3. Capital asset pricing model and factor models

|

|

|

- Gwendolyn Howard

- 5 years ago

- Views:

Transcription

1 3. Capital asset pricing model and factor models (3.1) Capital asset pricing model and beta values (3.2) Interpretation and uses of the capital asset pricing model (3.3) Factor models (3.4) Performance indexes 1

2 3.1 Capital asset pricing model and beta values Capital market line (CML) The CML is the tangent line drawn from the risk free point to the feasible region for risky assets. This line shows the relation between r P and σ P for efficient portfolios (risky assets plus the risk free asset). The tangency point M represents the market portfolio, so named since all rational investors (minimum variance criterion) should hold their risky assets in the same proportions as their weights in the market portfolio. If every investor is a mean-variance investor and all have homogeneous expectations on means and variances, then everyone buys the same portfolio. Prices adjust to drive the market to efficiency. 2

3 Based on the risk level that an investor can take, she will combine the market portfolio of risky assets with the risk free asset. 3

4 Equation of the CML: r = r f + r M r f σ M σ, where r and σ are the mean and standard deviation of the rate of return of an efficient portfolio. Slope of the CML = r M r f σ M = price of risk of an efficient portfolio. This indicates how much the expected rate of return must increase when the standard deviation increases by one unit. 4

5 Example Consider an oil drilling venture; current share price of the venture = $875, expected to yield $1,000 in one year. The standard deviation of return, σ = 40%; and r f = 10%. Also, r M = 17% and σ M = 12% for the market portfolio. Question How does this venture compare with the investment on efficient portfolios on the CML? Given this level of σ, the expected rate of return predicted by the CML is r = = 33% The actual expected rate of return = 1,000 1 = 14%, which is well 875 below 33%. This venture does not constitute an efficient portfolio. It bears certain type of risk that does not contribute to the expected rate of return. 5

6 Sharpe ratio One index that is commonly used in performance measure is the Sharpe ratio, defined as r i r f σ i = excess return above riskfree rate. standard deviation We expect Sharpe ratio slope of CML. Closer the Sharpe ratio to the slope of CML, the better the performance of the fund in terms of return against risk. In previous example, Slope of CML = Sharpe ratio of venture = 17% 10% 12% 14% 10% 40% = 7 12 = = 0.1 < Slope of CML. 6

7 Capital Asset Pricing Model (CAPM) Let M be the market portfolio M, then the expected return r i of any asset i satisfies where r i r f = β i (r M r f ) β i = σ im σm 2. Here, σ im is the correlation between the return of risky asset i and the return of the market portfolio M. Remark If we write σ im = ρ im σ i σ M, then r i r f r M r f = ρ im. σ i σ M The Sharpe ratio of asset i is given by the product of ρ im and the slope of CML. 7

8 Assumptions underlying the standard CAPM 1. No transaction costs. 2. Assets are infinitely divisible. 3. Absence of personal income tax. 4. An individual cannot affect the price of a stock by his buying or selling action. 5. Investors are expected to make decisions solely in terms of expected values and standard deviations of the returns on their portfolios. 8

9 6. Unlimited short sales are allowed. 7. Unlimited lending and borrowing at the riskless rate. 8. Investors are assumed to be concerned with the mean and variance of returns, and all investors are assumed to define the relevant period in exactly the same manner. 9. All investors are assumed to have identical expectations with respect to the necessary inputs to the portfolio decision. Both (8) and (9) are called homogeneity of expectations. 9

10 Proof Consider the portfolio with α portion invested in asset i and 1 α portion invested in the market portfolio M. The expected rate of return of this portfolio is and its variance is r α = αr i + (1 α)r M σ 2 α = α 2 σ 2 i + 2α(1 α)σ im + (1 α) 2 σ 2 M. As α varies, (σ α, r α ) traces out a curve in the σ r diagram. The market portfolio M corresponds to α = 0. The curve cannot cross the CML, otherwise this would violate the property that the CML is an efficient boundary of the feasible region. Hence, as α passes through zero, the curve traced out by (σ α, r α ) must be tangent to the CML at M. 10

11 Tangency condition Slope of the curve at M = slope of CML. 11

12 First, we obtain dr α dα = r i r M and so that dσ α dα dσ α dα = ασ2 i + (1 2α)σ im + (α 1)σ 2 M σ α = σ im σm 2. α=0 σ M Next, we apply the relation dr α dσ α = dr α dα dσ α dα to obtain dr α = (r i r M )σ M dσ α α=0 σ im σm 2. However, dr α should be equal to the slope of CML, that is, dσ α α=0 (r i r M )σ M σ im σ 2 M = r M r f σ M. 12

13 Solving for r i, we obtain Now, β i = r i r f r M r f r i = r f + σ im σm 2 (r M r f ) = r f + β i (r M r f ). }{{} β i = expected excess return of asset i over r f expected excess return of market portfolio over r f. Predictability of equilibrium return The CAPM implies that in equilibrium the expected excess return on any single risky asset is proportional to the expected excess return on the market portfolio. The constant of proportionality is β i. 13

14 Alternative proof of CAPM Consider σ im = cov(r i, r M ) = e T i Ωw M, where e i = (0 1 0) = i th co-ordinate vector. Recall w M = Ω 1 (µ r1) b ar so that σ im = (µ r1) i b ar = r i r, provided b ar 0. (1) b ar Also, we recall µ M = c br b ar and σ2 M = c 2rb + r2 a (b ar) 2 so that µ M r = c br b ar r = c 2rb + r2 a (b ar) 2 = (b ar)σ 2 M. (2) Eliminating b ar from eqs. (1) and (2), we obtain r i r = σ im σ 2 M (µ M r). 14

15 What is the interpretation of σ im σ M, where σ im = cov(r i, r M )? Consider σ 2 M = w T M Ωw M, we differentiate with respect to w i and obtain so that 2σ M dσ M dw M i dσ M dw M i = σ im σ M = 2e T i Ωw M = 2σ im or dσ M σ M = β i dw M i. This is a measure of how the change in weight of one asset affecting the relative risk of the market portfolio. 15

16 Beta of a portfolio Consider a portfolio containing n assets with weights w 1, w 2,, w n. Since r P = n i=1 w i r i, we have cov(r P, r M ) = n i=1 w i cov(r i, r M ) so that β P = cov(r P, r M ) σ 2 M = ni=1 w i cov(r i, r M ) σ 2 M = n i=1 w i β i. 16

17 Some special cases of beta values 1. When β i = 0, r i = r f. A risky asset (with σ i > 0) that is uncorrelated with the market portfolio will have an expected rate of return equal to the risk free rate. There is no expected excess return over r f even the investor bears some risk in holding a risky asset with zero beta. These risky assets can be represented by points lying on the horizontal line segment r = r f contained in the feasible region of risky assets in the σ r diagram. 2. When β i = 1, r i = r M. In this case, the risky asset has the same expected rate of return as that of the market portfolio. 17

