Interest Rate Risk Managing Through The Uptick in Rates

|

|

|

- Mercy Gardner

- 5 years ago

- Views:

Transcription

1 Interest Rate Risk Managing Through The Uptick in Rates

2 Outline Asset Liability Management as Performance Management Sensitivity and the Sources of Risk History of Interest Rate Risk Management How to Effectively Manage Risk Six Questions The Difference between Planning and Risk Management The Importance of Stress Testing Unpacking your Risk Profile Focusing on Non Maturity Deposits

3 ALM as Performance Management Coordinated Management of a Bank s Entire Balance Sheet Deliver a High Return for Shareholders while Managing and Understanding Risk Interest Rate Risk Liquidity Risk Credit Risk (in terms of cash flow or financial risk)

4 ALM as Performance Management Managing Net Interest Margin at the Margin Incremental Production What was produced this month? Who did it? Was it a good thing or a bad thing? What was the incremental ROA/ROE? What went away this month what did it cost us?

5 ALM as Performance Management Managing Net Interest Margin at the Margin The Key is Funds Transfer Pricing Marginal Profitability How do the incremental decisions affect Product Profitability Organizational Profitability What went away this month what did it cost us? The Impact on the Efficiency Ratio The Result is a Higher Return for Shareholders

6 What is Sensitivity The degree to which changes in: interest rates, foreign exchange rates, commodity prices, or equity prices can adversely affect a financial institution s earnings or economic capital.

7 Primary Sources of Risk The primary source of market risk arises from the projected cash flows of loans, investments, deposits and borrowings. In some cases off-balance sheet items are critical.

8 Critical Considerations Management s ability to identify, measure, monitor, and control market risk; The institution s size; the nature and complexity of its activities; and The adequacy of its capital and earnings in relation to its level of market risk exposure.

9 How the Regulators Classify You RATING RESULT GREAT JOB! Everything is under control. There is not a lot of risk and management knows what it is doing. OK, I SUPPOSE. Risk is adequately under control. A slight chance that you can be hurt ( adversely affected ). Management understanding is adequate but not great. Earnings and capital possibly might not support your level of risk. NEEDS IMPROVEMENT! Get some help management practices are not adequate. There is a good chance that you are going be hurt ( adversely affected). Earnings and capital might not support your level of risk. UNACCEPTABLE! Being adversely affected is pretty much a sure thing. Management doesn t understand. Earnings and capital are not sufficient to support the lack of understanding. 5 UH OH! REALLY UNACCEPTABLE! Market risk is an imminent threat to viability. Management is less knowledgeable that 4. Earnings and capital wholly inadequate!

10

11 Regression Line with Confidence Bands

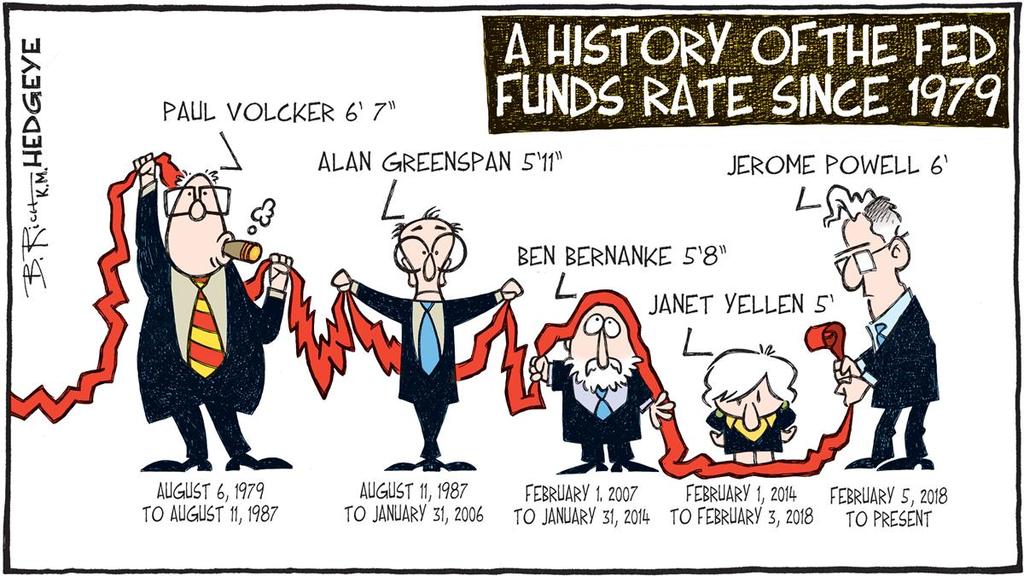

12 Proposed Nobel Prize Winning Analysis Regression Equation Results: Average Fed Funds =.60453*Height of the Fed Chair R-Square = (not great ) P-Value <.0001 (not bad) Prediction: Average Fed Funds Rate for Jay Powell s Tenure = %

13 The History of IRR January was Pivotal FFIEC Issues an Advisory on Interest Rate Risk Interest Rate Risk Prior to the Advisory IRR, so what, who cares? After the advisory, You better care, OR ELSE!

14 What did the FFIEC Advisory Say Material weakness in risk management processes or high levels of IRR exposure relative to capital will require corrective action. Such actions could include recommendations or directives to: Raise additional capital Reduce levels of IRR exposure Strengthen IRR management expertise Improve IRR management information and measurement systems

15 What did the FFIEC Say Before 2010 Joint Agency Policy Statement: Interest Rate Risk (1996) Banks that are found to have high levels of exposure and/or weak management practices will be directed by the agencies to take corrective action. Such actions will include directives to: Raise additional capital, Strengthen management expertise, Improve management information systems, Reduce levels of exposure, or a combination thereof.

16 What Changed in 2010 In Principle Nothing Practically Speaking Everything Now the Board and Management have to: Understand IRR The Concern of the Regulators is: Capital - EVE

17 What Changed in FAQ In Principle Nothing Specific guidance on: Model validation, Model assumptions, Levels of Stress and time horizons to consider Clear attempt to resolve problem areas many banks were facing in implementing IRR analysis and modeling.

18 What Changed in FIL In Principle Nothing Clear instruction to reemphasize the importance of IRR management program in light of challenging IRR environment (read, since rates are about to go up.) Directly addressed risk of securities valuation deterioration, and the impact of unrealized losses Clear reminder to Board, of its oversight responsibilities

19 Understanding & Managing Risk Six Key Questions 1. What is my risk? 2. What is causing my risk? 3. What material assumptions I am making? 4. Where did I get those assumptions? 5. What happens if I am wrong about those assumptions? 6. What is my plan if I am wrong?

20 A Key Distinction Risk vs. Planning What is Planning? What I think is going to happen. What I want to happen. What I hope will happen. What better happen if I want to keep my job!

21 A Key Distinction Risk vs. Planning What is Risk? What happens if I am wrong? What causes me to blow up? When does my institution collapse?

22 You have to do both. Plan Manage Risk A Key Distinction Risk vs. Planning Planning is Educated Guessing Risk Management is Stress Testing your Guessing

23 Stress vs. Guess What does the Advisory say about Stress Testing? Stress Testing should include a sensitivity analysis to help determine which assumptions have the most influence on model output can be used to determine the conditions under which key business assumptions and model parameters break down

24 Stress vs. Guess Stress Testing is the Heart of Risk Management Stress Testing Answers the Three Questions What happens if I am wrong? What causes me to blow up? When does my institution collapse?

25 How Do You Stress Test? There are Two Ingredients in every Risk Model Facts Assumptions

26 How Do You Stress Test? What are the Facts? Balance Sheet and Market Facts Contractual Facts Balance Rate Repricing characteristics Payment characteristics, etc.

27 How Do You Stress Test? What are the Assumptions? Things that are made up Rate scenarios Discount rates Non maturity deposit behavior Prepayments

28 How Do You Stress Test? Assumptions: Are elements of the Planning Process because they are made up This means your Risk Profile is NOT a Scientific Fact Your Risk Profile is a Belief System

29 How Do You Stress Test? Determine which Assumptions are Most Critical Stress Test Critical Assumptions

30 What do Regulators Want? Management and the Board should be able to: Understand and Explain your Risk

31 What do You Want? The Regulators to go away If you want them to go away, see previous slide.

32 What Should You Do? Demonstrate you Understand Cooperate and Graduate

33 Unpacking Your Risk EVE Volatility All Assumptions

34 Unpacking Your Risk EVE Volatility Removing Options

35 Unpacking Your Risk EVE Volatility Removing Prepayments

36 Unpacking Your Risk EVE Volatility - Removing NMD Assumptions

37 Unpacking Your Risk The analysis identifies Non Maturity Deposit assumptions as the MOST critical. Regulators are also VERY concerned about these You may be extremely liability sensitive and not asset sensitive Rising rates will significantly hurt you

38 What do the Regulators Require? Non Maturity Deposit Studies Regulators want to make sure: Your assumptions have historical validity Based on your history, not someone else s

39 What is Included in an NMD Study? A Non Maturity Deposit Study should include: Estimates of Decay Terms Estimates of Betas

40 How do You Estimate Decay Terms? A Non Maturity Deposit Study should include: Estimates of decay terms using multiple methodologies: Average Life Accounts Closed Balance Decay or Declining Balances Decay analysis should track the behavior of individual accounts through time

41 Non Maturity Deposit Decay Terms

42 What is a Beta? More IRR Jargon! An estimate of how much you will change your NMD rates when market rates rise or fall. If the Fed raises rates 100 bps, how much will your Money Market rates go up? 50% of the change (a 50% beta)? 75% of the change (a 75% beta)?

43 How do You Estimate Betas? Use Statistics! Perform a regression analysis. Analyze your deposit rates as a function of several market indices (Fed Funds, Libor Rates etc.) Determine which index is the best predictor Statistically it is the slope of the line through the data points

44 Non Maturity Deposit Betas Money Market Rates vs. 1-Year Swap Rate Money Market rates go up/down about 55 bps for every 100 bp change in 1-Year Swap rates

45 What else Does an NMD Study Measure? Surge Balances! Have balances moved from time deposits into non maturity deposits will those balances move back? Has the average balance per account grown significantly over time will that money leave the bank?

46 What are the Regulators Worried About? Surge Deposits Change in Balance Sheet Mix

47 What are the Regulators Worried About? Surge Deposits Change in Average Balance per Account

48 What Next? After you have gone through the trouble of doing an NMD study Don t believe the results! After all they are still just assumptions Stress test your assumptions.

49 Non Maturity Deposit Stress Test

50 Conclusion The most important question: Why?

51 Contact Information Phone: (770)

ALM Process & Strategies

ALM Process & Strategies Requirements for a Solid Foundation Chad McKeithen, Managing Director Duncan-Williams Inc. Al Forrester, CEO FiCast Data Corp Outline History of Interest Rate Risk Management How

ALM Process & Strategies Requirements for a Solid Foundation Chad McKeithen, Managing Director Duncan-Williams Inc. Al Forrester, CEO FiCast Data Corp Outline History of Interest Rate Risk Management How

Your State Association Presents. Interest Rate Risk: What Does th Future Hold? Program Materials

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply Conference Call will begin at 10:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 920 722 897 # You can also

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply Conference Call will begin at 10:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 920 722 897 # You can also

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

Developing Deposit Strategies for Rising Rates Session 1. Agenda

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

What is a Dynamic ALCO

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Core Deposit Analytics Session 1

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Market and Liquidity Risk Assessment Overview. Federal Reserve System

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Measuring Your IRR Profile Against Peers & Regulatory Targets. February 26, 2015 Webinar

Measuring Your IRR Profile Against Peers & Regulatory Targets February 26, 2015 Webinar. PRESENTERS Tom Hauck joined Austin Associates in 1991. He works with financial institutions around the country in

Measuring Your IRR Profile Against Peers & Regulatory Targets February 26, 2015 Webinar. PRESENTERS Tom Hauck joined Austin Associates in 1991. He works with financial institutions around the country in

Revised Interest Rate Risk Supervision Effective January 1, 2017

Revised Interest Rate Risk Supervision Effective January 1, 2017 Key Changes to NCUA s interest rate risk supervision: 1. Development of Interest Rate Risk Review Procedures Workbook 2. Updated IRR tolerance

Revised Interest Rate Risk Supervision Effective January 1, 2017 Key Changes to NCUA s interest rate risk supervision: 1. Development of Interest Rate Risk Review Procedures Workbook 2. Updated IRR tolerance

Deposit Pricing in Rising Rates Session 1. Three Part Series

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Developing a Funding Strategy for Rising Rates. Agenda

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Core Deposit Analytics Session 2: Beyond Basics - Applying Results

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

MAKING LIQUIDITY YOUR NEW BEST FRIEND

FHLB INDIANAPOLIS MAKING LIQUIDITY YOUR NEW BEST FRIEND David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Friends vs. Best Friends 2 3 Types of Friendship 1. Friendship of

FHLB INDIANAPOLIS MAKING LIQUIDITY YOUR NEW BEST FRIEND David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Friends vs. Best Friends 2 3 Types of Friendship 1. Friendship of

Deposit Pricing in Rising Rates Session 1. Three Part Series

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Effective Process Deposit Analysis Tools Betas Decay Rates

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Effective Process Deposit Analysis Tools Betas Decay Rates

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

Southeast Bankers Outreach Forum

Southeast Bankers Outreach Forum IRR in a Protracted Low Rate Environment Date: September 30, 2014 Presented by: Trent Cowsert Director of Capital Markets The opinions expressed are those of the presenter

Southeast Bankers Outreach Forum IRR in a Protracted Low Rate Environment Date: September 30, 2014 Presented by: Trent Cowsert Director of Capital Markets The opinions expressed are those of the presenter

Interagency Advisory on Interest Rate Risk Management

Interagency Management As part of our continued efforts to help our clients navigate through these volatile times, we recently sent out the attached checklist that briefly describes how c. myers helps

Interagency Management As part of our continued efforts to help our clients navigate through these volatile times, we recently sent out the attached checklist that briefly describes how c. myers helps

Interest Rate Risk Measurement

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

Lectures 13 and 14: Fixed Exchange Rates

Christiano 362, Winter 2003 February 21 Lectures 13 and 14: Fixed Exchange Rates 1. Fixed versus flexible exchange rates: overview. Over time, and in different places, countries have adopted a fixed exchange

Christiano 362, Winter 2003 February 21 Lectures 13 and 14: Fixed Exchange Rates 1. Fixed versus flexible exchange rates: overview. Over time, and in different places, countries have adopted a fixed exchange

Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08)

NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08)") Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08) Dan Frilot Senior Vice President Balance Sheet Solutions, LLC Background Balance Sheet

Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08) Dan Frilot Senior Vice President Balance Sheet Solutions, LLC Background Balance Sheet

NCUA Regulatory Update on ALM

Peter Jensen, Regional Capital Markets Specialist NCUA, Region 4, Division of Special Actions NCUA Regulatory Update on ALM University for Credit Unions September 23, 2014 Agenda Introduction Interest

Peter Jensen, Regional Capital Markets Specialist NCUA, Region 4, Division of Special Actions NCUA Regulatory Update on ALM University for Credit Unions September 23, 2014 Agenda Introduction Interest

Interest Rate Risk. Asset Liability Management. Asset Liability Management. Interest Rate Risk. Risk-Return Tradeoff. ALM Policy and Procedures

Interest Rate Risk Asset Liability Management The potential significant changes in a bank s profitability and market value of equity due to unexpected changes in interest rates Reinvestment rate risk Interest

Interest Rate Risk Asset Liability Management The potential significant changes in a bank s profitability and market value of equity due to unexpected changes in interest rates Reinvestment rate risk Interest

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

Understanding Interest Rate Risk is Not a Static Issue By c. myers corporation

c.notes www.cmyers.com Understanding Interest Rate Risk is Not a Static Issue By c. myers corporation It is clear that effective interest rate risk management (IRR) is at the top of NCUA s priority list.

c.notes www.cmyers.com Understanding Interest Rate Risk is Not a Static Issue By c. myers corporation It is clear that effective interest rate risk management (IRR) is at the top of NCUA s priority list.

Leading Practices. Non-Maturity Deposit Modeling: June 26, :45 AM 12:45 PM. Presented by:

Non-Maturity Deposit Modeling: Leading Practices June 26, 2017 11:45 AM 12:45 PM Presented by: Thomas E Bowers, CFA Managing Director ZM Financial Systems, Inc. 1020 Southhill Drive, Ste. 200 Cary, North

Non-Maturity Deposit Modeling: Leading Practices June 26, 2017 11:45 AM 12:45 PM Presented by: Thomas E Bowers, CFA Managing Director ZM Financial Systems, Inc. 1020 Southhill Drive, Ste. 200 Cary, North

Liquidity Basics Measuring and Managing Liquidity

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Mind Your Own Business

Mind Your Own Business In this article we are going to discuss the Big Picture and what the Bottom Line on your Balance Sheet, Income Statement and Cash Flow Statement tell you. I am sure you have heard

Mind Your Own Business In this article we are going to discuss the Big Picture and what the Bottom Line on your Balance Sheet, Income Statement and Cash Flow Statement tell you. I am sure you have heard

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017 by Alpha-Numeric Consulting, LLC December 20, 2017 Introduction Financial institutions recognize the need for accurate

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017 by Alpha-Numeric Consulting, LLC December 20, 2017 Introduction Financial institutions recognize the need for accurate

Introduction to Asset/Liability Management

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

ASSET/LIABILITY MANAGEMENT - YEAR 2

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

Aaron Campbell Thank you very much. Glad to be here.

Folks, retirement comes faster than you think. You may be listening now; you re already in retirement, but it s never too late or too early to start planning for retirement. So I d thought it d be good

Folks, retirement comes faster than you think. You may be listening now; you re already in retirement, but it s never too late or too early to start planning for retirement. So I d thought it d be good

Monthly Treasurers Tasks

As a club treasurer, you ll have certain tasks you ll be performing each month to keep your clubs financial records. In tonights presentation, we ll cover the basics of how you should perform these. Monthly

As a club treasurer, you ll have certain tasks you ll be performing each month to keep your clubs financial records. In tonights presentation, we ll cover the basics of how you should perform these. Monthly

HPM Module_7_Financial_Ratio_Analysis

HPM Module_7_Financial_Ratio_Analysis Hi, class, welcome to this tutorial. We're going to be doing income statement, conditional analysis, and ratio analysis. And the problem that we're going to be working

HPM Module_7_Financial_Ratio_Analysis Hi, class, welcome to this tutorial. We're going to be doing income statement, conditional analysis, and ratio analysis. And the problem that we're going to be working

Interest Rate Risk in the Banking Book. Taking a close look at the latest IRRBB developments

Interest Rate Risk in the Banking Book Taking a close look at the latest IRRBB developments Interest Rate Risk in the Banking Book Interest rate risk in the banking book (IRRBB) can be a significant risk

Interest Rate Risk in the Banking Book Taking a close look at the latest IRRBB developments Interest Rate Risk in the Banking Book Interest rate risk in the banking book (IRRBB) can be a significant risk

Weathering the Storm: Rates, Recession, and Risk

Weathering the Storm: Rates, Recession, and Risk Presenters: Charles McQueen Ed Lis Greg Gibson President VP of Finance & Compliance Chief Financial Officer McQueen Financial Adv. First Choice Financial

Weathering the Storm: Rates, Recession, and Risk Presenters: Charles McQueen Ed Lis Greg Gibson President VP of Finance & Compliance Chief Financial Officer McQueen Financial Adv. First Choice Financial

Georgia Banking School

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

Private Information I

Private Information I Private information and the bid-ask spread Readings (links active from NYU IP addresses) STPP Chapter 10 Bagehot, W., 1971. The Only Game in Town. Financial Analysts Journal 27, no.

Private Information I Private information and the bid-ask spread Readings (links active from NYU IP addresses) STPP Chapter 10 Bagehot, W., 1971. The Only Game in Town. Financial Analysts Journal 27, no.

Strategic And Tactical ALM In A Commercial Bank. Suresh Sankaran

Strategic And Tactical ALM In A Commercial Bank Suresh Sankaran Back To Basics Risks And Economics In a strict sense, there wasn t any risk if the world had behaved as it did in the past - Merton miller,

Strategic And Tactical ALM In A Commercial Bank Suresh Sankaran Back To Basics Risks And Economics In a strict sense, there wasn t any risk if the world had behaved as it did in the past - Merton miller,

Lecture Materials Topic 3 Yield Curves and Interest Forecasts ECONOMICS, MONEY MARKETS AND BANKING

Lecture Materials Topic 3 Yield Curves and Interest Forecasts ECONOMICS, MONEY MARKETS AND BANKING Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com

Lecture Materials Topic 3 Yield Curves and Interest Forecasts ECONOMICS, MONEY MARKETS AND BANKING Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com

Chapter 16. Random Variables. Copyright 2010 Pearson Education, Inc.

Chapter 16 Random Variables Copyright 2010 Pearson Education, Inc. Expected Value: Center A random variable assumes a value based on the outcome of a random event. We use a capital letter, like X, to denote

Chapter 16 Random Variables Copyright 2010 Pearson Education, Inc. Expected Value: Center A random variable assumes a value based on the outcome of a random event. We use a capital letter, like X, to denote

Financial planning. Kirt C. Butler Department of Finance Broad College of Business Michigan State University February 3, 2015

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

Financial planning Making financial decisions How will things change if I take this action? Financial decision modeling A framework for decision-making What-ifs - breakeven, sensitivities, & scenarios,

CECL: YOU RE GOING TO NEED A BETTER ALM MODEL Z-CONCEPTS

CECL: YOU RE GOING TO NEED A BETTER ALM MODEL The new Allowance for Loan and Lease Losses standard (called CECL) reminds me of the scene from Jaws, where, after first trying to capture the monstrous shark,

CECL: YOU RE GOING TO NEED A BETTER ALM MODEL The new Allowance for Loan and Lease Losses standard (called CECL) reminds me of the scene from Jaws, where, after first trying to capture the monstrous shark,

2

1 2 3 4 5 6 7 8 The Changing Deposit / Funding Landscape 2018 Promontory Interfinancial Network, LLC The Market Is Changing Funding pressures knocking at community bank doors S&P Global Market Intelligence,

1 2 3 4 5 6 7 8 The Changing Deposit / Funding Landscape 2018 Promontory Interfinancial Network, LLC The Market Is Changing Funding pressures knocking at community bank doors S&P Global Market Intelligence,

Financial Institutions

Unofficial Translation This translation is for the convenience of those unfamiliar with the Thai language Please refer to Thai text for the official version -------------------------------------- Notification

Unofficial Translation This translation is for the convenience of those unfamiliar with the Thai language Please refer to Thai text for the official version -------------------------------------- Notification

Financial Literacy Mastery

Financial Literacy Mastery Presented by Eileen Iles Colette Wagner Crowe Horwath LLP Session Objectives Satisfy your NCUA financial literacy requirement by taking your knowledge of financial statements

Financial Literacy Mastery Presented by Eileen Iles Colette Wagner Crowe Horwath LLP Session Objectives Satisfy your NCUA financial literacy requirement by taking your knowledge of financial statements

ASSET/LIABILITY MANAGEMENT - YEAR 2

ASSET/LIABILITY MANAGEMENT - YEAR 2 Interest Rate Risk Measurement & Management Raleigh A. Trovillion Executive Vice President UMB Bank Investment Division St. Louis, MO raleigh.trovillion@umb.com 314-612-8039

ASSET/LIABILITY MANAGEMENT - YEAR 2 Interest Rate Risk Measurement & Management Raleigh A. Trovillion Executive Vice President UMB Bank Investment Division St. Louis, MO raleigh.trovillion@umb.com 314-612-8039

Loan Pricing Structure and the Nature of Interest Rates

Loan Pricing Structure and the Nature of Interest Rates S. Blake Scharlach Senior Vice President / Director of Capital Markets Sales TIB- The Independent BankersBank, N.A. S. Blake Scharlach Blake joined

Loan Pricing Structure and the Nature of Interest Rates S. Blake Scharlach Senior Vice President / Director of Capital Markets Sales TIB- The Independent BankersBank, N.A. S. Blake Scharlach Blake joined

What Is Asset/Liability Management?

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT Scott J. Hopf, CPA Senior Manager BKD, LLP 375 North Shore Drive, Suite 501 Pittsburgh, PA 15212 shopf@bkd.com 412.364.9395 AGENDA The Basics

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT Scott J. Hopf, CPA Senior Manager BKD, LLP 375 North Shore Drive, Suite 501 Pittsburgh, PA 15212 shopf@bkd.com 412.364.9395 AGENDA The Basics

CREDIT UNION INVESTMENT PRICE RISK

A CU*ANSWERS/CALLAHAN & ASSOCIATES WHITEPAPER OCTOBER 24, 2013 CREDIT UNION INVESTMENT PRICE RISK Jim Vilker Patrick Sickels and Chip Filson Expect NCUA and state examiners to stress credit union investment

A CU*ANSWERS/CALLAHAN & ASSOCIATES WHITEPAPER OCTOBER 24, 2013 CREDIT UNION INVESTMENT PRICE RISK Jim Vilker Patrick Sickels and Chip Filson Expect NCUA and state examiners to stress credit union investment

Three Reasons Why The Fed Should Not Worry Too Much About Inflation Now

Three Reasons Why The Fed Should Not Worry Too Much About Inflation Now William T. Dickens Northeastern University and The Brookings Institution Peterson Institute for International Economics conference

Three Reasons Why The Fed Should Not Worry Too Much About Inflation Now William T. Dickens Northeastern University and The Brookings Institution Peterson Institute for International Economics conference

Loan Pricing Deals & Relationships Session 1. Agenda

Loan Pricing Deals & Relationships Session 1 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Loan Pricing Deals & Relationships Session 1 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Jeremy Siegel s 2016 Forecast for Stocks

Jeremy Siegel s 2016 Forecast for Stocks December 7, 2015 by Robert Huebscher Jeremy Siegel is the Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania and a senior

Jeremy Siegel s 2016 Forecast for Stocks December 7, 2015 by Robert Huebscher Jeremy Siegel is the Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania and a senior

Core Deposit Analytics Session 1: Determining Core The Basics

Core Deposit Analytics Session 1: Determining Core The Basics Thomas A. Farin Chairman of the Board tfarin@farin.com 1 Building Blocks for Deposit Analysis Pricing Betas Decay Rates Surge Balance Identification

Core Deposit Analytics Session 1: Determining Core The Basics Thomas A. Farin Chairman of the Board tfarin@farin.com 1 Building Blocks for Deposit Analysis Pricing Betas Decay Rates Surge Balance Identification

4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT!

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: 4 Big Reasons You Can t Afford To Ignore Business Credit Copyright 2012 All rights reserved. No part of

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: 4 Big Reasons You Can t Afford To Ignore Business Credit Copyright 2012 All rights reserved. No part of

Loan Pricing Deals/Relationships Session 2. Agenda

Loan Pricing Deals/Relationships Session 2 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Loan Pricing Deals/Relationships Session 2 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 Raleigh A. Andy Trovillion Executive Vice President UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com 800-433-5962 August 1, 2017 INTEREST RATE

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 Raleigh A. Andy Trovillion Executive Vice President UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com 800-433-5962 August 1, 2017 INTEREST RATE

Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Objectives. NCUA Interest Rate Risk Supervision

NCUA Interest Rate Supervision Lisa Boylen Senior ALM Analyst March 21, 2017 Objectives Understand NCUA s Revised Exam Procedures For Interest Rate Understand Exam Scope and Ratings Help You Prepare For

NCUA Interest Rate Supervision Lisa Boylen Senior ALM Analyst March 21, 2017 Objectives Understand NCUA s Revised Exam Procedures For Interest Rate Understand Exam Scope and Ratings Help You Prepare For

The Provision for Credit Losses & the Allowance for Loan Losses. How Much Do You Expect to Lose?

The Provision for Credit Losses & the Allowance for Loan Losses How Much Do You Expect to Lose? This Lesson: VERY Specific to Banks This is about a key accounting topic for banks and financial institutions.

The Provision for Credit Losses & the Allowance for Loan Losses How Much Do You Expect to Lose? This Lesson: VERY Specific to Banks This is about a key accounting topic for banks and financial institutions.

CREDIT AGRICOLE s response to the proposed changes to the regulatory capital treatment and supervision of IRRBB

CREDIT AGRICOLE s response to the proposed changes to the regulatory capital treatment and supervision of IRRBB BCBS s Consultation Paper, 11 th September 2015 CREDIT AGRICOLE is a mutual banking group

CREDIT AGRICOLE s response to the proposed changes to the regulatory capital treatment and supervision of IRRBB BCBS s Consultation Paper, 11 th September 2015 CREDIT AGRICOLE is a mutual banking group

That means the average cost for just one four-year degree will be $132,000

With the cost of tuition constantly going up these days, it is a rarity that I speak to a recent graduate who is not in student loan debt of some kind. In fact, the most recent statistics show that over

With the cost of tuition constantly going up these days, it is a rarity that I speak to a recent graduate who is not in student loan debt of some kind. In fact, the most recent statistics show that over

Optimal Taxation : (c) Optimal Income Taxation

Optimal Income Taxation") Optimal Taxation : (c) Optimal Income Taxation Optimal income taxation is quite a different problem than optimal commodity taxation. In optimal commodity taxation the issue was which commodities to tax,

Optimal Taxation : (c) Optimal Income Taxation Optimal income taxation is quite a different problem than optimal commodity taxation. In optimal commodity taxation the issue was which commodities to tax,

High School Lesson Plan

Standards New York 12.G5b. On various issues, certain governmental branches and agencies are responsible for determining policy. Those who create public policies attempt to balance regional and national

Standards New York 12.G5b. On various issues, certain governmental branches and agencies are responsible for determining policy. Those who create public policies attempt to balance regional and national

Potential Financial Exposure (PFE)

") Dan Diebold September 19, 2017 Potential Financial Exposure (PFE) dan.diebold@avangrid.com www.avangridrenewables.com 1 Current vs. Future Exposure Credit risk managers traditionally focus on current exposure

Dan Diebold September 19, 2017 Potential Financial Exposure (PFE) dan.diebold@avangrid.com www.avangridrenewables.com 1 Current vs. Future Exposure Credit risk managers traditionally focus on current exposure

Market Risk: FROM VALUE AT RISK TO STRESS TESTING. Agenda. Agenda (Cont.) Traditional Measures of Market Risk

Traditional Measures of Market Risk") Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

Thomas H. Billeter, CPA Newsletter Fall Illinois Ave, Saint Charles, IL 60174

Thomas H. Billeter, CPA 630.377.4635 Newsletter Fall 2013 527 Illinois Ave, Saint Charles, IL 60174 Well here it is-the fall newsletter and it is still fall! Not only that-but it is coming out when I promised

Thomas H. Billeter, CPA 630.377.4635 Newsletter Fall 2013 527 Illinois Ave, Saint Charles, IL 60174 Well here it is-the fall newsletter and it is still fall! Not only that-but it is coming out when I promised

Lecture Materials FUNDING. Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Middle School Lesson Plan

Standards New York 8.2e Progressive reformers sought to address political and social issues at the local, state, and federal levels of government between 1890 and 1920. New Jersey 6.1.8.A.2.b Explain how

Standards New York 8.2e Progressive reformers sought to address political and social issues at the local, state, and federal levels of government between 1890 and 1920. New Jersey 6.1.8.A.2.b Explain how

Treatment of IRRBB in Latin America

Treatment of IRRBB in Latin America Survey results Meeting on Interest Rate Risk in the Banking Book (IRRBB) and the Revised Standardised Approach (RSA) for Credit Risk Sao Paulo, Brazil 27-28 April 2016

Treatment of IRRBB in Latin America Survey results Meeting on Interest Rate Risk in the Banking Book (IRRBB) and the Revised Standardised Approach (RSA) for Credit Risk Sao Paulo, Brazil 27-28 April 2016

Asset/Liability Management

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Revenue Forecasting in Local Government. Hitting the Bulls Eye. Slide 1. Slide 2. Slide 3. Slide 4. School of Government 1

Slide 1 Revenue Forecasting in Local Government: Hitting the Bulls Eye November 10, 2010 Key objectives for this session. 1. Understand the importance and difficulties of revenue estimation 2. Learn six

Slide 1 Revenue Forecasting in Local Government: Hitting the Bulls Eye November 10, 2010 Key objectives for this session. 1. Understand the importance and difficulties of revenue estimation 2. Learn six

Estimating Beta. The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ): R j = a + b R m

against market returns (R m ): R j = a + b R m") Estimating Beta 122 The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ): R j = a + b R m where a is the intercept and b is the slope of the regression.

Estimating Beta 122 The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ): R j = a + b R m where a is the intercept and b is the slope of the regression.

Testing of the ALM Process: What Should it Really Entail?

Testing of the ALM Process: What Should it Really Entail? Tuesday, June 18, 2013 2:00 PM 3:15 PM Presented by: Bert Purdy, CPA, CTFA Senior Manager BKD, LLP 211 N. Broadway, Suite 600 St. Louis, MO 63102

Testing of the ALM Process: What Should it Really Entail? Tuesday, June 18, 2013 2:00 PM 3:15 PM Presented by: Bert Purdy, CPA, CTFA Senior Manager BKD, LLP 211 N. Broadway, Suite 600 St. Louis, MO 63102

The CECL Workshop Series. CECL Finalization & Methodologies

The CECL Workshop Series. CECL Finalization & Methodologies June 7, 2016 P R E S E N T E D B Y Todd Sprang CliftonLarsonAllen Tom Danielson CliftonLarsonAllen Tim McPeak Sageworks About the Webinar. Ask

The CECL Workshop Series. CECL Finalization & Methodologies June 7, 2016 P R E S E N T E D B Y Todd Sprang CliftonLarsonAllen Tom Danielson CliftonLarsonAllen Tim McPeak Sageworks About the Webinar. Ask

Corporate Finance, Module 3: Common Stock Valuation. Illustrative Test Questions and Practice Problems. (The attached PDF file has better formatting.

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Balance Sheet Strategies For Changing Rate Environments

Balance Sheet Strategies For Changing Rate Environments Moss Adams 2017 Credit Union Conference Portland, OR June 22 nd, 2017 Ryan W. Hayhurst Managing Director ryan@gobaker.com 800 962 9468 Credit Union

Balance Sheet Strategies For Changing Rate Environments Moss Adams 2017 Credit Union Conference Portland, OR June 22 nd, 2017 Ryan W. Hayhurst Managing Director ryan@gobaker.com 800 962 9468 Credit Union

International Financial Markets Prices and Policies. Second Edition Richard M. Levich. Overview. ❿ Measuring Economic Exposure to FX Risk

International Financial Markets Prices and Policies Second Edition 2001 Richard M. Levich 16C Measuring and Managing the Risk in International Financial Positions Chap 16C, p. 1 Overview ❿ Measuring Economic

International Financial Markets Prices and Policies Second Edition 2001 Richard M. Levich 16C Measuring and Managing the Risk in International Financial Positions Chap 16C, p. 1 Overview ❿ Measuring Economic

Robust Models of Core Deposit Rates

Robust Models of Core Deposit Rates by Michael Arnold, Principal ALCO Partners, LLC & OLLI Professor Dominican University Bruce Lloyd Campbell Principal ALCO Partners, LLC Introduction and Summary Our

Robust Models of Core Deposit Rates by Michael Arnold, Principal ALCO Partners, LLC & OLLI Professor Dominican University Bruce Lloyd Campbell Principal ALCO Partners, LLC Introduction and Summary Our

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Activity: After the Bell Before the Curtain

Activity: After the Bell Before the Curtain Activity Objective: Students will review terms and concepts from the Stock Market Game. They will also realize that winning the SMG is not the most important

Activity: After the Bell Before the Curtain Activity Objective: Students will review terms and concepts from the Stock Market Game. They will also realize that winning the SMG is not the most important

Appendix B: Messages. The (5,7)-game

-game") Appendix B: Messages The (5,7)-game In the tables below: R = Roll, D = Don't. We classify messages as HR = Promise High & Roll, IHR = Implicit promise High & Roll, LD = Promise Low, then Don t, ILD = Implicit

Appendix B: Messages The (5,7)-game In the tables below: R = Roll, D = Don't. We classify messages as HR = Promise High & Roll, IHR = Implicit promise High & Roll, LD = Promise Low, then Don t, ILD = Implicit

We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo

in São Paulo") Executive Summary We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo Although we achieve a 26% IRR in the Base Case, we earn above the

Executive Summary We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo Although we achieve a 26% IRR in the Base Case, we earn above the

Asset Liability Management. Craig Roodt Australian Prudential Regulation Authority

Asset Liability Management Craig Roodt Australian Prudential Regulation Authority Outline of Topics 1. ALM Defined 2. Role of ALM in the Organisation 3. Some History 4. Main Approaches - Measurement 5.

Asset Liability Management Craig Roodt Australian Prudential Regulation Authority Outline of Topics 1. ALM Defined 2. Role of ALM in the Organisation 3. Some History 4. Main Approaches - Measurement 5.

Chapter 16. Random Variables. Copyright 2010, 2007, 2004 Pearson Education, Inc.

Chapter 16 Random Variables Copyright 2010, 2007, 2004 Pearson Education, Inc. Expected Value: Center A random variable is a numeric value based on the outcome of a random event. We use a capital letter,

Chapter 16 Random Variables Copyright 2010, 2007, 2004 Pearson Education, Inc. Expected Value: Center A random variable is a numeric value based on the outcome of a random event. We use a capital letter,

Practice Set #1: Forward pricing & hedging.

Derivatives (3 credits) Professor Michel Robe What to do with this practice set? Practice Set #1: Forward pricing & hedging To help students with the material, eight practice sets with solutions shall

Derivatives (3 credits) Professor Michel Robe What to do with this practice set? Practice Set #1: Forward pricing & hedging To help students with the material, eight practice sets with solutions shall

Riding the Stock Market Wave in the First Half of 2009

Riding the Stock Market Wave in the First Half of 2009 July 7, 2009 by Ron Surz Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor

Riding the Stock Market Wave in the First Half of 2009 July 7, 2009 by Ron Surz Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor

Loan-to-deposit ratio in the banking system hit a 35-year low recently.

For a while I have said the US commercial banking industry is on a path to long term contraction and consolidation. The last banks standing are already known JP Morgan, Wells Fargo, Bank of America, Citi,

For a while I have said the US commercial banking industry is on a path to long term contraction and consolidation. The last banks standing are already known JP Morgan, Wells Fargo, Bank of America, Citi,

This presentation is part of a three part series.

As a club treasurer, you ll have certain tasks you ll be performing each month to keep your clubs financial records. In tonight s presentation, we ll cover the basics of how you should perform these. Monthly

As a club treasurer, you ll have certain tasks you ll be performing each month to keep your clubs financial records. In tonight s presentation, we ll cover the basics of how you should perform these. Monthly

CECL Implementation Concepts: Reasonable and Supportable Forecasts. A Discussion Paper of the AMERICAN BANKERS ASSOCIATION

CECL Implementation Concepts: Reasonable and Supportable Forecasts A Discussion Paper of the AMERICAN BANKERS ASSOCIATION ABA Contacts: Michael L. Gullette SVP, Tax and Accounting mgullette@aba.com 202-663-4986

CECL Implementation Concepts: Reasonable and Supportable Forecasts A Discussion Paper of the AMERICAN BANKERS ASSOCIATION ABA Contacts: Michael L. Gullette SVP, Tax and Accounting mgullette@aba.com 202-663-4986

2018 Mid-Cycle Dodd-Frank Act Stress Test (DFAST) October 22, 2018

October 22, 2018") 2018 Mid-Cycle Dodd-Frank Act Stress Test (DFAST) October 22, 2018 Table of Contents A B C D E F Section Page Disclaimer 3 Requirements for Mid-Cycle Dodd-Frank Act Stress Test 4 Description of the Company-Run

2018 Mid-Cycle Dodd-Frank Act Stress Test (DFAST) October 22, 2018 Table of Contents A B C D E F Section Page Disclaimer 3 Requirements for Mid-Cycle Dodd-Frank Act Stress Test 4 Description of the Company-Run

Lecture 13: Social Insurance

Lecture 13: Social Insurance November 24, 2015 Overview Course Administration Ripped From Headlines Why Should We Care? What is Insurance? Why Social Insurance? Additional Reasons for Government Intervention

Lecture 13: Social Insurance November 24, 2015 Overview Course Administration Ripped From Headlines Why Should We Care? What is Insurance? Why Social Insurance? Additional Reasons for Government Intervention

The Hard Lessons of Stock Market History

The Hard Lessons of Stock Market History The Lessons of Stock Market History If you re like most people, you believe there s a great deal of truth in the old adage that history tends to repeats itself

The Hard Lessons of Stock Market History The Lessons of Stock Market History If you re like most people, you believe there s a great deal of truth in the old adage that history tends to repeats itself

ECON DISCUSSION NOTES ON CONTRACT LAW-PART 2. Contracts. I.1 Investment in Performance

ECON 522 - DISCUSSION NOTES ON CONTRACT LAW-PART 2 I Contracts I.1 Investment in Performance Investment in performance is investment to reduce the probability of breach. For example, suppose I decide to

ECON 522 - DISCUSSION NOTES ON CONTRACT LAW-PART 2 I Contracts I.1 Investment in Performance Investment in performance is investment to reduce the probability of breach. For example, suppose I decide to

Monthly Treasurers Tasks

As a club treasurer, you ll have certain tasks you ll be performing each month to keep your clubs financial records. In tonights presentation, we ll cover the basics of how you should perform these. Monthly

As a club treasurer, you ll have certain tasks you ll be performing each month to keep your clubs financial records. In tonights presentation, we ll cover the basics of how you should perform these. Monthly

Global Imbalances. January 23rd

Global Imbalances January 23rd Fact #1: The US deficit is big But there is little agreement on why, or on how much we should worry about it Global current account identity (CA = S-I = I*-S*) is a useful

Global Imbalances January 23rd Fact #1: The US deficit is big But there is little agreement on why, or on how much we should worry about it Global current account identity (CA = S-I = I*-S*) is a useful