In terms of covariance the Markowitz portfolio optimisation problem is:

|

|

|

- Laurence Carter

- 6 years ago

- Views:

Transcription

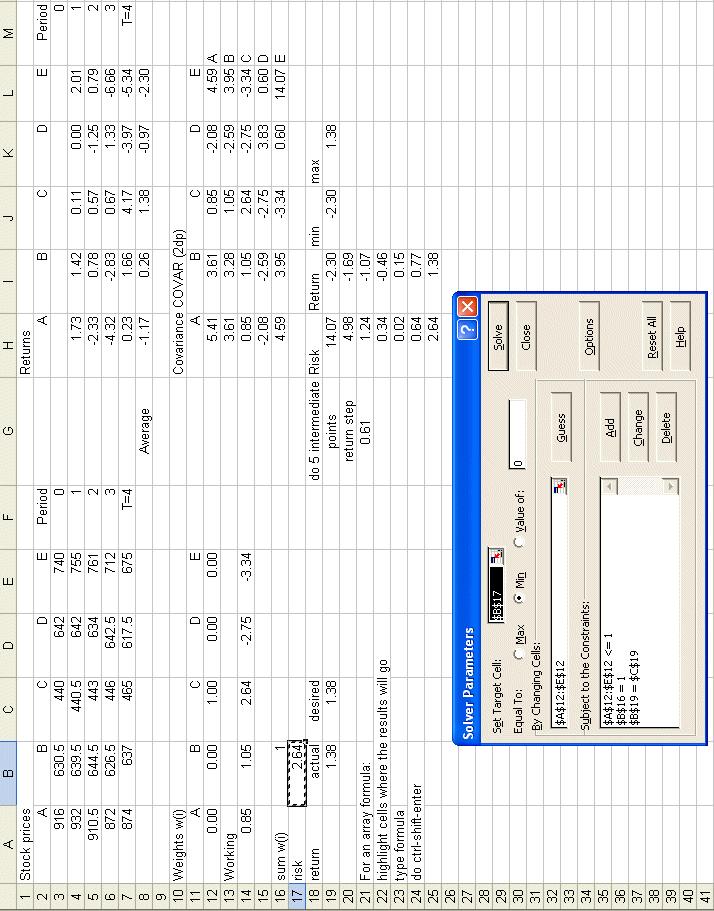

1 Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation it is much more convenient to make use of the COVAR (covariance) function in Excel. In terms of covariance the Markowitz portfolio optimisation problem is: minimise w i w j σ ij () j= subject to w i μ i = R (2) w i = (3) 0 w i,...,n (4) Equation () minimises the total variance (risk) associated with the portfolio (where σ ij is the covariance between the returns associated with assets i and j) whilst equation (2) ensures that the portfolio has an expected return of R. Equation (3) ensures that the proportions add to one. In the Excel sheet seen below we make use of an array formula using MMULT. To see the logic behind this we need to look at the Markowitz objective function in terms of matrix arithmetic. For simplicity suppose N=2 so we have j= w i w j σ ij = w w σ + w w 2 σ 2 + w 2 w σ 2 + w 2 w 2 σ 22 Let us consider the matrix multiplication w w 2 σ σ 2 w σ 2 σ 22 w 2 so we have the row matrix of weights multiplied by the square covariance matrix multiplied by the column matrix of weights If we perform the first multiplication

2 w w 2 σ σ 2 σ 2 σ 22 we will get a row matrix (vector) with two elements. The first element will be w σ +w 2 σ 2 and the second element will be w σ 2 +w 2 σ 22. This row matrix is w σ +w 2 σ 2 w σ 2 +w 2 σ 22 Our complete matrix multiplication w w 2 σ σ 2 w σ 2 σ 22 w 2 therefore becomes w σ +w 2 σ 2 w σ 2 +w 2 σ 22 w w 2 = w σ w + w 2 σ 2 w + w σ 2 w 2 + w 2 σ 22 w 2 The expression we had before from the direct expansion of the summation was w w σ + w w 2 σ 2 + w 2 w σ 2 + w 2 w 2 σ 22 and these two are the same. The MMULT term in the Excel sheet below performs the first multiplication, of the row matrix (array) of weights by the square covariance matrix. In more detail in the Excel sheet shown the MMULT term is in the working cells A4 to E4 and is =MMULT(A2:E2,H2:L6) The risk is shown in cell B7 and is the second matrix multiplication. Here we can make a short cut and just use SUMPRODUCT and so the term in cell B7 is =SUMPRODUCT(A2:E2,A4:E4) so we are taking the SUMPRODUCT of the weights A2:E2 with the working cells A4:E4.

3

4 Capital market line The curve we get when we repeatedly use Solver to find the minimum risk portfolio associated with a given return is a frontier. Parts of that frontier (the portfolios that are efficient, non-dominated) are of interest to us and other parts (in the absence of other considerations) not of interest. Given a number of portfolios that we have plotted on the efficient frontier how can we choose a single portfolio in which to invest? One approach is simply to use our human intuition look at the curve, and make some sort of implicit tradeoff of risk against return. Another approach is to plot what is known as the capital market line. The capital market line is the tangent to the efficient frontier that passes through the risk-free rate on the return axis. This is illustrated below for an example efficient frontier associated with the FTSE00 (assuming a 5% risk-free rate for illustrative purposes). Note here that when we plot the capital market line we need to express risk on the horizontal axis by standard deviation (not variance). FTSE 00 Efficient frontier Capital market line Return Risk (sd) The portfolio associated with the point at which the capital market line and the efficient frontier meet is the one to choose. Simply put this portfolio maximises the (linear) tradeoff between risk and return over and above the risk-free rate.

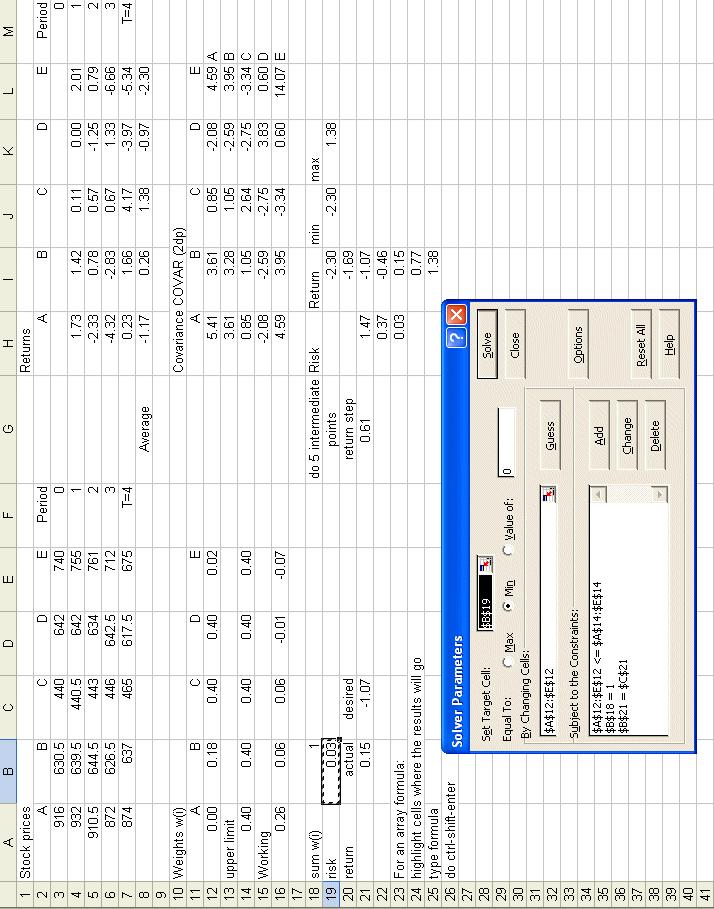

5 Constraining asset investment Practical portfolio optimisation inevitably requires that we move beyond the simple Markowitz model seen above and introduce extra constraints into the problem to better reflect our view as to what we consider an acceptable portfolio. We consider a number of such constraints below. Maximum proportion In our Markowitz portfolio optimisation problem we have no constraint on the proportion of the total investment made in each asset (i.e. each w i can take any value between zero and one). In practice a large w i may (even though the portfolio is on the efficient frontier) expose us to an unacceptable degree of risk via putting too much of our total investment into a single asset. To extend our Markowitz portfolio optimisation problem to the case where we have an upper limit on the proportion of the total investment that can be made in each asset let: δ i be the maximum proportion that can be invested in asset i then we have that the problem becomes minimise subject to j= w i w j σ ij w i μ i = R w i = 0 w i δ i,...,n where the only change from before is that whereas previously we had 0 w i now we have 0 w i δ i The Excel sheet below shows the Solver model with this change implemented with δ i =0.4 Question as you make this change would you expect the risk you incur (for a given return) to be more, or less than before? To see what happens and gain insight then: find the minimum risk associated with a return of.38 (the maximum possible) with δ i =0.4 find the minimum risk associated with a return of -.07 with δ i =0.4

6 These cases illustrate that: certain returns that previously were achievable become unachievable as you add constraints as you add constraints risk (as measured by the Markowitz objective) can only increase The reason we add constraints is that there are considerations outside the Markowitz objective, we are shaping our portfolio through legitimate considerations of our own by adding constraints to the Markowitz model.

7

8 Sector constraints An extension to constraining the total investment in any particular asset is to deal with sector constraints. Typically this assumes that the assets can be classified as belonging to one of a number of sectors (e.g. energy, banking, telecommunications, etc) and then constraining the total investment in any sector. For example suppose for the Excel example shown above we have 2 sectors with sector one containing assets {A, B and E} and sector two containing assets {C and D}. Then constraining the amount invested in each sector to be no more than 60% of the total investment (for example) would mean we need the two constraints: w + w 2 + w w 3 + w Question here we have shown the two sectors as mutually exclusive, so no asset is in both sectors. In reality do you think you will ever encounter an asset that is in two (or more) sectors? Note here that for assets in the same sector we might expect to see positive correlation (i.e. they move together, up or down, with the sector). Hence we have, in an implicit way, already included sector constraints (do not make too much investment in the same sector) in our risk objective. But in reality we might do better to include such constraints explicitly, as we have done here. Trade constraints So far we have talked purely in terms of the proportion invested in each asset. Indeed you may have had the impression of a pile of cash waiting to be invested. However a moment s thought will reveal that in virtually all practical situations we will have already invested in some existing portfolio of assets. We, when we come to portfolio optimisation, are seeking to change that existing portfolio perhaps because we feel we can get better performance from a new portfolio. Technically changing an existing portfolio to a new portfolio is known as rebalancing the portfolio (or just rebalancing). In practical situations we also need to consider: investing new cash in our portfolio (e.g. new pension contributions we might have received); or taking cash out of the portfolio (e.g. to meet liabilities, necessitating selling some of the assets in our existing portfolio) However to ease the mathematical discussion here we will neglect these issues. Suppose X i is the number of units of asset i that we currently own. As a result of portfolio rebalancing we end up with x i units of asset i (where x i is a variable that will be decided as a result of the optimisation). Suppose, for the sake of illustration, we wish to restrict the amount of trading in asset i that we do to T i units so we do not wish to trade more than T i units of asset i, where T i is our choice not something the

9 optimisation can decide for us. Then the trade constrained portfolio rebalancing problem, assuming we have zero transaction cost, is: minimise j= w i w j σ ij subject to w i μ i = R w i = 0 w i,...,n X i T i x i X i + T i,...,n w i = (x i current price of asset i)/ (X i current price of asset i),...,n where the first set of equations are as before. The equation X i T i x i X i + T i ensures that the number of units of asset i after rebalancing (x i ) lies within the desired amount T i of the number of units X i before rebalancing. The last equation here defines the proportion (w i ) invested in each asset in terms of the number of units (x i ) of that asset held. Minimum proportion Sometimes we may end up with a very small proportion w i value as a result of the optimisation indicating that we should just invest a small amount in asset i. This may be administratively inconvenient and so we might wish to impose a constraint upon the minimum amount invested in each asset, say % of our total investment. This can be easily done via the constraint w i 0.0,...,N. Try this for yourself in one of the Solver models how many assets do you end up with in your portfolio? Is this what you expected to happen? This example illustrates that in reality we wanted the constraint if we invest, and we may not, then our investment must have w i 0.0. In other words we wanted the constraint either w i =0 or w i 0.0. This latter constraint cannot be achieved unless

10 we expand our model to include integer variables, which we will do as we turn to cardinality constrained portfolio optimisation.

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall Financial mathematics

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

Lecture 2: Fundamentals of meanvariance

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

Lecture 3: Factor models in modern portfolio choice

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Chapter 2 Portfolio Management and the Capital Asset Pricing Model

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

MARKOWITS EFFICIENT PORTFOLIO (HUANG LITZENBERGER APPROACH)

") MARKOWITS EFFICIENT PORTFOLIO (HUANG LITZENBERGER APPROACH) Huang-Litzenberger approach allows us to find mathematically efficient set of portfolios Assumptions There are no limitations on the positions'

MARKOWITS EFFICIENT PORTFOLIO (HUANG LITZENBERGER APPROACH) Huang-Litzenberger approach allows us to find mathematically efficient set of portfolios Assumptions There are no limitations on the positions'

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Markowitz portfolio theory

Markowitz portfolio theory Farhad Amu, Marcus Millegård February 9, 2009 1 Introduction Optimizing a portfolio is a major area in nance. The objective is to maximize the yield and simultaneously minimize

Markowitz portfolio theory Farhad Amu, Marcus Millegård February 9, 2009 1 Introduction Optimizing a portfolio is a major area in nance. The objective is to maximize the yield and simultaneously minimize

Chapter 6: Supply and Demand with Income in the Form of Endowments

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

Business Mathematics (BK/IBA) Quantitative Research Methods I (EBE) Computer tutorial 4

Quantitative Research Methods I (EBE) Computer tutorial 4") Business Mathematics (BK/IBA) Quantitative Research Methods I (EBE) Computer tutorial 4 Introduction In the last tutorial session, we will continue to work on using Microsoft Excel for quantitative modelling.

Business Mathematics (BK/IBA) Quantitative Research Methods I (EBE) Computer tutorial 4 Introduction In the last tutorial session, we will continue to work on using Microsoft Excel for quantitative modelling.

Mean-variance portfolio rebalancing with transaction costs and funding changes

Journal of the Operational Research Society (2011) 62, 667 --676 2011 Operational Research Society Ltd. All rights reserved. 0160-5682/11 www.palgrave-journals.com/jors/ Mean-variance portfolio rebalancing

Journal of the Operational Research Society (2011) 62, 667 --676 2011 Operational Research Society Ltd. All rights reserved. 0160-5682/11 www.palgrave-journals.com/jors/ Mean-variance portfolio rebalancing

[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright

![[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright](/thumbs/92/107898301.jpg "[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright") Faculty and Institute of Actuaries Claims Reserving Manual v.2 (09/1997) Section D7 [D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright 1. Introduction

Faculty and Institute of Actuaries Claims Reserving Manual v.2 (09/1997) Section D7 [D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright 1. Introduction

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Chapter 7: Portfolio Theory

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

Chapter 7: Portfolio Theory 1. Introduction 2. Portfolio Basics 3. The Feasible Set 4. Portfolio Selection Rules 5. The Efficient Frontier 6. Indifference Curves 7. The Two-Asset Portfolio 8. Unrestriceted