18 Representation of risky assets with β = 0 and β = 1 in the σ r diagram. 18

19 3. When β i > 1, expected excess rate of return is higher than that of market portfolio - aggressive asset. When β i < 1, the asset is said to be defensive. 4. When β i < 0, r i < r f. Since dσ M σ M = β i dw M i, so a risky asset with negative beta reduces the variance of the portfolio. This risk reduction potential of asset with negative β is something like paying premium to reduce risk. 19

20 Extension (replacing market portfolio M by any efficient portfolio P) Let P be any efficient portfolio along the upper tangent line and Q be any portfolio. We also have R Q r = β PQ (R P r), (A) that is, P is not necessarily to be the market portfolio, where β PQ = σ QP σ 2 P. More generally, R Q r = β PQ (R P r) + ǫ PQ (B) with cov(r P, ǫ PQ ) = E[ǫ PQ ] = 0. 20

21 The first result (A) can be deduced from the CAPM by observing σ QP = cov(r Q, αr M + (1 α)r f ) = αcov(r Q, R M ) = ασ QM, σ 2 P = α2 σ 2 M and R P r = α(r M r). Consider R Q r = β MQ (R M r) = σ QM σm 2 (R M r) = σ QP/α σp 2/α2(R P r)/α = β PQ (R P r). 21

22 The relationship among R Q, R P and r can be formally expressed as R Q = α 0 + α 1 R P + ǫ PQ where the residual ǫ PQ observes cov(r P, ǫ PQ ) = E[ǫ PQ ] = 0. Here, α 0 and α 1 are coefficients from the linear regression of R Q on R P. Observe that and from result (A), we obtain R Q = α 0 + α 1 R P so that R Q = β QP R P + r(1 β QP ), where β QP = σ QP σ 2 P Hence, we obtain result (B). α 0 = r(1 β QP ) and α 1 = β QP. 22

23 Zero-beta CAPM There exists a portfolio Z M that lies on the frontier of risky assets and whose beta is zero. Consider the CML r Q = r + β QM (r M r), since β MZM = 0, we have r ZM = r. Hence the CML can be expressed in terms of the market portfolio M and its zero-beta counterpart Z M as follows r Q = r ZM + β QM (r M r ZM ). In this form, the role of the riskfree asset is replaced by the zerobeta portfolio Z M. In this sense, we allow the absence of riskfree asset. The more general version of the CAPM allows the choice of any efficient (mean-variance) portfolio and its zero-beta counterpart. 23

24 Finding the uncorrelated counterpart Let P and Q be any two frontier portfolios of risky assets. Recall where w P = Ω 1 (λ P 11 + λ P 2 µ) and w Q = Ω 1 (λ Q 11 + λ Q 2 µ) λ P 1 = c bµ P, λp 2 = aµ P b, λq 1 = c bµ Q, λq 2 = aµ Q b, a =1 T Ω 1 1, b =1 T Ω 1 µ, c = µ T Ω 1 µ, = ac b 2. Find the covariance between R P and R Q. cov(r P, R Q ) = w T P Ωw Q = [ Ω 1 (λ P 11 + λ P 2 µ)] T (λ Q 11 + λ Q 2 µ) = λ P 1 λq 1 a + (λp 1 λq 2 + λq 1 λp 2 )b + λp 2 λq 2 c = a ( µ P b ) ( µ Q b ) + 1 a a a. Recall σ 2 P = a ( µ P b ) a a. 24

25 Given portfolio P, find the portfolio Z such that cov(r P, R Z ) = 0. Here, Z is called the uncorrelated counterpart of P. It is seen that µ Z = b a a 2 µ P a b. Since (µ P µ g )(µ Z µ g ) = a 2 < 0, where µ g = b, if one portfolio a is efficient, then the uncorrelated counterpart is non-efficient. Slope of the tangent at P to the frontier curve: dµ P dσ P = σ P aµ P b. The itnercept of the tangent line at the vertical axis is µ P dµ P dσ P σ P = µ P σ2 P aµ P b = µ P aµ2 P 2bµ P + c aµ P b = b a /a2 µ P b/a = µ Z. 25

26 26

27 Let P be a frontier portfolio other than the global minimum variance portfolio and Q be any portfolio, then cov(r P, R Q ) = [ Ω 1 ( λ P 11 + λ P 2 µ)] T ΩwQ = λ P 11 T w Q + λ P 2 µt w Q = λ P 1 + λp 2 µ Q. Solving for µ Q and substituting λ P 1 = c bµ P µ Q = bµ P c aµ P b + cov(r P, R Q ) aµ P b ( = b a /a2 µ P b/a + cov(r P, R Q ) 1 µp σp 2 a + a b /a ( = µ ZP + β PQ µ P b ) a + /a2 µ P b/a = µ ZP + β PQ (µ P µ ZP ). This gives the generalized version of the CAPM: µ Q µ ZP = β PQ (µ P µ ZP ). and λp 2 = aµ P b ) 2 aµ P b 27

28 Summary The zero-beta CAPM provides an alternative model of equilibrium returns to the standard CAPM. With no borrowing or lending at the riskless rate, an investor can attain his own optimal portfolio by combining any meanvariance efficient Portfolio P with its corresponding zero-beta Portfolio Z. Portfolio Z observes the properties (i) cov(r P, R Z ) = 0 (ii) Z is a frontier portfolio The choice of P is not unique so does the combination of portfolio P and Z. The rate of return of any portfolio Q can be expressed as where cov(r P, ǫ Q ) = E[ ǫ Q ] = 0. R Q R Z = β PQ (R P R Z ) + ǫ Q 28

29 3.2 Interpretations and uses of the capital asset pricing model Security market line (SML) From the two relations: r = r f + r M r f σ 2 M σ im r = r f + (r M r f )β i, we can plot either r against σ im or r against β i. 29

30 Under the equilibrium conditions as assumed by the CAPM, every asset should fall on the SML. The SML expresses the risk reward structure of assets according to the CAPM. Point O represents an under-priced security. This is because the expected return is higher than the return with reference to the risk. In this case, the demand for such security will increase and this results in price increase and lowering of expected return. 30

31 Suppose we write the random rate of return of asset i formally as r i = r f + β i (r M r f ) + ǫ i. The CAPM tells us something about ǫ i. (i) Taking the expectation on both sides E[r i ] = r f + β i (r M r f ) + E[ǫ i ] while r i = r f + β i (r M r f ) so that E[ǫ i ] = 0. (ii) Taking the covariance of r i with r M cov(r i, r M ) = so that zero {}}{ cov(r f, r M )+β i + cov(ǫ i, r M ) cov(ǫ i, r M ) = 0. }{{} zero cov(r M, r M ) cov(r f, r M ) 31

32 (iii) Consider the variance of r i so that var(r i ) = βi 2 cov(r M r f, r M r f ) + var(ǫ i ) }{{} var(r M ) σ 2 i = β2 i σ2 M + var(ǫ i). Decomposition of risk Systematic risk = βi 2σ2 M, this risk cannot be reduced by diversification because every asset with nonzero beta contains this risk. Non-systematic (idiosyncratic or specific) risk = var(ǫ i ), this risk is uncorrelated with the market and can be reduced by diversification. 32

