Outline. Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion

|

|

|

- Noreen Warner

- 6 years ago

- Views:

Transcription

1 Uncertainty

2 Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion 2

3 Simple Lotteries 3

4 Simple Lotteries Advanced Microeconomic Theory 4

5 Simple Lotteries A simple lottery with 2 possible outcomes Degenerated probability pairs at (0,1), outcome 2 happens with certainty. at (1,0), outcome 1 happens with certainty. Strictly positive probability pairs Individual faces some uncertainty, i.e., p 1 + p 2 = 1 p 2 1 p 2 (0,1) p 1 2 { p R : p1 p2 1} (1,0) 1 p 1 Advanced Microeconomic Theory 5

6 Simple Lotteries A simple lottery with 3 possible outcomes (i.e., 3-dim. simplex). Intercepts represent degenerated probabilities where one outcome is certain. Points strictly inside the hyperplane connecting the three intercepts denote a lottery where the individual faces uncertainty. (1,0,0) p 1 1 p 3 1 p 3 p 2 p 1 (0,0,1) { p 0: p p p 1} (0,1,0) 1 p 2 Advanced Microeconomic Theory 6

7 Simple Lotteries 2-dim. projection of the 3-dim. simplex Vertices represent the intercepts The distance from a given point to the side of the triangle measures the probability that the outcome represented at the opposite vertex occurs. 3 x 2 x 1 x L ( p, p, p ) where x1 x2 x3 1 Advanced Microeconomic Theory 7

8 Simple Lotteries A lottery lies on one of the boundaries of the triangle: We can only construct segments connecting the lottery to two of the outcomes. The probability associated with the third outcome is zero. x 2 x 3 1 x x2 1 x 1 Advanced Microeconomic Theory 8

9 Compound Lotteries Given simple lotteries L k = p k 1, p k 2,, p k N for k = 1,2,, K and probabilities α k 0 with σk n=1 α k = 1, then the compound lottery L 1, L 2,, L K ; α 1, α 2,, α K is the risky alternative that yields the simple lottery L k with probability α k for k = 1,2,, K. Think about a compound lottery as a lottery of lotteries : first, I have probability α k of playing lottery 1, and if that happens, I have probability p k 1 of outcome 1 occurring. Then, the joint probability of outcome 1 is p 1 = α 1 p α 2 p 2 K α K p 1 Advanced Microeconomic Theory 9

10 Compound and Reduced Lotteries Given that interpretation, the following result should come at no surprise: For any compound lottery L 1, L 2,, L K ; α 1, α 2,, α K, we can calculate a corresponding reduced lottery as the simple lottery L = p 1, p 2,, p N that generates the same ultimate probability distribution of outcomes. The reduced lottery L of any compound lottery can be obtained by L = α 1 L 1 + α 2 L α K L K 10

11 Compound and Reduced Lotteries Example 1: All three lotteries are equally likely P outcome 1 = = 1 2 P outcome 2 = = 1 4 P outcome 3 = = / 3 2 1/ 3 3 1/ 3 L1 (1,0,0) L 2 L ,, ,, Reduced Lottery 1 1 1,,

1 1 1 1 1 1 L L1 L2 L3,, 3 3 3 2 4 4 2 12")

12 Compound and Reduced Lotteries 3 L L 2 3 x 2 1 L1 (1,0,0) L L1 L2 L3,,

13 x 1 Compound and Reduced Lotteries Example 2: Both lotteries are equally likely 1 1/ 2 2 1/ 2 Outcome 1 Outcome 2 L 4 1 1,, L5,0, Reduced Lottery Outcome ,,

14 Compound and Reduced Lotteries Example 2 (continued): probability simplex of the reduced lottery of a compound lottery L 5 1 1,0, (0, 0,1) L4 L5 L,, (1,0,0) L 4 1 1,,0 2 2 (0,1, 0) 14

15 Compound and Reduced Lotteries Consumer is indifferent between the two compound lotteries which induce the same reduced lottery This was illustrated in the previous examples where, despite facing different compound lotteries, the consumer obtained the same reduced lottery. We refer to this assumption as the Consequentialist hypothesis: Only consequences, and the probability associated to every consequence (outcome) matters, but not the route that we follow in order to obtain a give consequence. 15

16 Preferences over Lotteries 16

17 Preferences over Lotteries 17

18 Preferences over Lotteries Advanced Microeconomic Theory 18

19 Preferences over Lotteries The worst case scenario: First, attach a number v(z) to every outcome z C, v z R. Then L L, if and only if min v z : p z > 0 > min v z : p z > 0 The decision maker prefers lottery L if the lowest utility he can get from playing lottery L is higher than the lowest utility he can obtain from playing lottery L. Advanced Microeconomic Theory 19

20 Preferences over Lotteries 20

L L a BL ( ) L ' L b 1 2")

21 Preferences over Lotteries 3 BL ( ') L L a BL ( ) L ' L b

22 Preferences over Lotteries Example: 3 B(L ) 1 2 If L L, then L a L b. 22

23 Preferences over Lotteries 23

24 Preferences over Lotteries 24

25 Preferences over Lotteries L L if and only if αl + 1 α L αl + (1 α)l

26 Preferences over Lotteries Example 1 (intuition): The decision maker prefers lottery L to L, L L Construct a compound lottery by a coin toss play lottery L if heads comes up play lottery L if tails comes up By IA, if L L, then 1 2 L L 1 2 L L 26

