Lecture Materials Topic 3 Yield Curves and Interest Forecasts ECONOMICS, MONEY MARKETS AND BANKING

|

|

|

- Julian Gardner

- 5 years ago

- Views:

Transcription

1 Lecture Materials Topic 3 Yield Curves and Interest Forecasts ECONOMICS, MONEY MARKETS AND BANKING Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com August 2, 2017

2

3 Topic 3 Yield Curves and Interest Forecasts

4 I. Yield Curve (Term Structure of Interest Rates) Basics 1. What is the Yield Curve? Interest rates on financial instruments vary because of default risk, liquidity risk, call provisions, etc. Holding all the above constant, it also appears rates vary because of maturity. The relationship between interest rates and maturity, all else fixed, is called the term structure of interest rates or the yield curve. Where do we find the yield curve? Typical yield curve.

5 Yield Curves are Important so Found Everywhere

6 Normal curve looking good!

7 Steep Curve let s go! 281 Bps 475 Bps

8 Flat Curve What s next?

9 Inverted Curve Uh-oh!

10 Note: downward sloping when rates high Flatter when rates moderate Upward sloping when rates low

11 How does the bond market react? T10Y vs FF s target 30yr review

12 What Determines the Shape and Movement of the Yield Curve

13 A. The Segmented Markets View: independent markets i S i S.10 D Short-term funds D Long-term funds Players: Fed Banks Insurance/pension companies Instruments: T-bills, commercial paper Mortgages, bonds, note

14 Implied Yield Curve i maturity Operation Twist (early 1960 s) To raise short rates and lower long rates Fed was to sell bills and buy bonds.

15 Implied Yield Curve i Fed sold T-bills from its portfolio. This should lower T-bill prices and raise short term rates Fed then purchased long term Treasury Securities, trying to drive long term debt prices up, and long rates down maturity Operation Twist (early 1960 s) To raise short rates and lower long rates Fed was to sell bills and buy bonds.

16 Observation 1: Twist does not change money in circulation-if the Fed sells one thing and buys another the money * stays the same! *technically, the monetary base, more on this friday

17 Point 2: Operation Twist no help for bankers! Government Yield Curve Interest Rate Original spread 4% New spread 1% Maturity (years)

can be neutral as far as the money supply goes but can also be a credit policy that is not neutral in outcome.")

: Fed lending $ it earned off investing bank reserves in treasury securities ($ it could have given back to the Treasury)to JPMorgan to purchase Bear")

18 Good point to bring up the many different dimensions of monetary policy Pure Monetary policy is usually viewed as something that affects the money supply, monetary base or bank reserves or maybe basic interest rate levels. Credit Policy (like a pure twist operation) can be neutral as far as the money supply goes but can also be a credit policy that is not neutral in outcome. For example, suppose the Fed twists by selling Treasury securities and buying Mortgage backed securities. Money supply stays the same but the Fed provides credit directly and specifically to the housing sector. Credit policy is not monetary policy because it does not increase bank reserves or the monetary base. Fiscal policy ( government spending ): Fed lending $ it earned off investing bank reserves in treasury securities ($ it could have given back to the Treasury)to JPMorgan to purchase Bear Stearns or the $50 billion dollars the Fed loaned its subsidiaries Maiden Lane II and III to purchase, residential mortgage-backed securities from AIG, and multi-sector collateralized debt obligations on which AIG has written credit default swap contracts to keep AIG afloat.

19 B.Pure Expectations View (sometimes called the Rational Expectations View) Suppose an investor has a two-year time horizon (holding period). Suppose further that 1-year and 2-year deposits exist. Suppose further that the current 1-year rates is 4% and the depositor thinks the 1-year rate one year from now will be 10%. What rate would you have to offer to get this depositor to put money in a 2-year deposit.

20 Strategy 1: Rollover One year CDs 4% 10% (I think) One Year OR Strategy 2: Just Buy a Two Year CD What rate would banker put on this to interest you in a two year CD? Annual Rate has to be 7% Two Year One Year

21 What would seller of 2-year deposit have to offer to attract a buyer? Rollover Strategy R 1 + E( 1 R 1 ) = 4% + 10% = 14% Just Go Long Strategy R 2 + R 2 =.14 2 R 2 =.14 R 2 =.07 = 7%

22 2. Implications for Yield Curve i Example shows that the 2-year rate will end up being roughly the average of the current 1-year rate and the expected 1-year rate, i.e., * This implies that the yield curve is drawn for some market expectation of short-term rates in the future. Yield curve given the.07 Market thinks the 1-year.04 10% 1 2 maturity 2 rate next year is going to be * What if This Doesn t Hold? a) If R 2 < 7, nobody will buy 2yr Bonds. Price will fall, rate will increase b) If R 2 > 7, everybody will buy 2yr Bonds. Price will Rise, rate will fall

23 This implies that the expected future direction of rates is embedded in the yield curve. To see this, what if the market thinks the 1-year rate next year will be 4% or 20%? I.12 If 1-year rate next year expected to be 20%.07 If 1-year rate next year expected to be 10%.04 If 1-year rate next year expected to be 4%.03 If 1-year rate next year expected to be 2% 1 2 maturity R2 R2 R2 R

24

25 Conclusion (compare to picture of typical yield curve) Yield Curve Slope Flat Upward Downward Markets Guess of Where Rates are Headed No change in rates Rates will rise Rates will fall

26 Then, Formal yield curve forecasts Let R i = current known rate from the WSJ on i period Investments t F i = forward rates = markets guess of rate on i period investments, t periods from now 2R 2 = R F 1 (invest in a 2 yr, or two 1 yrs) 3R 3 = R F 2 (invest in a 3 yr, or a one and a two) 3R 3 = 2R F 1 (invest in a 3 yr, or a two and a one) Solutions R R R R R 1 1 2R 2 1F1 2 21F2 3 2F1 3

27 Example Yield Curve on June 2, 2017 R 1 =.0068 R 2 =.0089 R 3 =.0103 What does the market think the 1-year rate will be in 2018? 2 R 2 = R F 1 1F 1 = 2 R 2 - R 1 = 2(.0089) =.011 Last year 1 F 1 =.011 so it overestimated What does the market think the 1-year rate will be in Aug 2019? 3R 3 = 2R F 1 2F 1 = 3(.0103) - 2(.0089) =.0131

28 Real Expectations Yield Curve Theory at Work Which is the better choice for a $1mm purchase? 3yr 0.93% or 7yr 1.53% The real expectations yield curve theory would suggest that you would accumulate the same level of income by holding either bond. In order for that to hold true, the principal balance on the 3yr bullet would have to earn a level of return equivalent to the earnings gap when reinvested at maturity for 4yrs. Copyright 2016 S&P Global. Knowledge Center, a part of S&P Global Market Intelligence, a division of S&P Global Inc.

