2018 Economic Outlook 2Q Update

|

|

|

- Wilfrid Carson

- 5 years ago

- Views:

Transcription

1 2018 Economic Outlook 2Q Update The Sky Is the Limit And the U.S. Economy Is Closer Dudley Carter Economist, Vining Sparks Craig Dismuke Chief Economist, Vining Sparks

2 Weak Q1 Growth Expected to Fade First quarter growth indicators, specifically those related to the consumer, have been weaker than expected. However, that s after a stellar 4Q for final sales and could also reflect residual seasonality % Weaker durable goods orders Weaker retail sales 0.0 Jan 29 Feb 3 Feb 8 Feb 13 Feb 18 Feb 23 Feb 28 Mar 5 Mar 10 Mar 15 Mar 20 Mar 25 Mar 30 Sources: Federal Reserve Bank of Atlanta, Vining Sparks Weaker durable goods orders Weaker retail sales 2 2.8%

3 Almost All Economic Engines Firing A strong consumer and more favorable business climate created a positive outlook for growth. Global growth also synchronized providing three engines of economic growth. 3 Low Unemployment Decent Wage Growth Low Household Debt Low Gas Prices Record-High Stocks Low Interest Rates Booming Confidence Booming Confidence Deregulation Expectations for Sales Record-High Stocks Low Interest Rates Weaker Dollar Housing Momentum Unprecedented Monetary Stimulus Low Interest Rates Record-High Stocks Synchronized Growth Strong U.S. Economy Federal: 2011 Budget Caps State and Local: Improved Tax Receipts, Property Values CONSUMPTION INVESTMENT GLOBAL GROWTH GOVERNMENT Tax Reform Tax Reform = Stable Outlook / Low Inflation / Patient Fed / Low Rates

4 Job Growth Continues to Beat Forecasts Total nonfarm payroll growth beat expectations again, initially rising 200k in January. The labor market has shown very few signs of slowing despite being almost nine years into the cycle JAN Sources: BLS, Vining Sparks

5 Earnings Growth Shows Traction Three separate measures of wage growth showed traction in late January. While the average hourly earnings data were likely distorted by the weather, inflation fears gripped investors. 3.0% 2.5% Average Hourly Earnings (YoY) Employee Cost Index 5 2.9% 2.6% 2.0% 1.5% 1.0% Sources: BLS, Vining Sparks

6 Fiscal Stimulus Added to Tailwinds Washington agreed to lift spending caps, increasing defense spending by 24% and non-defense spending by 29% over the next two years. This will be another deficit-financed boost to GDP. 15% 10% 5% Government Expenditures by Category (QoQ, SAAR) Previous Federal Spending Caps Replaced by: Defense: +$165 Billion ($80B in 18 / $85B in 19) Non-Defense: +$131 Billion ($63 B in 18 / $68 B in 19) Disaster Relief: +$84.4 Billion Total Government Including State and Local Federal Non-Defense Federal Defense 6 0% -5% Projected GDP Impact: % +0.4% Sources: BEA, Vining Sparks

7 Core CPI Inflation Rises 0.35% MoM Core CPI inflation showed the strongest monthly gain in prices since 2005, rising 0.35% MoM. While some of the increase should prove temporary, it exacerbated investors fears. 0.5% 0.4% 0.3% Core CPI (MoM) Core CPI (YoY) 3.5% 0.351% 0.349% 3.0% 7 2.5% 0.2% 0.1% 0.0% -0.1% 2.0% 1.8% 1.5% 1.0% 0.5% -0.2% % Sources: BLS, Vining Sparks

8 All Economic Engines Firing Add the boost from tax reform and more fiscal stimulus (deficit spending) to an already stable backdrop, and markets began to fear the economy over-heating. 8 Low Unemployment Decent Wage Growth Low Household Debt Low Gas Prices Record-High Stocks Low Interest Rates Booming Confidence Booming Confidence Deregulation Expectations for Sales Record-High Stocks Low Interest Rates Weaker Dollar Housing Momentum Unprecedented Monetary Stimulus Low Interest Rates Record-High Stocks Synchronized Growth Strong U.S. Economy Federal: Raised Budget Caps State and Local: Improved Tax Receipts, Property Values CONSUMPTION INVESTMENT GLOBAL GROWTH GOVERNMENT Tax Reform Tax Reform Fiscal Stimulus = Hot = Stable Outlook Outlook / Risks / Balanced to Inflation Risks / Reactive / Patient Fed // Higher Low Rates

9 Investors Fear Economy Over-Heating Driving longer interest rates have been 1) U.S. fiscal policy developments, 2) central bank actions, 3) geopolitical concerns, and 4) decent economic data French GOP lacks support for healthcare bill, election uncertainty about fiscal reform agenda fears Weak CPI, retail sales start Trump sworn in Fedspeak shifts markets to March Fed hikes Dots unchanged month of weaker economic data French Election Comey memos 2.99% J F M A M J J A S O N D J F M Sources: Bloomberg, Citi Eco Surprise Index, Vining Sparks 1.85% - Pre-Election Yield Fed hikes, hawkish slant, dots unchanged, roll-off cap sizes Senate healthcare failures begin Fed debate on inflation begins Fed announces October start date for roll-off Presidential advisory councils disbanded Fed Balance Sheet Roll-Off ECB Extends QE at 30B/Month BOE Hikes Tax framework ECB, BoE, BoC Irma and Harvey less surprisingly severe than feared hawkish North Korea tests hydrogen bomb Fed hikes Dots unchanged U.S. and Eurozone Eco Data Beating Expectations Tax Bill Passed Progress on Tax Reform 9 Fiscal Stimulus Firmer Inflation Stronger Earnings Economic Surprise Index

