Arbitrage Pricing Theory and Multifactor Models of Risk and Return

|

|

|

- Edward Bridges

- 5 years ago

- Views:

Transcription

1 Arbitrage Pricing Theory and Multifactor Models of Risk and Return

2 Recap : CAPM Is a form of single factor model (one market risk premium) Based on a set of assumptions. Many of which are unrealistic One factor to proxy for risk premium In CAPM, alpha assumed to be zero. But real-world test reject this. The search for better model continues..

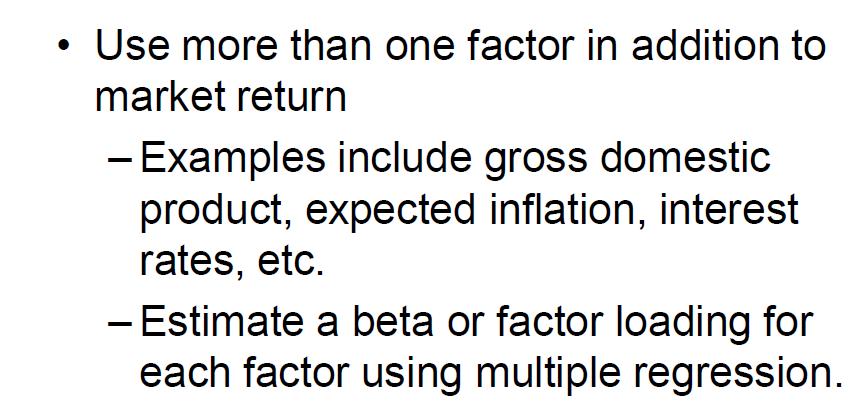

3 Single Factor Model Returns on a security come from two sources: 1) Common macro-economic factor (market risk) 2) Firm specific events (specific risk) In reality, many possible common macro-economic factors. (more than 1) Gross Domestic Product Growth Interest Rates Inflation Etc

4 Single Factor Model : Equation

5 Multifactor Models

6 Multifactor Models Equation

7 Multifactor SML Models

8 Multifactor Model Interpretation

9 Multifactor Model Example Suppose Eazyjet has a theoretical market beta of 1.2 and T-bond beta of 0.7. The European market risk premium is 6% while T-bond portfolio (comprise of a basket of European Gov. bonds) is 3%. What is the expected return of Eazyjet? Sol. E(r) = 4%+1.2*6%+0.7*3% = 13.3%

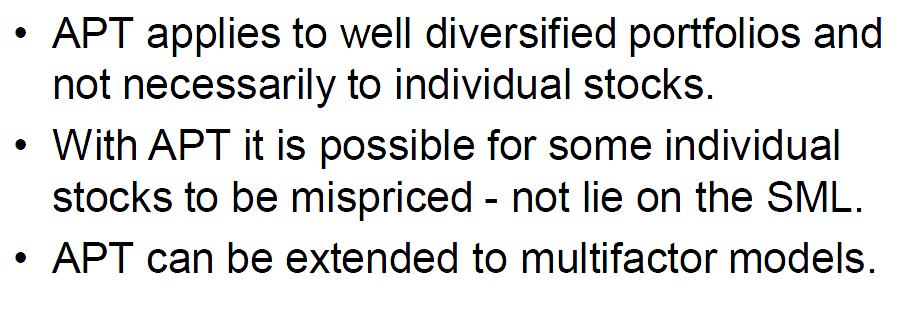

10 Arbitrage Pricing Theory Arbitrage is the act of exploiting mispricing of two of more securities to achieve risk-free returns. Arbitrage occurs if there is a zero investment portfolio with a sure profit. Ross (1976) derived APT based on an assumption that well-functioning market preclude arbitrage opportunities

11 Arbitrage Pricing Theory Since the return from arbitrage opportunity is risk free and to earn such profit require zero net investment (Example : short high price long low price of the same security) Since no investment is required, investors can create large positions to obtain sure profits. Violation of APT pricing relationships will cause extremely high pressure to correct price.