29 Real Expectations Yield Curve Theory at Work 60 bps of additional yield equates to $6000 more in annual earnings (per $1mm) on the 7yr bullet for a total of $18,000 over the 3yr bullet s holding period The 7yr bullet will earn an $61,200 in interest income during the last four years of its term In order to capture total income, we add the additional $18,000 earned over the first three years to the $61,200 for a total of $79,200 Therefore, we will need to reinvest our maturing 3yr bullet at an average rate of 1.98% ((79,200/4)/1,000,000 = 1.98%) over the next 4yrs to break even with the 7yr bullet Copyright 2016 S&P Global. Knowledge Center, a part of S&P Global Market Intelligence, a division of S&P Global Inc.

30 The Forward Curve

31 Four Applications of this Theory 1. Riding the yield curve 2. Loan interest swaps 3. QE s and Twist 4. Forecasting rates

32

33 III. Yield Yield Curve Games A. Riding the Yield Curve for Fun and Profit Basic idea: Assuming a positively sloped yield curve, purchase a security with a maturity longer than your expected holding period. Rationale: You will make money because 1) longer maturities pay higher rates, 2) when you sell it in the security will have a shorter maturity, hence lower rates, hence a capital gain maturity (years)

34 Example: You want to invest for 1 year. Current 1-year rate is 4%, 2-year rate is 7%. -- If you buy 1-year security make 4% -- If ride, price per dollar of face of 2-year security is If sell in one year when 1-year rate is 4%, get.9615 Profit % 2 Price * (1.07) Price (1.07) Price*(1.04) 1.00 Price 1.00 (1.04).9615

35 Will this work in an efficient market? --What will you be able to sell the security at next year? The market expects the rate on 1-year securities to be 10%. This implies the price will be Profit % Price*1.10 = 1.00 Price = 1.00/1.10 = 90.90

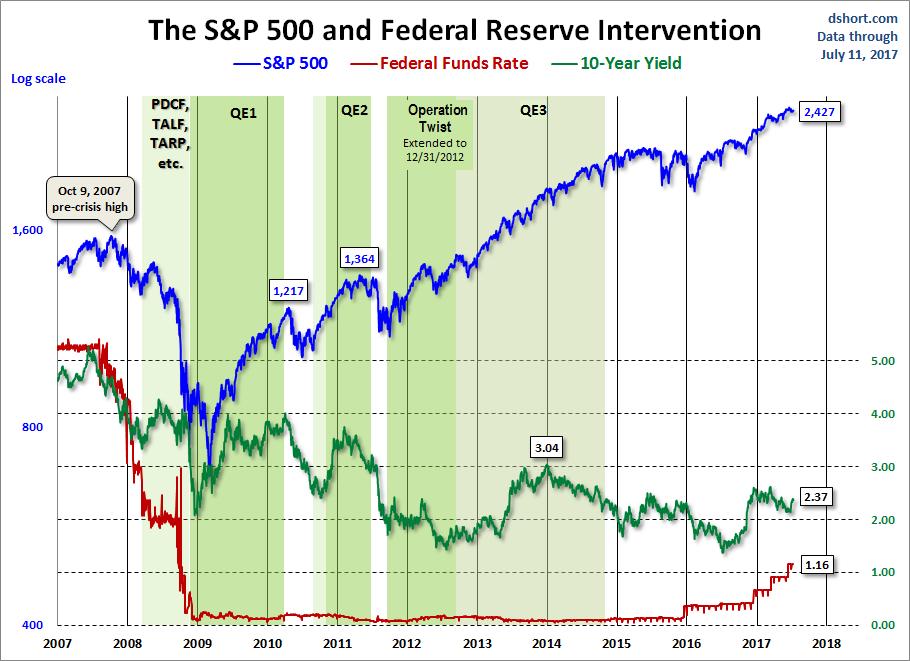

36 What if 1 year rate next year ends up 14%! Profit ! Price*1.14 = 1.00 Price = 1.00/1.14 =.8772

37 So when do you make extra $ (above 4%) riding the yield curve? Whenever the actual rate in the future is less than the rate the market expects which is the implied forward rate. actual rate a year from now < 1 f 1 make extra $ actual rate a year from now > 1 f 1 lose $ actual rate a year from now = 1 f 1 break even

38

39 Forward Rate - Actual Rate 4.0% 3.0% If positive, market overestimated what rates would be, i.e. rate ended up less than the market expected. 2.0% 1.0% 0.0% 06/ / / / / / / / / / / / / / % -2.0% -3.0% Article recom -mands riding! Rates went up more than the market thought! i.e got burned is you rode (markets underestimated inflation) -4.0% Forwards over estimate, in part, because the risk premium is not netted out of the long rate before the calculation is done.

40 LIBOR SWAPS Suppose the banker wants to receive variable rate interest, but the customer wants to pay fixed. Impasse! No Deal? Solution: Let the customer pay fixed, then swap the fixed for Libor (variable) in the interest swap market. The curve on the next page says the market will trade about 4.13% fixed each year for two years in exchange for 3 month Libor each quarter for two years.

41 So let s use a somewhat far fetched example to show the principle. The customer pays fixed 7% and our bank SWAPs it out by paying 4.13% to get whatever Libor turns out to be.

