Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

|

|

|

- Ronald Wilson

- 6 years ago

- Views:

Transcription

1 Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

2 Return, Risk, and the Security Market Line Our goal in this chapter is to define risk more precisely, and discuss how to measure it. In addition, we will quantify the relation between risk and return in financial markets. 12-2

3 Expected and Unexpected Returns The return on any stock traded in a financial market is composed of two parts. The normal, or expected, part of the return is the return that investors predict or expect. The uncertain, or risky, part of the return comes from unexpected information revealed during the year. Total Return = Expected Return + Unexpected Return Unexpected Return = Total Return - Expected Return U = R - E(R) 12-3

4 Announcements and News Firms make periodic announcements about events that may significantly impact the profits of the firm. Earnings Product development Personnel The impact of an announcement depends on how much of the announcement represents new information. When the situation is not as bad as previously thought, what seems to be bad news is actually good news. When the situation is not as good as previously thought, what seems to be good news is actually bad news. News about the future is what really matters. Market participants factor predictions about the future into the expected part of the stock return. Announcement = Expected News + Surprise News 12-4

5 Systematic and Unsystematic Risk Systematic risk is risk that influences a large number of assets. Also called market risk. Unsystematic risk is risk that influences a single company or a small group of companies. Also called unique risk or firm-specific risk. Total risk = Systematic risk + Unsystematic risk 12-5

6 Systematic and Unsystematic Components of Return Recall: R E(R) = U = Systematic portion + Unsystematic portion = m + ε R E(R) = m + ε 12-6

7 Diversification and Risk In a large portfolio: Some stocks will go up in value because of positive companyspecific events, while Others will go down in value because of negative companyspecific events. Unsystematic risk is essentially eliminated by diversification, so a portfolio with many assets has almost no unsystematic risk. Unsystematic risk is also called diversifiable risk. Systematic risk is also called non-diversifiable risk. 12-7

8 The Systematic Risk Principle What determines the size of the risk premium on a risky asset? The systematic risk principle states: The expected return on an asset depends only on its systematic risk. So, no matter how much total risk an asset has, only the systematic portion is relevant in determining the expected return (and the risk premium) on that asset. 12-8

9 Measuring Systematic Risk To be compensated for risk, the risk has to be special. Unsystematic risk is not special. Systematic risk is special. The Beta coefficient (β) measures the relative systematic risk of an asset. Assets with Betas larger than 1.0 have more systematic risk than average. Assets with Betas smaller than 1.0 have less systematic risk than average. Because assets with larger betas have greater systematic risks, they will have greater expected returns. Note that not all Betas are created equally. 12-9

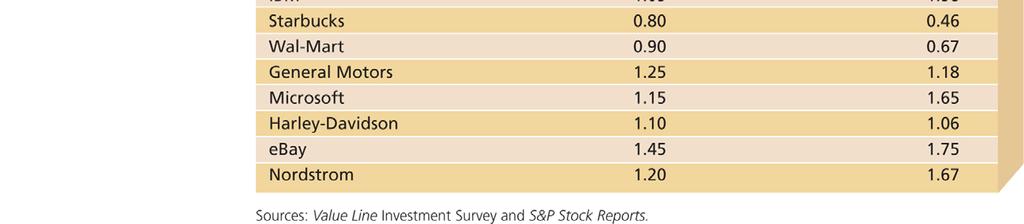

10 Published Beta Coefficients 12-10

11 Finding a Beta on the Web 12-11

12 Portfolio Betas The total risk of a portfolio has no simple relation to the total risk of the assets in the portfolio. Recall the variance of a portfolio equation For two assets, you need two variances and the covariance. For four assets, you need four variances, and six covariances. In contrast, a portfolio Beta can be calculated just like the expected return of a portfolio. That is, you can multiply each asset s Beta by its portfolio weight and then add the results to get the portfolio s Beta

13 Example: Calculating a Portfolio Beta Using data from Table 12.1, we see Beta for IBM is 1.05 Beta for ebay is 1.45 You put half your money into IBM and half into ebay. What is your portfolio Beta? β p =.50 β IBM +.50 β ebay = =

14 Beta and the Risk Premium, I. Consider a portfolio made up of asset A and a risk-free asset. For asset A, E(R A ) = 16% and β A = 1.6 The risk-free rate R f = 4%. Note that for a risk-free asset, β = 0 by definition. We can calculate some different possible portfolio expected returns and betas by changing the percentages invested in these two assets. Note that if the investor borrows at the risk-free rate and invests the proceeds in asset A, the investment in asset A will exceed 100%

15 Beta and the Risk Premium, II. % of Portfolio in Asset A 0% Portfolio Expected Return Portfolio Beta

16 Portfolio Expected Returns and Betas for Asset A 12-16

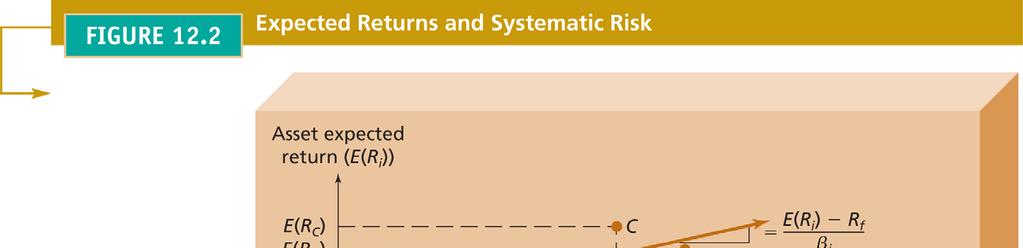

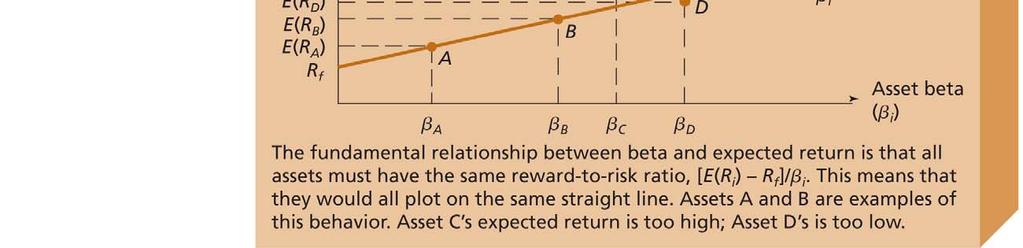

17 The Reward-to-Risk Ratio Notice that all the combinations of portfolio expected returns and betas fall on a straight line. Slope (Rise over Run): ( ) E R A = β A R f = 16% 4% 1.6 = 7.50% What this tells us is that asset A offers a reward-to-risk ratio of 7.50%. In other words, asset A has a risk premium of 7.50% per unit of systematic risk

18 The Basic Argument, I. Recall that for asset A: E(R A ) = 16% and β A = 1.6 Suppose there is a second asset, asset B. For asset B: E(R B ) = 12% and β A = 1.2 Which investment is better, asset A or asset B? Asset A has a higher expected return Asset B has a lower systematic risk measure 12-18

19 The Basic Argument, II As before with Asset A, we can calculate some different possible portfolio expected returns and betas by changing the percentages invested in asset B and the risk-free rate. % of Portfolio in Asset B 0% Portfolio Expected Return Portfolio Beta

20 Portfolio Expected Returns and Betas for Asset B 12-20

21 Portfolio Expected Returns and Betas for Both Assets 12-21

22 The Fundamental Result, I. The situation we have described for assets A and B cannot persist in a well-organized, active market Investors will be attracted to asset A (and buy A shares) Investors will shy away from asset B (and sell B shares) This buying and selling will make The price of A shares increase The price of B shares decrease This price adjustment continues until the two assets plot on exactly the same line. That is, until: E ( R ) R E( R ) A β A f = B β B R f 12-22

23 The Fundamental Result, II. In general The reward-to-risk ratio must be the same for all assets in a competitive financial market. If one asset has twice as much systematic risk as another asset, its risk premium will simply be twice as large. Because the reward-to-risk ratio must be the same, all assets in the market must plot on the same line

24 The Fundamental Result, III

25 The Security Market Line (SML) The Security market line (SML) is a graphical representation of the linear relationship between systematic risk and expected return in financial markets. For a market portfolio, = = ( ) R E( R ) E R M M ( M ) R f E R β f = M 1 R f 12-25

26 The Security Market Line, II. The term E(R M ) R f is often called the market risk premium because it is the risk premium on a market portfolio. For any asset i in the market: ( ) E R i β R i f = ( M ) R f E R ( R ) [ ( ) ] i = R f + E R M R f βi E Setting the reward-to-risk ratio for all assets equal to the market risk premium results in an equation known as the capital asset pricing model

27 The Security Market Line, III. The Capital Asset Pricing Model (CAPM) is a theory of risk and return for securities on a competitive capital market. ( R ) [ ( ) ] i = R f + E R M R f βi E The CAPM shows that E(R i ) depends on: R f, the pure time value of money. E(R M ) R f, the reward for bearing systematic risk. β i, the amount of systematic risk

28 The Security Market Line, IV

29 Risk and Return Summary, I

30 Risk and Return Summary, II

31 A Closer Look at Beta R E(R) = m + ε, where m is the systematic portion of the unexpected return. m = β [R M E(R M )] So, R E(R) = β [R M E(R M )] + ε In other words: A high-beta security is simply one that is relatively sensitive to overall market movements A low-beta security is one that is relatively insensitive to overall market movements

32 Decomposition of Total Returns 12-32

33 Unexpected Returns and Beta 12-33

34 Where Do Betas Come From? A security s Beta depends on: How closely correlated the security s return is with the overall market s return, and How volatile the security is relative to the market. A security s Beta is equal to the correlation multiplied by the ratio of the standard deviations. ( R,R ) β = Corr i i M σ σ i m 12-34

35 Where Do Betas Come From? 12-35

36 Using a Spreadsheet to Calculate Beta Using a Spreadsheet to Calculate Beta To illustrate how to calculate betas, correlations, and covariances using a spreadsheet, we have entered the information from Table 12.4 into the spreadsheet below. Here, we use Excel functions to do all the calculations. Returns Security Market % 8% % -12% % 16% % 26% % 22% Note: The Excel Format is set to percent, but the numbers are entered as decimals. Average: 10% 12% (Using the =AVERAGE function) Std. Dev.: 18.87% 15.03% (Using the =STDEV function) Correlation: 0.72 =CORREL(D10:D14,E10:E14) Beta: 0.90 Excel also has a covariance function, =COVAR, but we do not use it because it divides by n instead of n-1. Verify that you get a Beta of about 0.72 if you use the COVAR function divided by the variance of the Market Returns (Use the Excel function, =VAR)

37 Why Do Betas Differ? Betas are estimated from actual data. Different sources estimate differently, possibly using different data. For data, the most common choices are three to five years of monthly data, or a single year of weekly data. To measure the overall market, the S&P 500 stock market index is commonly used. The calculated betas may be adjusted for various statistical reasons

38 Extending CAPM The CAPM has a stunning implication: What you earn on your portfolio depends only on the level of systematic risk that you bear As a diversified investor, you do not need to worry about total risk, only systematic risk. But, does expected return depend only on Beta? Or, do other factors come into play? The above bullet point is a hotly debated question

39 Important General Risk-Return Principles Investing has two dimensions: risk and return. It is inappropriate to look at the total risk of an individual security. It is appropriate to look at how an individual security contributes to the risk of the overall portfolio Risk can be decomposed into nonsystematic and systematic risk. Investors will be compensated only for systematic risk

40 The Fama-French Three-Factor Model Professors Gene Fama and Ken French argue that two additional factors should be added. In addition to beta, two other factors appear to be useful in explaining the relationship between risk and return. Size, as measured by market capitalization The book value to market value ratio, i.e., B/M Whether these two additional factors are truly sources of systematic risk is still being debated

41 Returns from 25 Portfolios Formed on Size and Book-to-Market Note that the portfolio containing the smallest cap and the highest book-to-market have had the highest returns

42 Useful Internet Sites (visit the earnings calendar) earnings.nasdaq.com (to see recent earnings surprises) (helps you analyze risk) (another source for betas) finance.yahoo.com (a terrific source of financial information) (for information on risk management) (for a CAPM calculator) (source for data behind the FAMA-French model) money.cnn.com

43 Chapter Review, I. Announcements, Surprises, and Expected Returns Expected and unexpected returns Announcements and news Risk: Systematic and Unsystematic Systematic and unsystematic risk Systematic and unsystematic components of return Diversification, Systematic Risk, and Unsystematic Risk Diversification and unsystematic risk Diversification and systematic risk Systematic Risk and Beta The systematic risk principle Measuring systematic risk Portfolio Betas 12-43

44 Chapter Review, II. The Security Market Line Beta and the risk premium The reward-to-risk ratio The basic argument The fundamental result The Security Market Line More on Beta A closer look at Beta Where do Betas come from? Why do Betas differ? Extending CAPM A (very) Brief History of Testing CAPM The Fama-French three-factor model 12-44

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

Risk and Return - Capital Market Theory. Chapter 8

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

Risk and Return - Capital Market Theory. Chapter 8

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Chapter. Diversification and Risky Asset Allocation. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Financial Markets. Laurent Calvet. John Lewis Topic 13: Capital Asset Pricing Model (CAPM)

") Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

Solutions to the problems in the supplement are found at the end of the supplement

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Return, Risk, and the Security Market Line

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Return, Risk, and the Security Market Line

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

Capital Asset Pricing Model - CAPM

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

CHAPTER 8 Risk and Rates of Return

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

Define risk, risk aversion, and riskreturn

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

Asset Pricing Model 2

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

FIN Chapter 8. Risk and Return: Capital Asset Pricing Model. Liuren Wu

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Module 3: Factor Models

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Note 11. Portfolio Return and Risk, and the Capital Asset Pricing Model

Note 11 Portfolio Return and Risk, and the Capital Asset Pricing Model Outline Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing

Note 11 Portfolio Return and Risk, and the Capital Asset Pricing Model Outline Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Statistically Speaking

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

The Capital Asset Pricing Model CAPM: benchmark model of the cost of capital

70391 - Finance The Capital Asset Pricing Model CAPM: benchmark model of the cost of capital 70391 Finance Fall 2016 Tepper School of Business Carnegie Mellon University c 2016 Chris Telmer. Some content

70391 - Finance The Capital Asset Pricing Model CAPM: benchmark model of the cost of capital 70391 Finance Fall 2016 Tepper School of Business Carnegie Mellon University c 2016 Chris Telmer. Some content

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Microéconomie de la finance

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Performance Measurement and Attribution in Asset Management

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

Chapter 10. Chapter 10 Topics. What is Risk? The big picture. Introduction to Risk, Return, and the Opportunity Cost of Capital

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

Chapter 11. Topics Covered. Chapter 11 Objectives. Risk, Return, and Capital Budgeting

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

MBA 203 Executive Summary

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Uniwersytet Ekonomiczny. George Matysiak. Presentation outline. Motivation for Performance Analysis

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Chapter 12 RISK & RETURN: PORTFOLIO APPROACH. Alex Tajirian

Chapter 12 RISK & RETURN: PORTFOLIO APPROACH Alex Tajirian Risk & Return: Portfolio Approach 12-2 1. OBJECTIVE! What type of risk do investors care about? Is it "volatility"?...! What is the risk premium

Chapter 12 RISK & RETURN: PORTFOLIO APPROACH Alex Tajirian Risk & Return: Portfolio Approach 12-2 1. OBJECTIVE! What type of risk do investors care about? Is it "volatility"?...! What is the risk premium

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Use partial derivatives just found, evaluate at a = 0: This slope of small hyperbola must equal slope of CML:

Derivation of CAPM formula, contd. Use the formula: dµ σ dσ a = µ a µ dµ dσ = a σ. Use partial derivatives just found, evaluate at a = 0: Plug in and find: dµ dσ σ = σ jm σm 2. a a=0 σ M = a=0 a µ j µ

Derivation of CAPM formula, contd. Use the formula: dµ σ dσ a = µ a µ dµ dσ = a σ. Use partial derivatives just found, evaluate at a = 0: Plug in and find: dµ dσ σ = σ jm σm 2. a a=0 σ M = a=0 a µ j µ

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Chapter 13 Return, Risk, and the Security Market Line

Chapter 13 Return, Risk, and the Security Market Line 1. You own a stock that you think will produce a return of 11 percent in a good economy and 3 percent in a poor economy. Given the probabilities of

Chapter 13 Return, Risk, and the Security Market Line 1. You own a stock that you think will produce a return of 11 percent in a good economy and 3 percent in a poor economy. Given the probabilities of

University of Texas at Dallas School of Management. Investment Management Spring Estimation of Systematic and Factor Risks (Due April 1)

") University of Texas at Dallas School of Management Finance 6310 Professor Day Investment Management Spring 2008 Estimation of Systematic and Factor Risks (Due April 1) This assignment requires you to perform

University of Texas at Dallas School of Management Finance 6310 Professor Day Investment Management Spring 2008 Estimation of Systematic and Factor Risks (Due April 1) This assignment requires you to perform

When we model expected returns, we implicitly model expected prices

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

CHAPTER 6: PORTFOLIO SELECTION

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

Example 1 of econometric analysis: the Market Model

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

The Effect of Kurtosis on the Cross-Section of Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

CHAPTER 8: INDEX MODELS

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

Analysis INTRODUCTION OBJECTIVES

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

FEEDBACK TUTORIAL LETTER ASSIGNMENT 1 AND 2 MANAGERIAL FINANCE 4B MAF412S

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 AND 2 MANAGERIAL FINANCE 4B MAF412S 1 ASSIGNMENT 1 QUESTION 1 (i) Investment A at end of Year 3: Year 4 5 6 7 8 Cash flows 1 000 1 000 1 000 1 000

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 AND 2 MANAGERIAL FINANCE 4B MAF412S 1 ASSIGNMENT 1 QUESTION 1 (i) Investment A at end of Year 3: Year 4 5 6 7 8 Cash flows 1 000 1 000 1 000 1 000

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Diversification. Finance 100

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty

![ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty](/thumbs/83/88403560.jpg "ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty") ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015 Reading Chapters 11 13, not Appendices Chapter 11 Skip 11.2 Mean variance optimization in practice

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015 Reading Chapters 11 13, not Appendices Chapter 11 Skip 11.2 Mean variance optimization in practice

All else equal, people dislike risk.

All else equal, people like returns. All else equal, people dislike risk. On October 7, 07, Home Depot stock closed at $64.. It paid dividends of $0.89 per share on November 9, 07, and $.03 per share on

All else equal, people like returns. All else equal, people dislike risk. On October 7, 07, Home Depot stock closed at $64.. It paid dividends of $0.89 per share on November 9, 07, and $.03 per share on

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INVESTMENT PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

Risk and Risk Aversion

Risk and Risk Aversion Do markets price in new information? Refer to spreadsheet Risk.xls ci Price of a financial asset will be the present value of future cash flows. PV i 1 (1 Rs ) (where c i = are the

Risk and Risk Aversion Do markets price in new information? Refer to spreadsheet Risk.xls ci Price of a financial asset will be the present value of future cash flows. PV i 1 (1 Rs ) (where c i = are the

Chapter 7 Capital Asset Pricing and Arbitrage Pricing Theory

Chapter 7 Capital Asset ricing and Arbitrage ricing Theory 1. a, c and d 2. a. E(r X ) = 12.2% X = 1.8% E(r Y ) = 18.5% Y = 1.5% b. (i) For an investor who wants to add this stock to a well-diversified

Chapter 7 Capital Asset ricing and Arbitrage ricing Theory 1. a, c and d 2. a. E(r X ) = 12.2% X = 1.8% E(r Y ) = 18.5% Y = 1.5% b. (i) For an investor who wants to add this stock to a well-diversified

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

INVESTMENTS Lecture 2: Measuring Performance

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

A Portfolio s Risk - Return Analysis

A Portfolio s Risk - Return Analysis 1 Table of Contents I. INTRODUCTION... 4 II. BENCHMARK STATISTICS... 5 Capture Indicators... 5 Up Capture Indicator... 5 Down Capture Indicator... 5 Up Number ratio...

A Portfolio s Risk - Return Analysis 1 Table of Contents I. INTRODUCTION... 4 II. BENCHMARK STATISTICS... 5 Capture Indicators... 5 Up Capture Indicator... 5 Down Capture Indicator... 5 Up Number ratio...

CAPITAL ASSET PRICING AND ARBITRAGE PRICING THEORY

II. Portfolio 7 CAPITAL ASSET PRICING AND ARBITRAGE PRICING THEORY AFTER STUDYING THIS CHAPTER YOU SHOULD BE ABLE TO: Use the implications of capital market theory to compute security risk premiums. Construct

II. Portfolio 7 CAPITAL ASSET PRICING AND ARBITRAGE PRICING THEORY AFTER STUDYING THIS CHAPTER YOU SHOULD BE ABLE TO: Use the implications of capital market theory to compute security risk premiums. Construct

Note on Cost of Capital

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

Behavioral Finance 1-1. Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships

Behavioral Finance 1-1 Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships 1 The Pricing of Risk 1-2 The expected utility theory : maximizing the expected utility across possible states

Behavioral Finance 1-1 Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships 1 The Pricing of Risk 1-2 The expected utility theory : maximizing the expected utility across possible states

The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Risk and Return (Introduction) Professor: Burcu Esmer

Professor: Burcu Esmer") Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

Understanding Risk and Return, the CAPM, and the Fama-French Three-Factor Model

no. 1-20 No. 03-111 Understanding Risk and Return, the CPM, and the Fama-French Three-Factor Model RISK ND RETURN The General Concept: Higher Expected Returns Require Taking Higher Risk Most investors

no. 1-20 No. 03-111 Understanding Risk and Return, the CPM, and the Fama-French Three-Factor Model RISK ND RETURN The General Concept: Higher Expected Returns Require Taking Higher Risk Most investors