27 Preferences over Lotteries 27

28 Preferences over Lotteries 28

29 Preferences over Lotteries Advanced Microeconomic Theory 29

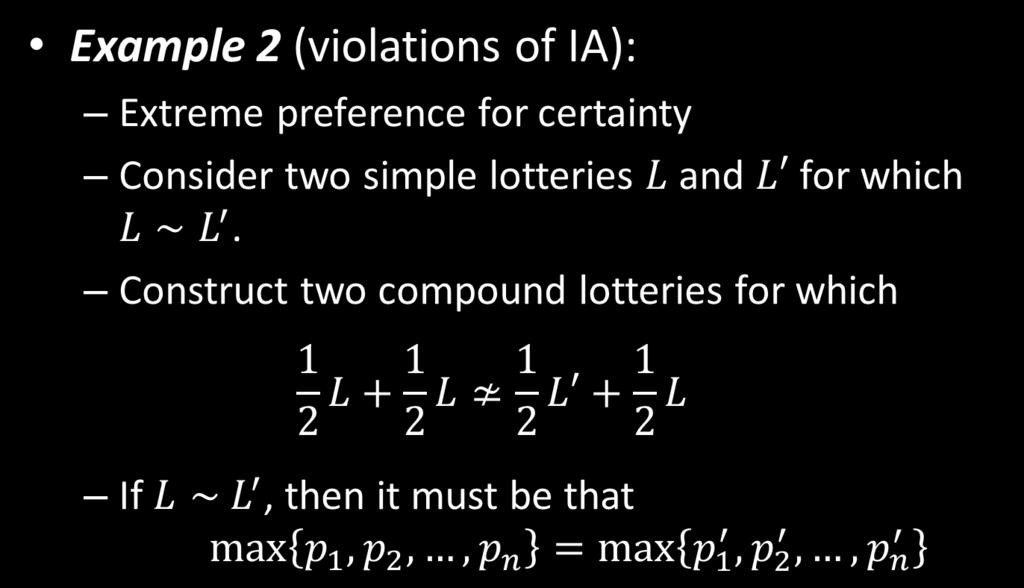

30 Preferences over Lotteries Example 3 (violations of IA, a numerical example): Therefore, max 0.4, 0.5, 0.1 = 0.5 > 0.45 = max 0.45, 0.25, 0.3 and thus L 1 2 L L. This violates the IA, which requires 1 2 L L 1 2 L L Advanced Microeconomic Theory 30

31 Preferences over Lotteries Example 4 (violations of IA, worst case scenario ): Consider L L. Then, the compound lottery 1 L + 1 L does not 2 2 need to be preferred to 1 L + 1 L. 2 2 Example: Consider the simple lotteries L = (1,3) and L = (10,0), with probabilities (p 1, p 2 ) and (p 1, p 2 ), respectively. This implies min v z : p z > 0 = 1 for lottery L min v z : p z > 0 = 0 for lottery L Hence, L L. 31

32 Preferences over Lotteries Example 4 (violations of IA, worst case scenario ): Example (continued): However, the compound lottery 1 L + 1 L is 11, 3, whose worst possible outcome is 3, which is preferred to 2 that of 1 L + 1 L, which is Hence, despite L L over simple lotteries, L = 1 2 L + 1 L 1 L + 1 L, which violates the IA Advanced Microeconomic Theory 32

33 Expected Utility Theory 33

34 Expected Utility Theory Hence, a utility function U: L R has the expected utility form if and only if it is linear in the probabilities, i.e., U K k=1 α k L k = K k=1 α k U(L k ) for any K lotteries L k L, k = 1,2,, K and probabilities α 1, α 2,, α K 0 and σk k=1 α k = 1. Intuition: the utility of the expected value of the K lotteries, U σk k=1 α k L k, coincides with the expected utility of the K lotteries, σk k=1 α k U(L k ). 34

35 Expected Utility Theory Note that the utility of the expected value of playing the K lotteries is U K k=1 α k L k = n u n k α k p n k where σ k α k p n k is the total joint probability of outcome n occurring. 35

36 Expected Utility Theory 36

37 Expected Utility Theory The EU property is a cardinal property: Not only rank matters, the particular number resulting form U: L R also matters. Hence, the EU form is preserved only under increasing linear transformations (a.k.a. affine transformations). Hence, the expected utility function U: L R is another vnm utility function if and only if U L = βu L + γ for every L L, where β > 0. 37

38 Expected Utility Theory: Representability 38

39 Expected Utility Theory: Indifference Curves 39

40 Expected Utility Theory: Indifference Curves 3 If L ~ L, then L ~ αl = + (1 α)l 1 2 Straight indifference curves 40

41 Expected Utility Theory: Indifference Curves 41

42 Expected Utility Theory: Indifference Curves 42

43 Expected Utility Theory: Indifference Curves 43

44 Expected Utility Theory: Indifference Curves Nonparallel indifference curves are incompatible with the IA L L 1 3 L L

45 Expected Utility Theory: Violations of the IA 1 st prize 2 nd prize 3 rd prize $2.5mln $500,000 $0 45

46 Expected Utility Theory: Violations of the IA 46

47 Expected Utility Theory: Violations of the IA 47

48 Expected Utility Theory: Violations of the IA 48

49 Expected Utility Theory: Violations of the IA 49

50 Expected Utility Theory: Violations of the IA 50

51 Expected Utility Theory: Violations of the IA 51

52 Expected Utility Theory: Violations of the IA Dutch books: In the above two anomalies, actual behavior is inconsistent with the IA. Can we then rely on the IA? What would happen to individuals whose behavior violates the IA? They would be weeded out of the market because they would be open to the acceptance of so-called Dutch books, leading them to a sure loss of money. 52

53 Expected Utility Theory: Violations of the IA 53

54 Expected Utility Theory: Violations of the IA 54

55 Expected Utility Theory: Violations of the IA Further reading: Developments in non-expected utility theory: The hunt for a descriptive theory of choice under risk (2000) by Chris Starmer, Journal of Economic Literature, vol. 38(2) Choices, Values and Frames (2000) by Nobel prize winners Daniel Kahneman and Amos Tversky, Cambridge University Press. Theory of Decision under Uncertainty (2009) by Itzhak Gilboa, Cambridge University Press. Advanced Microeconomic Theory 55

56 Money Lotteries We now restrict our attention to lotteries over monetary amounts, i.e., C = R. Money is continuous variable, x R, with cumulative distribution function (CDF) F x = Prob y x for all y R 56

57 Money Lotteries A uniform, continuous CDF, F x = x Same probability weight to every possible payoff F(.) 1 1/2 F(x)=x Uniform Distribution 45 o 1/2 1 x 57

58 Money Lotteries A non-uniform, continuous CDF, F x F(.) 1 1/2 1/2 1 x 58

59 Money Lotteries A non-uniform, discrete CDF F x = if x < 1 if x [1, 4) if x [4, 6) 1 if x 6 F(.) 1 3/4 1/2 1/ x 59

60 Money Lotteries If f x is a density function associated with the continuous CDF F x, then F x = න x f t dt f(.) x 60

61 Money Lotteries If f x is a density function associated with the discrete CDF F x, then f(.) F x = t<x f t 1/2 1/ x 61

62 Money Lotteries We can represent simple lotteries by F x. For compound lotteries: If the list of CDF s F 1 x, F 2 x,..., F K x represent K simple lotteries, each occurring with probability α 1, α 2,, α K, then the compound lottery can be represented as F K x x = K k=1 α k F k For simplicity, assume that CDF s are distributed over non-negative amounts of money. x 62

63 Money Lotteries We can express EU as EU F = u x f x dx or u x df(x) where u x is an assignment of utility value to every non-negative amount of money. If there is a density function f x associated with the CDF F(x), then we can use either of the expressions. If there is no, we can only use the latter. Note: we do not need to write down the limits of integration, since the integral is over the full range of possible realizations of x. 63