42 CURRENT RATES DOWN RATES UPRATES UP 1% 2% 4% LOAN RATE 7% 7% 7% 7% CD RATE (LIBOR) 4% 3% 6% 8% Internal Spread 3% 4% 1% 1% (LOAN RATE CD RATE) SWAP SIDE Pay Fixed 4.13% 4.13% 4.13% 4.13% Get Libor 4% 3% 6% 8% Net on SWAP.13% 1.13% +1.87% +3.87% $ IN Loan Rate 7% 7% 7% 7% Get Libor in SWAP Mkt 4% 3% 6% 8% $OUT CD Rate to Customer 4% 3% 6% 8% Fixed to SWAP Mkt 4.13% 4.13% 4.13% 4.13% Interest to Bank 2.87% 2.87% 2.87% 2.87%

43 How does the market come up with this tradeoff? (Let s use annual Libor for simplicity) R 1 2 Libor now 4% 1F1 Libor next year 10 % 2 R The fixed rate for two years 2(7%) Then market will add a risk premium in case customer defaults.

44 Real World Suppose a customer knows that the market typically overestimates short-term rates. In our example, suppose customer thinks rate next year on 1 year stuff is going to be 8%, not 10%. Then, they will prefer the variable to the fixed, because 4% + 8% < 7% + 7%.

45 Quantitative Easing: How Did the Fed Get Away with Lowering Long-term rates? Huge shift in fed portfolio away from Treasury Securities

46 Total Assets held by the Federal Reserve $ tillions $4 QE1 QE2 QE3 $3 $2 $1 $

47 QE1 Bailout Phase QE1 is a nickname developed to refer to the first round of quantitative easing in November Purchase GSE debt of $100 billion and MBS of $500 billion (then increased to $200 billion and $1.25 trillion in 2009 plus $300 billion in long term treasuries). QE2 KICK START ECONOMY PHASE 1 Basically $600 billion in longer term treasuries. QE3 We Need More The Fed buys $85 billion a month in both MBS and Treasuries from banks. Then promised rates would stay low! Called forward guidance. Why did they do this? Go back to our example. Suppose R 1 =4%, 1 f 1 =10%, then R 2 =7%. Only way Fed can drive R 2 =5% for example is to promise that 1 f 1 =6%, In other words promise that short rates would stay low! If not, nobody would hold the 5% security, they would sell, P down, rate up defeating the Fed s intention!

48

49 Interest Forecasting There are three ways to forecast interest rates. 1. Roll your own Nominal rate = real rate + expected inflation Forecast Real GDP 2. Use implied forward rates 3. Look at the futures market Forecast inflation Suppose you (I) think a bushel of corn will sell for $100 a year from now. Would you agree now to sell it to me then for less than $100? Would I agree to pay more than $100? So, the price will end up being close to our best guess of the price. Same is true for the t-bills, fed funds, bonds.

Lecture Materials ECONOMICS, MONEY MARKETS AND BANKING

Lecture Materials TOPIC 3: YIELD CURVES AND INTEREST FORECASTS ECONOMICS, MONEY MARKETS AND BANKING James M. Johannes Interim Associate Dean for Executive and Evening MBA Programs Aschenbrener Chair of

Lecture Materials TOPIC 3: YIELD CURVES AND INTEREST FORECASTS ECONOMICS, MONEY MARKETS AND BANKING James M. Johannes Interim Associate Dean for Executive and Evening MBA Programs Aschenbrener Chair of

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy Some of the following material comes from a variety of

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy Some of the following material comes from a variety of

1. Parallel and nonparallel shifts in the yield curve. 2. Factors that drive U.S. Treasury security returns.

LEARNING OUTCOMES 1. Parallel and nonparallel shifts in the yield curve. 2. Factors that drive U.S. Treasury security returns. 3. Construct the theoretical spot rate curve. 4. The swap rate curve (LIBOR

LEARNING OUTCOMES 1. Parallel and nonparallel shifts in the yield curve. 2. Factors that drive U.S. Treasury security returns. 3. Construct the theoretical spot rate curve. 4. The swap rate curve (LIBOR

LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing. October 10, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Financial Highlights

January 20, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Consumer Credit Revolving and Nonrevolving 3 Compared with Past Recessions 4 Credit Card Delinquencies

January 20, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Consumer Credit Revolving and Nonrevolving 3 Compared with Past Recessions 4 Credit Card Delinquencies

LECTURE 11 Monetary Policy at the Zero Lower Bound: Quantitative Easing. November 2, 2016

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 11 Monetary Policy at the Zero Lower Bound: Quantitative Easing November 2, 2016 I. OVERVIEW Monetary Policy at the Zero Lower Bound: Expectations

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 11 Monetary Policy at the Zero Lower Bound: Quantitative Easing November 2, 2016 I. OVERVIEW Monetary Policy at the Zero Lower Bound: Expectations

BOND ANALYTICS. Aditya Vyas IDFC Ltd.

BOND ANALYTICS Aditya Vyas IDFC Ltd. Bond Valuation-Basics The basic components of valuing any asset are: An estimate of the future cash flow stream from owning the asset The required rate of return for

BOND ANALYTICS Aditya Vyas IDFC Ltd. Bond Valuation-Basics The basic components of valuing any asset are: An estimate of the future cash flow stream from owning the asset The required rate of return for

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com 770-850-3403 August 7, 2017 Intro

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com 770-850-3403 August 7, 2017 Intro

3.36pt. Karl Whelan (UCD) Term Structure of Interest Rates Spring / 36

Term Structure of Interest Rates Spring / 36") 3.36pt Karl Whelan (UCD) Term Structure of Interest Rates Spring 2018 1 / 36 International Money and Banking: 12. The Term Structure of Interest Rates Karl Whelan School of Economics, UCD Spring 2018 Karl

3.36pt Karl Whelan (UCD) Term Structure of Interest Rates Spring 2018 1 / 36 International Money and Banking: 12. The Term Structure of Interest Rates Karl Whelan School of Economics, UCD Spring 2018 Karl

13 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Chapter. Key Concepts

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Finance 527: Lecture 30, Options V2

Finance 527: Lecture 30, Options V2 [John Nofsinger]: This is the second video for options and so remember from last time a long position is-in the case of the call option-is the right to buy the underlying

Finance 527: Lecture 30, Options V2 [John Nofsinger]: This is the second video for options and so remember from last time a long position is-in the case of the call option-is the right to buy the underlying

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 330 Spring 2015: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate

Econ 330 Spring 2015: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate

Find Private Lenders Now CHAPTER 10. At Last! How To. 114 Copyright 2010 Find Private Lenders Now, LLC All Rights Reserved

CHAPTER 10 At Last! How To Structure Your Deal 114 Copyright 2010 Find Private Lenders Now, LLC All Rights Reserved 1. Terms You will need to come up with a loan-to-value that will work for your business

CHAPTER 10 At Last! How To Structure Your Deal 114 Copyright 2010 Find Private Lenders Now, LLC All Rights Reserved 1. Terms You will need to come up with a loan-to-value that will work for your business

Asset and Net Worth Growth Loan Allocation Trends 2

Growth, Capital, and Concentration Risk Management Jonathan Jackson, CFA Advisor Catalyst Strategic Solutions Asset and Net Worth Growth 1 Asset and Net Worth Growth Loan Allocation Trends 2 Loan Allocations

Growth, Capital, and Concentration Risk Management Jonathan Jackson, CFA Advisor Catalyst Strategic Solutions Asset and Net Worth Growth 1 Asset and Net Worth Growth Loan Allocation Trends 2 Loan Allocations

Theory of Consumer Behavior First, we need to define the agents' goals and limitations (if any) in their ability to achieve those goals.

in their ability to achieve those goals.") Theory of Consumer Behavior First, we need to define the agents' goals and limitations (if any) in their ability to achieve those goals. We will deal with a particular set of assumptions, but we can modify

Theory of Consumer Behavior First, we need to define the agents' goals and limitations (if any) in their ability to achieve those goals. We will deal with a particular set of assumptions, but we can modify

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 03

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 03

Getting ahead of the (yield) curve

curve") Capital market insights Conversation guide May 2018 Getting ahead of the (yield) curve The yield curve has been a hot topic in the financial media recently. It is one of the best indicators of future economic

Capital market insights Conversation guide May 2018 Getting ahead of the (yield) curve The yield curve has been a hot topic in the financial media recently. It is one of the best indicators of future economic

A BOND MARKET IS-LM SYNTHESIS OF INTEREST RATE DETERMINATION

A BOND MARKET IS-LM SYNTHESIS OF INTEREST RATE DETERMINATION By Greg Eubanks e-mail: dismalscience32@hotmail.com ABSTRACT: This article fills the gaps left by leading introductory macroeconomic textbooks

A BOND MARKET IS-LM SYNTHESIS OF INTEREST RATE DETERMINATION By Greg Eubanks e-mail: dismalscience32@hotmail.com ABSTRACT: This article fills the gaps left by leading introductory macroeconomic textbooks

ECON DISCUSSION NOTES ON CONTRACT LAW. Contracts. I.1 Bargain Theory. I.2 Damages Part 1. I.3 Reliance

ECON 522 - DISCUSSION NOTES ON CONTRACT LAW I Contracts When we were studying property law we were looking at situations in which the exchange of goods/services takes place at the time of trade, but sometimes

ECON 522 - DISCUSSION NOTES ON CONTRACT LAW I Contracts When we were studying property law we were looking at situations in which the exchange of goods/services takes place at the time of trade, but sometimes

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

The perceived chance that the issuer will default (i.e. fail to live up to repayment contract)

") Chapter 6: The Risk and Term Structure of Interest Rates In previous chapter we analyzed the determination of "the interest rate" as if there were only 1. YTM's, though, differ according to risk and maturity,

Chapter 6: The Risk and Term Structure of Interest Rates In previous chapter we analyzed the determination of "the interest rate" as if there were only 1. YTM's, though, differ according to risk and maturity,

11 EXPENDITURE MULTIPLIERS* Chapt er. Key Concepts. Fixed Prices and Expenditure Plans1

Chapt er EXPENDITURE MULTIPLIERS* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded. As a result: The price

Chapt er EXPENDITURE MULTIPLIERS* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded. As a result: The price

So far in the short-run analysis we have ignored the wage and price (we assume they are fixed).

.") Chapter 6: Labor Market So far in the short-run analysis we have ignored the wage and price (we assume they are fixed). Key idea: In the medium run, rising GD will lead to lower unemployment rate (more

Chapter 6: Labor Market So far in the short-run analysis we have ignored the wage and price (we assume they are fixed). Key idea: In the medium run, rising GD will lead to lower unemployment rate (more

Bond Basics June 2006

Yield Curve Basics The yield curve, a graph that depicts the relationship between bond yields and maturities, is an important tool in fixed-income investing. Investors use the yield curve as a reference

Yield Curve Basics The yield curve, a graph that depicts the relationship between bond yields and maturities, is an important tool in fixed-income investing. Investors use the yield curve as a reference

U. S. Economic Projections. GDP Core PCE Price Index Unemployment Rate (YE)

") The Federal Reserve will likely hold short-term interest rates steady until late 2015. U. S. Economic Projections 2014 2015 2014 2015 2014 2015 Stifel FI Strategy Group Forecast 2.5% 3.1% 1.4% 1.7% 6.4%

The Federal Reserve will likely hold short-term interest rates steady until late 2015. U. S. Economic Projections 2014 2015 2014 2015 2014 2015 Stifel FI Strategy Group Forecast 2.5% 3.1% 1.4% 1.7% 6.4%

Macroeconomics for Finance

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 1 Contact E-mail: jmackiewicz@wne.uw.edu.pl Office hours: Wednesdays, 5:00-6:00 p.m., room 409. Webpage: http://coin.wne.uw.edu.pl/jmackiewicz/

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 1 Contact E-mail: jmackiewicz@wne.uw.edu.pl Office hours: Wednesdays, 5:00-6:00 p.m., room 409. Webpage: http://coin.wne.uw.edu.pl/jmackiewicz/

Key Idea: We consider labor market, goods market and money market simultaneously.

Chapter 7: AS-AD Model Key Idea: We consider labor market, goods market and money market simultaneously. (1) Labor Market AS Curve: We first generalize the wage setting (WS) equation as W = e F(u, z) (1)

Chapter 7: AS-AD Model Key Idea: We consider labor market, goods market and money market simultaneously. (1) Labor Market AS Curve: We first generalize the wage setting (WS) equation as W = e F(u, z) (1)

Title: Market Timing Risk in Laddering a CD Portfolio

Title: Market Timing Risk in Laddering a Portfolio Author: Don Taylor Institution: Penn State Brandywine Submission for: AFS 2012 Fall Conference Abstract: A laddered portfolio of non-marketable s behaves

Title: Market Timing Risk in Laddering a Portfolio Author: Don Taylor Institution: Penn State Brandywine Submission for: AFS 2012 Fall Conference Abstract: A laddered portfolio of non-marketable s behaves

Financial Highlights

June 16, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Commercial Mortgage Backed Securities Yield Spreads 3 Issuance 3 Residential Mortgages Rates

June 16, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Commercial Mortgage Backed Securities Yield Spreads 3 Issuance 3 Residential Mortgages Rates

International Money and Banking: 6. Problems with Monetarism

International Money and Banking: 6. Problems with Monetarism Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Money and Inflation Spring 2018 1 / 30 The Basic Elements of Monetarism Last

International Money and Banking: 6. Problems with Monetarism Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Money and Inflation Spring 2018 1 / 30 The Basic Elements of Monetarism Last

Foreign Trade and the Exchange Rate

Foreign Trade and the Exchange Rate Chapter 12 slide 0 Outline Foreign trade and aggregate demand The exchange rate The determinants of net exports A A model of the real exchange rates The IS curve and

Foreign Trade and the Exchange Rate Chapter 12 slide 0 Outline Foreign trade and aggregate demand The exchange rate The determinants of net exports A A model of the real exchange rates The IS curve and

Financial Highlights

January 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Mortgage Backed Securities Issuance and Spreads 3 CMBS TALF Operations 4 Broad Financial

January 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Mortgage Backed Securities Issuance and Spreads 3 CMBS TALF Operations 4 Broad Financial

Financial Mathematics Principles

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

The Mortgage Debt Market: A Tragedy

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Homework Assignment #6. Due Tuesday, 11/28/06. Multiple Choice Questions:

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

ECO LECTURE TWENTY-FOUR 1 OKAY. WELL, WE WANT TO CONTINUE OUR DISCUSSION THAT WE HAD

ECO 155 750 LECTURE TWENTY-FOUR 1 OKAY. WELL, WE WANT TO CONTINUE OUR DISCUSSION THAT WE HAD STARTED LAST TIME. WE SHOULD FINISH THAT UP TODAY. WE WANT TO TALK ABOUT THE ECONOMY'S LONG-RUN EQUILIBRIUM

ECO 155 750 LECTURE TWENTY-FOUR 1 OKAY. WELL, WE WANT TO CONTINUE OUR DISCUSSION THAT WE HAD STARTED LAST TIME. WE SHOULD FINISH THAT UP TODAY. WE WANT TO TALK ABOUT THE ECONOMY'S LONG-RUN EQUILIBRIUM

Notes VI - Models of Economic Fluctuations

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Review Material for Exam I

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

Financial Risk Measurement/Management

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

MONETARY POLICY. 8Topic

MONETARY POLICY 8Topic The Central Bank: CB The Federal Reserve System, commonly known as the Fed, is the central bank of the United States. A Central Bank (CB) is the public authority that, typically,

MONETARY POLICY 8Topic The Central Bank: CB The Federal Reserve System, commonly known as the Fed, is the central bank of the United States. A Central Bank (CB) is the public authority that, typically,

Savings and Investment

Lecture Notes for Chapter 3 of MACROECONOMICS: An Introduction Savings and Investment Copyright 2000-2009 by Charles R. Nelson 1/8/09 In this chapter we will discuss- How savings becomes investment. Banks

Lecture Notes for Chapter 3 of MACROECONOMICS: An Introduction Savings and Investment Copyright 2000-2009 by Charles R. Nelson 1/8/09 In this chapter we will discuss- How savings becomes investment. Banks

International Money and Banking: 14. Real Interest Rates, Lower Bounds and Quantitative Easing

International Money and Banking: 14. Real Interest Rates, Lower Bounds and Quantitative Easing Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Real Interest Rates Spring 2018 1 / 23

International Money and Banking: 14. Real Interest Rates, Lower Bounds and Quantitative Easing Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Real Interest Rates Spring 2018 1 / 23

The Effects of Quantitative Easing on Interest Rates: Channels and Implications for Policy

The Effects of Quantitative Easing on Interest Rates: Channels and Implications for Policy Arvind Krishnamurthy Northwestern University and NBER Annette Vissing-Jorgensen Northwestern University, CEPR

The Effects of Quantitative Easing on Interest Rates: Channels and Implications for Policy Arvind Krishnamurthy Northwestern University and NBER Annette Vissing-Jorgensen Northwestern University, CEPR

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy. Martin Blomhoff Holm

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices.

: how GDP and interest rates are determined in Short Run with Sticky Prices.") Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Financial Highlights

April 7, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Paper Issuance 3 Outstanding 3 Broad Financial Market Indicators LIBOR Spreads 4 Fed Funds

April 7, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Agency Debt and MBS Purchases 2 Commercial Paper Issuance 3 Outstanding 3 Broad Financial Market Indicators LIBOR Spreads 4 Fed Funds

Worksheet 27.1: Monetary Policy Cause and Effect

Worksheet 27.1: Monetary Policy Cause and Effect 1. If the FED wants to increase the supply, determine the use of the three FED tools and explain how the supply increase would happen. Increase the supply

Worksheet 27.1: Monetary Policy Cause and Effect 1. If the FED wants to increase the supply, determine the use of the three FED tools and explain how the supply increase would happen. Increase the supply

Chapter 15. Multiple Deposit Creation and the Money Supply Process

Chapter 15 Multiple Deposit Creation and the Money Supply Process Players in the Money Supply Process Central bank - the government agency that oversees the banking system and is responsible for the conduct

Chapter 15 Multiple Deposit Creation and the Money Supply Process Players in the Money Supply Process Central bank - the government agency that oversees the banking system and is responsible for the conduct

The Term Structure and Interest Rate Dynamics Cross-Reference to CFA Institute Assigned Topic Review #35

Study Sessions 12 & 13 Topic Weight on Exam 10 20% SchweserNotes TM Reference Book 4, Pages 1 105 The Term Structure and Interest Rate Dynamics Cross-Reference to CFA Institute Assigned Topic Review #35

Study Sessions 12 & 13 Topic Weight on Exam 10 20% SchweserNotes TM Reference Book 4, Pages 1 105 The Term Structure and Interest Rate Dynamics Cross-Reference to CFA Institute Assigned Topic Review #35

DEBT VALUATION AND INTEREST. Chapter 9

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

10/30/2018. Chapter 17. The Money Supply Process. Preview. Learning Objectives

Chapter 17 The Money Supply Process Preview This chapter provides an overview of how the banking system create and describes the basic principles of the money supply creation process Learning Objectives

Chapter 17 The Money Supply Process Preview This chapter provides an overview of how the banking system create and describes the basic principles of the money supply creation process Learning Objectives

POPULAR IBC TOPICS Notes on Lecture 4: Paying Cash vs. IBC. Robert P. Murphy July, 2015

POPULAR IBC TOPICS Notes on Lecture 4: Paying Cash vs. IBC Robert P. Murphy July, 2015 REVIEW FROM MANUAL: (Taken from SOL-II in the Course Manual.) Here we can be brief, because I reviewed Nelson s diagram

POPULAR IBC TOPICS Notes on Lecture 4: Paying Cash vs. IBC Robert P. Murphy July, 2015 REVIEW FROM MANUAL: (Taken from SOL-II in the Course Manual.) Here we can be brief, because I reviewed Nelson s diagram

Interest Rate Environment and FHLB Advance Strategies

Interest Rate Environment and FHLB Advance Strategies Jason Hwang Director, Financial Strategies, Research, and Membership Applications Kevin Martin Manager, Member Financial Strategies September 22, 2015

Interest Rate Environment and FHLB Advance Strategies Jason Hwang Director, Financial Strategies, Research, and Membership Applications Kevin Martin Manager, Member Financial Strategies September 22, 2015

II. Determinants of Asset Demand. Figure 1

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending Today: I. What s a Repo? II. Financing with Repos III. Shorting with Repos IV. Specialness and Supply

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending Today: I. What s a Repo? II. Financing with Repos III. Shorting with Repos IV. Specialness and Supply

Financial Highlights

May 5, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Commercial Paper Issuance 2 Outstanding 2 Stocks and Bonds S&P and Dow Jones 3 VIX and MOVE volatility indices 3 European Debt Bond Spreads

May 5, 2010 Financial Highlights Federal Reserve Balance Sheet 1 Commercial Paper Issuance 2 Outstanding 2 Stocks and Bonds S&P and Dow Jones 3 VIX and MOVE volatility indices 3 European Debt Bond Spreads

MFE8825 Quantitative Management of Bond Portfolios

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

Economics Guided Notes Unit Six Day #1 Personal Finance Banking

Name: Date: Block # Economics Guided Notes Unit Six Day #1 Personal Finance Banking Directions Activity listen and view today s PowerPoint lesson. As you view each slide, write in any missing words or

Name: Date: Block # Economics Guided Notes Unit Six Day #1 Personal Finance Banking Directions Activity listen and view today s PowerPoint lesson. As you view each slide, write in any missing words or

CHAPTER 4 INTEREST RATES AND PRESENT VALUE

CHAPTER 4 INTEREST RATES AND PRESENT VALUE CHAPTER OBJECTIVES Once you have read this chapter you will understand what interest rates are, why economists delineate nominal from real interest rates, how

CHAPTER 4 INTEREST RATES AND PRESENT VALUE CHAPTER OBJECTIVES Once you have read this chapter you will understand what interest rates are, why economists delineate nominal from real interest rates, how

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT. AMIfs Institute July 18, 2016 Monday Afternoon Session

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT AMIfs Institute July 18, 2016 Monday Afternoon Session 1 Agenda - Introduction to ALM Monday, July 18 Afternoon Best Practices in ALM Structuring the ALCO Process

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT AMIfs Institute July 18, 2016 Monday Afternoon Session 1 Agenda - Introduction to ALM Monday, July 18 Afternoon Best Practices in ALM Structuring the ALCO Process

To and through Quantitative Easing

To and through Quantitative Easing Josh Howard, CFA Advanced Capital Group Goals for the Session Review interest rate environment of last years What the has Fed done, and what it can do How are borrowers

To and through Quantitative Easing Josh Howard, CFA Advanced Capital Group Goals for the Session Review interest rate environment of last years What the has Fed done, and what it can do How are borrowers

Operation Twist: 1961 vs. 2011

Amol Agrawal amol@stcipd.com +91-22-66202234 Operation Twist: 1961 vs. 2011 Ever since the crisis, Federal Reserve (and other central banks following Fed) has introduced new innovative measures to stimulate

Amol Agrawal amol@stcipd.com +91-22-66202234 Operation Twist: 1961 vs. 2011 Ever since the crisis, Federal Reserve (and other central banks following Fed) has introduced new innovative measures to stimulate

The following pages explain some commonly used bond terminology, and provide information on how bond returns are generated.

1 2 3 Corporate bonds play an important role in a diversified portfolio. The opportunity to receive regular income streams from corporate bonds can be appealing to investors, and the focus on capital preservation

1 2 3 Corporate bonds play an important role in a diversified portfolio. The opportunity to receive regular income streams from corporate bonds can be appealing to investors, and the focus on capital preservation

Financial Highlights

December 1, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 CMBS Delinquency Rates 4 Senior Loan Officer

December 1, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 CMBS Delinquency Rates 4 Senior Loan Officer

16. Foreign Exchange

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

TOPIC 5. Fed Policy and Money Markets

TOPIC 5 Fed Policy and Money Markets 1 2 Outline What is Money? What does affect the supply of Money? How the banking system works? What is the Fed and how does it work? What is a monetary policy? What

TOPIC 5 Fed Policy and Money Markets 1 2 Outline What is Money? What does affect the supply of Money? How the banking system works? What is the Fed and how does it work? What is a monetary policy? What

Financial Highlights

October 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad Financial

October 6, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Securitization Markets CMBS Yields and Issuance 3 ABX and CMBX 4 Mortgage Rates 5 Broad Financial

Predicting a US recession: has the yield curve lost its relevance?

Global Perspective Predicting a US recession: has the yield curve lost its relevance? For professional investor use only Asset Management August 2018 Executive summary It is becoming apparent the US economy

Global Perspective Predicting a US recession: has the yield curve lost its relevance? For professional investor use only Asset Management August 2018 Executive summary It is becoming apparent the US economy

The investment map that we will develop in this book works so well

CHAPTER 1 Demystifying the Investment World The investment map that we will develop in this book works so well because it is rooted in fundamental economics. These fundamentals will be our first screen

CHAPTER 1 Demystifying the Investment World The investment map that we will develop in this book works so well because it is rooted in fundamental economics. These fundamentals will be our first screen

Chapter 11 The Determination of Aggregate Output, the Price Level, and the Interest Rate

Principles of Macroeconomics Twelfth Edition Chapter 11 The Determination of Aggregate Output, the Price Level, and the Interest Rate Copyright 2017 Pearson Education, Inc. 11-1 Copyright 11-2 Chapter

Principles of Macroeconomics Twelfth Edition Chapter 11 The Determination of Aggregate Output, the Price Level, and the Interest Rate Copyright 2017 Pearson Education, Inc. 11-1 Copyright 11-2 Chapter

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 330 Spring 2016: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If a perpetuity has a price of $500 and an

Econ 330 Spring 2016: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If a perpetuity has a price of $500 and an

International Finance

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapt er. Key Concepts. Aggregate Supply1

Chapt er 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Aggregate Supply1 Key Concepts The aggregate supply/aggregate demand model is used to determine how real GDP and the price level are determined and why

Chapt er 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Aggregate Supply1 Key Concepts The aggregate supply/aggregate demand model is used to determine how real GDP and the price level are determined and why

FNCE 302, Investments H Guy Williams, Equilibrium Rates (how changes in world effect int rates)

") Overview Real vs. Nominal Rate (consumable vs. financial) Equilibrium Rates (how changes in world effect int rates) Structure of the Yield Curve (will review 3 theories) Some of the following material

Overview Real vs. Nominal Rate (consumable vs. financial) Equilibrium Rates (how changes in world effect int rates) Structure of the Yield Curve (will review 3 theories) Some of the following material

Lecture 11: The Demand for Money and the Price Level

Lecture 11: The Demand for Money and the Price Level See Barro Ch. 10 Trevor Gallen Spring, 2016 1 / 77 Where are we? Taking stock 1. We ve spent the last 7 of 9 chapters building up an equilibrium model

Lecture 11: The Demand for Money and the Price Level See Barro Ch. 10 Trevor Gallen Spring, 2016 1 / 77 Where are we? Taking stock 1. We ve spent the last 7 of 9 chapters building up an equilibrium model

The Yield Curve WHAT IT IS AND WHY IT MATTERS. UWA Student Managed Investment Fund ECONOMICS TEAM ALEX DYKES ARKA CHANDA ANDRE CHINNERY

The Yield Curve WHAT IT IS AND WHY IT MATTERS UWA Student Managed Investment Fund ECONOMICS TEAM ALEX DYKES ARKA CHANDA ANDRE CHINNERY What is it? The Yield Curve: What It Is and Why It Matters The yield

The Yield Curve WHAT IT IS AND WHY IT MATTERS UWA Student Managed Investment Fund ECONOMICS TEAM ALEX DYKES ARKA CHANDA ANDRE CHINNERY What is it? The Yield Curve: What It Is and Why It Matters The yield

Two examples demonstrate potential upside of leverage strategy, if your bank can stand the increase posed in interest rate risk

Leverage strategies: Is now the right time? Two examples demonstrate potential upside of leverage strategy, if your bank can stand the increase posed in interest rate risk By Michael Hambrick, Timothy

Leverage strategies: Is now the right time? Two examples demonstrate potential upside of leverage strategy, if your bank can stand the increase posed in interest rate risk By Michael Hambrick, Timothy

Term Structure of Interest Rates. For 9.220, Term 1, 2002/03 02_Lecture7.ppt

Term Structure of Interest Rates For 9.220, Term 1, 2002/03 02_Lecture7.ppt Outline 1. Introduction 2. Term Structure Definitions 3. Pure Expectations Theory 4. Liquidity Premium Theory 5. Interpreting

Term Structure of Interest Rates For 9.220, Term 1, 2002/03 02_Lecture7.ppt Outline 1. Introduction 2. Term Structure Definitions 3. Pure Expectations Theory 4. Liquidity Premium Theory 5. Interpreting

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

ECON Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2015 Answer sheet

Second Midterm Examination: Fall 2015 Answer sheet") ECON 311 - Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2015 Answer sheet YOUR NAME: Student ID: Circle the TA session you attend: INSTRUCTIONS: Chris 10AM Michael -

ECON 311 - Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2015 Answer sheet YOUR NAME: Student ID: Circle the TA session you attend: INSTRUCTIONS: Chris 10AM Michael -

ECON DISCUSSION NOTES ON CONTRACT LAW-PART 2. Contracts. I.1 Investment in Performance

ECON 522 - DISCUSSION NOTES ON CONTRACT LAW-PART 2 I Contracts I.1 Investment in Performance Investment in performance is investment to reduce the probability of breach. For example, suppose I decide to

ECON 522 - DISCUSSION NOTES ON CONTRACT LAW-PART 2 I Contracts I.1 Investment in Performance Investment in performance is investment to reduce the probability of breach. For example, suppose I decide to

Reach Out and Take This ARM! Financing with an Adjustable Rate Mortgage

Reach Out and Take This ARM! Financing with an Adjustable Rate Mortgage by Natalie Danielson email: clockhours@gmail.com www.clockhours.com A Washington State Approved Real Estate School under R.C.W. 18.85.

Reach Out and Take This ARM! Financing with an Adjustable Rate Mortgage by Natalie Danielson email: clockhours@gmail.com www.clockhours.com A Washington State Approved Real Estate School under R.C.W. 18.85.

Foundations of Finance

Lecture 9 Lecture 9: Theories of the Yield Curve. I. Reading. II. Expectations Hypothesis III. Liquidity Preference Theory. IV. Preferred Habitat Theory. Lecture 9: Bond Portfolio Management. V. Reading.

Lecture 9 Lecture 9: Theories of the Yield Curve. I. Reading. II. Expectations Hypothesis III. Liquidity Preference Theory. IV. Preferred Habitat Theory. Lecture 9: Bond Portfolio Management. V. Reading.

Lecture 8 Foundations of Finance

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Homework Assignment #6. Due Tuesday, 11/28/06. Multiple Choice Questions:

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

Homework Assignment #6. Due Tuesday, 11/28/06 Multiple Choice Questions: 1. When the inflation rate is expected to be zero, Steve plans to lend money if the interest rate is at least 4 percent a year and

18 INTERNATIONAL FINANCE* Chapter. Key Concepts

Chapter 18 INTERNATIONAL FINANCE* Key Concepts Financing International Trade The balance of payments accounts measure international transactions. Current account records exports, imports, net interest,

Chapter 18 INTERNATIONAL FINANCE* Key Concepts Financing International Trade The balance of payments accounts measure international transactions. Current account records exports, imports, net interest,

ECON 3303 Money and Banking Final Exam. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

RE CAPITAL GROUP PRIVATE LENDER PRESENTATION

RE CAPITAL GROUP www.recapitalgroup.net PRIVATE LENDER PRESENTATION Be The Bank! Become A Private Money Lender Invest In Real Estate For Guaranteed Returns of up to 12% Annually What Is Private Money Lending?

RE CAPITAL GROUP www.recapitalgroup.net PRIVATE LENDER PRESENTATION Be The Bank! Become A Private Money Lender Invest In Real Estate For Guaranteed Returns of up to 12% Annually What Is Private Money Lending?

SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT. 2) A bond is a security which typically offers a combination of two forms of payments:

A bond is a security which typically offers a combination of two forms of payments:") Solutions to Problem Set #: ) r =.06 or r =.8 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT PVA[T 0, r.06] j 0 $8000 $8000 { {.06} t.06 &.06 (.06) 0} $8000(7.36009) $58,880.70 > $50,000 PVA[T 0, r.8] $8000(4.49409)

Solutions to Problem Set #: ) r =.06 or r =.8 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT PVA[T 0, r.06] j 0 $8000 $8000 { {.06} t.06 &.06 (.06) 0} $8000(7.36009) $58,880.70 > $50,000 PVA[T 0, r.8] $8000(4.49409)

FEDERAL RESERVE statistical release

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks August 28, 2014 1. Factors Affecting Reserve Balances

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks August 28, 2014 1. Factors Affecting Reserve Balances

[Image of Investments: Analysis and Behavior textbook]

![[Image of Investments: Analysis and Behavior textbook]](/thumbs/83/88392803.jpg "[Image of Investments: Analysis and Behavior textbook]") Finance 527: Lecture 19, Bond Valuation V1 [John Nofsinger]: This is the first video for bond valuation. The previous bond topics were more the characteristics of bonds and different kinds of bonds. And

Finance 527: Lecture 19, Bond Valuation V1 [John Nofsinger]: This is the first video for bond valuation. The previous bond topics were more the characteristics of bonds and different kinds of bonds. And

ECON2123 TUT: AS-AD NOTE

ECON2123 TUT: AS-AD NOTE This note is preliminary, and subject to further revision. ding.dong@connect.ust.hk 1 AS-AD: Introduction 1.1 Supply and Demand In every commodity good market, there will be supply

ECON2123 TUT: AS-AD NOTE This note is preliminary, and subject to further revision. ding.dong@connect.ust.hk 1 AS-AD: Introduction 1.1 Supply and Demand In every commodity good market, there will be supply

Monetary Economics Fixed Income Securities Term Structure of Interest Rates Gerald P. Dwyer November 2015

Monetary Economics Fixed Income Securities Term Structure of Interest Rates Gerald P. Dwyer November 2015 Readings This Material Read Chapters 21 and 22 Responsible for part of 22.2, but only the material

Monetary Economics Fixed Income Securities Term Structure of Interest Rates Gerald P. Dwyer November 2015 Readings This Material Read Chapters 21 and 22 Responsible for part of 22.2, but only the material

Problem 3 Solutions. l 3 r, 1

. Economic Applications of Game Theory Fall 00 TA: Youngjin Hwang Problem 3 Solutions. (a) There are three subgames: [A] the subgame starting from Player s decision node after Player s choice of P; [B]

. Economic Applications of Game Theory Fall 00 TA: Youngjin Hwang Problem 3 Solutions. (a) There are three subgames: [A] the subgame starting from Player s decision node after Player s choice of P; [B]

Introduction to Interest Rate Trading. Andrew Wilkinson

Introduction to Interest Rate Trading Andrew Wilkinson Risk Disclosure Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures,

Introduction to Interest Rate Trading Andrew Wilkinson Risk Disclosure Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures,

Financial Risk Measurement/Management

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

FIN 6160 Investment Theory. Lecture 9-11 Managing Bond Portfolios

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

An old stock market saying is, "Bulls can make money, bears can make money, but pigs end up getting slaughtered.

In this lesson, you will learn about buying on margin and selling short. You will learn how buying on margin and selling short can increase potential gains on stock purchases, but at the risk of greater

In this lesson, you will learn about buying on margin and selling short. You will learn how buying on margin and selling short can increase potential gains on stock purchases, but at the risk of greater

UNDERSTANDING AND MANAGING OPTION RISK

UNDERSTANDING AND MANAGING OPTION RISK Daniel J. Dwyer Managing Principal Dwyer Capital Strategies L.L.C. Bloomington, MN dan@dwyercap.com 952-681-7920 August 9 & 10, 2018 Dwyer Capital Strategies L.L.C.

UNDERSTANDING AND MANAGING OPTION RISK Daniel J. Dwyer Managing Principal Dwyer Capital Strategies L.L.C. Bloomington, MN dan@dwyercap.com 952-681-7920 August 9 & 10, 2018 Dwyer Capital Strategies L.L.C.

The Leverage Cycle. John Geanakoplos

The Leverage Cycle John Geanakoplos Collateral Levels = Margins = Leverage From Irving Fisher in 890s and before it has been commonly supposed that the interest rate is the most important variable in the

The Leverage Cycle John Geanakoplos Collateral Levels = Margins = Leverage From Irving Fisher in 890s and before it has been commonly supposed that the interest rate is the most important variable in the