Chapter. Diversification and Risky Asset Allocation. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

|

|

|

- Wilfred Franklin

- 6 years ago

- Views:

Transcription

1 Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved.

2 Diversification Intuitively, we all know that if you hold many investments Through time, some will increase in value Through time, some will decrease in value It is unlikely that their values will all change in the same way Diversification has a profound effect on portfolio return and portfolio risk. ut, exactly how does diversification work? 11-

3 Diversification and Asset Allocation Our goal in this chapter is to examine the role of diversification and asset allocation in investing. In the early 1950s, professor Harry Markowitz was the first to examine the role and impact of diversification. ased on his work, we will see how diversification works, and we can be sure that we have efficiently diversified portfolios. An efficiently diversified portfolio is one that has the highest expected return, given its risk. You must be aware that diversification concerns expected returns. 11-3

4 Expected Returns, I. Expected return is the weighted average return on a risky asset, from today to some future date. The formula is: expected return i = n [ ps returni,s ] To calculate an expected return, you must first: Decide on the number of possible economic scenarios that might occur. Estimate how well the security will perform in each scenario, and Assign a probability to each scenario (TW, finance professors call these economic scenarios, states. ) The next slide shows how the expected return formula is used when there are two states. Note that the states are equally likely to occur in this example. UT! They do not have to be equally likely--they can have different probabilities of occurring. s=

5 Expected Return, II. Suppose: There are two stocks: Starcents Jpod We are looking at a period of one year. Investors agree that the expected return: for Starcents is 5 percent for Jpod is 0 percent Why would anyone want to hold Jpod shares when Starcents is expected to have a higher return? 11-5

6 Expected Return, III. The answer depends on risk Starcents is expected to return 5 percent ut the realized return on Starcents could be significantly higher or lower than 5 percent Similarly, the realized return on Jpod could be significantly higher or lower than 0 percent. 11-6

7 Calculating Expected Returns 11-7

8 Expected Risk Premium Recall: expected risk premium = expected return riskfree rate Suppose riskfree investments have an 8% return. If so, the expected risk premium on Jpod is 1% The expected risk premium on Starcents is 17% This expected risk premium is simply the difference between the expected return on the risky asset in question and the certain return on a risk-free investment 11-8

9 Calculating the Variance of Expected Returns The variance of expected returns is calculated using this formula: Variance = = [ n ( ) ] ps returns expected return s= 1 This formula is not as difficult as it appears. This formula says is to add up the squared deviations of each return from its expected return after it has been multiplied by the probability of observing a particular economic state (denoted by s ). The standard deviation is simply the square root of the variance. Standard Deviation = = Variance 11-9

10 Example: Calculating Expected Returns and Variances: Equal State Probabilities Calculating Expected Returns: Starcents: Jpod: (1) () (3) (4) (5) (6) Return if Return if State of Probability of State Product: State Product: Economy State of Economy Occurs () x (3) Occurs () x (5) Recession oom Sum: 1.00 E(Ret): 0.5 E(Ret): 0.0 Calculating Variance of Expected Returns: Starcents: (1) () (3) (4) (5) (6) (7) Return if State of Probability of State Expected Difference: Squared: Product: Economy State of Economy Occurs Return: (3) - (4) (5) x (5) () x (6) Recession oom Sum: 1.00 Sum = the Variance: Note that the second spreadsheet is only for Starcents. What would you get for Jpod? Standard Deviation:

11 Expected Returns and Variances, Starcents and Jpod 11-11

12 Portfolios Portfolios are groups of assets, such as stocks and bonds, that are held by an investor. One convenient way to describe a portfolio is by listing the proportion of the total value of the portfolio that is invested into each asset. These proportions are called portfolio weights. Portfolio weights are sometimes expressed in percentages. However, in calculations, make sure you use proportions (i.e., decimals). 11-1

13 Portfolios: Expected Returns The expected return on a portfolio is a linear combination, or weighted average, of the expected returns on the assets in that portfolio. The formula, for n assets, is: ( ) = [ ( )] P wi E Ri E R i= 1 In the formula: E(R P ) = expected portfolio return w i = portfolio weight in portfolio asset i E(R i ) = expected return for portfolio asset i n 11-13

