Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October Wilbert van der Klaauw

|

|

|

- Amos Fields

- 5 years ago

- Views:

Transcription

1 Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October Wilbert van der Klaauw The views presented here are those of the author and do not necessarily reflect those of the Federal Reserve Bank of New York, or the Federal Reserve System

2 Outline Brief overview of financial literacy related research at the NYFed Study what consumers know content of individual information sets/knowledge Study how individuals form and update expectations -- how information is used Study how expectations, knowledge and education influence consumer decision making Inflation expectations and behavior: Do survey respondents act on their beliefs? (with Olivier Armantier, Wandi Bruine de Bruin, Giorgio Topa, Basit Zafar) 2

3 Two key components of this research Collection of new data on consumer expectations and behavior RAND s American Life Panel (ALP) Survey of Consumer Expectations (SCE) Started in June Fielded by the Demand Institute, a partnership between the Conference Board and Nielsen Overall goal: collect timely, high quality information on consumer expectations and decisions A nationally representative, monthly internet-based survey of a rotating panel of ~ 1,200 household heads. The use of field experiments to establish causal relationships 3

4 Financial literacy related research at NYFed Three main research themes: 1. Study what consumers know content of individual information sets/knowledge Measure numeracy, financial literacy and heterogeneity therein Identify holes in knowledge/awareness of financially relevant information (i) Student loan literacy: Widespread lack of understanding of the implications of student loan indebtedness Only 37% considers forgiveness of student debt delinquency in bankruptcy as extremely unlikely (18% somewhat unlikely) Only 27% aware of three actions the government can take if not repaying federal student loan 4

5 Findings on: What Consumers Know (continued) (ii) Misconceptions of College Benefits and Costs We find biased beliefs, with the average respondent underestimating the average wage premium, and over-estimating the average costs of a college education Higher accuracy among those with higher numeracy Misperceptions are larger for more disadvantaged groups, so information may help reduce gaps in college attendance This suggests a role for potential information campaigns to inform the public about population returns to a college education 5

6 Financial literacy related research at NYFed (cont) 2. Study how individuals form and update expectations how information is used Document differences by levels of financial literacy & numeracy New SCE provides monthly changes in a large range of expectations by low/high numeracy/financial literacy Analyze updating of expectations in response to new information while accounting for endogeneity of information acquisition (randomized price information experiment) (i) Inflation Expectations: Differences by financial literacy/numeracy During the next 12 months, do you think that prices in general will go up, or go down, or stay where they are now?. By about what percent do you expect prices to go [up/down] on the average? 6

7 Findings on: How Consumers Form/Update Expectations Find that demographic differences in reported inflation expectations are mostly explained by differences in financial literacy: Respondents with lower financial literacy scores report higher and more extreme inflation expectations Evidence of differences in expectation formation: They thought more about specific (salient) prices; covering expenses reported higher uncertainty about future inflation, estimates more volatile over time: can lead to upward bias if perceived 0% floor had lower confidence in their financial knowledge and shorter planning horizons 7

8 Financial literacy related research at NYFed (cont) 3. Study how expectations, knowledge and education influence consumer decision making Analyze whether and how individuals act on their expectations Investigate role of expectations as channel through which numeracy, financial literacy, knowledge affects consumer decisions and outcomes Randomized financially incentivized investment experiment: Do Survey Respondents Act on their Beliefs about Inflation? 8

9 Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? Background Inflation expectations are at the center of modern Macro Theory Transmission effect : Beliefs about future inflation affect current behavior and therefore realized inflation Managing inflation expectations is first step in controlling inflation Recent research aims at better understanding and survey measures of inflation expectations 9

10 What we do We ask the same subjects to respond to a survey and participate in a financially incentivized experiment In survey, we elicit inflation expectations In experiment, subjects chose between investments whose final payoffs depend on future inflation The objective is to compare the survey responses with the behavior in experiment The survey and the experiment is repeated with the same respondents 10

11 Motivation 1 : Are Survey Responses Informative? Inflation surveys are widely used in practice and in academia Are these surveys informative? Possible reasons why surveys may not be informative about the true inflation beliefs of individual consumers: Respondents may not provide truthful responses Respondents may not provide thoughtful responses Survey questions may not be clear. What we do: We test how informative the subjects survey responses are about their decisions in the experiment. 11

12 Motivation 2 : Do agents act on their inflation beliefs? There is a debate about expectation formation, but macro models assume agents act on their inflation beliefs. Is there empirical support for this assumption? Possible reasons why agents may not act on their inflation beliefs: The impact of future inflation may not be sufficiently salient Lab evidence of money illusion What we do: We examine whether actions in financially incentivized experiment are consistent with self reported beliefs in survey 12

13 The Survey Conducted by RAND as part of American Life Panel We contacted 771 respondents randomly from participants in the Reuters/UMichigan Survey of Consumers conducted in 2007 Two waves: Wave 1, end of July Wave 2, January Consists of several parts, including inflation expectations elicitation, experiment, elicitation of risk attitude, numeracy and financial literacy 13

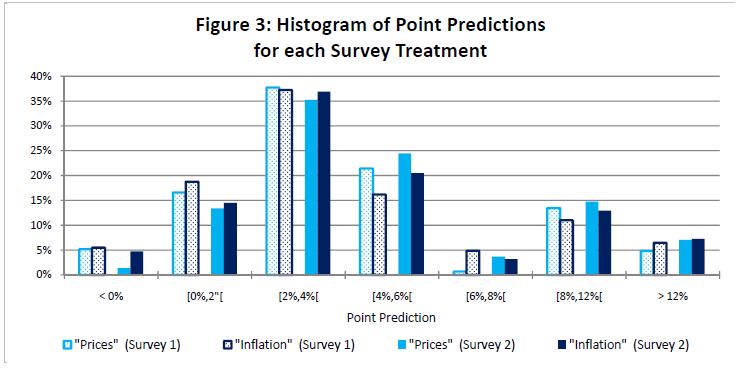

14 Inflation Expectations Questions Two survey treatments: 1. Inflation : Over the next 12 months, I expect the rate of inflation to be % OR the rate of deflation (the opposite of inflation) to be %. 2. Prices Over the next 12 months, I expect prices of the things I usually spend money on to go up by % OR to go down by % 14

15 Elicitation of Probabilistic Beliefs What do you think is the percent chance that, over the next 12 months: the rate of inflation will be 12% or more the rate of inflation will be between 8% and 12% the rate of inflation will be between 4% and 8% the rate of inflation will be between 2% and 4% the rate of inflation will be between 0% and 2% the rate of deflation will be between 0% and 2% the rate of deflation will be between 2% and 4% the rate of deflation will be between 4% and 8% the rate of deflation will be between 8% and 12% the rate of deflation will be 12% or more % Total To verify if your responses add up to 100% press Add 15

16 The experiment Consists of 10 questions In each question, a subject chooses between investment A or B Each investment generates a payoff 12 months from now Once survey completed, we draw randomly 2 subjects and 1 question 12 months later, each of the selected subjects is paid according to his/her choice for the selected question 16

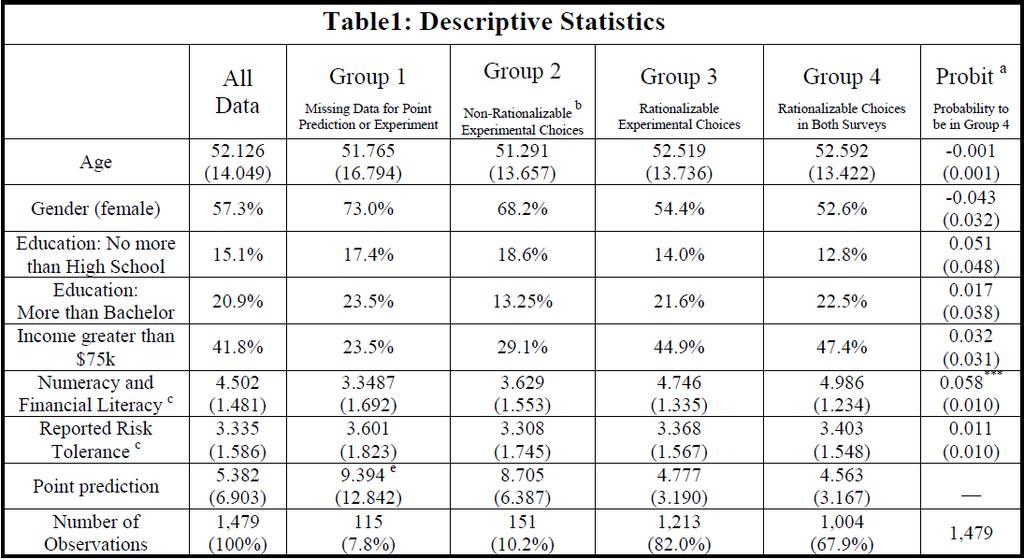

17 The Experimental Questions Rate of inflation -1% or less (deflation) Earnings under investment A 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% or more Earnings $600 $550 $500 $450 $400 $350 $300 $250 $200 $150 $100 $50 Question 1: Which one of these two investments do you choose? ( ) Investment A: your earnings are determined by the table above. ( ) Investment B: your earnings are exactly $100. Question 2: Which one of these two investments do you choose? ( ) Investment A: your earnings are determined by the table above. ( ) Investment B: your earnings are exactly $ Question 10: Which one of these two investments do you choose? ( ) Investment A: your earnings are determined by the table above. ( ) Investment B: your earnings are exactly $

