $, Year-over-Year % Change) Nominal Broad Trade-Weighted Exchange Value of the US$ Economic Developments July 2017 Moderating Growth Expected in the Second Half;

Corporate Profits with IVA and CCAdj (SAAR, $, Year-over-Year % Change) Nominal Broad Trade-Weighted Exchange Value of the US$ Economic Developments July 2017 Moderating Growth Expected in the Second Half;

2018 U.S. and Rochester Area Economic Outlook. Gary Keith Vice President, Regional Economist Commercial Banking Division January 26, 2018

2018 U.S. and Rochester Area Economic Outlook Gary Keith Vice President, Regional Economist Commercial Banking Division January 26, 2018 Solid Economic Momentum Heading Into 2018 6.5 Number of Non-farm

2018 U.S. and Rochester Area Economic Outlook Gary Keith Vice President, Regional Economist Commercial Banking Division January 26, 2018 Solid Economic Momentum Heading Into 2018 6.5 Number of Non-farm

Economic Developments April 2019 Lower Mortgage Rates and Continued Wage Growth Provide Some Stability for Housing

Economic Developments April 2019 Lower Mortgage Rates and Continued Wage Growth Provide Some Stability for Housing U.S. economic growth is expected to slow from 3.0 percent in 2018 to 2.2 percent in 2019.

Economic Developments April 2019 Lower Mortgage Rates and Continued Wage Growth Provide Some Stability for Housing U.S. economic growth is expected to slow from 3.0 percent in 2018 to 2.2 percent in 2019.

Economic Update. Platts Aluminum Symposium 2014 Ft. Lauderdale, Florida January 13, Chris Oakley Federal Reserve Bank of Atlanta January 2014

1 Economic Update Platts Aluminum Symposium 2014 Ft. Lauderdale, Florida January 13, 2014 Chris Oakley Federal Reserve Bank of Atlanta January 2014 2 Summary of the Economic Environment 1. Economic growth

1 Economic Update Platts Aluminum Symposium 2014 Ft. Lauderdale, Florida January 13, 2014 Chris Oakley Federal Reserve Bank of Atlanta January 2014 2 Summary of the Economic Environment 1. Economic growth

Market Month: January 2018

Market Month: January 2018 The Markets (as of market close January 31, 2018) Equities pulled back off of their record-setting gains at the end of January, but not enough to forestall a month of significant

Market Month: January 2018 The Markets (as of market close January 31, 2018) Equities pulled back off of their record-setting gains at the end of January, but not enough to forestall a month of significant

The Coming Home Equity Line of Credit Crisis

The Coming Home Equity Line of Credit Crisis March 2, 2016 by Gary Halbert of Halbert Wealth Management IN THIS ISSUE: 1. Will HELOCs Trigger the Next Financial Crisis? 2. Millions of HELOCs to Reset in

The Coming Home Equity Line of Credit Crisis March 2, 2016 by Gary Halbert of Halbert Wealth Management IN THIS ISSUE: 1. Will HELOCs Trigger the Next Financial Crisis? 2. Millions of HELOCs to Reset in

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

LETTER. economic COULD INTEREST RATES HEAD UP IN 2015? JANUARY Canada. United States. Interest rates. Oil price. Canadian dollar.

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

Serious Doubts Remain despite Encouraging Signs

APRIL 18, 2019 ECONOMIC & FINANCIAL OUTLOOK Serious Doubts Remain despite Encouraging Signs #1 BEST OVERALL FORECASTER - CANADA HIGHLIGHTS ff The global economy and the volume of trade both remain fragile,

APRIL 18, 2019 ECONOMIC & FINANCIAL OUTLOOK Serious Doubts Remain despite Encouraging Signs #1 BEST OVERALL FORECASTER - CANADA HIGHLIGHTS ff The global economy and the volume of trade both remain fragile,

Leeds Business Confidence Index

Third Quarter 2018 Volume 11, number 3 colorado.edu/business/brd Leeds Business Confidence Steady Ahead of Q3 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Third Quarter 2018 Volume 11, number 3 colorado.edu/business/brd Leeds Business Confidence Steady Ahead of Q3 2018 The Leeds Business Confidence Index (LBCI) captures Colorado business leaders expectations

Bloomberg Survey of Economists

November 2017 Economists Expect Hurricanes to Weigh Down 3Q Data with 4Q Rebound The November Bloomberg Survey of Economists shows few changes to the economic outlook, no changes to the Fed Funds projections,

November 2017 Economists Expect Hurricanes to Weigh Down 3Q Data with 4Q Rebound The November Bloomberg Survey of Economists shows few changes to the economic outlook, no changes to the Fed Funds projections,

W HIGHLIGHTS - EXECUTIVE SUMMARY

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter June 2018 W HIGHLIGHTS - EXECUTIVE SUMMARY e had heard at the High Point Market that business seemed to have picked up a bit. We also heard that

FURNITURE INSIGHTS Smith Leonard PLLC s Industry Newsletter June 2018 W HIGHLIGHTS - EXECUTIVE SUMMARY e had heard at the High Point Market that business seemed to have picked up a bit. We also heard that

Malaysia s Exports Performance Steadied in April Despite Sluggish Global Trade

6 June 2016 MONTHLY ECONOMIC REVIEW May 2016 Malaysia s Exports Performance Steadied in April Despite Sluggish Global Trade Exports were up by 1.6%yoy in April, higher than consensus. This was largely

6 June 2016 MONTHLY ECONOMIC REVIEW May 2016 Malaysia s Exports Performance Steadied in April Despite Sluggish Global Trade Exports were up by 1.6%yoy in April, higher than consensus. This was largely

