Note 11. Portfolio Return and Risk, and the Capital Asset Pricing Model

|

|

|

- Muriel Randall

- 5 years ago

- Views:

Transcription

The Capital Asset Pricing Model and the Security Market Line The Security Market Line and Securities Pricing The Security Market Line and Capital Budgeting 2")

1 Note 11 Portfolio Return and Risk, and the Capital Asset Pricing Model Outline Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line The Security Market Line and Securities Pricing The Security Market Line and Capital Budgeting 2 1

2 Risk Aversion It is generally believed that investors prefer an investment with a higher expected return (to an investment with a lower return) and an investment with lower risk (to an investment with higher risk). Such an investment attitude is called risk aversion. Risk aversion is an attitude to avoid risk unless a sufficient amount of compensation (in return) is provided. 3 Exercise: Expected Return and Variance Investment in Single Assets Example) Calculate the expected returns, variances, and standard deviations of A and B. State of economy Probability of state Return on asset A Return on asset B Expansion % -5% Recession % 25% 1.00 To a risk-averse investor, which investment is better? 4 2

3 Exercise: Expected Return and Variance Investment in Single Assets For A, E(r A ) = (0.4)(0.3) + (0.6)(-0.1) = 0.06 Var(r A ) = (0.4)( ) 2 + (0.6)( ) 2 = S.D.(r A ) = [0.0384] 1/2 = For B, E(r A ) = (0.4)(-0.05) + (0.6)(0.25) = 0.13 Var(r A ) = (0.4)( ) 2 + (0.6)( ) 2 = S.D.(r A ) = [0.0216] 1/2 = Comparison between Stock A and Stock B Stock A Stock B E(r)

4 Comparison between Stock A and Stock B E(r) B (14.7%, 13%) A (19.6%, 6%) (Risk) 7 Portfolios A portfolio is a collection of assets An asset s risk and return are important in how they affect the risk and return of the portfolio The risk-return trade-off for a portfolio is measured by the portfolio expected return and standard deviation, just as with individual assets 8 4

5 Portfolio Returns Portfolio return is the weighted average of the return from each component asset of the portfolio, where the weights are the percentage of money invested in each asset. Thus, if a portfolio consists of two securities, A and B, and A s contribution to the portfolio is 40% while B s is 60%, then the portfolio s return is: r portfolio = (0.4)*(r A ) + (0.6)*(r B ) 9 Example: Expected Return and Variance Investment in a Portfolio Consider the case where you invest 50% of your money in Asset A and 50% in B (Let s call the new investment portfolio AB). State Probability A B Expans..4 30% -5% Recess..6-10% 25% Portfolio AB 12.5% 7.5% when expansion, r AB = (0.5)(0.3) + (0.5)(-0.05) = when recession, r AB = (0.5)(-0.1) + (0.5)(0.25) =

6 Exercise: Expected Return and Variance Investment in a Portfolio What is the expected return and standard deviation for the portfolio? (hint: we just treat the portfolio as if it were another stock) State Probability Port. AB Boom % Bust.6 7.5% E(r P ) = (0.4)(0.125) + (0.6)(0.075) = Var(r P ) = (0.4)( ) 2 + (0.6)( ) 2 = S.D.(r P ) = [0.0006] 1/2 = Comparison between Stock A, Stock B, and Portfolio Stock A Stock B Portfolio E(r)

7 Comparison between Portfolio and Individual Stocks E(r) B (14.7%, 13%) P (2.5%, 9.5%) A (19.6%, 6%) (Risk) 13 Portfolio Risk: One Plus One is Not Two Stock A returns Stock B returns Portfolio returns: 50% A and 50% B

Risk of Portfolio Number")

8 Portfolio Size and Risk 15 But Why? Risk (Portfolio standard deviation) Risk of Portfolio Number of stocks in portfolio 16 8

(2) Unsystematic Risk: Risk due to firm specific factors (also called unique")

9 Total Risk and Its Components The standard deviation of returns is a measure of total risk Total Risk is the sum of Systematic Risk and Unsystematic Risk Two Components of Total Risk (1) Systematic Risk: Risk due to market wide, macroeconomic factors (also called market risk, systematic risk, non-diversifiable risk) (2) Unsystematic Risk: Risk due to firm specific factors (also called unique risk, firm-specific risk, diversifiable risk) 17 Example: Market wide information event 18 9