SciBeta CoreShares South-Africa Multi-Beta Multi-Strategy Six-Factor EW

SciBeta CoreShares South-Africa Multi-Beta Multi-Strategy Six-Factor EW Table of Contents Introduction Methodological Terms Geographic Universe Definition: Emerging EMEA Construction: Multi-Beta Multi-Strategy

SciBeta CoreShares South-Africa Multi-Beta Multi-Strategy Six-Factor EW Table of Contents Introduction Methodological Terms Geographic Universe Definition: Emerging EMEA Construction: Multi-Beta Multi-Strategy

Chapter 1 Microeconomics of Consumer Theory

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Techniques for Calculating the Efficient Frontier

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

The Fixed Income Valuation Course. Sanjay K. Nawalkha Gloria M. Soto Natalia A. Beliaeva

Interest Rate Risk Modeling The Fixed Income Valuation Course Sanjay K. Nawalkha Gloria M. Soto Natalia A. Beliaeva Interest t Rate Risk Modeling : The Fixed Income Valuation Course. Sanjay K. Nawalkha,

Interest Rate Risk Modeling The Fixed Income Valuation Course Sanjay K. Nawalkha Gloria M. Soto Natalia A. Beliaeva Interest t Rate Risk Modeling : The Fixed Income Valuation Course. Sanjay K. Nawalkha,

Leverage Aversion, Efficient Frontiers, and the Efficient Region*

Posted SSRN 08/31/01 Last Revised 10/15/01 Leverage Aversion, Efficient Frontiers, and the Efficient Region* Bruce I. Jacobs and Kenneth N. Levy * Previously entitled Leverage Aversion and Portfolio Optimality:

Posted SSRN 08/31/01 Last Revised 10/15/01 Leverage Aversion, Efficient Frontiers, and the Efficient Region* Bruce I. Jacobs and Kenneth N. Levy * Previously entitled Leverage Aversion and Portfolio Optimality:

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired February 2015 Newfound Research LLC 425 Boylston Street 3 rd Floor Boston, MA 02116 www.thinknewfound.com info@thinknewfound.com

Minimizing Timing Luck with Portfolio Tranching The Difference Between Hired and Fired February 2015 Newfound Research LLC 425 Boylston Street 3 rd Floor Boston, MA 02116 www.thinknewfound.com info@thinknewfound.com

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

Problem 1: Markowitz Portfolio (Risky Assets) cov([r 1, r 2, r 3 ] T ) = V =

![Problem 1: Markowitz Portfolio (Risky Assets) cov([r 1, r 2, r 3 ] T ) = V =](/thumbs/92/109671864.jpg "Problem 1: Markowitz Portfolio (Risky Assets) cov([r 1, r 2, r 3 ] T ) = V =") Homework II Financial Mathematics and Economics Professor: Paul J. Atzberger Due: Monday, October 3rd Please turn all homeworks into my mailbox in Amos Eaton Hall by 5:00pm. Problem 1: Markowitz Portfolio

Homework II Financial Mathematics and Economics Professor: Paul J. Atzberger Due: Monday, October 3rd Please turn all homeworks into my mailbox in Amos Eaton Hall by 5:00pm. Problem 1: Markowitz Portfolio

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

1.1 Interest rates Time value of money

Lecture 1 Pre- Derivatives Basics Stocks and bonds are referred to as underlying basic assets in financial markets. Nowadays, more and more derivatives are constructed and traded whose payoffs depend on

Lecture 1 Pre- Derivatives Basics Stocks and bonds are referred to as underlying basic assets in financial markets. Nowadays, more and more derivatives are constructed and traded whose payoffs depend on

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return Value of Money A cash flow is a series of payments or receipts spaced out in time. The key concept in analyzing cash flows is that receiving a $1

TIM 50 Fall 2011 Notes on Cash Flows and Rate of Return Value of Money A cash flow is a series of payments or receipts spaced out in time. The key concept in analyzing cash flows is that receiving a $1

Optimal Portfolios and Random Matrices

Optimal Portfolios and Random Matrices Javier Acosta Nai Li Andres Soto Shen Wang Ziran Yang University of Minnesota, Twin Cities Mentor: Chris Bemis, Whitebox Advisors January 17, 2015 Javier Acosta Nai

Optimal Portfolios and Random Matrices Javier Acosta Nai Li Andres Soto Shen Wang Ziran Yang University of Minnesota, Twin Cities Mentor: Chris Bemis, Whitebox Advisors January 17, 2015 Javier Acosta Nai

Traditional Optimization is Not Optimal for Leverage-Averse Investors

Posted SSRN 10/1/2013 Traditional Optimization is Not Optimal for Leverage-Averse Investors Bruce I. Jacobs and Kenneth N. Levy forthcoming The Journal of Portfolio Management, Winter 2014 Bruce I. Jacobs

Posted SSRN 10/1/2013 Traditional Optimization is Not Optimal for Leverage-Averse Investors Bruce I. Jacobs and Kenneth N. Levy forthcoming The Journal of Portfolio Management, Winter 2014 Bruce I. Jacobs

Elementary Statistics

Chapter 7 Estimation Goal: To become familiar with how to use Excel 2010 for Estimation of Means. There is one Stat Tool in Excel that is used with estimation of means, T.INV.2T. Open Excel and click on

Chapter 7 Estimation Goal: To become familiar with how to use Excel 2010 for Estimation of Means. There is one Stat Tool in Excel that is used with estimation of means, T.INV.2T. Open Excel and click on

The misleading nature of correlations

The misleading nature of correlations In this note we explain certain subtle features of calculating correlations between time-series. Correlation is a measure of linear co-movement, to be contrasted with

The misleading nature of correlations In this note we explain certain subtle features of calculating correlations between time-series. Correlation is a measure of linear co-movement, to be contrasted with

Mean-Variance Portfolio Choice in Excel

Mean-Variance Portfolio Choice in Excel Prof. Manuela Pedio 20550 Quantitative Methods for Finance August 2018 Let s suppose you can only invest in two assets: a (US) stock index (here represented by the

Mean-Variance Portfolio Choice in Excel Prof. Manuela Pedio 20550 Quantitative Methods for Finance August 2018 Let s suppose you can only invest in two assets: a (US) stock index (here represented by the

Portfolio Theory and Diversification

Topic 3 Portfolio Theoryand Diversification LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of portfolio formation;. Discuss the idea of diversification; 3. Calculate

Topic 3 Portfolio Theoryand Diversification LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of portfolio formation;. Discuss the idea of diversification; 3. Calculate

ELEMENTS OF MATRIX MATHEMATICS

QRMC07 9/7/0 4:45 PM Page 5 CHAPTER SEVEN ELEMENTS OF MATRIX MATHEMATICS 7. AN INTRODUCTION TO MATRICES Investors frequently encounter situations involving numerous potential outcomes, many discrete periods

QRMC07 9/7/0 4:45 PM Page 5 CHAPTER SEVEN ELEMENTS OF MATRIX MATHEMATICS 7. AN INTRODUCTION TO MATRICES Investors frequently encounter situations involving numerous potential outcomes, many discrete periods

Random Variables and Probability Distributions

Chapter 3 Random Variables and Probability Distributions Chapter Three Random Variables and Probability Distributions 3. Introduction An event is defined as the possible outcome of an experiment. In engineering

Chapter 3 Random Variables and Probability Distributions Chapter Three Random Variables and Probability Distributions 3. Introduction An event is defined as the possible outcome of an experiment. In engineering

Portfolios that Contain Risky Assets 3: Markowitz Portfolios

Portfolios that Contain Risky Assets 3: Markowitz Portfolios C. David Levermore University of Maryland, College Park, MD Math 42: Mathematical Modeling March 21, 218 version c 218 Charles David Levermore

Portfolios that Contain Risky Assets 3: Markowitz Portfolios C. David Levermore University of Maryland, College Park, MD Math 42: Mathematical Modeling March 21, 218 version c 218 Charles David Levermore

FINANCIAL OPERATIONS RESEARCH: Mean Absolute Deviation And Portfolio Indexing

[1] FINANCIAL OPERATIONS RESEARCH: Mean Absolute Deviation And Portfolio Indexing David Galica Tony Rauchberger Luca Balestrieri A thesis submitted in partial fulfillment of the requirements for the degree

[1] FINANCIAL OPERATIONS RESEARCH: Mean Absolute Deviation And Portfolio Indexing David Galica Tony Rauchberger Luca Balestrieri A thesis submitted in partial fulfillment of the requirements for the degree

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

Modeling Portfolios that Contain Risky Assets Risk and Reward II: Markowitz Portfolios

Modeling Portfolios that Contain Risky Assets Risk and Reward II: Markowitz Portfolios C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling February 4, 2013 version c

Modeling Portfolios that Contain Risky Assets Risk and Reward II: Markowitz Portfolios C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling February 4, 2013 version c

MATH4512 Fundamentals of Mathematical Finance. Topic Two Mean variance portfolio theory. 2.1 Mean and variance of portfolio return

MATH4512 Fundamentals of Mathematical Finance Topic Two Mean variance portfolio theory 2.1 Mean and variance of portfolio return 2.2 Markowitz mean-variance formulation 2.3 Two-fund Theorem 2.4 Inclusion

MATH4512 Fundamentals of Mathematical Finance Topic Two Mean variance portfolio theory 2.1 Mean and variance of portfolio return 2.2 Markowitz mean-variance formulation 2.3 Two-fund Theorem 2.4 Inclusion

Solution Guide to Exercises for Chapter 4 Decision making under uncertainty

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

OR-Notes. J E Beasley

1 of 17 15-05-2013 23:46 OR-Notes J E Beasley OR-Notes are a series of introductory notes on topics that fall under the broad heading of the field of operations research (OR). They were originally used

1 of 17 15-05-2013 23:46 OR-Notes J E Beasley OR-Notes are a series of introductory notes on topics that fall under the broad heading of the field of operations research (OR). They were originally used

The Effects of Responsible Investment: Financial Returns, Risk, Reduction and Impact

The Effects of Responsible Investment: Financial Returns, Risk Reduction and Impact Jonathan Harris ET Index Research Quarter 1 017 This report focuses on three key questions for responsible investors:

The Effects of Responsible Investment: Financial Returns, Risk Reduction and Impact Jonathan Harris ET Index Research Quarter 1 017 This report focuses on three key questions for responsible investors:

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

Course objective. Modélisation Financière et Applications UE 111. Application series #2 Diversification and Efficient Frontier

Course objective Modélisation Financière et Applications UE 111 Application series #2 Diversification and Efficient Frontier Juan Raposo and Fabrice Riva Université Paris Dauphine The previous session

Course objective Modélisation Financière et Applications UE 111 Application series #2 Diversification and Efficient Frontier Juan Raposo and Fabrice Riva Université Paris Dauphine The previous session

RiskTorrent: Using Portfolio Optimisation for Media Streaming

RiskTorrent: Using Portfolio Optimisation for Media Streaming Raul Landa, Miguel Rio Communications and Information Systems Research Group Department of Electronic and Electrical Engineering University

RiskTorrent: Using Portfolio Optimisation for Media Streaming Raul Landa, Miguel Rio Communications and Information Systems Research Group Department of Electronic and Electrical Engineering University

The Markowitz framework

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

IGIDR, Bombay 4 May, 2011 Goals What is a portfolio? Asset classes that define an Indian portfolio, and their markets. Inputs to portfolio optimisation: measuring returns and risk of a portfolio Optimisation

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Jacob: The illustrative worksheet shows the values of the simulation parameters in the upper left section (Cells D5:F10). Is this for documentation?

. Is this for documentation?") PROJECT TEMPLATE: DISCRETE CHANGE IN THE INFLATION RATE (The attached PDF file has better formatting.) {This posting explains how to simulate a discrete change in a parameter and how to use dummy variables

PROJECT TEMPLATE: DISCRETE CHANGE IN THE INFLATION RATE (The attached PDF file has better formatting.) {This posting explains how to simulate a discrete change in a parameter and how to use dummy variables

Portfolios that Contain Risky Assets Portfolio Models 3. Markowitz Portfolios

Portfolios that Contain Risky Assets Portfolio Models 3. Markowitz Portfolios C. David Levermore University of Maryland, College Park Math 42: Mathematical Modeling March 2, 26 version c 26 Charles David

Portfolios that Contain Risky Assets Portfolio Models 3. Markowitz Portfolios C. David Levermore University of Maryland, College Park Math 42: Mathematical Modeling March 2, 26 version c 26 Charles David

$0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 $4.00 Price

Orange Juice Sales and Prices In this module, you will be looking at sales and price data for orange juice in grocery stores. You have data from 83 stores on three brands (Tropicana, Minute Maid, and the

Orange Juice Sales and Prices In this module, you will be looking at sales and price data for orange juice in grocery stores. You have data from 83 stores on three brands (Tropicana, Minute Maid, and the

Econ 424/CFRM 462 Portfolio Risk Budgeting

Econ 424/CFRM 462 Portfolio Risk Budgeting Eric Zivot August 14, 2014 Portfolio Risk Budgeting Idea: Additively decompose a measure of portfolio risk into contributions from the individual assets in the

Econ 424/CFRM 462 Portfolio Risk Budgeting Eric Zivot August 14, 2014 Portfolio Risk Budgeting Idea: Additively decompose a measure of portfolio risk into contributions from the individual assets in the

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

MLC at Boise State Polynomials Activity 2 Week #3

Polynomials Activity 2 Week #3 This activity will discuss rate of change from a graphical prespective. We will be building a t-chart from a function first by hand and then by using Excel. Getting Started

Polynomials Activity 2 Week #3 This activity will discuss rate of change from a graphical prespective. We will be building a t-chart from a function first by hand and then by using Excel. Getting Started

Statistics 431 Spring 2007 P. Shaman. Preliminaries

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

Optimal Portfolio Selection

Optimal Portfolio Selection We have geometrically described characteristics of the optimal portfolio. Now we turn our attention to a methodology for exactly identifying the optimal portfolio given a set

Optimal Portfolio Selection We have geometrically described characteristics of the optimal portfolio. Now we turn our attention to a methodology for exactly identifying the optimal portfolio given a set

Mean Variance Portfolio Theory

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

Chapter 1 Mean Variance Portfolio Theory This book is about portfolio construction and risk analysis in the real-world context where optimization is done with constraints and penalties specified by the

The Expenditure-Output

The Expenditure-Output Model By: OpenStaxCollege (This appendix should be consulted after first reading The Aggregate Demand/ Aggregate Supply Model and The Keynesian Perspective.) The fundamental ideas

The Expenditure-Output Model By: OpenStaxCollege (This appendix should be consulted after first reading The Aggregate Demand/ Aggregate Supply Model and The Keynesian Perspective.) The fundamental ideas

MATH362 Fundamentals of Mathematical Finance. Topic 1 Mean variance portfolio theory. 1.1 Mean and variance of portfolio return

MATH362 Fundamentals of Mathematical Finance Topic 1 Mean variance portfolio theory 1.1 Mean and variance of portfolio return 1.2 Markowitz mean-variance formulation 1.3 Two-fund Theorem 1.4 Inclusion

MATH362 Fundamentals of Mathematical Finance Topic 1 Mean variance portfolio theory 1.1 Mean and variance of portfolio return 1.2 Markowitz mean-variance formulation 1.3 Two-fund Theorem 1.4 Inclusion

