UBS Global Consumer Conference

|

|

|

- Sara Allison

- 6 years ago

- Views:

Transcription

1 UBS Global Consumer Conference Boston, March 2013

2 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk. ( Kalbe or the Company ). This presentation has been prepared solely for use in connection with the release of 31 December 2012 indicative unaudited results of the Company. The information contained in this presentation has not been independently verified. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. None of the Company or any of their respective affiliates, and their respective commissioners, directors and employees, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with the presentation. Any decision to purchase or subscribe for securities of the Company should not be made on the basis of the information contained in this presentation. The presentation is not an offer of securities for sale in the United States. Securities may not be offered or sold in the United States absent registration or an exemption from registration. This presentation and its contents are confidential unless they are or become generally available as public information in accordance with prevailing laws and regulations (other than as a result of a disclosure by you) and must not be distributed, published or reproduced (in whole or in part) or disclosed by recipients to any other person. This presentation does not constitute a recommendation regarding the securities of the Company. This presentation, including the information and opinions contained herein, is provided as of the date of this presentation and is subject to change without notice, including change as a result of the issuance of 31 December 2012 indicative unaudited results of the Company. This presentation includes "forward-looking statements". These statements contain the words "anticipate", "believe", "intend", estimate", "expect" and words of similar meaning. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding the Company's financial position, business strategy, plans and objectives of management for future operations (including development plans, objectives relating to the Company's products and services and anticipated product launches) are forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company's present and future business strategies and the environment in which the Company will operate in the future. These forward-looking statements speak only as at the date of this presentation. The Company expressly disclaims any obligation or reflection of any change in the Company's expectations with regard thereto, or any change in events, conditions or circumstances on which any statement is based. Market data and certain industry forecasts used in this presentation were obtained from market research, publicly available information and industry publications which have not been independently verified, and no representation is made as to the accuracy of such information. 2

3 Table of Contents BUSINESS OVERVIEW OUR STRATEGIES IN

4 BUSINESS OVERVIEW

5 Corporate Overview Largest Publicly-Listed Pharmaceuticals Company in Southeast Asia Established in 1966 and headquartered in Jakarta A public company since 1991 and listed in the Indonesia Stock Exchange The largest publicly-listed pharmaceuticals company in Southeast Asia Sales breakdown by segment and by geographical location for YTD December 2012 is as follows: Distribution & Logistics 38% Prescription Pharmaceuticals 24% Export, 4% Nutritionals 22% Total Sales = Rp Bn Consumer Health 16% Total Sales = Rp Bn Domestic, 96% Over 10,000 employees and a marketing and sales force of 4,000 covering 80% of the Indonesian consumer health and 100% of the Indonesian prescription pharmaceuticals market 5

6 Indonesia s Health Spending Trends Total expenditure on health averaged 2.1% of GDP over the 11 year period In Q4 2009, the new Healthcare Law has been approved and provides guideline for Government to increase the healthcare spending from 2% up to 5% of GDP. Law on National Social Security System has been passed since 2004, but implementation regulation on Social Security Provider Body (BPJS) has just been passed in October There will be two BPJS: BPJS Health (Jan 1, 2014) and BPJS Labor (Jul 1, 2015) (Rp Tn) Growth of 14.1% Total Healthcare Expenditure % 4.50% 4.00% 3.50% 3.00% 2.50% 2.00% 1.50% 1.00% 0.50% 0.00% % Healthcare Expenditure/GDP % 3.8% 3.5% 3.3% 2.1% Malaysia Thailand Philippines India Singapore Indonesia Source : Business Monitor International: Pharmaceutical & Healthcare Report, Q (Indonesia, Malaysia, Thailand, Philippines, India, Singapore) Share of Total Health Expenditure (%) public private out-of-pocket private F 2012F 2013F 2014F 2015F Source : Business Monitor International: Pharmaceutical & Healthcare Report, Q (Indonesia, Malaysia, Thailand, Philippines, India, Singapore) Source: The World Bank 6

")

7 Indonesian Pharmaceuticals Market Highly Fragmented Industry with more than 200 Pharmaceutical Players Total Market (ITMA) YTD Pharmacy (IPA) YTD Hospital (IHPA) YTD KALBE GROUP 13% a 5% b 5% c 5% d 5% e 4% f 3% KALBE GROUP 8% a 7% b 6% c 5% d 4% e 4% f 3% KALBE GROUP 9% a 7% b 7% c 5% d 4% e 4% f 4% OTHERS 60% OTHERS 63% OTHERS 60% Total Market = Rp 43.1Tn Total Market = Rp 7.9Tn Total Market = Rp 13.8Tn Source : IMS Health Prescription Pharmaceuticals YTD (Ethical + OTC) 7

8 Prescription Pharmaceuticals Division Comprehensive Product Range Targeted to All Income Groups Sales Contribution By Product Categories YTD Unbranded Generics 10% Licensed Products 32% Branded Generics 58% Total Sales = Rp 2,412 Bn Licensed Products Branded Generics Unbranded Generics Number of Products Therapeutic Class General Anti-Infectives Hospital Solutions Oncology Blood and Blood Forming Organs Musculo-Skeletal System Alimentary Tract and Metabolism General Anti-Infectives Central Nervous system Musculo-Skeletal System Cardiovascular System Alimentary Tract and Metabolism General Anti-Infectives Alimentary Tract and Metabolism Cardiovascular System Central Nervous system Key Licensors 8

9 Prescription Pharmaceuticals Division New Production Facilities Completed new production facility for generic drugs in Cikarang Construction of oncology plant in Pulogadung 9

10 Consumer Health Division Strong Brand Equity with Leading Market Position Market share of Kalbe s brands YTD December 2011 Therapeutic Class Kalbe s Products Market Share by Volume Antacid Promag, Waisan 77.4%* Anti Diarrhea Neo Entrostop 44.8%** Cough Remedies Komix, Woods, Mextril, Mixadin 39.1% Cold Remedies Mixagrip Reg, Mixagrip FB, Procold 35.9% Multivitamin & Vitamin C Cerebrovit, Fatigon, Sakatonik Liver, Xon-Ce 42.2% Children Multivitamin Cerebrofort, Sakatonik ABC 21.1% Energy Drink ExtraJoss 23.8% Source : AC Nielsen jaguar method, based on volume (unit) Note : * urban data only ** based on AC Nielsen August

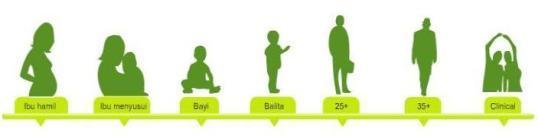

11 Nutritionals Division Complete Range of Nutritional Products Catered to expecting & lactating mothers, babies, toddlers, children, tweens and adults. Expecting Lactating Baby Toddler Kid Tween Teen Clinical 11

12 Nutritionals Division Relatively Low Milk per Capita Consumption Milk per Capita Consumption (kg) -2.3% 1.6% 0.5% 2.7% 1.1% 1.6% 0 Indonesia Thailand Philippines Malaysia Vietnam South Korea Source: FAPRI (Food & Agricultural Policy Research Institute) for whole milk powder, liquid milk and non fat dry milk categories = Real Data; = Projection Note : %growth represents 6 years ( ) CAGR 12

13 Business Overview 2012 Launched new innovative products Acquisition of PT Hale International Established a joint venture company PT Kalbe Milko Indonesia 13

14 Nutritionals Division Multi Channel Customer Touch Points Kalbe e-store - the 1 st Online Nutrition Store in Indonesia Nutritionals Division launched new channel of consumer order through hotline service Kalbe Home Delivery and online shopping through Kalbe Family Reward Card offers point rewards for consumers to increase Kalbe products consumption. 14

15 Distribution & Logistics Division The Most Extensive Distribution Network RDC 2 Branches Cities

16 Distribution & Logistics Division Major Third Party Principals by Category Expansion of distribution and logistics facilities Banjarmasin Jember Surakarta Banda Aceh Denpasar Multi-channel customer touch points : Kalbe e-store, Kalbe Family Rewards Card, Kalbe Home Delivery, Kalbe Customer Care Continued to improve retail health service business model : Mitrasana Clinic 4-in-1 concept : family doctor, pharmacy, laboratory, and convenient store. To date, Kalbe has opened 39 Mitrasana clinics in Jakarta and its Greater Area. 16

17 Distribution & Logistics Division Major Third Party Principals by Category Prescription Pharmaceuticals Consumer Medical Instrument & Diagnostic Fine Chemical Raw Materials 17

18 International Overview 2012 Continued regional expansion Long-lasting kick Diabetasol and Extra Joss Events in the Philippines 18

19 Indicative Results 2012 Strong Top Line Growth in All Segments Net Sales (in Rp Bn) 24.9% 31 Dec 2011 (Audited) 31 Dec 2012 (Unaudited) 13,630 10, % 2, % 3,288 1, % 2, % 2,420 3,012 3,873 5,179 Prescription PharmaceuticalsConsumer Health Nutritionals Distribution & Logistics Consolidation 19

31 Dec 2012")

20 Indicative Results 2012 Improved operating expenses efficiency Gross Profit Margin Operating Expenses to Net Sales Ratios 50.9% - 3.0% 47.8% 32.8% 31.6% 0.8% 0.7% 5.4% 4.9% -1.2% Selling & Marketing 26.6% 26.0% General & Administrative Research & Development 31 Dec 2011 (Audited) 31 Dec 2012 (Unaudited) 31 Dec 2011 (Audited) 31 Dec 2012 (Unaudited) Gross Profit Margin decreased by 3.0% mostly due to change in business mix. Improved Operating Expenses to Net Sales Ratio by 1.2% due to strong sales growth. 20

31 Dec 2012 (Unaudited) 31 Dec 2011 (Audited) 31 Dec 2012 (Unaudited) Income before tax margin declined from 18.2% in 2011 to 16.")

21 Indicative Results 2012 Strong Earnings Growth Income Before Tax (in Rp bn) Net Income (in Rp bn) +15.1% 2, % 1,732 1,987 1, Dec 2011 (Audited) 31 Dec 2012 (Unaudited) 31 Dec 2011 (Audited) 31 Dec 2012 (Unaudited) Income before tax margin declined from 18.2% in 2011 to 16.8% in 2012 Net income margin declined from 13.6% in 2011 to 12.7% in

22 OUR STRATEGIES IN

23 Strategies for Improve marketing and sales effectiveness CORPORATE BRANDING 2. Strengthen business portfolio through innovation and M&A 23

24 Strategies for Go global deeper ASEAN penetration with more product offering 4. Expand distribution coverage New RDC New branches and existing branch capacity expansion Additional trucks & motorcycles 5. Enhance human capital development 24

25 Outlook 2013 Earnings Guidance Year-on-year Sales Growth 15% - 18% 2. Operating Profit Margin 16.0% -17.0% 3. Earnings per Share growth of 15% - 18% 4. Dividend payout ratio minimum 50% Capex Rp Tn for production capacity and distribution network expansion Cancellation of Treasury Stocks - subject to shareholders approval in EGMS in May

26 THANK YOU For further information: PT Kalbe Farma Tbk. Jalan Let.Jend. Suprapto Kav. 4 Jakarta 10510, Indonesia Tel. : Fax. : vidjongtius@kalbe.co.id jhandajani@kalbe.co.id investor.relations@kalbe.co.id Website : 26

Company Update Unaudited YTD September 2013

Fight Free Radicals with High Antioxidant Milk Company Update Unaudited YTD September 2013 October 2013 Free radicals are everywhere Lower the risk with Entrasol high antioxidant milk to fight free radicals

Fight Free Radicals with High Antioxidant Milk Company Update Unaudited YTD September 2013 October 2013 Free radicals are everywhere Lower the risk with Entrasol high antioxidant milk to fight free radicals

Not all collagen is the same, it s time to choose the right one Company Update Unaudited YTD September 2014

Not all collagen is the same, it s time to choose the right one Company Update Unaudited YTD September 2014 October 2014 Forward Looking Statement This presentation has been prepared for informational

Not all collagen is the same, it s time to choose the right one Company Update Unaudited YTD September 2014 October 2014 Forward Looking Statement This presentation has been prepared for informational

Company Update Audited FY December March 2015

Company Update Audited FY December 2014 March 2015 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk. ( Kalbe or the Company ). This presentation

Company Update Audited FY December 2014 March 2015 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk. ( Kalbe or the Company ). This presentation

Company Update YTD September 2010 Results

Company Update YTD September 2010 Results October 2010 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk.( Kalbe or the Company ). This

Company Update YTD September 2010 Results October 2010 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk.( Kalbe or the Company ). This

Company Update H Results

Company Update H1 2010 Results July 2010 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk.( Kalbe or the Company ). This presentation

Company Update H1 2010 Results July 2010 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk.( Kalbe or the Company ). This presentation

Comp m a p ny n y Up U d p a d te t Un U a n u a d u i d ted d Y TD T D Ju J n u e n 2017 July 2017

Company Update Unaudited YTD June 2017 July 2017 Forward Looking Statement 2 This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk.( Kalbe or the Company ). This presentation

Company Update Unaudited YTD June 2017 July 2017 Forward Looking Statement 2 This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk.( Kalbe or the Company ). This presentation

Mitra Keluarga. Rapat Gabungan Dewan Komisaris, Direksi & Komite Audit

Mitra Keluarga Rapat Gabungan Dewan Komisaris, Direksi & Komite Audit 24 Agustus 2017 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Mitra Keluarga

Mitra Keluarga Rapat Gabungan Dewan Komisaris, Direksi & Komite Audit 24 Agustus 2017 Forward Looking Statement This presentation has been prepared for informational purposes only by PT Mitra Keluarga

CHALLENGES WITH ASEAN PHARMACEUTICAL REGULATION SCHEMES TO OTC PRODUCTS INDONESIA EXPERIENCE RACHMADI JOESOEF GP FARMASI - INDONESIA

CHALLENGES WITH ASEAN PHARMACEUTICAL REGULATION SCHEMES TO OTC PRODUCTS INDONESIA EXPERIENCE RACHMADI JOESOEF GP FARMASI - INDONESIA 1 OUTLINE INTRODUCTION 2 3 4 5 6 SCOPE OF REGULATION SCHEME CHALLENGES

CHALLENGES WITH ASEAN PHARMACEUTICAL REGULATION SCHEMES TO OTC PRODUCTS INDONESIA EXPERIENCE RACHMADI JOESOEF GP FARMASI - INDONESIA 1 OUTLINE INTRODUCTION 2 3 4 5 6 SCOPE OF REGULATION SCHEME CHALLENGES

MACRO-ECONOMICS REGULATORY INFRASTRUCTURE PHARMA INDUSTRY

MACRO-ECONOMICS Economic growth are potentially good GDP per capita above $ 3.000 Government health budget increases to 5% Middle class category is projected into 150 Mn in 2014, average life expectancy

MACRO-ECONOMICS Economic growth are potentially good GDP per capita above $ 3.000 Government health budget increases to 5% Middle class category is projected into 150 Mn in 2014, average life expectancy

PT Ultrajaya Milk Industry & Trading Company Tbk. FY 2013 results update

PT Ultrajaya Milk Industry & Trading Company Tbk. FY 2013 results update April 2014 0 Disclaimer These materials are not intended to be a public offering document under Law of the Republic of Indonesia

PT Ultrajaya Milk Industry & Trading Company Tbk. FY 2013 results update April 2014 0 Disclaimer These materials are not intended to be a public offering document under Law of the Republic of Indonesia

Public-Private Partnerships and Financial Inclusion

Section 8: Public-Private Partnerships and Financial Inclusion Workshop on Enhancing Access to Formal Financial Services in Indonesia Eugene Keith Galbraith President Commissioner PT Bank Central Asia

Section 8: Public-Private Partnerships and Financial Inclusion Workshop on Enhancing Access to Formal Financial Services in Indonesia Eugene Keith Galbraith President Commissioner PT Bank Central Asia

Global Markets Group. Trade Performance: Narrowing Surplus Author: Juniman Chief Economist. Economic Research. Trade Outlook Monthly Report

Global Markets Group Trade Outlook Monthly Report Economic Research November 2016 Trade Performance: Narrowing Surplus Author: Juniman Chief Economist Trade Highlights Exports in September 2016 fell to

Global Markets Group Trade Outlook Monthly Report Economic Research November 2016 Trade Performance: Narrowing Surplus Author: Juniman Chief Economist Trade Highlights Exports in September 2016 fell to

Global Markets Group. Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist. Economic Research. Trade Outlook Monthly Report

Global Markets Group Trade Outlook Monthly Report Economic Research August 2016 Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist Trade Highlights Exports in June 2016 rose

Global Markets Group Trade Outlook Monthly Report Economic Research August 2016 Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist Trade Highlights Exports in June 2016 rose

Economic outlook. Bangkok Bank position. Strategic priorities and targets

20110721 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.2% +2.6% 2 0 2008 2009 2010 2011f

20110721 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.2% +2.6% 2 0 2008 2009 2010 2011f

Investor Highlight. October 2016

Investor Highlight October 2016 Company Disclaimer Company Disclaimer This confidential document (the Presentation ) and the information contained herein do not constitute or form part of and should not

Investor Highlight October 2016 Company Disclaimer Company Disclaimer This confidential document (the Presentation ) and the information contained herein do not constitute or form part of and should not

Investor Highlight 1Q 2018

Invesor Highlight October 2017 Investor Highlight 1Q 2018 Ver. 2017.10.24 Company Disclaimer This confidential document (the Presentation ) and the information contained herein do not constitute or form

Invesor Highlight October 2017 Investor Highlight 1Q 2018 Ver. 2017.10.24 Company Disclaimer This confidential document (the Presentation ) and the information contained herein do not constitute or form

HOLD Target Price, IDR 1,900 Upside 5.2%

Friday, 20 February 2015 HOLD Target Price, IDR 1,900 Upside 5.2% KLBF IJ/KLBF.JK Last Price, IDR 1,805 No. of shares (bn) 46,875 Market Cap, IDR bn 84,609 (US$ mn) 6,594 3M T/O, US$mn 5.1 Last Recommendation

Friday, 20 February 2015 HOLD Target Price, IDR 1,900 Upside 5.2% KLBF IJ/KLBF.JK Last Price, IDR 1,805 No. of shares (bn) 46,875 Market Cap, IDR bn 84,609 (US$ mn) 6,594 3M T/O, US$mn 5.1 Last Recommendation

Hikma Pharmaceuticals PLC

Hikma Pharmaceuticals PLC This document, which has been issued by Hikma Pharmaceuticals PLC (the Company ), comprises the written materials/slides for a presentation. This document and its contents are

Hikma Pharmaceuticals PLC This document, which has been issued by Hikma Pharmaceuticals PLC (the Company ), comprises the written materials/slides for a presentation. This document and its contents are

IMS Retail Drug Monitor

IMS Retail Drug Monitor Tracking 13 Key Global Pharma Markets 12 months to November 2004 Regional Sales Breakdown: $US Billions 200 10% 180 Value US$Bill 160 % Growth IMS HEALTH, the global healthcare

IMS Retail Drug Monitor Tracking 13 Key Global Pharma Markets 12 months to November 2004 Regional Sales Breakdown: $US Billions 200 10% 180 Value US$Bill 160 % Growth IMS HEALTH, the global healthcare

2. Managing Director s Review 3. Ordinary Resolutions 4. Question & Answer Time

23 May 2013 0 This document has been prepared by Vita Life Sciences Limited (Vita Life) and comprises written material/slides for a presentation concerning Vita Life. The presentation is for information

23 May 2013 0 This document has been prepared by Vita Life Sciences Limited (Vita Life) and comprises written material/slides for a presentation concerning Vita Life. The presentation is for information

2017 1Q Results. May 2017

217 1Q Results May 217 Agenda 1. Financials 2. Market Fundamental 3. Industry Outlook 4. Plant Operation 5.Expansion 2 Financial Status (Unit: NTD Million) 4Q16 1Q17 QoQ 1Q16 YoY Revenues 152,287 164,486

217 1Q Results May 217 Agenda 1. Financials 2. Market Fundamental 3. Industry Outlook 4. Plant Operation 5.Expansion 2 Financial Status (Unit: NTD Million) 4Q16 1Q17 QoQ 1Q16 YoY Revenues 152,287 164,486

F r a s e r a n d N e a v e, L i m i t e d

F r a s e r a n d N e a v e, L i m i t e d Important notice Certain statements in this Presentation constitute forward-looking statements, including forward-looking financial information. Such forward-looking

F r a s e r a n d N e a v e, L i m i t e d Important notice Certain statements in this Presentation constitute forward-looking statements, including forward-looking financial information. Such forward-looking

Presentation 22 August 2018

Presentation 22 August 2018 Exceeded 3YP targets in 2017, but 2018 is challenging due to continued destocking, store closures and bankruptcies Profit attributable to shareholders (like-for-like) down 19%

Presentation 22 August 2018 Exceeded 3YP targets in 2017, but 2018 is challenging due to continued destocking, store closures and bankruptcies Profit attributable to shareholders (like-for-like) down 19%

Economic outlook. Bangkok Bank position. Strategic priorities and targets

20110603 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.0% 2 0 2008 2009 2010 2011f 1Q11(A)

20110603 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.0% 2 0 2008 2009 2010 2011f 1Q11(A)

Kalbe Farma(KLBF IJ) BUY(Unchanged) Not a Fruitful Year. Equity Indonesia Consumer. Results Note. 29 February 2016

BUY(Unchanged) Not a Fruitful Year. Equity Indonesia Consumer. Results Note. 29 February 2016") Equity Indonesia Consumer Kalbe Farma(KLBF IJ) BUY(Unchanged) Stock Data Target price (Rp) Prior TP (Rp) Shareprice (Rp) Rp1,600 Rp1,710 Rp1,275 Upside/downside (%) +25.5 Sharesoutstanding (m) 47 Marketcap.

Equity Indonesia Consumer Kalbe Farma(KLBF IJ) BUY(Unchanged) Stock Data Target price (Rp) Prior TP (Rp) Shareprice (Rp) Rp1,600 Rp1,710 Rp1,275 Upside/downside (%) +25.5 Sharesoutstanding (m) 47 Marketcap.

Leadership in life insurance. April 2008

Leadership in life insurance April 2008 Agenda Indian life insurance opportunity Organisational overview Performance highlights 2 Agenda Indian life insurance opportunity Organisational overview Performance

Leadership in life insurance April 2008 Agenda Indian life insurance opportunity Organisational overview Performance highlights 2 Agenda Indian life insurance opportunity Organisational overview Performance

Investment Theme 3Q18. Ageing Population. Source: AFP Photo

Investment Theme 3Q18 Ageing Population Source: AFP Photo 91 Investment Theme III: Ageing Population Jason Low, CFA Strategist The global population is growing older and people are living longer. Demographics

Investment Theme 3Q18 Ageing Population Source: AFP Photo 91 Investment Theme III: Ageing Population Jason Low, CFA Strategist The global population is growing older and people are living longer. Demographics

Uni-President 2016 Annual Results ( Updated) :1216 TT

:1216 TT") Uni-President 2016 Annual Results (2017.4.7 Updated) :1216 TT Disclaimers The information contained in this presentation is intended solely for your personal reference. Such information is subject to change

Uni-President 2016 Annual Results (2017.4.7 Updated) :1216 TT Disclaimers The information contained in this presentation is intended solely for your personal reference. Such information is subject to change

Strategic Divestment of Product Verticals. December 14, 2017

Strategic Divestment of Product Verticals December 14, 2017 Disclaimer Important notice The information contained in this presentation is intended solely for your information. Such information is subject

Strategic Divestment of Product Verticals December 14, 2017 Disclaimer Important notice The information contained in this presentation is intended solely for your information. Such information is subject

Morgan Stanley Asia: Overview

Morgan Stanley Asia: Overview July 2007 Notice The information provided herein may include certain non-gaap financial measures. The reconciliation of such measures to the comparable GAAP figures are included

Morgan Stanley Asia: Overview July 2007 Notice The information provided herein may include certain non-gaap financial measures. The reconciliation of such measures to the comparable GAAP figures are included

Investor Presentation. December 2013

Investor Presentation December 2013 24.02.2014 Table of Contents 1. Thai economy 2. Strengthening bank and client base 3. BBL s financial results Thai economy in 2014-2015 Thailand is facing short-term

Investor Presentation December 2013 24.02.2014 Table of Contents 1. Thai economy 2. Strengthening bank and client base 3. BBL s financial results Thai economy in 2014-2015 Thailand is facing short-term

PT Nipress Tbk. Analyst Meeting Presentation. Indonesia Stock Exchange Conference Room Tower 2, 1 st Fl 22 November 2013

PT Nipress Tbk. Analyst Meeting Presentation Indonesia Stock Exchange Conference Room Tower 2, 1 st Fl 22 November 2013 Important Notice and Disclaimer The information and opinions contained in this presentation

PT Nipress Tbk. Analyst Meeting Presentation Indonesia Stock Exchange Conference Room Tower 2, 1 st Fl 22 November 2013 Important Notice and Disclaimer The information and opinions contained in this presentation

INTERIM RESULTS FOR THE SIX MONTHS ENDED 28 FEBRUARY 2015

INTERIM RESULTS FOR THE SIX MONTHS ENDED 28 FEBRUARY 2015 PRESENTATION OUTLINE Review of the period Financial results Trading performance Outlook Questions CLICKS GROUP INTERIM RESULTS 2015 2 REVIEW OF

INTERIM RESULTS FOR THE SIX MONTHS ENDED 28 FEBRUARY 2015 PRESENTATION OUTLINE Review of the period Financial results Trading performance Outlook Questions CLICKS GROUP INTERIM RESULTS 2015 2 REVIEW OF

Investor Presentation. For 2016

Investor Presentation For 216 Bangkok Bank 1. Operating Environment 2. Our Financial Results 216 3. Bangkok Bank s Position 4. Our Key Focus & Strategy 2 The Thai Economy: Steady Trend of Moderate Recovery

Investor Presentation For 216 Bangkok Bank 1. Operating Environment 2. Our Financial Results 216 3. Bangkok Bank s Position 4. Our Key Focus & Strategy 2 The Thai Economy: Steady Trend of Moderate Recovery

ANNUAL RESULTS FOR THE YEAR ENDED 31 AUGUST 2017

ANNUAL RESULTS FOR THE YEAR ENDED 31 AUGUST 2017 PRESENTATION OUTLINE Review of the year Financial results Trading performance Outlook Questions 2 REVIEW OF THE YEAR DAVID KNEALE REVIEW OF THE YEAR Strong

ANNUAL RESULTS FOR THE YEAR ENDED 31 AUGUST 2017 PRESENTATION OUTLINE Review of the year Financial results Trading performance Outlook Questions 2 REVIEW OF THE YEAR DAVID KNEALE REVIEW OF THE YEAR Strong

Important economic directions

3Q 2012 Important economic directions 1. Higher investment both from government and private sectors 2. Higher investment both from foreign direct investment and Thai direct investment 2 Private investment

3Q 2012 Important economic directions 1. Higher investment both from government and private sectors 2. Higher investment both from foreign direct investment and Thai direct investment 2 Private investment

PT Semen Indonesia (Persero) Tbk. And the Prospect of Indonesia Cement Industry. Corporate Presentation - April 2018

Tbk. And the Prospect of Indonesia Cement Industry. Corporate Presentation - April 2018") PT Semen Indonesia (Persero) Tbk. And the Prospect of Indonesia Cement Industry Corporate Presentation - April 2018 Cement Companies in Indonesia Domestic Capacity 2017 Total 107.4 Mio Ton 2017 SMGR market

PT Semen Indonesia (Persero) Tbk. And the Prospect of Indonesia Cement Industry Corporate Presentation - April 2018 Cement Companies in Indonesia Domestic Capacity 2017 Total 107.4 Mio Ton 2017 SMGR market

This presentation contains forward-looking statements, which are based on current expectations and projections about future events, and include all

This presentation contains forward-looking statements, which are based on current expectations and projections about future events, and include all statements other than statements of historical facts,

This presentation contains forward-looking statements, which are based on current expectations and projections about future events, and include all statements other than statements of historical facts,

/ RO

Q1 2016 Quarterly Report Date of report: May 13, 2016 Name of the issuing entity: Antibiotice SA Registered office: 1 Valea Lupului Street, Iasi, zip code 707410, http://www.antibiotice.ro E-mail: relatiicuinvestitorii@antibiotice.ro

Q1 2016 Quarterly Report Date of report: May 13, 2016 Name of the issuing entity: Antibiotice SA Registered office: 1 Valea Lupului Street, Iasi, zip code 707410, http://www.antibiotice.ro E-mail: relatiicuinvestitorii@antibiotice.ro

The emerging Asian middle class -What does it mean for Australian & International Equities

Clime Asset Management The emerging Asian middle class -What does it mean for Australian & International Equities Presented by John Abernethy 1 Disclaimer The information contained in this document is

Clime Asset Management The emerging Asian middle class -What does it mean for Australian & International Equities Presented by John Abernethy 1 Disclaimer The information contained in this document is

Together We Build a Better Future 0

Together We Build a Better Future 0 INDONESIA S CEMENT INDUSTRY: NOW and THE FUTURE OCTOBER 2013 SMGR Corporate Presentation Together We Build a Better Future 1 CEMENT INDUSTRY AT A GLANCE 2 1 Kuala Lumpur

Together We Build a Better Future 0 INDONESIA S CEMENT INDUSTRY: NOW and THE FUTURE OCTOBER 2013 SMGR Corporate Presentation Together We Build a Better Future 1 CEMENT INDUSTRY AT A GLANCE 2 1 Kuala Lumpur

IGG Inc. March Annual Results

IGG Inc. March 2017 Annual Results Disclaimer This presentation and the accompanying slides (the Presentation ) which have been prepared by IGG INC (the Group ) do not constitute any offer or invitation

IGG Inc. March 2017 Annual Results Disclaimer This presentation and the accompanying slides (the Presentation ) which have been prepared by IGG INC (the Group ) do not constitute any offer or invitation

Unilever Investor Event 2018 Graeme Pitkethly 4 th December 2018

Unilever Investor Event 2018 Graeme Pitkethly 4 th December 2018 SAFE HARBOUR STATEMENT This announcement may contain forward-looking statements, including forward-looking statements within the meaning

Unilever Investor Event 2018 Graeme Pitkethly 4 th December 2018 SAFE HARBOUR STATEMENT This announcement may contain forward-looking statements, including forward-looking statements within the meaning

Cordlife delivers 1QFY2015 core net profit before income tax from operations of S$1.7 million

PRESS RELEASE Cordlife delivers 1QFY2015 core net profit before income tax from operations of S$1.7 million - Revenue increased 17.0%, driven by increased client deliveries, while maintaining high and

PRESS RELEASE Cordlife delivers 1QFY2015 core net profit before income tax from operations of S$1.7 million - Revenue increased 17.0%, driven by increased client deliveries, while maintaining high and

Equity Funds and Market Assessing the Damage

Analyst Tan Xuan +6565311579 tanx@phillip.com.sg Equity and Market Assessing the Damage Executive Summary Equity markets and the mutual funds industry experienced sharp sell-off on concerns regarding ongoing

Analyst Tan Xuan +6565311579 tanx@phillip.com.sg Equity and Market Assessing the Damage Executive Summary Equity markets and the mutual funds industry experienced sharp sell-off on concerns regarding ongoing

Opportunity Day Q118. The Stock Exchange of Thailand. 1 June COL Public Company Limited

COL Public Company Limited 1 June 2018 Opportunity Day Q118 The Stock Exchange of Thailand Important Notice The information contained in this presentation is for information purposes only and does not

COL Public Company Limited 1 June 2018 Opportunity Day Q118 The Stock Exchange of Thailand Important Notice The information contained in this presentation is for information purposes only and does not

DKSH Holding Ltd. Presentation Half-year results 2018

DKSH Holding Ltd. Presentation Half-year results 2018 Overview Half-Year 2018 Net sales grew by 7.4% Profit after tax increases 4.5% EBIT on last year s level Increased performance in Healthcare, Performance

DKSH Holding Ltd. Presentation Half-year results 2018 Overview Half-Year 2018 Net sales grew by 7.4% Profit after tax increases 4.5% EBIT on last year s level Increased performance in Healthcare, Performance

Mitra Keluarga Company Focus

October 13, 2015 Mitra Keluarga Company Focus Patricia Gabriela (patricia.gabriela@trimegah.com) Titan in medical industry Initiate coverage on MIKA with BUY We initiate our coverage on MIKA with a Buy

October 13, 2015 Mitra Keluarga Company Focus Patricia Gabriela (patricia.gabriela@trimegah.com) Titan in medical industry Initiate coverage on MIKA with BUY We initiate our coverage on MIKA with a Buy

Together We Build a Better Future 0

Together We Build a Better Future 0 INDONESIA S CEMENT INDUSTRY: NOW and THE FUTURE APRIL 2014 SMGR Corporate Presentation Together We Build a Better Future 1 CEMENT INDUSTRY AT A GLANCE 2 1 Kuala Lumpur

Together We Build a Better Future 0 INDONESIA S CEMENT INDUSTRY: NOW and THE FUTURE APRIL 2014 SMGR Corporate Presentation Together We Build a Better Future 1 CEMENT INDUSTRY AT A GLANCE 2 1 Kuala Lumpur

10 pillars of change in India

10 pillars of change in India India is one of the fastest-growing emerging markets. The government is introducing dramatic changes to strengthen the economy, improve efficiency, reduce corruption and attract

10 pillars of change in India India is one of the fastest-growing emerging markets. The government is introducing dramatic changes to strengthen the economy, improve efficiency, reduce corruption and attract

To put our customers, employees and suppliers at the heart of our business decisions. Operating results 1Q16

To put our customers, employees and suppliers at the heart of our business decisions. Operating results 1Q16 Date 13 May 2016 Important Notice The information contained in this presentation is for information

To put our customers, employees and suppliers at the heart of our business decisions. Operating results 1Q16 Date 13 May 2016 Important Notice The information contained in this presentation is for information

Security Code: 1216 TT Interim Results UPCH UPEC PCSC

Security Code: 1216 TT 2018 Interim Results UPCH UPEC PCSC Disclaimers The information contained in this presentation is intended solely for your personal reference. Such information is subject to change

Security Code: 1216 TT 2018 Interim Results UPCH UPEC PCSC Disclaimers The information contained in this presentation is intended solely for your personal reference. Such information is subject to change

The information contained in this presentation has not been independently verified. No representation or warranty express or implied is made as to,

This This document is not is not for for distribution distribution in the in United the United States States The information contained in this presentation has not been independently verified. No representation

This This document is not is not for for distribution distribution in the in United the United States States The information contained in this presentation has not been independently verified. No representation

Sigma Pharmaceuticals Limited

Investor Relations Contact: Gary Woodford Corporate Affairs Manager Gary.Woodford@signet.com.au Phone: 03 9215 9632 Mobile: 0417 399 204 Mark Hooper CEO and Managing Director Gary Woodford Corporate Affairs

Investor Relations Contact: Gary Woodford Corporate Affairs Manager Gary.Woodford@signet.com.au Phone: 03 9215 9632 Mobile: 0417 399 204 Mark Hooper CEO and Managing Director Gary Woodford Corporate Affairs

BRI Pursuing a Sustainable and Quality Growth

PT Bank Rakyat Indonesia (Persero) Tbk. BRI Pursuing a Sustainable and Quality Growth Expanding Micro and Recovering Small and Medium Businesses Financial Updates Q3-2011 Jakarta, 28 October 2011 Agenda

PT Bank Rakyat Indonesia (Persero) Tbk. BRI Pursuing a Sustainable and Quality Growth Expanding Micro and Recovering Small and Medium Businesses Financial Updates Q3-2011 Jakarta, 28 October 2011 Agenda

Investor Presentation. For 3Q18

Investor Presentation For 3Q18 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 3Q18 2 For 2018, global economic expansion remains solid However, the outlook

Investor Presentation For 3Q18 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 3Q18 2 For 2018, global economic expansion remains solid However, the outlook

Q3/9M FYE19 Results Update

Listing Board Bursa Malaysia Securities Berhad, Main Market Stock Name/ Code AEONCR/ 5139 /9M Results Update 20 Dec 2018 Forward-Looking Statements This document has been prepared by AEON Credit Service

Listing Board Bursa Malaysia Securities Berhad, Main Market Stock Name/ Code AEONCR/ 5139 /9M Results Update 20 Dec 2018 Forward-Looking Statements This document has been prepared by AEON Credit Service

Investor Presentation DBS Group Holdings Ltd November 2017

Investor Presentation DBS Group Holdings Ltd November 2017 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed

Investor Presentation DBS Group Holdings Ltd November 2017 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed

Together We Build a Better Future 0

Together We Build a Better Future 0 INDONESIA S CEMENT INDUSTRY: NOW and THE FUTURE FEBRUARY 2014 SMGR Corporate Presentation Together We Build a Better Future 1 CEMENT INDUSTRY AT A GLANCE 2 1 Kuala Lumpur

Together We Build a Better Future 0 INDONESIA S CEMENT INDUSTRY: NOW and THE FUTURE FEBRUARY 2014 SMGR Corporate Presentation Together We Build a Better Future 1 CEMENT INDUSTRY AT A GLANCE 2 1 Kuala Lumpur

Drug Reimbursement - Croatia. Roganovic Jelena

Drug Reimbursement - Croatia Roganovic Jelena Population: 4,292,095 (July 2017) Area: 56,594 km 2 Density: 75.8/km 2 21 counties http://www.lokalniizbori.com/wp-content/uploads/2013/04/hrvatska-%c5%beupanije.jpg;

Drug Reimbursement - Croatia Roganovic Jelena Population: 4,292,095 (July 2017) Area: 56,594 km 2 Density: 75.8/km 2 21 counties http://www.lokalniizbori.com/wp-content/uploads/2013/04/hrvatska-%c5%beupanije.jpg;

Sanofi India NEUTRAL. Performance Highlights. CMP `4,007 Target Price - 3QCY2017 Result Update Pharmaceutical. Investment Period 12 months

3QCY2017 Result Update Pharmaceutical November 20, 2017 Sanofi India Performance Highlights Y/E Dec. (` cr) 3QCY2017 2QCY2017 % chg (qoq) 3QCY2016 % chg (yoy) Net sales Other income Operating profit 627

3QCY2017 Result Update Pharmaceutical November 20, 2017 Sanofi India Performance Highlights Y/E Dec. (` cr) 3QCY2017 2QCY2017 % chg (qoq) 3QCY2016 % chg (yoy) Net sales Other income Operating profit 627

Strategic Investment in Bank Danamon. December 26, 2017

Strategic Investment in Bank Danamon December 26, 2017 This document contains forward-looking statements in regard to forecasts, targets and plans of PT Bank Danamon Indonesia, Tbk. and its group companies

Strategic Investment in Bank Danamon December 26, 2017 This document contains forward-looking statements in regard to forecasts, targets and plans of PT Bank Danamon Indonesia, Tbk. and its group companies

Sanofi India NEUTRAL. Performance Highlights. CMP `4,007 Target Price - 2QCY2017 Result Update Pharmaceutical. 3-year price chart.

2QCY2017 Result Update Pharmaceutical August 28, 2017 Sanofi India Performance Highlights Y/E Dec. (` cr) 2QCY2017 1QCY2017 % chg (qoq) 2QCY2016 % chg (yoy) Net sales Other income Operating profit 556

2QCY2017 Result Update Pharmaceutical August 28, 2017 Sanofi India Performance Highlights Y/E Dec. (` cr) 2QCY2017 1QCY2017 % chg (qoq) 2QCY2016 % chg (yoy) Net sales Other income Operating profit 556

Cash and Treasury Management Country Report JAPAN

Underwritten by Cash and Treasury Management Country Report Executive Summary Banking The Japanese central bank is the Bank of Japan (BOJ). Bank supervision is performed by the Federal Services Agency

Underwritten by Cash and Treasury Management Country Report Executive Summary Banking The Japanese central bank is the Bank of Japan (BOJ). Bank supervision is performed by the Federal Services Agency

Q4 Presentation February, 2012

Q4 Presentation 2011 15 February, 2012 Disclaimer This presentation has been prepared by Duni AB (the Company ) solely for use at this investor presentation and is furnished to you solely for your information

Q4 Presentation 2011 15 February, 2012 Disclaimer This presentation has been prepared by Duni AB (the Company ) solely for use at this investor presentation and is furnished to you solely for your information

new business seize the potential H&M GROUP CAPITAL MARKETS DAY 2018

new business seize the potential H&M GROUP CAPITAL MARKETS DAY 2018 Disclaimer THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT A CAPITAL

new business seize the potential H&M GROUP CAPITAL MARKETS DAY 2018 Disclaimer THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT A CAPITAL

Tesco in Asia key messages

Tesco in Asia key messages Laurie McIlwee, Group Finance Director Tesco in Asia 2010, 21st 23rd November With a population of more than 3.2 billion, Asia offers enormous opportunity China Tesco is a leading

Tesco in Asia key messages Laurie McIlwee, Group Finance Director Tesco in Asia 2010, 21st 23rd November With a population of more than 3.2 billion, Asia offers enormous opportunity China Tesco is a leading

VINACAPITAL VIETNAM OPPORTUNITY FUND ( VOF ) 30 June 2018 Annual Results

30 June 2018 Annual Results") VINACAPITAL VIETNAM OPPORTUNITY FUND ( VOF ) 30 June 2018 Annual Results 24 October 2018 Public ANDY HO Managing Director and Chief Investment Officer Vietnam s macro indicators GDP growth is among the

VINACAPITAL VIETNAM OPPORTUNITY FUND ( VOF ) 30 June 2018 Annual Results 24 October 2018 Public ANDY HO Managing Director and Chief Investment Officer Vietnam s macro indicators GDP growth is among the

Introduction to INDONESIA

Introduction to INDONESIA Indonesia is the fifth largest economy in Asia in nominal GDP terms and the third most populous nation behind China and India. It has recorded strong economic growth over the

Introduction to INDONESIA Indonesia is the fifth largest economy in Asia in nominal GDP terms and the third most populous nation behind China and India. It has recorded strong economic growth over the

Pre-poll Methodology for Asiamoney Brokers Poll 2016

Pre-poll Methodology for Asiamoney Brokers Poll 2016 Asiamoney s 27 th annual Brokers Poll is scheduled for launch on 4 th July, we invite senior institutional investors at fund management companies, hedge

Pre-poll Methodology for Asiamoney Brokers Poll 2016 Asiamoney s 27 th annual Brokers Poll is scheduled for launch on 4 th July, we invite senior institutional investors at fund management companies, hedge

Investment Case for Asian Fixed Income

For professional clients only Asian Fixed Income Investment Case for Asian Fixed Income July 217 The Outlook for Asia The market outlook for Asia and how it translates into bond market demand remains positive

For professional clients only Asian Fixed Income Investment Case for Asian Fixed Income July 217 The Outlook for Asia The market outlook for Asia and how it translates into bond market demand remains positive

Strategic benefits Building bridges, shaping globalisation

Strategic benefits Building bridges, shaping globalisation An even closer relationship Taking a stand for open trade Working together to shape globalisation Strengthening our ties with Asia The EU-Singapore

Strategic benefits Building bridges, shaping globalisation An even closer relationship Taking a stand for open trade Working together to shape globalisation Strengthening our ties with Asia The EU-Singapore

Receive daily cash for your medical needs. ManuMediCash

Receive daily cash for your medical needs ManuMediCash Benefits at a Glance: Daily Hospital Income Benefit in the event that you need to be hospitalized in Singapore or overseas due to sickness. Daily

Receive daily cash for your medical needs ManuMediCash Benefits at a Glance: Daily Hospital Income Benefit in the event that you need to be hospitalized in Singapore or overseas due to sickness. Daily

ASAHI Group Holdings, LTD.

ASAHI Group Holdings, LTD. FY2012 2Q Financial Results NOTE: All information has been prepared in accordance with generally accepted accounting principles in Japan. Amounts shown in this accounting report

ASAHI Group Holdings, LTD. FY2012 2Q Financial Results NOTE: All information has been prepared in accordance with generally accepted accounting principles in Japan. Amounts shown in this accounting report

Financial Results for the Fiscal Year Ended December, Lion Corporation Itsuo Hama Representative Director and President, Executive Officer

February 10, 2017 Financial Results for the Fiscal Year Ended December, 2016 Lion Corporation Itsuo Hama Representative Director and President, Executive Officer Contents Financial Results for 2016 Financial

February 10, 2017 Financial Results for the Fiscal Year Ended December, 2016 Lion Corporation Itsuo Hama Representative Director and President, Executive Officer Contents Financial Results for 2016 Financial

A new inflection point. 10 February 2017

A new inflection point 10 February 2017 1 Important notice This presentation contains statements with respect to the financial condition, results of operations and business of RB (the Group ) and certain

A new inflection point 10 February 2017 1 Important notice This presentation contains statements with respect to the financial condition, results of operations and business of RB (the Group ) and certain

October 3Q 2018/ 9M 2018 COMPANY AND FINANCIAL UPDATES 1

October 2018 3Q 2018/ 9M 2018 COMPANY AND FINANCIAL UPDATES 1 TABLE OF CONTENT Indonesia Macro Overview 4 Q3 2018/ 9M 2018 Key Financial Highlights 6 Sales and DP/CV Mix 7 Same Store Sales Growth 8 Regional

October 2018 3Q 2018/ 9M 2018 COMPANY AND FINANCIAL UPDATES 1 TABLE OF CONTENT Indonesia Macro Overview 4 Q3 2018/ 9M 2018 Key Financial Highlights 6 Sales and DP/CV Mix 7 Same Store Sales Growth 8 Regional

Understanding the Global ASEAN Consumer

Understanding the Global ASEAN Consumer The Philippines Millennials Roberto B. Tan Treasurer of the Philippines February 2015 ASEAN Offers a Future of Prosperity and Stability Combined GDP of nearly USD3tr

Understanding the Global ASEAN Consumer The Philippines Millennials Roberto B. Tan Treasurer of the Philippines February 2015 ASEAN Offers a Future of Prosperity and Stability Combined GDP of nearly USD3tr

Agenda. Financial Review. Review of Operations. Future Plans and Strategies. Open Forum

22 October 2009 1 Disclaimer The information contained in this presentation is intended solely for your personal reference. Such information is subject to change without notice, its accuracy is not guaranteed

22 October 2009 1 Disclaimer The information contained in this presentation is intended solely for your personal reference. Such information is subject to change without notice, its accuracy is not guaranteed

F&N HALF-YEAR FINANCIAL HIGHLIGHTS

F&N HALF-YEAR FINANCIAL HIGHLIGHTS Important notice Certain statements in this Presentation constitute forward-looking statements, including forward-looking financial information. Such forward-looking

F&N HALF-YEAR FINANCIAL HIGHLIGHTS Important notice Certain statements in this Presentation constitute forward-looking statements, including forward-looking financial information. Such forward-looking

United Overseas Bank Investor Roadshow November 2006

United Overseas Bank Investor Roadshow November 2006 Disclaimer : This material that follows is a presentation of general background information about the Bank s activities current at the date of the presentation.

United Overseas Bank Investor Roadshow November 2006 Disclaimer : This material that follows is a presentation of general background information about the Bank s activities current at the date of the presentation.

JOM FUNDS Monthly Report September 2014

At first some thoughts on my latest trip to Indonesia: JOM FUNDS Monthly Report September 2014 Met with Indonesian companies in Jakarta and Java Island in mid-september. The meeting schedule consisted

At first some thoughts on my latest trip to Indonesia: JOM FUNDS Monthly Report September 2014 Met with Indonesian companies in Jakarta and Java Island in mid-september. The meeting schedule consisted

16 May M FY 2017/18 FINANCIAL RESULTS

16 May 2018 6M FY 2017/18 FINANCIAL RESULTS NOTICE TO RECIPIENTS This presentation and any materials distributed in connection herewith (together, the Presentation ) have been prepared by Douglas GmbH

16 May 2018 6M FY 2017/18 FINANCIAL RESULTS NOTICE TO RECIPIENTS This presentation and any materials distributed in connection herewith (together, the Presentation ) have been prepared by Douglas GmbH

Indian Healthcare Industry

Indian Healthcare Industry 2012 Synopsis Disclaimer: All information contained in this report has been obtained from sources believed to be accurate by Gyan Research and Analytics Pvt. Ltd. (Gyan). While

Indian Healthcare Industry 2012 Synopsis Disclaimer: All information contained in this report has been obtained from sources believed to be accurate by Gyan Research and Analytics Pvt. Ltd. (Gyan). While

53 rd Annual General Meeting Presentation to Shareholders. Tan Sri Dato Megat Zaharuddin Chairman 28 March 2013

53 rd Annual General Meeting Presentation to Shareholders 0 Tan Sri Dato Megat Zaharuddin Chairman 28 March 2013 FY2012 is the first 12-month financial period of our new financial year ended 31 December

53 rd Annual General Meeting Presentation to Shareholders 0 Tan Sri Dato Megat Zaharuddin Chairman 28 March 2013 FY2012 is the first 12-month financial period of our new financial year ended 31 December

2010 Results. Paris - March 2, 2011

2010 Results Paris - March 2, 2011 > Highlights of 2010 > Financial results > Strategy and outlook 2010 Results 2 2010: A Year of Acceleration Highlights of 2010 Revenue of 3,892m, up 19.1% Operating profit

2010 Results Paris - March 2, 2011 > Highlights of 2010 > Financial results > Strategy and outlook 2010 Results 2 2010: A Year of Acceleration Highlights of 2010 Revenue of 3,892m, up 19.1% Operating profit

Challenge of chance: Creating opportunities October 16 19, 2013, Rovinj, Croatia

Travanj 2012. Challenge of chance: Creating opportunities October 16 19, 2013, Rovinj, Croatia Veljača 2012. Content About Overview of key events Sales Business results Share Disclaimer This presentation

Travanj 2012. Challenge of chance: Creating opportunities October 16 19, 2013, Rovinj, Croatia Veljača 2012. Content About Overview of key events Sales Business results Share Disclaimer This presentation

Corporate Presentation Investor Relations Second Quarter 2017

Corporate Presentation Investor Relations Second Quarter 2017 Disclaimer Statements made in this presentation relate to CCU s future performance or financial results are forward-looking statements within

Corporate Presentation Investor Relations Second Quarter 2017 Disclaimer Statements made in this presentation relate to CCU s future performance or financial results are forward-looking statements within

INVESTOR PRESENTATION 9M PT Japfa Comfeed Indonesia Tbk

INVESTOR PRESENTATION 9M 2015 PT Japfa Comfeed Indonesia Tbk Agenda Company Overview Key Investment Highlights Financial Highlights Appendix 2 Company Overview Introduction to Japfa Tbk Established vertically

INVESTOR PRESENTATION 9M 2015 PT Japfa Comfeed Indonesia Tbk Agenda Company Overview Key Investment Highlights Financial Highlights Appendix 2 Company Overview Introduction to Japfa Tbk Established vertically

Investor Day Asia Region Lausanne, June 23, Matteo Pellegrini President, Asia Region Philip Morris International

Investor Day Asia Region Lausanne, June 23, 2010 Matteo Pellegrini President, Asia Region Philip Morris International Agenda environment PMI strategic priorities in Asia Brand portfolio and innovations

Investor Day Asia Region Lausanne, June 23, 2010 Matteo Pellegrini President, Asia Region Philip Morris International Agenda environment PMI strategic priorities in Asia Brand portfolio and innovations

No Boundaries Only Possibilities

No Boundaries Only Possibilities 1 MegaChem Limited Results Presentation Half Year Ended 30 June 2010 2 Industry Overview Value and Profitability Industry Positioning Specialty Chemicals Commodity Chemicals

No Boundaries Only Possibilities 1 MegaChem Limited Results Presentation Half Year Ended 30 June 2010 2 Industry Overview Value and Profitability Industry Positioning Specialty Chemicals Commodity Chemicals

ASEA Global X FTSE Southeast Asia ETF

Global X FTSE Southeast Asia ETF ETF.com segment: Equity: Southeast Asia - Total Market Competing ETFs: N/A Related ETF Channels: Southeast Asia, Total Market, Broad-based, Asia-Pacific, Equity, Vanilla,

Global X FTSE Southeast Asia ETF ETF.com segment: Equity: Southeast Asia - Total Market Competing ETFs: N/A Related ETF Channels: Southeast Asia, Total Market, Broad-based, Asia-Pacific, Equity, Vanilla,

A.M. Best Market Briefing at the EAIC 2018

A.M. Best Market Briefing at the EAIC 2018 Agenda 2 Perspectives on the Global Reinsurance Market Stefan Holzberger Chief Rating Officer 7 May 2018 AM Best Company, Inc. (AMB) and/or its licensors and

A.M. Best Market Briefing at the EAIC 2018 Agenda 2 Perspectives on the Global Reinsurance Market Stefan Holzberger Chief Rating Officer 7 May 2018 AM Best Company, Inc. (AMB) and/or its licensors and

EBOS Group Ltd. For personal use only. Results presentation Financial Year ended 30 June August 2016

EBOS Group Ltd Results presentation Financial Year ended 30 June 2016 Patrick Davies John Cullity Chief Executive Officer Chief Financial Officer 25 August 2016 Disclaimer The information in this presentation

EBOS Group Ltd Results presentation Financial Year ended 30 June 2016 Patrick Davies John Cullity Chief Executive Officer Chief Financial Officer 25 August 2016 Disclaimer The information in this presentation

Highlights. 9M17 Results. Rp billion; % 9M16 9M17 % FY16 1Q17 2Q17 3Q17

Investor Newsletter December 2017 Shareholding Composition Sep-16 Sep-17 Bank Danamon Indonesia 92.1% 92.1% Public ( 5%) 7.9% 7.9% Credit Ratings (PEFINDO) Rating/Outlook Corporate Bonds Mudharabah Bonds

Investor Newsletter December 2017 Shareholding Composition Sep-16 Sep-17 Bank Danamon Indonesia 92.1% 92.1% Public ( 5%) 7.9% 7.9% Credit Ratings (PEFINDO) Rating/Outlook Corporate Bonds Mudharabah Bonds

FINANCE TO ENSURE ASIA S ECONOMIC GROWTH DR. RANEE JAYAMAHA CHAIRPERSON - HATTON NATIONAL BANK PLC

FINANCE TO ENSURE ASIA S ECONOMIC GROWTH DR. RANEE JAYAMAHA CHAIRPERSON - HATTON NATIONAL BANK PLC TABLE 1 : REAL GDP GROWTH OF SOUTHEAST ASIA, CHINA AND INDIA (ANNUAL PERCENTAGE CHANGE) PROJECTIONS ASEAN-6

FINANCE TO ENSURE ASIA S ECONOMIC GROWTH DR. RANEE JAYAMAHA CHAIRPERSON - HATTON NATIONAL BANK PLC TABLE 1 : REAL GDP GROWTH OF SOUTHEAST ASIA, CHINA AND INDIA (ANNUAL PERCENTAGE CHANGE) PROJECTIONS ASEAN-6

Full Year 2011 Results

Jakarta, 28 March 2012 PT Semen Gresik (Persero) Tbk. JSX : SMGR Reuters : SMGR.JK Bloomberg : SMGR.IJ Market Capitalization as of 30/12/2011 Rp 67,915,904,000,000 Issued shares 5,931,520,000 Share Price

Jakarta, 28 March 2012 PT Semen Gresik (Persero) Tbk. JSX : SMGR Reuters : SMGR.JK Bloomberg : SMGR.IJ Market Capitalization as of 30/12/2011 Rp 67,915,904,000,000 Issued shares 5,931,520,000 Share Price

Ezion Holdings Limited. Informal Meeting with Shareholders 23 March 2018

Ezion Holdings Limited Informal Meeting with Shareholders 23 March 2018 1 Disclaimer This informal meeting is being convened for the purpose of providing the Shareholders with a summary of the Proposed

Ezion Holdings Limited Informal Meeting with Shareholders 23 March 2018 1 Disclaimer This informal meeting is being convened for the purpose of providing the Shareholders with a summary of the Proposed

AXA. Henri de Castries. Chairman & CEO. London - October 2, Sanford C. Bernstein Strategic Decisions Conference

AXA Henri de Castries Chairman & CEO London - October 2, 2013 Sanford C. Bernstein Strategic Decisions Conference Cautionary note concerning forward-looking statements Certain statements contained herein

AXA Henri de Castries Chairman & CEO London - October 2, 2013 Sanford C. Bernstein Strategic Decisions Conference Cautionary note concerning forward-looking statements Certain statements contained herein

4 th Quarter 2015 Financial Results

4 th Quarter 2015 Financial Results 23 rd February 2016 Disclaimer The presentation is prepared by Super Group Ltd ( Super or the Group ) and is solely for the purpose of corporate communication and general

4 th Quarter 2015 Financial Results 23 rd February 2016 Disclaimer The presentation is prepared by Super Group Ltd ( Super or the Group ) and is solely for the purpose of corporate communication and general