18 The Experimental Questions Earnings under investment A Rate of inflation -1% or less (deflation) 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% or more Earnings $600 $550 $500 $450 $400 $350 $300 $250 $200 $150 $100 $50 Question 1: Which one of these two investments do you choose? ( ) Investment A: your earnings are determined by the table above. ( ) Investment B: your earnings are exactly $100.. Question 6: Which one of these two investments do you choose? ( ) Investment A: your earnings are determined by the table above. ( ) Investment B: your earnings are exactly $350.. Question 10: Which one of these two investments do you choose? ( ) Investment A: your earnings are determined by the table above. ( ) Investment B: your earnings are exactly $

19 Switching Point If rational a subject should switch investment at most once from investment A to investment B Define Switching Point as the number of A choices before the subject switch to investment B Switching point is only defined for respondents with rationalizable choices 19

20 The investments Investment A corresponds to the following scenario: An agent borrows $5,000 for 12 months at a rate equal to the inflation rate, and invests the $5,000 for 12 months in an account that earns a fixed annual rate of 11%. Investment B corresponds to the following scenario: An agent borrows $5,000 for 12 months at a rate equal to the inflation rate, and invests the $5,000 for 12 months in an inflation protected account that earns an annual rate equal to the inflation rate plus k % A is an affine transformation of B, and A is riskier than B 20

21 Theoretical Predictions Proposition 1: If a risk averse agent is indifferent between investment A and investment B, then, all else equal, a more risk averse agent prefers investment B to investment A. Proposition 2: If a risk averse agent is indifferent between investment A and investment B, then the agent prefers investment B to investment A for any increase in risk 21

22 Numeracy and Financial Literacy Questions We ask 6 questions to measure a respondent s numeracy and financial literacy Imagine that we roll a fair, six-sided die 1,000 times. Out of 1,000 rolls, how many times do you think the die would come up as an even number? If you have $100 in a savings account, the interest rate is 10% per year and you never withdraw money or interest payments, how much will you have in the account after: one year? two years? Number of correct answers: 4.5 on average with a median at 5 22

23 Self reported Risk Tolerance On a scale from 1 to 7, how would you rate your willingness to take risks regarding financial matters? (Note: 1 means "not willing at all" and 7 means "very willing") This instrument has been shown to produce meaningful measures of risk attitudes Average is 3.3 with a median at 3 33% less or equal to 2. 25% greater or equal to 5 Correlation of between the two surveys 23

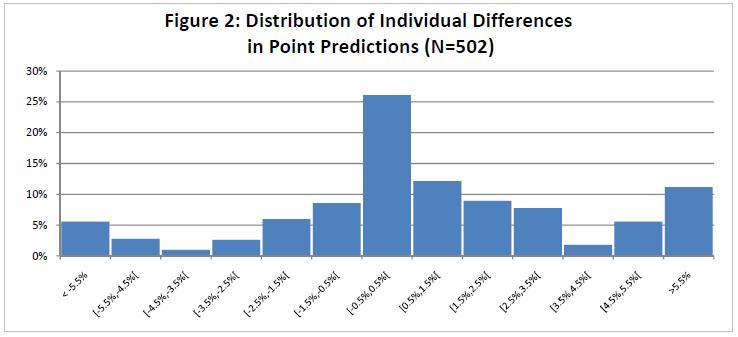

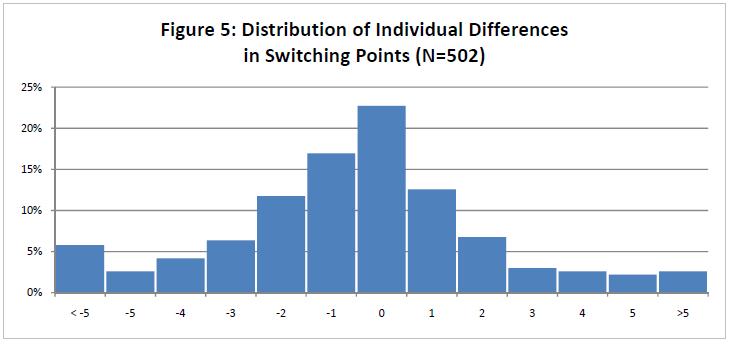

24 Survey Responses Out of the 771 respondents we contacted, 745 completed survey 1 and 734 completed survey respondents (57 in survey 1, 58 in survey 2) with missing data Out of the 1,364 remaining respondents, 88.9% (598 in Survey 1 and 615 in survey) made rationalizable experimental decisions 502 repeat respondents with rationalizable choices in both surveys 24

25 25

26 26

27 27

28 28

29 29

30 Question 1: Are survey responses informative about experimental choices? 30

31 Prediction 10% Choices and Predictions 9% 8% 7% As if Risk Loving 6% 5% 4% 3% 2% 1% 0% -1% As if Risk Averse Switching Point Risk Neutral Bandwidth 31

32 Reported Point Prediction Survey 1 11% Choices and Predictions 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% Switching Point Average Prediction Survey 1 (N=598) Risk Neutral Band 32

33 Reported Point Prediction Survey 2 11% Choices and Predictions 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% Switching Point Average Prediction Survey 1 (N=598) Average Prediction Survey 2 (N=615) 33

34 Predictions Observed Behavior in Investment Experiment 25 Choices and Dispersion of Predictions Switching Point Average Prediction Risk Neutral Bandwith 34

35 Summary of Result Inflation expectations is correlated with behavior in experiment. Average behavior is consistent with expected payoff maximization Substantial heterogeneity in choices Distribution of Subjects According to Observed Behavior As if Risk Averse As if Risk Neutral As if Risk Loving 39% 41% 20% 35

36 Prediction Deviations from Risk neutrality Choices and Predictions 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% Risk Neutral Bandwidth Number of A choices 36

37 Prediction Deviations from Risk neutrality Choices and Predictions 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% Risk Neutral Bandwidth Number of A choices 37

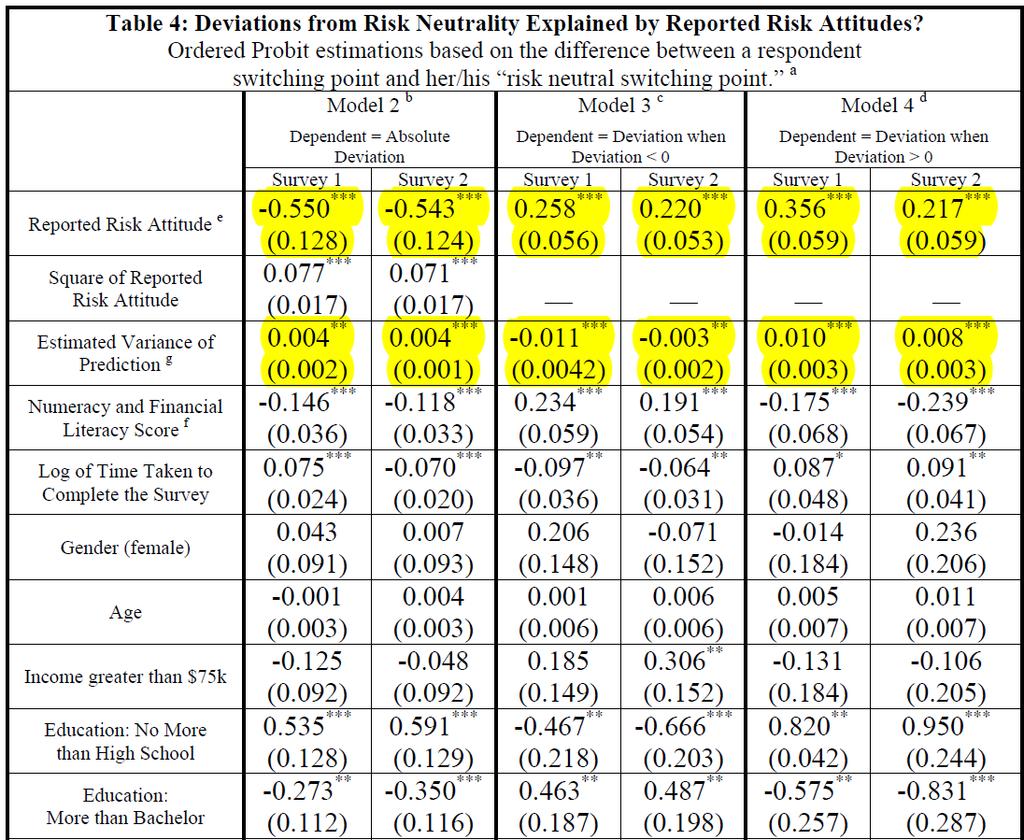

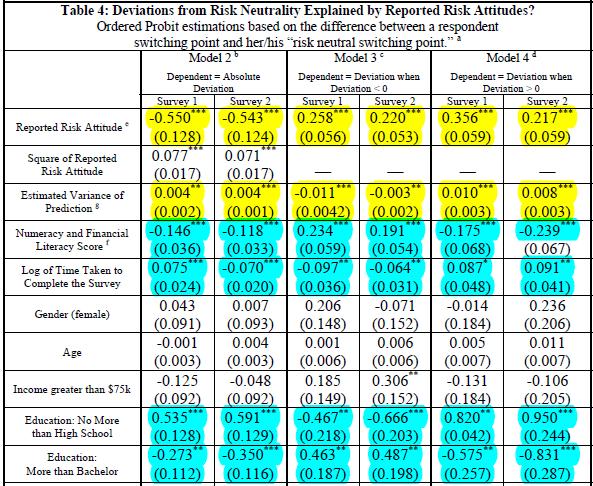

38 Deviations from Risk neutrality We calculate the deviation from Risk Neutrality for each respondent Under expected utility theory deviations from risk neutrality should be explained only by: Risk attitude Investment subjective risk 38