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

Comparison of FRBNY Staff and Blue Chip Forecasts

Comparison of and Forecasts Real GDP Growth Forecasts % Change (AR) % Change (AR) May Note: The blue band represents the top and bottom averages of the Blue Chip survey. Source: and Economic Indicators

Comparison of and Forecasts Real GDP Growth Forecasts % Change (AR) % Change (AR) May Note: The blue band represents the top and bottom averages of the Blue Chip survey. Source: and Economic Indicators

Editor: Thomas Nilsson. The Week Ahead Key Events 31 Jul 6 Aug, 2017

Editor: Thomas Nilsson The Week Ahead Key Events 31 Jul 6 Aug, 2017 European Sovereign Rating Reviews Recent rating reviews Friday, 21 July 2017 Agency previous new action Greece S&P B- / Stable B- /

Editor: Thomas Nilsson The Week Ahead Key Events 31 Jul 6 Aug, 2017 European Sovereign Rating Reviews Recent rating reviews Friday, 21 July 2017 Agency previous new action Greece S&P B- / Stable B- /

Economic Outlook for FY2010 and FY2011

Economic Outlook for FY2010 and FY2011 (revised to reflect the Second Preliminary Quarterly Estimates of GDP for the Jan-Mar quarter of 2010) June 2010 Key points of Mizuho Research Institute s (MHRI)

Economic Outlook for FY2010 and FY2011 (revised to reflect the Second Preliminary Quarterly Estimates of GDP for the Jan-Mar quarter of 2010) June 2010 Key points of Mizuho Research Institute s (MHRI)

April 13, Economics Research - Globanomics - Q4/16. Globanomics. World s Dashboard of Economic Indicators Q4 2016

April 13, 2017 Economics Research - Globanomics - Q4/16 Globanomics World s Dashboard of Economic Indicators Q4 2016 Globanomics: Global Economic Indicators Q4 16 1 Quarter at a Glance The IMF revised

April 13, 2017 Economics Research - Globanomics - Q4/16 Globanomics World s Dashboard of Economic Indicators Q4 2016 Globanomics: Global Economic Indicators Q4 16 1 Quarter at a Glance The IMF revised

Comments on: Economic Outlook for 2013 Beyond the Fiscal Cliff

Comments on: Economic Outlook for 2013 Beyond the Fiscal Cliff Marc Hayford Department of Economics December 3, 2012 Themes in the Outlook 1 st Theme: Substantial Slack in the U.S. economy 16,000 15,000

Comments on: Economic Outlook for 2013 Beyond the Fiscal Cliff Marc Hayford Department of Economics December 3, 2012 Themes in the Outlook 1 st Theme: Substantial Slack in the U.S. economy 16,000 15,000

NFIB SMALL BUSINESS. William C. Dunkelberg Holly Wade SMALL BUSINESS OPTIMISM INDEX COMPONENTS. Seasonally Adjusted Level

NFIB SMALL BUSINESS ECONOMIC TRENDS William C. Dunkelberg Holly Wade 21 Based on a Survey of Small and Independent Business Owners SMALL BUSINESS OPTIMISM INDEX COMPONENTS Index Component Seasonally Adjusted

NFIB SMALL BUSINESS ECONOMIC TRENDS William C. Dunkelberg Holly Wade 21 Based on a Survey of Small and Independent Business Owners SMALL BUSINESS OPTIMISM INDEX COMPONENTS Index Component Seasonally Adjusted

Austria s economy set to grow by close to 3% in 2018

Austria s economy set to grow by close to 3% in 218 Gerhard Fenz, Friedrich Fritzer, Fabio Rumler, Martin Schneider 1 Economic growth in Austria peaked at the end of 217. The first half of 218 saw a gradual

Austria s economy set to grow by close to 3% in 218 Gerhard Fenz, Friedrich Fritzer, Fabio Rumler, Martin Schneider 1 Economic growth in Austria peaked at the end of 217. The first half of 218 saw a gradual

Fourth Quarter Market Outlook. Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Market Update. May 19, PFM Asset Management LLC 300 South Orange Avenue Suite 1170 Orlando, FL (407) (407) fax

(407) fax") ket Update 19, 25 PFM Asset Management LLC 3 South Orange Avenue Suite 1170 Orlando, FL 328 (407) 648-2208 (407) 648-1323 fax The Economy: Solid Growth GDP grew at 3.1% in the first quarter Follows 3.9%

ket Update 19, 25 PFM Asset Management LLC 3 South Orange Avenue Suite 1170 Orlando, FL 328 (407) 648-2208 (407) 648-1323 fax The Economy: Solid Growth GDP grew at 3.1% in the first quarter Follows 3.9%

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 2017

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

2014 Annual Review & Outlook

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

Current Economic Conditions and Selected Forecasts

Order Code RL30329 Current Economic Conditions and Selected Forecasts Updated May 20, 2008 Gail E. Makinen Economic Policy Consultant Government and Finance Division Current Economic Conditions and Selected

Order Code RL30329 Current Economic Conditions and Selected Forecasts Updated May 20, 2008 Gail E. Makinen Economic Policy Consultant Government and Finance Division Current Economic Conditions and Selected

What s Ahead for the Economy: Choppy Waters or Smooth Sailing?

What s Ahead for the Economy: Choppy Waters or Smooth Sailing? NCSL Legislative Summit 21 Louisville, KY July 27, 21 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

What s Ahead for the Economy: Choppy Waters or Smooth Sailing? NCSL Legislative Summit 21 Louisville, KY July 27, 21 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago