Risks and Rate of Return

|

|

|

- Abigayle Nichols

- 6 years ago

- Views:

Transcription

1 Risks and Rate of Return

2 Definition of Risk Risk is a chance of financial loss or the variability of returns associated with a given asset A $1000 holder government bond guarantees its holder $5 interest after 30 days has no risk, because there is no variability associated with the return. A $1000 investment in a firm s common stock which over the same 30 days may earn anywhere from $0 to $10 is very risky because of the high variability of return Financial assets are judged in terms of cash flows and hence the riskiness of a financial asset is measured in terms of the riskiness of its cash flows.

3 Definition of Return Return is the total gain or loss associated with an investment over a given period of time. It is commonly measured by cash distributions during the period plus the change in value, expressed as a percentage of the beginning-of-period investment value. (formula) If you have invested in a share on April 1, 2011 at Rs.$25, the annual dividend received at the end of the year is $1 and the year end price on march 31, 2012 is $30, ROR = 24% ROR has two components: Current yield (dividends) Capital gains/loss from appreciation/depreciation

4 Sources of risk Firm specific risks Business risks: the chance that a firm will be unable to cover its operating costs. Level driven by the firm s revenue earning stability and the structure of its operating costs Financial risk: the chance that the firm will be unable to cover its financial obligations. Level is driven by the predictability of the firm s operating cash flows and its fixed cost obligations

5 Sources of risk: Shareholder specific risks Interest rate risks: the chance that changes (rise and fall) in interest rates will adversely affect the value of an investment. Liquidity risk: the chance that an investment cannot be easily liquidated at a reasonable price. Liquidity is significantly affected by the size and depth of the market in which an investment is customarily traded Market risk: the chance that the value of an investment will decline because of market factors that are independent of the investment (economic, political, social). The more an investment value responds to the market, greater is the risk

6 Sources of risk: Firm & shareholder risks Event risk: the chance that a totally unexpected event will have a significant effect on the value of the firm or a specific investment. (government mandated withdrawal of a popular prescription drug affects a small group of firms or investments) Exchange rate risk: the exposure of future expected cash flows to fluctuations in the currency exchange rate. Greater the chance of undesirable exchange rate fluctuations, greater the risk of cash flows Purchasing power risk: the chance that changing price levels caused by inflation or deflation in the economy will adversely affect the investment s cashflows and value. Those with cashflows that do not move with general price levels have a high purchasing power risk Tax risk: the chance that unfavorable changes in tax laws will occur. Investments with values sensitive to tax law changes are more risky

7 Risk assessment Sensitivity analysis and probability distributions can be used to assess the general level of risk embodied in a given asset Sensitivity analysis is an approach for assessing risk that uses several possible return estimates to obtain a sense of the variability among outcomes Pessimistic, most likely and optimistic estimates of the returns associated with a given asset is made The asset s risk can be measured by the range of returns Greater the range, greater the risk

8 Measuring stand-alone risk Refer excel sheet..\calculation of SD to assess risk.xlsx The tighter or more peaked probability distribution, the more likely it is that the actual outcome will be close to the expected value and less likely it is that the actual return will end up far below the expected return Tighter the probability distribution, the lower the risk assigned to a stock In the example, Martin Products has a higher SD, which indicates a greater variation of returns and thus a greater chance that the expected return will not be realized meaning it is riskier investment There is only a small probability that US Water s return would be significantly less than expected, so that stock is not very risky

9 Risk Aversion and Required returns Two choices of investing $1m 5% US Treasury Bill or purchasing stock of R&D Enterprises If the company s research programs are successful, stock value will increase to $2.1m, but if the programs fail, stock value becomes zero Chances of success and failure is so the expected value of the stock one year from now is 0.5($0) + 0.5($2,100,000) = $1,050,000, which amounts to 5% expected rate of return (same as for treasury bill). A risk averse investor would choose treasury bill Risk Premium is the difference between the expected rate of return on a given risky asset and that on a less risky asset

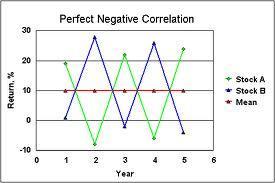

10 Risk of a portfolio An efficient portfolio is one that maximizes return for a given level of risk or minimizes risk for a given level of return As a rule portfolio risks decrease as the number of stocks in the portfolio increases If the stocks move in the same direction they are positively correlated, if opposite direction negative correlation To reduce overall risks, diversify by adding assets have a negative or a low positive correlation The degree of correlation is measured by correlation coefficient, which ranges from +1 for perfectly positively correlated series to -1 for perfectly negatively correlated series, 0 for uncorrelated assets Combining uncorrelated assets can reduce risk, not so effectively than combining negatively correlated assets, but more effectively than combining positively correlated assets

11 POSITIVE CORRELATION

12 Total Security Risk Total security risk = Non-diversifiable risk + diversifiable risk Diversifiable or unsystematic risk represents the portion of an asset s risk that can be eliminated through diversification It is attributable to firm specific events, such as strikes, lawsuits, regulatory actions and loss of a key account Non-diversifiable risk also called systematic risk is attributable to market factors that affect all firms; it cannot be eliminated through diversification It is shareholder specific market risk through factors such as war, inflation, international incidents and political events

13 Beta measure of systematic risk Beta coefficient, b, is a relative measure of non diversifiable risk. It is an index of the degree of movement of an asset s return in response to a change in the market return. Beta coefficient for the market is considered to be equal to 1.0 Betas maybe positive or negative, but positive betas are the norm Majority of them fall between 0.5 and 2.0 The return on stock with a beta of 0.5, is expected to change by half percent for each 1 percent change in the return of the market portfolio. The beta of a portfolio can be easily estimated by using the betas of the individual assets it includes.

14 Capital Asset Pricing Model (CAPM) The capital asset pricing model (CAPM), developed by William F. Sharpe and John Lintner, uses the beta of a particular security, the risk-free rate of return, and the market return to calculate the required return of an investment to its expected risk. Required Return = Risk Free Rate + Risk Premium Risk premium = Beta (Market Return Risk Free Rate) The term, Market Return Risk-Free Rate, is simply the required return on stocks in general because stocks have a certain amount of risk. Hence, this term is the risk premium of stocks what stocks have to return to compensate investors for the additional risk of holding stocks over holding risk-free Treasury Bills. Since different stocks have differing amounts of volatility, or risk, the required risk premium should also differ. The particular risk premium of a stock compared to the risk premium of the market is calculated by modifying the risk premium of the market with the stock s beta. If the beta is greater than 1, then the risk premium must be greater to compensate the investor for the additional risk; if it is less, then the risk premium will be less.

15 If the risk-free rate of a Treasury bill is 4%, and the return of the stock market has averaged about 12%, what is the required return of a stock that has a beta of 1.4? By using the CAPM formula, shown above, we find that: Required Return = 4% + [1.4 (12% - 4%)] = 4% % = 4% % = 15.2%

16 Security Market Line When the relative risk premium, represented by beta, is plotted in a graph against the required return, it yields a straight line known as the security market line(sml). This line begins at the risk-free rate and rises with beta. A graph of a security market line, assuming a market return of 12% and a risk-free rate of 4%. Note that a beta of 0 is equal to the risk-free rate while a beta of 1 has a relative risk equal to the market.

17 A graph of a security market line, assuming a market return of 12% and a risk-free rate of 4%. Note that a beta of 0 is equal to the risk-free rate while a beta of 1 has a relative risk equal to the market. Expected return SML Rm 12% Rf 4% Beta 1.0

18 Determinants of Market Interest Rates Interest rate r = r* +IP + DRP + LP + MRP r* is the real risk-free rate of interest. r* is the rate that would exist on a riskless security in a world where no inflation was expected Risk free security = r* + IP IP = Inflation premium is equal to the average expected rate of inflation over the life of the security. DRP = default risk premium that reflects the possibility that the issuer will not pay the promised interest or principal at the stated time LP = Liquidity premium reflects the fact that some securities cannot be converted into cash on short notice at a reasonable price MRP = maturity risk premium that reflects interest rate risk; longer the maturity period, greater the risk that market interest rates would rise