10 And Higher Rates Spooked Stocks Despite the sensational news headlines, stocks have recovered and remain well above preelection levels. As a result, the risk of frothy asset prices remains. 50% 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% Percentage Gains since U.S. Election Nasdaq Dow S&P 500 MSCI All-World Index, Ex-U.S. N D J F M A M J J A S O N D J F M Sources: Bloomberg, Vining Sparks Election Jan 26 (YTD) +45.2% (+7.7%) +43.8% (+8.7%) +34.3% (+7.5%) +33.5% (+7.1%) 10 Jan 26-Feb 8 (YTD) -10.4% (-3.5%) -9.7% (-1.8%) -10.2% (-3.5%) -7.8% (-2.8%)

11 Second Wildest Week of the Cycle Combining the intraday percentage trading ranges, those swings ultimately added up to the second wildest week for stocks since the Great Recession. 30% U.S. Debt S&P 500, Weekly Percentage Downgrade 24.92% 25% Trading Range 2010 Flash Inflation Chinese Market Crash Freak Out 20% Turmoil 18.34% 15% 10% 5% 17.72% 16.36% 0% Sources: Bloomberg, Vining Sparks 11

12 Second Wildest Week of the Cycle Combining the intraday percentage trading ranges, those swings ultimately added up to the second wildest week for stocks since the Great Recession. 4.0% 3.0% 2.0% 1.0% 0.0% -1.0% -2.0% -3.0% -4.0% Daily % Change S&P % Sources: Bloomberg, Vining Sparks 8 Days with >1% Move Days with >1% Move

13 Growing Risks to Stability in 2018 The risks to economic stability are growing. As the economy begins to heat up, imbalances are likely to become more pronounced with the largest risk coming from an asset price correction. Inflation runs hotter-than-expected Fed feels they re behind the curve, leading to more a aggressive policy Asset price recalibration stock prices, bond yields, credit spreads, cap rates Volatility excessively suppressed in financial markets, exacerbating future moves Global central banks simultaneously shift to less accommodative posture Geopolitical tensions and trade tensions Mid-term elections creating more political uncertainty Longer-term obstacles Aging population, Federal debt, Weak productivity 13

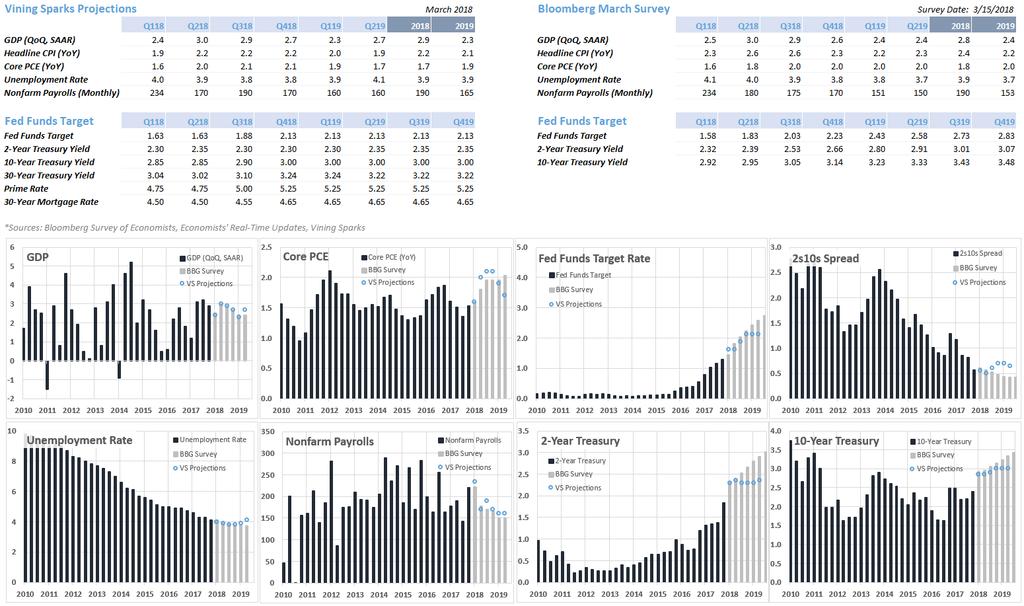

14 Expectations for Fed Rate Hikes The markets are now pricing in three hikes in 2018, but only one or two additional hikes through the end of The Fed continues to project a longer period of rate hikes % Fed Projections March SEP Fed Funds Futures December 29, % Fed Funds Futures March 29, % 2.44% % 2.07% Sources: Fed Funds Futures Contracts, March 2018 Fed SEP Projections, Vining Sparks

15 Unemployment Rate Below Target The Fed is likely to remain hawkish so long as unemployment rate 1) remains below their longerrun sustainable rate, 2) is not rising, and 3) financial conditions do not deteriorate dramatically. 10 Headline Unemployment Rate Fed s Longer-Run Projected Rate 4.1% Sources: BLS, Federal Reserve Summary of Economic Projections, Vining Sparks

16 Less Risk of Disinflation in 2018 There appear to be more risks to a modest acceleration in price gains in 2018 than deceleration. Rising commodity prices, possible wage growth, and a weaker Dollar should push prices higher. 16 $125 $100 $75 $ Oil Price per Barrel $ Trade-Weighted Dollar +46% Since June Small Business Compensation Plans Commodity Prices Highest Since % YoY % Since June Sources: Bloomberg, CRB Core Commodity Index, NFIB, Federal Reserve, Vining Sparks

17 FOMC Tilting More Hawkish 1) A strong assessment of future activity, 2) increased expectations for future growth and lower unemployment, and 3) more confidence in inflation stabilizing show a more confident Fed. FOMC Statement Labor Market: Job gains have been strong Economic Activity: rising at a solid moderate rate Economic Outlook: The economic outlook has strengthened in recent months Inflation: to move up this year in coming months Powell Press Conference no sense in the data we re on the cusp of inflation accelerating Because of the flatness of the Phillips curve 17 Sources: FOMC Statement, Vining Sparks

18 FOMC Tilting More Hawkish The FOMC s March SEP reflects expectations for faster growth in the short- to medium-term. However, the longer run outlook remains just 1.8%. 18 GDP Projections MARCH DECEMBER % % 2.4% % Longer Run 2.0% 1.8% 2.0% 1.8% U.R. Projections MARCH DECEMBER % 3.6% Longer Run 3.6% 4.5% % 3.9% 4.0% 4.6% Sources: FOMC Summary of Economic Projections, Vining Sparks

19 March FOMC Dot Plot Projections Thirty-four of forty-five dots through 2020 were raised in the March SEP Raised Dot *Based on estimation of which dot corresponds with each FOMC participant Longer Run

20 March FOMC Dot Plot Projections Additionally, the voting participants have tilted to the more hawkish side of the Committee in Non-Voters (by Year) Voters (by Year) Raised Dot *Based on estimation of which dot corresponds with each FOMC participant Longer Run

21 Financial Conditions Tightening Financial conditions have tightened in 2018 as fears of inflation and higher interest rates have roiled markets. This will be key to watch and is the most likely factor to limit Fed hikes. Normalized Versus Median* Tighter Financial Conditions Easier Financial Conditions A M J J A S O N D J F M A Sources: Chicago Fed, St. Louis Fed, Bloomberg, Vining Sparks Overall Financial Conditions - Bloomberg Index (Inverted) Interbank Liquidity - TED Spread Health of Financial System/Banks - Libor/OIS Spread Short-Term Corporate Borrowing - CP/3M TBill Spread Long-Term Corporate Borrowing - Corp 10Y Baa/Treasury Spread Municiapl Borrowing - Muni 10Y Aa/Treasury Spread Stock Values - S&P 500 YoY (Inverted) Stock Volatility - S&P 500 VIX Expected Bond Market Volatility - Swaption Volatility Chicago Fed Adj. National Financial Conditions Index St. Louis Fed Financial Stress Index Bloomberg Financial Conditions Index (Inv)

22 Longer Yields Remain Anchored Treasury yields continue to we weighed down by global yields, generally, and the impact of stilleasy monetary policy from the ECB and BoJ. 6.0 Fed, ECB, BOE, and BoJ Assets (Inverted, USD) $1 $3 $5 $ Year Treasury $ Y German Bund 10Y Japan JGB Trillions $11 $13 $15 Sources: Federal Reserve, BOE, ECB, BoJ, Bloomberg, Vining Sparks

23 Inflation Firming, but Remains Low Inflation in Japan and the Eurozone continue to run below-target despite the improving economic data and financial asset prices. This is likely to limit adjustments to monetary policy Core Inflation Measures by Country Sources: BoJ, CEIN, UK ONS, Eurostat, BLS, Vining Sparks U.K. U.S. Eurozone Japan % 1.6% 1.0% 0.5%

24 Housing Proven to Be Rate Sensitive Home sales have proven historically to be very rate-sensitive. The higher the 10-year yield rises above 3.00% (mortgage rates above 4.75%), residential investment is likely to weaken Homeowners Average Outstanding Mortgage Rate Homeowners Mortgage Current 30-Year Mortgage Rate Rates above Prevailing Market Rates Δ Economics Work to Buy More House Average Outstanding Mortgage Rate Minus Current 30-Year Mortgage Rate Sources: Census Bureau, NAR, Freddie Mac MMS 30-Year Mortgage Rate, Vining Sparks

25 YoY Change in Home Sales Home Sales Prove to Be Rate Sensitive Home sales have proven historically to be very rate-sensitive. The higher the 10-year yield rises above 3.00% (mortgage rates above 4.50%), residential investment is likely to weaken New Home Sales (YoY) Existing Home Sales (YoY) Sources: Census Bureau, NAR, Freddie Mac MMS 30-Year Mortgage Rate, Vining Sparks Outstanding Rate Less Available Rate

26 Federal Interest Expense Politicians have significant incentive to keep interest rates anchored now more than ever. Using modest projections, annual interest expense is expected to rise $580 billion by $900 $800 $700 $600 $500 $400 $300 $200 $100 $0 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% Underlying Rate Assumptions 10Y Treasury and CBO Projection 3M Bill and CBO Projection 2.90% $240 B Sources: CBO March 2017 Projections, Treasury, Bloomberg, Vining Sparks 3.70% 2.80% 1.65% Annual Interest Expense 26 $818 B

27 Inflation Outlook Remains Anchored The biggest risk to longer yields rising more than expected appears to be an increase in inflation. While the New York Fed s UIG points to an imminent increase, market expectations remain tame Underlying Inflation Gauge New York Fed UIG (Adv. 18M) Sources: New York Fed, Bloomberg, Vining Sparks Core CPI (YoY) TIPS-Implied Inflation Expectations 5Y/5Y Forward Implied Inflation 10-Year Implied Inflation M A M J J A S O N D J F M Year Implied Inflation

28 Interest Rate Projections Short-end of yield curve likely to be pressured higher from Fed hikes while longer-end responds to inflation expectations, supply/demand, global yields, and other limiting factors March Vining Sparks Projections March 29 Forward Curve March 15 Bloomberg Survey (Avg) March 29 Current Yield Curve Risk to Financial Conditions Inflation Remains below Target Somewhat Fragile Economy 2.125% 2.35% Historically Low Unemployment Signs of Potential Inflation Continued Inflation of Asset Prices 2.75% FF 3M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y Sources: Bloomberg Survey (March), Vining Sparks Projections (March), Forward Curve (March 15) Easy Monetary Policy Globally Weak Inflation Outlook Slower Rate of Future Growth Risk to Financial Conditions Risk to Housing Sector Risk to Federal Interest Expense Geopolitical Fears / Trade Fears Stronger U.S. Growth Outlook Improved Global Outlook Signs of Potential Inflation Expectations for More Hawkish FOMC 3.00% Year-End 2018 Interest Rate Projections 28

29 2018 Economic Outlook Consumer Firmer wages, stronger labor market, and $140 billion boost from tax cuts Business Investment Improved capex as a result of tax reform, particularly structures Housing Tax reform diminishes some incentives to homeownership; however, housing should see another year of growth in presuming mortgage rates remain anchored Government Spending More deficit spending will yield better growth in the near-term but may tip the inflation scale; adds to the already excessive debt burden Risks to Growth Rising inflation biggest risk to outlook (higher interest rates, asset price correction, etc ) Too much of a good thing leads to correction-inducing imbalances Fed walking tightrope in removing support without roiling markets Interest Rates (Short Maturities) Fed likely to remain hawkish so long as financial conditions remain easy, particularly with unemployment below-target Interest Rates (Longer Maturities) - Longer yields likely to rise moderately on tug-of-war between stabilizing inflation, improving growth, and global supply/demand Longer Term Outlook Aging population Weak productivity Excessive debt 29

30

31 INTENDED FOR INSTITUTIONAL INVESTORS ONLY. The information included herein has been obtained from sources deemed reliable, but it is not in any way guaranteed, and it, together with any opinions expressed, is subject to change at any time. Any and all details offered in this publication are preliminary and are therefore subject to change at any time. This has been prepared for general information purposes only and does not consider the specific investment objectives, financial situation and particular needs of any individual or institution. This information is, by its very nature, incomplete and specifically lacks information critical to making final investment decisions. Investors should seek financial advice as to the appropriateness of investing in any securities or investment strategies mentioned or recommended. The accuracy of the financial projections is dependent on the occurrence of future events which cannot be assured; therefore, the actual results achieved during the projection period may vary from the projections. The firm may have positions, long or short, in any or all securities mentioned. Member FINRA/SIPC. 31

2018 Economic Outlook 2Q Update

2018 Economic Outlook 2Q Update The Sky Is the Limit And the U.S. Economy Is Closer Dudley Carter Economist, Vining Sparks dcarter@viningsparks.com Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com

2018 Economic Outlook 2Q Update The Sky Is the Limit And the U.S. Economy Is Closer Dudley Carter Economist, Vining Sparks dcarter@viningsparks.com Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com

2018 Economic Outlook

2018 Economic Outlook The Sky Is the Limit And the U.S. Economy Is Close Dudley Carter Economist, Vining Sparks dcarter@viningsparks.com Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com

2018 Economic Outlook The Sky Is the Limit And the U.S. Economy Is Close Dudley Carter Economist, Vining Sparks dcarter@viningsparks.com Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com

2018 Economic Outlook 3Q Update

2018 Economic Outlook 3Q Update The Sky Is Still the Limit And the U.S. Economy Is Closer Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com Dudley Carter Economist, Vining Sparks dcarter@viningsparks.com

2018 Economic Outlook 3Q Update The Sky Is Still the Limit And the U.S. Economy Is Closer Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com Dudley Carter Economist, Vining Sparks dcarter@viningsparks.com

4Q The Synchronization of Growth Engines

4Q 2017 - The Synchronization of Growth Engines Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com Dudley Carter Economic Analyst, Vining Sparks dcarter@viningsparks.com 10-Year Treasury

4Q 2017 - The Synchronization of Growth Engines Craig Dismuke Chief Economist, Vining Sparks cdismuke@viningsparks.com Dudley Carter Economic Analyst, Vining Sparks dcarter@viningsparks.com 10-Year Treasury

Q Economic Outlook

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Economic Outlook In the Shoes of an FOMC Member

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Bloomberg Survey of Economists

November 2017 Economists Expect Hurricanes to Weigh Down 3Q Data with 4Q Rebound The November Bloomberg Survey of Economists shows few changes to the economic outlook, no changes to the Fed Funds projections,

November 2017 Economists Expect Hurricanes to Weigh Down 3Q Data with 4Q Rebound The November Bloomberg Survey of Economists shows few changes to the economic outlook, no changes to the Fed Funds projections,

National Economic Outlook

National Economic Outlook MSBO Financial Strategies Conference January 17, 2018 Presented by: Kyle Jones, Director of Portfolio Strategies PFM Asset Management LLC One Keystone Plaza, Suite 300 N. Front

National Economic Outlook MSBO Financial Strategies Conference January 17, 2018 Presented by: Kyle Jones, Director of Portfolio Strategies PFM Asset Management LLC One Keystone Plaza, Suite 300 N. Front

Fourth Quarter Market Outlook. Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

2012 Economic Outlook: Overview of U.S. Economy. Presented by: Mark Evans, CFA Director of Investment Strategies

2012 Economic Outlook: Overview of U.S. Economy Presented by: Mark Evans, CFA Director of Investment Strategies mevans@viningsparks.com A Recovery of Sorts Rates have fallen even further Economy is getting

2012 Economic Outlook: Overview of U.S. Economy Presented by: Mark Evans, CFA Director of Investment Strategies mevans@viningsparks.com A Recovery of Sorts Rates have fallen even further Economy is getting

Economic and Financial Markets Monthly Review & Outlook Detailed Report. June 2014

Economic and Financial Markets Monthly Review & Outlook Detailed Report June 1 Overview of the Economy In the U.S., the Federal Reserve s Beige Book report on the economy through late May indicated that

Economic and Financial Markets Monthly Review & Outlook Detailed Report June 1 Overview of the Economy In the U.S., the Federal Reserve s Beige Book report on the economy through late May indicated that

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

U.S. Economic Outlook: recent developments

U.S. Economic Outlook Recent developments Washington, D.C., 6 February 2018 This document was prepared by Helvia Velloso, Economic Affairs Officer, under the supervision of Inés Bustillo, Director, ECLAC

U.S. Economic Outlook Recent developments Washington, D.C., 6 February 2018 This document was prepared by Helvia Velloso, Economic Affairs Officer, under the supervision of Inés Bustillo, Director, ECLAC

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Moving On Up Today s Economic Environment

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 2017

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Fixed income market update. April BMO Fixed Income Brickell Bay Dr. Suite 2100 Miami, Florida bmogam.

Fixed income market update April 218 BMO Fixed Income 11 Brickell Bay Dr. Suite 21 Miami, Florida 33131 bmogam.com/usfixedincome Fixed income market update For the quarter ended March 31, 218, the Bloomberg

Fixed income market update April 218 BMO Fixed Income 11 Brickell Bay Dr. Suite 21 Miami, Florida 33131 bmogam.com/usfixedincome Fixed income market update For the quarter ended March 31, 218, the Bloomberg

Baseline U.S. Economic Outlook, Summary Table*

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

Economic Developments April 2019 Lower Mortgage Rates and Continued Wage Growth Provide Some Stability for Housing

Economic Developments April 2019 Lower Mortgage Rates and Continued Wage Growth Provide Some Stability for Housing U.S. economic growth is expected to slow from 3.0 percent in 2018 to 2.2 percent in 2019.

Economic Developments April 2019 Lower Mortgage Rates and Continued Wage Growth Provide Some Stability for Housing U.S. economic growth is expected to slow from 3.0 percent in 2018 to 2.2 percent in 2019.

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

Interest Rate Forecast

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

GLOBAL OUTLOOK ECONOMIC WATCH. July 2017

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

Economic and market snapshot for January 2016

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist.

January 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Another Fed Rate Hike in December, Inflation Remains

January 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Another Fed Rate Hike in December, Inflation Remains

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

September PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy September 2015 Stock Market Volatility likely to Remain Elevated in Near-term on China Concerns & Fed Uncertainty.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy September 2015 Stock Market Volatility likely to Remain Elevated in Near-term on China Concerns & Fed Uncertainty.

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

The Implications of an Inverted Yield Curve

What to Make of the Flattening Yield Curve Yield curve has flattened significantly; 2yr10yr spread has compressed from a peak of 2.91% An inverted yield curve has proven to be most accurate indicator of

What to Make of the Flattening Yield Curve Yield curve has flattened significantly; 2yr10yr spread has compressed from a peak of 2.91% An inverted yield curve has proven to be most accurate indicator of

November PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

March 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Job Growth Picks Up in 218, Inflation Pressures Are Building

March 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Job Growth Picks Up in 218, Inflation Pressures Are Building

Fixed income market update

April 1, 216 Fixed income market update Taplin, Canida & Habacht, LLC BMO Global Asset Management 11 Brickell Bay Drive Suite 21 Miami, Florida 33131 p 35-379-21 f 35-379-4452 tchinc.com Fixed income market

April 1, 216 Fixed income market update Taplin, Canida & Habacht, LLC BMO Global Asset Management 11 Brickell Bay Drive Suite 21 Miami, Florida 33131 p 35-379-21 f 35-379-4452 tchinc.com Fixed income market

The Macroeconomic Outlook

The Macroeconomic Outlook 2 nd Quarter, 2018 Ramirez & Co., Inc. 61 Broadway, 29th Floor New York, NY 10006 (800) 888-4086 Synopsis Almost a decade after the onset of the Great Contraction of 2007 2009,

The Macroeconomic Outlook 2 nd Quarter, 2018 Ramirez & Co., Inc. 61 Broadway, 29th Floor New York, NY 10006 (800) 888-4086 Synopsis Almost a decade after the onset of the Great Contraction of 2007 2009,

Financial Market Outlook: Stocks Rebounding from July Correction, Further Gains Likely. Bond Yields Range Bound

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Rebounding from July Correction, Further Gains Likely. Bond

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Key takeaways. What it may mean for investors WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS. Veronica Willis Investment Strategy Analyst

Veronica Willis Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS May 8, 2018 Monetary Policy Divergence Could Last a Little Longer Key takeaways» Recent economic improvement

Veronica Willis Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS May 8, 2018 Monetary Policy Divergence Could Last a Little Longer Key takeaways» Recent economic improvement

Economic Data and Interest Rate Forecast

Economic Data and Interest Rate Forecast February 2018 (Data through February 14, 2018) Monthly highlights Nonfarm Payroll off to solid start in 2018 Year over year wage growth jumps Manufacturing sector

Economic Data and Interest Rate Forecast February 2018 (Data through February 14, 2018) Monthly highlights Nonfarm Payroll off to solid start in 2018 Year over year wage growth jumps Manufacturing sector

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 2018

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

US Economic Outlook Improving

Government Bonds Have Never Looked Less Attractive OUTLOOK Executive Summary Kenneth J. Taubes Chief Investment Officer, US Economic Outlook US GDP growth may lead growth among developed nations, at approximately

Government Bonds Have Never Looked Less Attractive OUTLOOK Executive Summary Kenneth J. Taubes Chief Investment Officer, US Economic Outlook US GDP growth may lead growth among developed nations, at approximately

March 22, 2017 Boston, MA

March 22, 2017 Boston, MA Make or Break: Five Pivotal Drivers in 2017 Holly H. MacDonald Chief Investment Strategist Past performance is no guarantee of future results. This material is provided for your

March 22, 2017 Boston, MA Make or Break: Five Pivotal Drivers in 2017 Holly H. MacDonald Chief Investment Strategist Past performance is no guarantee of future results. This material is provided for your

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

May 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Slower but Still Solid Economic Growth in the First Quarter;

May 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Slower but Still Solid Economic Growth in the First Quarter;

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

NESGFOA Economic Assessment Impact on Rates

NESGFOA Economic Assessment Impact on Rates September 18, 2017 Not FDIC Insured May Lose Value No Bank Guarantee Not NCUA or NCUSIF insured. May lose value. No credit union guarantee. For institutional

NESGFOA Economic Assessment Impact on Rates September 18, 2017 Not FDIC Insured May Lose Value No Bank Guarantee Not NCUA or NCUSIF insured. May lose value. No credit union guarantee. For institutional

U.S. Slack Keeps Shrinking, Slowed But Not Stopped By Global Headwinds; Case For Fed Tightening Builds

U.S. Slack Keeps Shrinking, Slowed But Not Stopped By Global Headwinds; Case For Fed Tightening Builds QE To End, Bond Yields To Rise: Just What The G-7 Does Not Need For The End Of 2! Carl Weinberg, Chief

U.S. Slack Keeps Shrinking, Slowed But Not Stopped By Global Headwinds; Case For Fed Tightening Builds QE To End, Bond Yields To Rise: Just What The G-7 Does Not Need For The End Of 2! Carl Weinberg, Chief

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

US Economy Update May 2014

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 18, 2018 Are Rising Household Debt Concerns Warranted?

Craig P. Holke Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 18, 2018 Are Rising Household Debt Concerns Warranted? Key takeaways» Concerns have risen about the

Craig P. Holke Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 18, 2018 Are Rising Household Debt Concerns Warranted? Key takeaways» Concerns have risen about the

Global Macroeconomic Outlook March LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA FAX

March 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook The IMF continues to forecast a slight pick-up in growth

March 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook The IMF continues to forecast a slight pick-up in growth

Economic Growth Expected to Slow and Housing to Stabilize in 2019

Consumer Confidence Expectations in the Next Six Months (%) Economic Developments December 218 Economic Growth Expected to Slow and Housing to Stabilize in 219 The U.S. economy is expected to grow 2.6

Consumer Confidence Expectations in the Next Six Months (%) Economic Developments December 218 Economic Growth Expected to Slow and Housing to Stabilize in 219 The U.S. economy is expected to grow 2.6

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

Key Trends in the US Economy, the Industrial and the Rail Sectors. Sam Kyei Chief Economist SAK ECONOMICS. December 5, 2018

Key Trends in the US Economy, the Industrial and the Rail Sectors Sam Kyei Chief Economist SAK ECONOMICS December 5, 2018 0 NATIONAL ASSOCIATION OF BUSINESS ECONOMICS There are many exciting NABE events

Key Trends in the US Economy, the Industrial and the Rail Sectors Sam Kyei Chief Economist SAK ECONOMICS December 5, 2018 0 NATIONAL ASSOCIATION OF BUSINESS ECONOMICS There are many exciting NABE events

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

Global Investment Strategy

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Fourth Quarter Market Outlook. Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

The Mid-Year Economic Forecast. June 20, 2018

The Mid-Year Economic Forecast June 20, 2018 Agenda National Economy: On a Solid Footing Construction & Housing: Still Strong Risks: What Could Go Wrong? 2 National Economy On a Solid Footing 3 GDP Grew

The Mid-Year Economic Forecast June 20, 2018 Agenda National Economy: On a Solid Footing Construction & Housing: Still Strong Risks: What Could Go Wrong? 2 National Economy On a Solid Footing 3 GDP Grew

November 2017 Market Update

Market Update (11/2017) Allianz Investment Management LLC November 2017 Market Update Key Points Equities rallied to fresh all-time highs as the prospects for tax reform continued to move forward. Jay

Market Update (11/2017) Allianz Investment Management LLC November 2017 Market Update Key Points Equities rallied to fresh all-time highs as the prospects for tax reform continued to move forward. Jay

Monthly Market Update August 2016

Monthly Market Update August 2016 Steven Alexander, CTP, CGFO, CPPT, Managing Director D. Scott Stitcher, CFA, Director Richard Pengelly, CFA, CTP, Director Khalid Yasin, CHP, Senior Managing Consultant

Monthly Market Update August 2016 Steven Alexander, CTP, CGFO, CPPT, Managing Director D. Scott Stitcher, CFA, Director Richard Pengelly, CFA, CTP, Director Khalid Yasin, CHP, Senior Managing Consultant

Economic Outlook. Lauren Bresnahan, Ph.D. Deputy Chief Economist, KPMG May 17, 2018

Economic Outlook Lauren Bresnahan, Ph.D. Deputy Chief Economist, KPMG lbresnahan@kpmg.com May 17, 2018 Today s Outline 1 Global Economic Backdrop 2 U.S. Economic Backdrop 3 Economic Outlook 4 Economic

Economic Outlook Lauren Bresnahan, Ph.D. Deputy Chief Economist, KPMG lbresnahan@kpmg.com May 17, 2018 Today s Outline 1 Global Economic Backdrop 2 U.S. Economic Backdrop 3 Economic Outlook 4 Economic

June 2013 Equities Rally Drive Global Re-rating

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

Baseline U.S. Economic Outlook, Summary Table*

January 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Great December Jobs Report;

January 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Great December Jobs Report;

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook February 2015 Stocks to Fully Rebound from Late 2014/Early 2015 Sell-off with ECB Launching Aggressive QE, Rate Cuts by Several

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook February 2015 Stocks to Fully Rebound from Late 2014/Early 2015 Sell-off with ECB Launching Aggressive QE, Rate Cuts by Several

Global Economic Outlook Brittle Strength

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

FOMC Stresses Importance of Data-Dependent Policy in October Minutes

Economic Analysis FOMC Stresses Importance of Data-Dependent Policy in October Minutes Kim Fraser Chase The minutes from October s FOMC meeting revealed some further discussion on forward guidance and

Economic Analysis FOMC Stresses Importance of Data-Dependent Policy in October Minutes Kim Fraser Chase The minutes from October s FOMC meeting revealed some further discussion on forward guidance and

The Outlook for the U.S. Economy: Sunny Skies But Developing Storm Clouds? The Financial Executives Networking Group Des Peres, MO

The Outlook for the U.S. Economy: Sunny Skies But Developing Storm Clouds? The Financial Executives Networking Group Des Peres, MO Kevin L. Kliesen Business Economist and Research Officer March 28, 2018

The Outlook for the U.S. Economy: Sunny Skies But Developing Storm Clouds? The Financial Executives Networking Group Des Peres, MO Kevin L. Kliesen Business Economist and Research Officer March 28, 2018

Global Macroeconomic Outlook March 2016

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.*

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Editor: Felix Ewert. The Week Ahead Key Events Oct, 2017

Editor: Felix Ewert The Week Ahead Key Events 16 22 Oct, 2017 Tuesday 17, 11.00 ZEW Survey (Oct), Germany and EMU Germany SEB Cons. Previous Current Situation 89.5 88.5 87.9 Growth expectations 20.0 20.0

Editor: Felix Ewert The Week Ahead Key Events 16 22 Oct, 2017 Tuesday 17, 11.00 ZEW Survey (Oct), Germany and EMU Germany SEB Cons. Previous Current Situation 89.5 88.5 87.9 Growth expectations 20.0 20.0

National Economic Indicators. May 7, 2018

National Economic Indicators May 7, 18 Table of Contents GDP Release Date Latest Period Page Table: Real Gross Domestic Product Apr-7-18 8:31 Q1-18 Real Gross Domestic Product Apr-7-18 8:31 Q1-18 5 Decomposition

National Economic Indicators May 7, 18 Table of Contents GDP Release Date Latest Period Page Table: Real Gross Domestic Product Apr-7-18 8:31 Q1-18 Real Gross Domestic Product Apr-7-18 8:31 Q1-18 5 Decomposition

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014)

") Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Economic and Market Outlook

Economic and Market Outlook Fourth Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Economic and Market Outlook Fourth Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Global Macroeconomic Outlook March 2017

March 2017 M E K E T A I N V E S T M E N T G R O U P 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA 02090 781 471 3500 FAX 781 471 3411 Global Economic Outlook 1 For the first time in six years, the IMF

March 2017 M E K E T A I N V E S T M E N T G R O U P 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA 02090 781 471 3500 FAX 781 471 3411 Global Economic Outlook 1 For the first time in six years, the IMF

Editor: Felix Ewert. The Week Ahead Key Events Mar 2018

Editor: Felix Ewert The Week Ahead Key Events 12 18 Mar 2018 Monday 12, 08.00 SWE: Unemployment, registered (Feb) SEB Cons. Prev. Open 3.9 --- 4.0 Open, seas. adj. 3.8 --- 3.8 Total seas. adj. 7.1 ---

Editor: Felix Ewert The Week Ahead Key Events 12 18 Mar 2018 Monday 12, 08.00 SWE: Unemployment, registered (Feb) SEB Cons. Prev. Open 3.9 --- 4.0 Open, seas. adj. 3.8 --- 3.8 Total seas. adj. 7.1 ---

The U.S. Economic Outlook

The U.S. Economic Outlook Gering/Scottsbluff Economic Forum August 23, 216 George A. Kahn Vice President and Economist The views expressed are those of the author and do not necessarily reflect the opinions

The U.S. Economic Outlook Gering/Scottsbluff Economic Forum August 23, 216 George A. Kahn Vice President and Economist The views expressed are those of the author and do not necessarily reflect the opinions

Fixed income market update

September 1, 217 Fixed income market update Taplin, Canida & Habacht, LLC BMO Global Asset Management 11 Brickell Bay Drive Suite 21 Miami, Florida 33131 p 35-379-21 f 35-379-4452 tchinc.com Fixed income

September 1, 217 Fixed income market update Taplin, Canida & Habacht, LLC BMO Global Asset Management 11 Brickell Bay Drive Suite 21 Miami, Florida 33131 p 35-379-21 f 35-379-4452 tchinc.com Fixed income

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Real GDP Growth Rebounds 4.0% in 2Q14

Economic Analysis Real GDP Growth Rebounds 4.% in 2Q14 Kim Fraser Chase The advance estimate for 2Q14 GDP growth was slightly higher than expected, coming in at 4.% on a QoQ seasonally-adjusted annualized

Economic Analysis Real GDP Growth Rebounds 4.% in 2Q14 Kim Fraser Chase The advance estimate for 2Q14 GDP growth was slightly higher than expected, coming in at 4.% on a QoQ seasonally-adjusted annualized

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Economic Summary. Visit us online at for the most recent market updates, Insights and Perspectives

Economic Summary During the June Meeting, the Federal Open Market Committee (FOMC) raised the federal funds rate by 25 bps to a range of 1.75% to 2.%. Encouraged by falling unemployment rates and rising

Economic Summary During the June Meeting, the Federal Open Market Committee (FOMC) raised the federal funds rate by 25 bps to a range of 1.75% to 2.%. Encouraged by falling unemployment rates and rising

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

October 2016 Market Update

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

Foreign Exchange Rates. Key Global Indices. Straits Times 3, % 5.50%

Review for week ending 5 Sep 2014 Equities U.S. equities were midly higher for the week, despite a weaker than expected US labour repot. The Dow Jones Industrial Average, S&P 500 and Nasdaq gained 0.23%,

Review for week ending 5 Sep 2014 Equities U.S. equities were midly higher for the week, despite a weaker than expected US labour repot. The Dow Jones Industrial Average, S&P 500 and Nasdaq gained 0.23%,

Monthly Economic Insight

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

MARCH 2018 Capital Markets Update

MARCH 2018 Market commentary ECONOMIC CLIMATE Hiring slowed from its fast pace last month the U.S. added 103,000 jobs to nonfarm payrolls in March, below the consensus estimate of 185,000. The U-3 unemployment

MARCH 2018 Market commentary ECONOMIC CLIMATE Hiring slowed from its fast pace last month the U.S. added 103,000 jobs to nonfarm payrolls in March, below the consensus estimate of 185,000. The U-3 unemployment

Key Takeaways. What it may mean for investors WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS. Luis Alvarado Investment Strategy Analyst

Luis Alvarado Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 12, 2017 The Mystery of Inflation and What Lies Ahead Key Takeaways» As most investors know, inflation

Luis Alvarado Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 12, 2017 The Mystery of Inflation and What Lies Ahead Key Takeaways» As most investors know, inflation

MACRO INVESTMENT OUTLOOK

MACRO INVESTMENT OUTLOOK AUGUST 18 INVESTMENT STRATEGY AND DYNAMIC MARKETS TEAM, MULTI ASSET GROUP GLOBAL SHARES CONSTRAINED BY TRADE WAR FEARS BUT AUSTRALIAN SHARES RELATIVELY RESILIENT 5 Australia -

MACRO INVESTMENT OUTLOOK AUGUST 18 INVESTMENT STRATEGY AND DYNAMIC MARKETS TEAM, MULTI ASSET GROUP GLOBAL SHARES CONSTRAINED BY TRADE WAR FEARS BUT AUSTRALIAN SHARES RELATIVELY RESILIENT 5 Australia -

DECEMBER 7, 2018 Market Commentary by Scott J. Brown, Ph.D., Chief Economist

DECEMBER 7, 2018 Market Commentary by Scott J. Brown, Ph.D., Chief Economist Two key issues rattled stock market investors: trade policy and the yield curve. The weekend meeting between President Trump

DECEMBER 7, 2018 Market Commentary by Scott J. Brown, Ph.D., Chief Economist Two key issues rattled stock market investors: trade policy and the yield curve. The weekend meeting between President Trump

The Outlook for the U.S. Economy March Summary View. The Current State of the Economy

The Outlook for the U.S. Economy March 2010 Summary View The Current State of the Economy 8% 6% Quarterly Change (SAAR) Chart 1. The Economic Outlook History Forecast The December 2007-2009 recession is

The Outlook for the U.S. Economy March 2010 Summary View The Current State of the Economy 8% 6% Quarterly Change (SAAR) Chart 1. The Economic Outlook History Forecast The December 2007-2009 recession is

Q3/17. Quarterly Market Commentary. Highlights. Canadian & U.S. Fixed Income. U.S. Equities. International Equities.

Q3/17 Highlights Canadian & U.S. Fixed Income The Canadian government bond index declined during Q3/17, underperforming the U.S. government bond index as the Canadian index fell 2.02% Q/Q, compared to

Q3/17 Highlights Canadian & U.S. Fixed Income The Canadian government bond index declined during Q3/17, underperforming the U.S. government bond index as the Canadian index fell 2.02% Q/Q, compared to

Economic Review Fourth Quarter 2017

Economic Review Fourth Quarter 2017 The state of the general economy can help or hinder a business prospects by influencing the demand for its goods and services and the availability and price of inputs

Economic Review Fourth Quarter 2017 The state of the general economy can help or hinder a business prospects by influencing the demand for its goods and services and the availability and price of inputs

2012 As the Fundamentals Improve Stateside, They Deteriorate Abroad

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H 212 As the Fundamentals Improve Stateside, They Deteriorate Abroad December 211 Paul L. Kasriel, Chief Economist PH: 312..15 plk1@ntrs.com

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H 212 As the Fundamentals Improve Stateside, They Deteriorate Abroad December 211 Paul L. Kasriel, Chief Economist PH: 312..15 plk1@ntrs.com

Fresno County Employees' Retirement Association

Fresno County Employees' Retirement Association Investment Performance Review Period Ending: December 31, 2006 999 Third Avenue, Suite 3650 2321 Rosecrans Avenue, Suite 2250 Seattle, Washington 98104 El

Fresno County Employees' Retirement Association Investment Performance Review Period Ending: December 31, 2006 999 Third Avenue, Suite 3650 2321 Rosecrans Avenue, Suite 2250 Seattle, Washington 98104 El

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

GLOBAL ECONOMIC ENVIRONMENT AND OUTLOOK

19 Global Market Outlook Press Briefing GLOBAL ECONOMIC ENVIRONMENT AND OUTLOOK Alan Levenson Chief U.S. Economist November 13, 18 Economic Outlook Summary Global growth moderating into 19 Advanced economies

19 Global Market Outlook Press Briefing GLOBAL ECONOMIC ENVIRONMENT AND OUTLOOK Alan Levenson Chief U.S. Economist November 13, 18 Economic Outlook Summary Global growth moderating into 19 Advanced economies

US ECONOMIC OUTLOOK. Joseph Brusuelas Chief Economist RMS US LLP. October 2016

US ECONOMIC OUTLOOK Joseph Brusuelas Chief Economist RMS US LLP October 2016 US Economic Outlook Base Case: Trend US growth near 2 percent in 2016 Long-term growth trend 1.5 percent Sustained growth above

US ECONOMIC OUTLOOK Joseph Brusuelas Chief Economist RMS US LLP October 2016 US Economic Outlook Base Case: Trend US growth near 2 percent in 2016 Long-term growth trend 1.5 percent Sustained growth above

The Outlook for the U.S. Economy National Association of Credit Union Supervisory and Auditing Committees Annual Conference and Expo Louisville, KY

The Outlook for the U.S. Economy National Association of Credit Union Supervisory and Auditing Committees Annual Conference and Expo Louisville, KY Kevin L. Kliesen Business Economist and Research Officer

The Outlook for the U.S. Economy National Association of Credit Union Supervisory and Auditing Committees Annual Conference and Expo Louisville, KY Kevin L. Kliesen Business Economist and Research Officer