39 39

40 40

41 Summary of Result Consistent with EU, deviations from Risk Neutrality seem to be explained in large part by risk aversion and inflation uncertainty Other variables have explanatory power: Financial literacy and numeracy Education Time taken to complete survey 41

42 Exploiting the panel Question 2: Is the direction of the changes in predictions and choices between survey 1 and 2 consistent with theory? 42

43 Prediction Changes in Revealed Risk Attitude Choices and Predictions 10% 9% 8% As if Risk Loving in Survey 2 7% 6% 5% 4% 3% 2% As if Risk Averse in Survey 1 1% 0% -1% Risk Neutral Bandwidth Number of A choices 43

44 Prediction Changes in Revealed Risk Attitude Choices and Predictions 10% 9% 8% As if Risk Loving in Survey 1 7% 6% 5% 4% 3% 2% As if Risk Averse in Survey 2 1% 0% -1% Risk Neutral Bandwidth Number of A choices 44

45 70% Distribution of Revealed Risk Attitude in each Survey (N=502) 60% 50% 40% 30% 20% 10% 0% As if RA in Survey 2 As if RN in Survey 2 As if RL in Survey 2 As if RA in Survey 1 As if RN in Survey 1 As if RL in Survey 1 45

46 46

47 Changes in Revealed Risk Attitude Out of 502 respondents 6.0% have inconsistent revealed risk attitudes. Predominantly low education, low numerical and financial literacy. 47

48 Prediction Changes in predictions and Switching points 10% 9% 8% 7% First order effect 6% 5% 4% 3% 2% 1% 0% -1% Risk Neutral Bandwidth Number of A choices 48

49 Prediction Changes in predictions and Switching points 10% 9% 8% 7% First order effect 6% 5% 4% 3% 2% 1% 0% -1% Risk Neutral Bandwidth Number of A choices 49

50 Prediction Changes in predictions and Switching points 10% First order effect 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% Risk Neutral Bandwidth Number of A choices 50

51 Prediction Changes in predictions and Switching points 10% 9% 8% 7% First order effect 6% 5% 4% 3% 2% 1% 0% -1% Risk Neutral Bandwidth Number of A choices 51

52 Prediction Changes in predictions and Switching points 10% 9% 8% 7% 6% First order effect 5% 4% 3% 2% 1% 0% -1% Risk Neutral Bandwidth Number of A choices 52

53 53

54 54

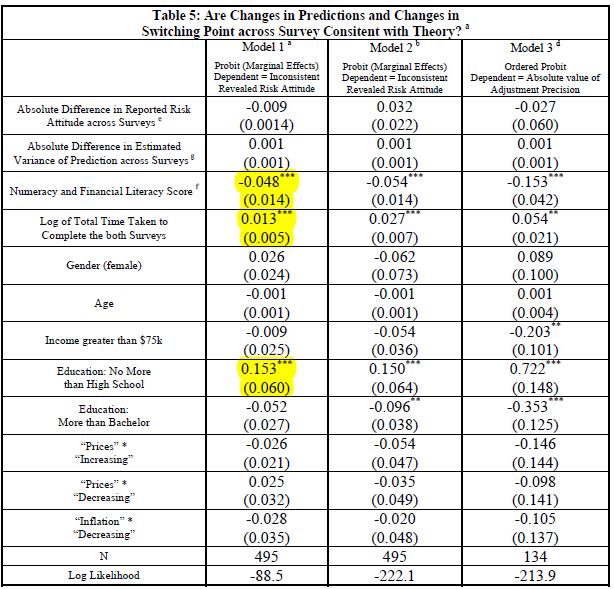

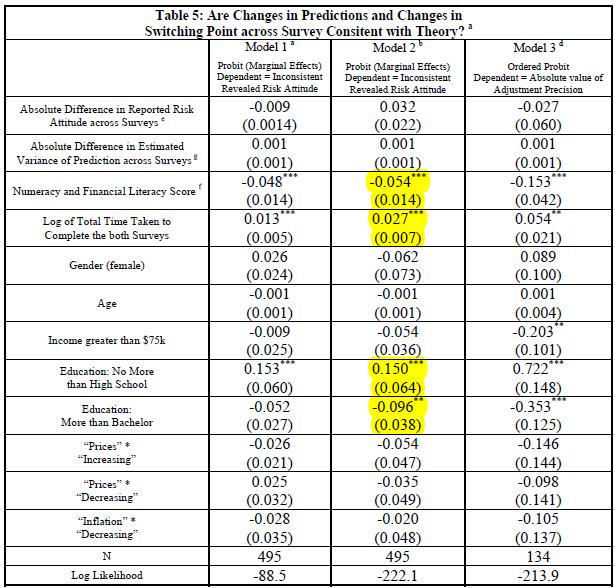

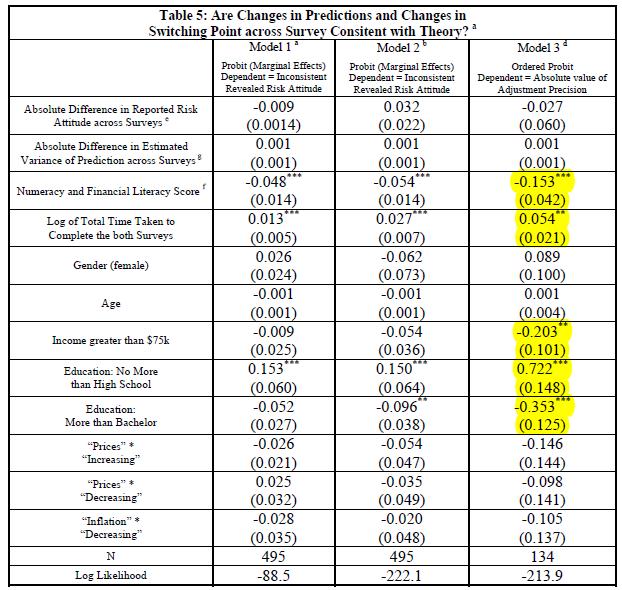

55 Inconsistent correlations Out of 502 respondents 21.5% have an inconsistent correlation between their change in predictions and their change in switching points Predominantly low education, low numerical and financial literacy. 55

56 Question 3: Is the magnitude of the changes in predictions and choices between survey 1 and 2 consistent with theory? 56

57 Methodology Assume each respondent has a simple power utility function x θ Based on respondent s i) elicited probabilistic belief and ii) experimental choice in survey 1, we calculate bounds for θ for the respondent Based on estimated θ and respondent s probabilistic belief in survey 2, we calculate the theoretical choice in survey 2 Compare actual and theoretical choice in survey 2 57

58 58

59 59

60 Findings For 41% of respondents the magnitude of the changes between predictions and experimental choices in the 2 surveys is exactly consistent with theory. Large differences between theoretical and actual choices are predominantly due to respondents with low education, low numerical and financial literacy. 60

61 Conclusion On average, subjects do seem to act on their self reported belief about future inflation We find evidence that behavior in the experiment is often consistent (both in direction and magnitude) with expected utility Subjects who violate expected utility tend to have lower education and lower numeracy and financial literacy By identifying a breakdown of the connection between beliefs and actions, our results suggest a specific channel through which financial literacy affects economic behavior 61

62 Conclusion Our results therefore : Confirm that inflation expectations surveys are informative Support micro foundation of modern macro-economic models 62

63 Thank You 63

64 How Consumers Form/Update Expectations (cont) The Price is Right: Updating of Inflation Expectations in a randomized price information experiment (with Olivier Armantier, Giorgio Topa, Basit Zafar). Implemented on RAND s ALP Stage 1: Elicit inflation expectations Stage 2: the respondent receives one of two information treatments. First ask one of two questions: The Food treatment : Over the last twelve months, by how much do you think the average prices of food and beverages in the US have changed? The SPF Forecast Treatment : A group of professional economists report their expectations of future inflation on a regular basis. What do you think these professional economists predicted inflation to be over the next twelve months? We then randomly provide each group with (i) no information, (ii) latest Food/SPF information Stage 3: We re-elicit inflation expectations 64

65 Randomized Information Experiment Methodology has advantage of being able to infer causal effect of different types of inflation-relevant information on expectation updating, without having to make assumptions about elements of the respondent s information set or updating rules Findings: Respondents are not fully informed about the objective inflation measures in our information treatments generally report higher numbers Respondents, on average, update sensibly in response to information we provided, indicating relevance of the information Updating reflects both the sign and size of the perception gaps Findings suggests that high survey inflation forecasts may be due in part to incorrect perceptions about objective measures of inflation. => possible scope for public information campaigns as part of prudent monetary policy 65

66 SCE Findings: Randomized Investment Experiment Findings: Reported inflation expectations are informative in the sense that the beliefs reported by the respondents are correlated with their choices in the experiment Furthermore, most respondents appear to act on their inflation expectations in ways consistent (both in direction and magnitude) with expected utility theory Respondents whose behavior cannot be rationalized or whose choices are inconsistent with expected utility theory tend to be less educated and score lower on a numeracy and financial literacy scale By identifying a breakdown of the connection between beliefs and actions, our results suggest a specific channel through which financial literacy affects economic behavior 66

67 SCE Findings on: What Consumers Know Student Loan Literacy: To what extent does the American public understand the implications of student loan indebtedness? We asked1,029 survey respondents in the SCE: What is the likelihood that someone s student debt would be forgiven if they were to file for bankruptcy, on a scale from 1 to 5 (where 1 is extremely unlikely and 5 is extremely likely )? Only 37% chose extremely unlikely 18% somewhat unlikely 67

68 SCE Findings: Student Loan Literacy If a borrower is unable to repay her federal student loan, what steps can the government take to collect the debt? A. Report that the student debt is past due to the credit bureaus. B. Garnish wages until the debt, plus any interest and fees, is repaid. C. Retain tax refunds and Social Security payments until the debt, plus any interest and fees, is repaid. 41% checked A, 41% checked B, 51% checked C 35% checked none, 38% checked only 1 or 2 Only 27% correctly chose all three Higher for those with student loans, children with student loans, or delinquent student loans but rate still under 50% 68

69 SCE Findings on: What Consumers Know Misconceptions of College Benefits and Costs We asked SCE respondents about average earnings (at age 40) of current workers with and without college degrees in the population, as well as about the average annual cost of a 4yr Bachelor s degree at a public university. We also asked about future returns for themselves or their children We find biased beliefs about the population, with the average respondent under-estimating the average benefits, and overestimating the costs of a college education 74% of respondents under-estimate the population relative returns to a college education (which is 1.83). 78% among those without a college degree (average RCE of 1.63), 66% with college degree (average RCE of 1.83). Higher accuracy among those with higher numeracy 69

70 SCE Findings: Misconceptions on College Returns 77% (86%) over-estimate average sticker (net) public university costs Among parents with children 6-17, we find strong relationship between beliefs about population RCE and beliefs about SCE for own child and beliefs about child s RCE is a significant predictor of intended college attendance This suggests a role for potential information campaigns to inform the public about population RCE Misperceptions are larger for more disadvantaged groups, so information may help reduce gaps in college attendance Open question on how to best get information in a credible and cost-effective and feasible way to consumers 70

71 SCE Findings on: What Consumers Know Inflation Expectations: Differences by financial literacy/numeracy During the next 12 months, do you think that prices in general will go up, or go down, or stay where they are now?. By about what percent do you expect prices to go [up/down] on the average? Find considerable demographic differences in reported inflation expectations - mostly explained by differences in financial literacy: Respondents with lower financial literacy scores report higher and more extreme inflation expectations Evidence of differences in expectation formation: They thought more about specific (salient) prices; covering expenses reported higher uncertainty about future inflation, estimates more volatile over time: can lead to upward bias if perceived 0% floor had lower confidence in their financial knowledge and shorter planning horizons 71

72 SCE Findings on: Do Consumers Act on Their Expectations/Knowledge Randomized financially incentivized investment experiment: In experiment (conducted on ALP), subjects chose between investments whose final payoffs depend on future inflation Objective: compare inflation expectations with behavior in experiment Experiment Consists of 10 questions: In each question, a subject chooses between investment A or B generating a payoff 12 months from now 12 months later, two randomly selected individuals are paid according to his/her choice for the selected question A rational individual should switch investment at most once from investment A to investment B Define Switching Point as the number of A choices before the subject switch to investment B Switching point only defined for respondents with rationalizable choices 72

73 73

Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs?

: Do Survey Respondents Act on their Beliefs? Olivier Armantier Wändi Bruine de Bruin Giorgio Topa Wilbert van der Klaauw Basit Zafar 1 September 2014 ABSTRACT We compare the inflation expectations reported

: Do Survey Respondents Act on their Beliefs? Olivier Armantier Wändi Bruine de Bruin Giorgio Topa Wilbert van der Klaauw Basit Zafar 1 September 2014 ABSTRACT We compare the inflation expectations reported

A NOTE ON SANDRONI-SHMAYA BELIEF ELICITATION MECHANISM

The Journal of Prediction Markets 2016 Vol 10 No 2 pp 14-21 ABSTRACT A NOTE ON SANDRONI-SHMAYA BELIEF ELICITATION MECHANISM Arthur Carvalho Farmer School of Business, Miami University Oxford, OH, USA,

The Journal of Prediction Markets 2016 Vol 10 No 2 pp 14-21 ABSTRACT A NOTE ON SANDRONI-SHMAYA BELIEF ELICITATION MECHANISM Arthur Carvalho Farmer School of Business, Miami University Oxford, OH, USA,

An Overview of the Survey of Consumer Expectations

Federal Reserve Bank of New York Staff Reports An Overview of the Survey of Consumer Expectations Olivier Armantier Giorgio Topa Wilbert van der Klaauw Basit Zafar Staff Report No. 800 November 2016 This

Federal Reserve Bank of New York Staff Reports An Overview of the Survey of Consumer Expectations Olivier Armantier Giorgio Topa Wilbert van der Klaauw Basit Zafar Staff Report No. 800 November 2016 This

The Price is Right: Updating Inflation Expectations in a Randomized Price Information Experiment

The Price is Right: Updating Inflation Expectations in a Randomized Price Information Experiment Olivier Armantier 1 Scott Nelson 2 Giorgio Topa 1 Wilbert van der Klaauw 1 Basit Zafar 1 ABSTRACT Understanding

The Price is Right: Updating Inflation Expectations in a Randomized Price Information Experiment Olivier Armantier 1 Scott Nelson 2 Giorgio Topa 1 Wilbert van der Klaauw 1 Basit Zafar 1 ABSTRACT Understanding

An Overview of the Survey of Consumer Expectations

Olivier Armantier, Giorgio Topa, Wilbert van der Klaauw, and Basit Zafar An Overview of the Survey of Consumer Expectations The New York Fed s Survey of Consumer Expectations (SCE) gathers information

Olivier Armantier, Giorgio Topa, Wilbert van der Klaauw, and Basit Zafar An Overview of the Survey of Consumer Expectations The New York Fed s Survey of Consumer Expectations (SCE) gathers information

Cognitive Constraints on Valuing Annuities. Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S. Mitchell

Cognitive Constraints on Valuing Annuities Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S. Mitchell Under a wide range of assumptions people should annuitize to guard against length-of-life uncertainty

Cognitive Constraints on Valuing Annuities Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S. Mitchell Under a wide range of assumptions people should annuitize to guard against length-of-life uncertainty

The Causal Effects of Economic Incentives, Health and Job Characteristics on Retirement: Estimates Based on Subjective Conditional Probabilities*

The Causal Effects of Economic Incentives, Health and Job Characteristics on Retirement: Estimates Based on Subjective Conditional Probabilities* Péter Hudomiet, Michael D. Hurd, and Susann Rohwedder October,

The Causal Effects of Economic Incentives, Health and Job Characteristics on Retirement: Estimates Based on Subjective Conditional Probabilities* Péter Hudomiet, Michael D. Hurd, and Susann Rohwedder October,

NYFed s Center for Microeconomic Data currently houses two major data collection efforts:

Presentation Outline NYFed s Center for Microeconomic Data currently houses two major data collection efforts: Survey of Consumer Expectations (SCE) NYFed Consumer Credit Panel (CCP) For each: Brief description

Presentation Outline NYFed s Center for Microeconomic Data currently houses two major data collection efforts: Survey of Consumer Expectations (SCE) NYFed Consumer Credit Panel (CCP) For each: Brief description

Home Price Expectations and Behavior: Evidence from a Randomized Information Experiment

Home Price Expectations and Behavior: Evidence from a Randomized Information Experiment Luis Armona, Andreas Fuster, and Basit Zafar September 9, 2016 Abstract Home price expectations are believed to play

Home Price Expectations and Behavior: Evidence from a Randomized Information Experiment Luis Armona, Andreas Fuster, and Basit Zafar September 9, 2016 Abstract Home price expectations are believed to play

MetLife Retirement Income. A Survey of Pre-Retiree Knowledge of Financial Retirement Issues

MetLife Retirement Income IQ Study A Survey of Pre-Retiree Knowledge of Financial Retirement Issues June, 2008 The MetLife Mature Market Institute Established in 1997, the Mature Market Institute (MMI)

MetLife Retirement Income IQ Study A Survey of Pre-Retiree Knowledge of Financial Retirement Issues June, 2008 The MetLife Mature Market Institute Established in 1997, the Mature Market Institute (MMI)

Investment Decisions and Negative Interest Rates

Investment Decisions and Negative Interest Rates No. 16-23 Anat Bracha Abstract: While the current European Central Bank deposit rate and 2-year German government bond yields are negative, the U.S. 2-year

Investment Decisions and Negative Interest Rates No. 16-23 Anat Bracha Abstract: While the current European Central Bank deposit rate and 2-year German government bond yields are negative, the U.S. 2-year

The Role of Exponential-Growth Bias and Present Bias in Retirment Saving Decisions

The Role of Exponential-Growth Bias and Present Bias in Retirment Saving Decisions Gopi Shah Goda Stanford University & NBER Matthew Levy London School of Economics Colleen Flaherty Manchester University

The Role of Exponential-Growth Bias and Present Bias in Retirment Saving Decisions Gopi Shah Goda Stanford University & NBER Matthew Levy London School of Economics Colleen Flaherty Manchester University

How Do You Measure Which Retirement Income Strategy Is Best?

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

How Are Credit Line Decreases Impacting Consumer Credit Risk?

How Are Credit Line Decreases Impacting Consumer Credit Risk? As lenders reduce or close credit lines to mitigate exposure, new research explores its impact on FICO scores Number 22 August 2009 With recent

How Are Credit Line Decreases Impacting Consumer Credit Risk? As lenders reduce or close credit lines to mitigate exposure, new research explores its impact on FICO scores Number 22 August 2009 With recent

ECON 312: MICROECONOMICS II Lecture 11: W/C 25 th April 2016 Uncertainty and Risk Dr Ebo Turkson

ECON 312: MICROECONOMICS II Lecture 11: W/C 25 th April 2016 Uncertainty and Risk Dr Ebo Turkson Chapter 17 Uncertainty Topics Degree of Risk. Decision Making Under Uncertainty. Avoiding Risk. Investing

ECON 312: MICROECONOMICS II Lecture 11: W/C 25 th April 2016 Uncertainty and Risk Dr Ebo Turkson Chapter 17 Uncertainty Topics Degree of Risk. Decision Making Under Uncertainty. Avoiding Risk. Investing

Selection of High-Deductible Health Plans: Attributes Influencing Likelihood and Implications for Consumer-Driven Approaches

Selection of High-Deductible Health Plans: Attributes Influencing Likelihood and Implications for Consumer-Driven Approaches Wendy D. Lynch, Ph.D. Harold H. Gardner, M.D. Nathan L. Kleinman, Ph.D. Health

Selection of High-Deductible Health Plans: Attributes Influencing Likelihood and Implications for Consumer-Driven Approaches Wendy D. Lynch, Ph.D. Harold H. Gardner, M.D. Nathan L. Kleinman, Ph.D. Health

IN ECONOMICS AND FINANCE

current FEDERAL RESERVE BANK OF NEW YORK issues IN ECONOMICS AND FINANCE Volume, Number 7 August/September 00 www.newyorkfed.org/research/current_issues Improving Survey Measures of Household Inflation

current FEDERAL RESERVE BANK OF NEW YORK issues IN ECONOMICS AND FINANCE Volume, Number 7 August/September 00 www.newyorkfed.org/research/current_issues Improving Survey Measures of Household Inflation

Risk attitude, investments, and the taste for luxuries versus. necessities. Introduction. Jonathan Baron

Risk attitude, investments, and the taste for luxuries versus necessities Jonathan Baron Introduction Individuals should differ in their tolerance for risky financial investments. For one thing, people

Risk attitude, investments, and the taste for luxuries versus necessities Jonathan Baron Introduction Individuals should differ in their tolerance for risky financial investments. For one thing, people

Effect of Health on Risk Tolerance and Stock Market Behavior

Effect of Health on Risk Tolerance and Stock Market Behavior Shailesh Reddy 4/23/2010 The goal of this paper is to try to gauge the effect that an individual s health has on his risk tolerance and in turn

Effect of Health on Risk Tolerance and Stock Market Behavior Shailesh Reddy 4/23/2010 The goal of this paper is to try to gauge the effect that an individual s health has on his risk tolerance and in turn

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997 CORPORATE MANAGERS RISKY BEHAVIOR: RISK TAKING OR AVOIDING?

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997 CORPORATE MANAGERS RISKY BEHAVIOR: RISK TAKING OR AVOIDING? Kathryn Sullivan* Abstract This study reports on five experiments that

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997 CORPORATE MANAGERS RISKY BEHAVIOR: RISK TAKING OR AVOIDING? Kathryn Sullivan* Abstract This study reports on five experiments that

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions Susan K. Laury and Charles A. Holt Prepared for the Handbook of Experimental Economics Results February 2002 I. Introduction

Payoff Scale Effects and Risk Preference Under Real and Hypothetical Conditions Susan K. Laury and Charles A. Holt Prepared for the Handbook of Experimental Economics Results February 2002 I. Introduction

Inflation Targeting and Revisions to Inflation Data: A Case Study with PCE Inflation * Calvin Price July 2011

Inflation Targeting and Revisions to Inflation Data: A Case Study with PCE Inflation * Calvin Price July 2011 Introduction Central banks around the world have come to recognize the importance of maintaining

Inflation Targeting and Revisions to Inflation Data: A Case Study with PCE Inflation * Calvin Price July 2011 Introduction Central banks around the world have come to recognize the importance of maintaining

Learning Objectives = = where X i is the i t h outcome of a decision, p i is the probability of the i t h

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

DETERMINANTS OF RISK AVERSION: A MIDDLE-EASTERN PERSPECTIVE

DETERMINANTS OF RISK AVERSION: A MIDDLE-EASTERN PERSPECTIVE Amit Das, Department of Management & Marketing, College of Business & Economics, Qatar University, P.O. Box 2713, Doha, Qatar amit.das@qu.edu.qa,

DETERMINANTS OF RISK AVERSION: A MIDDLE-EASTERN PERSPECTIVE Amit Das, Department of Management & Marketing, College of Business & Economics, Qatar University, P.O. Box 2713, Doha, Qatar amit.das@qu.edu.qa,

Asymmetric Information and the Impact on Interest Rates. Evidence from Forecast Data

Asymmetric Information and the Impact on Interest Rates Evidence from Forecast Data Asymmetric Information Hypothesis (AIH) Asserts that the federal reserve possesses private information about the current

Asymmetric Information and the Impact on Interest Rates Evidence from Forecast Data Asymmetric Information Hypothesis (AIH) Asserts that the federal reserve possesses private information about the current

Understanding and Achieving Participant Financial Wellness

Understanding and Achieving Participant Financial Wellness Insights from our research From August 25, 2017 to January 31, 2018, the companies of OneAmerica fielded an online survey to retirement plan participants

Understanding and Achieving Participant Financial Wellness Insights from our research From August 25, 2017 to January 31, 2018, the companies of OneAmerica fielded an online survey to retirement plan participants

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the

and not those of the Wharton School or the") All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

Consumer Literacy & Credit Worthiness

Consumer Literacy & Credit Worthiness June 1, 2005 Marsha J. Courchane, Principal, ERS Group Peter M. Zorn, VP, Housing Analysis, Research & Policy, FMAC Prepared for: Wisconsin Department of Financial

Consumer Literacy & Credit Worthiness June 1, 2005 Marsha J. Courchane, Principal, ERS Group Peter M. Zorn, VP, Housing Analysis, Research & Policy, FMAC Prepared for: Wisconsin Department of Financial

Random Variables and Applications OPRE 6301

Random Variables and Applications OPRE 6301 Random Variables... As noted earlier, variability is omnipresent in the business world. To model variability probabilistically, we need the concept of a random

Random Variables and Applications OPRE 6301 Random Variables... As noted earlier, variability is omnipresent in the business world. To model variability probabilistically, we need the concept of a random

SURVEY OF CONSUMER EXPECTATIONS. Housing Survey 2016

SURVEY OF CONSUMER EXPECTATIONS Housing Survey 2016 Federal Reserve Bank of New York Andreas Fuster and Basit Zafar with Kevin Morris une 2, 2016 SCE ederal Housing Reserve Survey 2016 Bank of New York

SURVEY OF CONSUMER EXPECTATIONS Housing Survey 2016 Federal Reserve Bank of New York Andreas Fuster and Basit Zafar with Kevin Morris une 2, 2016 SCE ederal Housing Reserve Survey 2016 Bank of New York

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending Tetyana Balyuk BdF-TSE Conference November 12, 2018 Research Question Motivation Motivation Imperfections in consumer credit market

THE CODING OF OUTCOMES IN TAXPAYERS REPORTING DECISIONS. A. Schepanski The University of Iowa

THE CODING OF OUTCOMES IN TAXPAYERS REPORTING DECISIONS A. Schepanski The University of Iowa May 2001 The author thanks Teri Shearer and the participants of The University of Iowa Judgment and Decision-Making

THE CODING OF OUTCOMES IN TAXPAYERS REPORTING DECISIONS A. Schepanski The University of Iowa May 2001 The author thanks Teri Shearer and the participants of The University of Iowa Judgment and Decision-Making

Selection of High-Deductible Health Plans

Selection of High-Deductible Health Plans Attributes Influencing Likelihood and Implications for Consumer- Driven Approaches Wendy Lynch, PhD Harold H. Gardner, MD Nathan Kleinman, PhD 415 W. 17th St.,

Selection of High-Deductible Health Plans Attributes Influencing Likelihood and Implications for Consumer- Driven Approaches Wendy Lynch, PhD Harold H. Gardner, MD Nathan Kleinman, PhD 415 W. 17th St.,

HCEO WORKING PAPER SERIES

HCEO WORKING PAPER SERIES Working Paper The University of Chicago 1126 E. 59th Street Box 107 Chicago IL 60637 www.hceconomics.org Labor Market Search With Imperfect Information and Learning John J. Conlon

HCEO WORKING PAPER SERIES Working Paper The University of Chicago 1126 E. 59th Street Box 107 Chicago IL 60637 www.hceconomics.org Labor Market Search With Imperfect Information and Learning John J. Conlon

Expectation Formation

Expectation Formation Theresa Kuchler ; Basit Zafar PRELIMINARY VERSION Abstract We use novel survey panel data to estimate how personal experiences affect household expectations about aggregate economic

Expectation Formation Theresa Kuchler ; Basit Zafar PRELIMINARY VERSION Abstract We use novel survey panel data to estimate how personal experiences affect household expectations about aggregate economic

5IE475 Program Evaluation and Cost-Benefit Analysis

5IE475 Program Evaluation and Cost-Benefit Analysis LECTURE 12 Instrumental Variable Approach (contd) Qualitative program evaluation Klára Kalíšková EXAMPLES OF INSTRUMENTAL VARIABLES STUDIES (CONTD) 2

5IE475 Program Evaluation and Cost-Benefit Analysis LECTURE 12 Instrumental Variable Approach (contd) Qualitative program evaluation Klára Kalíšková EXAMPLES OF INSTRUMENTAL VARIABLES STUDIES (CONTD) 2

Two plus two makes five? Survey evidence that investors overvalue structured deposits Technical Appendix

Financial Conduct Authority Two plus two makes five? Survey evidence that investors overvalue structured deposits Technical Appendix March 2015 Occasional Paper No.9 Two plus two makes five? Survey evidence

Financial Conduct Authority Two plus two makes five? Survey evidence that investors overvalue structured deposits Technical Appendix March 2015 Occasional Paper No.9 Two plus two makes five? Survey evidence

Household Debt and Saving during the 2007 Recession 1

Household Debt and Saving during the 2007 Recession 1 Rajashri Chakrabarti, Donghoon Lee, Wilbert van der Klaauw and Basit Zafar Federal Reserve Bank of New York October 2010 Abstract Using detailed administrative

Household Debt and Saving during the 2007 Recession 1 Rajashri Chakrabarti, Donghoon Lee, Wilbert van der Klaauw and Basit Zafar Federal Reserve Bank of New York October 2010 Abstract Using detailed administrative

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next?

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next? Presentation to Financial Literacy 09 Retirement Commission, New Zealand June 26, 2009 Annamaria Lusardi

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next? Presentation to Financial Literacy 09 Retirement Commission, New Zealand June 26, 2009 Annamaria Lusardi

Harris Interactive. ACEP Emergency Care Poll

ACEP Emergency Care Poll Table of Contents Background and Objectives 3 Methodology 4 Report Notes 5 Executive Summary 6 Detailed Findings 10 Demographics 24 Background and Objectives To assess the general

ACEP Emergency Care Poll Table of Contents Background and Objectives 3 Methodology 4 Report Notes 5 Executive Summary 6 Detailed Findings 10 Demographics 24 Background and Objectives To assess the general

Learning Objectives 6/2/18. Some keys from yesterday

Valuation and pricing (November 5, 2013) Lecture 12 Decisions Risk & Uncertainty Olivier J. de Jong, LL.M., MM., MBA, CFD, CFFA, AA www.centime.biz Some keys from yesterday Learning Objectives v Explain

Valuation and pricing (November 5, 2013) Lecture 12 Decisions Risk & Uncertainty Olivier J. de Jong, LL.M., MM., MBA, CFD, CFFA, AA www.centime.biz Some keys from yesterday Learning Objectives v Explain

Finish what s been left... CS286r Fall 08 Finish what s been left... 1

Finish what s been left... CS286r Fall 08 Finish what s been left... 1 Perfect Bayesian Equilibrium A strategy-belief pair, (σ, µ) is a perfect Bayesian equilibrium if (Beliefs) At every information set

Finish what s been left... CS286r Fall 08 Finish what s been left... 1 Perfect Bayesian Equilibrium A strategy-belief pair, (σ, µ) is a perfect Bayesian equilibrium if (Beliefs) At every information set

Suppose you plan to purchase

Volume 71 Number 1 2015 CFA Institute What Practitioners Need to Know... About Time Diversification (corrected March 2015) Mark Kritzman, CFA Although an investor may be less likely to lose money over

Volume 71 Number 1 2015 CFA Institute What Practitioners Need to Know... About Time Diversification (corrected March 2015) Mark Kritzman, CFA Although an investor may be less likely to lose money over

Differential Interpretation of Public Signals and Trade in Speculative Markets. Kandel & Pearson, JPE, 1995

Differential Interpretation of Public Signals and Trade in Speculative Markets Kandel & Pearson, JPE, 1995 Presented by Shunlan Fang May, 14 th, 2008 Roadmap Why differential opinions matter to asset pricing

Differential Interpretation of Public Signals and Trade in Speculative Markets Kandel & Pearson, JPE, 1995 Presented by Shunlan Fang May, 14 th, 2008 Roadmap Why differential opinions matter to asset pricing

NOTES ON THE BANK OF ENGLAND OPTION IMPLIED PROBABILITY DENSITY FUNCTIONS

1 NOTES ON THE BANK OF ENGLAND OPTION IMPLIED PROBABILITY DENSITY FUNCTIONS Options are contracts used to insure against or speculate/take a view on uncertainty about the future prices of a wide range

1 NOTES ON THE BANK OF ENGLAND OPTION IMPLIED PROBABILITY DENSITY FUNCTIONS Options are contracts used to insure against or speculate/take a view on uncertainty about the future prices of a wide range

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April Revised 5 July 2015

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April 2015 Revised 5 July 2015 [Slide 1] Let me begin by thanking Wolfgang Lutz for reaching

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April 2015 Revised 5 July 2015 [Slide 1] Let me begin by thanking Wolfgang Lutz for reaching

Unit 4.3: Uncertainty

Unit 4.: Uncertainty Michael Malcolm June 8, 20 Up until now, we have been considering consumer choice problems where the consumer chooses over outcomes that are known. However, many choices in economics

Unit 4.: Uncertainty Michael Malcolm June 8, 20 Up until now, we have been considering consumer choice problems where the consumer chooses over outcomes that are known. However, many choices in economics

Chapter 5: Answers to Concepts in Review

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

How to Measure Herd Behavior on the Credit Market?

How to Measure Herd Behavior on the Credit Market? Dmitry Vladimirovich Burakov Financial University under the Government of Russian Federation Email: dbur89@yandex.ru Doi:10.5901/mjss.2014.v5n20p516 Abstract

How to Measure Herd Behavior on the Credit Market? Dmitry Vladimirovich Burakov Financial University under the Government of Russian Federation Email: dbur89@yandex.ru Doi:10.5901/mjss.2014.v5n20p516 Abstract

Retirement Plans Preferences in the Philippines

DOI: 10.7763/IPEDR. 2014. V71. 12 Retirement Plans Preferences in the Philippines Ma. Belinda S. Mandigma College of Commerce and Business Administration, University of Santo Tomas, Philippines Abstract.

DOI: 10.7763/IPEDR. 2014. V71. 12 Retirement Plans Preferences in the Philippines Ma. Belinda S. Mandigma College of Commerce and Business Administration, University of Santo Tomas, Philippines Abstract.

What Influences Investor Decisions and Behaviors?

What Influences Investor Decisions and Behaviors? by Lewis Mandell, Ph.D. Professor of Finance and Dean Emeritus State University of New York at Buffalo In a world where financial products grow increasingly

What Influences Investor Decisions and Behaviors? by Lewis Mandell, Ph.D. Professor of Finance and Dean Emeritus State University of New York at Buffalo In a world where financial products grow increasingly

Health Insurance for Humans: Information Frictions, Plan Choice, and Consumer Welfare

Health Insurance for Humans: Information Frictions, Plan Choice, and Consumer Welfare Benjamin R. Handel Economics Department, UC Berkeley and NBER Jonathan T. Kolstad Wharton School, University of Pennsylvania

Health Insurance for Humans: Information Frictions, Plan Choice, and Consumer Welfare Benjamin R. Handel Economics Department, UC Berkeley and NBER Jonathan T. Kolstad Wharton School, University of Pennsylvania

Wilbert van der Klaauw, Federal Reserve Bank of New York Interactions Conference, September 26, 2015

Discussion of Partial Identification in Regression Discontinuity Designs with Manipulated Running Variables by Francois Gerard, Miikka Rokkanen, and Christoph Rothe Wilbert van der Klaauw, Federal Reserve

Discussion of Partial Identification in Regression Discontinuity Designs with Manipulated Running Variables by Francois Gerard, Miikka Rokkanen, and Christoph Rothe Wilbert van der Klaauw, Federal Reserve

Jamie Wagner Ph.D. Student University of Nebraska Lincoln

An Empirical Analysis Linking a Person s Financial Risk Tolerance and Financial Literacy to Financial Behaviors Jamie Wagner Ph.D. Student University of Nebraska Lincoln Abstract Financial risk aversion

An Empirical Analysis Linking a Person s Financial Risk Tolerance and Financial Literacy to Financial Behaviors Jamie Wagner Ph.D. Student University of Nebraska Lincoln Abstract Financial risk aversion

Econ 219B Psychology and Economics: Applications (Lecture 1)

") Econ 219B Psychology and Economics: Applications (Lecture 1) Stefano DellaVigna January 23, 2008 Outline 1. Introduction / Prerequisites 2. Getting started! Psychology and Economics: The Topics 3. Psychology

Econ 219B Psychology and Economics: Applications (Lecture 1) Stefano DellaVigna January 23, 2008 Outline 1. Introduction / Prerequisites 2. Getting started! Psychology and Economics: The Topics 3. Psychology

Financial Accounting Theory SeventhEdition William R. Scott. Chapter 9 An Analysis of Conflict

Financial Accounting Theory SeventhEdition William R. Scott Chapter 9 An Analysis of Conflict How Is This Chapter Different? BEFORE in CAPM we have the market meaning everyone else Market price is the

Financial Accounting Theory SeventhEdition William R. Scott Chapter 9 An Analysis of Conflict How Is This Chapter Different? BEFORE in CAPM we have the market meaning everyone else Market price is the

Risk Aversion and Tacit Collusion in a Bertrand Duopoly Experiment

Risk Aversion and Tacit Collusion in a Bertrand Duopoly Experiment Lisa R. Anderson College of William and Mary Department of Economics Williamsburg, VA 23187 lisa.anderson@wm.edu Beth A. Freeborn College

Risk Aversion and Tacit Collusion in a Bertrand Duopoly Experiment Lisa R. Anderson College of William and Mary Department of Economics Williamsburg, VA 23187 lisa.anderson@wm.edu Beth A. Freeborn College

No THE MIRACLE OF COMPOUND INTEREST: DOES OUR INTUITION FAIL? By Johannes Binswanger, Katherine Grace Carman. December 2010 ISSN

No. 2010-137 THE MIRACLE OF COMPOUND INTEREST: DOES OUR INTUITION FAIL? By Johannes Binswanger, Katherine Grace Carman December 2010 ISSN 0924-7815 The Miracle of Compound Interest: Does our Intuition

No. 2010-137 THE MIRACLE OF COMPOUND INTEREST: DOES OUR INTUITION FAIL? By Johannes Binswanger, Katherine Grace Carman December 2010 ISSN 0924-7815 The Miracle of Compound Interest: Does our Intuition

FROM BEHAVIORAL BIAS TO RATIONAL INVESTING

FROM BEHAVIORAL BIAS TO RATIONAL INVESTING April 2016 Classical economics assumes individuals make rational choices, but human behavior is not always so rational. The application of psychology to economics

FROM BEHAVIORAL BIAS TO RATIONAL INVESTING April 2016 Classical economics assumes individuals make rational choices, but human behavior is not always so rational. The application of psychology to economics

Assessing Client Risk: A Two-Dimensional Approach

Page 1 of 5 Home Workstation Managed Portfolios Due-Diligence Center Assessing Client Risk: A Two- Dimensional Approach Departments 529 Plans Broker-Dealer Financial Planning Investments Newswire Portfolio

Page 1 of 5 Home Workstation Managed Portfolios Due-Diligence Center Assessing Client Risk: A Two- Dimensional Approach Departments 529 Plans Broker-Dealer Financial Planning Investments Newswire Portfolio

INVESTOR RISK PERCEPTION IN THE NETHERLANDS

Research Paper INVESTOR RISK PERCEPTION IN THE NETHERLANDS Contents 2 Summary 3 Demographics 4 Perceived Risk and investment Propensity 8 Investor Beliefs 10 Conclusion Summary Risk perception plays a

Research Paper INVESTOR RISK PERCEPTION IN THE NETHERLANDS Contents 2 Summary 3 Demographics 4 Perceived Risk and investment Propensity 8 Investor Beliefs 10 Conclusion Summary Risk perception plays a

Online Appendix A: Complete experimental materials for all studies and conditions

1 Online Appendix A: Complete experimental materials for all studies and conditions This document has all the experimental materials for the paper "Intertemporal Uncertainty Avoidance: When the Future

1 Online Appendix A: Complete experimental materials for all studies and conditions This document has all the experimental materials for the paper "Intertemporal Uncertainty Avoidance: When the Future

THE IMPORTANCE OF ASSET ALLOCATION vs. SECURITY SELECTION: A PRIMER. Highlights:

THE IMPORTANCE OF ASSET ALLOCATION vs. SECURITY SELECTION: A PRIMER Highlights: Investment results depend mostly on the market you choose, not the selection of securities within that market. For mutual

THE IMPORTANCE OF ASSET ALLOCATION vs. SECURITY SELECTION: A PRIMER Highlights: Investment results depend mostly on the market you choose, not the selection of securities within that market. For mutual

Price Theory Lecture 9: Choice Under Uncertainty

I. Probability and Expected Value Price Theory Lecture 9: Choice Under Uncertainty In all that we have done so far, we've assumed that choices are being made under conditions of certainty -- prices are

I. Probability and Expected Value Price Theory Lecture 9: Choice Under Uncertainty In all that we have done so far, we've assumed that choices are being made under conditions of certainty -- prices are

Executive Summary: Aging in Place: Analyzing the Use of Reverse Mortgages to Preserve Independent Living. Highlights Report of Survey Results

Executive Summary: Aging in Place: Analyzing the Use of Reverse Mortgages to Preserve Independent Living Highlights Report of Survey Results January 21, 2016 Research Study Team Stephanie Moulton,* Donald

Executive Summary: Aging in Place: Analyzing the Use of Reverse Mortgages to Preserve Independent Living Highlights Report of Survey Results January 21, 2016 Research Study Team Stephanie Moulton,* Donald

Executive Summary INCREASING LONG-TERM SAVINGS 66

Executive Summary When most households begin to make a budget, retirement savings is often the last bucket, only to be filled if there s anything left over after paying bills, loans, and everyday consumption.

Executive Summary When most households begin to make a budget, retirement savings is often the last bucket, only to be filled if there s anything left over after paying bills, loans, and everyday consumption.

Prices or Knowledge? What drives demand for financial services in emerging markets?

Prices or Knowledge? What drives demand for financial services in emerging markets? Shawn Cole (Harvard), Thomas Sampson (Harvard), and Bilal Zia (World Bank) CeRP September 2009 Motivation Access to financial

Prices or Knowledge? What drives demand for financial services in emerging markets? Shawn Cole (Harvard), Thomas Sampson (Harvard), and Bilal Zia (World Bank) CeRP September 2009 Motivation Access to financial

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics Annamaria Lusardi, GFLEC Carlo de Bassa Scheresberg, GFLEC Paul Yakoboski, TIAA-CREF Institute National

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics Annamaria Lusardi, GFLEC Carlo de Bassa Scheresberg, GFLEC Paul Yakoboski, TIAA-CREF Institute National

Measuring Impact. Impact Evaluation Methods for Policymakers. Sebastian Martinez. The World Bank

Impact Evaluation Measuring Impact Impact Evaluation Methods for Policymakers Sebastian Martinez The World Bank Note: slides by Sebastian Martinez. The content of this presentation reflects the views of

Impact Evaluation Measuring Impact Impact Evaluation Methods for Policymakers Sebastian Martinez The World Bank Note: slides by Sebastian Martinez. The content of this presentation reflects the views of

Banks Incentives and the Quality of Internal Risk Models

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

Banks Incentives and the Quality of Internal Risk Models Matthew Plosser Federal Reserve Bank of New York and João Santos Federal Reserve Bank of New York & Nova School of Business and Economics The views

An Introduction to Experimental Economics and Insurance Experiments. J. Todd Swarthout

An Introduction to Experimental Economics and Insurance Experiments J. Todd Swarthout One possible way of figuring out economic laws... is by controlled experiments.... Economists (unfortunately )... cannot

An Introduction to Experimental Economics and Insurance Experiments J. Todd Swarthout One possible way of figuring out economic laws... is by controlled experiments.... Economists (unfortunately )... cannot

INVESTOR QUESTIONNAIRE FIND YOUR FIT

INVESTOR QUESTIONNAIRE FIND YOUR FIT I L L U M I N A T I N G GRANITE INVESTOR QUESTIONNAIRE This questionnaire is designed to be used with your advisor when assessing your investment objectives and tolerance

INVESTOR QUESTIONNAIRE FIND YOUR FIT I L L U M I N A T I N G GRANITE INVESTOR QUESTIONNAIRE This questionnaire is designed to be used with your advisor when assessing your investment objectives and tolerance

ARE LOSS AVERSION AFFECT THE INVESTMENT DECISION OF THE STOCK EXCHANGE OF THAILAND S EMPLOYEES?

ARE LOSS AVERSION AFFECT THE INVESTMENT DECISION OF THE STOCK EXCHANGE OF THAILAND S EMPLOYEES? by San Phuachan Doctor of Business Administration Program, School of Business, University of the Thai Chamber

ARE LOSS AVERSION AFFECT THE INVESTMENT DECISION OF THE STOCK EXCHANGE OF THAILAND S EMPLOYEES? by San Phuachan Doctor of Business Administration Program, School of Business, University of the Thai Chamber

FIGURE A1.1. Differences for First Mover Cutoffs (Round one to two) as a Function of Beliefs on Others Cutoffs. Second Mover Round 1 Cutoff.

as a Function of Beliefs on Others Cutoffs. Second Mover Round 1 Cutoff.") APPENDIX A. SUPPLEMENTARY TABLES AND FIGURES A.1. Invariance to quantitative beliefs. Figure A1.1 shows the effect of the cutoffs in round one for the second and third mover on the best-response cutoffs

APPENDIX A. SUPPLEMENTARY TABLES AND FIGURES A.1. Invariance to quantitative beliefs. Figure A1.1 shows the effect of the cutoffs in round one for the second and third mover on the best-response cutoffs

CENTER FOR MICROECONOMIC DATA

CENTER FOR MICROECONOMIC DATA WWW.NEWYORKFED.ORG/MICROECONOMICS QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT 2018:Q1 (RELEASED MAY 2018 ) FEDERAL RESERVE BANK of NEW YORK RESEARCH AND STATISTICS GROUP

CENTER FOR MICROECONOMIC DATA WWW.NEWYORKFED.ORG/MICROECONOMICS QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT 2018:Q1 (RELEASED MAY 2018 ) FEDERAL RESERVE BANK of NEW YORK RESEARCH AND STATISTICS GROUP

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the

and not those of the Wharton School or the") All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

Irrational people and rational needs for optimal pension plans

Gordana Drobnjak CFA MBA Executive Director Republic of Srpska Pension reserve fund management company Irrational people and rational needs for optimal pension plans CEE Pension Funds Conference & Awards

Gordana Drobnjak CFA MBA Executive Director Republic of Srpska Pension reserve fund management company Irrational people and rational needs for optimal pension plans CEE Pension Funds Conference & Awards

CHAPTER 5 RESULT AND ANALYSIS

CHAPTER 5 RESULT AND ANALYSIS This chapter presents the results of the study and its analysis in order to meet the objectives. These results confirm the presence and impact of the biases taken into consideration,

CHAPTER 5 RESULT AND ANALYSIS This chapter presents the results of the study and its analysis in order to meet the objectives. These results confirm the presence and impact of the biases taken into consideration,

Fuzzy-Trace Theory & Financial Risk Tolerance. Meghaan Lurtz, Michael Kothakota, CFP, & Dr. S. Heckman, PhD/CFP 2018

Fuzzy-Trace Theory & Financial Risk Tolerance Meghaan Lurtz, Michael Kothakota, CFP, & Dr. S. Heckman, PhD/CFP 2018 Today s Plan Why & Literature Review Theoretical & Study Goals Method & Analysis Results

Fuzzy-Trace Theory & Financial Risk Tolerance Meghaan Lurtz, Michael Kothakota, CFP, & Dr. S. Heckman, PhD/CFP 2018 Today s Plan Why & Literature Review Theoretical & Study Goals Method & Analysis Results

Alex Morgano Ladji Bamba Lucas Van Cleef Computer Skills for Economic Analysis E226 11/6/2015 Dr. Myers. Abstract

1 Alex Morgano Ladji Bamba Lucas Van Cleef Computer Skills for Economic Analysis E226 11/6/2015 Dr. Myers Abstract This essay focuses on the causality between specific questions that deal with people s

1 Alex Morgano Ladji Bamba Lucas Van Cleef Computer Skills for Economic Analysis E226 11/6/2015 Dr. Myers Abstract This essay focuses on the causality between specific questions that deal with people s

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Finance Dissertation Topics The Rapid development of international micro-finance. Micro-finance in the UK banking industry. The demand for collective

Finance Dissertation Topics The Rapid development of international micro-finance. Micro-finance in the UK banking industry. The demand for collective investment schemes in the UK; A strategic analysis,

Finance Dissertation Topics The Rapid development of international micro-finance. Micro-finance in the UK banking industry. The demand for collective investment schemes in the UK; A strategic analysis,

CHAPTER 4: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 4: ANSWERS TO CONCEPTS IN REVIEW 4.1 The return on investment is the expected profit that motivates people to invest. It includes both current income and/or capital gains (or losses). Without a

CHAPTER 4: ANSWERS TO CONCEPTS IN REVIEW 4.1 The return on investment is the expected profit that motivates people to invest. It includes both current income and/or capital gains (or losses). Without a

Aaron Sojourner & Jose Pacas December Abstract:

Union Card or Welfare Card? Evidence on the relationship between union membership and net fiscal impact at the individual worker level Aaron Sojourner & Jose Pacas December 2014 Abstract: This paper develops

Union Card or Welfare Card? Evidence on the relationship between union membership and net fiscal impact at the individual worker level Aaron Sojourner & Jose Pacas December 2014 Abstract: This paper develops

Risk, Balanced Skills and Entrepreneurship

Risk, Balanced Skills and Entrepreneurship Mirjam van Praag Maersk Mc-Kinney Møller Professor of Entrepreneurship at Copenhagen Business School Co-authors : Chihmao Hsieh Yonsei University Simon C. Parker

Risk, Balanced Skills and Entrepreneurship Mirjam van Praag Maersk Mc-Kinney Møller Professor of Entrepreneurship at Copenhagen Business School Co-authors : Chihmao Hsieh Yonsei University Simon C. Parker

Bringing Meaning to Measurement

Review of Data Analysis of Insider Ontario Lottery Wins By Donald S. Burdick Background A data analysis performed by Dr. Jeffery S. Rosenthal raised the issue of whether retail sellers of tickets in the

Review of Data Analysis of Insider Ontario Lottery Wins By Donald S. Burdick Background A data analysis performed by Dr. Jeffery S. Rosenthal raised the issue of whether retail sellers of tickets in the

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 21 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS MICROECONOMIC AND REGIONAL STUDIES Household Debt and Credit Developments in 21Q3 1 Aggregate

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 21 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS MICROECONOMIC AND REGIONAL STUDIES Household Debt and Credit Developments in 21Q3 1 Aggregate

Consumer s behavior under uncertainty

Consumer s behavior under uncertainty Microéconomie, Chap 5 1 Plan of the talk What is a risk? Preferences under uncertainty Demand of risky assets Reducing risks 2 Introduction How does the consumer choose

Consumer s behavior under uncertainty Microéconomie, Chap 5 1 Plan of the talk What is a risk? Preferences under uncertainty Demand of risky assets Reducing risks 2 Introduction How does the consumer choose

INVESTMENT POLICY STATEMENT

INVESTMENT POLICY STATEMENT FOR CLIENT NAME DATE Investment Policy Statement i TABLE OF CONTENTS Introduction... 1 Goals / Objectives... 1 Primary or Strategic Goals... 1 Secondary or Tactical Goals...

INVESTMENT POLICY STATEMENT FOR CLIENT NAME DATE Investment Policy Statement i TABLE OF CONTENTS Introduction... 1 Goals / Objectives... 1 Primary or Strategic Goals... 1 Secondary or Tactical Goals...

$1,000 1 ( ) $2,500 2,500 $2,000 (1 ) (1 + r) 2,000

$2,500 2,500 $2,000 (1 ) (1 + r) 2,000") Answers To Chapter 9 Review Questions 1. Answer d. Other benefits include a more stable employment situation, more interesting and challenging work, and access to occupations with more prestige and more

Answers To Chapter 9 Review Questions 1. Answer d. Other benefits include a more stable employment situation, more interesting and challenging work, and access to occupations with more prestige and more

Future Beneficiary Expectations of the Returns to Delayed Social Security Benefit Claiming and Choice Behavior

Future Beneficiary Expectations of the Returns to Delayed Social Security Benefit Claiming and Choice Behavior Jeff Dominitz Angela Hung Arthur van Soest RAND Preliminary and Incomplete Draft Updated for

Future Beneficiary Expectations of the Returns to Delayed Social Security Benefit Claiming and Choice Behavior Jeff Dominitz Angela Hung Arthur van Soest RAND Preliminary and Incomplete Draft Updated for

What Would You Do with $500? Spending Responses to Gains, Losses, News, and Loans

Federal Reserve Bank of New York Staff Reports What Would You Do with $500? Spending Responses to Gains, Losses, News, and Loans Andreas Fuster Greg Kaplan Basit Zafar Staff Report No. 843 March 2018 This

Federal Reserve Bank of New York Staff Reports What Would You Do with $500? Spending Responses to Gains, Losses, News, and Loans Andreas Fuster Greg Kaplan Basit Zafar Staff Report No. 843 March 2018 This

Restoring Trust in Financial Markets: Why We Need Financial Literacy and Simple Portfolio Solutions

Restoring Trust in Financial Markets: Why We Need Financial Literacy and Simple Portfolio Solutions Tullio Jappelli Università di Napoli and CSEF Venice, 26 November 2008 What do we know? Often the quality

Restoring Trust in Financial Markets: Why We Need Financial Literacy and Simple Portfolio Solutions Tullio Jappelli Università di Napoli and CSEF Venice, 26 November 2008 What do we know? Often the quality

Chapter 13. Efficient Capital Markets and Behavioral Challenges

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Defined contribution retirement plan design and the role of the employer default

Trends and Issues October 2018 Defined contribution retirement plan design and the role of the employer default Chester S. Spatt, Carnegie Mellon University and TIAA Institute Fellow 1. Introduction An

Trends and Issues October 2018 Defined contribution retirement plan design and the role of the employer default Chester S. Spatt, Carnegie Mellon University and TIAA Institute Fellow 1. Introduction An

WORKING PAPER SERIES 2011-ECO-05

October 2011 WORKING PAPER SERIES 2011-ECO-05 Even (mixed) risk lovers are prudent David Crainich CNRS-LEM and IESEG School of Management Louis Eeckhoudt IESEG School of Management (LEM-CNRS) and CORE

October 2011 WORKING PAPER SERIES 2011-ECO-05 Even (mixed) risk lovers are prudent David Crainich CNRS-LEM and IESEG School of Management Louis Eeckhoudt IESEG School of Management (LEM-CNRS) and CORE

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application Vivek H. Dehejia Carleton University and CESifo Email: vdehejia@ccs.carleton.ca January 14, 2008 JEL classification code:

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application Vivek H. Dehejia Carleton University and CESifo Email: vdehejia@ccs.carleton.ca January 14, 2008 JEL classification code:

DOES MONEY BUY CREDIT? FIRM-LEVEL EVIDENCE ON BRIBERY AND BANK DEBT

DOES MONEY BUY CREDIT? FIRM-LEVEL EVIDENCE ON BRIBERY AND BANK DEBT Zuzana Fungáčová (Bank of Finland) Anna Kochanova (Max Planck Institute, Bonn) Laurent Weill (University of Strasbourg & Bank of Finland)

DOES MONEY BUY CREDIT? FIRM-LEVEL EVIDENCE ON BRIBERY AND BANK DEBT Zuzana Fungáčová (Bank of Finland) Anna Kochanova (Max Planck Institute, Bonn) Laurent Weill (University of Strasbourg & Bank of Finland)

Potential drivers of insurers equity investments

Potential drivers of insurers equity investments Petr Jakubik and Eveline Turturescu 67 Abstract As a consequence of the ongoing low-yield environment, insurers are changing their business models and looking

Potential drivers of insurers equity investments Petr Jakubik and Eveline Turturescu 67 Abstract As a consequence of the ongoing low-yield environment, insurers are changing their business models and looking