14 Example: Calculating Portfolio Expected Returns Note that the portfolio weight in Jpod = 1 portfolio weight in Starcents. Calculating Expected Portfolio Returns: (1) () (3) (4) (5) (6) (7) (8) (9) (10) Starcents Starcents Jpod Jpod Portfolio Return if Portfolio Contribution Return if Portfolio Contribution Return State of Prob. State Weight Product: State Weight Product: Sum: Product: Economy of State Occurs in Starcents: (3) x (4) Occurs in Jpod: (6) x (7) (5) + (8) () x (9) Recession oom Sum: 1.00 Sum is Expected Portfolio Return:

15 Variance of Portfolio Expected Returns Note: Unlike returns, portfolio variance is generally not a simple weighted average of the variances of the assets in the portfolio. If there are n states, the formula is: VAR n [ ] s p, s P ( R ) = p { E( R ) E( R )} P s = 1 In the formula, VAR(R P ) = variance of portfolio expected return p s = probability of state of economy, s E(R p,s ) = expected portfolio return in state s E(R p ) = portfolio expected return Note that the formula is like the formula for the variance of the expected return of a single asset

16 Example: Calculating Variance of Portfolio Expected Returns It is possible to construct a portfolio of risky assets with zero portfolio variance! What? How? (Open this spreadsheet, scroll up, and set the weight in Starcents to /11ths.) What happens when you use.40 as the weight in Starcents? Calculating Variance of Expected Portfolio Returns: (1) () (3) (4) (5) (6) (7) Return if State of Prob. State Expected Difference: Squared: Product: Economy of State Occurs: Return: (3) - (4) (5) x (5) () x (6) Recession oom Sum: 1.00 Sum is Variance: Standard Deviation:

17 Diversification and Risk, I

18 Diversification and Risk, II

19 Why Diversification Works, I. Correlation: The tendency of the returns on two assets to move together. Imperfect correlation is the key reason why diversification reduces portfolio risk as measured by the portfolio standard deviation. Positively correlated assets tend to move up and down together. Negatively correlated assets tend to move in opposite directions. Imperfect correlation, positive or negative, is why diversification reduces portfolio risk

20 Why Diversification Works, II. The correlation coefficient is denoted by Corr(R A, R ) or simply, ρ A,. The correlation coefficient measures correlation and ranges from: From: Through: To: (perfect negative correlation) (uncorrelated) (perfect positive correlation) 11-0

21 Why Diversification Works, III. 11-1

22 Why Diversification Works, IV. 11-

23 Why Diversification Works, V. 11-3

24 11-4 Calculating Portfolio Risk For a portfolio of two assets, A and, the variance of the return on the portfolio is: Where: x A = portfolio weight of asset A x = portfolio weight of asset such that x A + x = 1. (Important: Recall Correlation Definition!) ) R CORR(R x x x x COV(A,) x x x x A A A A A p A A A p + + = + + =

25 The Importance of Asset Allocation, Part 1. Suppose that as a very conservative, risk-averse investor, you decide to invest all of your money in a bond mutual fund. Very conservative, indeed? Uh, is this decision a wise one? 11-5

26 Correlation and Diversification, I. 11-6

27 Correlation and Diversification, II. 11-7

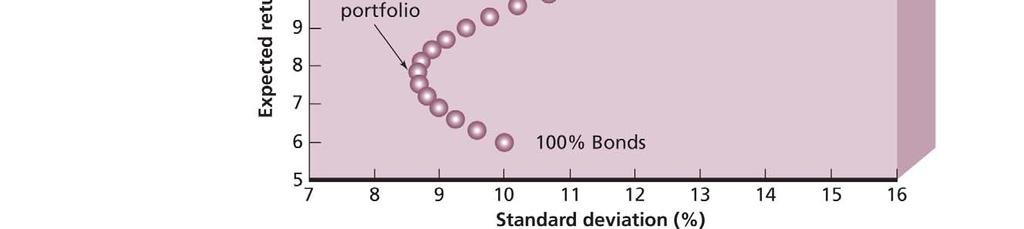

28 Correlation and Diversification, III. The various combinations of risk and return available all fall on a smooth curve. This curve is called an investment opportunity set,because it shows the possible combinations of risk and return available from portfolios of these two assets. A portfolio that offers the highest return for its level of risk is said to be an efficient portfolio. The undesirable portfolios are said to be dominated or inefficient. 11-8

29 More on Correlation & the Risk-Return Trade-Off (The Next Slide is an Excel Example) 11-9

30 Example: Correlation and the Risk-Return Trade-Off, Two Risky Assets Expected Standard Inputs Return Deviation Risky Asset % 0.0% Risky Asset 8.0% 15.0% Correlation 30.0% Expected Return 18% 16% 14% 1% 10% 8% 6% 4% % 0% Efficient Set--Two Asset Portfolio 0% 5% 10% 15% 0% 5% 30% Standard Deviation 11-30

31 The Importance of Asset Allocation, Part. We can illustrate the importance of asset allocation with 3 assets. How? Suppose we invest in three mutual funds: One that contains Foreign Stocks, F One that contains U.S. Stocks, S One that contains U.S. onds, Foreign Stocks, F U.S. Stocks, S U.S. onds, Expected Return 18% 1 8 Standard Deviation 35% 14 Figure 11.6 shows the results of calculating various expected returns and portfolio standard deviations with these three assets

32 Risk and Return with Multiple Assets, I. 11-3

33 11-33 Risk and Return with Multiple Assets, II. Figure 11.6 used these formulas for portfolio return and variance: ut, we made a simplifying assumption. We assumed that the assets are all uncorrelated. If so, the portfolio variance becomes: S S F F p S S S F F F S F S F S F S S F F p S S F F p x x x ) R CORR(R x x ) CORR(R R x x ) CORR(R R x x x x x R x R x R x r + + = = + + =

34 The Markowitz Efficient Frontier The Markowitz Efficient frontier is the set of portfolios with the maximum return for a given risk AND the minimum risk given a return. For the plot, the upper left-hand boundary is the Markowitz efficient frontier. All the other possible combinations are inefficient. That is, investors would not hold these portfolios because they could get either more return for a given level of risk, or less risk for a given level of return

35 Example: Web-ased Markowitz Frontiers

36 Useful Internet Sites (to find expected returns) (for more on risk measures) (also contains more on risk measure) (measure diversification using instant x-ray ) (review modern portfolio theory) (check out the online journal) 11-36

37 Chapter Review, I. Expected Returns and Variances Expected returns Calculating the variance Portfolios Portfolio weights Portfolio expected returns Portfolio variance 11-37

38 Chapter Review, II. Diversification and Portfolio Risk The Effect of diversification: Another lesson from market history The principle of diversification Correlation and Diversification Why diversification works Calculating portfolio risk More on correlation and the risk-return trade-off The Markowitz Efficient Frontier Risk and return with multiple assets 11-38

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

1 A Brief History of. Chapter. Risk and Return. Dollar Returns. PercentReturn. Learning Objectives. A Brief History of Risk and Return

Chapter Learning Objectives To become a wise investor (maybe even one with too much money), you need to know: 1 A Brief History of Risk and Return How to calculate the return on an investment using different

Chapter Learning Objectives To become a wise investor (maybe even one with too much money), you need to know: 1 A Brief History of Risk and Return How to calculate the return on an investment using different

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

Portfolio Theory and Diversification

Topic 3 Portfolio Theoryand Diversification LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of portfolio formation;. Discuss the idea of diversification; 3. Calculate

Topic 3 Portfolio Theoryand Diversification LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of portfolio formation;. Discuss the idea of diversification; 3. Calculate

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

COPYRIGHTED MATERIAL. Portfolio Selection CHAPTER 1. JWPR026-Fabozzi c01 June 22, :54

CHAPTER 1 Portfolio Selection FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management HARRY M. MARKOWITZ, PhD Consultant FRANCIS GUPTA, PhD Director, Research, Dow

CHAPTER 1 Portfolio Selection FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management HARRY M. MARKOWITZ, PhD Consultant FRANCIS GUPTA, PhD Director, Research, Dow

P2.T8. Risk Management & Investment Management. Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition.

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

Mean-Variance Model for Portfolio Selection

Mean-Variance Model for Portfolio Selection FRANK J. FABOZZI, PhD, CFA, CPA Professor of Finance, EDHEC Business School HARRY M. MARKOWITZ, PhD Consultant PETTER N. KOLM, PhD Director of the Mathematics

Mean-Variance Model for Portfolio Selection FRANK J. FABOZZI, PhD, CFA, CPA Professor of Finance, EDHEC Business School HARRY M. MARKOWITZ, PhD Consultant PETTER N. KOLM, PhD Director of the Mathematics

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

MS-E2114 Investment Science Lecture 5: Mean-variance portfolio theory A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

Chapter 6 Efficient Diversification. b. Calculation of mean return and variance for the stock fund: (A) (B) (C) (D) (E) (F) (G)

(B) (C) (D) (E) (F) (G)") Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Chapter 10. Chapter 10 Topics. What is Risk? The big picture. Introduction to Risk, Return, and the Opportunity Cost of Capital

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Lecture 8 & 9 Risk & Rates of Return

Lecture 8 & 9 Risk & Rates of Return We start from the basic premise that investors LIKE return and DISLIKE risk. Therefore, people will invest in risky assets only if they expect to receive higher returns.

Lecture 8 & 9 Risk & Rates of Return We start from the basic premise that investors LIKE return and DISLIKE risk. Therefore, people will invest in risky assets only if they expect to receive higher returns.

Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai. online.wsu.

Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 8 INTRODUCTION TO RISK AND RETURN, AND THE OPPORTUNITY COST OF

Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 8 INTRODUCTION TO RISK AND RETURN, AND THE OPPORTUNITY COST OF

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Risk and Return: From Securities to Portfolios

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

Theoretical Aspects Concerning the Use of the Markowitz Model in the Management of Financial Instruments Portfolios

Theoretical Aspects Concerning the Use of the Markowitz Model in the Management of Financial Instruments Portfolios Lecturer Mădălina - Gabriela ANGHEL, PhD Student madalinagabriela_anghel@yahoo.com Artifex

Theoretical Aspects Concerning the Use of the Markowitz Model in the Management of Financial Instruments Portfolios Lecturer Mădălina - Gabriela ANGHEL, PhD Student madalinagabriela_anghel@yahoo.com Artifex

Chapter 2 Portfolio Management and the Capital Asset Pricing Model

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

Financial Analysis The Price of Risk. Skema Business School. Portfolio Management 1.

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Appendix S: Content Portfolios and Diversification

Appendix S: Content Portfolios and Diversification 1188 The expected return on a portfolio is a weighted average of the expected return on the individual id assets; but estimating the risk, or standard

Appendix S: Content Portfolios and Diversification 1188 The expected return on a portfolio is a weighted average of the expected return on the individual id assets; but estimating the risk, or standard

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 5 Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Supply Interest

CHAPTER 5 Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Supply Interest

FIN Second (Practice) Midterm Exam 04/11/06

Midterm Exam 04/11/06") FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

In March 2010, GameStop, Cintas, and United Natural Foods, Inc., joined a host of other companies

CHAPTER Return and Risk: The Capital 11 Asset Pricing Model (CAPM) OPENING CASE In March 2010, GameStop, Cintas, and United Natural Foods, Inc., joined a host of other companies in announcing operating

CHAPTER Return and Risk: The Capital 11 Asset Pricing Model (CAPM) OPENING CASE In March 2010, GameStop, Cintas, and United Natural Foods, Inc., joined a host of other companies in announcing operating

Analysis INTRODUCTION OBJECTIVES

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Financial Market Analysis (FMAx) Module 6

Module 6") Financial Market Analysis (FMAx) Module 6 Asset Allocation and iversification This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for

Financial Market Analysis (FMAx) Module 6 Asset Allocation and iversification This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for

(Modern Portfolio Theory Review)

") (Modern Portfolio Theory Review) IFS-A76898 Charts 1-9 Reminder: You must include the Modern Portfolio Theory Disclosure pages with all charts you select to use, either individually or as a group. Information

(Modern Portfolio Theory Review) IFS-A76898 Charts 1-9 Reminder: You must include the Modern Portfolio Theory Disclosure pages with all charts you select to use, either individually or as a group. Information

Risk, return, and diversification

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

BOND ANALYTICS. Aditya Vyas IDFC Ltd.

BOND ANALYTICS Aditya Vyas IDFC Ltd. Bond Valuation-Basics The basic components of valuing any asset are: An estimate of the future cash flow stream from owning the asset The required rate of return for

BOND ANALYTICS Aditya Vyas IDFC Ltd. Bond Valuation-Basics The basic components of valuing any asset are: An estimate of the future cash flow stream from owning the asset The required rate of return for

Chapter 8. Portfolio Selection. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

Chapter 13 Return, Risk, and the Security Market Line

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Finance 100: Corporate Finance. Professor Michael R. Roberts Quiz 3 November 8, 2006

Finance 100: Corporate Finance Professor Michael R. Roberts Quiz 3 November 8, 006 Name: Solutions Section ( Points...no joke!): Question Maximum Student Score 1 30 5 3 5 4 0 Total 100 Instructions: Please

Finance 100: Corporate Finance Professor Michael R. Roberts Quiz 3 November 8, 006 Name: Solutions Section ( Points...no joke!): Question Maximum Student Score 1 30 5 3 5 4 0 Total 100 Instructions: Please

EFFICIENT DIVERSIFICATION

6 EFFICIENT DIVERSIFICATION AFTER STUDYING THIS CHAPTER YOU SHOULD BE ABLE TO: Show how covariance and correlation affect the power of diversification to reduce portfolio risk. Construct efficient portfolios.

6 EFFICIENT DIVERSIFICATION AFTER STUDYING THIS CHAPTER YOU SHOULD BE ABLE TO: Show how covariance and correlation affect the power of diversification to reduce portfolio risk. Construct efficient portfolios.

Lecture Notes 9. Jussi Klemelä. December 2, 2014

Lecture Notes 9 Jussi Klemelä December 2, 204 Markowitz Bullets A Markowitz bullet is a scatter plot of points, where each point corresponds to a portfolio, the x-coordinate of a point is the standard

Lecture Notes 9 Jussi Klemelä December 2, 204 Markowitz Bullets A Markowitz bullet is a scatter plot of points, where each point corresponds to a portfolio, the x-coordinate of a point is the standard

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Key investment insights

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

Basic Portfolio Theory B. Espen Eckbo 2011 Key investment insights Diversification: Always think in terms of stock portfolios rather than individual stocks But which portfolio? One that is highly diversified

In terms of covariance the Markowitz portfolio optimisation problem is:

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Session 8: The Markowitz problem p. 1

Session 8: The Markowitz problem Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 8: The Markowitz problem p. 1 Portfolio optimisation Session 8: The Markowitz problem

Session 8: The Markowitz problem Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 8: The Markowitz problem p. 1 Portfolio optimisation Session 8: The Markowitz problem

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

The Fallacy of Large Numbers

The Fallacy of Large umbers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: ovember 6, 2003 ABSTRACT Traditional mean-variance calculations tell us that the

The Fallacy of Large umbers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: ovember 6, 2003 ABSTRACT Traditional mean-variance calculations tell us that the

Mean-Variance Portfolio Choice in Excel

Mean-Variance Portfolio Choice in Excel Prof. Manuela Pedio 20550 Quantitative Methods for Finance August 2018 Let s suppose you can only invest in two assets: a (US) stock index (here represented by the

Mean-Variance Portfolio Choice in Excel Prof. Manuela Pedio 20550 Quantitative Methods for Finance August 2018 Let s suppose you can only invest in two assets: a (US) stock index (here represented by the

Lecture 3: Factor models in modern portfolio choice

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Portfolio models - Podgorica

Outline Holding period return Suppose you invest in a stock-index fund over the next period (e.g. 1 year). The current price is 100$ per share. At the end of the period you receive a dividend of 5$; the

Outline Holding period return Suppose you invest in a stock-index fund over the next period (e.g. 1 year). The current price is 100$ per share. At the end of the period you receive a dividend of 5$; the

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 2 Due: October 20

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

The Fallacy of Large Numbers and A Defense of Diversified Active Managers

The Fallacy of Large umbers and A Defense of Diversified Active Managers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: March 27, 2003 ABSTRACT Traditional