12 Arbitrage Pricing Theory

13 Port Weight APT & Well-Diversified Portfolios In Asset Contribution to Excess Returns W p = 1 Portfolio P W p (α p +β p R M +e p ) = α p +β p R M +e p W M = -β p Benchmark W M R M = -β p R M W f = β p -1 Risk-free asset W = 0 Portfolio A (Will be Arbitrage Portfolio if it is well diversified e p =0) W f *0 = 0 (excess returns measured over r f ) α p +e p

14 APT & Well-Diversified Portfolios

15 Returns as Function of Systematic Factor

16 An arbitrage opportunity

17 APT Model

18 APT & CAPM

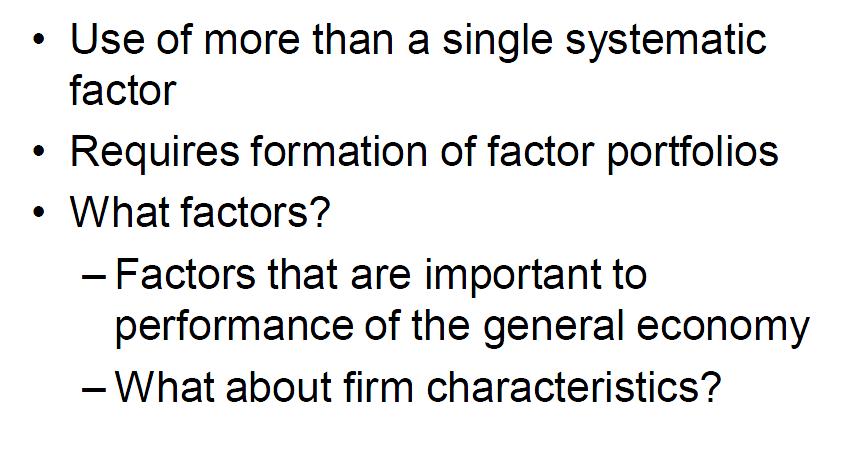

19 Multifactor APT

20 Two Factor model

21 Factor Portfolios

22 What factors in Multifactor model? Need important systematic risk factors Chen, Roll, and Ross used industrial production, expected inflation, unanticipated inflation, excess return on corporate bonds, and excess return on government bonds. (Macroeconomic Factors) Fama and French used firm characteristics that proxy for systematic risk factors. (HML, SMB)

23 Fama-French 3 factor model

24 Fama-French 3 factor model Motivated by the observation that average returns on small stocks (SMB) & value stocks (HML) SMB : Small (mkt. cap) minus big Small stocks maybe more sensitive to changes in business conditions HML : High (book-to-market) minus low Firms in financial distress tend to have market value close to its book value

25 APT : Homework The market price of security is $30. Its expected rate of return is 10%. R f =4% and risk premium is 8%. The stock is expected to pay a constant dividend in perpetuity. What will be the market price of the securities be if the beta double (all other variable remains unchanged) $18.75

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 10-2 Single Factor Model Returns on

CHAPTER 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS

CHAPTER 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS

Index Models and APT

Index Models and APT (Text reference: Chapter 8) Index models Parameter estimation Multifactor models Arbitrage Single factor APT Multifactor APT Index models predate CAPM, originally proposed as a simplification

Index Models and APT (Text reference: Chapter 8) Index models Parameter estimation Multifactor models Arbitrage Single factor APT Multifactor APT Index models predate CAPM, originally proposed as a simplification

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Investment Companies Pool funds of individual investors and invest in a wide range of securities or other assets. pooling of assets Mutual Funds and Other Investment Companies Provide several functions

Investment Companies Pool funds of individual investors and invest in a wide range of securities or other assets. pooling of assets Mutual Funds and Other Investment Companies Provide several functions

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

P1.T1. Foundations of Risk. Bionic Turtle FRM Practice Questions. Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition

P1.T1. Foundations of Risk Bionic Turtle FRM Practice Questions Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition By David Harper, CFA FRM CIPM www.bionicturtle.com Bodie, Chapter 10:

P1.T1. Foundations of Risk Bionic Turtle FRM Practice Questions Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition By David Harper, CFA FRM CIPM www.bionicturtle.com Bodie, Chapter 10:

Predictability of Stock Returns

Predictability of Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Iraq Correspondence: Ahmet Sekreter, Ishik University, Iraq. Email: ahmet.sekreter@ishik.edu.iq

Predictability of Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Iraq Correspondence: Ahmet Sekreter, Ishik University, Iraq. Email: ahmet.sekreter@ishik.edu.iq

An Analysis of Theories on Stock Returns

An Analysis of Theories on Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq.

An Analysis of Theories on Stock Returns Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq.

Overview of Concepts and Notation

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Study Session 10. Equity Valuation: Valuation Concepts

Study Session 10 : Valuation Concepts Quantitative Methods Study Session 10 Valuation Concepts 30. : Applications and Processes 31. Valuation Concepts LOS 30.a Define/Explain CFAI V4 p. 6, Schweser B3

Study Session 10 : Valuation Concepts Quantitative Methods Study Session 10 Valuation Concepts 30. : Applications and Processes 31. Valuation Concepts LOS 30.a Define/Explain CFAI V4 p. 6, Schweser B3

Chapter 13: Investor Behavior and Capital Market Efficiency

Chapter 13: Investor Behavior and Capital Market Efficiency -1 Chapter 13: Investor Behavior and Capital Market Efficiency Note: Only responsible for sections 13.1 through 13.6 Fundamental question: Is

Chapter 13: Investor Behavior and Capital Market Efficiency -1 Chapter 13: Investor Behavior and Capital Market Efficiency Note: Only responsible for sections 13.1 through 13.6 Fundamental question: Is

Microéconomie de la finance

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

B. Arbitrage Arguments support CAPM.

1 E&G, Ch. 16: APT I. Background. A. CAPM shows that, under many assumptions, equilibrium expected returns are linearly related to β im, the relation between R ii and a single factor, R m. (i.e., equilibrium

1 E&G, Ch. 16: APT I. Background. A. CAPM shows that, under many assumptions, equilibrium expected returns are linearly related to β im, the relation between R ii and a single factor, R m. (i.e., equilibrium

Module 3: Factor Models

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Stocks with Extreme Past Returns: Lotteries or Insurance?

Stocks with Extreme Past Returns: Lotteries or Insurance? Alexander Barinov Terry College of Business University of Georgia June 14, 2013 Alexander Barinov (UGA) Stocks with Extreme Past Returns June 14,

Stocks with Extreme Past Returns: Lotteries or Insurance? Alexander Barinov Terry College of Business University of Georgia June 14, 2013 Alexander Barinov (UGA) Stocks with Extreme Past Returns June 14,

FIN822 project 3 (Due on December 15. Accept printout submission or submission )

") FIN822 project 3 (Due on December 15. Accept printout submission or email submission donglinli2006@yahoo.com. ) Part I The Fama-French Multifactor Model and Mutual Fund Returns Dawn Browne, an investment

FIN822 project 3 (Due on December 15. Accept printout submission or email submission donglinli2006@yahoo.com. ) Part I The Fama-French Multifactor Model and Mutual Fund Returns Dawn Browne, an investment

Topic Four: Fundamentals of a Tactical Asset Allocation (TAA) Strategy

Strategy") Topic Four: Fundamentals of a Tactical Asset Allocation (TAA) Strategy Fundamentals of a Tactical Asset Allocation (TAA) Strategy Tactical Asset Allocation has been defined in various ways, including:

Topic Four: Fundamentals of a Tactical Asset Allocation (TAA) Strategy Fundamentals of a Tactical Asset Allocation (TAA) Strategy Tactical Asset Allocation has been defined in various ways, including:

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Capital Asset Pricing Model - CAPM

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

DOES FINANCIAL LEVERAGE AFFECT TO ABILITY AND EFFICIENCY OF FAMA AND FRENCH THREE FACTORS MODEL? THE CASE OF SET100 IN THAILAND

DOES FINANCIAL LEVERAGE AFFECT TO ABILITY AND EFFICIENCY OF FAMA AND FRENCH THREE FACTORS MODEL? THE CASE OF SET100 IN THAILAND by Tawanrat Prajuntasen Doctor of Business Administration Program, School

DOES FINANCIAL LEVERAGE AFFECT TO ABILITY AND EFFICIENCY OF FAMA AND FRENCH THREE FACTORS MODEL? THE CASE OF SET100 IN THAILAND by Tawanrat Prajuntasen Doctor of Business Administration Program, School

Arbitrage Pricing Theory (APT)

") Arbitrage Pricing Theory (APT) (Text reference: Chapter 11) Topics arbitrage factor models pure factor portfolios expected returns on individual securities comparison with CAPM a different approach 1 Arbitrage

Arbitrage Pricing Theory (APT) (Text reference: Chapter 11) Topics arbitrage factor models pure factor portfolios expected returns on individual securities comparison with CAPM a different approach 1 Arbitrage

IMPLEMENTING THE THREE FACTOR MODEL OF FAMA AND FRENCH ON KUWAIT S EQUITY MARKET

IMPLEMENTING THE THREE FACTOR MODEL OF FAMA AND FRENCH ON KUWAIT S EQUITY MARKET by Fatima Al-Rayes A thesis submitted in partial fulfillment of the requirements for the degree of MSc. Finance and Banking

IMPLEMENTING THE THREE FACTOR MODEL OF FAMA AND FRENCH ON KUWAIT S EQUITY MARKET by Fatima Al-Rayes A thesis submitted in partial fulfillment of the requirements for the degree of MSc. Finance and Banking

The Effect of Kurtosis on the Cross-Section of Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Empirical Evidence. r Mt r ft e i. now do second-pass regression (cross-sectional with N 100): r i r f γ 0 γ 1 b i u i

: r i r f γ 0 γ 1 b i u i") Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM Samit Majumdar Virginia Commonwealth University majumdars@vcu.edu Frank W. Bacon Longwood University baconfw@longwood.edu ABSTRACT: This study

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM Samit Majumdar Virginia Commonwealth University majumdars@vcu.edu Frank W. Bacon Longwood University baconfw@longwood.edu ABSTRACT: This study

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Debt/Equity Ratio and Asset Pricing Analysis

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies Summer 8-1-2017 Debt/Equity Ratio and Asset Pricing Analysis Nicholas Lyle Follow this and additional works

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies Summer 8-1-2017 Debt/Equity Ratio and Asset Pricing Analysis Nicholas Lyle Follow this and additional works

Using risk factors to evaluate investments and build portfolios. Michael Furey Managing Director Delta Research & Advisory

Using risk factors to evaluate investments and build portfolios Michael Furey Managing Director Delta Research & Advisory Pillars for building better quality investor portfolios PortfolioConstruction.com.au

Using risk factors to evaluate investments and build portfolios Michael Furey Managing Director Delta Research & Advisory Pillars for building better quality investor portfolios PortfolioConstruction.com.au

Common Macro Factors and Their Effects on U.S Stock Returns

2011 Common Macro Factors and Their Effects on U.S Stock Returns IBRAHIM CAN HALLAC 6/22/2011 Title: Common Macro Factors and Their Effects on U.S Stock Returns Name : Ibrahim Can Hallac ANR: 374842 Date

2011 Common Macro Factors and Their Effects on U.S Stock Returns IBRAHIM CAN HALLAC 6/22/2011 Title: Common Macro Factors and Their Effects on U.S Stock Returns Name : Ibrahim Can Hallac ANR: 374842 Date

ATestofFameandFrenchThreeFactorModelinPakistanEquityMarket

Global Journal of Management and Business Research Finance Volume 13 Issue 7 Version 1.0 Year 2013 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA)

Global Journal of Management and Business Research Finance Volume 13 Issue 7 Version 1.0 Year 2013 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA)

Measuring Performance with Factor Models

Measuring Performance with Factor Models Bernt Arne Ødegaard February 21, 2017 The Jensen alpha Does the return on a portfolio/asset exceed its required return? α p = r p required return = r p ˆr p To

Measuring Performance with Factor Models Bernt Arne Ødegaard February 21, 2017 The Jensen alpha Does the return on a portfolio/asset exceed its required return? α p = r p required return = r p ˆr p To

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

The Capital Asset Pricing Model

INTRO TO PORTFOLIO RISK MANAGEMENT IN PYTHON The Capital Asset Pricing Model Dakota Wixom Quantitative Analyst QuantCourse.com The Founding Father of Asset Pricing Models CAPM The Capital Asset Pricing

INTRO TO PORTFOLIO RISK MANAGEMENT IN PYTHON The Capital Asset Pricing Model Dakota Wixom Quantitative Analyst QuantCourse.com The Founding Father of Asset Pricing Models CAPM The Capital Asset Pricing

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

Trinity College and Darwin College. University of Cambridge. Taking the Art out of Smart Beta. Ed Fishwick, Cherry Muijsson and Steve Satchell

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

Trinity College and Darwin College University of Cambridge 1 / 32 Problem Definition We revisit last year s smart beta work of Ed Fishwick. The CAPM predicts that higher risk portfolios earn a higher return

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015 Reading Chapters 11 13, not Appendices Chapter 11 Skip 11.2 Mean variance optimization in practice

Monetary Economics Portfolios Risk and Returns Diversification and Risk Factors Gerald P. Dwyer Fall 2015 Reading Chapters 11 13, not Appendices Chapter 11 Skip 11.2 Mean variance optimization in practice

Delta Factors. Glossary

Delta Factors Understanding Investment Performance Behaviour Glossary October 2015 Table of Contents Background... 3 Asset Class Benchmarks used... 4 Methodology... 5 Glossary... 6 Single Factors... 6

Delta Factors Understanding Investment Performance Behaviour Glossary October 2015 Table of Contents Background... 3 Asset Class Benchmarks used... 4 Methodology... 5 Glossary... 6 Single Factors... 6

Financial Markets. Laurent Calvet. John Lewis Topic 13: Capital Asset Pricing Model (CAPM)

") Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Volatility Appendix. B.1 Firm-Specific Uncertainty and Aggregate Volatility

B Volatility Appendix The aggregate volatility risk explanation of the turnover effect relies on three empirical facts. First, the explanation assumes that firm-specific uncertainty comoves with aggregate

B Volatility Appendix The aggregate volatility risk explanation of the turnover effect relies on three empirical facts. First, the explanation assumes that firm-specific uncertainty comoves with aggregate

Economics of Behavioral Finance. Lecture 3

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Solutions to the problems in the supplement are found at the end of the supplement

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

Capital Asset Pricing Model and Arbitrage Pricing Theory

Capital Asset Pricing Model and Nico van der Wijst 1 D. van der Wijst TIØ4146 Finance for science and technology students 1 Capital Asset Pricing Model 2 3 2 D. van der Wijst TIØ4146 Finance for science

Capital Asset Pricing Model and Nico van der Wijst 1 D. van der Wijst TIØ4146 Finance for science and technology students 1 Capital Asset Pricing Model 2 3 2 D. van der Wijst TIØ4146 Finance for science

10 Things We Don t Understand About Finance. 3: The CAPM Is Missing Something!

10 Things We Don t Understand About Finance 3: The CAPM Is Missing Something! Models Need two features Simple enough to understand Complex enough to be generally applicable Does the CAPM satisfy these?

10 Things We Don t Understand About Finance 3: The CAPM Is Missing Something! Models Need two features Simple enough to understand Complex enough to be generally applicable Does the CAPM satisfy these?

Size and Book-to-Market Factors in Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Size and Book-to-Market Factors in Returns Qian Gu Utah State University Follow this and additional

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Size and Book-to-Market Factors in Returns Qian Gu Utah State University Follow this and additional

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF FINANCE

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF FINANCE EXAMINING THE IMPACT OF THE MARKET RISK PREMIUM BIAS ON THE CAPM AND THE FAMA FRENCH MODEL CHRIS DORIAN SPRING 2014 A thesis

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF FINANCE EXAMINING THE IMPACT OF THE MARKET RISK PREMIUM BIAS ON THE CAPM AND THE FAMA FRENCH MODEL CHRIS DORIAN SPRING 2014 A thesis

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Optimal Debt-to-Equity Ratios and Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2014 Optimal Debt-to-Equity Ratios and Stock Returns Courtney D. Winn Utah State University Follow this

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2014 Optimal Debt-to-Equity Ratios and Stock Returns Courtney D. Winn Utah State University Follow this

NBER WORKING PAPER SERIES EXPLAINING THE CROSS-SECTION OF STOCK RETURNS IN JAPAN: FACTORS OR CHARACTERISTICS?

NBER WORKING PAPER SERIES EXPLAINING THE CROSS-SECTION OF STOCK RETURNS IN JAPAN: FACTORS OR CHARACTERISTICS? Kent Daniel Sheridan Titman K.C. John Wei Working Paper 7246 http://www.nber.org/papers/w7246

NBER WORKING PAPER SERIES EXPLAINING THE CROSS-SECTION OF STOCK RETURNS IN JAPAN: FACTORS OR CHARACTERISTICS? Kent Daniel Sheridan Titman K.C. John Wei Working Paper 7246 http://www.nber.org/papers/w7246

LECTURE NOTES 3 ARIEL M. VIALE

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

REVISITING THE ASSET PRICING MODELS

REVISITING THE ASSET PRICING MODELS Mehak Jain 1, Dr. Ravi Singla 2 1 Dept. of Commerce, Punjabi University, Patiala, (India) 2 University School of Applied Management, Punjabi University, Patiala, (India)

REVISITING THE ASSET PRICING MODELS Mehak Jain 1, Dr. Ravi Singla 2 1 Dept. of Commerce, Punjabi University, Patiala, (India) 2 University School of Applied Management, Punjabi University, Patiala, (India)

Information Release and the Fit of the Fama-French Model

Information Release and the Fit of the Fama-French Model Thomas Gilbert Christopher Hrdlicka Avraham Kamara Michael G. Foster School of Business University of Washington April 25, 2014 Risk and Return

Information Release and the Fit of the Fama-French Model Thomas Gilbert Christopher Hrdlicka Avraham Kamara Michael G. Foster School of Business University of Washington April 25, 2014 Risk and Return

HOW TO GENERATE ABNORMAL RETURNS.