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets C. David Levermore University of Maryland, College Park, MD Math 420: Mathematical Modeling March 21, 2018 version c 2018

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets C. David Levermore University of Maryland, College Park, MD Math 420: Mathematical Modeling March 21, 2018 version c 2018

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Freeman School of Business Fall 2003

FINC 748: Investments Ramana Sonti Freeman School of Business Fall 2003 Lecture Note 3B: Optimal risky portfolios To be read with BKM Chapter 8 Statistical Review Portfolio mathematics Mean standard deviation

FINC 748: Investments Ramana Sonti Freeman School of Business Fall 2003 Lecture Note 3B: Optimal risky portfolios To be read with BKM Chapter 8 Statistical Review Portfolio mathematics Mean standard deviation

Budget Setting Strategies for the Company s Divisions

Budget Setting Strategies for the Company s Divisions Menachem Berg Ruud Brekelmans Anja De Waegenaere November 14, 1997 Abstract The paper deals with the issue of budget setting to the divisions of a

Budget Setting Strategies for the Company s Divisions Menachem Berg Ruud Brekelmans Anja De Waegenaere November 14, 1997 Abstract The paper deals with the issue of budget setting to the divisions of a

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

Portfolio Sharpening

Portfolio Sharpening Patrick Burns 21st September 2003 Abstract We explore the effective gain or loss in alpha from the point of view of the investor due to the volatility of a fund and its correlations

Portfolio Sharpening Patrick Burns 21st September 2003 Abstract We explore the effective gain or loss in alpha from the point of view of the investor due to the volatility of a fund and its correlations

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 21, 2016 version

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 21, 2016 version

Research Factor Indexes and Factor Exposure Matching: Like-for-Like Comparisons

Research Factor Indexes and Factor Exposure Matching: Like-for-Like Comparisons October 218 ftserussell.com Contents 1 Introduction... 3 2 The Mathematics of Exposure Matching... 4 3 Selection and Equal

Research Factor Indexes and Factor Exposure Matching: Like-for-Like Comparisons October 218 ftserussell.com Contents 1 Introduction... 3 2 The Mathematics of Exposure Matching... 4 3 Selection and Equal

Module 6 Portfolio risk and return

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Financial Analysis The Price of Risk. Skema Business School. Portfolio Management 1.

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

the display, exploration and transformation of the data are demonstrated and biases typically encountered are highlighted.

1 Insurance data Generalized linear modeling is a methodology for modeling relationships between variables. It generalizes the classical normal linear model, by relaxing some of its restrictive assumptions,

1 Insurance data Generalized linear modeling is a methodology for modeling relationships between variables. It generalizes the classical normal linear model, by relaxing some of its restrictive assumptions,

Mean-Variance Model for Portfolio Selection

Mean-Variance Model for Portfolio Selection FRANK J. FABOZZI, PhD, CFA, CPA Professor of Finance, EDHEC Business School HARRY M. MARKOWITZ, PhD Consultant PETTER N. KOLM, PhD Director of the Mathematics

Mean-Variance Model for Portfolio Selection FRANK J. FABOZZI, PhD, CFA, CPA Professor of Finance, EDHEC Business School HARRY M. MARKOWITZ, PhD Consultant PETTER N. KOLM, PhD Director of the Mathematics

SOCIETY OF ACTUARIES Advanced Topics in General Insurance. Exam GIADV. Date: Thursday, May 1, 2014 Time: 2:00 p.m. 4:15 p.m.

SOCIETY OF ACTUARIES Exam GIADV Date: Thursday, May 1, 014 Time: :00 p.m. 4:15 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 40 points. This exam consists of 8

SOCIETY OF ACTUARIES Exam GIADV Date: Thursday, May 1, 014 Time: :00 p.m. 4:15 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 40 points. This exam consists of 8

Chapter 33: Public Goods

Chapter 33: Public Goods 33.1: Introduction Some people regard the message of this chapter that there are problems with the private provision of public goods as surprising or depressing. But the message

Chapter 33: Public Goods 33.1: Introduction Some people regard the message of this chapter that there are problems with the private provision of public goods as surprising or depressing. But the message

Lecture 10: Performance measures

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

PAULI MURTO, ANDREY ZHUKOV

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

Global Financial Management

Global Financial Management Bond Valuation Copyright 24. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 24. Bonds Bonds are securities that establish a creditor

Global Financial Management Bond Valuation Copyright 24. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 24. Bonds Bonds are securities that establish a creditor

Game Theory. Lecture Notes By Y. Narahari. Department of Computer Science and Automation Indian Institute of Science Bangalore, India October 2012

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India October 22 COOPERATIVE GAME THEORY Correlated Strategies and Correlated

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India October 22 COOPERATIVE GAME THEORY Correlated Strategies and Correlated

7.1 Graphs of Normal Probability Distributions

7 Normal Distributions In Chapter 6, we looked at the distributions of discrete random variables in particular, the binomial. Now we turn out attention to continuous random variables in particular, the

7 Normal Distributions In Chapter 6, we looked at the distributions of discrete random variables in particular, the binomial. Now we turn out attention to continuous random variables in particular, the

Chapter 3. Numerical Descriptive Measures. Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1

Chapter 3 Numerical Descriptive Measures Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1 Objectives In this chapter, you learn to: Describe the properties of central tendency, variation, and

Chapter 3 Numerical Descriptive Measures Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1 Objectives In this chapter, you learn to: Describe the properties of central tendency, variation, and

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Version A. Problem 1. Let X be the continuous random variable defined by the following pdf: 1 x/2 when 0 x 2, f(x) = 0 otherwise.

= 0 otherwise.") Math 224 Q Exam 3A Fall 217 Tues Dec 12 Version A Problem 1. Let X be the continuous random variable defined by the following pdf: { 1 x/2 when x 2, f(x) otherwise. (a) Compute the mean µ E[X]. E[X] x

Math 224 Q Exam 3A Fall 217 Tues Dec 12 Version A Problem 1. Let X be the continuous random variable defined by the following pdf: { 1 x/2 when x 2, f(x) otherwise. (a) Compute the mean µ E[X]. E[X] x

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Modeling Portfolios that Contain Risky Assets Risk and Reward III: Basic Markowitz Portfolio Theory

Modeling Portfolios that Contain Risky Assets Risk and Reward III: Basic Markowitz Portfolio Theory C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 30, 2013

Modeling Portfolios that Contain Risky Assets Risk and Reward III: Basic Markowitz Portfolio Theory C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 30, 2013

The Optimization Process: An example of portfolio optimization

ISyE 6669: Deterministic Optimization The Optimization Process: An example of portfolio optimization Shabbir Ahmed Fall 2002 1 Introduction Optimization can be roughly defined as a quantitative approach

ISyE 6669: Deterministic Optimization The Optimization Process: An example of portfolio optimization Shabbir Ahmed Fall 2002 1 Introduction Optimization can be roughly defined as a quantitative approach

Global Currency Hedging

Global Currency Hedging JOHN Y. CAMPBELL, KARINE SERFATY-DE MEDEIROS, and LUIS M. VICEIRA ABSTRACT Over the period 1975 to 2005, the U.S. dollar (particularly in relation to the Canadian dollar), the euro,

Global Currency Hedging JOHN Y. CAMPBELL, KARINE SERFATY-DE MEDEIROS, and LUIS M. VICEIRA ABSTRACT Over the period 1975 to 2005, the U.S. dollar (particularly in relation to the Canadian dollar), the euro,

Chapter. Diversification and Risky Asset Allocation. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

The Multiplier Model

The Multiplier Model Allin Cottrell March 3, 208 Introduction The basic idea behind the multiplier model is that up to the limit set by full employment or potential GDP the actual level of employment and

The Multiplier Model Allin Cottrell March 3, 208 Introduction The basic idea behind the multiplier model is that up to the limit set by full employment or potential GDP the actual level of employment and

Attilio Meucci. Managing Diversification

Attilio Meucci Managing Diversification A. MEUCCI - Managing Diversification COMMON MEASURES OF DIVERSIFICATION DIVERSIFICATION DISTRIBUTION MEAN-DIVERSIFICATION FRONTIER CONDITIONAL ANALYSIS REFERENCES

Attilio Meucci Managing Diversification A. MEUCCI - Managing Diversification COMMON MEASURES OF DIVERSIFICATION DIVERSIFICATION DISTRIBUTION MEAN-DIVERSIFICATION FRONTIER CONDITIONAL ANALYSIS REFERENCES

Exercise 14 Interest Rates in Binomial Grids

Exercise 4 Interest Rates in Binomial Grids Financial Models in Excel, F65/F65D Peter Raahauge December 5, 2003 The objective with this exercise is to introduce the methodology needed to price callable

Exercise 4 Interest Rates in Binomial Grids Financial Models in Excel, F65/F65D Peter Raahauge December 5, 2003 The objective with this exercise is to introduce the methodology needed to price callable

Expected utility theory; Expected Utility Theory; risk aversion and utility functions

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

Continuous Probability Distributions

Continuous Probability Distributions Chapter 7 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. GOALS 1. Understand the difference between discrete and continuous

Continuous Probability Distributions Chapter 7 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. GOALS 1. Understand the difference between discrete and continuous

Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9

Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9 Optimal Investment with Risky Assets There are N risky assets, named 1, 2,, N, but no risk-free asset. With fixed total dollar

Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9 Optimal Investment with Risky Assets There are N risky assets, named 1, 2,, N, but no risk-free asset. With fixed total dollar

Robust portfolio optimization using second-order cone programming

1 Robust portfolio optimization using second-order cone programming Fiona Kolbert and Laurence Wormald Executive Summary Optimization maintains its importance ithin portfolio management, despite many criticisms

1 Robust portfolio optimization using second-order cone programming Fiona Kolbert and Laurence Wormald Executive Summary Optimization maintains its importance ithin portfolio management, despite many criticisms

Chapter 14 : Statistical Inference 1. Note : Here the 4-th and 5-th editions of the text have different chapters, but the material is the same.

Chapter 14 : Statistical Inference 1 Chapter 14 : Introduction to Statistical Inference Note : Here the 4-th and 5-th editions of the text have different chapters, but the material is the same. Data x

Chapter 14 : Statistical Inference 1 Chapter 14 : Introduction to Statistical Inference Note : Here the 4-th and 5-th editions of the text have different chapters, but the material is the same. Data x