Framing Lottery Choices

|

|

|

- Peregrine Newton

- 5 years ago

- Views:

Transcription

1 Framing Lottery Choices by Dale O. Stahl Department of Economics University of Texas at Austin February 3, 2016 ABSTRACT There are many ways to present lotteries to human subjects: pie charts, vertical or horizontal bars, sometimes with numerical probabilities, sometimes with an indifference options. Unfortunately, the theories to be tested are silent on all these framing aspects. Expected Utility Theory (EUT) simply assumes that the decision maker has a complete understanding of the feasible payoffs and their respective probabilities, and can costlessly, instantaneously and errorlessly evaluate each lottery. We design and conduct an experiment which varies the framing of the lotteries in ways that lessen the cognitive difficulty of comparing lotteries. We find that as the ease of comparing lotteries increases, choice behavior becomes more consistent with EUT. 1

2 1. Introduction. The simplest case of a decision under risk is the choice between two objective lotteries. Indeed, theories about decisions under risk are typically developed first for these simple cases. Consequently, it is natural to test proposed theories with experiments that entail such choices. It is at the experimental design stage that we encounter many questions about how to present (or frame) the choices. 1 One common design is to present a lottery in the form of a pie chart: each section of the pie corresponds to a particular monetary payoff and the area of the section (as a percentage of the whole pie) is equal to the probability the lottery will yield that payoff. For a choice task, two pie charts are displayed on a computer screen side-by-side. Usually colors or distinctive shadings are used for specific payoffs. Sometimes, the numerical probabilities are listed below the pie chart. The choice screen also displays buttons to click (or keys to press) to make a choice. Sometimes an option of indifference is also available. 2 Unfortunately, the theories to be tested are silent on all these framing aspects. For instance, Expected Utility Theory simply assumes that the decision maker has a complete understanding of the lotteries (i.e. the feasible payoffs and their respective probabilities), and can costlessly, instantaneously and errorlessly evaluate each lottery. We do not have to be very cynical to question whether human subjects satisfy this auxiliary assumption in experiments when lotteries are presented as pie charts. Without numerical probabilities it is not easy to accurately assess the relative areas of the pie sections, and comparisons across the lotteries can be difficult due to the rotational orientation of the pies. Computing expected monetary values, let alone expected utilities, can be challenging to typical human subjects. Furthermore, the subjects almost surely have no experience with this specific or similar decision task, so they will not have a conceptual framework or useful heuristics to help them make the decision. They will find themselves in a situation similar to arriving in a foreign country with no knowledge of the local language and having to answer a question by the local customs official. 1 See Harrison and Rutström (2008) for a review of designs. 2 E.g. Hey and Orme (1994) and Harrison and Rutström (2009). 2

3 One of the main roles of college economics courses is to provide students with new concepts and a vocabulary to analyze economic choices. Therefore, we must recognize that lottery choice experiments test the joint hypotheses of an idealized theory and a complete and accurate understanding of the task and consequences by the subjects. When the latter understanding hypothesis is unlikely to hold, observations at odds with the joint hypotheses do not logically imply that the theory is false. Fortunately there are ways to exogenously vary the veracity of the understanding hypothesis, thereby partially unravelling the cause of the observed behavior. Specifically, we can change the presentation of the lotteries in ways that make the comparisons easier for the subjects. In this paper we report results from three presentation treatments. We start with a treatment that is similar to the standard framing to serve as a benchmark. The second treatment is essentially a rearrangement of the computer display that we believe makes it visually easier to compare the lotteries. The third treatment adds statements of facts about differences between the lotteries. To rule out learning across treatments, a subject participated in only one treatment. We find that each successive treatment results in less risk-averse behavior and an increase in risk-neutral behavior. We also want to infer any change in the proportion of the subjects who behave consistently with EUT. For this purpose, we estimate a two-parameter logistic choice function in which one parameter is for the utility function and the second parameter is for the precision. The lower the estimated precision, the more inconsistencies with EUT. We find a monotonic increase in the average precision, indicating fewer inconsistencies with EUT with the latter treatments. We believe it is important to recognize the heterogeneity in behavior in the subject population. Accordingly, we characterize the heterogeneity using a Bayesian method to estimate the distribution of the two parameters in the subject population (by treatment). Using this method, we estimate a dramatic increase in the proportion of the population that is behaviorally indistinguishable from risk-neutrality (i.e. maximize expected monetary value) from 12% to 45%. We also find no evidence of systematic fanning-out. 3

4 Section 2 presents the experimental design. Section 3 presents the analysis of the data. Section 4 concludes with a discussion. 2. The Experimental Design. We will first describe the lotteries that were used, and second the treatments. To avoid confounding effects from complicated lotteries, we chose lotteries with three possible outcomes: $5, $25, and $45. The lowest payoff was $5 instead of $0 to avoid the psychological effect of $0. This choice allows us to specify the utility function with just one parameter, such that U($5) = 0, U($45) = 1, and U($25) = u. Further, u = 0.5 represents risk neutrality. With three possible outcomes, lotteries can be represented as points in a Machina (1982) triangle. Figure 1 displays a Machina triangle with the lottery pairs shown as a line connecting two points (lotteries). For each pair, the one closest to the origin is the safe lottery, and the one closest to the diagonal boundary is the risky lottery. EUT implies that all indifference curves have slope u/(1-u). Whether EUT predicts choice of the safe or risky lottery depends solely u/(1-u). If the slope is less than u/(1-u), EUT predicts choice of the safe lottery, and if the slope is greater than u/(1-u), EUT predicts choice of the risky lottery. Since u can vary by subjects, we want to have lottery pairs with a variety of slopes. The slopes in our lottery pairs range from 0.5 to 4.0. To maximize the monetary incentive of each choice, we choose lotteries close to the safe origin and the diagonal boundary. The difference in the expected monetary value of the pairs ranged from $0 to $3, with an average of $2. Also to maximize the monetary incentive of each choice within our budget, we used 15 choices. While only 15 choices would be inadequate for some purposes, it suffices for our purpose. Moreover, there is a reasonable variety of pairs and instances of identical slopes to test for the EUT implication of parallel indifference curves. 4

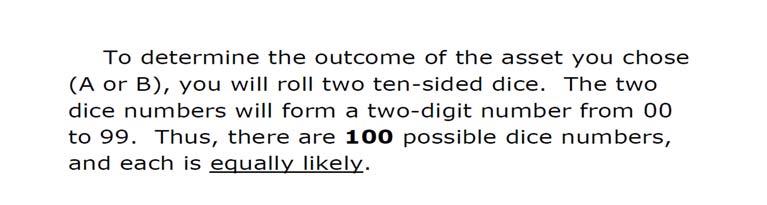

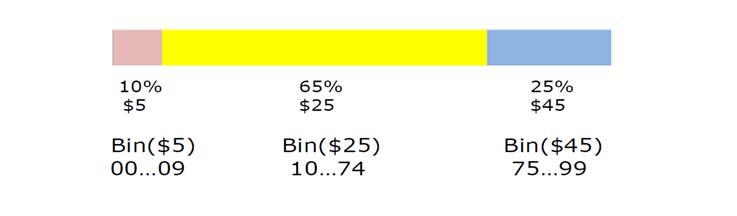

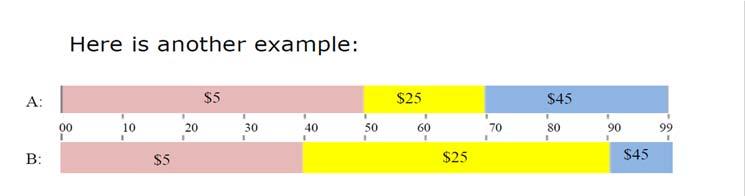

5 Figure 1. Lottery Pairs p p 5 All three treatments use sectioned horizontal bars to represent the lotteries with the sections ordered by increasing payoff. The $5 section was always colored pink; the $25 section was always colored yellow; and the $45 section was always colored blue. The length of each section as a proportion of the whole bar was exactly equal to the lottery s probability of the associated payoff. Figure 2. Representation of a Lottery The implementation of a lottery was described and carried out as follows. Two ten-sided dice are thrown: one blue die and one red die. The blue die counts 10s and the red die counts 1s. If the blue die is 6 and the red die is 3, the dice number is 63. All dice numbers from 00 to 99 are equally likely. Let pi (i = 5, 25, 45) denote the probability the lottery will yield payoff $5, 5

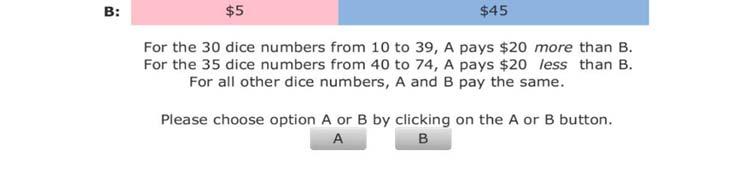

6 $25 and $45 respectively. If the dice number is less than p5, then the lottery will yield $5; if the dice number is greater than p5 but less than p5+p25, then the lottery will yield $25; if the dice number is greater than p5+p25, then the lottery will yield $45. We argue that this description and presentation is at least as understandable as the pie chart alternative. In the first treatment, two lotteries are displayed as side-by-side horizontal bars, comparable to side-by-side pie charts. Full instructions for each treatment are provided in Appendices A-C. In the second treatment, the horizontal bars are displayed one above the other. In addition each bar has a ruler line that runs from 00 to 99 corresponding to the possible dice numbers. In our opinion, it is much easier to compare the two lotteries in this stacked display. 3 For example, if lottery A pays $5 with probability 15%, and lottery B pays $5 with probability 25%, then it is fairly easy to see that both lotteries will pay $5 for all dice numbers from 00 to 14, and B will pay $20 more than A for dice number from 15 to 24. However, not all subjects may notice this, so we display these facts in a statement on the choice screen. It is possible that not all subjects recognize the usefulness of these facts. Therefore, we designed a third treatment in which the instructions focus the subjects attention on these facts via a short quiz, as well as also including in the Instructions 4 a statement of the form: because lottery A will pay $20 more than B for 35 dice numbers, and pay $20 less than B for 20 dice numbers, on average A will pay more than B. Obviously this additional statement is equivalent to informing the subjects about which lottery has the highest expected monetary value, but it does not suggest that maximizing expected monetary value is the right choice. 5 All subjects are free to consider the riskiness of each lottery. Indeed, risky lotteries stand out visually because the $25 payoff for a risky lottery corresponds to a much shorter (yellow) section of the bar. This visual saliency of the risk could discourage other comparisons. Moreover, the understanding 3 Camerer (1989), and Wakker, Erev and Webber (1994) utilized a similar display. 4 This statement is not displayed on the choice screens (see Appendix C). 5 Harrison and Rutström (2008) report that providing subjects with the expected monetary value of each lottery induces a sharp reduction in the estimated risk aversion. 6

7 hypothesis assumes that all subjects know the difference in expected monetary value. We argue that this third treatment makes the understanding hypothesis more likely to hold. Forty subjects participated in each treatment. The subjects were recruited from the general population of students at the University of Texas at Austin; however, graduate students in economics were not allowed to participate. An individual subject sat at a computer screen, read the instructions and made choices at their own pace. The experiment took from 10 to 30 minutes, and the average payoff was $ Analysis of the Data. a. Aggregate Percentage of Risky Choices A central hypothesis is that the proportion of risky lottery choices should increase with the slope ( p45/ p5) of the pair. Further, we expect the proportion also to increase with the treatment. Figure 3 displays the relevant aggregate data. In the legend, Tn stands for Treatment n. Figure 3. Percent Risky Lottery Choices T3 T2 T p 45 / p 5 7

8 Visually the data is consistent with our hypotheses for slopes greater than 1. That is, the curves are mostly upward sloping and each successive treatment shifts the curves upward for slopes greater than 1. A 3-by-12 ANOVA shows that the visual result is statistically significant at all common confidence levels. Detailed analysis of the treatment effect reveals that while the change from treatment 1 to treatment 3 is statistically significant, the change from treatment 1 to treatment 2 is not statistically significant at the 10% level. Since a EUT subject who is not riskloving will never choose a risky lottery when the slope is less than 1, the lack of any effect in this region can be attributed to the lack of risk-lovers in the subject pool. b. Mapping Behavior to EUT Model. The next question we want to address is how the framing treatment affects the likelihood that subjects behave according to EUT. Our first step is to map the observed behavior into a distribution over the two parameters of a simple logistic EUT model. Letting u U($25), the expected utility of a generic lottery is EU(p u) i {5,25,45} piui = p45 + (1- p5 p45)u. (1) Thus, given two lotteries p A and p B, the difference in expected utility is EU A,B (u) EU(p A u) - EU(p B u) = (1-u) p45 - u p5, (2) where p45 = (p45 p45), etc. A B Letting be the precision of the logistic choice, the probability of choosing lottery p A over p B is P(u, ) 1/[1 + exp{- EU A,B (u)}]. (3) 8

9 Obviously, the probability of choosing lottery p B over p A is 1 - P(u, ). Given a subject s 15 choices, we can calculate the likelihood of those choices as a function of (u, ) by computing the product of the probabilities for each choice. Provided we are willing to assume a prior on (u, ), we can compute a Bayesian posterior distribution on (u, ). In other words, we can map the behavior into a distribution on parameters of the logistic EUT model. Moreover, assuming the subjects are random draws from a common subject pool, we can refine the posterior distribution. Adopting the method of Stahl (2014, 2015), briefly described in Appendix D, we compute the posterior distribution of (u, ) for the population of subjects for each treatment. Figure 3 displays the results. 9

(a) Treatment 1 1.4 1.3 1.2 1.1 1 0.9 0.8 0.7 0.6 0.5 0.4 0.3 0.2 0.1 0 0 0.075 0.15 0.225 0.3 0.375 0.45 0.525 0.6 0.675 0.75 0.825 0.9 0.975 u 0.5 0.95 0.838 0.725 0.613 p( ) 10")

10 Figure 3. Population Distribution of (u, ) by Treatment u p( ) (a) Treatment u p( ) 10

(c) Treatment 3 The vertical scales are the same for all three graphs to facilitate comparisons. Instead of on the depth axis, we plot p( ) 1/[1 + exp(-0.")

11 (b) Treatment u p ) (c) Treatment 3 The vertical scales are the same for all three graphs to facilitate comparisons. Instead of on the depth axis, we plot p( ) 1/[1 + exp(-0.05 )], which translates into the behavioral probability that an option with a 5% greater value will be chosen. The visual differences between these graphs is dramatic. With treatment 1, the posterior is diffuse and spread over low precisions and u > 0.5, which is consistent with the common finding that subjects appear to be risk averse and that EUT does not fit behavior well. Moving to treatment 2, we see a decrease in high values of u (risk-aversion) and two small spikes at high precisions. This observation suggests that the stacked bars did facilitate comparisons for some subjects thereby increasing their consistency. 11

12 With treatment 3, we see a dramatic spike near u = 0.5 and p = 1, which represents the risk-neutral EU maximizer. We also observe a further decrease in the spread over u. Table 1 shows the mean and standard deviation of the distribution by treatment. Table 1. Mean and Standard Deviation by Treatment Treatment 1 Treatment 2 Treatment 3 u (0.161) (0.122) (0.126) p( ) (0.112) (0.120) (0.124) Clearly the mean u decreases and the mean p( ) increases with the treatment. c. Shifts in Probability Mass by Treatment. Our next objective is to use the posterior distributions to discern the shift in probability mass towards the risk-neutral EUT model with treatment. To do this, we need the concept of behaviorally distinguishable parameters. To assess whether our data (xi) was generated by (u, ) or (u, ), we typically compute the log-likelihood ratio (LLR): ln[f(xi u, )/f(xi u, )]. However, it is well-known that likelihood-ratio tests are subject to type-i and type-ii errors. We define (u, ) to be behaviorally indistinguishable from (u, ), if either of the type-i and type-ii error rates 6 exceed 10%, and to be behaviorally distinguishable if both of the type-i and type-ii error rates are less than or equal to 10%. To begin, we want to know what percent of the population is behaviorally indistinguishable from 50:50 random choices (hereafter referred to as Level-0 or L0 behavior). Since the latter entails the simple restriction that = 0, we can compute whether (u, ) is behaviorally indistinguishable from (u, 0), and then integrate the posterior over all the points (u, ) that are behaviorally indistinguishable from (u, 0). We do this for each treatment and report the results in the first row of Table 2. It is curious that Treatment 2 produces the largest mass of Level-0 behavior. One possible explanation is that there was some learning by doing (even 6 These rates can be computed exactly since there are only 2 15 possible 15-tuples of choice data for an individual subject. For details, see Stahl (2014, 2015). 12

13 without feedback) which manifests itself as inconsistent behavior, whereas the quiz in Treatment 3 induced similar learning before the choices were made. Table 2. Posterior Probability of Hypotheses Treatment 1 Treatment 2 Treatment 3 Level Not L0 & u= Not L0 & u EMV* The second computation of interest is the probability mass that is behaviorally distinguishable from Level-0 but indistinguishable from risk-neutrality: i.e. the integral of the posterior over all the points (u, ) that are behaviorally indistinguishable from (0.5, ). These results are reported in the second row of Table 2. Clearly, Treatment 3 more than doubles the amount of risk-neutral behavior. The third row of Table 2 is calculated as 1.0 minus the sum of the first two rows. Thus, the numbers in this row are the probability mass that is behaviorally distinguishable from Level=0 and behaviorally distinguishable from risk-neutrality. This mass decreases substantially from treatment 1 to treatment 3. The third and final computation of interest is the probability mass that is behaviorally indistinguishable from very precise maximization of EMV: i.e. the integral of the posterior over all the points (u, ) that are behaviorally distinguishable from Level=0 but behaviorally indistinguishable from (0.5, 138) 7. These results are reported in the fourth row of Table 2. Clearly, Treatment 3 produces the largest mass of very precise maximization of EMV. Moreover, the proportions of those who are risk neutral but not Level-0 (second row of Table 2), and who are very precise (fourth row) by treatment are 0.391, and respectively. 8 In 7 p(138) = 0.999, so choosing the inferior lottery when the difference in expected value is 5% would happen only 1 out of 1000 times; hence, we consider this very high precision. 8 Row 4 divided by row 2. 13

14 other words, Treatment 3 also produces a significant increase in the precision of the risk-neutral types. d. Common Ratio Tests. In the design there are three p45/ p5 slope values that occurred twice: (3, 2 and 0.5). One occurrence entailed lottery pairs that were in the northwest area of Figure1, and the other entailed lottery pairs that were in the southeast area of Figure 1. These pairs allow us to test the common ratio implication of EUT: that the choices in each occurrence with a common slope should be both risky or both safe. The Allais paradox is the classic example of failure of this prediction. In the Allais paradox, one lottery pair is in the northwest area of Figure 1 and the other pair is in the southeast area. The typical finding is that subjects choose the safe lottery from the northwest pair and the risky lottery from the southeast pair. This behavior suggests a fanning out of the indifference curves such that U($25) is larger for the northwest pair than for the southwest pair, as if subjects were more risk averse when the expected value is high. 9 Table 3 displays the number of switches from safe to risky (S to R) and vice versa. Table 3. Common Ratio Results Treatment 1 Treatment 2 Treatment 3 S to R R to S Total % EUT Since EUT predicts no switching (although the logistic choice model allows switching as an idiosyncratic error), the total number of switches (out of 120 possible) indicates the possible violations of EUT. The number of switches decreases with treatment, and with Treatment 3, 83.3% of all choices are consistent with EUT (i.e. no switches). Curiously, we find essentially 9 See Machina (1982, 1987). 14

15 the same number of R to S switches as S to R switches. Thus, the fanning out hypothesis is no more likely than the contrary fanning in hypothesis. It seems more plausible that these switches are idiosyncratic errors rather than a manifestation of non-eut preferences. These findings are consistent with Kagel, et al. (1990). 4. Conclusions. We designed three presentation treatments for binary lottery experiments. The treatments systematically increased ease of comparing the lotteries. As anticipated, with increased ease of comparison, behavior became more consistent with EUT. More risky choices were made, and the mean measure of risk-aversion decreased from 0.7 to 0.6. Further, behavior became more precise, which can be interpreted as the influence of the fundamentals increasing relative to idiosyncratic features, inattention or noise. Moreover, the proportion of behavior that was consistent with maximizing expected monetary value went from 12% to 45%. Finally, we found no evidence for the fanning out hypothesis that is used to explain the Alais paradox. Clearly, framing effects are significant. Therefore, observed behavior that appears to be inconsistent with EUT may actually be driven by obscure framing of the choice. Of course, outside the laboratory, choices are often obscurely framed, so it would be premature to predict EUT behavior for those choices. On the other hand, when stakes are high and experience has provided useful tools of comparison, EUT may perform well. 15

16 References Camerer, C. (1989). An experimental test of several generalized utility theories, J. of Risk and Uncertainty, 2, Harrison, G. (1989). Theory and Misbehavior of First-Price Auctions, Am. Econ. Rev., 79, Harrison, G. (1992). Theory and Misbehavior of First-Price Auctions: Reply, Am. Econ. Rev., 82, Harrison, G., and Rutström, E. (2008). Risk Aversion in the Laboratory, In J. C. Cox and G. W. Harrison, eds., Research in Experimental Economics, 12, Harrison, G., and Rutström, E. (2009). Expected Utility and Prospect Theory: One Wedding and Decent Funeral, Experimental Economics, 12, Hey, J., and Orme, C. (1994). Investigating Generalizations of Expected Utility Theory Using Experimental Data, Econometrica, 62, Kagel, J., MacDonald, D., and Battalio, R. (1990). "Tests of `Fanning Out of Indifference Curves: Results from Animal and Human Experiments American Economic Review, 80, Machina, M. (1982). 'Expected Utility' Analysis Without the Independence Axiom, Econometrica, 50, Machina, M. (1987). Choice Under Uncertainty: Problems Solved and Unsolved," Journal of Economic Perspectives, 1, Stahl, D. (2014). Heterogeneity of Ambiguity Preferences, Rev. of Econ. and Statistics, 96, Stahl, D. (2015)."Re-examination of Experiment Data on Lottery Choices," working paper. Wakker, P., Erev, I., and Weber, E. (1994). Comonotonic independence: The critical test between classical and rank-dependent utility theories, J. of Risk and Uncertainty, 9,

17 APPENDIX A Instructions for Treatment 1 Pg 1: Welcome. This is an experiment about economic decision making in which you are asked to make 15 choices. Each choice will be between two assets whose dollar returns have different levels of uncertainty. You may take as much time as you need to make your 15 choices. After you have made your choices, the uncertainty about the return to the assets you chose will be resolved by the roll of dice. When you conclude, you will be paid in cash an amount that depends on the choices you made, and on the outcomes of the dice rolls. Earnings can range from $5 to $45. Pg 2: Pg 3: 1

18 Pg 4: 2

19 Pg 5: Pg 6: 3

20 Pg 7: 4

21 Pg 8: 5

22 APPENDIX B Instructions for Treatment 2 Pages 1-2 are the same as in Treatment 1. Pg 3: Pg 4: Pg 5: 6

23 Demo Screen: Pg 6: Pg 7: 7

24 APPENDIX C Instructions for Treatment 3 Page 1 is the same as in Treatments 1 and 2. Pg 2: Pg 3: 8

25 Pg 4: Pg 5: Pg 6: 9

26 Pg 7: 10

27 Pg 8: Demo Screen: Pg 9: 11

28 Pg 10: 12

29 APPENDIX D: Method Used to Produce Figure 3. Let xi denote the choice data for subject i, and let f(xi ) denote the probability of xi given parameter vector (, u). Given a prior g0 on, by Bayes rule, the posterior on is g( xi) f(xi )g0( )/ f(xi z)g0(z)dz. (D1) However, eq(d1) does not use information from the other subjects even though those subjects were randomly drawn from a common subject pool. Let N be the number of subjects in the data set. When considering subject i, it is reasonable to use as a prior, not g0, but gi( ) 1 N 1 h i g( xh) (D2) In other words, having observed N-1 subjects, gi( ) is the probability that the N th random draw from the subject pool will have parameter vector. We then compute ĝ i ( x) f(xi )gi( )/ f(xi z)gi(z)dz, (D3) where x denotes the entire N-subject data set. Finally, we aggregate these posteriors to obtain 1 N g*( x) ĝ i 1 i ( x). (D4) N We can interpret g*( x) as the probability density that a random draw from the subject pool will have parameter vector. When implementing this method we specified the prior g0 as follows. For the logit precision parameter, we specify = 20ln[p/(1-p)] with p uniform on [0, 0.999]. In this formulation, p can be interpreted as the probability an option with a 5% greater value will be chosen. u is uniform on [0, 1]. These two distributions are assumed to be independent. For computations, we used a grid of 41x41points.

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions Susan K. Laury and Charles A. Holt Prepared for the Handbook of Experimental Economics Results February 2002 I. Introduction

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions Susan K. Laury and Charles A. Holt Prepared for the Handbook of Experimental Economics Results February 2002 I. Introduction

Rational theories of finance tell us how people should behave and often do not reflect reality.

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

On the Performance of the Lottery Procedure for Controlling Risk Preferences *

On the Performance of the Lottery Procedure for Controlling Risk Preferences * By Joyce E. Berg ** John W. Dickhaut *** And Thomas A. Rietz ** July 1999 * We thank James Cox, Glenn Harrison, Vernon Smith

On the Performance of the Lottery Procedure for Controlling Risk Preferences * By Joyce E. Berg ** John W. Dickhaut *** And Thomas A. Rietz ** July 1999 * We thank James Cox, Glenn Harrison, Vernon Smith

A NOTE ON SANDRONI-SHMAYA BELIEF ELICITATION MECHANISM

The Journal of Prediction Markets 2016 Vol 10 No 2 pp 14-21 ABSTRACT A NOTE ON SANDRONI-SHMAYA BELIEF ELICITATION MECHANISM Arthur Carvalho Farmer School of Business, Miami University Oxford, OH, USA,

The Journal of Prediction Markets 2016 Vol 10 No 2 pp 14-21 ABSTRACT A NOTE ON SANDRONI-SHMAYA BELIEF ELICITATION MECHANISM Arthur Carvalho Farmer School of Business, Miami University Oxford, OH, USA,

Making Hard Decision. ENCE 627 Decision Analysis for Engineering. Identify the decision situation and understand objectives. Identify alternatives

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

PAULI MURTO, ANDREY ZHUKOV

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

Learning Objectives = = where X i is the i t h outcome of a decision, p i is the probability of the i t h

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

Outline. Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion

Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion 2 Simple Lotteries 3 Simple Lotteries Advanced Microeconomic Theory

Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion 2 Simple Lotteries 3 Simple Lotteries Advanced Microeconomic Theory

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

Reduction of Compound Lotteries with. Objective Probabilities: Theory and Evidence

Reduction of Compound Lotteries with Objective Probabilities: Theory and Evidence by Glenn W. Harrison, Jimmy Martínez-Correa and J. Todd Swarthout July 2015 ABSTRACT. The reduction of compound lotteries

Reduction of Compound Lotteries with Objective Probabilities: Theory and Evidence by Glenn W. Harrison, Jimmy Martínez-Correa and J. Todd Swarthout July 2015 ABSTRACT. The reduction of compound lotteries

Answers to chapter 3 review questions

Answers to chapter 3 review questions 3.1 Explain why the indifference curves in a probability triangle diagram are straight lines if preferences satisfy expected utility theory. The expected utility of

Answers to chapter 3 review questions 3.1 Explain why the indifference curves in a probability triangle diagram are straight lines if preferences satisfy expected utility theory. The expected utility of

Chapter 1 Microeconomics of Consumer Theory

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

Risk aversion, Under-diversification, and the Role of Recent Outcomes

Risk aversion, Under-diversification, and the Role of Recent Outcomes Tal Shavit a, Uri Ben Zion a, Ido Erev b, Ernan Haruvy c a Department of Economics, Ben-Gurion University, Beer-Sheva 84105, Israel.

Risk aversion, Under-diversification, and the Role of Recent Outcomes Tal Shavit a, Uri Ben Zion a, Ido Erev b, Ernan Haruvy c a Department of Economics, Ben-Gurion University, Beer-Sheva 84105, Israel.

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes,

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

Unraveling versus Unraveling: A Memo on Competitive Equilibriums and Trade in Insurance Markets

Unraveling versus Unraveling: A Memo on Competitive Equilibriums and Trade in Insurance Markets Nathaniel Hendren October, 2013 Abstract Both Akerlof (1970) and Rothschild and Stiglitz (1976) show that

Unraveling versus Unraveling: A Memo on Competitive Equilibriums and Trade in Insurance Markets Nathaniel Hendren October, 2013 Abstract Both Akerlof (1970) and Rothschild and Stiglitz (1976) show that

Reverse Common Ratio Effect

Institute for Empirical Research in Economics University of Zurich Working Paper Series ISSN 1424-0459 Working Paper No. 478 Reverse Common Ratio Effect Pavlo R. Blavatskyy February 2010 Reverse Common

Institute for Empirical Research in Economics University of Zurich Working Paper Series ISSN 1424-0459 Working Paper No. 478 Reverse Common Ratio Effect Pavlo R. Blavatskyy February 2010 Reverse Common

Expected utility theory; Expected Utility Theory; risk aversion and utility functions

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

Probability. An intro for calculus students P= Figure 1: A normal integral

Probability An intro for calculus students.8.6.4.2 P=.87 2 3 4 Figure : A normal integral Suppose we flip a coin 2 times; what is the probability that we get more than 2 heads? Suppose we roll a six-sided

Probability An intro for calculus students.8.6.4.2 P=.87 2 3 4 Figure : A normal integral Suppose we flip a coin 2 times; what is the probability that we get more than 2 heads? Suppose we roll a six-sided

ANASH EQUILIBRIUM of a strategic game is an action profile in which every. Strategy Equilibrium

Draft chapter from An introduction to game theory by Martin J. Osborne. Version: 2002/7/23. Martin.Osborne@utoronto.ca http://www.economics.utoronto.ca/osborne Copyright 1995 2002 by Martin J. Osborne.

Draft chapter from An introduction to game theory by Martin J. Osborne. Version: 2002/7/23. Martin.Osborne@utoronto.ca http://www.economics.utoronto.ca/osborne Copyright 1995 2002 by Martin J. Osborne.

Basic Data Analysis. Stephen Turnbull Business Administration and Public Policy Lecture 4: May 2, Abstract

Basic Data Analysis Stephen Turnbull Business Administration and Public Policy Lecture 4: May 2, 2013 Abstract Introduct the normal distribution. Introduce basic notions of uncertainty, probability, events,

Basic Data Analysis Stephen Turnbull Business Administration and Public Policy Lecture 4: May 2, 2013 Abstract Introduct the normal distribution. Introduce basic notions of uncertainty, probability, events,

On the provision of incentives in finance experiments. Web Appendix

On the provision of incentives in finance experiments. Daniel Kleinlercher Thomas Stöckl May 29, 2017 Contents Web Appendix 1 Calculation of price efficiency measures 2 2 Additional information for PRICE

On the provision of incentives in finance experiments. Daniel Kleinlercher Thomas Stöckl May 29, 2017 Contents Web Appendix 1 Calculation of price efficiency measures 2 2 Additional information for PRICE

Section 3.1 Distributions of Random Variables

Section 3.1 Distributions of Random Variables Random Variable A random variable is a rule that assigns a number to each outcome of a chance experiment. There are three types of random variables: 1. Finite

Section 3.1 Distributions of Random Variables Random Variable A random variable is a rule that assigns a number to each outcome of a chance experiment. There are three types of random variables: 1. Finite

Notes 10: Risk and Uncertainty

Economics 335 April 19, 1999 A. Introduction Notes 10: Risk and Uncertainty 1. Basic Types of Uncertainty in Agriculture a. production b. prices 2. Examples of Uncertainty in Agriculture a. crop yields

Economics 335 April 19, 1999 A. Introduction Notes 10: Risk and Uncertainty 1. Basic Types of Uncertainty in Agriculture a. production b. prices 2. Examples of Uncertainty in Agriculture a. crop yields

Chapter 19: Compensating and Equivalent Variations

Chapter 19: Compensating and Equivalent Variations 19.1: Introduction This chapter is interesting and important. It also helps to answer a question you may well have been asking ever since we studied quasi-linear

Chapter 19: Compensating and Equivalent Variations 19.1: Introduction This chapter is interesting and important. It also helps to answer a question you may well have been asking ever since we studied quasi-linear

Choice under risk and uncertainty

Choice under risk and uncertainty Introduction Up until now, we have thought of the objects that our decision makers are choosing as being physical items However, we can also think of cases where the outcomes

Choice under risk and uncertainty Introduction Up until now, we have thought of the objects that our decision makers are choosing as being physical items However, we can also think of cases where the outcomes

An experimental investigation of evolutionary dynamics in the Rock- Paper-Scissors game. Supplementary Information

An experimental investigation of evolutionary dynamics in the Rock- Paper-Scissors game Moshe Hoffman, Sigrid Suetens, Uri Gneezy, and Martin A. Nowak Supplementary Information 1 Methods and procedures

An experimental investigation of evolutionary dynamics in the Rock- Paper-Scissors game Moshe Hoffman, Sigrid Suetens, Uri Gneezy, and Martin A. Nowak Supplementary Information 1 Methods and procedures

Reduction of Compound Lotteries with. Objective Probabilities: Theory and Evidence

Reduction of Compound Lotteries with Objective Probabilities: Theory and Evidence by Glenn W. Harrison, Jimmy Martínez-Correa and J. Todd Swarthout March 2012 ABSTRACT. The reduction of compound lotteries

Reduction of Compound Lotteries with Objective Probabilities: Theory and Evidence by Glenn W. Harrison, Jimmy Martínez-Correa and J. Todd Swarthout March 2012 ABSTRACT. The reduction of compound lotteries

Supplementary Material for: Belief Updating in Sequential Games of Two-Sided Incomplete Information: An Experimental Study of a Crisis Bargaining

Supplementary Material for: Belief Updating in Sequential Games of Two-Sided Incomplete Information: An Experimental Study of a Crisis Bargaining Model September 30, 2010 1 Overview In these supplementary

Supplementary Material for: Belief Updating in Sequential Games of Two-Sided Incomplete Information: An Experimental Study of a Crisis Bargaining Model September 30, 2010 1 Overview In these supplementary

The following content is provided under a Creative Commons license. Your support

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

Investment Decisions and Negative Interest Rates

Investment Decisions and Negative Interest Rates No. 16-23 Anat Bracha Abstract: While the current European Central Bank deposit rate and 2-year German government bond yields are negative, the U.S. 2-year

Investment Decisions and Negative Interest Rates No. 16-23 Anat Bracha Abstract: While the current European Central Bank deposit rate and 2-year German government bond yields are negative, the U.S. 2-year

Section 8.1 Distributions of Random Variables

Section 8.1 Distributions of Random Variables Random Variable A random variable is a rule that assigns a number to each outcome of a chance experiment. There are three types of random variables: 1. Finite

Section 8.1 Distributions of Random Variables Random Variable A random variable is a rule that assigns a number to each outcome of a chance experiment. There are three types of random variables: 1. Finite

* Financial support was provided by the National Science Foundation (grant number

Risk Aversion as Attitude towards Probabilities: A Paradox James C. Cox a and Vjollca Sadiraj b a, b. Department of Economics and Experimental Economics Center, Georgia State University, 14 Marietta St.

Risk Aversion as Attitude towards Probabilities: A Paradox James C. Cox a and Vjollca Sadiraj b a, b. Department of Economics and Experimental Economics Center, Georgia State University, 14 Marietta St.

ANDREW YOUNG SCHOOL OF POLICY STUDIES

ANDREW YOUNG SCHOOL OF POLICY STUDIES On the Coefficient of Variation as a Criterion for Decision under Risk James C. Cox and Vjollca Sadiraj Experimental Economics Center, Andrew Young School of Policy

ANDREW YOUNG SCHOOL OF POLICY STUDIES On the Coefficient of Variation as a Criterion for Decision under Risk James C. Cox and Vjollca Sadiraj Experimental Economics Center, Andrew Young School of Policy

Lecture 11: Critiques of Expected Utility

Lecture 11: Critiques of Expected Utility Alexander Wolitzky MIT 14.121 1 Expected Utility and Its Discontents Expected utility (EU) is the workhorse model of choice under uncertainty. From very early

Lecture 11: Critiques of Expected Utility Alexander Wolitzky MIT 14.121 1 Expected Utility and Its Discontents Expected utility (EU) is the workhorse model of choice under uncertainty. From very early

Regret Lotteries: Short-Run Gains, Long-run Losses For Online Publication: Appendix B - Screenshots and Instructions

Regret Lotteries: Short-Run Gains, Long-run Losses For Online Publication: Appendix B - Screenshots and Instructions Alex Imas Diego Lamé Alistair J. Wilson February, 2017 Contents B1 Interface Screenshots.........................

Regret Lotteries: Short-Run Gains, Long-run Losses For Online Publication: Appendix B - Screenshots and Instructions Alex Imas Diego Lamé Alistair J. Wilson February, 2017 Contents B1 Interface Screenshots.........................

THE CODING OF OUTCOMES IN TAXPAYERS REPORTING DECISIONS. A. Schepanski The University of Iowa

THE CODING OF OUTCOMES IN TAXPAYERS REPORTING DECISIONS A. Schepanski The University of Iowa May 2001 The author thanks Teri Shearer and the participants of The University of Iowa Judgment and Decision-Making

THE CODING OF OUTCOMES IN TAXPAYERS REPORTING DECISIONS A. Schepanski The University of Iowa May 2001 The author thanks Teri Shearer and the participants of The University of Iowa Judgment and Decision-Making

Chapter 6: Supply and Demand with Income in the Form of Endowments

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

the display, exploration and transformation of the data are demonstrated and biases typically encountered are highlighted.

1 Insurance data Generalized linear modeling is a methodology for modeling relationships between variables. It generalizes the classical normal linear model, by relaxing some of its restrictive assumptions,

1 Insurance data Generalized linear modeling is a methodology for modeling relationships between variables. It generalizes the classical normal linear model, by relaxing some of its restrictive assumptions,

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Lecture 3: Prospect Theory, Framing, and Mental Accounting. Expected Utility Theory. The key features are as follows:

Topics Lecture 3: Prospect Theory, Framing, and Mental Accounting Expected Utility Theory Violations of EUT Prospect Theory Framing Mental Accounting Application of Prospect Theory, Framing, and Mental

Topics Lecture 3: Prospect Theory, Framing, and Mental Accounting Expected Utility Theory Violations of EUT Prospect Theory Framing Mental Accounting Application of Prospect Theory, Framing, and Mental

Behavioral Economics & the Design of Agricultural Index Insurance in Developing Countries

Behavioral Economics & the Design of Agricultural Index Insurance in Developing Countries Michael R Carter Department of Agricultural & Resource Economics BASIS Assets & Market Access Research Program

Behavioral Economics & the Design of Agricultural Index Insurance in Developing Countries Michael R Carter Department of Agricultural & Resource Economics BASIS Assets & Market Access Research Program

8/28/2017. ECON4260 Behavioral Economics. 2 nd lecture. Expected utility. What is a lottery?

ECON4260 Behavioral Economics 2 nd lecture Cumulative Prospect Theory Expected utility This is a theory for ranking lotteries Can be seen as normative: This is how I wish my preferences looked like Or

ECON4260 Behavioral Economics 2 nd lecture Cumulative Prospect Theory Expected utility This is a theory for ranking lotteries Can be seen as normative: This is how I wish my preferences looked like Or

The Fallacy of Large Numbers

The Fallacy of Large umbers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: ovember 6, 2003 ABSTRACT Traditional mean-variance calculations tell us that the

The Fallacy of Large umbers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: ovember 6, 2003 ABSTRACT Traditional mean-variance calculations tell us that the

Solution Guide to Exercises for Chapter 4 Decision making under uncertainty

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

CHAPTER 13. Duration of Spell (in months) Exit Rate

Exit Rate") CHAPTER 13 13-1. Suppose there are 25,000 unemployed persons in the economy. You are given the following data about the length of unemployment spells: Duration of Spell (in months) Exit Rate 1 0.60 2 0.20

CHAPTER 13 13-1. Suppose there are 25,000 unemployed persons in the economy. You are given the following data about the length of unemployment spells: Duration of Spell (in months) Exit Rate 1 0.60 2 0.20

TECHNIQUES FOR DECISION MAKING IN RISKY CONDITIONS

RISK AND UNCERTAINTY THREE ALTERNATIVE STATES OF INFORMATION CERTAINTY - where the decision maker is perfectly informed in advance about the outcome of their decisions. For each decision there is only

RISK AND UNCERTAINTY THREE ALTERNATIVE STATES OF INFORMATION CERTAINTY - where the decision maker is perfectly informed in advance about the outcome of their decisions. For each decision there is only

Experimental Payment Protocols and the Bipolar Behaviorist

Experimental Payment Protocols and the Bipolar Behaviorist by Glenn W. Harrison and J. Todd Swarthout March 2014 ABSTRACT. If someone claims that individuals behave as if they violate the independence

Experimental Payment Protocols and the Bipolar Behaviorist by Glenn W. Harrison and J. Todd Swarthout March 2014 ABSTRACT. If someone claims that individuals behave as if they violate the independence

Exploring the Scope of Neurometrically Informed Mechanism Design. Ian Krajbich 1,3,4 * Colin Camerer 1,2 Antonio Rangel 1,2

Exploring the Scope of Neurometrically Informed Mechanism Design Ian Krajbich 1,3,4 * Colin Camerer 1,2 Antonio Rangel 1,2 Appendix A: Instructions from the SLM experiment (Experiment 1) This experiment

Exploring the Scope of Neurometrically Informed Mechanism Design Ian Krajbich 1,3,4 * Colin Camerer 1,2 Antonio Rangel 1,2 Appendix A: Instructions from the SLM experiment (Experiment 1) This experiment

FIGURE A1.1. Differences for First Mover Cutoffs (Round one to two) as a Function of Beliefs on Others Cutoffs. Second Mover Round 1 Cutoff.

as a Function of Beliefs on Others Cutoffs. Second Mover Round 1 Cutoff.") APPENDIX A. SUPPLEMENTARY TABLES AND FIGURES A.1. Invariance to quantitative beliefs. Figure A1.1 shows the effect of the cutoffs in round one for the second and third mover on the best-response cutoffs

APPENDIX A. SUPPLEMENTARY TABLES AND FIGURES A.1. Invariance to quantitative beliefs. Figure A1.1 shows the effect of the cutoffs in round one for the second and third mover on the best-response cutoffs

Rational Choice and Moral Monotonicity. James C. Cox

Rational Choice and Moral Monotonicity James C. Cox Acknowledgement of Coauthors Today s lecture uses content from: J.C. Cox and V. Sadiraj (2010). A Theory of Dictators Revealed Preferences J.C. Cox,

Rational Choice and Moral Monotonicity James C. Cox Acknowledgement of Coauthors Today s lecture uses content from: J.C. Cox and V. Sadiraj (2010). A Theory of Dictators Revealed Preferences J.C. Cox,

Random Variables and Applications OPRE 6301

Random Variables and Applications OPRE 6301 Random Variables... As noted earlier, variability is omnipresent in the business world. To model variability probabilistically, we need the concept of a random

Random Variables and Applications OPRE 6301 Random Variables... As noted earlier, variability is omnipresent in the business world. To model variability probabilistically, we need the concept of a random

Midterm #1 EconS 527 Wednesday, September 28th, 2016 ANSWER KEY

Midterm #1 EconS 527 Wednesday, September 28th, 2016 ANSWER KEY Instructions. Show all your work clearly and make sure you justify all your answers. 1. Question #1 [10 Points]. Discuss and provide examples

Midterm #1 EconS 527 Wednesday, September 28th, 2016 ANSWER KEY Instructions. Show all your work clearly and make sure you justify all your answers. 1. Question #1 [10 Points]. Discuss and provide examples

Getting started with WinBUGS

1 Getting started with WinBUGS James B. Elsner and Thomas H. Jagger Department of Geography, Florida State University Some material for this tutorial was taken from http://www.unt.edu/rss/class/rich/5840/session1.doc

1 Getting started with WinBUGS James B. Elsner and Thomas H. Jagger Department of Geography, Florida State University Some material for this tutorial was taken from http://www.unt.edu/rss/class/rich/5840/session1.doc

Essential Question: What is a probability distribution for a discrete random variable, and how can it be displayed?

COMMON CORE N 3 Locker LESSON Distributions Common Core Math Standards The student is expected to: COMMON CORE S-IC.A. Decide if a specified model is consistent with results from a given data-generating

COMMON CORE N 3 Locker LESSON Distributions Common Core Math Standards The student is expected to: COMMON CORE S-IC.A. Decide if a specified model is consistent with results from a given data-generating

Portfolio Management

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

Thank you very much for your participation. This survey will take you about 15 minutes to complete.

This appendix provides sample surveys used in the experiments. Our study implements the experiment through Qualtrics, and we use the Qualtrics functionality to randomize participants to different treatment

This appendix provides sample surveys used in the experiments. Our study implements the experiment through Qualtrics, and we use the Qualtrics functionality to randomize participants to different treatment

This assignment is due on Tuesday, September 15, at the beginning of class (or sooner).

.") Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

A.REPRESENTATION OF DATA

A.REPRESENTATION OF DATA (a) GRAPHS : PART I Q: Why do we need a graph paper? Ans: You need graph paper to draw: (i) Histogram (ii) Cumulative Frequency Curve (iii) Frequency Polygon (iv) Box-and-Whisker

A.REPRESENTATION OF DATA (a) GRAPHS : PART I Q: Why do we need a graph paper? Ans: You need graph paper to draw: (i) Histogram (ii) Cumulative Frequency Curve (iii) Frequency Polygon (iv) Box-and-Whisker

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Expected Value of a Random Variable

Knowledge Article: Probability and Statistics Expected Value of a Random Variable Expected Value of a Discrete Random Variable You're familiar with a simple mean, or average, of a set. The mean value of

Knowledge Article: Probability and Statistics Expected Value of a Random Variable Expected Value of a Discrete Random Variable You're familiar with a simple mean, or average, of a set. The mean value of

Chapter 23: Choice under Risk

Chapter 23: Choice under Risk 23.1: Introduction We consider in this chapter optimal behaviour in conditions of risk. By this we mean that, when the individual takes a decision, he or she does not know

Chapter 23: Choice under Risk 23.1: Introduction We consider in this chapter optimal behaviour in conditions of risk. By this we mean that, when the individual takes a decision, he or she does not know

Problem 1 / 25 Problem 2 / 25 Problem 3 / 25 Problem 4 / 25

Department of Economics Boston College Economics 202 (Section 05) Macroeconomic Theory Midterm Exam Suggested Solutions Professor Sanjay Chugh Fall 203 NAME: The Exam has a total of four (4) problems and

Department of Economics Boston College Economics 202 (Section 05) Macroeconomic Theory Midterm Exam Suggested Solutions Professor Sanjay Chugh Fall 203 NAME: The Exam has a total of four (4) problems and

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

The Fallacy of Large Numbers and A Defense of Diversified Active Managers

The Fallacy of Large umbers and A Defense of Diversified Active Managers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: March 27, 2003 ABSTRACT Traditional

The Fallacy of Large umbers and A Defense of Diversified Active Managers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: March 27, 2003 ABSTRACT Traditional

On the Empirical Relevance of St. Petersburg Lotteries. James C. Cox, Vjollca Sadiraj, and Bodo Vogt

On the Empirical Relevance of St. Petersburg Lotteries James C. Cox, Vjollca Sadiraj, and Bodo Vogt Experimental Economics Center Working Paper 2008-05 Georgia State University On the Empirical Relevance

On the Empirical Relevance of St. Petersburg Lotteries James C. Cox, Vjollca Sadiraj, and Bodo Vogt Experimental Economics Center Working Paper 2008-05 Georgia State University On the Empirical Relevance

Traditional Optimization is Not Optimal for Leverage-Averse Investors

Posted SSRN 10/1/2013 Traditional Optimization is Not Optimal for Leverage-Averse Investors Bruce I. Jacobs and Kenneth N. Levy forthcoming The Journal of Portfolio Management, Winter 2014 Bruce I. Jacobs

Posted SSRN 10/1/2013 Traditional Optimization is Not Optimal for Leverage-Averse Investors Bruce I. Jacobs and Kenneth N. Levy forthcoming The Journal of Portfolio Management, Winter 2014 Bruce I. Jacobs

Lecture Slides. Elementary Statistics Tenth Edition. by Mario F. Triola. and the Triola Statistics Series. Slide 1

Lecture Slides Elementary Statistics Tenth Edition and the Triola Statistics Series by Mario F. Triola Slide 1 Chapter 6 Normal Probability Distributions 6-1 Overview 6-2 The Standard Normal Distribution

Lecture Slides Elementary Statistics Tenth Edition and the Triola Statistics Series by Mario F. Triola Slide 1 Chapter 6 Normal Probability Distributions 6-1 Overview 6-2 The Standard Normal Distribution

Working Paper #1. Optimizing New York s Reforming the Energy Vision

Center for Energy, Economic & Environmental Policy Rutgers, The State University of New Jersey 33 Livingston Avenue, First Floor New Brunswick, NJ 08901 http://ceeep.rutgers.edu/ 732-789-2750 Fax: 732-932-0394

Center for Energy, Economic & Environmental Policy Rutgers, The State University of New Jersey 33 Livingston Avenue, First Floor New Brunswick, NJ 08901 http://ceeep.rutgers.edu/ 732-789-2750 Fax: 732-932-0394

Choice Under Uncertainty

Choice Under Uncertainty Lotteries Without uncertainty, there is no need to distinguish between a consumer s choice between alternatives and the resulting outcome. A consumption bundle is the choice and

Choice Under Uncertainty Lotteries Without uncertainty, there is no need to distinguish between a consumer s choice between alternatives and the resulting outcome. A consumption bundle is the choice and

[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright

![[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright](/thumbs/92/107898301.jpg "[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright") Faculty and Institute of Actuaries Claims Reserving Manual v.2 (09/1997) Section D7 [D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright 1. Introduction

Faculty and Institute of Actuaries Claims Reserving Manual v.2 (09/1997) Section D7 [D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright 1. Introduction

ECON 2100 Principles of Microeconomics (Fall 2018) Consumer Choice Theory

Consumer Choice Theory") ECON 21 Principles of Microeconomics (Fall 218) Consumer Choice Theory Relevant readings from the textbook: Mankiw, Ch 21 The Theory of Consumer Choice Suggested problems from the textbook: Chapter 21

ECON 21 Principles of Microeconomics (Fall 218) Consumer Choice Theory Relevant readings from the textbook: Mankiw, Ch 21 The Theory of Consumer Choice Suggested problems from the textbook: Chapter 21

CS 361: Probability & Statistics

March 12, 2018 CS 361: Probability & Statistics Inference Binomial likelihood: Example Suppose we have a coin with an unknown probability of heads. We flip the coin 10 times and observe 2 heads. What can

March 12, 2018 CS 361: Probability & Statistics Inference Binomial likelihood: Example Suppose we have a coin with an unknown probability of heads. We flip the coin 10 times and observe 2 heads. What can

Paradoxes and Mechanisms for Choice under Risk. by James C. Cox, Vjollca Sadiraj, and Ulrich Schmidt

Paradoxes and Mechanisms for Choice under Risk by James C. Cox, Vjollca Sadiraj, and Ulrich Schmidt No. 1712 June 2011 Kiel Institute for the World Economy, Hindenburgufer 66, 24105 Kiel, Germany Kiel

Paradoxes and Mechanisms for Choice under Risk by James C. Cox, Vjollca Sadiraj, and Ulrich Schmidt No. 1712 June 2011 Kiel Institute for the World Economy, Hindenburgufer 66, 24105 Kiel, Germany Kiel

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Risk Aversion in Laboratory Asset Markets

Risk Aversion in Laboratory Asset Markets Peter Bossaerts California Institute of Technology Centre for Economic Policy Research William R. Zame UCLA California Institute of Technology March 15, 2005 Financial

Risk Aversion in Laboratory Asset Markets Peter Bossaerts California Institute of Technology Centre for Economic Policy Research William R. Zame UCLA California Institute of Technology March 15, 2005 Financial

Key concepts: Certainty Equivalent and Risk Premium

Certainty equivalents Risk premiums 19 Key concepts: Certainty Equivalent and Risk Premium Which is the amount of money that is equivalent in your mind to a given situation that involves uncertainty? Ex:

Certainty equivalents Risk premiums 19 Key concepts: Certainty Equivalent and Risk Premium Which is the amount of money that is equivalent in your mind to a given situation that involves uncertainty? Ex:

Visualizing 360 Data Points in a Single Display. Stephen Few

Visualizing 360 Data Points in a Single Display Stephen Few This paper explores ways to visualize a dataset that Jorge Camoes posted on the Perceptual Edge Discussion Forum. Jorge s initial visualization

Visualizing 360 Data Points in a Single Display Stephen Few This paper explores ways to visualize a dataset that Jorge Camoes posted on the Perceptual Edge Discussion Forum. Jorge s initial visualization

ECON 214 Elements of Statistics for Economists

ECON 214 Elements of Statistics for Economists Session 7 The Normal Distribution Part 1 Lecturer: Dr. Bernardin Senadza, Dept. of Economics Contact Information: bsenadza@ug.edu.gh College of Education

ECON 214 Elements of Statistics for Economists Session 7 The Normal Distribution Part 1 Lecturer: Dr. Bernardin Senadza, Dept. of Economics Contact Information: bsenadza@ug.edu.gh College of Education

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997 CORPORATE MANAGERS RISKY BEHAVIOR: RISK TAKING OR AVOIDING?

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997 CORPORATE MANAGERS RISKY BEHAVIOR: RISK TAKING OR AVOIDING? Kathryn Sullivan* Abstract This study reports on five experiments that

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997 CORPORATE MANAGERS RISKY BEHAVIOR: RISK TAKING OR AVOIDING? Kathryn Sullivan* Abstract This study reports on five experiments that

Learning Goals: * Determining the expected value from a probability distribution. * Applying the expected value formula to solve problems.

Learning Goals: * Determining the expected value from a probability distribution. * Applying the expected value formula to solve problems. The following are marks from assignments and tests in a math class.

Learning Goals: * Determining the expected value from a probability distribution. * Applying the expected value formula to solve problems. The following are marks from assignments and tests in a math class.

Ideal Bootstrapping and Exact Recombination: Applications to Auction Experiments

Ideal Bootstrapping and Exact Recombination: Applications to Auction Experiments Carl T. Bergstrom University of Washington, Seattle, WA Theodore C. Bergstrom University of California, Santa Barbara Rodney

Ideal Bootstrapping and Exact Recombination: Applications to Auction Experiments Carl T. Bergstrom University of Washington, Seattle, WA Theodore C. Bergstrom University of California, Santa Barbara Rodney

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati.

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati. Module No. # 06 Illustrations of Extensive Games and Nash Equilibrium

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati. Module No. # 06 Illustrations of Extensive Games and Nash Equilibrium

Chapter 3. Consumer Behavior

Chapter 3 Consumer Behavior Question: Mary goes to the movies eight times a month and seldom goes to a bar. Tom goes to the movies once a month and goes to a bar fifteen times a month. What determine consumers

Chapter 3 Consumer Behavior Question: Mary goes to the movies eight times a month and seldom goes to a bar. Tom goes to the movies once a month and goes to a bar fifteen times a month. What determine consumers

Consumer Choice and Demand

Consumer Choice and Demand CHAPTER12 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Calculate and graph a budget line that shows the limits to

Consumer Choice and Demand CHAPTER12 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Calculate and graph a budget line that shows the limits to

The mathematical definitions are given on screen.

Text Lecture 3.3 Coherent measures of risk and back- testing Dear all, welcome back. In this class we will discuss one of the main drawbacks of Value- at- Risk, that is to say the fact that the VaR, as

Text Lecture 3.3 Coherent measures of risk and back- testing Dear all, welcome back. In this class we will discuss one of the main drawbacks of Value- at- Risk, that is to say the fact that the VaR, as

S = 1,2,3, 4,5,6 occurs

Chapter 5 Discrete Probability Distributions The observations generated by different statistical experiments have the same general type of behavior. Discrete random variables associated with these experiments

Chapter 5 Discrete Probability Distributions The observations generated by different statistical experiments have the same general type of behavior. Discrete random variables associated with these experiments

Yao s Minimax Principle

Complexity of algorithms The complexity of an algorithm is usually measured with respect to the size of the input, where size may for example refer to the length of a binary word describing the input,

Complexity of algorithms The complexity of an algorithm is usually measured with respect to the size of the input, where size may for example refer to the length of a binary word describing the input,

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Ambiguity Aversion. Mark Dean. Lecture Notes for Spring 2015 Behavioral Economics - Brown University

Ambiguity Aversion Mark Dean Lecture Notes for Spring 2015 Behavioral Economics - Brown University 1 Subjective Expected Utility So far, we have been considering the roulette wheel world of objective probabilities:

Ambiguity Aversion Mark Dean Lecture Notes for Spring 2015 Behavioral Economics - Brown University 1 Subjective Expected Utility So far, we have been considering the roulette wheel world of objective probabilities:

Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October Wilbert van der Klaauw

Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October 16 2014 Wilbert van der Klaauw The views presented here are those of the author and do not necessarily reflect those

Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October 16 2014 Wilbert van der Klaauw The views presented here are those of the author and do not necessarily reflect those

Statistics 431 Spring 2007 P. Shaman. Preliminaries

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

PROBABILITY DISTRIBUTIONS

CHAPTER 3 PROBABILITY DISTRIBUTIONS Page Contents 3.1 Introduction to Probability Distributions 51 3.2 The Normal Distribution 56 3.3 The Binomial Distribution 60 3.4 The Poisson Distribution 64 Exercise

CHAPTER 3 PROBABILITY DISTRIBUTIONS Page Contents 3.1 Introduction to Probability Distributions 51 3.2 The Normal Distribution 56 3.3 The Binomial Distribution 60 3.4 The Poisson Distribution 64 Exercise

Supplementary Material: Strategies for exploration in the domain of losses

1 Supplementary Material: Strategies for exploration in the domain of losses Paul M. Krueger 1,, Robert C. Wilson 2,, and Jonathan D. Cohen 3,4 1 Department of Psychology, University of California, Berkeley

1 Supplementary Material: Strategies for exploration in the domain of losses Paul M. Krueger 1,, Robert C. Wilson 2,, and Jonathan D. Cohen 3,4 1 Department of Psychology, University of California, Berkeley

Speculative Trade under Ambiguity

Speculative Trade under Ambiguity Jan Werner March 2014. Abstract: Ambiguous beliefs may lead to speculative trade and speculative bubbles. We demonstrate this by showing that the classical Harrison and

Speculative Trade under Ambiguity Jan Werner March 2014. Abstract: Ambiguous beliefs may lead to speculative trade and speculative bubbles. We demonstrate this by showing that the classical Harrison and

Equivalence Tests for the Difference of Two Proportions in a Cluster- Randomized Design

Chapter 240 Equivalence Tests for the Difference of Two Proportions in a Cluster- Randomized Design Introduction This module provides power analysis and sample size calculation for equivalence tests of

Chapter 240 Equivalence Tests for the Difference of Two Proportions in a Cluster- Randomized Design Introduction This module provides power analysis and sample size calculation for equivalence tests of

Comparing Allocations under Asymmetric Information: Coase Theorem Revisited

Comparing Allocations under Asymmetric Information: Coase Theorem Revisited Shingo Ishiguro Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka 560-0043, Japan August 2002

Comparing Allocations under Asymmetric Information: Coase Theorem Revisited Shingo Ishiguro Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka 560-0043, Japan August 2002

Spike Statistics: A Tutorial

Spike Statistics: A Tutorial File: spike statistics4.tex JV Stone, Psychology Department, Sheffield University, England. Email: j.v.stone@sheffield.ac.uk December 10, 2007 1 Introduction Why do we need

Spike Statistics: A Tutorial File: spike statistics4.tex JV Stone, Psychology Department, Sheffield University, England. Email: j.v.stone@sheffield.ac.uk December 10, 2007 1 Introduction Why do we need