33 Portfolios on the CML efficient portfolios Consider a portfolio formed by the combination of the market portfolio and the risk free asset. This portfolio is an efficient portfolio (one fund theorem) and it lies on the CML with a beta value equal to β 0 (say). Its rate of return can be expressed as r p = (1 β 0 )r f + β 0 r M = r f + β 0 (r M r f ) so that ǫ p = 0. The portfolio variance is β0 2σ2 M. This portfolio has only systematic risk (zero non-systematic risk). Suppose the portfolio lies both on the SML and CML, then SML : r p = r f + β(r M r f ) CML : r p = r f + r M r f σ M β = ρ pmσ M σ p σ 2 M σ p = σ p σ M ρ pm = 1. 33

34 Portfolios not on the CML non-efficient portfolios For other portfolios with the same value of β 0 but not lying on the CML, they lie below the CML since they are non-efficient portfolios. With the same value of β 0, they all have the same expected rate of return given by r = r f + β 0 (r M r f ) but the portfolio variance is greater than β0 2σ2 M. The extra part of the portfolio variance is var(ǫ p ). 34

35 equation of CML: r = r f + r M r f σ σ M 35

36 Note that ǫ i is uncorrelated with r M as revealed by cov(ǫ i, r M ) = 0. The term var(ǫ i ) is called the non-systematic or specific risk. This risk can be reduced by diversification. Consider Let β PM = µ P = n i=1 σ 2 P = n n i=1 i,j=1 w i r i = n i=1 (1 β im )w i r f + w i w j β im β jm σ 2 M + n w i β im and α P = n i=1 i=1 µ P = α P + β PM µ M n = β2 PM σ2 M + σ 2 P n i=1 w 2 i σ2 ǫ i. β im w i r M w i (1 β im )r f, then i=1 w 2 i σ2 ǫ i. 36

37 Suppose we take w i = 1/n so that σp 2 = β2 PM σ2 M + 1 n n 2 σǫ 2 i = βpm 2 σ2 M + σ2 /n, i=1 where σ 2 is the average of σ 2 ǫ 1,, σ 2 ǫ n. When n is sufficiently large σ P n i=1 w i β im σ M = β PM σ M. From σ 2 i = β2 im σ2 M +σ2 ǫ i, the contribution from σ 2 ǫ i to the portfolio variance goes to zero as n. 37

38 Example Consider the following set of data for 3 risky assets, market portfolio and risk free asset: portfolio/security σ ρ im β actual expected rate of return = E[P 1 + D 1 ] 1.0 P % % 2 20% % 3 20% % market portfolio 20% % risk free asset % P 1 is the price at time 1 and D 1 is the dividend paid at time 1, both are random quantities. 38

39 Use of CML The CML identifies expected rates of return which are available on efficient portfolios of all possible risk levels. Portfolios 2 and 3 lie below the CML. The market portfolio, the risk free asset and Portfolio 1 all lie on the CML. Hence, Portfolio 1 is efficient while Portfolios 2 and 3 are non-efficient. At σ = 10%, r = 10% }{{} +10% }{{} r f σ (16 10)% 20% }{{} (r M r f )/σ M = 13%. At σ = 20%, r = 10% + 20% (16 10)% 20% = 16%. 39

40 Use of the security market line (SML) The SML asks whether the portfolio provides a return equal to what equilibrium conditions suggest of the amount that should be earned. 40

41 Impact of ρ im Portfolio 1 has unit value of ρ im, that is, it is perfectly correlated with the market portfolio. Hence, Portfolio 1 has zero nonsystematic risk. Portfolios 2 and 3 both have ρ im less than one. Portfolio 2 has ρ im closer to one and so it lies closer to the CML. The expected rates of return of the portfolios for the given values of beta are given by r 1 = r 3 = 10% }{{} +0.5 }{{} r f β (16% 10% }{{} r M r f ) = 13% r 2 = 10% (16% 10%) = 15.4%. These expected rates of return suggested by the SML agree with the actual expected rates of return. Hence, each investment is fairly priced. 41

42 Summary The CAPM predicts that the excess return on any stock (portfolio) adjusted for the risk on that stock (portfolio) should be the same E[r i ] r f β i = E[r j] r f β j. Recall the somewhat restrictive assumptions of the standard CAPM all agents have homogeneous expectations agents maximize expected return relative to the standard deviation agents can borrow or lend unlimited amounts at the riskfree rate the market is in equilibrium at all times. In real world, it is possible that over short periods the market is not in equilibrium and profitable opportunities arises. 42

43 CAPM as a pricing formula Suppose an asset is purchased at P and later sold at Q. The rate of return is Q P, P is known and Q is random. Using the CAPM, P Q P P = r f + β(r M r f ) so that P = 1 The factor 1 + r f + β(r M r f ) discount rate. Q 1 + r f + β(r M r f ). can be regarded as the risk adjusted 43

44 Example (Investment in a mutual fund) A mutual fund invests 10% of its funds at the risk free rate of 7% and the remaining 90% at a widely diversified portfolio that closely approximates the market portfolio, and r M = 15%. The beta of the fund is then equal to 0.9. Suppose the expected value of one share of the fund one year later is $110, what should be the fair price of one share of the fund now? According to the pricing form of the CAPM, the current fair price $110 of one share = 1 + 7% (15 7)% = $ = $

45 Linearity of pricing? ( Q Note that β = cov P 1, r M then have so that 1 = ) / σm 2 so that β = cov(q, r M). We Q P(1 + r f ) + cov(q, r M )(r M r f )/σ 2 M P = r f [ Q cov(q, r M)(r M r f ) σ 2 M ]. Pσ 2 M The bracket term is called the certainty equivalent of Q. In this form, the linearity of Q is more apparent! Note that the riskfree 1 discount factor is applied. Net present value is 1 + r f P r f [ Q cov(q, r M)(r M r f ) σ 2 M ]. 45

46 3.3 Factor models Difficulties associated with the implementation of the CAPM 1. Application of the mean-variance theory requires the determination of the parameter values: mean values of the asset returns and the covariances among them. Suppose there are n assets, n(n 1) then there are n mean values, n variances and covariances. For example, when n = 1,000, the number of parameter 2 values required = 501, In the CAPM, there is really only one factor that influences the expected return, namely, the covariance between the asset return and the return on the market portfolio. 46

47 The assumption of investors utilizing a mean variance framework is replaced by an assumption of the process generating security returns. Merit of the Arbitrage Pricing Theory (APT) 1. APT requires that the returns on any stock be linearly related to a number of factors. It implies that the return on a security can be broken down into an expected return and an unexpected (or surprise) component. 2. Randomness as displayed by the returns of n assets can be traced back to a smaller number of underlying basic sources of randomness (factors). Hopefully, this leads to a simpler covariance structure. 47

48 Specifying the influences affecting the return-generating process 1. Inflation Inflation impacts both the level of the discount rate and the size of the future cash flows. 2. Risk premia Differences between the return on safe bonds and more risky bonds are used to measure the market s reaction to risk. 3. Industrial production Changes in industrial production affect the opportunities facing investors and the real value of cash flow. 48

49 Single-factor model Rates of return r i and the factor are related by r i = a i + b i f + e i i = 1,2,, n. Here, f is a random quantity, a i and b i are fixed constants, e i s are random errors (without loss of generality, take E[e i ] = 0 since any non-zero mean can be absorbed by a i ). Further, we assume We can deduce E[(f f)e i ] = 0 and E[e i e j ] = 0, i j. cov(e i, f) = E[e i f] E[e i ]E[f] = 0. The variances of e i s are known, which are denoted by σ 2 e i. Let b i be the factor loading, which measures the sensitivity of the return to the factor. 49

50 Different data sets (past one month or two months data) may lead to different estimated values. r i = a i + b i f σi 2 = b 2 i σ2 f + σ2 e i σ ij = b i b j σf 2, i j b i = cov(r i, f)/σ 2 f. Only a i s, b i s, σe 2 i s, f and σf 2 parameters. are required. There are (3n + 2) 50

51 Portfolio parameter Let w i denote the weight for asset i, i = 1,2,, n. The portfolio rate of return is r p = n i=1 w i a i + so that r p = a + bf + e, where a = n i=1 w i a i, b = n i=1 n i=1 w i b i f + n i=1 w i b i and e = w i e i n i=1 w i e i. Further, since E[e i ] = 0, E[(f f)e i ] = 0 so that E[e] = 0 and E[(f f)e] = 0; e and f are uncorrelated. Also, σ 2 e = Overall variance of portfolio = σ 2 p = b 2 σ 2 f + σ2 e. n i=1 w 2 i σ2 e i. For simplicity, we take σ 2 e i = S 2 and w i = 1/n so that σ 2 e = S2 n. 51

52 As n, σe 2 0. The overall variance of portfolio σp 2 tends to decrease as n increases since σe 2 goes to zero, but σ2 p does not go to zero since b 2 σf 2 remains finite. The risk due to e i is said to be diversifiable since its contribution to overall risk is essentially zero in a well-diversified portfolio. This is because e i s are independent and so each can be reduced by diversification. The risk due to b i f is said to be systematic since it is present even in a diversified portfolio. 52

53 CAPM as a factor model Express the model in terms of excess returns r i r f and r M r f. r i r f = α i + β i (r M r f ) + e i. With e i = 0, this corresponds to the characteristic line Taking the expectation on both sides r i r f = α i + β i (r M r f ). (1) r i r f = α i + β i (r M r f ). With α i = 0, the above relation reduces to the CAPM. We assume that e i is uncorrelated with the market return r M. 53

54 The characteristic line is more general than the CAPM since it allows α i to be non-zero. The factor model does not assume any utility function or that agents consider only the mean and variance of prospective portfolios. Remarks 1. The presence of non-zero α i can be regarded as a measure of the amount that asset i is mispriced. A stock with positive α i is considered performing better than it should. 2. The general CAPM model is based on an arbitrary covariance structure while the one-factor model assumes very simple covariance structure. 54

55 Single-factor, residual-risk-free models Assume zero idiosyncratic (asset-specific) risk, r i = a i + b i f, i = 1,2,, n, where f is taken that satisfies E[f] = 0 so that r i = a i. Consider two assets which have two different b i s, what should be the relation between their expected returns under the assumption of no arbitrage? Consider a portfolio with weight w in asset i and weight 1 w in asset j. The portfolio return is r p = w(a i a j ) + a j + [w(b i b j ) + b j ]f. 55

56 By choosing w = b j b j b i, the portfolio becomes riskfree and r p = b j(a i a j ) b j b i + a j. This must be equal to the return of the riskfree asset, denoted by r 0. We write the relation as a j r 0 b j = a i r 0 b i = λ. Hence, r i = r 0 + b i λ, where λ is the factor risk premium. Here, λ represents the expected excess return above the riskfree rate per unit of risk (as quantified by f). Note that when two assets are hedgeable, they have the same factor risk premium. set 56

57 Example 1 (Four stocks and one index) Historical rates of return for four stocks over 10 years, record of industrial price index over the same period. Estimate of r i is r i = k=1 var(r i ) = 1 9 r k i. 10 cov(r i, f) = 1 9 k=1 10 (r k i r i ) 2 k=1 (r k i r i )(f k f). Once the covariances are estimated, b i and a i are obtained: b i = cov(r i, f) var(f) and a i = r i b i f. 57

58 We estimate the variance of the error under the assumption that these errors are uncorrelated with each other and with the index. The formula to be used is var(e i ) = var(r i ) b 2 i var(f). Unfortunately, the error variances are almost as large as the variances of the stock returns. There is a high non-systematic risk, so the choice of this factor does not explain much of the variation in returns. Further, cov(e i, e j ) are not small so that the errors are highly correlated. We have cov(e 1, e 2 ) = 44 and cov(e 2, e 3 ) = 91. Recall that the factor model was constructed under the assumption of zero error covariances. 58

59 Year Stock 1 Stock 2 Stock 3 Stock 4 Index aver var cov b a e-var The record of the rates of return for four stocks and an index of industrial prices are shown. The averages and variances are all computed, as well as the covariance of each with the index. From these quantities, the b i s and the a i s are calculated. Finally, the computed error variances are also shown. The index does not explain the stock price variations very well. 59

60 Two-factor extension Consider the two-factor model r i = a i + b i1 f 1 + b i2 f 2, i = 1,2,, n, where the factor f 1 and f 2 are chosen such that E[f 1 f 2 ] = 0, E[f 2 1 ] = E[f2 2 ] = 1, E[f 1] = E[f 2 ] = 0. We assume 1, b 1 = b 11 b 21 b 31 and b 2 = b 12 b 22 b 32 to be linearly independent. Form the portfolio with weights w 1, w 2 and w 3 so that r p = 3 i=1 w i a i + f w i b i1 + f 2 w i b i2. i=1 i=1 60

61 Since 1, b 1 and b 2 are independent, the following system of equations b 11 b 21 b 31 b 12 b 22 b 32 w 1 w 2 w 3 = always has unique solution. In this case, the portfolio becomes riskfree so or r p = 3 i=1 3 i=1 w i a i = r 0 (a i r 0 )w i =

62 Hence, there is a non-trivial solution to a 1 r 0 a 2 r 0 a 3 r 0 b 11 b 21 b 31 b 12 b 22 b 32 w 1 w 2 w 3 = The above coefficient matrix must be singular so that a i r 0 = λ 1 b i1 + λ 2 b i2 for some λ 1 and λ 2. The risk premium on asset i is a i r 0. Absence of riskfree asset r i r 0 = λ 1 b i1 + λ 2 b i2, i = 1,2,, n. If no riskfree asset exists naturally, then we replace r 0 by λ 0. Once λ 0, λ 1 and λ 2 are known, the expected return of an asset is completely determined by the factor loadings b i1 and b i2. Theoretically, a riskless asset can be constructed from any three risky assets so that λ 0 can be determined

63 Prices of risk, λ 1 and λ 2 interpreted as the excess expected return per unit risk associated with the factors f 1 and f 2. Given any two portfolios P and M with b P1 b M1, we can b P2 b M2 solve for λ 1 and λ 2 in terms of the expected return on these two portfolios: r M r 0 and r P r 0. One can show that where r i = r 0 + b i1 (r M r 0 ) + b i2 (r P r 0 ) b i1 = b i1b P2 b i2 b P1 b M1 b P2 b M2 b P1, b i2 = b i2b M1 b i1 b M2 b M1 b P2 b M2 b P1. 63

64 Linkage between CAPM and factor model Consider a two-factor model r i = a i + b i1 f 1 + b i2 f 2 + e i, the covariance of the rate of return of the i th asset with that of the market portfolio is given by cov(r M, r i ) = b i1 cov(r M, f 1 ) + b i2 cov(r M, f 2 ) + cov(r M, e i ). It is reasonable to ignore cov(r M, e i ) if the market represents a welldiversified portfolio. 64

65 We write the beta of the asset as β i = cov(r M, r i ) σ 2 M = b i1 cov(r M, f 1 ) σ 2 M }{{} β f1 cov(r + b M, f 2 ) i2 σm 2. }{{} β f2 The factor betas β f1 and β f2 do not depend on the particular asset. The weight of these factor betas in the overall asset beta is equal to the factor loadings. In this framework, different assets have different betas corresponding to different loadings. 65

66 Example 2 Assume that a two factor model is appropriate, and there are an infinite number of assets in the economy. The cross-sectional relationship between expected return and factor loadings indicates that the price of factor 1 is 0.15, and the price of factor 2 is 0.2. You have estimated factor loadings for stocks X and Y as follows: b 1 b 2 Stock X Stock Y Also, the expected return on an asset having zero betas (with respect to both factors) is What are the approximate equilibrium returns on each of the two stocks? 66

67 Solution The expected return of an asset based on a two-factor model is given by r i = λ 0 + λ 1 b i1 + λ 2 b i2. Here, λ 0 = zero-beta return = 0.05 λ 1 = 0.15 and λ 2 = 0.2. Now, r 1 = λ 0 + λ 1 b 11 + λ 2 b 12 = = 01.8; r 2 = λ 0 + λ 1 b 21 + λ 2 b 22 = =

68 Example 3 Assume that a three-factor model is appropriate, and there are an infinite number of assets. The expected return on a portfolio with zero beta values is 5 percent. You are interested in an equally weighted portfolio of two stocks, A and B. The factor prices are indicated in the accompanying table, along with the factor loadings for A and B. Compute the approximate expected return of the portfolio. Factor i b ia b ib Factor Prices

69 Solution: By APT, the expected return of a portfolio is given by r p = λ 0 + λ 1 b P1 + λ 2 b P2 + λ 3 b P3. Here, λ 0 = 5%, b P1 = 2 1 (b 1A + b 1B ) = 1 2 ( ) = 0.4, b P2 = 1 2 (b 2A + b 2B ) = 1 ( ) = 0.4, 2 b P3 = 1 2 (b 3A + b 3B ) = 1 ( ) = Given λ 1 = 0.07, λ 2 = 0.09, λ 3 = 0.02, so r P = 5% = 13.1%. 69

70 Example 4 Stocks 1 and 2 are affected by three factors, as shown here. Factor 2 and 3 are unique to each stock. Expected values of each are E(F 1 ) = 3.0%, E(F 2 ) = 0.0%, and E(F 3 ) = 0.0%. Neither stock pays a dividend, and they are now selling at prices P 1 = $40 and P 2 = $10. You expect their prices in a year to be E(P 1 ) = $45 and E(P 2 ) = $ R 1 = 6.0( F 1 ) + 0.3( F 2 ) + 0.0( F 3 ) R 2 = 1.5( F 1 ) + 0.0( F 2 ) + 0.4( F 3 ) a. What do factors 2 and 3 reflect? In the context of a broadly diversified portfolio, should the weights 0.3 and 0.4 be positive, as they are shown? b. Neglecting F 2 and F 3, create a riskless arbitrage. c. Relate the return equations to the CAPM. 70

71 Solution a. Factors 2 and 3 appear to be firm specific factors in that they affect only a single stock. Across a large number of stocks, these factors will net to zero. b. By APT, the expected returns of Stock 1 and Stock 2 are r 1 = 6F 1 = 18%, r 2 = 1.5F 2 = 4,5%. The market expected returns are r 1,market = = 12.5%; r 2,market = = 7%. The arbitrage strategy is to short 1/4 unit of Stock 1 and buy one unit of Stock 2. The portfolio is riskless but the expected return = % + 7% = 4.875%. 4 c. Here, r i = 0 + β i F 1 ; while CAPM gives r i = r f + β i (r M r f ). These correspond to r f = 0 and F 1 = r M. 71

72 3.4 Performance indexes Risk-adjusted performance measures based on CAPM We compute some performance indexes which could help assess actual investment performance of different mutual fund managers. Such an index would have to measure the actual returns of traders relative to some equilibrium risk-return relationship. A fund manager may perform better than portfolios on the CML (trading based on the publicly available information) by trading on private information depth: magnitude of the excess return captured by the fund manager breadth: number of different securities for which a fund manager can capture excess return 72

73 Jensen index r _ X Jensen index SML M( =1) r f The Jensen index J uses the SML as a benchmark. It measures the height above the SML. J = r p [r f + (r M r f )β p ] where β p is the beta of the portfolio and r p is the expected rate of return of the portfolio. 73

74 selectivity = net selectivity + diverification Jensen index measures the depth captured by comparing return with the same β (the portfolio may have high σ 2 p with moderate β 2 pσ 2 m) while the total risk measures the depth and breadth. The Jensen index is sensitive to depth but not breadth. The term r f + (r M r f )β p represents the expected return if the portfolio were positioned on the SML. 74

75 According to the CAPM, a fund manager could obtain any point along the SML by investing in the market portfolio and mixing this with the riskless asset to obtain the desired level of β. If the fund manager s choice is to actively manage the fund, then we measure the difference in return between active management and the passive management of investing in the market portfolio and riskless asset. Empirical studies based on Jensen s performance index Out of more than 250 mutual funds, only 9 out-performed an unmanaged S & P 500 index. 75

76 Turn around the argument, J can be used to test the validity of the CAPM. If we find a security with a non-zero Jensen index, then this indicates that the market is not efficient. The CAPM formula is often applied to new financial instruments or projects that are not traded, which are not part of the portfolio. In this case, J can be a useful measure. 76

77 Sharpe index The Sharpe index uses the capital market line (CML) as the benchmark. It is an excess return to variability measure: r _ CML M ABC r f S = r p r f σ p 77

78 The sample estimate of the Sharpe index is Ŝ = r p r f σ p. S is sensitive to both breadth and depth since σ p is a measure of the full risk of the fund. 78

79 Treynov index Risk premium earned per unit of risk taken, where risk is measured in terms of β p. T p = r p r f β p. 79

80 Under the CAPM, the Treynor index should be the same for all portfolios of securities when the market is in equilibrium. If T i of a fund exceeds that of the market portfolio, then the fund is earning an abnormal return relative to that given by the CAPM. Note that J i > 0 iff T i > 0. Further, (i) T i > T j if J i = J j and β i < β j ; (ii) J j > T i if T i = T j and β j > β i. 80

81 Consider two funds Alpha and Omega, both of which have excess expected rate of return of 2% above the SML. Alpha has lower value of beta so that it has a greater excess rate of return per unit of risk. Assume that we can borrow at the riskfree rate r f, we can lever a position in Alpha fund to a position at A by selling the riskfree bond and using the proceed to invest in Alpha. 81

82 Example The data given below are the rate of return achieved by the ABC fund, S & P 500 (as proxy for the market portfolio) and Treasury bill (as the riskless asset) over 10-year period. ABC Fund Performance Rate of return percentages Year ABC S & P T-bills Average Standard deviation Geometric mean Cov(ABC, S & P) Beta Jensen Sharpe

83 Calculation steps 1. Given r i, i = 1,2,, n, the average rate of return is r = 1 n n r i i=1 which serves as an estimate of the true expected return r. The estimate of the average variance is sample variance = ŝ 2 = 1 n 1 n i=1 ( ri r i ) Calculate an estimate of the covariance of the fund and the S & P 500 (proxy for the market portfolio) cov(r, r M ) = 1 n 1 The beta is obtain by n i=1 β = cov(r, r M) var(r M ). (r i r)(r Mi r M ). 83

84 β ABC = = S ABC = r ABC r f ŝ ABC = = Note that the calculated Jensen index for the S & P 500 must be zero. Based on the CAPM, all securities and portfolios should have zero Jensen index value. A positive value of J (as exhibited by the ABC fund) presumably implies that the fund did better than the CAPM prediction (based on the use of a finite data set). 84

85 Sharpe ratio versus Treynor index An investor choosing a mutual fund to represent a large part of her wealth would like to be concerned with the full risk of the fund and σ P is a measure of that risk Sharpe index is more appropriate as the performance index. Look at the other side of the coin, the pension fund of a large corporation may allocate more than 100 fund managers for management. The contribution to the risk of the pension fund as a whole from the portfolio of any of these managers is primarily the non-diversifiable risk. In this case, the Treynor index (which uses β as the risk parameter) is more appropriate to serve as the performance index. 85

86 Decomposition of overall evaluation 86

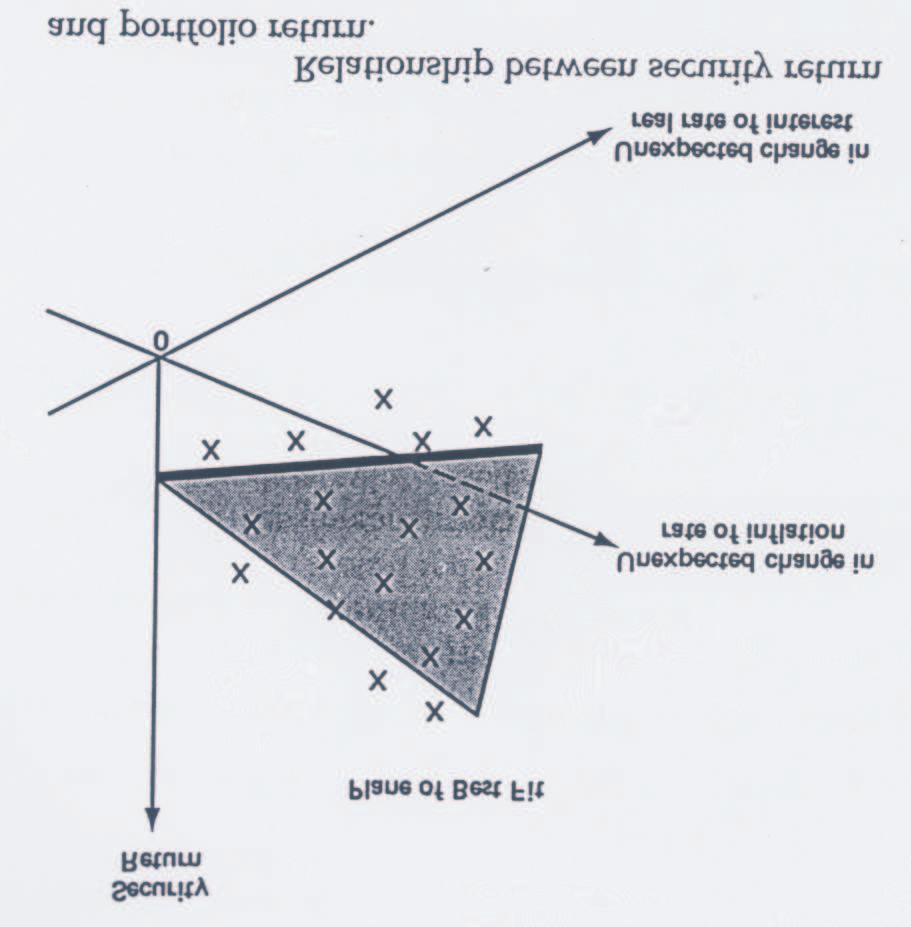

87 1. Portfolios A and A have the same beta and thus have the same non-diversifiable risk. Since portfolio A lies on the SML, all the risk of portfolio A is completely non-diversifiable. For portfolio A, in the process of earning extra return, diversifiable risk was incurred. 2. Is the extra return worth the extra risk? Compare a naive portfolio with the same total risk as that of portfolio A. This is portfolio A. 3. R A R A = R A R A }{{} net selectivity + R A R A. }{{} diversification 87

88 4. How to decompose R R R F, which is the extra return earned on the naive portfolio for bearing risk? Let β F be the target risk level that the investor is willing to bear. R A R F = R T R F }{{} return from investor s risk + R A R T }{{} return from manager s risk + R A R A }{{} return from selectivity 88

89 Mutual fund performance How much of the risk incurred by the portfolio is due to market movements and how much is due to unique movements of the individual securities in the portfolio? Most mutual funds are well diversified and the majority of the risk they incur is the risk of market movement. However, mutual funds also bear non-market risk. Empirical evidence showed that most mutual funds do not earn sufficient return to justify incurring this extra risk. 89

90 Triumph of Index Tracking Most investors, both institutional and individual, will find that the best way to own common stocks is through an index fund that charges minimal fees. Passive investment management or index tracking certainly has impressive credentials. John C. Bogle, the founder of the Vanguard Group of Investment Companies and an early proponent of the approach has calculated that the S&P 500 Index outperformed the average U.S. equity mutual fund by 3.4 percent per year over the 10 years to December 31, The degree of annual outperformance over five and 15 years was even greater 5.0 percent and 4.0 percent, respectively. 90

