ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 6

|

|

|

- Ronald Watkins

- 5 years ago

- Views:

Transcription

1 ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 6

2 MVO IN TWO STAGES Calculate the forecasts Calculate forecasts for returns, standard deviations and correlations for the set of assets in which you can invest This is often done using historical data. Calculate the Efficient Frontier. The efficient frontier is the set of portfolios that minimizes risk at the possible levels of return. A portfolio can be selected from the frontier based on risk, utility maximization, maximum Sharpe Ratio, etc. MVO OPTIMIZATION STEP Create or calculate Forecasts for Return, Risk and Correlations for a set of assets. These parameters describe a multivariate return distribution Calculate the Efficient Frontier. Assume that all portfolios have positive weights (no short-selling) and add to 100. Calculate the minimum variance portfolios and maximum return portfolio using the forecasts. Calculate the portfolio that minimizes risk for each of 98 portfolios between the minimum variance and maximum return portfolios. This set of 100 portfolios is the efficient frontier 2

3 MVO LIMITS (& SOLUTIONS) Returns are very difficult to forecast. MVO requires forecasts on ALL assets. Historical returns are very poor forecasts. Input Sensitivity--MVO is highly sensitive to the return forecasts. Small changes in return assumptions often lead to large changes in the optimal allocations. Estimation Error is built into forecasting and magnified by MVO Portfolios are very concentrated (no diversification). Portfolios are unintuitive. Both of these issues must be solved to make MVO a practical real-world tool. Black-Litterman Technique developed by Fischer Black and Robert Litterman of Goldman Sachs to create better return estimates. Resampling Technique developed by Richard Michaud to average over the statistical equivalence region and create a new efficient frontier. 3

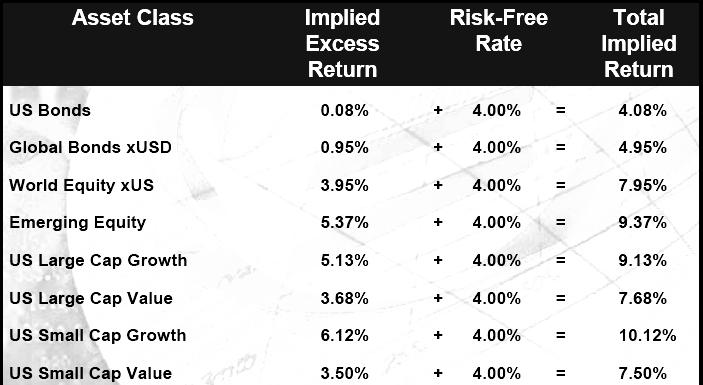

4 IMPLIED RETURNS The Black-Litterman Model starts with Implied Returns Other Names for Implied Returns: CAPM Returns Reverse Optimized Returns Market Returns Consensus Returns Equilibrium Returns The return of any asset or asset class can be separated into three parts: Risk-Free Return Return Correlated with Benchmark Return Not Correlated with Benchmark Returns that are correlated with the benchmark result in beta risk (systematic risk, benchmark risk, nondiversifiable risk, or market risk) Beta risk is the type of risk that is rewarded with a premium 4

5 IMPLIED RETURNS USING CAPM Expected returns are a function of beta risk R f β i,b R b R b - R f Risk-Free Rate Beta of Asset Class i Relative to Benchmark Return of Benchmark Forward Looking Risk Premium of Benchmark = Return of Benchmark over the Risk-Free In this case the benchmark is the market capitalization weighted portfolio. 5

6 IMPLIED RETURNS: RISK AVERSION COEFFICIENT The Risk Aversion Coefficient characterizes the risk-return trade-off. Using historical risk premium and variance, we got a ג of approximately

7 IMPLIED RETURNS USING REVERSE OPTIMIZATION The same excess returns results from reverse optimization The denominator is basically the variance of market portfolio. The numerator is the covariance of the assets in the market portfolio. Asset weights are the equilibrium weights. Covariance matrix is historical covariance 7

8 EXAMPLE 8

9 HISTORICAL VS IMPLIED RETURNS OPTIMIZATION 9

10 BLACK- LITTERMAN MODEL Start with the market returns using reverse optimization and CAPM. You may or may not agree with the implied returns If you don t agree with the implied returns, the Black-Litterman model provides an elegant framework for combining the implied returns with your unique views that results in well-diversified portfolios that reflect your views B-L model uses a Bayesian approach to combine the subjective views of an investor regarding the expected returns of one or more assets with the market equilibrium vector of expected returns (the prior distribution) to form a new mixed estimate of expected returns (the posterior distribution). Apply your own unique views of how certain markets are going to behave. The end result includes both a set of expected returns of assets as well as the optimal portfolio weights. If you do not have views, you hold the market portfolio (the benchmark). Your views will tilt the final weights away from the market portfolio, the degree to which depending on how confident you are about your views. Types of view: Absolute Views Asset A will have a return of X% Relative Views Asset A will outperform Asset B by X% 10

11 FORMING VIEW Our view is: Q=Pu+η,µ~Φ(0,Ω) Note: same as Pu=Q+η, becauseη~φ(0,ω) -η~φ(0,ω) u is the expected future returns (a NX1 vector of random variables). Ω is assumed to be diagonal What does this Q=P*u+η, Or equivalently P*u=Q+ηmean? Look at P*u: each row of P represents a set of weights on the N assets, in other words, each row is a portfolio of the N assets. (aka view portfolio ) u is the expected return vector of the N assets P*u means we are expressing our views through k view portfolios Expressing views so important because the practical value of BL model lies in the View Expressing Scheme; the model itself is just a publicly available view combining engine. Our view is the source of alpha. Expressing views quantitatively means efficiently and effectively translate fundamental analyses into Views 11

12 THE NEXT STEP IS TO DO MARKOWITZ MVO By using the combined forecasted means and the forecasted covariance matrix. So we start with Markowitz (reverse optimization) and CAPM (implied beta). Go though Black-Litterman View Combining engine. And end up with Markowitz again with predictive means, (and forward looking return covariance matrix.) First bracket [ ] (role of Denominator ) : Normalisation Second bracket [ ] (role of Numerator ) : Balance between returnsπ(equilibrium returns) and Q (Views). Covariance (τσ) -1 and confidence P Ω -1 P serve as weighting factors, and P Ω -1 Q = P Ω -1 P P -1 Q Extreme case 1: no estimates P=0: E(R) = Π i.e. BL-returns = equilibrium returns. Extreme case 2: no estimation errorsω -1 : E(R) = P -1 Q i.e. BL-returns = View returns. 12

13 ROAD MAP 13

14 AN EIGHT ASSETS EXAMPLE µ Hist is historical mean asset returns µ p is calculated relative to the market cap. weighted portfolio using implied betas and CAPM model. Market portfolio weights w mkt is based on market capitalization for each of the assets A s s e t C l a s s µ H i s t µ P w m k t U S B o n d s % % % I n t l B o n d s % % % U S L a r g e G r o w t h % % % U S L a r g e V a l u e % % % U S S m a l l G r o w t h % % % U S S m a l l V a l u e % % % I n t l D e v. E q u i t y % % % I n t l E m e r g. E q u i t y % % % W e i g h t e d A v e r a g e % % S t a n d a r d D e v i a t i o n % % H i g h % % % L o w % % % 14

15 COVARIANCE MATRIX Asset Class US Bonds Intl Bonds US Large Growth US Large Value US Small Growth US Small Value Int'l Dev. Equity Int'l Emerg.Equity

16 IMPLIED MARKET RETURNS П(NX1) Π = λσw mkt A s s e t C l a s s µ H i s t µ P Π U S B o n d s % % % I n t l B o n d s % % % U S L a r g e G r o w t h % % % U S L a r g e V a l u e % % % U S S m a l l G r o w t h % % % U S S m a l l V a l u e % % % I n t l D e v. E q u i t y % % % I n t l E m e r g. E q u i t y % % % W e i g h t e d A v e r a g e % % % S t a n d a r d D e v i a t i o n % % % H i g h % % % L o w % % % 16

17 WHAT IS A VIEW? Opinion: International Developed Equity will be doing well Absolute view: View 1: International Developed Equity will have an absolute excess return of 5.25% (Confidence of view = 25%) Relative view: View 2: International Bonds will outperform US bonds by 25 bp (Confidence of view = 50%) View 3: US Large Growth and US Small Growth will outperform US Large Value and US Small Value by 2% (Confidence of View = 65%) 17

18 WHAT IS THE VIEW VECTOR Q LIKE? Unless a clairvoyant investor is 100% confident in the views, the error termεis a positive or negative value other than 0 The error term vector does not enter the Black Litterman formula; instead, the variance of each error term (ω) does. 5.25% ε 1 Q + ε = 0.25% + ε % ε 3 18

19 WHAT IS THE VIEW MATRIX P LIKE? View 1 is represented by row 1. The absolute view results in the sum of row equal to 1 View 2 & 3 are represented by row 2 & 3. Relative views results in the sum of rows equal to 0 The weights in view 3 are based on relative market cap. weights, with outperforming assets receiving positive weights and underperforming assets receiving negative weights US Bonds Intl Bonds US Lg Growth US Lg Value US Sml Growth US Sml Value Int'l Dev. Eqt Int'l Emerg.Eqt P =

20 FINALLY, THE COVARIANCE MATRIX OF THE ERROR TERM Ω Ω is a diagonal covariance matrix with 0 s in all of the off-diagonal positions, because the model assumes that the views are independent of each other This essentially makesωthe variance (uncertainty) of views Ω =

21 RETURN VECTOR & RESULTING PORTFOLIO WEIGHTS Asset Class E[R] Π E[R]-Π norm w mkt US Bonds 0.07% 0.08% -0.02% 29.88% 28.83% 19.34% 10.54% Int l Bonds US Large Growth 0.50% 6.50% 0.67% 6.41% w = ( Σ ) % 0.08% 15.59% 9.35% 15.04% 9.02% 26.13% 12.09% % -2.73% US Large Value 4.32% 4.08% % 14.82% 14.30% 12.09% 2.73% E [ R ] US Small Growth 7.59% 7.43% 0.16% 1.04% 1.00% 1.34% -0.30% US Small Value 3.94% 3.70% 0.23% 1.65% 1.59% 1.34% 0.30% Int l Dev. Equity 4.93% 4.80% 0.13% 27.81% 26.84% 24.18% 3.63% Int l Emerg. Equity 6.84% 6.60% 0.24% 3.49% 3.37% 3.49% 0.00% Sum % 100% 100% 3.63% Π = λσw mkt w =(λσ) -1 Π w =(λσ) -1 E[R] 21

22 COMBINED RETURN E[R] VS. EQUIL. RETURN Π 8% 6% Π E[R] 4% 2% 0% US Bonds Int l Bonds US La rge Growt h US La rge Va lue US S ma ll Growt h US S ma ll Va lue Int l De v. Equit y Int l Eme rg. Equit y 22

23 IMPACT OF VIEW: NEW ASSET ALLOCATION View 2: Int l bonds will outperform US bonds less than market implied. View 1 Bullish view on Int l Dev. Equity increases allocation. 35% 30% 25% Market Cap. Weight View 3 Growth tilt towards value New Weight 20% 15% 10% 5% 0% US Bonds Int l Bonds US Large Growt h US Large Value US S mall Growt h US S mall Value Int l Dev. Equit y Int l Emerg. Equit y 23

24 RESAMPLING Resampling is a Monte Carlo technique for estimating the inputs for mean-variance optimization and eventually the resampled efficient frontier. It results in well diversified portfolios. 1. Estimate returns, standard deviations, and correlations 2. Run a multivariate simulation that results in a new set of returns, standard deviations, and correlations. 3. From the resulting efficient frontier record the weights and the returns of the efficient portfolios at predetermined standard deviation intervals (i.e. 5%, 6%, 7%, etc.) 4. Repeats Steps 2 and times 5. Calculate the average allocation to the assets for each predetermined interval and the average return, and then graph them in return standard deviation space to create the resampled frontier. CRITICAL ISSUES Portfolios inherit the estimation error in the original inputs Scherer 2002 Lack of theory No reason why resampled portfolios should be optimal Scherer 2002 In the absence of views, resampling results in active risk relative to a policy benchmark why take bets with out a reason? No framework for incorporating views 24

25 RESAMPLING CRITICAL ISSUES Surprising large amount of variation in recommended portfolio overtime 25

26 RESAMPLING CRITICAL ISSUES Resampling underperformed in historical backtest 26

Deconstructing Black-Litterman*

Deconstructing Black-Litterman* Richard Michaud, David Esch, Robert Michaud New Frontier Advisors Boston, MA 02110 Presented to: fi360 Conference Sheraton Chicago Hotel & Towers April 25-27, 2012, Chicago,

Deconstructing Black-Litterman* Richard Michaud, David Esch, Robert Michaud New Frontier Advisors Boston, MA 02110 Presented to: fi360 Conference Sheraton Chicago Hotel & Towers April 25-27, 2012, Chicago,

Expected Return Methodologies in Morningstar Direct Asset Allocation

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

International Finance. Estimation Error. Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc.

International Finance Estimation Error Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 17, 2017 Motivation The Markowitz Mean Variance Efficiency is the

International Finance Estimation Error Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 17, 2017 Motivation The Markowitz Mean Variance Efficiency is the

Quantitative Risk Management

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Black-Litterman Model

Institute of Financial and Actuarial Mathematics at Vienna University of Technology Seminar paper Black-Litterman Model by: Tetyana Polovenko Supervisor: Associate Prof. Dipl.-Ing. Dr.techn. Stefan Gerhold

Institute of Financial and Actuarial Mathematics at Vienna University of Technology Seminar paper Black-Litterman Model by: Tetyana Polovenko Supervisor: Associate Prof. Dipl.-Ing. Dr.techn. Stefan Gerhold

A STEP-BY-STEP GUIDE TO THE BLACK-LITTERMAN MODEL. Incorporating user-specified confidence levels

A STEP-BY-STEP GUIDE TO THE BLACK-LITTERMAN MODEL Incorporating user-specified confidence levels Thomas M. Idzore * Thomas M. Idzore, CFA Senior Quantitative Researcher Zephyr Associates, Inc. PO Box 12368

A STEP-BY-STEP GUIDE TO THE BLACK-LITTERMAN MODEL Incorporating user-specified confidence levels Thomas M. Idzore * Thomas M. Idzore, CFA Senior Quantitative Researcher Zephyr Associates, Inc. PO Box 12368

Black-Litterman model: Colombian stock market application

Black-Litterman model: Colombian stock market application Miguel Tamayo-Jaramillo 1 Susana Luna-Ramírez 2 Tutor: Diego Alonso Agudelo-Rueda Research Practise Progress Presentation EAFIT University, Medelĺın

Black-Litterman model: Colombian stock market application Miguel Tamayo-Jaramillo 1 Susana Luna-Ramírez 2 Tutor: Diego Alonso Agudelo-Rueda Research Practise Progress Presentation EAFIT University, Medelĺın

The Black-Litterman Model in Central Bank Practice: Study for Turkish Central Bank

Malaysian Journal of Mathematical Sciences 10(S) February: 193 203 (2016) Special Issue: The 3 rd International Conference on Mathematical Applications in Engineering 2014 (ICMAE 14) MALAYSIAN JOURNAL

Malaysian Journal of Mathematical Sciences 10(S) February: 193 203 (2016) Special Issue: The 3 rd International Conference on Mathematical Applications in Engineering 2014 (ICMAE 14) MALAYSIAN JOURNAL

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Tuomo Lampinen Silicon Cloud Technologies LLC

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

New Formal Description of Expert Views of Black-Litterman Asset Allocation Model

BULGARIAN ACADEMY OF SCIENCES CYBERNETICS AND INFORMATION TECHNOLOGIES Volume 17, No 4 Sofia 2017 Print ISSN: 1311-9702; Online ISSN: 1314-4081 DOI: 10.1515/cait-2017-0043 New Formal Description of Expert

BULGARIAN ACADEMY OF SCIENCES CYBERNETICS AND INFORMATION TECHNOLOGIES Volume 17, No 4 Sofia 2017 Print ISSN: 1311-9702; Online ISSN: 1314-4081 DOI: 10.1515/cait-2017-0043 New Formal Description of Expert

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired February 2015 Newfound Research LLC 425 Boylston Street 3 rd Floor Boston, MA 02116 www.thinknewfound.com info@thinknewfound.com

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired February 2015 Newfound Research LLC 425 Boylston Street 3 rd Floor Boston, MA 02116 www.thinknewfound.com info@thinknewfound.com

Introduction to Risk Parity and Budgeting

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Introduction to Risk Parity and Budgeting Thierry Roncalli CRC Press Taylor &. Francis Group Boca Raton London New York CRC Press is an imprint of the Taylor

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Introduction to Risk Parity and Budgeting Thierry Roncalli CRC Press Taylor &. Francis Group Boca Raton London New York CRC Press is an imprint of the Taylor

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 5

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 5 FLEXIBLE PRODUCT IN ITALY Risk control on low volatility profile? Broad range of volatility Volatility shift over time

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA MODULO ASSET MANAGEMENT LECTURE 5 FLEXIBLE PRODUCT IN ITALY Risk control on low volatility profile? Broad range of volatility Volatility shift over time

(High Dividend) Maximum Upside Volatility Indices. Financial Index Engineering for Structured Products

Maximum Upside Volatility Indices. Financial Index Engineering for Structured Products") (High Dividend) Maximum Upside Volatility Indices Financial Index Engineering for Structured Products White Paper April 2018 Introduction This report provides a detailed and technical look under the hood

(High Dividend) Maximum Upside Volatility Indices Financial Index Engineering for Structured Products White Paper April 2018 Introduction This report provides a detailed and technical look under the hood

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Global Tactical Asset Allocation (GTAA)

") JPMorgan Global Access Portfolios Presented at 2014 Matlab Computational Finance Conference April 2010 JPMorgan Global Access Investment Team Global Tactical Asset Allocation (GTAA) Jeff Song, Ph.D. CFA

JPMorgan Global Access Portfolios Presented at 2014 Matlab Computational Finance Conference April 2010 JPMorgan Global Access Investment Team Global Tactical Asset Allocation (GTAA) Jeff Song, Ph.D. CFA

Behavioral Finance 1-1. Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships

Behavioral Finance 1-1 Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships 1 The Pricing of Risk 1-2 The expected utility theory : maximizing the expected utility across possible states

Behavioral Finance 1-1 Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships 1 The Pricing of Risk 1-2 The expected utility theory : maximizing the expected utility across possible states

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Estimation Risk Modeling in Optimal Portfolio Selection:

Estimation Risk Modeling in Optimal Portfolio Selection: An Study from Emerging Markets By Sarayut Nathaphan Pornchai Chunhachinda 1 Agenda 2 Traditional efficient portfolio and its extension incorporating

Estimation Risk Modeling in Optimal Portfolio Selection: An Study from Emerging Markets By Sarayut Nathaphan Pornchai Chunhachinda 1 Agenda 2 Traditional efficient portfolio and its extension incorporating

Next Generation Fund of Funds Optimization

Next Generation Fund of Funds Optimization Tom Idzorek, CFA Global Chief Investment Officer March 16, 2012 2012 Morningstar Associates, LLC. All rights reserved. Morningstar Associates is a registered

Next Generation Fund of Funds Optimization Tom Idzorek, CFA Global Chief Investment Officer March 16, 2012 2012 Morningstar Associates, LLC. All rights reserved. Morningstar Associates is a registered

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 8: An Investment Process for Stock Selection Fall 2011/2012 Please note the disclaimer on the last page Announcements December, 20 th, 17h-20h:

Master in Money and Finance Goethe University Frankfurt Week 8: An Investment Process for Stock Selection Fall 2011/2012 Please note the disclaimer on the last page Announcements December, 20 th, 17h-20h:

FNCE 4030 Fall 2012 Roberto Caccia, Ph.D. Midterm_2a (2-Nov-2012) Your name:

Your name:") Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Mean Variance Portfolio Theory

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

Robust Portfolio Optimization SOCP Formulations

1 Robust Portfolio Optimization SOCP Formulations There has been a wealth of literature published in the last 1 years explaining and elaborating on what has become known as Robust portfolio optimization.

1 Robust Portfolio Optimization SOCP Formulations There has been a wealth of literature published in the last 1 years explaining and elaborating on what has become known as Robust portfolio optimization.

!"#$ 01$ 7.3"กก>E E?D:A 5"7=7 E!<C";E2346 <2H<

กก AEC Portfolio Investment!"#$ 01$ 7.3"กก>E E?D:A 5"7=7 >?@A?2346BC@ก"9D E!

กก AEC Portfolio Investment!"#$ 01$ 7.3"กก>E E?D:A 5"7=7 >?@A?2346BC@ก"9D E!

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

The Fundamental Law of Mismanagement

The Fundamental Law of Mismanagement Richard Michaud, Robert Michaud, David Esch New Frontier Advisors Boston, MA 02110 Presented to: INSIGHTS 2016 fi360 National Conference April 6-8, 2016 San Diego,

The Fundamental Law of Mismanagement Richard Michaud, Robert Michaud, David Esch New Frontier Advisors Boston, MA 02110 Presented to: INSIGHTS 2016 fi360 National Conference April 6-8, 2016 San Diego,

PORTFOLIO OPTIMIZATION: ANALYTICAL TECHNIQUES

PORTFOLIO OPTIMIZATION: ANALYTICAL TECHNIQUES Keith Brown, Ph.D., CFA November 22 nd, 2007 Overview of the Portfolio Optimization Process The preceding analysis demonstrates that it is possible for investors

PORTFOLIO OPTIMIZATION: ANALYTICAL TECHNIQUES Keith Brown, Ph.D., CFA November 22 nd, 2007 Overview of the Portfolio Optimization Process The preceding analysis demonstrates that it is possible for investors

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

A Broader View of the Mean-Variance Optimization Framework

A Broader View of the Mean-Variance Optimization Framework Christopher J. Donohue 1 Global Association of Risk Professionals January 15, 2008 Abstract In theory, mean-variance optimization provides a rich

A Broader View of the Mean-Variance Optimization Framework Christopher J. Donohue 1 Global Association of Risk Professionals January 15, 2008 Abstract In theory, mean-variance optimization provides a rich

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Asset Pricing Model 2

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Stochastic Portfolio Theory Optimization and the Origin of Rule-Based Investing.

Stochastic Portfolio Theory Optimization and the Origin of Rule-Based Investing. Gianluca Oderda, Ph.D., CFA London Quant Group Autumn Seminar 7-10 September 2014, Oxford Modern Portfolio Theory (MPT)

Stochastic Portfolio Theory Optimization and the Origin of Rule-Based Investing. Gianluca Oderda, Ph.D., CFA London Quant Group Autumn Seminar 7-10 September 2014, Oxford Modern Portfolio Theory (MPT)

The Markowitz framework

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Robust Portfolio Rebalancing with Transaction Cost Penalty An Empirical Analysis

August 2009 Robust Portfolio Rebalancing with Transaction Cost Penalty An Empirical Analysis Abstract The goal of this paper is to compare different techniques of reducing the sensitivity of optimal portfolios

August 2009 Robust Portfolio Rebalancing with Transaction Cost Penalty An Empirical Analysis Abstract The goal of this paper is to compare different techniques of reducing the sensitivity of optimal portfolios

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Solutions to the problems in the supplement are found at the end of the supplement

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

Understanding the Principles of Investment Planning Stochastic Modelling/Tactical & Strategic Asset Allocation

Understanding the Principles of Investment Planning Stochastic Modelling/Tactical & Strategic Asset Allocation John Thompson, Vice President & Portfolio Manager London, 11 May 2011 What is Diversification

Understanding the Principles of Investment Planning Stochastic Modelling/Tactical & Strategic Asset Allocation John Thompson, Vice President & Portfolio Manager London, 11 May 2011 What is Diversification

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Chapter 8: CAPM. 1. Single Index Model. 2. Adding a Riskless Asset. 3. The Capital Market Line 4. CAPM. 5. The One-Fund Theorem

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

The Black-Litterman model

The Black-Litterman model Christopher Øiestad Syvertsen Supervisor Post doc Trygve Kastberg Nilssen This Masters Thesis is carried out as a part of the education at the University of Agder and is therefore

The Black-Litterman model Christopher Øiestad Syvertsen Supervisor Post doc Trygve Kastberg Nilssen This Masters Thesis is carried out as a part of the education at the University of Agder and is therefore

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

International Diversification Revisited

International Diversification Revisited by Robert J. Hodrick and Xiaoyan Zhang 1 ABSTRACT Using country index returns from 8 developed countries and 8 emerging market countries, we re-explore the benefits

International Diversification Revisited by Robert J. Hodrick and Xiaoyan Zhang 1 ABSTRACT Using country index returns from 8 developed countries and 8 emerging market countries, we re-explore the benefits

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Motif Capital Horizon Models: A robust asset allocation framework

Motif Capital Horizon Models: A robust asset allocation framework Executive Summary By some estimates, over 93% of the variation in a portfolio s returns can be attributed to the allocation to broad asset

Motif Capital Horizon Models: A robust asset allocation framework Executive Summary By some estimates, over 93% of the variation in a portfolio s returns can be attributed to the allocation to broad asset

Optimal Portfolio Selection Under the Estimation Risk in Mean Return

Optimal Portfolio Selection Under the Estimation Risk in Mean Return by Lei Zhu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree of Master of Mathematics

Optimal Portfolio Selection Under the Estimation Risk in Mean Return by Lei Zhu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree of Master of Mathematics

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Estimation risk modeling in portfolio selection: Implicit approach implementation

Journal of Finance and Investment Analysis, vol.1, no.3, 2012, 21-31 ISSN: 2241-0988 (print version), 2241-0996 (online) Scienpress Ltd, 2012 Estimation risk modeling in portfolio selection: Implicit approach

Journal of Finance and Investment Analysis, vol.1, no.3, 2012, 21-31 ISSN: 2241-0988 (print version), 2241-0996 (online) Scienpress Ltd, 2012 Estimation risk modeling in portfolio selection: Implicit approach

LECTURE NOTES 10 ARIEL M. VIALE

LECTURE NOTES 10 ARIEL M VIALE 1 Behavioral Asset Pricing 11 Prospect theory based asset pricing model Barberis, Huang, and Santos (2001) assume a Lucas pure-exchange economy with three types of assets:

LECTURE NOTES 10 ARIEL M VIALE 1 Behavioral Asset Pricing 11 Prospect theory based asset pricing model Barberis, Huang, and Santos (2001) assume a Lucas pure-exchange economy with three types of assets:

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 8: From factor models to asset pricing Fall 2012/2013 Please note the disclaimer on the last page Announcements Solution to exercise 1 of problem

Master in Money and Finance Goethe University Frankfurt Week 8: From factor models to asset pricing Fall 2012/2013 Please note the disclaimer on the last page Announcements Solution to exercise 1 of problem

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Statistically Speaking

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

Chapter 6 Efficient Diversification. b. Calculation of mean return and variance for the stock fund: (A) (B) (C) (D) (E) (F) (G)

(B) (C) (D) (E) (F) (G)") Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

A Bayesian Implementation of the Standard Optimal Hedging Model: Parameter Estimation Risk and Subjective Views

A Bayesian Implementation of the Standard Optimal Hedging Model: Parameter Estimation Risk and Subjective Views by Wei Shi and Scott H. Irwin May 23, 2005 Selected Paper prepared for presentation at the

A Bayesian Implementation of the Standard Optimal Hedging Model: Parameter Estimation Risk and Subjective Views by Wei Shi and Scott H. Irwin May 23, 2005 Selected Paper prepared for presentation at the

Risk-Based Investing & Asset Management Final Examination

Risk-Based Investing & Asset Management Final Examination Thierry Roncalli February 6 th 2015 Contents 1 Risk-based portfolios 2 2 Regularizing portfolio optimization 3 3 Smart beta 5 4 Factor investing

Risk-Based Investing & Asset Management Final Examination Thierry Roncalli February 6 th 2015 Contents 1 Risk-based portfolios 2 2 Regularizing portfolio optimization 3 3 Smart beta 5 4 Factor investing

APPEND I X NOTATION. The product of the values produced by a function f by inputting all n from n=o to n=n

APPEND I X NOTATION In order to be able to clearly present the contents of this book, we have attempted to be as consistent as possible in the use of notation. The notation below applies to all chapters

APPEND I X NOTATION In order to be able to clearly present the contents of this book, we have attempted to be as consistent as possible in the use of notation. The notation below applies to all chapters

BUSM 411: Derivatives and Fixed Income

BUSM 411: Derivatives and Fixed Income 3. Uncertainty and Risk Uncertainty and risk lie at the core of everything we do in finance. In order to make intelligent investment and hedging decisions, we need

BUSM 411: Derivatives and Fixed Income 3. Uncertainty and Risk Uncertainty and risk lie at the core of everything we do in finance. In order to make intelligent investment and hedging decisions, we need

Capital Markets Assumptions 2018

Capital Markets Assumptions 2018 I. Overview Capital markets assumptions are the expected returns 1, standard deviations, and correlation estimates that represent the long-term risk/return forecasts for

Capital Markets Assumptions 2018 I. Overview Capital markets assumptions are the expected returns 1, standard deviations, and correlation estimates that represent the long-term risk/return forecasts for

Note 11. Portfolio Return and Risk, and the Capital Asset Pricing Model

Note 11 Portfolio Return and Risk, and the Capital Asset Pricing Model Outline Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing

Note 11 Portfolio Return and Risk, and the Capital Asset Pricing Model Outline Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing

1- The Role of Strategic Asset Allocation in Relation to Systematic Risk

READING 21: ASSET ALLOCATION A- What is Asset Allocation Asset allocation is a process and a result. In strategic asset allocation, an investor s return objectives, risk tolerance, and investment constraints

READING 21: ASSET ALLOCATION A- What is Asset Allocation Asset allocation is a process and a result. In strategic asset allocation, an investor s return objectives, risk tolerance, and investment constraints

Applying Index Investing Strategies: Optimising Risk-adjusted Returns

Applying Index Investing Strategies: Optimising -adjusted Returns By Daniel R Wessels July 2005 Available at: www.indexinvestor.co.za For the untrained eye the ensuing topic might appear highly theoretical,

Applying Index Investing Strategies: Optimising -adjusted Returns By Daniel R Wessels July 2005 Available at: www.indexinvestor.co.za For the untrained eye the ensuing topic might appear highly theoretical,

Key investment insights

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

Improving Returns-Based Style Analysis

Improving Returns-Based Style Analysis Autumn, 2007 Daniel Mostovoy Northfield Information Services Daniel@northinfo.com Main Points For Today Over the past 15 years, Returns-Based Style Analysis become

Improving Returns-Based Style Analysis Autumn, 2007 Daniel Mostovoy Northfield Information Services Daniel@northinfo.com Main Points For Today Over the past 15 years, Returns-Based Style Analysis become

The Case for TD Low Volatility Equities

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

Modern Portfolio Theory -Markowitz Model

Modern Portfolio Theory -Markowitz Model Rahul Kumar Project Trainee, IDRBT 3 rd year student Integrated M.Sc. Mathematics & Computing IIT Kharagpur Email: rahulkumar641@gmail.com Project guide: Dr Mahil

Modern Portfolio Theory -Markowitz Model Rahul Kumar Project Trainee, IDRBT 3 rd year student Integrated M.Sc. Mathematics & Computing IIT Kharagpur Email: rahulkumar641@gmail.com Project guide: Dr Mahil

Investment In Bursa Malaysia Between Returns And Risks

Investment In Bursa Malaysia Between Returns And Risks AHMED KADHUM JAWAD AL-SULTANI, MUSTAQIM MUHAMMAD BIN MOHD TARMIZI University kebangsaan Malaysia,UKM, School of Business and Economics, 43600, Pangi

Investment In Bursa Malaysia Between Returns And Risks AHMED KADHUM JAWAD AL-SULTANI, MUSTAQIM MUHAMMAD BIN MOHD TARMIZI University kebangsaan Malaysia,UKM, School of Business and Economics, 43600, Pangi

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Growth-indexed bonds and Debt distribution: Theoretical benefits and Practical limits

Growth-indexed bonds and Debt distribution: Theoretical benefits and Practical limits Julien Acalin Johns Hopkins University January 17, 2018 European Commission Brussels 1 / 16 I. Introduction Introduction

Growth-indexed bonds and Debt distribution: Theoretical benefits and Practical limits Julien Acalin Johns Hopkins University January 17, 2018 European Commission Brussels 1 / 16 I. Introduction Introduction

Financial Markets & Portfolio Choice

Financial Markets & Portfolio Choice 2011/2012 Session 6 Benjamin HAMIDI Christophe BOUCHER benjamin.hamidi@univ-paris1.fr Part 6. Portfolio Performance 6.1 Overview of Performance Measures 6.2 Main Performance

Financial Markets & Portfolio Choice 2011/2012 Session 6 Benjamin HAMIDI Christophe BOUCHER benjamin.hamidi@univ-paris1.fr Part 6. Portfolio Performance 6.1 Overview of Performance Measures 6.2 Main Performance

Statistical Models and Methods for Financial Markets

Tze Leung Lai/ Haipeng Xing Statistical Models and Methods for Financial Markets B 374756 4Q Springer Preface \ vii Part I Basic Statistical Methods and Financial Applications 1 Linear Regression Models

Tze Leung Lai/ Haipeng Xing Statistical Models and Methods for Financial Markets B 374756 4Q Springer Preface \ vii Part I Basic Statistical Methods and Financial Applications 1 Linear Regression Models

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Economics 483. Midterm Exam. 1. Consider the following monthly data for Microsoft stock over the period December 1995 through December 1996:

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

Quantitative Measure. February Axioma Research Team

February 2018 How When It Comes to Momentum, Evaluate Don t Cramp My Style a Risk Model Quantitative Measure Risk model providers often commonly report the average value of the asset returns model. Some

February 2018 How When It Comes to Momentum, Evaluate Don t Cramp My Style a Risk Model Quantitative Measure Risk model providers often commonly report the average value of the asset returns model. Some

Markowitz portfolio theory

Markowitz portfolio theory Farhad Amu, Marcus Millegård February 9, 2009 1 Introduction Optimizing a portfolio is a major area in nance. The objective is to maximize the yield and simultaneously minimize

Markowitz portfolio theory Farhad Amu, Marcus Millegård February 9, 2009 1 Introduction Optimizing a portfolio is a major area in nance. The objective is to maximize the yield and simultaneously minimize

Lecture 2: Fundamentals of meanvariance

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each