CHAPTER 8 Risk and Rates of Return

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Risk and Return. Chapter 5. Across the Disciplines Why This Chapter Matters To You LEARNING GOALS

Across the Disciplines Why This Chapter Matters To You Accounting: You need to understand the relationship between risk and return because of the effect that riskier projects will have on the firm s annual

Across the Disciplines Why This Chapter Matters To You Accounting: You need to understand the relationship between risk and return because of the effect that riskier projects will have on the firm s annual

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Lecture 8 & 9 Risk & Rates of Return

Lecture 8 & 9 Risk & Rates of Return We start from the basic premise that investors LIKE return and DISLIKE risk. Therefore, people will invest in risky assets only if they expect to receive higher returns.

Lecture 8 & 9 Risk & Rates of Return We start from the basic premise that investors LIKE return and DISLIKE risk. Therefore, people will invest in risky assets only if they expect to receive higher returns.

Analysis INTRODUCTION OBJECTIVES

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Return, Risk, and the Security Market Line

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Risk and Return - Capital Market Theory. Chapter 8

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

1) If you are thinking of investing in a stock, what things would you investigate? CF Risk News (company, industry, economy)

If you are thinking of investing in a stock, what things would you investigate? CF Risk News (company, industry, economy)") BUA321 Chapter 8 Class notes 1) If you are thinking of investing in a stock, what things would you investigate? CF Risk News (company, industry, economy) 2) What is inside trading? Trading on info that

BUA321 Chapter 8 Class notes 1) If you are thinking of investing in a stock, what things would you investigate? CF Risk News (company, industry, economy) 2) What is inside trading? Trading on info that

Risk and Return - Capital Market Theory. Chapter 8

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Chapter 5: Answers to Concepts in Review

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN Chapter 8. Risk and Return: Capital Asset Pricing Model. Liuren Wu

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

CHAPTER III RISK MANAGEMENT

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

RISK AND RETURN CHAPTER. Across the Disciplines WHY THIS CHAPTER MATTERS TO YOU

CHAPTER 5 RISK AND RETURN L E A R N I N G G O A L S LG1 LG2 LG3 Understand the meaning and fundamentals of risk, return, and risk preferences. Describe procedures for assessing and measuring the risk of

CHAPTER 5 RISK AND RETURN L E A R N I N G G O A L S LG1 LG2 LG3 Understand the meaning and fundamentals of risk, return, and risk preferences. Describe procedures for assessing and measuring the risk of

J B GUPTA CLASSES , Copyright: Dr JB Gupta. Chapter 4 RISK AND RETURN.

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 4 RISK AND RETURN Chapter Index Systematic and Unsystematic Risk Capital Asset Pricing Model

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 4 RISK AND RETURN Chapter Index Systematic and Unsystematic Risk Capital Asset Pricing Model

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

80 Solved MCQs of MGT201 Financial Management By

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

Financial Markets. Laurent Calvet. John Lewis Topic 13: Capital Asset Pricing Model (CAPM)

") Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

Investment In Bursa Malaysia Between Returns And Risks

Investment In Bursa Malaysia Between Returns And Risks AHMED KADHUM JAWAD AL-SULTANI, MUSTAQIM MUHAMMAD BIN MOHD TARMIZI University kebangsaan Malaysia,UKM, School of Business and Economics, 43600, Pangi

Investment In Bursa Malaysia Between Returns And Risks AHMED KADHUM JAWAD AL-SULTANI, MUSTAQIM MUHAMMAD BIN MOHD TARMIZI University kebangsaan Malaysia,UKM, School of Business and Economics, 43600, Pangi

Chapter 4. Investment Return and Risk

Chapter 4 Investment Return and Risk Return The reward for investing. Most returns are not guaranteed. E(r) is important factor in selection. Total Return consists of Current Income Appreciation 4-2 Importance

Chapter 4 Investment Return and Risk Return The reward for investing. Most returns are not guaranteed. E(r) is important factor in selection. Total Return consists of Current Income Appreciation 4-2 Importance

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Chapter 8 Risk and Rates of Return

Chapter 8 Risk and Rates of Return Answers to End-of-Chapter Questions 8-1 a. No, it is not riskless. The portfolio would be free of default risk and liquidity risk, but inflation could erode the portfolio

Chapter 8 Risk and Rates of Return Answers to End-of-Chapter Questions 8-1 a. No, it is not riskless. The portfolio would be free of default risk and liquidity risk, but inflation could erode the portfolio

Risk and Return Fundamentals. Risk, Return, and Asset Pricing Model. Risk and Return Fundamentals: Risk and Return Defined

Risk and Return Fundamentals Risk, Return, and Asset Pricing Model Financial Risk Management Nattawut Jenwittayaroje, PhD, CFA NIDA Business School National Institute of Development Administration In most

Risk and Return Fundamentals Risk, Return, and Asset Pricing Model Financial Risk Management Nattawut Jenwittayaroje, PhD, CFA NIDA Business School National Institute of Development Administration In most

CMA. Financial Decision Making

2018 Edition CMA Preparatory Program Part 2 Financial Decision Making Risk and Return Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box 6553 Columbus, Ohio 43206 (866) 807-HOCK

2018 Edition CMA Preparatory Program Part 2 Financial Decision Making Risk and Return Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box 6553 Columbus, Ohio 43206 (866) 807-HOCK

Statistically Speaking

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

MHSA 8630 Healthcare Financial Management Principles of Financial Risk

MHSA 8630 Healthcare Financial Management Principles of Financial Risk ** Risk, in a general context, refers to uncertainty of outcome, whether the outcome is a financial loss, a financial return that

MHSA 8630 Healthcare Financial Management Principles of Financial Risk ** Risk, in a general context, refers to uncertainty of outcome, whether the outcome is a financial loss, a financial return that

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Risk and Return (Introduction) Professor: Burcu Esmer

Professor: Burcu Esmer") Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

Define risk, risk aversion, and riskreturn

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

CHAPTER - IV RISK RETURN ANALYSIS

CHAPTER - IV RISK RETURN ANALYSIS Concept of Risk & Return Analysis The concept of risk and return analysis is integral to the process of investing and finance. 1 All financial decisions involve some risk.

CHAPTER - IV RISK RETURN ANALYSIS Concept of Risk & Return Analysis The concept of risk and return analysis is integral to the process of investing and finance. 1 All financial decisions involve some risk.

Chapter 10. Chapter 10 Topics. What is Risk? The big picture. Introduction to Risk, Return, and the Opportunity Cost of Capital

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

RISK AND RETURNS. Challenges of Risk - creates anxiety - discourages investment - demands a greater cost, e.g. insurance, indemnity

RISK AND RETURNS A risk is the probability that the outcome of a project may not be as expected. It implies that the project has clear-cut goals, and that information is available, but the future outcomes

RISK AND RETURNS A risk is the probability that the outcome of a project may not be as expected. It implies that the project has clear-cut goals, and that information is available, but the future outcomes

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Diversification. Finance 100

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INVESTMENT PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

Financial Markets 11-1

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 11: Measuring Financial Risk HEC MBA Financial Markets 11-1 Risk There are many types of risk in financial transactions

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 11: Measuring Financial Risk HEC MBA Financial Markets 11-1 Risk There are many types of risk in financial transactions

Lecture #2. YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship. Risk Premium over the Standard Deviation of portfolio excess return

REVIEW Lecture #2 YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship Sharpe Ratio: Risk Premium over the Standard Deviation of portfolio excess return (E(r p) r f ) / σ 8% / 20% = 0.4x. A higher

REVIEW Lecture #2 YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship Sharpe Ratio: Risk Premium over the Standard Deviation of portfolio excess return (E(r p) r f ) / σ 8% / 20% = 0.4x. A higher

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

Chapter 13 Return, Risk, and the Security Market Line

Chapter 13 Return, Risk, and the Security Market Line 1. You own a stock that you think will produce a return of 11 percent in a good economy and 3 percent in a poor economy. Given the probabilities of

Chapter 13 Return, Risk, and the Security Market Line 1. You own a stock that you think will produce a return of 11 percent in a good economy and 3 percent in a poor economy. Given the probabilities of

An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

- P P THE RELATION BETWEEN RISK AND RETURN. Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

Portfolio Management

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Capital Asset Pricing Model - CAPM

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Cost of equity in emerging markets. Evidence from Romanian listed companies

Cost of equity in emerging markets. Evidence from Romanian listed companies Costin Ciora Teaching Assistant Department of Economic and Financial Analysis Bucharest Academy of Economic Studies, Romania

Cost of equity in emerging markets. Evidence from Romanian listed companies Costin Ciora Teaching Assistant Department of Economic and Financial Analysis Bucharest Academy of Economic Studies, Romania

QCU and Exercise for Part 3 : 30 QCU (only one answer is right) and 1 Exercise

and 1 Exercise") QCU and Exercise for Part 3 : 30 QCU (only one answer is right) and 1 Exercise Risk and return Cost of equity From the cost of equity to the cost of capital Corporate Finance Master 1 2012-2013 All campuses

QCU and Exercise for Part 3 : 30 QCU (only one answer is right) and 1 Exercise Risk and return Cost of equity From the cost of equity to the cost of capital Corporate Finance Master 1 2012-2013 All campuses

Microéconomie de la finance

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

2013/2014. Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities.

Question One: Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities. 2. Diversification will normally reduce the riskiness

Question One: Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities. 2. Diversification will normally reduce the riskiness

OVERVIEW OF FINANCIAL RISK ASSESSMENT. A thesis submitted to the. Kent State University Honors College. in partial fulfillment of the requirements

i OVERVIEW OF FINANCIAL RISK ASSESSMENT A thesis submitted to the Kent State University Honors College in partial fulfillment of the requirements for University Honors by Bo Zhao May, 2014 ii iii Thesis

i OVERVIEW OF FINANCIAL RISK ASSESSMENT A thesis submitted to the Kent State University Honors College in partial fulfillment of the requirements for University Honors by Bo Zhao May, 2014 ii iii Thesis

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

The Case for TD Low Volatility Equities

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

CHAPTER 5 THE COST OF MONEY (INTEREST RATES)

") CHAPTER 5 THE COST OF MONEY (INTEREST RATES) 1 Learning Outcomes LO.1 Describe the cost of money and factors that affect the cost of money. LO.2 Describe how interest rates are determined. LO.3 Describe

CHAPTER 5 THE COST OF MONEY (INTEREST RATES) 1 Learning Outcomes LO.1 Describe the cost of money and factors that affect the cost of money. LO.2 Describe how interest rates are determined. LO.3 Describe

Ocean Hedge Fund. James Leech Matt Murphy Robbie Silvis

Ocean Hedge Fund James Leech Matt Murphy Robbie Silvis I. Create an Equity Hedge Fund Investment Objectives and Adaptability A. Preface on how the hedge fund plans to adapt to current and future market

Ocean Hedge Fund James Leech Matt Murphy Robbie Silvis I. Create an Equity Hedge Fund Investment Objectives and Adaptability A. Preface on how the hedge fund plans to adapt to current and future market

Which Investment Option Would You Choose?

CHAPTER 9 Investment Management: Concepts and Strategies Elements of risk Which Investment Option Would You Choose? FIXED INCOME SECURITIES FIXED-INCOME SECURITY RETURN Where does it come from? FIXED-INCOME

CHAPTER 9 Investment Management: Concepts and Strategies Elements of risk Which Investment Option Would You Choose? FIXED INCOME SECURITIES FIXED-INCOME SECURITY RETURN Where does it come from? FIXED-INCOME

Kingdom of Saudi Arabia Capital Market Authority. Investment

Kingdom of Saudi Arabia Capital Market Authority Investment The Definition of Investment Investment is defined as the commitment of current financial resources in order to achieve higher gains in the

Kingdom of Saudi Arabia Capital Market Authority Investment The Definition of Investment Investment is defined as the commitment of current financial resources in order to achieve higher gains in the

The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

International Financial Markets 1. How Capital Markets Work

International Financial Markets Lecture Notes: E-Mail: Colloquium: www.rainer-maurer.de rainer.maurer@hs-pforzheim.de Friday 15.30-17.00 (room W4.1.03) -1-1.1. Supply and Demand on Capital Markets 1.1.1.

