FIN Chapter 14. Cost of Capital. Liuren Wu

|

|

|

- Thomas Palmer

- 6 years ago

- Views:

Transcription

1 FIN 3000 Chapter 14 Cost of Capital Liuren Wu

2 Overview 1. Understand the concepts underlying the firm s overall cost of capital and the purpose of its calculation. 2. Evaluate a firm s capital structure, and determine the relative importance (weight) of each source of financing. 3. Calculate the after-tax cost of debt, preferred stock, and common equity. 4. Calculate a firm s weighted average cost of capital 5. Discuss the pros and cons of using multiple, riskadjusted discount rates. 6. Adjust net present value (NPV) for the costs of issuing new securities when analyzing new investment opportunities.

3 14.1 The Cost of Capital: An Overview Cost of capital is the weighted average of the required returns of the securities that are used to finance the firm. We refer to this as the firm s Weighted Average Cost of Capital, or WACC. Most firms raise capital with a combination of debt, equity, and hybrid securities. WACC incorporates the required rates of return of the firm s lenders and investors and the particular mix of financing sources that the firm uses.

4 How does riskiness of firm affect WACC? Required rate of return on securities will be higher if the firm is riskier. Risk will influence how the firm chooses to finance, i.e., the proportion of debt and equity. WACC is useful in a number of settings: WACC is used to value the firm. WACC is used as a starting point for determining the discount rate for investment projects the firm might undertake. WACC is the appropriate rate to use when evaluating performance, specifically whether or not the firm has created value for its shareholders.

5 The WACC equation

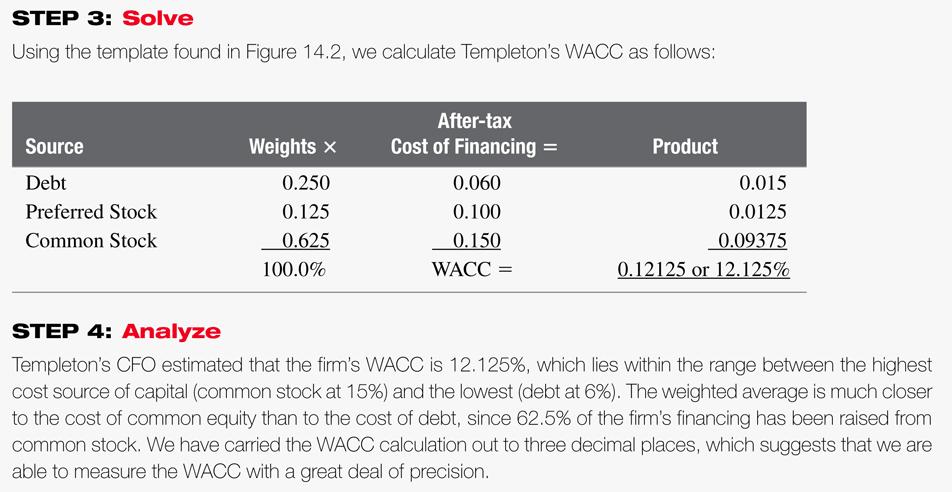

6 A Three-Step Procedure for Estimating Firm WACC 1. Define the firm s capital structure by determining the weight of each source of capital. 2. Estimate the opportunity cost of each source of financing. We will use the current market value of each source of capital based on its current, not historical, costs. 3. Calculate a weighted average of the costs of each source of financing.

7

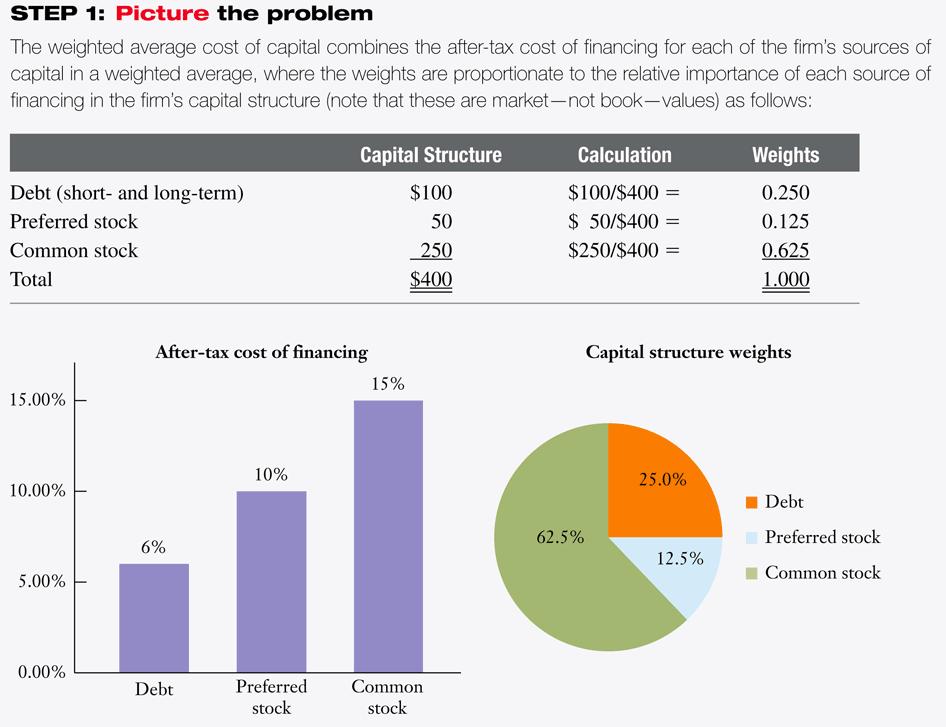

8 14.2 Determining the Firm s Capital Structure Weights The weights are based on the following sources of capital: debt (short-term and long-term), preferred stock, and common equity. Liabilities such as accounts payable and accrued expenses are not included in capital structure. Ideally, the weights should be based on observed market values. However, not all market values may be readily available. Hence, we generally use book values for debt and market values for equity.

9 Checkpoint 14.1 Calculating the WACC for Templeton Extended Care Facilities, Inc. In the spring of 2010, Templeton was considering the acquisition of a chain of extended care facilities and wanted to estimate its own WACC as a guide to the cost of capital for the acquisition. Templeton s capital structure consists of the following:

10 Checkpoint 14.1 Templeton contacted the firm s investment banker to get estimates of the firm s current cost of financing and was told that if the firm were to borrow the same amount of money today, it would have to pay lenders 8%; however, given the firm s 25% tax rate, the after-tax cost of borrowing would only be 6% = 8%(1-.25). Preferred stockholders currently demand a 10% rate of return, and common stockholders demand 15%. Templeton s CFO knew that the WACC would be somewhere between 6% and 15% since the firm s capital structure is a blend of the three sources of capital whose costs are bounded by this range.