10 19 Example: Firm-specific information event 20 10

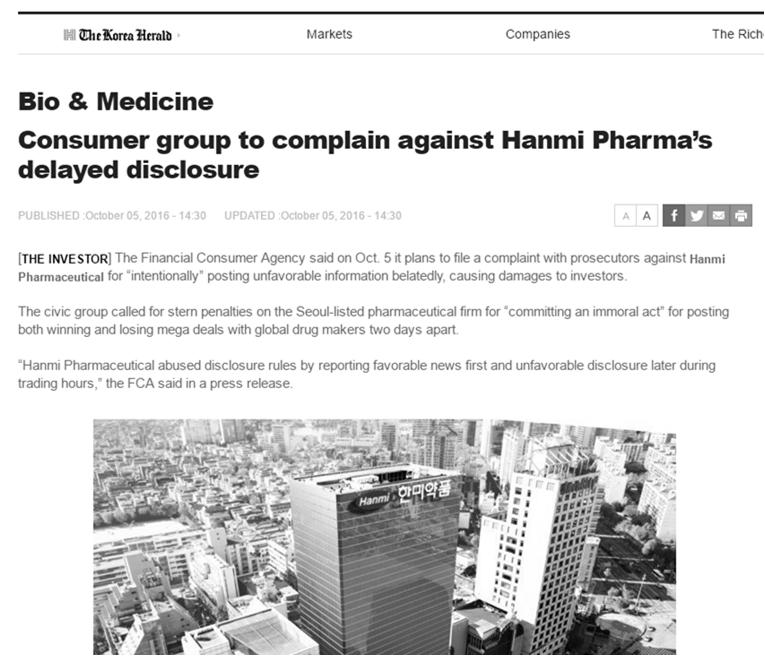

11 Disappointed by Boehringer s contract termination, Hanmi shares plummeted 24 percent during two trading sessions on Sept. 30 and Oct. 4, after the firm s stock price spiked nearly 5 percent on a disclosure made on Sept. 29 that it had clinched a 1 trillion won deal with Genentech, a member of Roche Group. 21 Portfolio Diversification You can eliminate the risk component due to firm-specific factors by including sufficiently large number of securities in your portfolio but the risk component due to the market wide factors still remain. Risk Total risk Unsystematic Risk, Firm-Specific Risk Systematic risk, Market Risk Portfolio Size 22 11

12 The Principle of Diversification Diversification can substantially reduce the variability of returns without an equivalent reduction in expected returns This reduction in risk arises because worse than expected returns from one asset are offset by better than expected returns from another However, there is a minimum level of risk that cannot be diversified away and that is the systematic portion For well-diversified portfolios, unsystematic risk is very small and, consequently, the total risk for a diversified portfolio is essentially equivalent to the systematic risk 23 Systematic Risk Principle There is a reward for bearing risk There is not a reward for bearing risk unnecessarily Unsystematic risk easily avoidable The expected return on a risky asset depends only on that asset s systematic risk since unsystematic risk can be diversified away 24 12

13 Measuring Systematic Risk How do we measure systematic risk? We use the beta coefficient ( ) to measure systematic risk How is beta measured? For Security A, The denominator in the above expression is the covariance between an individual security (e.g.: Security A above) and the market as a whole (market portfolio). The numerator is the variance of the market portfolio 25 What does tell us? (beta) measures the sensitivity (systematic movement) of stock A's return to the market movement. A beta of 1 implies the asset has the same systematic risk as the overall market A beta < 1 implies the asset has less systematic risk than the overall market A beta > 1 implies the asset has more systematic risk than the overall market 26 13

14 Beta Values: Examples (U.S.) Kraft Food: 0.06 Merck & Co.: 0.38 Exxon Mobil: 0.86 Microsoft: 1.17 Harley-Davidson: 1.58 The Goldman Sachs Group: 1.59 Abercrombie & Fitch: 1.9 MGM Resorts International: Some Beta Examples: Korea Exchange (Monthly Data Used, ) TS Corp. (Food & Bev.): Hyundai Steel (Steel): Samsung Electronics (Elec.): Nexen Tire (Mftg.-Auto): SK E&S (Utility - Gas) : 28 14

15 Total versus Systematic Risk Consider the following information: Standard Deviation Beta Security C 20% 1.25 Security K 30% 0.95 Which security has more total risk? Which security has more systematic risk? Which security should have the higher expected return? 29 Beta and the Risk Premium Remember : risk premium = expected return risk-free rate The higher the beta, the greater the risk premium Can we define the relationship between the risk premium and beta so that we can estimate the expected return? YES! 30 15

16 Capital Asset Pricing Model (CAPM) Stock returns show very systematic relationship with the market returns. E(r i ) r f = i [E(r m ) r f ] By moving r f to the L.H.S., we get E(r i ) = r f + i [E(r m ) r f ] E(r i ) Expected return on an individual security or portfolio r f Risk-free rate E(r M ) The average expected return on the whole market I The systematic risk of the individual security or portfolio In other words, the expected return of a stock is the sum of the risk-free rate and the market risk premium multiplied by the stock s beta. (beta) measures the sensitivity of stock i's return to the market risk premium (market movement). 31 Factors Affecting Expected Return Pure time value of money measured by the risk-free rate Reward for bearing systematic risk measured by the market risk premium Amount of systematic risk measured by beta E(r i ) = r f + i [E(r m ) r f ] 32 16

17 The Security Market Line (SML) Graphical illustration of the CAPM E(r) E(r i ) = r f + [E(r m ) r f ] i E(r M ) SML E(r M ) r F r f M 33 Example - CAPM Consider the betas for each of the assets given earlier. If the risk-free rate is 4.5% and the market risk premium is 8.5%, what is the expected return for each? Security Beta Expected Return DKNI (8.5) = % UBM (8.5) = 9.940% AAR (8.5) = % QTRI (8.5) = % 34 17

18 Capital Asset Pricing Model Developed by researchers including W. Sharpe * (1964) and J. Linter (1965). The CAPM provides us with a precise prediction of the relation between the risk of an asset and its expected return. The model also provides a benchmark required rate of return for evaluating possible investments. * Nobel economics prize winner in CAPM Application: Real Cases Risk-free rate (91-Day CD, End of July. 2017) = 1.65% Market risk premium (Based on Rating) = 7.03% Hyundai Steel Beta = 1.54 E(R HDS ) = Samsung Elec. = 0.89 E(R SSE ) = TS Corporate ( 대한제당 ) = 0.17 E(R TS ) = 18

19 An Important Lesson from the SML The security market line tells us the reward for bearing risk in financial markets. At an absolute minimum, any new investment our firm undertakes must offer an expected return that is no worse than what the financial markets offer for the same risk. If not, what will happen? Simply investors can always invest for themselves in the financial markets. This lesson has important meaning for capital budgeting

Asset Pricing Model 2

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

Chapter 13 Return, Risk, and the Security Market Line

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

Return, Risk, and the Security Market Line

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Statistically Speaking

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

CHAPTER 10 SOME LESSONS FROM CAPITAL MARKET HISTORY

CHAPTER 10 SOME LESSONS FROM CAPITAL MARKET HISTORY Answers to Concepts Review and Critical Thinking Questions 3. No, stocks are riskier. Some investors are highly risk averse, and the extra possible return

CHAPTER 10 SOME LESSONS FROM CAPITAL MARKET HISTORY Answers to Concepts Review and Critical Thinking Questions 3. No, stocks are riskier. Some investors are highly risk averse, and the extra possible return

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

All else equal, people dislike risk.

All else equal, people like returns. All else equal, people dislike risk. On October 7, 07, Home Depot stock closed at $64.. It paid dividends of $0.89 per share on November 9, 07, and $.03 per share on

All else equal, people like returns. All else equal, people dislike risk. On October 7, 07, Home Depot stock closed at $64.. It paid dividends of $0.89 per share on November 9, 07, and $.03 per share on

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 8 Risk and Rates of Return

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD PROBLEM SETS 1. The Fisher equation predicts that the nominal rate will equal the equilibrium real rate plus the expected inflation

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD PROBLEM SETS 1. The Fisher equation predicts that the nominal rate will equal the equilibrium real rate plus the expected inflation

Risk and Return - Capital Market Theory. Chapter 8

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

Risk and Return - Capital Market Theory. Chapter 8

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

When we model expected returns, we implicitly model expected prices

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Chapter 10. Chapter 10 Topics. What is Risk? The big picture. Introduction to Risk, Return, and the Opportunity Cost of Capital

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

Risk and Return (Introduction) Professor: Burcu Esmer

Professor: Burcu Esmer") Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

FNCE 4030 Fall 2012 Roberto Caccia, Ph.D. Midterm_2a (2-Nov-2012) Your name:

Your name:") Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Financial Markets 11-1

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 11: Measuring Financial Risk HEC MBA Financial Markets 11-1 Risk There are many types of risk in financial transactions

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 11: Measuring Financial Risk HEC MBA Financial Markets 11-1 Risk There are many types of risk in financial transactions

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Define risk, risk aversion, and riskreturn

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Uniwersytet Ekonomiczny. George Matysiak. Presentation outline. Motivation for Performance Analysis

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Solutions to the problems in the supplement are found at the end of the supplement

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 6

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 6 MVO IN TWO STAGES Calculate the forecasts Calculate forecasts for returns, standard deviations and correlations for the

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 6 MVO IN TWO STAGES Calculate the forecasts Calculate forecasts for returns, standard deviations and correlations for the

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below:

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

- P P THE RELATION BETWEEN RISK AND RETURN. Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Capital Asset Pricing Model

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar. L7 Portfolio and Risk Management

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk, return, and diversification

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

Chapter 11. Topics Covered. Chapter 11 Objectives. Risk, Return, and Capital Budgeting

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

Port(A,B) is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.

is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.") Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Chapter 7. Speculation and Risk in the Foreign Exchange Market Cambridge University Press 7-1

Chapter 7 Speculation and Risk in the Foreign Exchange Market 2018 Cambridge University Press 7-1 7.1 Speculating in the Foreign Exchange Market Uncovered foreign money market investments Kevin Anthony,

Chapter 7 Speculation and Risk in the Foreign Exchange Market 2018 Cambridge University Press 7-1 7.1 Speculating in the Foreign Exchange Market Uncovered foreign money market investments Kevin Anthony,

CHAPTER 1 AN OVERVIEW OF THE INVESTMENT PROCESS

CHAPTER 1 AN OVERVIEW OF THE INVESTMENT PROCESS TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T 2. An investment

CHAPTER 1 AN OVERVIEW OF THE INVESTMENT PROCESS TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T 2. An investment

MBA 203 Executive Summary

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Analysis INTRODUCTION OBJECTIVES

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Chapter 10: Capital Markets and the Pricing of Risk

Chapter 10: Capital Markets and the Pricing of Risk -1 Chapter 10: Capital Markets and the Pricing of Risk Fundamental question: What is the relationship between risk and return in a more complex world

Chapter 10: Capital Markets and the Pricing of Risk -1 Chapter 10: Capital Markets and the Pricing of Risk Fundamental question: What is the relationship between risk and return in a more complex world

RETURN, RISK, AND THE SECURITY MARKET LINE

RETURN, RISK, AND THE SECURITY MARKET LINE 13 On July 20, 2006, Apple Computer, Honeywell, and Yum Brands joined a host of other companies in announcing earnings. All three companies announced earnings

RETURN, RISK, AND THE SECURITY MARKET LINE 13 On July 20, 2006, Apple Computer, Honeywell, and Yum Brands joined a host of other companies in announcing earnings. All three companies announced earnings

Financial Strategy First Test

Financial Strategy First Test 1. The difference between the market value of an investment and its cost is the: A) Net present value. B) Internal rate of return. C) Payback period. D) Profitability index.

Financial Strategy First Test 1. The difference between the market value of an investment and its cost is the: A) Net present value. B) Internal rate of return. C) Payback period. D) Profitability index.

Chapter 6 Efficient Diversification. b. Calculation of mean return and variance for the stock fund: (A) (B) (C) (D) (E) (F) (G)

(B) (C) (D) (E) (F) (G)") Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar. L7 Portfolio and Risk Management

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

Chapter 7 Capital Asset Pricing and Arbitrage Pricing Theory

Chapter 7 Capital Asset ricing and Arbitrage ricing Theory 1. a, c and d 2. a. E(r X ) = 12.2% X = 1.8% E(r Y ) = 18.5% Y = 1.5% b. (i) For an investor who wants to add this stock to a well-diversified

Chapter 7 Capital Asset ricing and Arbitrage ricing Theory 1. a, c and d 2. a. E(r X ) = 12.2% X = 1.8% E(r Y ) = 18.5% Y = 1.5% b. (i) For an investor who wants to add this stock to a well-diversified

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

Chapter 10: Capital Markets and the Pricing of Risk

Chapter 0: Capital Markets and the Pricing of Risk- Chapter 0: Capital Markets and the Pricing of Risk Big Picture: ) To value a project, we need an interest rate to calculate present values ) The interest

Chapter 0: Capital Markets and the Pricing of Risk- Chapter 0: Capital Markets and the Pricing of Risk Big Picture: ) To value a project, we need an interest rate to calculate present values ) The interest

FIN3043 Investment Management. Assignment 1 solution

FIN3043 Investment Management Assignment 1 solution Questions from Chapter 1 9. Lanni Products is a start-up computer software development firm. It currently owns computer equipment worth $30,000 and has

FIN3043 Investment Management Assignment 1 solution Questions from Chapter 1 9. Lanni Products is a start-up computer software development firm. It currently owns computer equipment worth $30,000 and has

Harvard Business School Diversification, the Capital Asset Pricing Model, and the Cost of Equity Capital

Harvard Business School 9-276-183 Rev. November 10, 1993 Diversification, the Capital Asset Pricing Model, and the Cost of Equity Capital Risk as Variability in Return The rate of return an investor receives

Harvard Business School 9-276-183 Rev. November 10, 1993 Diversification, the Capital Asset Pricing Model, and the Cost of Equity Capital Risk as Variability in Return The rate of return an investor receives

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Calculating EAR and continuous compounding: Find the EAR in each of the cases below.

Problem Set 1: Time Value of Money and Equity Markets. I-III can be started after Lecture 1. IV-VI can be started after Lecture 2. VII can be started after Lecture 3. VIII and IX can be started after Lecture

Problem Set 1: Time Value of Money and Equity Markets. I-III can be started after Lecture 1. IV-VI can be started after Lecture 2. VII can be started after Lecture 3. VIII and IX can be started after Lecture

J B GUPTA CLASSES , Copyright: Dr JB Gupta. Chapter 4 RISK AND RETURN.

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 4 RISK AND RETURN Chapter Index Systematic and Unsystematic Risk Capital Asset Pricing Model

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 4 RISK AND RETURN Chapter Index Systematic and Unsystematic Risk Capital Asset Pricing Model

Chapter 12 RISK & RETURN: PORTFOLIO APPROACH. Alex Tajirian

Chapter 12 RISK & RETURN: PORTFOLIO APPROACH Alex Tajirian Risk & Return: Portfolio Approach 12-2 1. OBJECTIVE! What type of risk do investors care about? Is it "volatility"?...! What is the risk premium

Chapter 12 RISK & RETURN: PORTFOLIO APPROACH Alex Tajirian Risk & Return: Portfolio Approach 12-2 1. OBJECTIVE! What type of risk do investors care about? Is it "volatility"?...! What is the risk premium

Chapter 13 Portfolio Theory questions

Chapter 13 Portfolio Theory 15-20 questions 175 176 2. Portfolio Considerations Key factors Risk Liquidity Growth Strategies Stock selection - Fundamental analysis Use of fundamental data on the company,

Chapter 13 Portfolio Theory 15-20 questions 175 176 2. Portfolio Considerations Key factors Risk Liquidity Growth Strategies Stock selection - Fundamental analysis Use of fundamental data on the company,

Risks and Rate of Return

Risks and Rate of Return Definition of Risk Risk is a chance of financial loss or the variability of returns associated with a given asset A $1000 holder government bond guarantees its holder $5 interest

Risks and Rate of Return Definition of Risk Risk is a chance of financial loss or the variability of returns associated with a given asset A $1000 holder government bond guarantees its holder $5 interest

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Essential Performance Metrics to Evaluate and Interpret Investment Returns. Wealth Management Services

Essential Performance Metrics to Evaluate and Interpret Investment Returns Wealth Management Services Alpha, beta, Sharpe ratio: these metrics are ubiquitous tools of the investment community. Used correctly,

Essential Performance Metrics to Evaluate and Interpret Investment Returns Wealth Management Services Alpha, beta, Sharpe ratio: these metrics are ubiquitous tools of the investment community. Used correctly,

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

B6302 Sample Placement Exam Academic Year

Revised June 011 B630 Sample Placement Exam Academic Year 011-01 Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized units). Fund

Revised June 011 B630 Sample Placement Exam Academic Year 011-01 Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized units). Fund

Microéconomie de la finance

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Chapter 5: Answers to Concepts in Review

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

Finance 100: Corporate Finance. Professor Michael R. Roberts Quiz 3 November 8, 2006

Finance 100: Corporate Finance Professor Michael R. Roberts Quiz 3 November 8, 006 Name: Solutions Section ( Points...no joke!): Question Maximum Student Score 1 30 5 3 5 4 0 Total 100 Instructions: Please

Finance 100: Corporate Finance Professor Michael R. Roberts Quiz 3 November 8, 006 Name: Solutions Section ( Points...no joke!): Question Maximum Student Score 1 30 5 3 5 4 0 Total 100 Instructions: Please

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

THE OBJECTIVE OF RISK MANAGEMENT

THE OBJECTIVE OF RISK MANAGEMENT Risk Management Suppose the firm is closely owned Proprietorship Partnership Privately held corporation Suppose the owner(s) are risk averse Risk management can make owners

THE OBJECTIVE OF RISK MANAGEMENT Risk Management Suppose the firm is closely owned Proprietorship Partnership Privately held corporation Suppose the owner(s) are risk averse Risk management can make owners

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Homework #4 Suggested Solutions

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management. RSM332 FINAL EXAMINATION Geoffrey/Wang SOLUTIONS. (1 + r m ) r m

r m") UNIVERSITY OF TORONTO Joseph L. Rotman School of Management Dec. 9, 206 Burke/Corhay/Kan RSM332 FINAL EXAMINATION Geoffrey/Wang SOLUTIONS. (a) We first figure out the effective monthly interest rate, r

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management Dec. 9, 206 Burke/Corhay/Kan RSM332 FINAL EXAMINATION Geoffrey/Wang SOLUTIONS. (a) We first figure out the effective monthly interest rate, r

Chilton Investment Seminar

Chilton Investment Seminar Palm Beach, Florida - March 30, 2006 Applied Mathematics and Statistics, Stony Brook University Robert J. Frey, Ph.D. Director, Program in Quantitative Finance Objectives Be

Chilton Investment Seminar Palm Beach, Florida - March 30, 2006 Applied Mathematics and Statistics, Stony Brook University Robert J. Frey, Ph.D. Director, Program in Quantitative Finance Objectives Be

Chapter 10: Capital Markets and the Pricing of Risk

Chapter 0: Capital Markets and the Pricing of Risk- Chapter 0: Capital Markets and the Pricing of Risk Big Picture: ) To value a project, we need an interest rate to calculate present values ) The interest

Chapter 0: Capital Markets and the Pricing of Risk- Chapter 0: Capital Markets and the Pricing of Risk Big Picture: ) To value a project, we need an interest rate to calculate present values ) The interest

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

Financial Economics: Capital Asset Pricing Model

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INVESTMENT PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

CHAPTER 1 THE INVESTMENT SETTING

CHAPTER 1 THE INVESTMENT SETTING TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T PTS: 1 2. An investment is the

CHAPTER 1 THE INVESTMENT SETTING TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T PTS: 1 2. An investment is the