64 Money Lotteries EU F is the mathematical expectation of the values of u x, over all possible values of x. EU F is linear in the probabilities In the discrete probability distribution, EU F = p 1 u 1 + p 2 u 2 + The EU representation is sensitive not only to the mean of the distribution, but also to the variance, and higher order moments of the distribution of monetary payoffs. Let us next analyze this property. 64

65 Money Lotteries Example: Let us show that if u x = βx 2 + γx, then EU is determined by the mean and the variance alone. Indeed, EU x = න u x df x = න βx 2 + γx df x = β න x 2 df x + γ න x df x E x 2 E x On the other hand, we know that Var x = E x 2 E x 2 E x 2 = Var x + E x 2 65

66 Money Lotteries Example (continued): Substituting E x 2 in EU x, EU x = βvar x + β E x 2 βe x 2 + γe x Hence, the EU is determined by the mean and the variance alone. 66

67 Money Lotteries Recall that we refer to u x utility function, while EU x function. as the Bernoulli is the vnm We imposed few assumptions on u x : Increasing in money and continuous We must impose an additional assumption: u x is bounded Otherwise, we can end up in relatively absurd situations (St. Petersburg-Menger paradox). 67

68 Measuring Risk Preferences An individual exhibits risk aversion if න u x df x u න xdf x for any lottery F( ) Intuition: the utility of receiving the expected monetary value of playing the lottery is higher than the expected utility from playing the lottery. If this relationship happens with a) =, we denote this individual as risk neutral b) <, we denote him as strictly risk averter c), we denote him as risk lover. 68

69 Measuring Risk Preferences 69

70 Measuring Risk Preferences Risk averse individual Utility from the expected value of the lottery, u(2), is higher than the expected utility from playing the lottery, 1 2 u u(3). u(.) u(3) u(2) 1 1 u(1) u(3) 2 2 u(x) u(1) x 70

71 Measuring Risk Preferences Risk neutral individual Utility from the expected value of the lottery, u(2), coincides with the expected utility of playing the lottery, 1 2 u u(3). u(.) u(.) u(3) 1 1 u(1) u(3) u(2) 2 2 u(1) x 71

u(x) u(3) 1 1 u(1) u(3) 2 2 u(2) u(1)")

72 Measuring Risk Preferences u(.) u(x) u(3) 1 1 u(1) u(3) 2 2 u(2) u(1) x 72

73 Measuring Risk Preferences 73

74 Measuring Risk Preferences Certainty equivalent for a risk-averse individual

75 Measuring Risk Preferences Certainty equivalent for a risk lover 75

76 Measuring Risk Preferences Certainty equivalent for a risk neutral individual u(.) u(3) u(x) 1 1 u(1) u(3) u(2) 2 2 u(1) x c( F, u) 76

77 Measuring Risk Preferences 77

78 Measuring Risk Preferences 78

79 Measuring Risk Preferences 79

80 Measuring Risk Preferences 80

81 Measuring Risk Preferences 81

82 Measuring Risk Preferences 82

83 Measuring Risk Preferences Utility Increasing degree of risk aversion x 1/4 x 1/3 x 1/2 x Money, x 83

84 Measuring Risk Preferences 84

85 Measuring Risk Preferences 85

86 Measuring Risk Preferences 86

EU 1 EU 2 u 2 (.")

87 Measuring Risk Preferences u(.) u 1 (.) EU 1 EU 2 u 2 (.) 1 x 3 x c( F, u2) c( F, u1) 87

Advanced Microeconomic Theory. Chapter 5: Choices under Uncertainty

Advanced Microeconomic Theory Chapter 5: Choices under Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion Prospect Theory

Advanced Microeconomic Theory Chapter 5: Choices under Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion Prospect Theory

Rational theories of finance tell us how people should behave and often do not reflect reality.

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

MICROECONOMIC THEROY CONSUMER THEORY

LECTURE 5 MICROECONOMIC THEROY CONSUMER THEORY Choice under Uncertainty (MWG chapter 6, sections A-C, and Cowell chapter 8) Lecturer: Andreas Papandreou 1 Introduction p Contents n Expected utility theory

LECTURE 5 MICROECONOMIC THEROY CONSUMER THEORY Choice under Uncertainty (MWG chapter 6, sections A-C, and Cowell chapter 8) Lecturer: Andreas Papandreou 1 Introduction p Contents n Expected utility theory

Comparison of Payoff Distributions in Terms of Return and Risk

Comparison of Payoff Distributions in Terms of Return and Risk Preliminaries We treat, for convenience, money as a continuous variable when dealing with monetary outcomes. Strictly speaking, the derivation

Comparison of Payoff Distributions in Terms of Return and Risk Preliminaries We treat, for convenience, money as a continuous variable when dealing with monetary outcomes. Strictly speaking, the derivation

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

Micro Theory I Assignment #5 - Answer key

Micro Theory I Assignment #5 - Answer key 1. Exercises from MWG (Chapter 6): (a) Exercise 6.B.1 from MWG: Show that if the preferences % over L satisfy the independence axiom, then for all 2 (0; 1) and

Micro Theory I Assignment #5 - Answer key 1. Exercises from MWG (Chapter 6): (a) Exercise 6.B.1 from MWG: Show that if the preferences % over L satisfy the independence axiom, then for all 2 (0; 1) and

Financial Economics: Making Choices in Risky Situations

Financial Economics: Making Choices in Risky Situations Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 57 Questions to Answer How financial risk is defined and measured How an investor

Financial Economics: Making Choices in Risky Situations Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 57 Questions to Answer How financial risk is defined and measured How an investor

Choice under risk and uncertainty

Choice under risk and uncertainty Introduction Up until now, we have thought of the objects that our decision makers are choosing as being physical items However, we can also think of cases where the outcomes

Choice under risk and uncertainty Introduction Up until now, we have thought of the objects that our decision makers are choosing as being physical items However, we can also think of cases where the outcomes

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 3, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 3, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Risk aversion and choice under uncertainty

Risk aversion and choice under uncertainty Pierre Chaigneau pierre.chaigneau@hec.ca June 14, 2011 Finance: the economics of risk and uncertainty In financial markets, claims associated with random future

Risk aversion and choice under uncertainty Pierre Chaigneau pierre.chaigneau@hec.ca June 14, 2011 Finance: the economics of risk and uncertainty In financial markets, claims associated with random future

Choice Under Uncertainty

Chapter 6 Choice Under Uncertainty Up until now, we have been concerned with choice under certainty. A consumer chooses which commodity bundle to consume. A producer chooses how much output to produce

Chapter 6 Choice Under Uncertainty Up until now, we have been concerned with choice under certainty. A consumer chooses which commodity bundle to consume. A producer chooses how much output to produce

8/28/2017. ECON4260 Behavioral Economics. 2 nd lecture. Expected utility. What is a lottery?