11

12

13 Checkpoint 14.1: Check Yourself After completing her estimate of Templeton s WACC, the CFO decided to explore the possibility of adding more low-cost debt to the capital structure. With the help of the firm s investment banker, the CFO learned that Templeton could probably push its use of debt to 37.5% of the firm s capital structure by issuing more debt and retiring (purchasing) the firm s preferred shares. This could be done without increasing the firm s costs of borrowing or the required rate of return demanded by the firm s common stockholders. What is your estimate of the WACC for Templeton under this new capital structure proposal? WACC=w_cs k_cs + w_d k_d (1-T) =.625x15%+.375x6%=11.625%.

14 14.3 Estimating the Cost of Individual Sources of Capital The Cost of Debt The cost of debt is the rate of return the firm s lenders demand when they loan money to the firm. Note, the rate of return is not the same as coupon rate, which is the rate contractually set at the time of issue. We can estimate the market s required rate of return by examining the yield to maturity on the firm s debt. After-tax cost of debt = Yield (1-tax rate)

15 The Cost of Debt Example 14.1 What will be the yield to maturity on a debt that has par value of $1,000, a coupon interest rate of 5%, time to maturity of 10 years and is currently trading at $900? What will be the cost of debt if the tax rate is 30%? We can calculate yield to maturity of the bond using a financial calculator or excel: YTM=6.38%. After-tax cost of debt = YTM(1-Tax Rate)=6.38%(1-.3)=4.47%

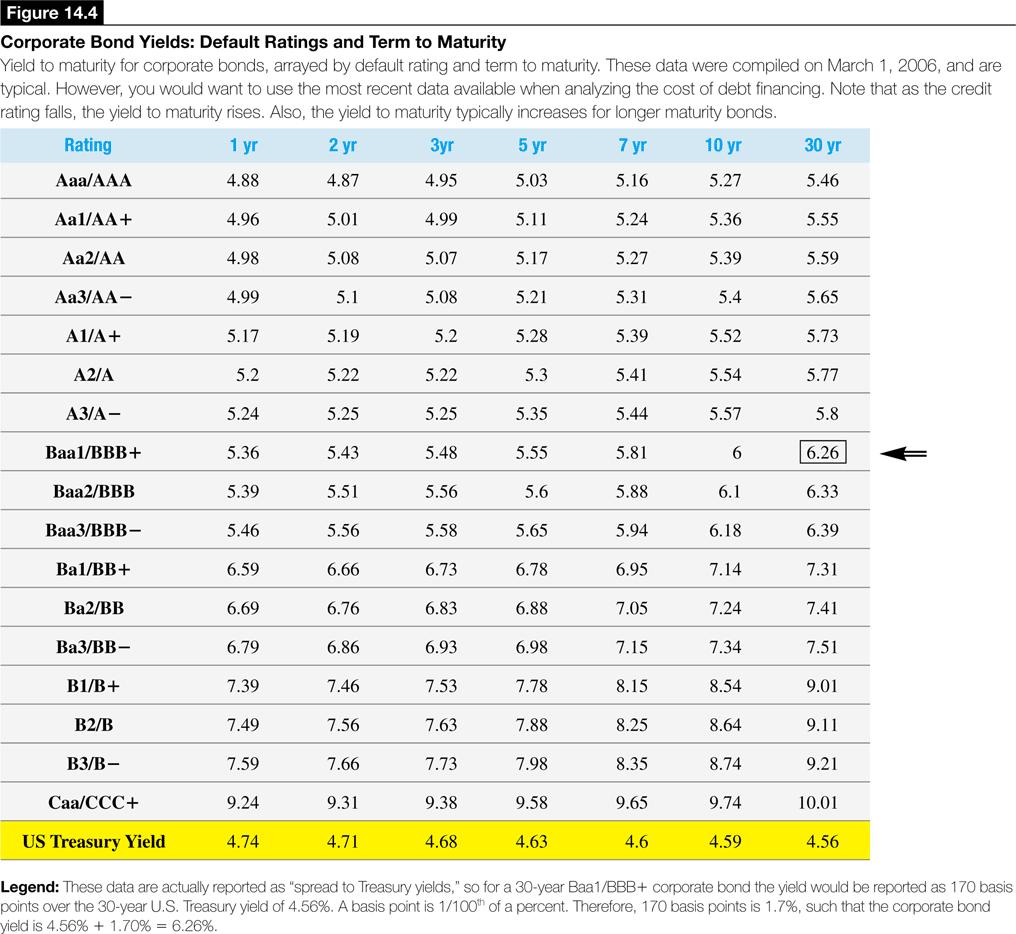

16 The Cost of Debt It is not easy to find the market price of a specific bond as most bonds do not trade in the public market. Because of this, it is a standard practice to estimate the cost of debt using the average yield to maturity on a portfolio of bonds with similar credit rating and maturity as the firm s outstanding debt. The average yield to maturity for a specific rating class varies over time. It can also differ across different industry groups.

17

18

19 The Cost of Preferred Equity The cost of preferred equity is the rate of return investors require of the firm when they purchase its preferred stock. The cost is not adjusted for taxes since dividends are paid to preferred stockholders out of after-tax income. The cost of preferred stock can be inferred from its trading price and the fixed dividend:

20 The Cost of Preferred Equity Example 14.2 Consider the preferred shares of Relay Company that are trading at $25 per share. What will be the cost of preferred equity if these stocks have a par value of $35 and pay annual dividend of 4%? Dividend =$35x4%=$1.4 Cost of preferred equity = Dividend/price=1.4/25=5.6%.

21 The Cost of Common Equity The cost of common equity is the rate of return investors expect to receive from investing in firm s stock. This return comes in the form of cash distributions of dividends and cash proceeds from the sale of the stock. Cost of common equity is harder to estimate since common stockholders do not have a contractually defined return similar to the interest on bonds or dividends on preferred stock. There are two approaches to estimating the cost of common equity: Dividend growth model (introduced in chapter 10) CAPM (introduced in chapter 8)

22 The Dividend Growth Model Discounted Cash Flow Approach Using this approach, we estimate the expected stream of dividends as the source of future estimated cash flows. We use the estimated dividends and current stock price to calculate the internal rate of return on the stock investment. This return is used as an estimate of cost of equity. Originally, we use the dividend growth model to estimate the stock value. Now we take the market price of the stock as the fair value, and learn what the discount rate (required rate of return) should be if the market price is the fair value.

23 The constant growth case If we assume that the dividend grows at a constant rate, g, the stock can be valued as where k cs is the cost of common equity or required rate of return on the equity and V cs is the fair value. If we set the market price to the fair value, P cs = V cs, we can infer the cost of common equity as, D/P is called the dividend yield (DY).

24 Checkpoint 14.2 Estimating the Cost of Common Equity for Pearson plc Using the Dividend Growth Model Pearson plc (PSO) is an international media company that operates three business groups: Pearson Education, the Financial Times, and Penguin. In the spring of 2009, Pearson s CFO called for an update of the firm s cost of capital. The first phase of the estimation focused on the firm s cost of common equity. How would the CFO determine the cost of the company s equity, using the dividend growth model? PSO stock is traded at $ The last dividend paid is $0.47 per share, and we expect a growth rate of 6.25%.

25 Checkpoint 14.2: Check Yourself Prepare two additional estimates of Pearson s cost of common equity using the dividend growth model where you use growth rates at 5% and 7.81%, respectively. 9.89%, 12.83%.

26 Estimating the Rate of Growth, g The growth rate can be obtained from various websites that post analysts forecasts of growth rates. We can also estimate the growth rate using the historical data and computing the arithmetic average or geometric average.

27 Estimating the Rate of Growth, g (cont.)

28 Pros and Cons of the Dividend Growth Model Approach While dividend growth model is easy to use, it is severely dependent upon the quality of growth rate estimates. Furthermore, not all firms pay dividends. Many times, the growth rate is estimated/forecasted on EPS instead of on dividends.

29 The Capital Asset Pricing Model CAPM was used in chapter 8 to determine the expected or required rate of return for risky investments. Cost of is determined by three key ingredients: The risk-free rate of interest, The beta or systematic risk of the common stock returns, and The market risk premium.

30 Pros & Cons the CAPM approach Pros 1. The model is simple to understand and use. 2. The model does not depend on dividends or growth rate. It can be applied to companies that do not currently pay dividends or are not expected to experience a constant rate of growth in dividends. Cons 1. CAPM does not offer any guidance on the appropriate choice for the risk-free rate. Risk-free rate may vary widely depending on the Treasury security chosen. 2. Estimates of beta can vary widely depending upon the market index and time period chosen. 3. Estimates of market risk premium will also vary depending on the time period and security chosen.

31 Checkpoint 14.3 Estimating the Cost of Common Equity for Pearson plc using the CAPM A review of current market conditions at the end of March 2009 reveals that the 10-year U.S. Treasury Bond yield that we will use to measure the risk-free rate was 2.81%, the estimated market risk premium is 6.5%, and the beta for Pearson s common stock is Determine Pearson s cost of common equity using the CAPM, as of March Cost of equity = Rf + Beta x Market risk premium =2.81% x6.5%=10.61%

32 Checkpoint 14.3: Check Yourself Prepare two additional estimates of Pearson s cost of common equity using the CAPM where you use the most extreme values of each of the three factors that drive the CAPM.

33 Checkpoint 14.3: Analysis CAPM describes the relationship between the expected rates of return on risky assets in terms of their systematic risk. Its value depends on: The risk-free rate of interest, The beta or systematic risk of the common stock returns, and The market risk premium. However, there can be wide variation in the estimates for each one of these variables. Here we are given the following estimates: The risk-free rate of interest (.03% or 3.73%) The beta or systematic risk of the common stock returns (1 or 1.5) The market risk premium (4% or 8%)

34 Checkpoint 14.3: Analysis The low-high range on the cost of equity: The low: k cs = 0.03% + 1(4%) = 4.03% The high: k cs = 3.73%+ 1.5(8%) = 15.73% Pearson s cost of equity is shown to be sensitive to the estimates used for risk-free rate of interest, beta and market risk premium. Based on the estimates used, the cost of common equity ranges from 4.03% to 15.73%.

35 14.4 Summing Up: Calculating the Firm s WACC The final step is to calculate the firm s overall cost of capital by taking the weighted average of the firm s financing mix that we evaluated in Steps One and Two. The following issues should be kept in mind: Determine weights based on market value rather than book value (if possible). Use market (current) costs rather than historical rates (such as coupon rates). Use forward looking weights and opportunity costs.

36 14.5 Estimating Project Cost of Capital Should the firm s WACC be used to evaluate all new investments? In theory, it is appropriate only if the risk of the new project is equal to the overall risk of the firm. This may generally not be the case necessitating the need for a unique cost of capital for each project. However, a recent survey found that more than 50% of the firms tend to use single, company-wide discount rate to evaluate all of their investment proposals. There are advantages and costs associated with estimating a unique discount rate for each project.

37 The Pros & Cons for Using Multiple Discount Rates Pros Multiple discount rates is consistent with finance theory that suggests that unique discount rate will reflect the unique risk of the investment. Cons It may be difficult to trace the source of financing for individual project since most firms raise money in bulk for all the projects. It adds to the time and cost in getting approval for new projects. Financing cost, in general, depends on the risk of firm (with the project included), not the risk of a specific project. If a firm fails on one project, it does not mean that the company will default on the debt used on that project. The equity holder has claims on the whole company, not just one particular project.

38 14.6 Floatation Costs Floatation costs are costs incurred by a firm when it raises money to finance new investments by selling bonds and stocks. For example, these costs may include fees paid to an investment banker, and costs incurred when securities are sold at a discount to the current market price. Because of floatation costs, the firm will have to raise more than the amount it needs.

39 Floatation Costs Example 14.3 If a firm needs $100 million to finance its new project and the floatation cost is expected to be 5.5%, how much should the firm raise by selling securities? Floating Cost Adjusted Money Need = $100 million (1-.055) = $ million The firm will raise $ million, which includes floatation cost of $5.82 million.

40 Checkpoint 14.4: Incorporating Floatation Costs into the Calculation of NPV The Tricon Telecom Company is considering a $100 million investment that would allow it to develop fiber optic high-speed Internet connectivity to its 2 million subscribers. The investment will be financed using the firm s desired mix of debt and equity with 40% debt financing and 60% common equity financing. The firm s investment banker advised the firm s CFO that the issue costs associated with debt would be 2% while the equity issue costs would be 10%. Tricon uses a 10% cost of capital to evaluate its telecom investments and has estimated that the new fiber optic project will yield future cash flows valued at $115 million. However, to this point no consideration has been given to the effect of the costs of raising the financing for the project or flotation costs. Should the firm go forward with the investment in light of the flotation costs?

41 Checkpoint 14.4: Floatation Costs and Project NPV Weighted average floatation cost: =40%(2%)+60%(10%)=6.8%. Floatation cost adjusted initial outlay =100/(1-6.8%)=107.3 million. Hence, floatation cost is 7.3 million. Project NPV: The present value of both cash inflows and cash outflows: =$ =7.70 million.

42 Checkpoint 14.4: Check Yourself Before Tricon could finalize the financing for the new project, stock market conditions changed such that new stock became more expensive to issue. In fact, floatation costs rose to 15% of new equity issued and the cost of debt rose to 3%. Is the project still viable (assuming the present value of future cash flows remain unchanged)? The project NPV will be equal to the present value of the future cash flows less the initial outlay and floatation costs. NPV = PV(inflows) (Floatation cost adjusted Initial outlay) = /(1-(.4*3%+.6*15%))= =$3.64 Floatation cost is million.

AGENDA LEARNING OBJECTIVES THE COST OF CAPITAL. Chapter 14. Learning Objectives Principles Used in This Chapter. financing.

Chapter 14 THE COST OF CAPITAL AGENDA Learning Objectives Principles Used in This Chapter 1. The Cost of Capital: An Overview 2. Determining the Firm s Capital Structure Weights 3. Estimating the Costs

Chapter 14 THE COST OF CAPITAL AGENDA Learning Objectives Principles Used in This Chapter 1. The Cost of Capital: An Overview 2. Determining the Firm s Capital Structure Weights 3. Estimating the Costs

The Cost of Capital. Principles Applied in This Chapter. The Cost of Capital: An Overview

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital. Chapter 14

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

2013, Study Session #11, Reading # 37 COST OF CAPITAL 1. INTRODUCTION

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

Cost of Capital. Chapter 15. Key Concepts and Skills. Cost of Capital

Chapter 5 Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how to determine a firm s cost of debt Know how to determine a firm s overall cost of capital Cost of Capital

Chapter 5 Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how to determine a firm s cost of debt Know how to determine a firm s overall cost of capital Cost of Capital

Chapter 14 The Cost of Capital

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Given the following information, what is the WACC for the following firm?

Chapter 1 Cost of Capital The required return for an asset is a function of the risk of the asset and the return to the investor is the same as the cost to the company. The firms cost of capital provides

Chapter 1 Cost of Capital The required return for an asset is a function of the risk of the asset and the return to the investor is the same as the cost to the company. The firms cost of capital provides

FIN Chapter 10. Stock Valuation. Liuren Wu

FIN 3000 Chapter 10 Stock Valuation Liuren Wu Overview 1. Common Stock Identify the basic characteristics and features of common stock and use the discounted cash flow model to value common shares. 2.

FIN 3000 Chapter 10 Stock Valuation Liuren Wu Overview 1. Common Stock Identify the basic characteristics and features of common stock and use the discounted cash flow model to value common shares. 2.

The Cost of Capital 1

The Cost of Capital 1 Learning Goals Sources of capital Cost of each type of funding Calculation of the weighted average cost of capital (WACC) Construction and use of the marginal cost of capital schedule

The Cost of Capital 1 Learning Goals Sources of capital Cost of each type of funding Calculation of the weighted average cost of capital (WACC) Construction and use of the marginal cost of capital schedule

Chapter 9 Debt Valuation and Interest Rates

Chapter 9 Debt Valuation and Interest Rates Slide Contents Learning Objectives Principles Used in This Chapter 1.Overview of Corporate Debt 2.Valuing Corporate Debt 3.Bond Valuation: Four Key Relationships

Chapter 9 Debt Valuation and Interest Rates Slide Contents Learning Objectives Principles Used in This Chapter 1.Overview of Corporate Debt 2.Valuing Corporate Debt 3.Bond Valuation: Four Key Relationships

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

COST OF CAPITAL CHAPTER LEARNING OUTCOMES

CHAPTER 4 COST OF CAPITAL r r r r LEARNING OUTCOMES Discuss the need and sources of finance to a business entity. Discuss the meaning of cost of capital for raising capital from different sources of finance.

CHAPTER 4 COST OF CAPITAL r r r r LEARNING OUTCOMES Discuss the need and sources of finance to a business entity. Discuss the meaning of cost of capital for raising capital from different sources of finance.

4. D Spread to treasuries. Spread to treasuries is a measure of a corporate bond s default risk.

www.liontutors.com FIN 301 Final Exam Practice Exam Solutions 1. C Fixed rate par value bond. A bond is sold at par when the coupon rate is equal to the market rate. 2. C As beta decreases, CAPM will decrease

www.liontutors.com FIN 301 Final Exam Practice Exam Solutions 1. C Fixed rate par value bond. A bond is sold at par when the coupon rate is equal to the market rate. 2. C As beta decreases, CAPM will decrease

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613. Business Finance Final Exam

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

( )/10 = 65/10 = 6.5 feet.

/10 = 65/10 = 6.5 feet.") Topic 5: Cost of Capital (Copyright 2018 Joseph W. Trefzger) Let s say we have a pile of wooden posts. Some of them are four feet each in length; the rest are nine feet long each. What is the average post

Topic 5: Cost of Capital (Copyright 2018 Joseph W. Trefzger) Let s say we have a pile of wooden posts. Some of them are four feet each in length; the rest are nine feet long each. What is the average post

Quiz Bomb. Page 1 of 12

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

Paper 3A: Cost Accounting Chapter 4 Unit-I. By: CA Kapileshwar Bhalla

Paper 3A: Cost Accounting Chapter 4 Unit-I By: CA Kapileshwar Bhalla Understand the concept of Cost of Capital that impacts the capital investments decisions for a business. Understand what are the different

Paper 3A: Cost Accounting Chapter 4 Unit-I By: CA Kapileshwar Bhalla Understand the concept of Cost of Capital that impacts the capital investments decisions for a business. Understand what are the different

FIN Chapter 8. Risk and Return: Capital Asset Pricing Model. Liuren Wu

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

Part A: Corporate Finance

Finance: Common Body of Knowledge Review Part A: Corporate Finance Time Value of Money Financial managers always want to determine how much a periodic receipt of future cash flow is worth in today s dollars.

Finance: Common Body of Knowledge Review Part A: Corporate Finance Time Value of Money Financial managers always want to determine how much a periodic receipt of future cash flow is worth in today s dollars.

Graded Project. Financial Management

Graded Project Financial Management OBJECTIVE 1 PURPOSE 1 SCORING GUIDELINES 11 Contents iii Financial Management OBJECTIVE Demonstrate the ability to perform financial calculations and analysis related

Graded Project Financial Management OBJECTIVE 1 PURPOSE 1 SCORING GUIDELINES 11 Contents iii Financial Management OBJECTIVE Demonstrate the ability to perform financial calculations and analysis related

Rate of Return. Finance Department Financial Analysis Division Public Utility Bureau

Rate of Return Finance Department Financial Analysis Division Public Utility Bureau Overview Rate of Return Cost of Short and Long-Term Debt Cost of Preferred Stock Cost of Common Equity Capital Asset

Rate of Return Finance Department Financial Analysis Division Public Utility Bureau Overview Rate of Return Cost of Short and Long-Term Debt Cost of Preferred Stock Cost of Common Equity Capital Asset

CHAPTER 19 RAISING CAPITAL

CHAPTER 19 RAISING CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. A company s internally generated cash flow provides a source of equity financing. For a profitable company, outside

CHAPTER 19 RAISING CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. A company s internally generated cash flow provides a source of equity financing. For a profitable company, outside

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 10 Raising Funds and Cost of Capital Concept Check 10.1 1. What are the three primary roles

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 10 Raising Funds and Cost of Capital Concept Check 10.1 1. What are the three primary roles

Analyzing Project Cash Flows. Principles Applied in This Chapter. Learning Objectives. Chapter 12. Principle 3: Cash Flows Are the Source of Value.

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. Learning Objectives 1. Identify

1. Why is it important for corporate managers to understand how bonds and shares are priced?

CHAPTER 4 CONCEPT REVIEW QUESTIONS 1. Why is it important for corporate managers to understand how bonds and shares are priced? Managers need to know this because (1) firms regularly issue stocks and bonds

CHAPTER 4 CONCEPT REVIEW QUESTIONS 1. Why is it important for corporate managers to understand how bonds and shares are priced? Managers need to know this because (1) firms regularly issue stocks and bonds

12. Cost of Capital. Outline

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

12. Cost of Capital 0 Outline The Cost of Capital: What is it? The Cost of Equity The Costs of Debt and Preferred Stock The Weighted Average Cost of Capital Economic Value Added 1 1 Required Return The

The Basics of Capital Budgeting

Chapter 11 The Basics of Capital Budgeting Should we build this plant? 11 1 What is capital budgeting? Analysis of potential additions to fixed assets. Long term decisions; involve large expenditures.

Chapter 11 The Basics of Capital Budgeting Should we build this plant? 11 1 What is capital budgeting? Analysis of potential additions to fixed assets. Long term decisions; involve large expenditures.

Valuation: Fundamental Analysis

Valuation: Fundamental Analysis Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Valuation: Fundamental Analysis Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

GLOBAL EDITION. Financial Management. Principles and Applications THIRTEENTH EDITION. Sheridan Titman Arthur J. Keown John D.

GLOBAL EDITION Financial Management Principles and Applications THIRTEENTH EDITION Sheridan Titman Arthur J. Keown John D. Martin The Pearson Series in Finance Berk/DeMarzo Corporate Finance* Corporate

GLOBAL EDITION Financial Management Principles and Applications THIRTEENTH EDITION Sheridan Titman Arthur J. Keown John D. Martin The Pearson Series in Finance Berk/DeMarzo Corporate Finance* Corporate

Financial Planning and Control. Semester: 1/2559

Financial Planning and Control Semester: 1/2559 Krisada Khruachalee Master of Science in Applied Statistics, Master of Science in Finance, Bachelor of Business Administration (Cum Laude), Finance and Banking

Financial Planning and Control Semester: 1/2559 Krisada Khruachalee Master of Science in Applied Statistics, Master of Science in Finance, Bachelor of Business Administration (Cum Laude), Finance and Banking

Chapter 12 Cost of Capital

Chapter 12 Cost of Capital 1. The return that shareholders require on their investment in the firm is called the: A) Dividend yield. B) Cost of equity. C) Capital gains yield. D) Cost of capital. E) Income

Chapter 12 Cost of Capital 1. The return that shareholders require on their investment in the firm is called the: A) Dividend yield. B) Cost of equity. C) Capital gains yield. D) Cost of capital. E) Income

Lecture Wise Questions of ACC501 By Virtualians.pk

Lecture Wise Questions of ACC501 By Virtualians.pk Lecture No.23 Zero Growth Stocks? Zero Growth Stocks are referred to those stocks in which companies are provided fixed or constant amount of dividend

Lecture Wise Questions of ACC501 By Virtualians.pk Lecture No.23 Zero Growth Stocks? Zero Growth Stocks are referred to those stocks in which companies are provided fixed or constant amount of dividend

INVESTING IN LONG-TERM ASSETS: CAPITAL BUDGETING

INVESTING IN LONG-TERM ASSETS: CAPITAL BUDGETING P A R T 4 10 11 12 13 The Cost of Capital The Basics of Capital Budgeting Cash Flow Estimation and Risk Analysis Real Options and Other Topics in Capital

INVESTING IN LONG-TERM ASSETS: CAPITAL BUDGETING P A R T 4 10 11 12 13 The Cost of Capital The Basics of Capital Budgeting Cash Flow Estimation and Risk Analysis Real Options and Other Topics in Capital

FINS2624: PORTFOLIO MANAGEMENT NOTES

FINS2624: PORTFOLIO MANAGEMENT NOTES UNIVERSITY OF NEW SOUTH WALES Chapter: Table of Contents TABLE OF CONTENTS Bond Pricing 3 Bonds 3 Arbitrage Pricing 3 YTM and Bond prices 4 Realized Compound Yield

FINS2624: PORTFOLIO MANAGEMENT NOTES UNIVERSITY OF NEW SOUTH WALES Chapter: Table of Contents TABLE OF CONTENTS Bond Pricing 3 Bonds 3 Arbitrage Pricing 3 YTM and Bond prices 4 Realized Compound Yield

Study Unit Cost of Equity, Debt and the WACC 133. Cost of Equity, Debt and the WACC

www.charteredgrindschool.com 133 Study Unit 12 Contents Page A. The Opportunity Cost of Equity Capital 135 B. The Opportunity Cost of Debt Capital 137 C. The Weighted Average Cost of Capital 137 134 www.charteredgrindschool.com

www.charteredgrindschool.com 133 Study Unit 12 Contents Page A. The Opportunity Cost of Equity Capital 135 B. The Opportunity Cost of Debt Capital 137 C. The Weighted Average Cost of Capital 137 134 www.charteredgrindschool.com

Financial Aspects. March 3, ECO 4934: Public Utilities Economics: International Infrastructure

Financial Aspects March 3, 2008 ECO 4934: Public Utilities Economics: International Infrastructure The importance of Financial data Regulators gather and study financial data to partially overcome the

Financial Aspects March 3, 2008 ECO 4934: Public Utilities Economics: International Infrastructure The importance of Financial data Regulators gather and study financial data to partially overcome the

The Cost of Capital

The Cost of Capital In previous classes, we discussed the important concept that the expected return on an investment should be a function of the market risk embedded in that investment the risk-return

The Cost of Capital In previous classes, we discussed the important concept that the expected return on an investment should be a function of the market risk embedded in that investment the risk-return

Module 5: Special Financing and Investment Decisions

Module 5: Special Financing and Investment Decisions Reading 5.1: Introduction to Project Financing Some projects are so large that it may be best to finance them as they are standalone operations. Projects

Module 5: Special Financing and Investment Decisions Reading 5.1: Introduction to Project Financing Some projects are so large that it may be best to finance them as they are standalone operations. Projects

Chapter 14 - Cost of Capital. Cost of Capital

Cost of Capital 1. A group of individuals got together and purchased all of the outstanding shares of common stock of DL Smith, Inc. What is the return that these individuals require on this investment

Cost of Capital 1. A group of individuals got together and purchased all of the outstanding shares of common stock of DL Smith, Inc. What is the return that these individuals require on this investment

CHAPTER 15 COST OF CAPITAL

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

Portfolio Project. Ashley Moss. MGMT 575 Financial Analysis II. 3 November Southwestern College Professional Studies

Running head: TOOLS 1 Portfolio Project Ashley Moss MGMT 575 Financial Analysis II 3 November 2012 Southwestern College Professional Studies TOOLS 2 Table of Contents 1. Valuation and Characteristics of

Running head: TOOLS 1 Portfolio Project Ashley Moss MGMT 575 Financial Analysis II 3 November 2012 Southwestern College Professional Studies TOOLS 2 Table of Contents 1. Valuation and Characteristics of

Chapter 13. Risk, Cost of Capital, and Valuation 13-0

Chapter 13 Risk, Cost of Capital, and Valuation 13-0 Key Concepts and Skills Know how to determine a firm s cost of equity capital Understand the impact of beta in determining the firm s cost of equity

Chapter 13 Risk, Cost of Capital, and Valuation 13-0 Key Concepts and Skills Know how to determine a firm s cost of equity capital Understand the impact of beta in determining the firm s cost of equity

CS- PROFESSIOANL- FINANCIAL MANAGEMENT COST OF CAPITAL

CS- PROFESSIOANL- FINANCIAL MANAGEMENT COST OF CAPITAL AUTHOR SPEAKS All business will require investment of capital. This capital comes with an expected price to pay. E.g. Equity shareholders expect dividend

CS- PROFESSIOANL- FINANCIAL MANAGEMENT COST OF CAPITAL AUTHOR SPEAKS All business will require investment of capital. This capital comes with an expected price to pay. E.g. Equity shareholders expect dividend

Essendon Manufacturing Company Limited

Essendon Manufacturing Company Limited Project Evaluation of New Die Casting Machine Dedicated to, Prof. Name of the student Year of the student 1 P a g e Contents Executive Summary... 3 Methodology...

Essendon Manufacturing Company Limited Project Evaluation of New Die Casting Machine Dedicated to, Prof. Name of the student Year of the student 1 P a g e Contents Executive Summary... 3 Methodology...

Chapter 14 Cost of Capital

Chapter 14 Cost of Capital Multiple Choice Questions 1. A group of individuals got together and purchased all of the outstanding shares of common stock of DL Smith, Inc. What is the return that these individuals

Chapter 14 Cost of Capital Multiple Choice Questions 1. A group of individuals got together and purchased all of the outstanding shares of common stock of DL Smith, Inc. What is the return that these individuals

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Capital Budgeting and Business Valuation

Capital Budgeting and Business Valuation Capital budgeting and business valuation concern two subjects near and dear to financial peoples hearts: What should we do with the firm s money and how much is

Capital Budgeting and Business Valuation Capital budgeting and business valuation concern two subjects near and dear to financial peoples hearts: What should we do with the firm s money and how much is

Stock valuation. Chapter 10

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

LECTURE 7 : CHAPTER 10 The Cost of Capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

LECTURE 7 : CHAPTER 10 The Cost of Capital Sources of capital Component costs WACC (Weighted Average Cost of Capital) Adjusting for flotation costs Adjusting for risk What sources of long-term capital

Understanding Financial Management: A Practical Guide Problems and Answers

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

] = [1 + (1 0.3)(10/70)] =

![] = [1 + (1 0.3)(10/70)] =](/thumbs/93/114475728.jpg "] = [1 + (1 0.3)(10/70)] =") 7.1. Sicily Pharmaceuticals has $10 million in debt and $70 million in equity. Its tax rate is 30%, cost of debt 8%, and beta 1.5. The riskless rate is 5% and the expected return on the market 12%. Sicily

7.1. Sicily Pharmaceuticals has $10 million in debt and $70 million in equity. Its tax rate is 30%, cost of debt 8%, and beta 1.5. The riskless rate is 5% and the expected return on the market 12%. Sicily

UWE has obtained warranties from all depositors as to their title in the material deposited and as to their right to deposit such material.

Tucker, J. (2009) How to set the hurdle rate for capital investments. In: Stauffer, D., ed. (2009) Qfinance: The Ultimate Resource. A & C Black, pp. 322-324. Available from: http://eprints.uwe.ac.uk/11334

Tucker, J. (2009) How to set the hurdle rate for capital investments. In: Stauffer, D., ed. (2009) Qfinance: The Ultimate Resource. A & C Black, pp. 322-324. Available from: http://eprints.uwe.ac.uk/11334

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting

Time Value of Money and Capital Budgeting") AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

Long-Term Financial Decisions

Part 4 Long-Term Financial Decisions Chapter 10 The Cost of Capital Chapter 11 Leverage and Capital Structure Chapter 12 Dividend Policy LG1 LG2 LG3 LG4 LG5 LG6 Chapter 10 The Cost of Capital LEARNING

Part 4 Long-Term Financial Decisions Chapter 10 The Cost of Capital Chapter 11 Leverage and Capital Structure Chapter 12 Dividend Policy LG1 LG2 LG3 LG4 LG5 LG6 Chapter 10 The Cost of Capital LEARNING

Key Concepts and Skills

Chapter 14 Cost of Capital McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how

Chapter 14 Cost of Capital McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how

80 Solved MCQs of MGT201 Financial Management By

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

80 Solved MCQs of MGT201 Financial Management By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

All In One MGT201 Mid Term Papers More Than (10) BY

BY") All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

Chapter 15. Topics in Chapter. Capital Structure Decisions

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Chapter 15 Capital Structure Decisions 1 Topics in Chapter Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Paper 2.7 Investment Management

CHARTERED INSTITUTE OF STOCKBROKERS September 2018 Specialised Certification Examination Paper 2.7 Investment Management 2 Question 2 - Portfolio Management 2a) An analyst gathered the following information

CHARTERED INSTITUTE OF STOCKBROKERS September 2018 Specialised Certification Examination Paper 2.7 Investment Management 2 Question 2 - Portfolio Management 2a) An analyst gathered the following information

Capital Structure Management

MBA III Semester Capital Structure Management POST RAJ POKHAREL M.Phil. (TU) 01/2010) 1 What is Capital Structure? Definition The capital structure of a firm is the mix of different securities issued

MBA III Semester Capital Structure Management POST RAJ POKHAREL M.Phil. (TU) 01/2010) 1 What is Capital Structure? Definition The capital structure of a firm is the mix of different securities issued

Chapter 12. Topics. Cost of Capital. The Cost of Capital

Chapter 12 The Cost of Capital Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC Measuring Capital Structure Required Rates of Return for individual types

Chapter 12 The Cost of Capital Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC Measuring Capital Structure Required Rates of Return for individual types

Forward and Futures Contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

Principals of Managerial Finance Spring 2017 FINAL EXAM VERSION B

FIN 301 Prof.Thistle Principals of Managerial Finance Spring 2017 FINAL EXAM VERSION B MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Schiller

FIN 301 Prof.Thistle Principals of Managerial Finance Spring 2017 FINAL EXAM VERSION B MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Schiller

Solved MCQs MGT201. (Group is not responsible for any solved content)

") Solved MCQs 2010 MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

Solved MCQs 2010 MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

600 Solved MCQs of MGT201 BY

600 Solved MCQs of MGT201 BY http://vustudents.ning.com Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

600 Solved MCQs of MGT201 BY http://vustudents.ning.com Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

Financial Strategy First Test

Financial Strategy First Test 1. The difference between the market value of an investment and its cost is the: A) Net present value. B) Internal rate of return. C) Payback period. D) Profitability index.

Financial Strategy First Test 1. The difference between the market value of an investment and its cost is the: A) Net present value. B) Internal rate of return. C) Payback period. D) Profitability index.

Gustafson Financial Information TAB You will find all the given data here

ACCT 2040 / FN 2040 Financial Management SLOA Problem Introduction Tab This financial planning project is split into several parts Each section has its own tab. Section Problem Introduction TAB This tab

ACCT 2040 / FN 2040 Financial Management SLOA Problem Introduction Tab This financial planning project is split into several parts Each section has its own tab. Section Problem Introduction TAB This tab

Principals of Managerial Finance Spring 2017 FINAL EXAM VERSION D

FIN 301 Prof.Thistle Principals of Managerial Finance Spring 2017 FINAL EXAM VERSION D MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Roddy Richards

FIN 301 Prof.Thistle Principals of Managerial Finance Spring 2017 FINAL EXAM VERSION D MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Roddy Richards

Lecture 20: Bond Portfolio Management. I. Reading. A. BKM, Chapter 16, Sections 16.1 and 16.2.

Lecture 20: Bond Portfolio Management. I. Reading. A. BKM, Chapter 16, Sections 16.1 and 16.2. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. 1. If an individual has a particular

Lecture 20: Bond Portfolio Management. I. Reading. A. BKM, Chapter 16, Sections 16.1 and 16.2. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. 1. If an individual has a particular

Session 2, Monday, April 3 rd (11:30-12:30)

") Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

PMBA 8135 Take Home Problem Set 3 Spring 2014

PMBA 8135 Take Home Problem Set 3 Spring 2014 Directions: Determine or compute an answer for each question/problem on this problem set. After you have computed an answer for every question, enter your

PMBA 8135 Take Home Problem Set 3 Spring 2014 Directions: Determine or compute an answer for each question/problem on this problem set. After you have computed an answer for every question, enter your

Chapter 12. Topics. Cost of Capital. The Cost of Capital

Chapter 12 The Cost of Capital 1 Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC McDonald s WACC estimation Measuring Capital Structure Required Rates

Chapter 12 The Cost of Capital 1 Topics Thinking through Frankenstein Co. s cost of capital Weighted Average Cost of Capital: WACC McDonald s WACC estimation Measuring Capital Structure Required Rates

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file Which group of ratios measures a firm's ability to meet short-term obligations? Liquidity ratios Debt ratios Coverage ratios Profitability

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file Which group of ratios measures a firm's ability to meet short-term obligations? Liquidity ratios Debt ratios Coverage ratios Profitability

Mid Term Papers. Spring 2009 (Session 02) MGT201. (Group is not responsible for any solved content)

MGT201. (Group is not responsible for any solved content)") Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

MGT201 Financial Management Solved MCQs

MGT201 Financial Management Solved MCQs Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because they have invested

MGT201 Financial Management Solved MCQs Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because they have invested

Question # 1 of 15 ( Start time: 01:53:35 PM ) Total Marks: 1

Total Marks: 1") MGT 201 - Financial Management (Quiz # 5) 380+ Quizzes solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Date Monday 31st January and Tuesday 1st February 2011 Question # 1 of 15 ( Start time: 01:53:35 PM

MGT 201 - Financial Management (Quiz # 5) 380+ Quizzes solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Date Monday 31st January and Tuesday 1st February 2011 Question # 1 of 15 ( Start time: 01:53:35 PM

Chapter 15 THE VALUATION OF SECURITIES THEORETICAL APPROACH

September-December 2016 Examinations ACCA F9 77 Chapter 15 THE VALUATION OF SECURITIES THEORETICAL APPROACH 1. Introduction In this chapter we will look at what, in theory, determines the market value

September-December 2016 Examinations ACCA F9 77 Chapter 15 THE VALUATION OF SECURITIES THEORETICAL APPROACH 1. Introduction In this chapter we will look at what, in theory, determines the market value

FINALTERM EXAMINATION Fall 2009 MGT201- Financial Management (Session - 3)

") FINALTERM EXAMINATION Fall 2009 MGT201- Financial Management (Session - 3) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one ABC s and XYZ s debt-to-total assets ratio is 0.4. What

FINALTERM EXAMINATION Fall 2009 MGT201- Financial Management (Session - 3) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one ABC s and XYZ s debt-to-total assets ratio is 0.4. What

Study Session 11 Corporate Finance

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

Basic Finance Exam #2

Basic Finance Exam #2 Chapter 10: Capital Budget list of planned investment project Sensitivity Analysis analysis of the effects on project profitability of changes in sales, costs and so on Fixed Cost

Basic Finance Exam #2 Chapter 10: Capital Budget list of planned investment project Sensitivity Analysis analysis of the effects on project profitability of changes in sales, costs and so on Fixed Cost

Sample Questions for Chapters 10 & 11

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Name: Class: Date: Sample Questions for Chapters 10 & 11 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Sacramento Paper is considering

Chapter 14 Capital Structure Decisions ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 14 Capital Structure Decisions ANSWERS TO END-OF-CHAPTER QUESTIONS 14-1 a. Capital structure is the manner in which a firm s assets are financed; that is, the righthand side of the balance sheet.

Chapter 14 Capital Structure Decisions ANSWERS TO END-OF-CHAPTER QUESTIONS 14-1 a. Capital structure is the manner in which a firm s assets are financed; that is, the righthand side of the balance sheet.

CA - FINAL SECURITY VALUATION. FCA, CFA L3 Candidate

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

The Hurdle Rate The minimum rate of return that must be met for a company to undertake a particular project

Risk, Return and Capital Budgeting The Hurdle Rate The minimum rate of return that must be met for a company to undertake a particular project The Weighted Average Cost of Capital (WACC) -The hurdle rate

Risk, Return and Capital Budgeting The Hurdle Rate The minimum rate of return that must be met for a company to undertake a particular project The Weighted Average Cost of Capital (WACC) -The hurdle rate

Chapter 10. Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common

Chapter 10 Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common Stock 3.Preferred Stock 4.The Stock Market 1. Identify the basic characteristics

Chapter 10 Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common Stock 3.Preferred Stock 4.The Stock Market 1. Identify the basic characteristics

Chapter 10: Capital Markets and the Pricing of Risk

Chapter 10: Capital Markets and the Pricing of Risk -1 Chapter 10: Capital Markets and the Pricing of Risk Fundamental question: What is the relationship between risk and return in a more complex world

Chapter 10: Capital Markets and the Pricing of Risk -1 Chapter 10: Capital Markets and the Pricing of Risk Fundamental question: What is the relationship between risk and return in a more complex world

DEBT VALUATION AND INTEREST. Chapter 9

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

FIN 571 Final Exam Guide (New) FOR MORE CLASSES VISIT

FOR MORE CLASSES VISIT") FIN 571 Final Exam Guide (New) 1.A proxy fight occurs when: the board of directors disagree on the members of the management team. 2. A stakeholder is any person or entity: 3.Which one of the following

FIN 571 Final Exam Guide (New) 1.A proxy fight occurs when: the board of directors disagree on the members of the management team. 2. A stakeholder is any person or entity: 3.Which one of the following

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Lecture 6 Cost of Capital

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

FIN622 Formulas

The quick ratio is defined as follows: Quick Ratio = (Current Assets Inventory)/ Current Liabilities Receivables Turnover = Annual Credit Sales / Accounts Receivable The collection period also can be written

The quick ratio is defined as follows: Quick Ratio = (Current Assets Inventory)/ Current Liabilities Receivables Turnover = Annual Credit Sales / Accounts Receivable The collection period also can be written

Chapter 9 Valuing Stocks

Chapter 9 Valuing Stocks Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 9.1 The Dividend Discount Model 9.2 Applying the Dividend Discount Model 9.3 Total Payout and Free Cash

Chapter 9 Valuing Stocks Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 9.1 The Dividend Discount Model 9.2 Applying the Dividend Discount Model 9.3 Total Payout and Free Cash

Solutions For all the benchmark Treasury securities shown below, compute the PVBP for $1 million

FIN 684 Professor Robert Hauswald Fixed-Income Analysis Kogod School of Business, AU Solutions 2 1. For all the benchmark Treasury securities shown below, compute the PVBP for $1 million par value. Explain

FIN 684 Professor Robert Hauswald Fixed-Income Analysis Kogod School of Business, AU Solutions 2 1. For all the benchmark Treasury securities shown below, compute the PVBP for $1 million par value. Explain

The Weighted-Average Cost of Capital and Company Valuation

The Weighted-Average Cost of Capital and Company Valuation Topics Covered Weighted Average Cost of Capital (WACC) Measuring Capital Structure Calculating Required Rates of Return Calculating WACC Interpreting

The Weighted-Average Cost of Capital and Company Valuation Topics Covered Weighted Average Cost of Capital (WACC) Measuring Capital Structure Calculating Required Rates of Return Calculating WACC Interpreting

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

ISSUES IN VALUATION UNDER FEMA

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value