91 How to explain the apparent inability of investment professionals to consistently beat the market? Money-management sector is now dominated by professionals. This severely limits the opportunities for outperformance. Active management is generally much more expensive than index tracking costs of employment of investment professionals transaction costs brokers commissions 91

92 Active management still has a role? There is considerable evidence to show that over the long term a diversified portfolio of equities will outperform every other asset class on a risk-adjusted basis. But over shorter periods investors can face the prospect of shortterm losses. Actively managed portfolios can in theory at least reduce these risks. Smart managers can employ many strategies to preserve capital if they foresee a severe market decline. Investments can be sold for cash or hedging strategies can be employed to safeguard the value of the underlying portfolio. 92

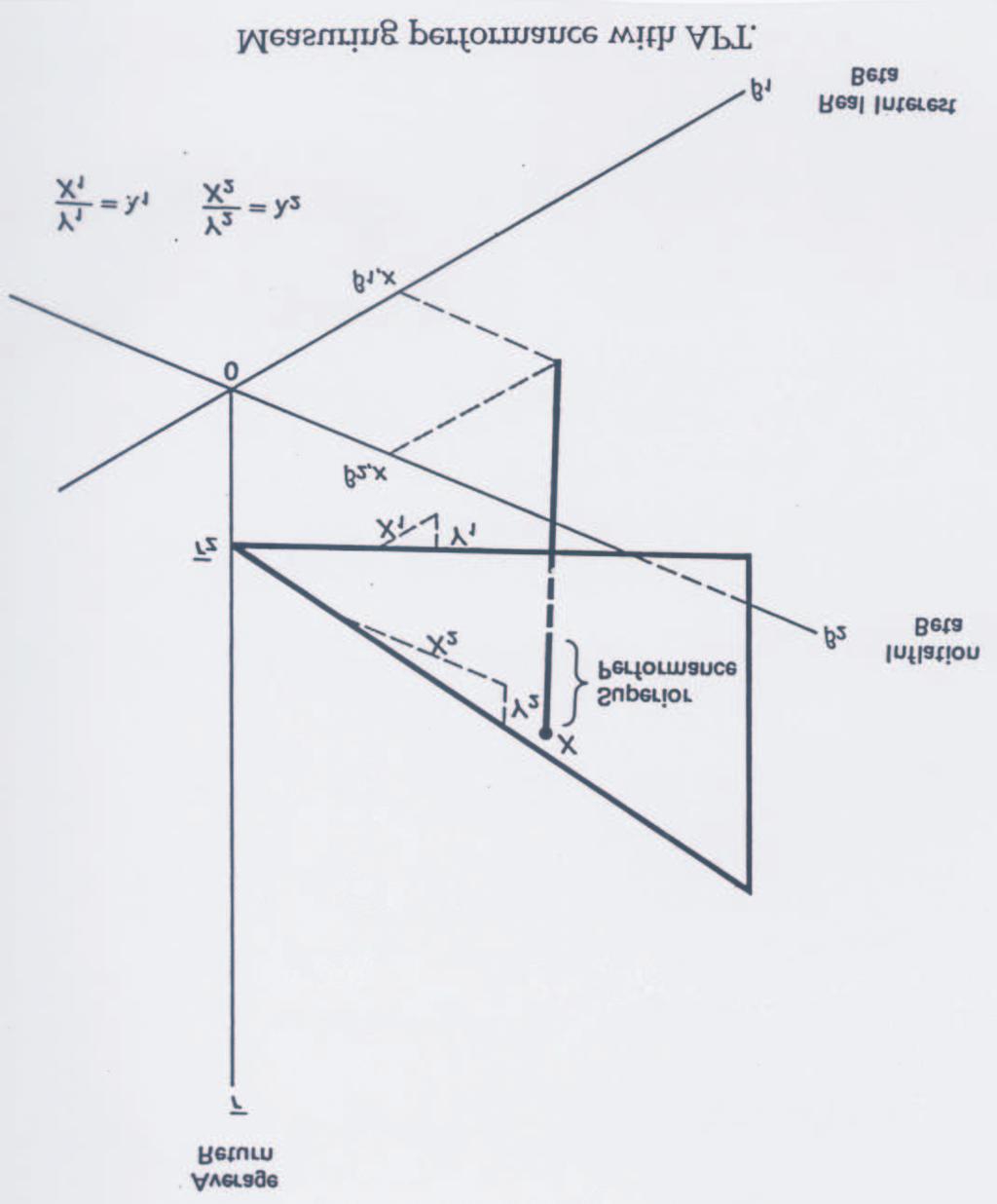

93 Measuring performance using the APT Using the APT, the relationship between the factor betas and the expected rates of return on a portfolio is given by r P = r Z + λ 1 β 1,P + + λ n β n,p that is, expected portfolio return = zero-beta portfolio return + sum of factor risk premium Once we have obtained estimates of r Z and λ i s, we can use the above relationship as a benchmark. 93

94 94

95 The slopes of the plane going down each axis represent the sensitivity of the security s return to changes in the two factors (hence, they are estimates of the factor betas). Steps 1. Decide on the factors needed to account for the covariance between stocks. 2. Estimate the factor betas for a cross-section of securities (see the figure where we slide a plane of best fit through the data points). 3. Estimation of the factor prices This is done by relating the estimated factor betas to the average rates of return on each stock. 95

96 96

97 The slope of the plane relative to each horizontal axis serves as the estimate of each factor price. Remark The APT really makes no prediction about what the factors are. Given the freedom to select factors, one can literally make the performance of the portfolio anything you want it to be. 97

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

MATH 4512 Fundamentals of Mathematical Finance

MATH 451 Fundamentals of Mathematical Finance Solution to Homework Three Course Instructor: Prof. Y.K. Kwok 1. The market portfolio consists of n uncorrelated assets with weight vector (x 1 x n T. Since

MATH 451 Fundamentals of Mathematical Finance Solution to Homework Three Course Instructor: Prof. Y.K. Kwok 1. The market portfolio consists of n uncorrelated assets with weight vector (x 1 x n T. Since

Lecture 5 Theory of Finance 1

Lecture 5 Theory of Finance 1 Simon Hubbert s.hubbert@bbk.ac.uk January 24, 2007 1 Introduction In the previous lecture we derived the famous Capital Asset Pricing Model (CAPM) for expected asset returns,

Lecture 5 Theory of Finance 1 Simon Hubbert s.hubbert@bbk.ac.uk January 24, 2007 1 Introduction In the previous lecture we derived the famous Capital Asset Pricing Model (CAPM) for expected asset returns,

Chapter 8: CAPM. 1. Single Index Model. 2. Adding a Riskless Asset. 3. The Capital Market Line 4. CAPM. 5. The One-Fund Theorem

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

MATH362 Fundamentals of Mathematical Finance. Topic 1 Mean variance portfolio theory. 1.1 Mean and variance of portfolio return

MATH362 Fundamentals of Mathematical Finance Topic 1 Mean variance portfolio theory 1.1 Mean and variance of portfolio return 1.2 Markowitz mean-variance formulation 1.3 Two-fund Theorem 1.4 Inclusion

MATH362 Fundamentals of Mathematical Finance Topic 1 Mean variance portfolio theory 1.1 Mean and variance of portfolio return 1.2 Markowitz mean-variance formulation 1.3 Two-fund Theorem 1.4 Inclusion

MATH4512 Fundamentals of Mathematical Finance. Topic Two Mean variance portfolio theory. 2.1 Mean and variance of portfolio return

MATH4512 Fundamentals of Mathematical Finance Topic Two Mean variance portfolio theory 2.1 Mean and variance of portfolio return 2.2 Markowitz mean-variance formulation 2.3 Two-fund Theorem 2.4 Inclusion

MATH4512 Fundamentals of Mathematical Finance Topic Two Mean variance portfolio theory 2.1 Mean and variance of portfolio return 2.2 Markowitz mean-variance formulation 2.3 Two-fund Theorem 2.4 Inclusion

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

Financial Economics: Capital Asset Pricing Model

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Use partial derivatives just found, evaluate at a = 0: This slope of small hyperbola must equal slope of CML:

Derivation of CAPM formula, contd. Use the formula: dµ σ dσ a = µ a µ dµ dσ = a σ. Use partial derivatives just found, evaluate at a = 0: Plug in and find: dµ dσ σ = σ jm σm 2. a a=0 σ M = a=0 a µ j µ

Derivation of CAPM formula, contd. Use the formula: dµ σ dσ a = µ a µ dµ dσ = a σ. Use partial derivatives just found, evaluate at a = 0: Plug in and find: dµ dσ σ = σ jm σm 2. a a=0 σ M = a=0 a µ j µ

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Chapter 7: Portfolio Theory

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Techniques for Calculating the Efficient Frontier

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Portfolio models - Podgorica

Outline Holding period return Suppose you invest in a stock-index fund over the next period (e.g. 1 year). The current price is 100$ per share. At the end of the period you receive a dividend of 5$; the

Outline Holding period return Suppose you invest in a stock-index fund over the next period (e.g. 1 year). The current price is 100$ per share. At the end of the period you receive a dividend of 5$; the

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory Hedge Portfolios A portfolio that has zero risk is said to be "perfectly hedged" or, in the jargon of Economics and Finance, is referred

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory Hedge Portfolios A portfolio that has zero risk is said to be "perfectly hedged" or, in the jargon of Economics and Finance, is referred

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Microéconomie de la finance

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Module 3: Factor Models

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

Application to Portfolio Theory and the Capital Asset Pricing Model

Appendix C Application to Portfolio Theory and the Capital Asset Pricing Model Exercise Solutions C.1 The random variables X and Y are net returns with the following bivariate distribution. y x 0 1 2 3

Appendix C Application to Portfolio Theory and the Capital Asset Pricing Model Exercise Solutions C.1 The random variables X and Y are net returns with the following bivariate distribution. y x 0 1 2 3

LECTURE NOTES 3 ARIEL M. VIALE

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

From optimisation to asset pricing

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Financial Markets. Laurent Calvet. John Lewis Topic 13: Capital Asset Pricing Model (CAPM)

") Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

The stochastic discount factor and the CAPM

The stochastic discount factor and the CAPM Pierre Chaigneau pierre.chaigneau@hec.ca November 8, 2011 Can we price all assets by appropriately discounting their future cash flows? What determines the risk

The stochastic discount factor and the CAPM Pierre Chaigneau pierre.chaigneau@hec.ca November 8, 2011 Can we price all assets by appropriately discounting their future cash flows? What determines the risk

Lecture 2: Fundamentals of meanvariance

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 OPTION RISK Introduction In these notes we consider the risk of an option and relate it to the standard capital asset pricing model. If we are simply interested

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 OPTION RISK Introduction In these notes we consider the risk of an option and relate it to the standard capital asset pricing model. If we are simply interested

Chapter 2 Portfolio Management and the Capital Asset Pricing Model

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Optimizing Portfolios

Optimizing Portfolios An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Investors may wish to adjust the allocation of financial resources including a mixture

Optimizing Portfolios An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Investors may wish to adjust the allocation of financial resources including a mixture

Quantitative Risk Management

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

Capital Asset Pricing Model

Capital Asset Pricing Model 1 Introduction In this handout we develop a model that can be used to determine how an investor can choose an optimal asset portfolio in this sense: the investor will earn the

Capital Asset Pricing Model 1 Introduction In this handout we develop a model that can be used to determine how an investor can choose an optimal asset portfolio in this sense: the investor will earn the

Performance Measurement and Attribution in Asset Management

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

You can also read about the CAPM in any undergraduate (or graduate) finance text. ample, Bodie, Kane, and Marcus Investments.

finance text. ample, Bodie, Kane, and Marcus Investments.") ECONOMICS 7344, Spring 2003 Bent E. Sørensen March 6, 2012 An introduction to the CAPM model. We will first sketch the efficient frontier and how to derive the Capital Market Line and we will then derive

ECONOMICS 7344, Spring 2003 Bent E. Sørensen March 6, 2012 An introduction to the CAPM model. We will first sketch the efficient frontier and how to derive the Capital Market Line and we will then derive

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management. RSM332 FINAL EXAMINATION Geoffrey/Wang SOLUTIONS. (1 + r m ) r m

r m") UNIVERSITY OF TORONTO Joseph L. Rotman School of Management Dec. 9, 206 Burke/Corhay/Kan RSM332 FINAL EXAMINATION Geoffrey/Wang SOLUTIONS. (a) We first figure out the effective monthly interest rate, r

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management Dec. 9, 206 Burke/Corhay/Kan RSM332 FINAL EXAMINATION Geoffrey/Wang SOLUTIONS. (a) We first figure out the effective monthly interest rate, r

The Markowitz framework

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

E(r) The Capital Market Line (CML)

The Capital Market Line (CML)") The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT. Professor B. Espen Eckbo

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011

When we model expected returns, we implicitly model expected prices

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

Derivation of zero-beta CAPM: Efficient portfolios

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Consumption- Savings, Portfolio Choice, and Asset Pricing

Finance 400 A. Penati - G. Pennacchi Consumption- Savings, Portfolio Choice, and Asset Pricing I. The Consumption - Portfolio Choice Problem We have studied the portfolio choice problem of an individual

Finance 400 A. Penati - G. Pennacchi Consumption- Savings, Portfolio Choice, and Asset Pricing I. The Consumption - Portfolio Choice Problem We have studied the portfolio choice problem of an individual

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Lecture 10: Performance measures

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty

![ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty](/thumbs/83/88403560.jpg "ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty") ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

CHAPTER 8: INDEX MODELS

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

23.1. Assumptions of Capital Market Theory

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS