FIN Chapter 8. Risk and Return: Capital Asset Pricing Model. Liuren Wu

|

|

|

- Cornelia Small

- 6 years ago

- Views:

Transcription

1 FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu

2 Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects the returns to a portfolio of investments. 2. Systematic Risk and the Market Portfolio Understand the concept of systematic risk for an individual investment and calculate portfolio systematic risk (beta). 3. The CAPM Estimate an investor s required rate of return using capital asset pricing model. 2

3 8.1 Portfolio Returns and Portfolio Risk By investing in many different stocks to form a portfolio, we can lower the risk without lowering the expected return. The effect of lowering risk via appropriate portfolio formulation is called diversification. By learning how to compute the expected return and risk on a portfolio, we illustrate the effect of diversification. 3

4 The Expected Return of a Portfolio To calculate a portfolio s expected rate of return, we weight each individual investment s expected rate of return using the fraction of money invested in each investment. Example 8.1 : If you invest 25%of your money in the stock of Citi bank (C) with an expected rate of return of -32% and 75% of your money in the stock of Apple (AAPL) with an expected rate of return of 120%, what will be the expected rate of return on this portfolio? Expected rate of return =.25(-32%) +.75 (120%) = 82% 4

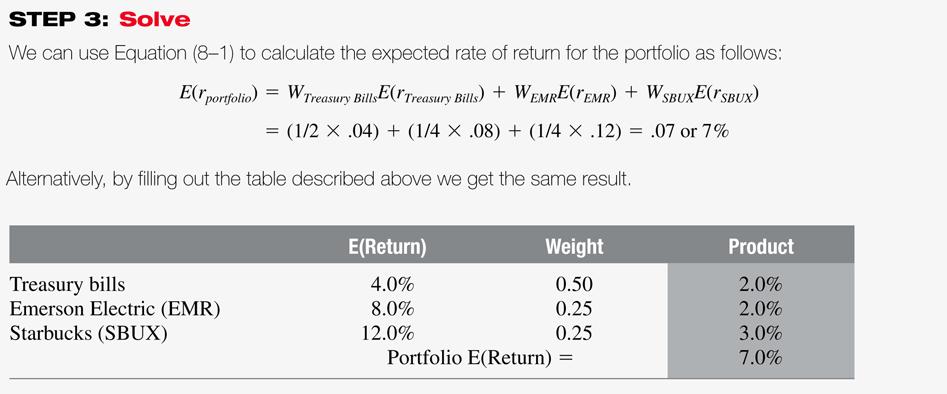

5 Checkpoint 8.1 Calculating a Portfolio s Expected Rate of Return Penny Simpson has her first full-time job and is considering how to invest her savings. Her dad suggested she invest no more than 25% of her savings in the stock of her employer, Emerson Electric (EMR), so she is considering investing the remaining 75% in a combination of a risk-free investment in U.S. Treasury bills, currently paying 4%, and Starbucks (SBUX) common stock. Penny s father has invested in the stock market for many years and suggested that Penny might expect to earn 9% on the Emerson shares and 12% from the Starbucks shares. Penny decides to put 25% in Emerson, 25% in Starbucks, and the remaining 50% in Treasury bills. Given Penny s portfolio allocation, what rate of return should she expect to receive on her investment? 5

6 Checkpoint 8.1 6

7 Checkpoint 8.1: Check Yourself Evaluate the expected return for Penny s portfolio where she places 1/4 th of her money in Treasury bills, half in Starbucks stock, and the remainder in Emerson Electric stock. Answer: 9%. 7

8 Evaluating Portfolio Risk Unlike expected return, standard deviation is not generally equal to the a weighted average of the standard deviations of the returns of investments held in the portfolio. This is because of diversification effects. The diversification gains achieved by adding more investments will depend on the degree of correlation among the investments. The degree of correlation is measured by using the correlation coefficient ( ). r 8

9 Correlation and diversification The correlation coefficient can range from -1.0 (perfect negative correlation), meaning two variables move in perfectly opposite directions to +1.0 (perfect positive correlation), which means the two assets move exactly together. A correlation coefficient of 0 means that there is no relationship between the returns earned by the two assets. As long as the investment returns are not perfectly positively correlated, there will be diversification benefits. However, the diversification benefits will be greater when the correlations are low or negative. The returns on most stocks tend to be positively correlated. 9

10 Standard Deviation of a Portfolio For simplicity, let s focus on a portfolio of 2 stocks: 10

11 Diversification effect Investigate the equation: When the correlation coefficient =1, the portfolio standard deviation becomes a simple weighted average: If the stocks are perfectly moving together, they are essentially the same stock. There is no diversification. For most two different stocks, correlation is less than perfect (<1). Hence, the portfolio standard deviation is less than the weighted average. This is the effect of diversification. r s portfolio = W 1 s 1 +W 2 s 2, when r =1 11

12 Example Determine the expected return and standard deviation of the following portfolio consisting of two stocks that have a correlation coefficient of.75. Portfolio Weight Expected Return Standard Deviation Apple Coca-Cola

13 Answer Expected Return =.5 (.14) +.5 (.14)=.14 or 14% Standard deviation = { (.5 2 x.2 2 )+(.5 2 x.2 2 )+(2x.5x.5x.75x.2x.2)} =.035=.187 or 18.7% Lower than the weighted average of 20%. 13

14 14

15 Portfolio return does not depend on correlation Portfolio standard deviation decreases with declining correlation. 15

16 Checkpoint 8.2 Evaluating a Portfolio s Risk and Return Sarah plans to invest half of her 401k savings in a mutual fund mimicking S&P 500 ad half in an international fun. The expected return on the two funds are 12% and 14%, respectively. The standard deviations are 20% and 30%, respectively. The correlation between the two funds is What would be the expected return and standard deviation for Sarah s portfolio? 16

17 Checkpoint 8.2: Check Yourself Verify the answer: 13%, 23.5% Evaluate the expected return and standard deviation of the portfolio, if the correlation is.20 instead of

18 Answer The expected return remains the same at 13%. The standard deviation declines from 23.5% to 19.62% as the correlations declines from 0.75 to The weight average of the standard deviation of the two funds is 25%, which would be the standard deviation of the portfolio if the two funds are perfectly correlated. Given less than perfect correlation, investing in the two funds leads to a reduction in standard deviation, as a result of diversification. 18

19 8.2 Systematic Risk and Market Portfolio It would be an onerous task to calculate the correlations when we have thousands of possible investments. Capital Asset Pricing Model or the CAPM provides a relatively simple measure of risk. CAPM assumes that investors choose to hold the optimally diversified portfolio that includes all risky investments. This optimally diversified portfolio that includes all of the economy s assets is referred to as the market portfolio. According to the CAPM, the relevant risk of an investment relates to how the investment contributes to the risk of this market portfolio. 19

20 Risk classification To understand how an investment contributes to the risk of the portfolio, we categorize the risks of the individual investments into two categories: 1 2 Systematic risk, and Unsystematic risk, or idiosyncratic risk The systematic risk component measures the contribution of the investment to the risk of the market. For example: War, hike in corporate tax rate. The unsystematic risk is the element of risk that does not contribute to the risk of the market. This component is diversified away when the investment is combined with other investments. For example: Product recall, labor strike, change of management. 20

21 Systematic versus Idiosyncratic Risk An investment s systematic risk is far more important than its unsystematic risk. If the risk of an investment comes mainly from unsystematic risk, the investment will tend to have a low correlation with the returns of most of the other stocks in the portfolio, and will make a minor contribution to the portfolio s overall risk. 21

22 22

23 Diversification and Systematic Risk Figure 8-2 illustrates that as the number of securities in a portfolio increases, the contribution of the unsystematic or diversifiable risk to the standard deviation of the portfolio declines. Systematic or non-diversifiable risk is not reduced even as we increase the number of stocks in the portfolio. Systematic sources of risk (such as inflation, war, interest rates) are common to most investments resulting in a perfect positive correlation and no diversification benefit. Large portfolios will not be affected by unsystematic risk but will be influenced by systematic risk factors. 23

24 Systematic Risk and Beta Systematic risk is measured by beta coefficient, which estimates the extent to which a particular investment s returns vary with the returns on the market portfolio. In practice, it is estimated as the slope of a straight line (see figure 8-3): R i = a + br m + e Beta could be estimated using excel or financial calculator, or readily obtained from various sources on the internet (such as Yahoo Finance and Money Central.com) 24

25 25

26 Utilities companies can be considered less risky because of their lower betas. 26

27 Portfolio Beta The beta of a portfolio measures the systematic risk of the portfolio and is calculated by taking a simple weighted average of the betas for the individual investments contained in the portfolio. Example 8.2 Consider a portfolio that is comprised of four investments with betas equal to 1.5,.75, 1.8 and.60. If you invest equal amount in each investment, what will be the beta for the portfolio? Portfolio beta= 1.5*(1/4)+.75*(1/4)+1.8*(1/4)+.6*(1/4) =

28 8.3 The CAPM CAPM also describes how the betas relate to the expected rates of return that investors require on their investments. The key insight of CAPM is that investors will require a higher rate of return on investments with higher betas. The relation is given by the following linear equation: R market is the expected return on the market portfolio R f is the riskfree rate (return for zero-beta assets). 28

29 Example Example 8.2 What will be the expected rate of return on AAPL stock with a beta of 1.49 if the risk-free rate of interest is 2% and if the market risk premium, which is the difference between expected return on the market portfolio and the risk-free rate of return is estimated to be 8%? AAPL expected return = 2% *8% = 13.92%. 29

30 Checkpoint 8.3: Check Yourself Estimate the expected rates of return for the three utility companies, found in Table 8-1, using the 4.5% risk-free rate and market risk premium of 6%. Use beta estimates from Yahoo: AEP = 0.74,DUK = 0.40,CNP =

31 Solution Beta (AEP) = 4.5% (6%) = 8.94% Beta (DUK) = 4.5% (6%) = 6.9% Beta (CNP) = 4.5% (6%) = 9.42% The higher the beta, higher is the expected return. 31

Risk and Return - Capital Market Theory. Chapter 8

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

Risk and Return - Capital Market Theory. Chapter 8

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 5: Answers to Concepts in Review

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

CHAPTER 8 Risk and Rates of Return

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Return, Risk, and the Security Market Line

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Financial Markets. Laurent Calvet. John Lewis Topic 13: Capital Asset Pricing Model (CAPM)

") Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Chapter 10. Chapter 10 Topics. What is Risk? The big picture. Introduction to Risk, Return, and the Opportunity Cost of Capital

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

Risks and Rate of Return

Risks and Rate of Return Definition of Risk Risk is a chance of financial loss or the variability of returns associated with a given asset A $1000 holder government bond guarantees its holder $5 interest

Risks and Rate of Return Definition of Risk Risk is a chance of financial loss or the variability of returns associated with a given asset A $1000 holder government bond guarantees its holder $5 interest

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Risk and Return Fundamentals. Risk, Return, and Asset Pricing Model. Risk and Return Fundamentals: Risk and Return Defined

Risk and Return Fundamentals Risk, Return, and Asset Pricing Model Financial Risk Management Nattawut Jenwittayaroje, PhD, CFA NIDA Business School National Institute of Development Administration In most

Risk and Return Fundamentals Risk, Return, and Asset Pricing Model Financial Risk Management Nattawut Jenwittayaroje, PhD, CFA NIDA Business School National Institute of Development Administration In most

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Solutions to the problems in the supplement are found at the end of the supplement

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

Chapter 11. Topics Covered. Chapter 11 Objectives. Risk, Return, and Capital Budgeting

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Statistically Speaking

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar. L7 Portfolio and Risk Management

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

(Modern Portfolio Theory Review)

") (Modern Portfolio Theory Review) IFS-A76898 Charts 1-9 Reminder: You must include the Modern Portfolio Theory Disclosure pages with all charts you select to use, either individually or as a group. Information

(Modern Portfolio Theory Review) IFS-A76898 Charts 1-9 Reminder: You must include the Modern Portfolio Theory Disclosure pages with all charts you select to use, either individually or as a group. Information

Risk and Return: From Securities to Portfolios

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below:

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Economics 483. Midterm Exam. 1. Consider the following monthly data for Microsoft stock over the period December 1995 through December 1996:

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar. L7 Portfolio and Risk Management

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management Portfolios A portfolio is a bundle or a combination of individual assets or securities. The portfolio theory provides

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

2013/2014. Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities.

Question One: Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities. 2. Diversification will normally reduce the riskiness

Question One: Tick true or false: 1. "Risk aversion" implies that investors require higher expected returns on riskier than on less risky securities. 2. Diversification will normally reduce the riskiness

FIN Chapter 14. Cost of Capital. Liuren Wu

FIN 3000 Chapter 14 Cost of Capital Liuren Wu Overview 1. Understand the concepts underlying the firm s overall cost of capital and the purpose of its calculation. 2. Evaluate a firm s capital structure,

FIN 3000 Chapter 14 Cost of Capital Liuren Wu Overview 1. Understand the concepts underlying the firm s overall cost of capital and the purpose of its calculation. 2. Evaluate a firm s capital structure,

Money & Capital Markets Fall 2011 Homework #1 Due: Friday, Sept. 9 th. Answer Key

Money & Capital Markets Fall 011 Homework #1 Due: Friday, Sept. 9 th Answer Key 1. (6 points) A pension fund manager is considering two mutual funds. The first is a stock fund. The second is a long-term

Money & Capital Markets Fall 011 Homework #1 Due: Friday, Sept. 9 th Answer Key 1. (6 points) A pension fund manager is considering two mutual funds. The first is a stock fund. The second is a long-term

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

Chapter 7. Introduction to Risk, Return, and the Opportunity Cost of Capital. Principles of Corporate Finance. Slides by Matthew Will

Principles of Corporate Finance Seventh Edition Richard A. Brealey Stewart C. Myers Chapter 7 Introduction to Risk, Return, and the Opportunity Cost of Capital Slides by Matthew Will - Topics Covered 75

Principles of Corporate Finance Seventh Edition Richard A. Brealey Stewart C. Myers Chapter 7 Introduction to Risk, Return, and the Opportunity Cost of Capital Slides by Matthew Will - Topics Covered 75

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar. L7 Portfolio and Risk Management

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management The Benefits of Studying Investments 1. It can help you to understand the financial news. 2. It can help you better

BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L7 Portfolio and Risk Management The Benefits of Studying Investments 1. It can help you to understand the financial news. 2. It can help you better

Optimal Portfolio Selection

Optimal Portfolio Selection We have geometrically described characteristics of the optimal portfolio. Now we turn our attention to a methodology for exactly identifying the optimal portfolio given a set

Optimal Portfolio Selection We have geometrically described characteristics of the optimal portfolio. Now we turn our attention to a methodology for exactly identifying the optimal portfolio given a set

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

Title: Risk, Return, and Capital Budgeting Speaker: Rebecca Stull Created by: Gene Lai. online.wsu.edu

Title: Risk, Return, and Capital Budgeting Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 9 RISK, RETURN, AND CAPITAL BUDGETING Revised by Gene Lai 12-2 Risk, Return and the Capital

Title: Risk, Return, and Capital Budgeting Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 9 RISK, RETURN, AND CAPITAL BUDGETING Revised by Gene Lai 12-2 Risk, Return and the Capital

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Harvard Business School Diversification, the Capital Asset Pricing Model, and the Cost of Equity Capital

Harvard Business School 9-276-183 Rev. November 10, 1993 Diversification, the Capital Asset Pricing Model, and the Cost of Equity Capital Risk as Variability in Return The rate of return an investor receives

Harvard Business School 9-276-183 Rev. November 10, 1993 Diversification, the Capital Asset Pricing Model, and the Cost of Equity Capital Risk as Variability in Return The rate of return an investor receives

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

4. D Spread to treasuries. Spread to treasuries is a measure of a corporate bond s default risk.

www.liontutors.com FIN 301 Final Exam Practice Exam Solutions 1. C Fixed rate par value bond. A bond is sold at par when the coupon rate is equal to the market rate. 2. C As beta decreases, CAPM will decrease

www.liontutors.com FIN 301 Final Exam Practice Exam Solutions 1. C Fixed rate par value bond. A bond is sold at par when the coupon rate is equal to the market rate. 2. C As beta decreases, CAPM will decrease

FIN Second (Practice) Midterm Exam 04/11/06

Midterm Exam 04/11/06") FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

23.1. Assumptions of Capital Market Theory

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

Portfolio Theory and Diversification

Topic 3 Portfolio Theoryand Diversification LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of portfolio formation;. Discuss the idea of diversification; 3. Calculate

Topic 3 Portfolio Theoryand Diversification LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of portfolio formation;. Discuss the idea of diversification; 3. Calculate

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

Binomial Trees. Liuren Wu. Zicklin School of Business, Baruch College. Options Markets

Binomial Trees Liuren Wu Zicklin School of Business, Baruch College Options Markets Binomial tree represents a simple and yet universal method to price options. I am still searching for a numerically efficient,

Binomial Trees Liuren Wu Zicklin School of Business, Baruch College Options Markets Binomial tree represents a simple and yet universal method to price options. I am still searching for a numerically efficient,

ESTIMATING DISCOUNT RATES AND CAPITALIZATION RATES

Intellectual Property Economic Analysis ESTIMATING DISCOUNT RATES AND CAPITALIZATION RATES Timothy J. Meinhart 27 INTRODUCTION In intellectual property analysis, the terms "discount rate" and "capitalization

Intellectual Property Economic Analysis ESTIMATING DISCOUNT RATES AND CAPITALIZATION RATES Timothy J. Meinhart 27 INTRODUCTION In intellectual property analysis, the terms "discount rate" and "capitalization

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

CHAPTER III RISK MANAGEMENT

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

CHAPTER III RISK MANAGEMENT Concept of Risk Risk is the quantified amount which arises due to the likelihood of the occurrence of a future outcome which one does not expect to happen. If one is participating

Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai. online.wsu.

Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 8 INTRODUCTION TO RISK AND RETURN, AND THE OPPORTUNITY COST OF

Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 8 INTRODUCTION TO RISK AND RETURN, AND THE OPPORTUNITY COST OF

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

FIN3043 Investment Management. Assignment 1 solution

FIN3043 Investment Management Assignment 1 solution Questions from Chapter 1 9. Lanni Products is a start-up computer software development firm. It currently owns computer equipment worth $30,000 and has

FIN3043 Investment Management Assignment 1 solution Questions from Chapter 1 9. Lanni Products is a start-up computer software development firm. It currently owns computer equipment worth $30,000 and has

Chapter. Diversification and Risky Asset Allocation. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

E120: Principles of Engineering Economics Part 1: Concepts. (20 points)

") E120: Principles of Engineering Economics Final Exam December 14 th, 2004 Instructor: Professor Shmuel Oren Part 1: Concepts. (20 points) 1. Circle the only correct answer. 1.1 Which of the following statements

E120: Principles of Engineering Economics Final Exam December 14 th, 2004 Instructor: Professor Shmuel Oren Part 1: Concepts. (20 points) 1. Circle the only correct answer. 1.1 Which of the following statements

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Financial Economics: Capital Asset Pricing Model

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

Key investment insights

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

E(r) The Capital Market Line (CML)

The Capital Market Line (CML)") The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

Monetary Economics Cost of Capital. Gerald P. Dwyer Fall 2015

Monetary Economics Cost of Capital Gerald P. Dwyer Fall 2015 Cost of Capital Value of firm and capital structure Cost of stock to a firm CAPM Weighted average cost of capital Leverage and risk Modigliani

Monetary Economics Cost of Capital Gerald P. Dwyer Fall 2015 Cost of Capital Value of firm and capital structure Cost of stock to a firm CAPM Weighted average cost of capital Leverage and risk Modigliani

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Port(A,B) is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.

is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.") Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

- P P THE RELATION BETWEEN RISK AND RETURN. Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Analysis INTRODUCTION OBJECTIVES

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

CMA. Financial Decision Making

2018 Edition CMA Preparatory Program Part 2 Financial Decision Making Risk and Return Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box 6553 Columbus, Ohio 43206 (866) 807-HOCK

2018 Edition CMA Preparatory Program Part 2 Financial Decision Making Risk and Return Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box 6553 Columbus, Ohio 43206 (866) 807-HOCK

By: Lenore E. Hawkins January 22 nd, 2010

The following is a high level overview of bonds, (including pricing, duration and the impact of maturity, yield and coupon rates on duration and price) which hopefully provides a thorough and not too painful

The following is a high level overview of bonds, (including pricing, duration and the impact of maturity, yield and coupon rates on duration and price) which hopefully provides a thorough and not too painful

Geoff Considine, Ph.D.

Accounting for Total Portfolio Diversification Geoff Considine, Ph.D. Copyright Quantext, Inc. 2006 1 Understanding Diversification One of the most central, but misunderstood, topics in asset allocation

Accounting for Total Portfolio Diversification Geoff Considine, Ph.D. Copyright Quantext, Inc. 2006 1 Understanding Diversification One of the most central, but misunderstood, topics in asset allocation

P2.T8. Risk Management & Investment Management. Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition.

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

Comprehensive Project

APPENDIX A Comprehensive Project One of the best ways to gain a clear understanding of the key concepts explained in this text is to apply them directly to actual situations. This comprehensive project

APPENDIX A Comprehensive Project One of the best ways to gain a clear understanding of the key concepts explained in this text is to apply them directly to actual situations. This comprehensive project

CHAPTER 8: INDEX MODELS

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

Investment Analysis (FIN 383) Fall Homework 5

Fall Homework 5") Investment Analysis (FIN 383) Fall 2009 Homework 5 Instructions: please read carefully You should show your work how to get the answer for each calculation question to get full credit The due date is Tuesday,

Investment Analysis (FIN 383) Fall 2009 Homework 5 Instructions: please read carefully You should show your work how to get the answer for each calculation question to get full credit The due date is Tuesday,

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

WEB APPENDIX 8A 7.1 ( 8.9)

") WEB APPENDIX 8A CALCULATING BETA COEFFICIENTS The CAPM is an ex ante model, which means that all of the variables represent before-the-fact expected values. In particular, the beta coefficient used in

WEB APPENDIX 8A CALCULATING BETA COEFFICIENTS The CAPM is an ex ante model, which means that all of the variables represent before-the-fact expected values. In particular, the beta coefficient used in

MHSA 8630 Healthcare Financial Management Principles of Financial Risk

MHSA 8630 Healthcare Financial Management Principles of Financial Risk ** Risk, in a general context, refers to uncertainty of outcome, whether the outcome is a financial loss, a financial return that

MHSA 8630 Healthcare Financial Management Principles of Financial Risk ** Risk, in a general context, refers to uncertainty of outcome, whether the outcome is a financial loss, a financial return that

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory Hedge Portfolios A portfolio that has zero risk is said to be "perfectly hedged" or, in the jargon of Economics and Finance, is referred

Hedge Portfolios, the No Arbitrage Condition & Arbitrage Pricing Theory Hedge Portfolios A portfolio that has zero risk is said to be "perfectly hedged" or, in the jargon of Economics and Finance, is referred