Microéconomie de la finance

|

|

|

- Maurice Gregory

- 5 years ago

- Views:

Transcription

1 Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1

2 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2

3 Introduction The Single-Index Model - Simplifying MV optimisation CAPM: Equilibrium model - One factor, where the factor is the excess return on the market. - Based on mean-variance analysis Arbitrage Pricing Theory (APT) - Empirical factors 3-4 CAPM - Beta is dead - Style analysis

4 Part 6. Asset Pricing Models 6.1 MV Optimization Pitfalls 6.2 Single-Index Model 6.3 CAPM 6.4 APT and Multi-Factor Models

5 6.1 MV Optimization Pitfalls

6 Three-Security Portfolio r p = W 1 r 1 + W 2 r 2 + W 3 r 3 s 2 = W 2 p 12 s 12 + W 22 s W 32 s W 1 W 2 Cov(r 1,r 2 ) + 2W 1 W 3 Cov(r 1,r 3 ) + 2W 2 W 3 Cov(r 2,r 3 )

7 In General, n-security Portfolio r p = Weighted average of the n-securities returns s 2 p = Own variance terms + all pair-wise covariances

8 MV Optimization Example Input Data for Asset Allocation Expected return, volatility, correlations

9 MV Optimization Results Efficient frontier with riskless lending and borrowing, and short sales allowed Diversification benefits are substantial

10 Pitfalls with the MV Optimisation Need large amount of input data Expected return, volatility, correlations Estimated portfolio weights are sensitive to estimation errors Small changes in mean returns have large effects on the efficient portfolio weights (Jorion, 1991) How long past time-period is necessary for the estimation? Volatility and correlations change over time, add predictions Static model, without considering rebalancing Transaction costs such as bid-ask spreads, price pressure (market impact), and brokerage fees should be considered.

11 Too many inputs for MV Analysis Expected return: E(R p ) = i w i E(R i ) N expected returns for N assets Std. Dev : p2 = i w i2 i2 + i j,i j w i w j i j ij N variances for N assets N(N-1) correlations for N assets Actually, we need N(N-1)/2 correlations since ij = ji For example, it amounts to 19,900 correlations for 200 assets Altogether, we need 2N+N(N-1)/2 estimates for the MV analysis Most of security analysts focus on estimating expected returns and variance for a limited number of securities. Pair-wise correlations across all assets have to be estimated from some kinds of models, which we are searching for The simplest model is the single-index model

12 6.2 The Single Index Model

13 Single Index Model: Individual Asset s Expected return Assuming that the market index is a common factor describing stock returns - We write stock returns as in the following form: (r i r f ) = i + i (r m r f ) + e i, or R i = i + i R m + e i where E(e i ) = 0 assumed. - This relates stock returns to the returns on a common factor, such as the S&P 500 Stock Index,

14 Single Index Model: Two Components It divides stock returns into two components A market-related part, i R m i measures the sensitivity of a stock to market movements A non-market-related or unique part, i + e i Therefore, expected return can be written as, E(R i ) = i + i E(R m )

15 Single Index Model: Systematic Risk & Unsystematic Risk It also divides a security s variance (total risk) into market risk & unique risk i2 = i2 m2 + ei 2 - This is obtained from taking variance operator on both sides of the single index model: Var (R i ) = Var( i + i R m + e i ) i2 = i2 m2 + ei 2.- From this, we see the following holds: i2 m 2 / i2 = 1- ei2 = i,m 2 Systematic Risk / Total Risk = i,m 2

16 Single Index Model: Individual Asset s Covariance If securities are related only in their response to the market: - Securities covary together, only because of their relationship to the market index, and thus, - Security covariances depend only on market risk: ij = i j m 2

17 Single Index Model: Individual Asset s Covariance ij = i j m 2 which is obtained as in the following: ij = E{[R i E(R i )][R j E(R j )]} = E{[( i + i R m + e i ) ( i + i E(R m ))] [( j + j R m + e j ) ( j + j E(R m ))]} = E{[ i (R m E(R m ) + e i ][ j (R m E(R m ) + e j ]} = i j E[R m E(R m )] 2 + i E[e j (R m E(R m ))] + j E[e i (R m E(R m ))] + E(e i e j ) = i j m 2 Note that E[e j R m ] = 0 and E(e i e j ) = 0 assumed above

18 Number of inputs for the MV Analysis Now, we need the following inputs for the MV analysis: E(R i ) = i + i E(R m ) i2 = i2 m2 + ei 2 ij = i j m 2 - That is, we need N i s, N i s, 1 E(R m ), 1 m2, and N ei2, which are 3N+2 estimates, instead of 2N+N(N-1)/2 without an index model

19 Advantage of the Single Index Model Reduces the number of inputs for portfolio optimization. Example: 50 (N) stocks, how many inputs? Expected Returns 50 N Variances 50 N Covariances 50*(50-1)/2=1225 N*(N-1)/2 Total 1325 N*(N+3)/2

20 Number of inputs for portfolio optimization Inputs required with a single-index model. What is the reduction in number of inputs? Expected (Excess) Returns 50 N betas 50 N Firm specific risk 2 (e i ) 50 N Market risk M Market Excess Returns 1 1 Total 152 3N+2

21 Well-diversified portfolio s Expected return Now, consider a well-diversified portfolio p with N assets: E(R p ) = i w i E(R i ) = i w i [ i + i E(R m )] (by the single index model) = i w i i + i w i i E(R m ) = p + p E(R m ) - This would equal the expected return on the market portfolio if p = 0 and p = 1 Thus, we see that the beta on the market should be 1

22 Well-diversified portfolio s Variance Now, look at the variance of the well-diversified portfolio: p2 = i w i2 i2 + i j,i j w i w j ij = i w i2 [ i2 m2 + ei2 ] + i j,i j w i w j [ i j m2 ] = i j w i w j i j m2 + i w i2 ei 2 = [ i w i i ][ i w j j ] m2 + i w i2 ei 2 = p2 m2 + i w i2 ei 2 p2 m2 = m2 [ i w i i ] 2 - Thus, the contribution of individual asset s risk to the portfolio is only thru i, and residual risk is diversified away by forming the welldiversified portfolio

23 Estimating the Index Model Regression analysis is often used to estimate an index model - Try to fit a best line - Dependent variable (Y): excess return of individual security (portfolio) - Independent variable (X): excess market return.

24 Security Characteristics Line Estimation of Harley's Beta (12/ /2008: 251 obs.) 60% 50% 40% 30% 20% Harley 10% 0% -10% -20% -30% -40% -20% -15% -10% -5% 0% 5% 10% 15% S&P500

25 Estimating the Index Model What is the best line? Minimize the prediction error What is the prediction error? Deviation of data points from predicted data points. We will square the deviations so that the positive deviations and negative deviations do not cancel each other out This estimation method is known as the least squared error (LSE) method.

26 Security Characteristics Line Estimation of Harley's Beta (12/ /2008: 251 obs.) 60% 50% 40% y = 1,3402x + 0,0141 R 2 = 0, % 20% Harley 10% 0% -10% -20% -30% -40% -20% -15% -10% -5% 0% 5% 10% 15% S&P500

27 Regression Results (using DROITEREG in Excel) r r ( r r ) ( r r ) Ha f m f m f Beta alpha SE SE R² SE(Y) F df SS reg SS err R² 1 SS SS err tot SS SS reg tot SS y y 2 tot ( t ) t 2 ( ˆ reg t ) tot reg err t SS y y SS SS SS 2 SS ( ˆ err yt yt ) t

28 Components of Risk Market or systematic risk: - risk related to the macro economic factor or market index. Unsystematic or firm specific risk: - risk not related to the macro factor or market index. Total risk = Systematic + Unsystematic

29 Measuring Components of Risk p 2 = p2 m (e i ) where: p 2 = total variance p2 m 2 = systematic variance 2 (e p ) = unsystematic variance

30 Examining Percentage of Variance Total Risk = Systematic Risk + Unsystematic Risk Systematic Risk/Total Risk = R 2 ß i 2 m 2 / 2 = R 2 2 (e i )/ 2 = 1-R 2

31 Index Model and Diversification Case of An Equally-Weighted Portfolio Return model for Portfolio P Beta for portfolio P Alpha for the portfolio Error term for the portfolio Risk for the portfolio

32 An Example Consider two stocks A & B with the following characteristics. Stock E(R) Beta i (e) A B The market index has a std of 22, and the risk free rate is 8. - What are the stds of stocks A and B? - Hint: first, find the variances ( e ) A A M A ( e ) B B M B

33 An Example (Cont d) Suppose that you were to construct a portfolio with w A =.30, w B =0.45, w f =0.25. What is the expected return of the portfolio? - Expected return on a portfolio is weighted average of returns of individual assets. E(r P ) w A E(r A ) w B E(r B ) w f r f (0.3013) (0.4518) (0.258) 14

34 An Example (Cont d) ) ( ) ( ) ( ) ( f f B B A A P e w e w e w e What is the non-systematic standard deviation of the portfolio? Because covariance between individual asset s nonsystematic risk is zero. We have 2 ( ) ( ) 405 P P e e 0) (0.25 ) 40 (0.45 ) 30 (

35 p wa β A wb β B w f β f An Example (Cont d) What is the standard deviation of the portfolio? - Recall: ( e ) p p M p - Therefore, we need portfolio beta - Beta of a portfolio is a weighted average of individual betas. ( ) ( ) (0.250) P M - We already have 2 (e P ). 2 P 2 P 2 M 2 ( e P )

36 Estimating Beta It is common to estimate the beta from running a regression with past data, and use this historical beta as an estimate for the future beta Problem with the historical beta - Beta estimates have a tendency to regress toward one - Beta may change over time - Adjusting historical beta to get a better forecast of betas or correlations

37 Adjusting Beta Many analysts adjust estimated betas to obtain better forecasts of future betas. Merrill Lynch adjusts beta estimates in a simple way: - Adjusted beta = 2/3 sample beta + 1/3 (1) When using daily or weekly returns, run a regression with lagged and leading market returns. - R it = a i + b 1 R mt-1 + b 2 R mt + b 3 R mt+1 - The estimate of beta is: Beta i = b 1 + b 2 + b 3.

38 Adjusted Beta Contents r i Fundamental Blume Vasicek S i i 0 f f 1 F f u i ˆ ˆ ˆ i i 2 1 t ˆ ˆ i* i 2 i i 2 1 ( 1 ) 1; 2 i i 1 Performance Work for the same industry Average sensitivity of firm Depending on the size of the uncertainty Bias Non-symmetry Upward forecast underestimation Accuracy Property of firm moderate good Fundamental factors: dividend payout, asset growth, leverage, liquidity, asset size, earning variability.

39 Index Model in Practice - Tracking Portfolios A portfolio with the following estimates: R P = R S&P500 + e P Is this portfolio desirable? Anything you could do to profit from your knowledge? Should you buy or sell assets in portfolio P? What if market moves unfavorably?

40 Tracking Portfolios What if market moves unfavorably? - Solution: try to neutralize the market movements. - Take an opposite position in the market portfolio (S&P 500) so that the effect of market movement can be removed. Let s call the opposite position as T. How large should be the beta of T? How to achieve it? in S&P 500. What is weight in T?. Need to take position in T-bill so that the weight in T is 1.0. How much to take? Therefore, the final position of T should be S&P500 + Tbills.

41 Tracking Portfolios What if market moves unfavorably? - Solution: try to neutralize the market movements. - Take an opposite position in the market portfolio (S&P 500) so that the effect of market movement can be removed. Let s call the opposite position as T. How large should be the beta of T? 1.4 How to achieve it? 1.4 in S&P 500. What is weight in T? 1. Need to take position in T-bill so that the weight in T is 1.0. How much to take? -.4 Therefore, the final position of T should be 1.4 S&P Tbills.

42 Tracking Portfolios What return will your combined position of P and T generate? R C =R P -R T =( XR S&P +e P ) 1.4XR S&P = e P Is there any risk in this strategy? This strategy is often called as the Long-short strategy, and is commonly used by many hedge funds! Use futures contracts to hedge your portfolio

43 6.3 CAPM

44 Capital Asset Pricing Model (CAPM) Assumptions Investors are price takers Investors have homogeneous expectations One period model Presence of a riskless asset No taxes, transaction costs, regulations or short-selling restrictions (perfect market assumption) Information is costless and available to all investors. Returns are normally distributed or investor s utility is a quadratic function in returns (MV optimisers)

45 CAPM Derivation Return m Efficient frontier R f p For a well-diversified portfolio, the equilibrium return is: E( Rm R f ) E( R ) R p f p m

46 CAPM Derivation For the individual security, the return-risk relationship is determined by using the following: E( R ) we( R ) (1 w) E( R ) p i m w (1 w) 2 w(1 w) p i m im 1/2 Rp Ri Rm w w p 2w i 2(1 w) m 2 im 4w im p

47 CAPM Derivation At the equilibrium, the excess weight of the security i in the market portfolio is 0, w = 0: R p w w0 2 2 w p m im im m w0 R i R m m m

48 CAPM Derivation The slope of this tangential portfolio at m must equal to: E( R R ) m m Thus : f E( Rm R f ) Rp Rp w E( Ri ) E( Rm ) w 2 m p p w0 im m m Then, we obtain the CAPM: E( R ) R E( R ) R m f i f 2 im m

49 Resulting Equilibrium Conditions All investors will hold the same portfolio for risky assets market portfolio Market portfolio contains all securities and the proportion of each security is its market value as a percentage of total market value.

50 Resulting Equilibrium Conditions (cont d) Risk premium on the market depends on the average risk aversion of all market participants. Risk premium on an individual security is a function of its covariance with the market.

51 The Premium of the Market Portfolio Let s assume that there are 3 investors, with risk aversion parameters A 1, A 2, and A 3. Each has $1 to invest. Recall (session 3; slide 12) that the optimal weight each investor assigns to the risky market portfolio should be: Investor Weight on market portfolio E( R ) R M A M E( R ) R M A M E( R ) R M A M f f f

52 The Premium of the Market Portfolio (cont d) The total money invested in the market portfolio therefore is: E( R ) R E( R ) R E( R ) R A A A M f M f M f M M M E( RM ) R f A1 A2 A3 M

53 The Premium of the Market Portfolio (cont d) What should be the total investment in the market portfolio? Let s take a look at a simple example. Let A 1 =1.5, A 2 =2, A 3 =3, and E(R m )-R f =9%, m =20%. Investor A x* 1-x* % 70% % 77.5% % 85%

54 The Premium of the Market Portfolio (cont d) What if E(R m )-R f =6%, m =20%? Investor A x* 1-x* % 80% % 85% % 90%

55 The Premium of the Market Portfolio (cont d) In a simplified economy, risk-free investment involve borrowing and lending among investors. - Any borrowing must be offset by the lending position i.e. net lending and net borrowing across all investors must be zero. E ( rm ) r f A1 A 2 A 3 M 1 E ( r ) r A M f 2 M Where A is called the (harmonic) average of A 1, A 2, and A 3 1 A A 1 1 A 2 1 A 3

56 The Premium of the Market Portfolio and Risk Aversion Historical market risk premium (proxied by the S&P 500 index) is 8.2% The standard deviation of the market portfolio is 20.6%. Based on these statistics, what is the average coefficient of risk aversion? E( r M ) r f 8.2 A 2 M A A Risk premium (E(R M ) R f ) on the market depends on the (harmonic) average risk aversion of all market participants.

57 Return and Risk For Individual Securities The risk premium on individual securities is a function of the individual security s contribution to the risk of the market portfolio. An individual security s risk premium is a function of the covariance of returns with the assets that make up the market portfolio.

58 Return and Risk For Individual Securities Simplified Derivation For simplicity, let s assume that there are only three assets in the market, then: R w R w R w R M R R w ( R R ) w ( R R ) M f 1 1 f 2 2 f w ( R R ) 3 3 Therefore, the marginal contribution of asset 1 to the expected risk premium of the market portfolio is: f w1 E( R1 ) R f

59 Return and Risk For Individual Securities Simplified Derivation (Cont d) Now, let s look at the variance of the market portfolio R w R w R w R M Var( r ) Cov( R, R ) M M M Cov( w R w R w R, R ) w Cov( R, R ) w Cov( R, R ) w Cov( R, R ) 1 1 M 2 2 M 3 3 M M The marginal contribution of asset 1 to the risk (variance) of the market portfolio is: w1 Cov R1 R M (, )

60 Return and Risk For Individual Securities Simplified Derivation (Cont d) The reward-to-risk ratio for asset 1 therefore is w1 ( E( R1 ) R f ) E( R1 ) R f w Cov( R, R ) Cov( R, R ) 1 1 M 1 M Now, recall that the market reward to risk ratio is: E( R ) R M 2 M f

61 Return and Risk For Individual Securities Simplified Derivation (Cont d) In equilibrium, the reward to risk ratio should be the same for all the assets. - Why? - Therefore, E( R1 ) R E( R ) R Cov( R, R ) 1 M f M f 2 M - since, E( R1 ) R E( R ) R Cov( R, R ) 1 f M f 2 M M Cov( R, R ) E( R ) R E( R ) r 1 M 1 f 2 M f M

62 Return and Risk For Individual Securities Simplified Derivation (Cont d) We call the following ratio as the beta for asset 1. Cov( R, RM ) M The equation for the expected rate of return can be simplified as: E( R ) R E( R ) R 1 f 1 M f E( R ) R E( R ) R 1 f 1 M f We did it! This is the CAPM model

63 Return and Risk For Individual Securities Beta of security i measures how the return of i moves with the return of the market. In other words, it is a measure of the systematic risk. Only systematic risk matters in determining the equilibrium expected return. Unsystematic risk affects only a single security or a limited number of securities. Systematic risk affects the entire market.

64 The Security Market Line (SML) E( R ) R E( R ) R i f i M f SML Expected return M R f Risk Premium E(R M ) R f ) = slope of the SML

65 Examples of SML E(R m ) - R f =.08 R f =.03 - What is the expected return for a security with a beta of 0? - What is the expected return for a security with a beta of 0.6? - What is the expected return for a security with a beta of 1.25?

66 Graph of Sample Calculations R x =13% R M =11% E(R) SML Slope=0.08 R y =7.8% 3% 0 f.6 y x

67 The CAPM and Beta Facts about beta If > 1.0, the security moves more than the market when the market moves If < 1.0, the security moves less than the market when the market moves. So, if > 1.0, the asset has more risk relative to the market portfolio and if < 1.0, the asset is has less risk relative to the market portfolio. Since all risk is measured relative to the market portfolio, the beta of the market portfolio must be 1.0.

68 Alpha and Disequilibrium The difference between the actual expected rate of return and that dictated by the SML is called as alpha. i E( ri ) [ rf i ( E( rm ) rf )] What should alpha be if a security is fairly priced according to CAPM?

69 Disequilibrium Example E(R m ) - R f =.08 R f =.03 - Suppose a security with a of 1.25 is offering expected return of 15%. - According to SML, it should be 13%. - What is the alpha for this security? - Is this security overpriced or underpriced, why?

70 Disequilibrium Example E(R) SML 15% 13% r f =3%

71 Alpha and Security Price What would happen if alpha is positive/negative? When are securities overpriced or underpriced?

72 The Security Market Line and Over- Undervaluation Identifying undervalued and overvalued assets - In equilibrium, all assets and portfolios of assets should fall on the SML. - Therefore, we can compare a security s estimated (or expected) return with its required return from the SML (CAPM) to determine if the asset is overvalued or undervalued.

73 The Security Market Line and Over- Undervaluation Identifying undervalued and overvalued assets If a security s expected return is below its required return, based upon the SML, it is overvalued and If a security s estimated return is above its required return, based upon the SML, it is undervalued.

74 The Security Market Line and Over- Undervaluation CAPM Example Investment Required return Beta Expected Return from CAPM A 14% % B 5% 0 4% C.75 10% D % E %

75 The Security Market Line and Over- Undervaluation CAPM Example Rm = 14%, Rf = 5% Why? See Required returns from the CAPM C: (14-5) = 11.75% D: (14-5) = 25.7% E: (14-5) = 15.8%

76 The Security Market Line and Over- Undervaluation CAPM Example: If we compare required returns to expected returns, investments A and E are undervalued and investments B, C, and D are overvalued. Graphically, this means investments A and E plot above the security market line and investments B, C, and D plot below the security market line.

77 Example of using the SML to identify overvalued and undervalued assets SML Expected return A E D R f C B 1

78 Extensions of CAPM Black s Zero Beta Model CAPM and Liquidity

79 Extensions of CAPM Black s Zero Beta Model - Absence of a risk-free asset - Combinations of portfolios on the efficient frontier are efficient. - All frontier portfolios have companion portfolios that are uncorrelated. - Returns on individual assets can be expressed as linear combinations of efficient portfolios.

80 Efficient Portfolios and Zero Companions E(R) E[R z (Q) ] E[R z (P) ] P Z(Q) Q Z(P) s

81 Zero Beta Market Model Cov( Ri, RM ) E( R ) E( R ) E( R ) E( R ) i Z ( M ) M Z ( M ) 2 M CAPM with E(R z (m) ) replacing R f

82 CAPM & Liquidity Liquidity Illiquidity Premium - If there are two assets with identical expected rate of returns and beta, but one costs more to trade, which asset do you prefer? Research supports a premium for illiquidity. - Amihud and Mendelson - Acharya and Pedersen

83 CAPM with a Liquidity Premium E( R ) R [ E( R ) R ] f ( c ) i f i i f i f (c i ) = liquidity premium for security i f (c i ) increases at a decreasing rate

84 Liquidity and Average Returns Average monthly return(%) Bid-ask spread (%)

85 Empirical tests of the CAPM: Is Beta Dead? Under CAPM, Beta is only risk - Higher ß higher return, & vice versa - Evidence is weak: the relationship between beta and rates of return is a moot point Fix Beta? - Treat as nonstationary Acknowledge other sources of risk? - Size, P/B ratio, skewness, leverage, inflation, momentum (overreactions)

86 Returns to Beta: Is Beta Dead? Mean Beta Monthly Mean Group Return (%) Beta 1 (High) (Low) Average Monthly Returns and Estimated Betas from July 1963 to December 1990 for Ten Beta Groups

87 Returns to Size Mean Size Mean Monthly Group Beta Return (%) 1 (Large) (Small) Average Monthly Returns and Estimated Betas from July 1963 to December 1990 for Ten Size Groups

88 Returns to Fundamental: Price-to-Book Mean Price/Book Monthly Mean Group Return (%) Beta 1 (High) (Low) Average Monthly Returns and Estimated Betas from July 1963 to December 1990 for Ten Price/Book Groups.

89 Returns to Fundamental Screens: Value vs Glamour/Growth high low Growth in sales high Cash-flow-to-price ratio low Value 5-year returns Glamour/ Growth Source: Lakonishok, Shleifer, & Vishny, Contrarian Investment, Extrapolation, and Risk, Journal of Finance, Vol. 49, No. 5. (Dec., 1994), p 1554.

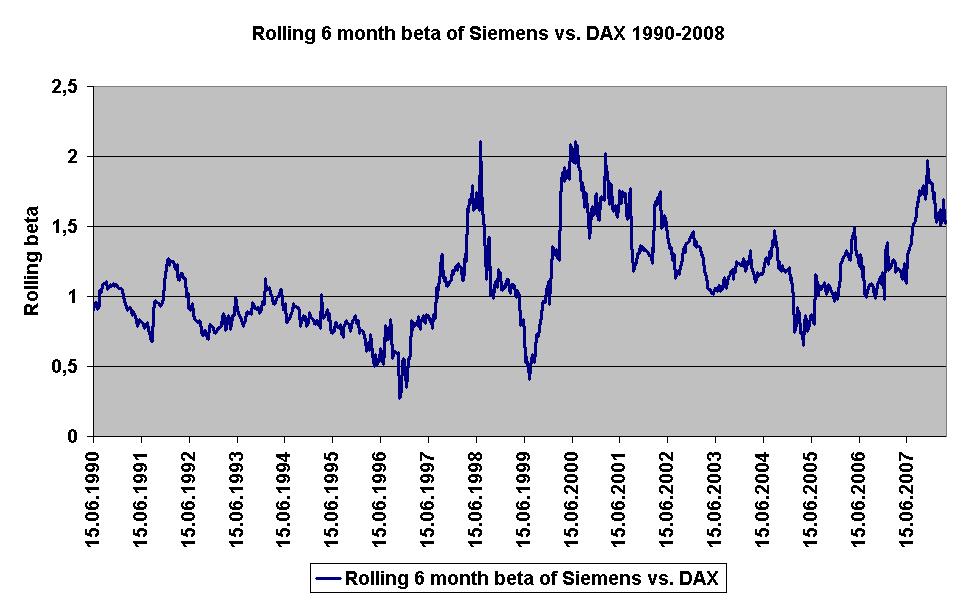

90 Time-varying Beta Siemens-Beta vs. DAX Index between estimated at 1.2 Source: Bloomberg

91 Time-varying Beta Siemens-Beta vs. DAX Index between (bull market) estimated at 0.99 Source: Bloomberg

92 Time-varying Beta Siemens-Beta vs. DAX Index between (bear market) estimated at 1.47 Source: Bloomberg

93 Time-varying Beta

94 Alternatives to the CAPM Factor models (APT) - Factor models assume that the return generating process on a security is sensitive to the movement of various factors or indices. - A factor model attempts to capture the major economic forces that systematically move the prices of all securities. Fama-French 3-factor Model (4-5-6 factors)

95 Roll Critique The market portfolio is unobservable so you have to use a proxy So if the CAPM is true, but your proxy is off, you can reject the model. On the other hand if the CAPM is false, but the proxy is meanvariance efficient you can not reject the model So the CAPM is not testable!!!

96 6.4 APT and Multi-Factor Models

97 The APT : Some Thoughts The Arbitrage Pricing Theory New and different approach to determine asset prices. Based on the law of one price : two items that are the same cannot sell at different prices. Requires fewer assumptions than CAPM Assumption : each investor, when given the opportunity to increase the return of his portfolio without increasing risk, will do so. Mechanism for doing so : arbitrage portfolio

98 Arbitrage Portfolio Arbitrage portfolio requires no own funds Assume there are 3 stocks : 1, 2 and 3 X i denotes the change in the investors holding (proportion) of security i, then X 1 + X 2 + X 3 = 0 No sensitivity to any factor, so that b 1 X 1 + b 2 X 2 + b 3 X 3 = 0 Example : 0.9 X X X 3 = 0 (assumes zero non factor risk)

99 Single Factor Model Returns on a security come from two sources Common macro-economic factor Firm specific events Possible common macro-economic factors Gross Domestic Product Growth Interest Rates

100 Single Factor Model Equation r i = E(r i ) + Beta i (F) + e i r i = Return for security I Beta i = Factor sensitivity or factor loading or factor beta F = Surprise in macro-economic factor (e.g. unexpected change in GDP) (F could be positive, negative or zero) e i = Firm specific events

101 Multifactor Models Use more than one factor Examples include gross domestic product, expected inflation, interest rates etc. Estimate a beta or factor loading for each factor using multiple regression.

102 Multifactor Model Equation r i = E(r i ) + Beta GDP (GDP) + Beta IR (IR) + e i r i = Return for security I Beta GDP = Factor sensitivity for GDP Beta IR = Factor sensitivity for Interest Rate e i = Firm specific events

103 Example Example: Beta GDP = 1.2, Beta IR =0.7, E(r i )=0.10 If GDP is revised to be 1% higher than expected, what should be your revised E(r i )? If interest rate is revised to be 1% lower than expected, what should be your revised E(r i )?

104 Example (solution) Example: Beta GDP = 1.2, Beta IR =0.7, E(r i )=0.10 If GDP is revised to be 1% higher than expected, what should be your revised E(r i )? = x 0.01 = If interest rate is revised to be 1% lower than expected, what should be your revised E(r i )? = x 0.01 = 0.093

105 Multifactor SML Models E(r) = r f + GDP RP GDP + IR RP IR GDP = Factor sensitivity for GDP RP GDP = Risk premium for GDP, which is the difference in the expected return of a portfolio ( GDP =1, IR =0) and the risk free rate. IR = Factor sensitivity for Interest Rate RP IR = Risk premium for IR, which is the difference in the expected return of a portfolio ( GDP =0, IR =1) and the risk free rate.

106 Multifactor SML - An Example r f = 4.0% GDP = 1.2 RP GDP = 6% IR = -.3 RP IR = -7% E(r) = r f + GDP RP GDP + IR RP IR = 13.3%

107 Arbitrage Pricing Theory Arbitrage - arises if an investor can construct a zero investment portfolio with a sure profit. Since no investment is required, an investor can create large positions to secure large levels of profit. In efficient markets, profitable arbitrage opportunities will quickly disappear.

108 APT & Well-Diversified Portfolios r P = E (r P ) + P F + e P F = some common factor For a well-diversified portfolio: Systematic risk or factor risk is captured by P, which is the weighted average of betas of individual assets. Unsystematic risks cancel each other out, therefore e P approaches zero, similar to CAPM.

109 Portfolios and Individual Security E(r)% E(r)% F F Portfolio Individual Security

110 Disequilibrium Example E(r)% 10 A 6 r f = 4 C Beta for F

111 Disequilibrium Example Which portfolio is over-valued? What to do with this portfolio? Any portfolio undervalued? Can we buy a fairly priced portfolio instead? How to control for systematic risk? Use funds to construct an equivalent risk higher return Portfolio D. D is composed of A & Risk-Free Asset What are weights of A and RF in Portfolio D? What is the arbitrage profit?

112 Disequilibrium Example E(r)% Create a portfolio D composed of half of portfolio A and half of the risk free rate r f = 4 D C A Beta for F

113 Disequilibrium Example E(r)% Arbitrage portfolio: D - C D has an equal beta but greater expected return r f = 4 D C A Beta for F

114 More Disequilibrium Examples Portfolio E(r) Beta A 12% 1.2 F 6% 0.0 E 8% 0.6 Is there an arbitrage opportunity? Yes. Reward to risk ratios are different. How to arbitrage? ½ A + ½ F (Long or short) E (long or short)

115 More Disequilibrium Examples Portfolio E(r) Beta A 12% 1.2 F 6% 0.0 E 8% 0.6 Is there an arbitrage opportunity? Yes. Reward to risk ratios are different. How to arbitrage? ½ A + ½ F (Long or short) E (long or short)

116 More Disequilibrium Examples Portfolio E(r) Beta X 16% 1.00 Y 12% 0.25 F 8% 0 Is there an arbitrage opportunity? Yes. Reward to risk ratios are different. How to arbitrage? ¼ X + ¾ F (Long or short) Y (long or short)

117 More Disequilibrium Examples Portfolio E(r) Beta X 16% 1.00 Y 12% 0.25 F 8% 0 Is there an arbitrage opportunity? Yes. Reward to risk ratios are different. How to arbitrage? ¼ X + ¾ F (Long or short) Y (long or short)

118 More Disequilibrium Examples What if we do not observe a risk free asset? Portfolio E(r) Beta X 16% 1.25 Y 14% 1.00 Z 8% 0.75 Is there an arbitrage opportunity? How to evaluate? Consider combining two portfolios so that the beta risk of the resulting portfolio is the same as the third portfolio, and compare the expected returns. ½ X + ½ Z (Long or short) Y (long or short)

119 More Disequilibrium Examples What if we do not observe a risk free asset? Portfolio E(r) Beta X 16% 1.25 Y 14% 1.00 Z 8% 0.75 Is there an arbitrage opportunity? How to evaluate? Consider combining two portfolios so that the beta risk of the resulting portfolio is the same as the third portfolio, and compare the expected returns. ½ X + ½ Z (Long or short) Y (long or short)

120 Identifying the Factors Unanswered questions : How many factors? Identity of factors Possible factors (literature suggests : 3 5) Chen, Roll and Ross (1986) Growth rate in industrial production Rate of inflation (both expected and unexpected) Spread between long-term and short-term interest rates Spread between low-grade and high-grade bonds

121 Three approaches to estimate factors Statistical factors Extracted from returns Macroeconomic factors Inflation, term structure, Fundamental factors SMB, HML, etc.

122 Principal Component Analysis (PCA) Technique to reduce the number of variables being studied without losing too much information in the covariance matrix. Objective : to reduce the dimension from N assets or M economics variables to k factors Principal components (PC) serve as factors First PC : (normalised) linear combination of asset returns with maximum variance Second PC : (normalised) linear combination of asset returns with maximum variance of all combinations orthogonal to the first component

123 Pro and Cons of Principal Component Analysis Advantage : Allows for time-varying factor risk premium Easy to compute Disadvantage : interpretation of the principal components, statistical approach

124 APT and CAPM Compared APT applies to well diversified portfolios and not necessarily to individual stocks. With APT it is possible for some individual stocks to be mispriced - not lie on the SML. APT is more general in that it gets to an expected return and beta relationship without the assumption of the market portfolio. APT can be extended to multifactor models.

125 APT and CAPM Compared (Cont d) APT is much robust than CAPM for several reasons: 1. APT makes no assumptions about the empirical distribution of asset returns; 2. APT makes no assumptions on investors utility function; 3. No special role about market portfolio 4. APT can be extended to multiperiod model.

126 Summary APT alternative approach to explain asset pricing Factor model requiring fewer assumptions than CAPM Based on concept of arbitrage portfolio Interpretation : Factor s are difficult to interpret, no economics about the factors and factor weightings.

127 Questions and Problems

128 Exercise 1. Index Model 1. Consider monthly returns on the next slide and calculate: A. Alpha for each stock B. Beta for each stock C. SD of the residuals from each regression D. Correlation coefficient between each security and the market E. Average return of the market F. Variance of the market

129 Exercise 1. Index Model Security Month A B C S&P

130 Exercise 1. Index Model 2. A. Compute the mean return and variance of return for each stock in problem 1 using: (1) The single index model (2) The historical data B. Compute the covariance between each possible pair of stocks using (1) The single index model (2) The historical data C. Compute the return and SD of a 1/N portfolio (equally weighted) using: (1) The single index model (2) The historical data D. Discuss the results

131 Exercise 2. CAPM 1. Assume that the following assets are correctly priced according to the SML. Derive the SML. What is the expected return on an asset with a Beta of two? R 1 = 6% and R 2 = 12% 1 = 0.5 and 2 = Assume the SML given below and suppose that analysts have estimated the Beta of two stocks as follows: x = 0.5 and y = 2. What must the expected return on the two securities be in order for them to be a good purchase? R i = i 3. Assume that over some period a CAPM was estimated. Results are shown below. Assume that over the same period two mutual funds had the following results: R A = 10% and R B = 15% 1 = 0.8 and 2 = 1.2 R i = i What can be said about the fund performance? 4. Consider the CAPM line shown below. What is the excess return of the market over the risk-free rate? What is the risk free rate? Ri = i

132 Exercise 3. APT and Multifactor Models 1. Assume that the following two factor-model describe returns: R i = a i + b i1.i 1 + b i2.i 2 + e i Assume that the following three portfolios are observed: Portfolio Expected Return b i1 b i2 A B C Find the equation of the plane that must describe equilibrium returns 2. Referring to the results of question 1, illustrate the arbitrage opportunities that would exist if a portfolio called D with the following properties were observed: R D = 10 b D1 = 2 b D2 = 0

133 Exercise 3. APT and Multifactor Models 3. Repeat Question 1 if the three portfolios observed have the following characteristics. Portfolio Expected Return b i1 b i2 A B C Referring to the results of Question 3, illustrate the arbitrage opportunities if a portfolio called D with the following properties were observed: R D = 15 b D1 = 1 b D2 = 0

134 Thank you for your attention See you next week

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Index Models and APT

Index Models and APT (Text reference: Chapter 8) Index models Parameter estimation Multifactor models Arbitrage Single factor APT Multifactor APT Index models predate CAPM, originally proposed as a simplification

Index Models and APT (Text reference: Chapter 8) Index models Parameter estimation Multifactor models Arbitrage Single factor APT Multifactor APT Index models predate CAPM, originally proposed as a simplification

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Lecture 3: Factor models in modern portfolio choice

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Quantitative Portfolio Theory & Performance Analysis

550.447 Quantitative Portfolio Theory & Performance Analysis Week of April 15, 013 & Arbitrage-Free Pricing Theory (APT) Assignment For April 15 (This Week) Read: A&L, Chapter 5 & 6 Read: E&G Chapters

550.447 Quantitative Portfolio Theory & Performance Analysis Week of April 15, 013 & Arbitrage-Free Pricing Theory (APT) Assignment For April 15 (This Week) Read: A&L, Chapter 5 & 6 Read: E&G Chapters

Arbitrage Pricing Theory and Multifactor Models of Risk and Return

Arbitrage Pricing Theory and Multifactor Models of Risk and Return Recap : CAPM Is a form of single factor model (one market risk premium) Based on a set of assumptions. Many of which are unrealistic One

Arbitrage Pricing Theory and Multifactor Models of Risk and Return Recap : CAPM Is a form of single factor model (one market risk premium) Based on a set of assumptions. Many of which are unrealistic One

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Financial Markets. Laurent Calvet. John Lewis Topic 13: Capital Asset Pricing Model (CAPM)

") Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

E(r) The Capital Market Line (CML)

The Capital Market Line (CML)") The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Testing Capital Asset Pricing Model on KSE Stocks Salman Ahmed Shaikh

Abstract Capital Asset Pricing Model (CAPM) is one of the first asset pricing models to be applied in security valuation. It has had its share of criticism, both empirical and theoretical; however, with

Abstract Capital Asset Pricing Model (CAPM) is one of the first asset pricing models to be applied in security valuation. It has had its share of criticism, both empirical and theoretical; however, with

LECTURE NOTES 3 ARIEL M. VIALE

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

Mean-Variance Theory at Work: Single and Multi-Index (Factor) Models

Models") Mean-Variance Theory at Work: Single and Multi-Index (Factor) Models Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives The number of parameters in MV problems and the curse

Mean-Variance Theory at Work: Single and Multi-Index (Factor) Models Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives The number of parameters in MV problems and the curse

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Module 3: Factor Models

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

B. Arbitrage Arguments support CAPM.

1 E&G, Ch. 16: APT I. Background. A. CAPM shows that, under many assumptions, equilibrium expected returns are linearly related to β im, the relation between R ii and a single factor, R m. (i.e., equilibrium

1 E&G, Ch. 16: APT I. Background. A. CAPM shows that, under many assumptions, equilibrium expected returns are linearly related to β im, the relation between R ii and a single factor, R m. (i.e., equilibrium

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Common Macro Factors and Their Effects on U.S Stock Returns

2011 Common Macro Factors and Their Effects on U.S Stock Returns IBRAHIM CAN HALLAC 6/22/2011 Title: Common Macro Factors and Their Effects on U.S Stock Returns Name : Ibrahim Can Hallac ANR: 374842 Date

2011 Common Macro Factors and Their Effects on U.S Stock Returns IBRAHIM CAN HALLAC 6/22/2011 Title: Common Macro Factors and Their Effects on U.S Stock Returns Name : Ibrahim Can Hallac ANR: 374842 Date

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

Cost of Capital (represents risk)

") Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Measuring the Systematic Risk of Stocks Using the Capital Asset Pricing Model

Journal of Investment and Management 2017; 6(1): 13-21 http://www.sciencepublishinggroup.com/j/jim doi: 10.11648/j.jim.20170601.13 ISSN: 2328-7713 (Print); ISSN: 2328-7721 (Online) Measuring the Systematic

Journal of Investment and Management 2017; 6(1): 13-21 http://www.sciencepublishinggroup.com/j/jim doi: 10.11648/j.jim.20170601.13 ISSN: 2328-7713 (Print); ISSN: 2328-7721 (Online) Measuring the Systematic

Chapter 6 Efficient Diversification. b. Calculation of mean return and variance for the stock fund: (A) (B) (C) (D) (E) (F) (G)

(B) (C) (D) (E) (F) (G)") Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

CHAPTER III RISK MANAGEMENT

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds Tahura Pervin Dept. of Humanities and Social Sciences, Dhaka University of Engineering & Technology (DUET), Gazipur, Bangladesh

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds Tahura Pervin Dept. of Humanities and Social Sciences, Dhaka University of Engineering & Technology (DUET), Gazipur, Bangladesh

From optimisation to asset pricing

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

An Analysis of Theories on Stock Returns

An Analysis of Theories on Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq.

An Analysis of Theories on Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq.

3. Capital asset pricing model and factor models

3. Capital asset pricing model and factor models (3.1) Capital asset pricing model and beta values (3.2) Interpretation and uses of the capital asset pricing model (3.3) Factor models (3.4) Performance

3. Capital asset pricing model and factor models (3.1) Capital asset pricing model and beta values (3.2) Interpretation and uses of the capital asset pricing model (3.3) Factor models (3.4) Performance

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Capital Asset Pricing Model and Arbitrage Pricing Theory

Capital Asset Pricing Model and Nico van der Wijst 1 D. van der Wijst TIØ4146 Finance for science and technology students 1 Capital Asset Pricing Model 2 3 2 D. van der Wijst TIØ4146 Finance for science

Capital Asset Pricing Model and Nico van der Wijst 1 D. van der Wijst TIØ4146 Finance for science and technology students 1 Capital Asset Pricing Model 2 3 2 D. van der Wijst TIØ4146 Finance for science

Capital Asset Pricing Model

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

Chapter 8: CAPM. 1. Single Index Model. 2. Adding a Riskless Asset. 3. The Capital Market Line 4. CAPM. 5. The One-Fund Theorem

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Certification Examination Detailed Content Outline

Certification Examination Detailed Content Outline Certification Examination Detailed Content Outline Percentage of Exam I. FUNDAMENTALS 15% A. Statistics and Methods 5% 1. Basic statistical measures (e.g.,

Certification Examination Detailed Content Outline Certification Examination Detailed Content Outline Percentage of Exam I. FUNDAMENTALS 15% A. Statistics and Methods 5% 1. Basic statistical measures (e.g.,

Overview of Concepts and Notation

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Financial Markets & Portfolio Choice

Financial Markets & Portfolio Choice 2011/2012 Session 6 Benjamin HAMIDI Christophe BOUCHER benjamin.hamidi@univ-paris1.fr Part 6. Portfolio Performance 6.1 Overview of Performance Measures 6.2 Main Performance

Financial Markets & Portfolio Choice 2011/2012 Session 6 Benjamin HAMIDI Christophe BOUCHER benjamin.hamidi@univ-paris1.fr Part 6. Portfolio Performance 6.1 Overview of Performance Measures 6.2 Main Performance

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Note on Cost of Capital

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

Example 1 of econometric analysis: the Market Model

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Example 1 of econometric analysis: the Market Model IGIDR, Bombay 14 November, 2008 The Market Model Investors want an equation predicting the return from investing in alternative securities. Return is

Uniwersytet Ekonomiczny. George Matysiak. Presentation outline. Motivation for Performance Analysis

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Portfolio Management

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Topic Four: Fundamentals of a Tactical Asset Allocation (TAA) Strategy

Strategy") Topic Four: Fundamentals of a Tactical Asset Allocation (TAA) Strategy Fundamentals of a Tactical Asset Allocation (TAA) Strategy Tactical Asset Allocation has been defined in various ways, including:

Topic Four: Fundamentals of a Tactical Asset Allocation (TAA) Strategy Fundamentals of a Tactical Asset Allocation (TAA) Strategy Tactical Asset Allocation has been defined in various ways, including:

Return, Risk, and the Security Market Line

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Economics 424/Applied Mathematics 540. Final Exam Solutions

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

Empirical Evidence. r Mt r ft e i. now do second-pass regression (cross-sectional with N 100): r i r f γ 0 γ 1 b i u i

: r i r f γ 0 γ 1 b i u i") Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Econ 219B Psychology and Economics: Applications (Lecture 10) Stefano DellaVigna

Stefano DellaVigna") Econ 219B Psychology and Economics: Applications (Lecture 10) Stefano DellaVigna March 31, 2004 Outline 1. CAPM for Dummies (Taught by a Dummy) 2. Event Studies 3. EventStudy:IraqWar 4. Attention: Introduction

Econ 219B Psychology and Economics: Applications (Lecture 10) Stefano DellaVigna March 31, 2004 Outline 1. CAPM for Dummies (Taught by a Dummy) 2. Event Studies 3. EventStudy:IraqWar 4. Attention: Introduction

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below:

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory Hedge Portfolios A portfolio that has zero risk is said to be "perfectly hedged" or, in the jargon of Economics and Finance, is referred

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory Hedge Portfolios A portfolio that has zero risk is said to be "perfectly hedged" or, in the jargon of Economics and Finance, is referred

INVESTMENTS Lecture 2: Measuring Performance

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

The Effect of Kurtosis on the Cross-Section of Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Derivatives and Asset Pricing in a Discrete-Time Setting: Basic Concepts and Strategies

Chapter 1 Derivatives and Asset Pricing in a Discrete-Time Setting: Basic Concepts and Strategies This chapter is organized as follows: 1. Section 2 develops the basic strategies using calls and puts.

Chapter 1 Derivatives and Asset Pricing in a Discrete-Time Setting: Basic Concepts and Strategies This chapter is organized as follows: 1. Section 2 develops the basic strategies using calls and puts.