ECON4260 Behavioral Economics 2 nd lecture Cumulative Prospect Theory Expected utility This is a theory for ranking lotteries Can be seen as normative: This is how I wish my preferences looked like Or

ECON4260 Behavioral Economics 2 nd lecture Cumulative Prospect Theory Expected utility This is a theory for ranking lotteries Can be seen as normative: This is how I wish my preferences looked like Or

Expected Utility and Risk Aversion

Expected Utility and Risk Aversion Expected utility and risk aversion 1/ 58 Introduction Expected utility is the standard framework for modeling investor choices. The following topics will be covered:

Expected Utility and Risk Aversion Expected utility and risk aversion 1/ 58 Introduction Expected utility is the standard framework for modeling investor choices. The following topics will be covered:

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty Prof. Massimo Guidolin Prep Course in Quant Methods for Finance August-September 2017 Outline and objectives Axioms of choice under

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty Prof. Massimo Guidolin Prep Course in Quant Methods for Finance August-September 2017 Outline and objectives Axioms of choice under

Summer 2003 (420 2)

") Microeconomics 3 Andreas Ortmann, Ph.D. Summer 2003 (420 2) 240 05 117 andreas.ortmann@cerge-ei.cz http://home.cerge-ei.cz/ortmann Week of May 12, lecture 3: Expected utility theory, continued: Risk aversion

Microeconomics 3 Andreas Ortmann, Ph.D. Summer 2003 (420 2) 240 05 117 andreas.ortmann@cerge-ei.cz http://home.cerge-ei.cz/ortmann Week of May 12, lecture 3: Expected utility theory, continued: Risk aversion

Choice under Uncertainty

Chapter 7 Choice under Uncertainty 1. Expected Utility Theory. 2. Risk Aversion. 3. Applications: demand for insurance, portfolio choice 4. Violations of Expected Utility Theory. 7.1 Expected Utility Theory

Chapter 7 Choice under Uncertainty 1. Expected Utility Theory. 2. Risk Aversion. 3. Applications: demand for insurance, portfolio choice 4. Violations of Expected Utility Theory. 7.1 Expected Utility Theory

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Session 9: The expected utility framework p. 1

Session 9: The expected utility framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 9: The expected utility framework p. 1 Questions How do humans make decisions

Session 9: The expected utility framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 9: The expected utility framework p. 1 Questions How do humans make decisions

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

ECON 581. Decision making under risk. Instructor: Dmytro Hryshko

ECON 581. Decision making under risk Instructor: Dmytro Hryshko 1 / 36 Outline Expected utility Risk aversion Certainty equivalence and risk premium The canonical portfolio allocation problem 2 / 36 Suggested

ECON 581. Decision making under risk Instructor: Dmytro Hryshko 1 / 36 Outline Expected utility Risk aversion Certainty equivalence and risk premium The canonical portfolio allocation problem 2 / 36 Suggested

Answers to chapter 3 review questions

Answers to chapter 3 review questions 3.1 Explain why the indifference curves in a probability triangle diagram are straight lines if preferences satisfy expected utility theory. The expected utility of

Answers to chapter 3 review questions 3.1 Explain why the indifference curves in a probability triangle diagram are straight lines if preferences satisfy expected utility theory. The expected utility of

Expected Utility And Risk Aversion

Expected Utility And Risk Aversion Econ 2100 Fall 2017 Lecture 12, October 4 Outline 1 Risk Aversion 2 Certainty Equivalent 3 Risk Premium 4 Relative Risk Aversion 5 Stochastic Dominance Notation From

Expected Utility And Risk Aversion Econ 2100 Fall 2017 Lecture 12, October 4 Outline 1 Risk Aversion 2 Certainty Equivalent 3 Risk Premium 4 Relative Risk Aversion 5 Stochastic Dominance Notation From

Microeconomic Theory III Spring 2009

MIT OpenCourseWare http://ocw.mit.edu 14.123 Microeconomic Theory III Spring 2009 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. MIT 14.123 (2009) by

MIT OpenCourseWare http://ocw.mit.edu 14.123 Microeconomic Theory III Spring 2009 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. MIT 14.123 (2009) by

Introduction to Economics I: Consumer Theory

Introduction to Economics I: Consumer Theory Leslie Reinhorn Durham University Business School October 2014 What is Economics? Typical De nitions: "Economics is the social science that deals with the production,

Introduction to Economics I: Consumer Theory Leslie Reinhorn Durham University Business School October 2014 What is Economics? Typical De nitions: "Economics is the social science that deals with the production,

Choice Under Uncertainty

Choice Under Uncertainty Lotteries Without uncertainty, there is no need to distinguish between a consumer s choice between alternatives and the resulting outcome. A consumption bundle is the choice and

Choice Under Uncertainty Lotteries Without uncertainty, there is no need to distinguish between a consumer s choice between alternatives and the resulting outcome. A consumption bundle is the choice and

EconS Micro Theory I Recitation #8b - Uncertainty II

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

On the Empirical Relevance of St. Petersburg Lotteries. James C. Cox, Vjollca Sadiraj, and Bodo Vogt

On the Empirical Relevance of St. Petersburg Lotteries James C. Cox, Vjollca Sadiraj, and Bodo Vogt Experimental Economics Center Working Paper 2008-05 Georgia State University On the Empirical Relevance

On the Empirical Relevance of St. Petersburg Lotteries James C. Cox, Vjollca Sadiraj, and Bodo Vogt Experimental Economics Center Working Paper 2008-05 Georgia State University On the Empirical Relevance

Ambiguity Aversion. Mark Dean. Lecture Notes for Spring 2015 Behavioral Economics - Brown University

Ambiguity Aversion Mark Dean Lecture Notes for Spring 2015 Behavioral Economics - Brown University 1 Subjective Expected Utility So far, we have been considering the roulette wheel world of objective probabilities:

Ambiguity Aversion Mark Dean Lecture Notes for Spring 2015 Behavioral Economics - Brown University 1 Subjective Expected Utility So far, we have been considering the roulette wheel world of objective probabilities:

Financial Economics. A Concise Introduction to Classical and Behavioral Finance Chapter 2. Thorsten Hens and Marc Oliver Rieger

Financial Economics A Concise Introduction to Classical and Behavioral Finance Chapter 2 Thorsten Hens and Marc Oliver Rieger Swiss Banking Institute, University of Zurich / BWL, University of Trier July

Financial Economics A Concise Introduction to Classical and Behavioral Finance Chapter 2 Thorsten Hens and Marc Oliver Rieger Swiss Banking Institute, University of Zurich / BWL, University of Trier July

Game Theory. Lecture Notes By Y. Narahari. Department of Computer Science and Automation Indian Institute of Science Bangalore, India October 2012

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India October 22 COOPERATIVE GAME THEORY Correlated Strategies and Correlated

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India October 22 COOPERATIVE GAME THEORY Correlated Strategies and Correlated

Utility and Choice Under Uncertainty

Introduction to Microeconomics Utility and Choice Under Uncertainty The Five Axioms of Choice Under Uncertainty We can use the axioms of preference to show how preferences can be mapped into measurable

Introduction to Microeconomics Utility and Choice Under Uncertainty The Five Axioms of Choice Under Uncertainty We can use the axioms of preference to show how preferences can be mapped into measurable

PAULI MURTO, ANDREY ZHUKOV

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

ANSWERS TO PRACTICE PROBLEMS oooooooooooooooo

University of California, Davis Department of Economics Giacomo Bonanno Economics 03: Economics of uncertainty and information TO PRACTICE PROBLEMS oooooooooooooooo PROBLEM # : The expected value of the

University of California, Davis Department of Economics Giacomo Bonanno Economics 03: Economics of uncertainty and information TO PRACTICE PROBLEMS oooooooooooooooo PROBLEM # : The expected value of the

3.1 The Marschak-Machina triangle and risk aversion

Chapter 3 Risk aversion 3.1 The Marschak-Machina triangle and risk aversion One of the earliest, and most useful, graphical tools used to analyse choice under uncertainty was a triangular graph that was

Chapter 3 Risk aversion 3.1 The Marschak-Machina triangle and risk aversion One of the earliest, and most useful, graphical tools used to analyse choice under uncertainty was a triangular graph that was

Decision Theory. Refail N. Kasimbeyli

Decision Theory Refail N. Kasimbeyli Chapter 3 3 Utility Theory 3.1 Single-attribute utility 3.2 Interpreting utility functions 3.3 Utility functions for non-monetary attributes 3.4 The axioms of utility

Decision Theory Refail N. Kasimbeyli Chapter 3 3 Utility Theory 3.1 Single-attribute utility 3.2 Interpreting utility functions 3.3 Utility functions for non-monetary attributes 3.4 The axioms of utility

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude Duan LI Department of Systems Engineering & Engineering Management The Chinese University of Hong Kong http://www.se.cuhk.edu.hk/

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude Duan LI Department of Systems Engineering & Engineering Management The Chinese University of Hong Kong http://www.se.cuhk.edu.hk/

Chapter 23: Choice under Risk

Chapter 23: Choice under Risk 23.1: Introduction We consider in this chapter optimal behaviour in conditions of risk. By this we mean that, when the individual takes a decision, he or she does not know

Chapter 23: Choice under Risk 23.1: Introduction We consider in this chapter optimal behaviour in conditions of risk. By this we mean that, when the individual takes a decision, he or she does not know

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

Uncertainty. Contingent consumption Subjective probability. Utility functions. BEE2017 Microeconomics

Uncertainty BEE217 Microeconomics Uncertainty: The share prices of Amazon and the difficulty of investment decisions Contingent consumption 1. What consumption or wealth will you get in each possible outcome

Uncertainty BEE217 Microeconomics Uncertainty: The share prices of Amazon and the difficulty of investment decisions Contingent consumption 1. What consumption or wealth will you get in each possible outcome

Comparative Risk Sensitivity with Reference-Dependent Preferences

The Journal of Risk and Uncertainty, 24:2; 131 142, 2002 2002 Kluwer Academic Publishers. Manufactured in The Netherlands. Comparative Risk Sensitivity with Reference-Dependent Preferences WILLIAM S. NEILSON

The Journal of Risk and Uncertainty, 24:2; 131 142, 2002 2002 Kluwer Academic Publishers. Manufactured in The Netherlands. Comparative Risk Sensitivity with Reference-Dependent Preferences WILLIAM S. NEILSON

We examine the impact of risk aversion on bidding behavior in first-price auctions.

Risk Aversion We examine the impact of risk aversion on bidding behavior in first-price auctions. Assume there is no entry fee or reserve. Note: Risk aversion does not affect bidding in SPA because there,

Risk Aversion We examine the impact of risk aversion on bidding behavior in first-price auctions. Assume there is no entry fee or reserve. Note: Risk aversion does not affect bidding in SPA because there,

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Making Hard Decision. ENCE 627 Decision Analysis for Engineering. Identify the decision situation and understand objectives. Identify alternatives

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

Part 4: Market Failure II - Asymmetric Information - Uncertainty

Part 4: Market Failure II - Asymmetric Information - Uncertainty Expected Utility, Risk Aversion, Risk Neutrality, Risk Pooling, Insurance July 2016 - Asymmetric Information - Uncertainty July 2016 1 /

Part 4: Market Failure II - Asymmetric Information - Uncertainty Expected Utility, Risk Aversion, Risk Neutrality, Risk Pooling, Insurance July 2016 - Asymmetric Information - Uncertainty July 2016 1 /

Effects of Wealth and Its Distribution on the Moral Hazard Problem

Effects of Wealth and Its Distribution on the Moral Hazard Problem Jin Yong Jung We analyze how the wealth of an agent and its distribution affect the profit of the principal by considering the simple

Effects of Wealth and Its Distribution on the Moral Hazard Problem Jin Yong Jung We analyze how the wealth of an agent and its distribution affect the profit of the principal by considering the simple

Incorporating Managerial Cash-Flow Estimates and Risk Aversion to Value Real Options Projects. The Fields Institute for Mathematical Sciences

Incorporating Managerial Cash-Flow Estimates and Risk Aversion to Value Real Options Projects The Fields Institute for Mathematical Sciences Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Yuri Lawryshyn

Incorporating Managerial Cash-Flow Estimates and Risk Aversion to Value Real Options Projects The Fields Institute for Mathematical Sciences Sebastian Jaimungal sebastian.jaimungal@utoronto.ca Yuri Lawryshyn

ECON Financial Economics

ECON 8 - Financial Economics Michael Bar August, 0 San Francisco State University, department of economics. ii Contents Decision Theory under Uncertainty. Introduction.....................................