International Financial Markets Lecture Notes: E-Mail: Colloquium: www.rainer-maurer.de rainer.maurer@hs-pforzheim.de Friday 15.30-17.00 (room W4.1.03) -1-1.1. Supply and Demand on Capital Markets 1.1.1.

Financial Management_MGT201. Lecture 19 to 22. Important Notes

Financial Management_MGT201 7 th Week of Lectures Lecture 19 to 22 Important Notes Explanation noted by me has shown with & symbols. Lecture No 19: 6 Dec 2015_Tuesday_ 2:13pm 3:02pm RISKS: Its very important

Financial Management_MGT201 7 th Week of Lectures Lecture 19 to 22 Important Notes Explanation noted by me has shown with & symbols. Lecture No 19: 6 Dec 2015_Tuesday_ 2:13pm 3:02pm RISKS: Its very important

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

CHAPTER II LITERATURE REVIEW

CHAPTER II LITERATURE REVIEW II.1. Risk II.1.1. Risk Definition According Brigham and Houston (2004, p170), Risk is refers to the chance that some unfavorable event will occur (a hazard, a peril, exposure

CHAPTER II LITERATURE REVIEW II.1. Risk II.1.1. Risk Definition According Brigham and Houston (2004, p170), Risk is refers to the chance that some unfavorable event will occur (a hazard, a peril, exposure

Estimating the Cost of Capital Using the CAPM

Estimating the Cost of Capital Using the CAPM John C. Handley Department of Finance University of Melbourne Melbourne Centre/ACCC Occasional Seminar Series 16 October 2007 1. THE PROBLEM OF ESTIMATION

Estimating the Cost of Capital Using the CAPM John C. Handley Department of Finance University of Melbourne Melbourne Centre/ACCC Occasional Seminar Series 16 October 2007 1. THE PROBLEM OF ESTIMATION

FNCE 4030 Fall 2012 Roberto Caccia, Ph.D. Midterm_2a (2-Nov-2012) Your name:

Your name:") Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

An Analysis of Theories on Stock Returns

An Analysis of Theories on Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq.

An Analysis of Theories on Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq.

CHAPTER 4: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 4: ANSWERS TO CONCEPTS IN REVIEW 4.1 The return on investment is the expected profit that motivates people to invest. It includes both current income and/or capital gains (or losses). Without a

CHAPTER 4: ANSWERS TO CONCEPTS IN REVIEW 4.1 The return on investment is the expected profit that motivates people to invest. It includes both current income and/or capital gains (or losses). Without a

FEEDBACK TUTORIAL LETTER ASSIGNMENT 1 AND 2 MANAGERIAL FINANCE 4B MAF412S

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 AND 2 MANAGERIAL FINANCE 4B MAF412S 1 ASSIGNMENT 1 QUESTION 1 (i) Investment A at end of Year 3: Year 4 5 6 7 8 Cash flows 1 000 1 000 1 000 1 000

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 AND 2 MANAGERIAL FINANCE 4B MAF412S 1 ASSIGNMENT 1 QUESTION 1 (i) Investment A at end of Year 3: Year 4 5 6 7 8 Cash flows 1 000 1 000 1 000 1 000

Finance 100: Corporate Finance

Finance 100: Corporate Finance Professor Michael R. Roberts Quiz 2 October 31, 2007 Name: Section: Question Maximum Student Score 1 30 2 40 3 30 Total 100 Instructions: Please read each question carefully

Finance 100: Corporate Finance Professor Michael R. Roberts Quiz 2 October 31, 2007 Name: Section: Question Maximum Student Score 1 30 2 40 3 30 Total 100 Instructions: Please read each question carefully

Predictability of Stock Returns

Predictability of Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Iraq Correspondence: Ahmet Sekreter, Ishik University, Iraq. Email: ahmet.sekreter@ishik.edu.iq

Predictability of Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Iraq Correspondence: Ahmet Sekreter, Ishik University, Iraq. Email: ahmet.sekreter@ishik.edu.iq