The Fallacy of Large umbers and A Defense of Diversified Active Managers Philip H. Dybvig Washington University in Saint Louis First Draft: March 0, 2003 This Draft: March 27, 2003 ABSTRACT Traditional

Mean-Variance Portfolio Theory

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

FIN Chapter 8. Risk and Return: Capital Asset Pricing Model. Liuren Wu

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

The stochastic discount factor and the CAPM

The stochastic discount factor and the CAPM Pierre Chaigneau pierre.chaigneau@hec.ca November 8, 2011 Can we price all assets by appropriately discounting their future cash flows? What determines the risk

The stochastic discount factor and the CAPM Pierre Chaigneau pierre.chaigneau@hec.ca November 8, 2011 Can we price all assets by appropriately discounting their future cash flows? What determines the risk

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Economics 483. Midterm Exam. 1. Consider the following monthly data for Microsoft stock over the period December 1995 through December 1996:

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 14 BOND PORTFOLIOS

CHAPTER 14 BOND PORTFOLIOS Chapter Overview This chapter describes the international bond market and examines the return and risk properties of international bond portfolios from an investor s perspective.

CHAPTER 14 BOND PORTFOLIOS Chapter Overview This chapter describes the international bond market and examines the return and risk properties of international bond portfolios from an investor s perspective.

Correlation vs. Trends in Portfolio Management: A Common Misinterpretation

Correlation vs. rends in Portfolio Management: A Common Misinterpretation Francois-Serge Lhabitant * Abstract: wo common beliefs in finance are that (i) a high positive correlation signals assets moving

Correlation vs. rends in Portfolio Management: A Common Misinterpretation Francois-Serge Lhabitant * Abstract: wo common beliefs in finance are that (i) a high positive correlation signals assets moving

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

Diversification. Finance 100

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

This assignment is due on Tuesday, September 15, at the beginning of class (or sooner).

.") Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

Econ 434 Professor Ickes Homework Assignment #1: Answer Sheet Fall 2009 This assignment is due on Tuesday, September 15, at the beginning of class (or sooner). 1. Consider the following returns data for

4. Why do you suppose Warren Buffett has never liked gold as an investment?

Econ 156 Gary Smith Fall 2010 Final Examination (150 minutes) No calculators allowed; if calculations are needed, write the explicit equation(s). Do not write Y = ax; solve for X. You can write 100 = 10X;

Econ 156 Gary Smith Fall 2010 Final Examination (150 minutes) No calculators allowed; if calculations are needed, write the explicit equation(s). Do not write Y = ax; solve for X. You can write 100 = 10X;

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Module 6 Portfolio risk and return

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

FINC3017: Investment and Portfolio Management

FINC3017: Investment and Portfolio Management Investment Funds Topic 1: Introduction Unit Trusts: investor s funds are pooled, usually into specific types of assets. o Investors are assigned tradeable

FINC3017: Investment and Portfolio Management Investment Funds Topic 1: Introduction Unit Trusts: investor s funds are pooled, usually into specific types of assets. o Investors are assigned tradeable

Web Extension: Continuous Distributions and Estimating Beta with a Calculator

19878_02W_p001-008.qxd 3/10/06 9:51 AM Page 1 C H A P T E R 2 Web Extension: Continuous Distributions and Estimating Beta with a Calculator This extension explains continuous probability distributions

19878_02W_p001-008.qxd 3/10/06 9:51 AM Page 1 C H A P T E R 2 Web Extension: Continuous Distributions and Estimating Beta with a Calculator This extension explains continuous probability distributions

CHAPTER 6: PORTFOLIO SELECTION

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

Modern Portfolio Theory -Markowitz Model

Modern Portfolio Theory -Markowitz Model Rahul Kumar Project Trainee, IDRBT 3 rd year student Integrated M.Sc. Mathematics & Computing IIT Kharagpur Email: rahulkumar641@gmail.com Project guide: Dr Mahil

Modern Portfolio Theory -Markowitz Model Rahul Kumar Project Trainee, IDRBT 3 rd year student Integrated M.Sc. Mathematics & Computing IIT Kharagpur Email: rahulkumar641@gmail.com Project guide: Dr Mahil

RESEARCH GROUP ADDRESSING INVESTMENT GOALS USING ASSET ALLOCATION

M A Y 2 0 0 3 STRATEGIC INVESTMENT RESEARCH GROUP ADDRESSING INVESTMENT GOALS USING ASSET ALLOCATION T ABLE OF CONTENTS ADDRESSING INVESTMENT GOALS USING ASSET ALLOCATION 1 RISK LIES AT THE HEART OF ASSET

M A Y 2 0 0 3 STRATEGIC INVESTMENT RESEARCH GROUP ADDRESSING INVESTMENT GOALS USING ASSET ALLOCATION T ABLE OF CONTENTS ADDRESSING INVESTMENT GOALS USING ASSET ALLOCATION 1 RISK LIES AT THE HEART OF ASSET

... possibly the most important and least understood topic in finance

Correlation...... possibly the most important and least understood topic in finance 2017 Gary R. Evans. This lecture is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Correlation...... possibly the most important and least understood topic in finance 2017 Gary R. Evans. This lecture is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Estimating Betas in Thinner Markets: The Case of the Athens Stock Exchange

Estimating Betas in Thinner Markets: The Case of the Athens Stock Exchange Thanasis Lampousis Department of Financial Management and Banking University of Piraeus, Greece E-mail: thanosbush@gmail.com Abstract

Estimating Betas in Thinner Markets: The Case of the Athens Stock Exchange Thanasis Lampousis Department of Financial Management and Banking University of Piraeus, Greece E-mail: thanosbush@gmail.com Abstract

Consumption- Savings, Portfolio Choice, and Asset Pricing

Finance 400 A. Penati - G. Pennacchi Consumption- Savings, Portfolio Choice, and Asset Pricing I. The Consumption - Portfolio Choice Problem We have studied the portfolio choice problem of an individual

Finance 400 A. Penati - G. Pennacchi Consumption- Savings, Portfolio Choice, and Asset Pricing I. The Consumption - Portfolio Choice Problem We have studied the portfolio choice problem of an individual

An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Does Portfolio Theory Work During Financial Crises?

Does Portfolio Theory Work During Financial Crises? Harry M. Markowitz, Mark T. Hebner, Mary E. Brunson It is sometimes said that portfolio theory fails during financial crises because: All asset classes

Does Portfolio Theory Work During Financial Crises? Harry M. Markowitz, Mark T. Hebner, Mary E. Brunson It is sometimes said that portfolio theory fails during financial crises because: All asset classes

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

THEORY & PRACTICE FOR FUND MANAGERS. SPRING 2011 Volume 20 Number 1 RISK. special section PARITY. The Voices of Influence iijournals.

T H E J O U R N A L O F THEORY & PRACTICE FOR FUND MANAGERS SPRING 0 Volume 0 Number RISK special section PARITY The Voices of Influence iijournals.com Risk Parity and Diversification EDWARD QIAN EDWARD

T H E J O U R N A L O F THEORY & PRACTICE FOR FUND MANAGERS SPRING 0 Volume 0 Number RISK special section PARITY The Voices of Influence iijournals.com Risk Parity and Diversification EDWARD QIAN EDWARD

MTH6154 Financial Mathematics I Stochastic Interest Rates

MTH6154 Financial Mathematics I Stochastic Interest Rates Contents 4 Stochastic Interest Rates 45 4.1 Fixed Interest Rate Model............................ 45 4.2 Varying Interest Rate Model...........................

MTH6154 Financial Mathematics I Stochastic Interest Rates Contents 4 Stochastic Interest Rates 45 4.1 Fixed Interest Rate Model............................ 45 4.2 Varying Interest Rate Model...........................

- P P THE RELATION BETWEEN RISK AND RETURN. Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

Measuring Risk. Expected value and expected return 9/4/2018. Possibilities, Probabilities and Expected Value

Chapter Five Understanding Risk Introduction Risk cannot be avoided. Everyday decisions involve financial and economic risk. How much car insurance should I buy? Should I refinance my mortgage now or later?

Chapter Five Understanding Risk Introduction Risk cannot be avoided. Everyday decisions involve financial and economic risk. How much car insurance should I buy? Should I refinance my mortgage now or later?