ECON 8 - Financial Economics Michael Bar August, 0 San Francisco State University, department of economics. ii Contents Decision Theory under Uncertainty. Introduction.....................................

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Key concepts: Certainty Equivalent and Risk Premium

Certainty equivalents Risk premiums 19 Key concepts: Certainty Equivalent and Risk Premium Which is the amount of money that is equivalent in your mind to a given situation that involves uncertainty? Ex:

Certainty equivalents Risk premiums 19 Key concepts: Certainty Equivalent and Risk Premium Which is the amount of money that is equivalent in your mind to a given situation that involves uncertainty? Ex:

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Lecture 3: Utility-Based Portfolio Choice

Lecture 3: Utility-Based Portfolio Choice Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives Choice under uncertainty: dominance o Guidolin-Pedio, chapter 1, sec. 2 Choice under

Lecture 3: Utility-Based Portfolio Choice Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives Choice under uncertainty: dominance o Guidolin-Pedio, chapter 1, sec. 2 Choice under

Subjective Expected Utility Theory

Subjective Expected Utility Theory Mark Dean Behavioral Economics Spring 2017 Introduction In the first class we drew a distinction betweem Circumstances of Risk (roulette wheels) Circumstances of Uncertainty

Subjective Expected Utility Theory Mark Dean Behavioral Economics Spring 2017 Introduction In the first class we drew a distinction betweem Circumstances of Risk (roulette wheels) Circumstances of Uncertainty

16 MAKING SIMPLE DECISIONS

253 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action a will have possible outcome states Result(a)

253 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action a will have possible outcome states Result(a)

Problem set 5. Asset pricing. Markus Roth. Chair for Macroeconomics Johannes Gutenberg Universität Mainz. Juli 5, 2010

Problem set 5 Asset pricing Markus Roth Chair for Macroeconomics Johannes Gutenberg Universität Mainz Juli 5, 200 Markus Roth (Macroeconomics 2) Problem set 5 Juli 5, 200 / 40 Contents Problem 5 of problem

Problem set 5 Asset pricing Markus Roth Chair for Macroeconomics Johannes Gutenberg Universität Mainz Juli 5, 200 Markus Roth (Macroeconomics 2) Problem set 5 Juli 5, 200 / 40 Contents Problem 5 of problem

Concave utility functions

Meeting 9: Addendum Concave utility functions This functional form of the utility function characterizes a risk avoider. Why is it so? Consider the following bet (better numbers than those used at Meeting

Meeting 9: Addendum Concave utility functions This functional form of the utility function characterizes a risk avoider. Why is it so? Consider the following bet (better numbers than those used at Meeting

ANASH EQUILIBRIUM of a strategic game is an action profile in which every. Strategy Equilibrium

Draft chapter from An introduction to game theory by Martin J. Osborne. Version: 2002/7/23. Martin.Osborne@utoronto.ca http://www.economics.utoronto.ca/osborne Copyright 1995 2002 by Martin J. Osborne.

Draft chapter from An introduction to game theory by Martin J. Osborne. Version: 2002/7/23. Martin.Osborne@utoronto.ca http://www.economics.utoronto.ca/osborne Copyright 1995 2002 by Martin J. Osborne.

Chapter 7: Portfolio Theory

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Lecture 06 Single Attribute Utility Theory

Lecture 06 Single Attribute Utility Theory Jitesh H. Panchal ME 597: Decision Making for Engineering Systems Design Design Engineering Lab @ Purdue (DELP) School of Mechanical Engineering Purdue University,

Lecture 06 Single Attribute Utility Theory Jitesh H. Panchal ME 597: Decision Making for Engineering Systems Design Design Engineering Lab @ Purdue (DELP) School of Mechanical Engineering Purdue University,

PAPER NO.1 : MICROECONOMICS ANALYSIS MODULE NO.6 : INDIFFERENCE CURVES

Subject Paper No and Title Module No and Title Module Tag 1: Microeconomics Analysis 6: Indifference Curves BSE_P1_M6 PAPER NO.1 : MICRO ANALYSIS TABLE OF CONTENTS 1. Learning Outcomes 2. Introduction

Subject Paper No and Title Module No and Title Module Tag 1: Microeconomics Analysis 6: Indifference Curves BSE_P1_M6 PAPER NO.1 : MICRO ANALYSIS TABLE OF CONTENTS 1. Learning Outcomes 2. Introduction

Module 1: Decision Making Under Uncertainty

Module 1: Decision Making Under Uncertainty Information Economics (Ec 515) George Georgiadis Today, we will study settings in which decision makers face uncertain outcomes. Natural when dealing with asymmetric

Module 1: Decision Making Under Uncertainty Information Economics (Ec 515) George Georgiadis Today, we will study settings in which decision makers face uncertain outcomes. Natural when dealing with asymmetric

EC989 Behavioural Economics. Sketch solutions for Class 2

EC989 Behavioural Economics Sketch solutions for Class 2 Neel Ocean (adapted from solutions by Andis Sofianos) February 15, 2017 1 Prospect Theory 1. Illustrate the way individuals usually weight the probability

EC989 Behavioural Economics Sketch solutions for Class 2 Neel Ocean (adapted from solutions by Andis Sofianos) February 15, 2017 1 Prospect Theory 1. Illustrate the way individuals usually weight the probability

Microeconomic Theory III Spring 2009

MIT OpenCourseWare http://ocw.mit.edu 14.123 Microeconomic Theory III Spring 2009 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. MIT 14.123 (2009) by

MIT OpenCourseWare http://ocw.mit.edu 14.123 Microeconomic Theory III Spring 2009 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. MIT 14.123 (2009) by

* Financial support was provided by the National Science Foundation (grant number

Risk Aversion as Attitude towards Probabilities: A Paradox James C. Cox a and Vjollca Sadiraj b a, b. Department of Economics and Experimental Economics Center, Georgia State University, 14 Marietta St.

Risk Aversion as Attitude towards Probabilities: A Paradox James C. Cox a and Vjollca Sadiraj b a, b. Department of Economics and Experimental Economics Center, Georgia State University, 14 Marietta St.