STOCKHOLM SCHOOL OF ECONOMICS Bachelor Thesis in Finance, Spring 2010 HOW TO GENERATE ABNORMAL RETURNS. An evaluation of how two famous trading strategies worked during the last two decades. HENRIK MELANDER

STOCKHOLM SCHOOL OF ECONOMICS Bachelor Thesis in Finance, Spring 2010 HOW TO GENERATE ABNORMAL RETURNS. An evaluation of how two famous trading strategies worked during the last two decades. HENRIK MELANDER

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds Tahura Pervin Dept. of Humanities and Social Sciences, Dhaka University of Engineering & Technology (DUET), Gazipur, Bangladesh

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds Tahura Pervin Dept. of Humanities and Social Sciences, Dhaka University of Engineering & Technology (DUET), Gazipur, Bangladesh

15.414: COURSE REVIEW. Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2

: CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2") 15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

Asset Management. Matthieu Gomez April 3, 2018

Asset Management Matthieu Gomez April 3, 2018 Individuals hold directly 47.9% of the market in 1980 and only 21.5% in 2007 1 Private Benefits of Asset Management Why do individuals prefer to pay professionals

Asset Management Matthieu Gomez April 3, 2018 Individuals hold directly 47.9% of the market in 1980 and only 21.5% in 2007 1 Private Benefits of Asset Management Why do individuals prefer to pay professionals

Note on Cost of Capital

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

Homework #4 Suggested Solutions

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

CHAPTER 13. Investor Behavior and Capital Market Efficiency. Chapter Synopsis

CHAPTER 13 Investor Behavior and Capital Market Eiciency Chapter Synopsis 13.1 Competition and Capital Markets When the market portolio is eicient, all stocks are on the security market line and have an

CHAPTER 13 Investor Behavior and Capital Market Eiciency Chapter Synopsis 13.1 Competition and Capital Markets When the market portolio is eicient, all stocks are on the security market line and have an

Chapter 13 Return, Risk, and the Security Market Line

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

Steve Monahan. Discussion of Using earnings forecasts to simultaneously estimate firm-specific cost of equity and long-term growth

Steve Monahan Discussion of Using earnings forecasts to simultaneously estimate firm-specific cost of equity and long-term growth E 0 [r] and E 0 [g] are Important Businesses are institutional arrangements

Steve Monahan Discussion of Using earnings forecasts to simultaneously estimate firm-specific cost of equity and long-term growth E 0 [r] and E 0 [g] are Important Businesses are institutional arrangements

In Search of Distress Risk

In Search of Distress Risk John Y. Campbell, Jens Hilscher, and Jan Szilagyi Presentation to Third Credit Risk Conference: Recent Advances in Credit Risk Research New York, 16 May 2006 What is financial

In Search of Distress Risk John Y. Campbell, Jens Hilscher, and Jan Szilagyi Presentation to Third Credit Risk Conference: Recent Advances in Credit Risk Research New York, 16 May 2006 What is financial

The Three-Factor Model

Chapter 5 The Three-Factor Model The CAPM revolutionized not just portfolio management, but also how we look at finance. Now the relationship between risks and returns is finally defined in a scientifically

Chapter 5 The Three-Factor Model The CAPM revolutionized not just portfolio management, but also how we look at finance. Now the relationship between risks and returns is finally defined in a scientifically

What is Venture Capital?

Venture Capital Topics Covered Definition of Venture Capital Activities of Venture Capitalists Organization Structure of Venture Capital History of Venture Capital Patterns of Venture Capital Investment

Venture Capital Topics Covered Definition of Venture Capital Activities of Venture Capitalists Organization Structure of Venture Capital History of Venture Capital Patterns of Venture Capital Investment

FIN3043 Investment Management. Assignment 1 solution

FIN3043 Investment Management Assignment 1 solution Questions from Chapter 1 9. Lanni Products is a start-up computer software development firm. It currently owns computer equipment worth $30,000 and has

FIN3043 Investment Management Assignment 1 solution Questions from Chapter 1 9. Lanni Products is a start-up computer software development firm. It currently owns computer equipment worth $30,000 and has

Anomalies and Liquidity

Anomalies and Liquidity Anomalies (relative to the CAPM): Small cap firms have higher average returns than predicted by the CAPM High E/P (low P/E) stocks have higher average returns than predicted by

Anomalies and Liquidity Anomalies (relative to the CAPM): Small cap firms have higher average returns than predicted by the CAPM High E/P (low P/E) stocks have higher average returns than predicted by

The study of enhanced performance measurement of mutual funds in Asia Pacific Market

Lingnan Journal of Banking, Finance and Economics Volume 6 2015/2016 Academic Year Issue Article 1 December 2016 The study of enhanced performance measurement of mutual funds in Asia Pacific Market Juzhen

Lingnan Journal of Banking, Finance and Economics Volume 6 2015/2016 Academic Year Issue Article 1 December 2016 The study of enhanced performance measurement of mutual funds in Asia Pacific Market Juzhen

Chilton Investment Seminar

Chilton Investment Seminar Palm Beach, Florida - March 30, 2006 Applied Mathematics and Statistics, Stony Brook University Robert J. Frey, Ph.D. Director, Program in Quantitative Finance Objectives Be

Chilton Investment Seminar Palm Beach, Florida - March 30, 2006 Applied Mathematics and Statistics, Stony Brook University Robert J. Frey, Ph.D. Director, Program in Quantitative Finance Objectives Be

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

State Ownership at the Oslo Stock Exchange. Bernt Arne Ødegaard

State Ownership at the Oslo Stock Exchange Bernt Arne Ødegaard Introduction We ask whether there is a state rebate on companies listed on the Oslo Stock Exchange, i.e. whether companies where the state

State Ownership at the Oslo Stock Exchange Bernt Arne Ødegaard Introduction We ask whether there is a state rebate on companies listed on the Oslo Stock Exchange, i.e. whether companies where the state

Sources and Uses of Available Cost of Capital Data

Sources and Uses of Available Cost of Capital Data American Institute of Certified Public Accountants Cost of Capital Webinar Series January 27, 2010 Robert F. Reilly, CFA, CPA/ABV/CFF Willamette Management

Sources and Uses of Available Cost of Capital Data American Institute of Certified Public Accountants Cost of Capital Webinar Series January 27, 2010 Robert F. Reilly, CFA, CPA/ABV/CFF Willamette Management

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

Is Economic Uncertainty Priced in the Cross-Section of Stock Returns?

Is Economic Uncertainty Priced in the Cross-Section of Stock Returns? Turan Bali, Georgetown University Stephen Brown, NYU Stern, University Yi Tang, Fordham University 2018 CARE Conference, Washington

Is Economic Uncertainty Priced in the Cross-Section of Stock Returns? Turan Bali, Georgetown University Stephen Brown, NYU Stern, University Yi Tang, Fordham University 2018 CARE Conference, Washington

FINS2624: PORTFOLIO MANAGEMENT NOTES

FINS2624: PORTFOLIO MANAGEMENT NOTES UNIVERSITY OF NEW SOUTH WALES Chapter: Table of Contents TABLE OF CONTENTS Bond Pricing 3 Bonds 3 Arbitrage Pricing 3 YTM and Bond prices 4 Realized Compound Yield

FINS2624: PORTFOLIO MANAGEMENT NOTES UNIVERSITY OF NEW SOUTH WALES Chapter: Table of Contents TABLE OF CONTENTS Bond Pricing 3 Bonds 3 Arbitrage Pricing 3 YTM and Bond prices 4 Realized Compound Yield

On the Use of Multifactor Models to Evaluate Mutual Fund Performance

On the Use of Multifactor Models to Evaluate Mutual Fund Performance Joop Huij and Marno Verbeek * We show that multifactor performance estimates for mutual funds suffer from systematic biases, and argue

On the Use of Multifactor Models to Evaluate Mutual Fund Performance Joop Huij and Marno Verbeek * We show that multifactor performance estimates for mutual funds suffer from systematic biases, and argue

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Internet Appendix to The Booms and Busts of Beta Arbitrage

Internet Appendix to The Booms and Busts of Beta Arbitrage Table A1: Event Time CoBAR This table reports some basic statistics of CoBAR, the excess comovement among low beta stocks over the period 1970

Internet Appendix to The Booms and Busts of Beta Arbitrage Table A1: Event Time CoBAR This table reports some basic statistics of CoBAR, the excess comovement among low beta stocks over the period 1970

On the robustness of the CAPM, Fama-French Three-Factor Model and the Carhart Four-Factor Model on the Dutch stock market.

Tilburg University 2014 Bachelor Thesis in Finance On the robustness of the CAPM, Fama-French Three-Factor Model and the Carhart Four-Factor Model on the Dutch stock market. Name: Humberto Levarht y Lopez

Tilburg University 2014 Bachelor Thesis in Finance On the robustness of the CAPM, Fama-French Three-Factor Model and the Carhart Four-Factor Model on the Dutch stock market. Name: Humberto Levarht y Lopez

Arbitrage Asymmetry and the Idiosyncratic Volatility Puzzle

Arbitrage Asymmetry and the Idiosyncratic Volatility Puzzle Robert F. Stambaugh, The Wharton School, University of Pennsylvania and NBER Jianfeng Yu, Carlson School of Management, University of Minnesota

Arbitrage Asymmetry and the Idiosyncratic Volatility Puzzle Robert F. Stambaugh, The Wharton School, University of Pennsylvania and NBER Jianfeng Yu, Carlson School of Management, University of Minnesota

The debate on NBIM and performance measurement, or the factor wars of 2015

The debate on NBIM and performance measurement, or the factor wars of 2015 May 2016 Bernt Arne Ødegaard University of Stavanger (UiS) How to think about NBIM Principal: People of Norway Drawing by Arild

The debate on NBIM and performance measurement, or the factor wars of 2015 May 2016 Bernt Arne Ødegaard University of Stavanger (UiS) How to think about NBIM Principal: People of Norway Drawing by Arild

Paper 2.7 Investment Management

CHARTERED INSTITUTE OF STOCKBROKERS September 2018 Specialised Certification Examination Paper 2.7 Investment Management 2 Question 2 - Portfolio Management 2a) An analyst gathered the following information

CHARTERED INSTITUTE OF STOCKBROKERS September 2018 Specialised Certification Examination Paper 2.7 Investment Management 2 Question 2 - Portfolio Management 2a) An analyst gathered the following information

From optimisation to asset pricing

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

Empirical Study on Market Value Balance Sheet (MVBS)

") Empirical Study on Market Value Balance Sheet (MVBS) Yiqiao Yin Simon Business School November 2015 Abstract This paper presents the results of an empirical study on Market Value Balance Sheet (MVBS).

Empirical Study on Market Value Balance Sheet (MVBS) Yiqiao Yin Simon Business School November 2015 Abstract This paper presents the results of an empirical study on Market Value Balance Sheet (MVBS).

Department of Finance Working Paper Series

NEW YORK UNIVERSITY LEONARD N. STERN SCHOOL OF BUSINESS Department of Finance Working Paper Series FIN-03-005 Does Mutual Fund Performance Vary over the Business Cycle? Anthony W. Lynch, Jessica Wachter

NEW YORK UNIVERSITY LEONARD N. STERN SCHOOL OF BUSINESS Department of Finance Working Paper Series FIN-03-005 Does Mutual Fund Performance Vary over the Business Cycle? Anthony W. Lynch, Jessica Wachter

Interpreting the Value Effect Through the Q-theory: An Empirical Investigation 1

Interpreting the Value Effect Through the Q-theory: An Empirical Investigation 1 Yuhang Xing Rice University This version: July 25, 2006 1 I thank Andrew Ang, Geert Bekaert, John Donaldson, and Maria Vassalou

Interpreting the Value Effect Through the Q-theory: An Empirical Investigation 1 Yuhang Xing Rice University This version: July 25, 2006 1 I thank Andrew Ang, Geert Bekaert, John Donaldson, and Maria Vassalou

CHAPTER II LITERATURE REVIEW

CHAPTER II LITERATURE REVIEW II.1. Risk II.1.1. Risk Definition According Brigham and Houston (2004, p170), Risk is refers to the chance that some unfavorable event will occur (a hazard, a peril, exposure

CHAPTER II LITERATURE REVIEW II.1. Risk II.1.1. Risk Definition According Brigham and Houston (2004, p170), Risk is refers to the chance that some unfavorable event will occur (a hazard, a peril, exposure

Mortgage REITs and Reaching for yield. Aurel Hizmo, Stijn Van Nieuwerburgh and James Vickery

Mortgage REITs and Reaching for yield Aurel Hizmo, Stijn Van Nieuwerburgh and James Vickery 1 Financial intermediation and low interest rates Important for policymakers to monitor emerging financial system

Mortgage REITs and Reaching for yield Aurel Hizmo, Stijn Van Nieuwerburgh and James Vickery 1 Financial intermediation and low interest rates Important for policymakers to monitor emerging financial system

Multiples and future returns

Norwegian School of Economics Bergen, spring, 2015 Multiples and future returns An investigation of pricing multiples ability to predict abnormal returns on the Oslo Stock Exchange Harald Berge and Eivind

Norwegian School of Economics Bergen, spring, 2015 Multiples and future returns An investigation of pricing multiples ability to predict abnormal returns on the Oslo Stock Exchange Harald Berge and Eivind

Chapter 12 Cost of Capital

Chapter 12 Cost of Capital 1. The return that shareholders require on their investment in the firm is called the: A) Dividend yield. B) Cost of equity. C) Capital gains yield. D) Cost of capital. E) Income

Chapter 12 Cost of Capital 1. The return that shareholders require on their investment in the firm is called the: A) Dividend yield. B) Cost of equity. C) Capital gains yield. D) Cost of capital. E) Income