Non-Monotonicity of the Tversky- Kahneman Probability-Weighting Function: A Cautionary Note

European Financial Management, Vol. 14, No. 3, 2008, 385 390 doi: 10.1111/j.1468-036X.2007.00439.x Non-Monotonicity of the Tversky- Kahneman Probability-Weighting Function: A Cautionary Note Jonathan Ingersoll

European Financial Management, Vol. 14, No. 3, 2008, 385 390 doi: 10.1111/j.1468-036X.2007.00439.x Non-Monotonicity of the Tversky- Kahneman Probability-Weighting Function: A Cautionary Note Jonathan Ingersoll

Prevention and risk perception : theory and experiments

Prevention and risk perception : theory and experiments Meglena Jeleva (EconomiX, University Paris Nanterre) Insurance, Actuarial Science, Data and Models June, 11-12, 2018 Meglena Jeleva Prevention and

Prevention and risk perception : theory and experiments Meglena Jeleva (EconomiX, University Paris Nanterre) Insurance, Actuarial Science, Data and Models June, 11-12, 2018 Meglena Jeleva Prevention and

BEEM109 Experimental Economics and Finance

University of Exeter Recap Last class we looked at the axioms of expected utility, which defined a rational agent as proposed by von Neumann and Morgenstern. We then proceeded to look at empirical evidence

University of Exeter Recap Last class we looked at the axioms of expected utility, which defined a rational agent as proposed by von Neumann and Morgenstern. We then proceeded to look at empirical evidence

Economic Risk and Decision Analysis for Oil and Gas Industry CE School of Engineering and Technology Asian Institute of Technology

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.9008 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.9008 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Advanced Microeconomic Theory

Advanced Microeconomic Theory Lecture Notes Sérgio O. Parreiras Fall, 2016 Outline Mathematical Toolbox Decision Theory Partial Equilibrium Search Intertemporal Consumption General Equilibrium Financial

Advanced Microeconomic Theory Lecture Notes Sérgio O. Parreiras Fall, 2016 Outline Mathematical Toolbox Decision Theory Partial Equilibrium Search Intertemporal Consumption General Equilibrium Financial

16 MAKING SIMPLE DECISIONS

247 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action A will have possible outcome states Result

247 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action A will have possible outcome states Result

Andreas Wagener University of Vienna. Abstract

Linear risk tolerance and mean variance preferences Andreas Wagener University of Vienna Abstract We translate the property of linear risk tolerance (hyperbolical Arrow Pratt index of risk aversion) from

Linear risk tolerance and mean variance preferences Andreas Wagener University of Vienna Abstract We translate the property of linear risk tolerance (hyperbolical Arrow Pratt index of risk aversion) from

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

Behavioral Finance Driven Investment Strategies

Behavioral Finance Driven Investment Strategies Prof. Dr. Rudi Zagst, Technical University of Munich joint work with L. Brummer, M. Escobar, A. Lichtenstern, M. Wahl 1 Behavioral Finance Driven Investment

Behavioral Finance Driven Investment Strategies Prof. Dr. Rudi Zagst, Technical University of Munich joint work with L. Brummer, M. Escobar, A. Lichtenstern, M. Wahl 1 Behavioral Finance Driven Investment

Expected utility theory; Expected Utility Theory; risk aversion and utility functions

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

Optimizing S-shaped utility and risk management

Optimizing S-shaped utility and risk management Ineffectiveness of VaR and ES constraints John Armstrong (KCL), Damiano Brigo (Imperial) Quant Summit March 2018 Are ES constraints effective against rogue

Optimizing S-shaped utility and risk management Ineffectiveness of VaR and ES constraints John Armstrong (KCL), Damiano Brigo (Imperial) Quant Summit March 2018 Are ES constraints effective against rogue

A Preference Foundation for Fehr and Schmidt s Model. of Inequity Aversion 1

A Preference Foundation for Fehr and Schmidt s Model of Inequity Aversion 1 Kirsten I.M. Rohde 2 January 12, 2009 1 The author would like to thank Itzhak Gilboa, Ingrid M.T. Rohde, Klaus M. Schmidt, and

A Preference Foundation for Fehr and Schmidt s Model of Inequity Aversion 1 Kirsten I.M. Rohde 2 January 12, 2009 1 The author would like to thank Itzhak Gilboa, Ingrid M.T. Rohde, Klaus M. Schmidt, and

Game Theory. Lecture Notes By Y. Narahari. Department of Computer Science and Automation Indian Institute of Science Bangalore, India July 2012

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India July 2012 The Revenue Equivalence Theorem Note: This is a only a draft

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India July 2012 The Revenue Equivalence Theorem Note: This is a only a draft

Chapter 4. Uncertainty

Chapter 4 Uncertainty So far, it has been assumed that consumers would know precisely what they were buying and getting. In real life, however, it is often the case that an action does not lead to a definite

Chapter 4 Uncertainty So far, it has been assumed that consumers would know precisely what they were buying and getting. In real life, however, it is often the case that an action does not lead to a definite

Intro to Economic analysis

Intro to Economic analysis Alberto Bisin - NYU 1 The Consumer Problem Consider an agent choosing her consumption of goods 1 and 2 for a given budget. This is the workhorse of microeconomic theory. (Notice

Intro to Economic analysis Alberto Bisin - NYU 1 The Consumer Problem Consider an agent choosing her consumption of goods 1 and 2 for a given budget. This is the workhorse of microeconomic theory. (Notice

Market Liquidity and Performance Monitoring The main idea The sequence of events: Technology and information

Market Liquidity and Performance Monitoring Holmstrom and Tirole (JPE, 1993) The main idea A firm would like to issue shares in the capital market because once these shares are publicly traded, speculators

Market Liquidity and Performance Monitoring Holmstrom and Tirole (JPE, 1993) The main idea A firm would like to issue shares in the capital market because once these shares are publicly traded, speculators

Building Consistent Risk Measures into Stochastic Optimization Models

Building Consistent Risk Measures into Stochastic Optimization Models John R. Birge The University of Chicago Graduate School of Business www.chicagogsb.edu/fac/john.birge JRBirge Fuqua School, Duke University

Building Consistent Risk Measures into Stochastic Optimization Models John R. Birge The University of Chicago Graduate School of Business www.chicagogsb.edu/fac/john.birge JRBirge Fuqua School, Duke University

1. Expected utility, risk aversion and stochastic dominance

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

Game Theory Lecture Notes

Game Theory Lecture Notes Sérgio O. Parreiras Economics Department, UNC at Chapel Hill Spring, 2015 Outline Road Map Decision Problems Static Games Nash Equilibrium Pareto Efficiency Constrained Optimization

Game Theory Lecture Notes Sérgio O. Parreiras Economics Department, UNC at Chapel Hill Spring, 2015 Outline Road Map Decision Problems Static Games Nash Equilibrium Pareto Efficiency Constrained Optimization

Copyright (C) 2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the

2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the") Copyright (C) 2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the open text license amendment to version 2 of the GNU General

Copyright (C) 2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the open text license amendment to version 2 of the GNU General

Advanced Risk Management

Winter 2014/2015 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 1: Introduction and Expected Utility Your Instructors for Part I: Prof. Dr. Andreas Richter Email:

Winter 2014/2015 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 1: Introduction and Expected Utility Your Instructors for Part I: Prof. Dr. Andreas Richter Email:

Problem Set 2. Theory of Banking - Academic Year Maria Bachelet March 2, 2017

Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmai.com March, 07 Exercise Consider an agency relationship in which the principal contracts the agent, whose effort

Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmai.com March, 07 Exercise Consider an agency relationship in which the principal contracts the agent, whose effort

April 28, Decision Analysis 2. Utility Theory The Value of Information

15.053 April 28, 2005 Decision Analysis 2 Utility Theory The Value of Information 1 Lotteries and Utility L1 $50,000 $ 0 Lottery 1: a 50% chance at $50,000 and a 50% chance of nothing. L2 $20,000 Lottery

15.053 April 28, 2005 Decision Analysis 2 Utility Theory The Value of Information 1 Lotteries and Utility L1 $50,000 $ 0 Lottery 1: a 50% chance at $50,000 and a 50% chance of nothing. L2 $20,000 Lottery

Insights from Behavioral Economics on Index Insurance

Insights from Behavioral Economics on Index Insurance Michael Carter Professor, Agricultural & Resource Economics University of California, Davis Director, BASIS Collaborative Research Support Program

Insights from Behavioral Economics on Index Insurance Michael Carter Professor, Agricultural & Resource Economics University of California, Davis Director, BASIS Collaborative Research Support Program

Chapter 6: Risky Securities and Utility Theory

Chapter 6: Risky Securities and Utility Theory Topics 1. Principle of Expected Return 2. St. Petersburg Paradox 3. Utility Theory 4. Principle of Expected Utility 5. The Certainty Equivalent 6. Utility

Chapter 6: Risky Securities and Utility Theory Topics 1. Principle of Expected Return 2. St. Petersburg Paradox 3. Utility Theory 4. Principle of Expected Utility 5. The Certainty Equivalent 6. Utility

TECHNIQUES FOR DECISION MAKING IN RISKY CONDITIONS

RISK AND UNCERTAINTY THREE ALTERNATIVE STATES OF INFORMATION CERTAINTY - where the decision maker is perfectly informed in advance about the outcome of their decisions. For each decision there is only

RISK AND UNCERTAINTY THREE ALTERNATIVE STATES OF INFORMATION CERTAINTY - where the decision maker is perfectly informed in advance about the outcome of their decisions. For each decision there is only

Math489/889 Stochastic Processes and Advanced Mathematical Finance Homework 5

Math489/889 Stochastic Processes and Advanced Mathematical Finance Homework 5 Steve Dunbar Due Fri, October 9, 7. Calculate the m.g.f. of the random variable with uniform distribution on [, ] and then

Math489/889 Stochastic Processes and Advanced Mathematical Finance Homework 5 Steve Dunbar Due Fri, October 9, 7. Calculate the m.g.f. of the random variable with uniform distribution on [, ] and then

Intertemporal Risk Attitude. Lecture 7. Kreps & Porteus Preference for Early or Late Resolution of Risk

Intertemporal Risk Attitude Lecture 7 Kreps & Porteus Preference for Early or Late Resolution of Risk is an intrinsic preference for the timing of risk resolution is a general characteristic of recursive

Intertemporal Risk Attitude Lecture 7 Kreps & Porteus Preference for Early or Late Resolution of Risk is an intrinsic preference for the timing of risk resolution is a general characteristic of recursive

Engineering Risk Benefit Analysis

Engineering Risk Benefit Analysis 1.155, 2.943, 3.577, 6.938, 10.816, 13.621, 16.862, 22.82, ESD.72, ESD.721 DA 4. Introduction to Utility George E. Apostolakis Massachusetts Institute of Technology Spring

Engineering Risk Benefit Analysis 1.155, 2.943, 3.577, 6.938, 10.816, 13.621, 16.862, 22.82, ESD.72, ESD.721 DA 4. Introduction to Utility George E. Apostolakis Massachusetts Institute of Technology Spring

Midterm #1 EconS 527 Wednesday, September 28th, 2016 ANSWER KEY

Midterm #1 EconS 527 Wednesday, September 28th, 2016 ANSWER KEY Instructions. Show all your work clearly and make sure you justify all your answers. 1. Question #1 [10 Points]. Discuss and provide examples

Midterm #1 EconS 527 Wednesday, September 28th, 2016 ANSWER KEY Instructions. Show all your work clearly and make sure you justify all your answers. 1. Question #1 [10 Points]. Discuss and provide examples

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2015

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2015 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2015 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Foundations of Financial Economics Choice under uncertainty

Foundations of Financial Economics Choice under uncertainty Paulo Brito 1 pbrito@iseg.ulisboa.pt University of Lisbon March 9, 2018 Topics covered Contingent goods Comparing contingent goods Decision under

Foundations of Financial Economics Choice under uncertainty Paulo Brito 1 pbrito@iseg.ulisboa.pt University of Lisbon March 9, 2018 Topics covered Contingent goods Comparing contingent goods Decision under

Information Processing and Limited Liability

Information Processing and Limited Liability Bartosz Maćkowiak European Central Bank and CEPR Mirko Wiederholt Northwestern University January 2012 Abstract Decision-makers often face limited liability

Information Processing and Limited Liability Bartosz Maćkowiak European Central Bank and CEPR Mirko Wiederholt Northwestern University January 2012 Abstract Decision-makers often face limited liability

Introduction. Two main characteristics: Editing Evaluation. The use of an editing phase Outcomes as difference respect to a reference point 2

Prospect theory 1 Introduction Kahneman and Tversky (1979) Kahneman and Tversky (1992) cumulative prospect theory It is classified as nonconventional theory It is perhaps the most well-known of alternative

Prospect theory 1 Introduction Kahneman and Tversky (1979) Kahneman and Tversky (1992) cumulative prospect theory It is classified as nonconventional theory It is perhaps the most well-known of alternative

This assignment is due on Tuesday, September 15, at the beginning of class (or sooner).

.") Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

UTILITY ANALYSIS HANDOUTS

UTILITY ANALYSIS HANDOUTS 1 2 UTILITY ANALYSIS Motivating Example: Your total net worth = $400K = W 0. You own a home worth $250K. Probability of a fire each yr = 0.001. Insurance cost = $1K. Question:

UTILITY ANALYSIS HANDOUTS 1 2 UTILITY ANALYSIS Motivating Example: Your total net worth = $400K = W 0. You own a home worth $250K. Probability of a fire each yr = 0.001. Insurance cost = $1K. Question: