Global Imbalances. January 23rd

|

|

|

- Clinton Payne

- 5 years ago

- Views:

Transcription

1 Global Imbalances January 23rd

2 Fact #1: The US deficit is big

3 But there is little agreement on why, or on how much we should worry about it Global current account identity (CA = S-I = I*-S*) is a useful way of understanding the debate. The identity must hold; after all, it s an identity. But one can imagine that any one of the four components (S,I,S*,I*) could be driving the imbalance. Depending on which variable one emphasizes, the global imbalance may or may not be a problem. New economy view (emphasizing productivity of investment in US) says not. Inadequate US savings view (decline in household and gov savings) says it is. Global savings glut view (emphasizing rise in global saving since 1997) says not. Global investment strike view (emphasizing decline in investment in Japan since 1992 and Asia since ) says that it is.

4 What about the new economy view?

5 What about the new economy view? Yes, U.S. productivity growth, however measured, has risen to Europe s. The next slide shows this for labor productivity

6

7 Here is some additional detail

8 But there are also objections Labor productivity is rising at 6-7% per annum in China. Productivity is now picking up in Europe and Japan as well. Is it plausible that investors really believe that investments in the US will continue to outperform that in these other countries?

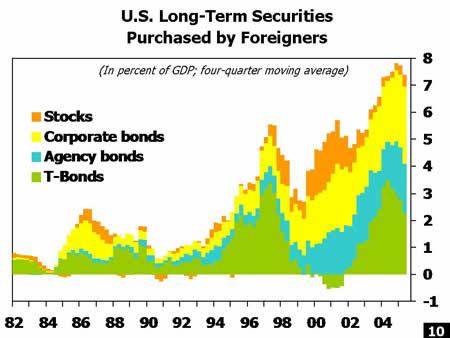

9 And there has been no investment surge in the United States. Since the collapse of the High Tech Bubble in 2000, foreign funds have been flowing mainly into debt, not into US stocks as this story would predict.

10

11 And the principle foreign investors have been foreign central banks, not private foreign investors. Indeed, so far as we can tell, foreign central banks have accounted for some 75 percent of finance for the US current account balance in recent years. All of this is a bit difficult to square with the New Economy story.

12 What about the inadequate US savings view? The fact that household savings rates have fallen to near zero is consistent with this emphasis. [See the next slide]

13 Yes, there has been a personal savings decline

14 Two objections to this emphasis on low U.S. savings Low household saving is the rational reaction to the high stock market and high housing prices. And the latter reflect the healthy fundamental condition of the US economy. But this assumes the validity of the new-economy argument. Household saving is not all that matters. Corporations save too, and corporate saving is at all-time highs. So the next graph shows a more comprehensive measure. It is still not all that reassuring. Note: Private +S&L adds State and Local Government (dis)saving to household and corporate saving. The other saving line then adds federal government (dis)saving. Thus, it is hard not to conclude that there is something to the inadequate U.S. savings view.

15

16 What about the foreign investment strike? It is true that European and Japanese investment have been stagnant, while Asian investment declined after 1997 (after the Asian financial crisis). The latter is not necessarily a bad thing, if you believe, as many do, that much of the investment of the prior period was relatively inefficient. But this generalization ignores China, where investment has been rising sharply.

17

18 Of course, S* has been rising faster than I* in China This brings us to the final high S* explanation. This is Chairman Bernanke s famous global savings glut story. With the world economy growing rapidly, there is lots of savings, outside the United States in particular. It has to go somewhere, and it flows toward the U.S., financing our current account deficit. This story has the singular merit of explaining how it could be that even though the U.S. is running big deficits, global interest rates are low. But the data do not obviously bear it out.

19 If the data were perfect, the two lines could have to coincide. But they do not obviously point to excess global savings as the driving force.

20 Where does this leave us? It is probably less appropriate to talk about a global saving glut than a regional saving shift, down in the US, up in the rest of the world. US investment has held steady, while investment has declined modestly in the rest of the world from mid-1990s levels. Foreigners thus may be willing to park some of their savings, of which they have many, in the U.S. To the extent that this is the driving force, external deficits at the current level are sustainable and benign. To the extent that investors portfolios have been inadequately diversified internationally, financial globalization points in the same direction. But the global imbalance is also being driven by the failure of Americans to finance investment in their economy out of their own savings. To the extent that this is the driving force, external deficits at the current level are not sustainable and benign. This eclectic view would then suggest that the U.S. can support a higher external debt/gdp ratio than before, but not without limit. U.S. debt/gdp ratio is currently on the order of 25 per cent. A consensus view would be that, in the future, levels as high as 50 per cent might be feasible.

21 So what kind of adjustment is needed? What adjustments will be needed to stabilize US debt at 50% of GDP? In equilibrium, n = c/g Where c = deficit/gnp, g = nominal growth If g = 0.05, then c has to fall to Thus, the deficit has to fall by 4 percentage points of GDP. And this will require the $ to fall by some 40 %. The rule of thumb economists use is that a 10% fall in the dollar produces a 1% of US GDP improvement in the current account Optimists would note that the dollar has fallen by 20 % since 2002, and argue that half the adjustment is already in the pipeline. Do recent data suggest this?

22 Aside: how does a falling dollar improve the savings/investment balance?

23 Aside: how does a falling dollar improve the savings/investment balance? Falling dollar raises import prices Higher inflation forces the Fed to normalize interest rates (as we have seen) Higher interest rates mean higher costs of borrowing for households, lower housing prices (as we have seen), less of a tendency for households to use their homes and ATM machines. Lower consumption means more saving. The less happy side for growth is that less consumption demand and higher financing costs also mean less investment. Both more saving and less investment means a stronger U.S. current account, but likely at the cost of a US recession.

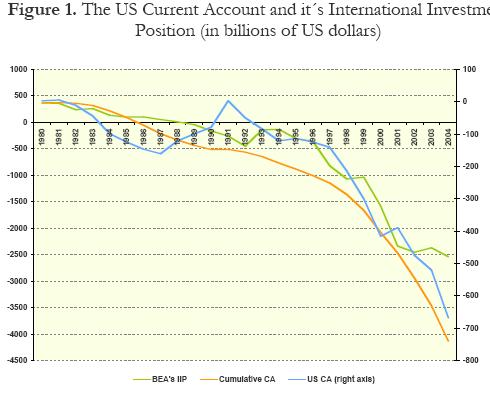

24 Aside: dark matter But, if you looked at Figure 1 of the Chinn article, you will see that the US current account has moved into deep deficit recently without also increasing US net foreign debt.

25

26 Why is this? The current account really isn t in deficit. There is something unmeasured holding it together (like dark matter holding together the universe). Unmeasured earnings from the value of US brands (Disney, Apple etc.). There is a deficit, but since US foreign liabilities are in dollars while our foreign assets are in, inter alia, euros, when the dollar loses value we enjoy capital gains and they suffer capital losses. In other words, the balance sheet effects work in our favor. Is this plausible? And will it continue?

27 Won t foreigners catch on? Won t they demand that we borrow from them in their own currencies? This will occur, in practice, by their diversifying out of existing dollar balances. If so, balance sheet effects won t automatically work in our favor. On these and other grounds, I am inclined to dismiss the reassuring dark matter view.

28 If so, the dollar must fall by at least another 20% US trade with Asia equals US trade with Europe to a first approximation. So this can be accomplished either by: A 20% fall against both the euro and Asian currencies Or a 10% fall against the euro and a 30% fall against Asian currencies (more appropriate given the strength of their respective economies). But it implies a brutal 40% appreciation of the euro against the dollar if Asian currencies don t move. And whether Asian currencies move hinges on what the big dog, China, does.

29 China objects: Its economy is growing at capacity Social stability requires moving 10 million peasants a year into the modern manufacturing sector. And that means growing exports by 20% per annum. It lacks the sophisticated financial markets and hedging instruments needed to cope with a variable exchange rate. Significantly greater flexibility, in the Chinese view, should wait on the development of deeper and more sophisticated financial markets.

30 But is the RMB in fact undervalued? Economists, not for the first time, don t agree. They take two approaches to answering this question:

31 So is the RMB undervalued? Economists take two approaches to answering this question: The simple or augmented PPP approach The external balance approach Everyone knows what these are?

32 Simple PPP approach P = e P* should hold in equilibrium If P is 10% lower than ep*, then the currency is 10% undervalued.

33 But are there problems with the simple PPP approach?

34 But are there problems with the simple PPP approach? Absolute PPP plausibly holds for traded goods. But not for traded goods. The cost of a shoeshine or a haircut in India is much lower than the cost of a shoeshine or haircut in America. Everyone understands why? This tendency for the price of nontraded goods to be higher where incomes are higher even has its own name, the Balassa-Samuelson effect. But how much higher? How do Chinn et al. attempt to answer this?

35 They use the augmented PPP approach They regress P/eP* on Y PC / Y PC * This then generates the typical ( equilibrium ) relationship. Then look to see by how much a country deviates from that to judge by how far its currency is out of equilibrium.

36 Here s the typical relationship (solid line), 1 & 2 s.e. bands, and actual for China. So they conclude: China s currency is 40% too low

37 What s wrong with this picture?

38 What s wrong with this picture? Answer depends on your null hypothesis. China is still within the 2 s.e. bands We also cannot reject the null that the renminbi is 0% undervalued. So the test is at best very weak.

39 What else is wrong with this picture?

40 What else is wrong with this picture? The test assumes that nothing besides relative incomes affects relative prices. In particular, as the authors acknowledge (you will have had to be a careful reader to find the footnote), it assumes external balance (that current accounts are in equilibrium). And the current account balance between the US and China is, in fact, far from zero.

41 So is it possible to augment the augmented PPP approach to take this fact on board?

42 So is it possible to augment the augmented PPP approach to take this fact on board? Imagine regressing P/eP* on Y PC / Y PC * and also on the Current Account Balance. But the CAB and relative prices are simultaneously determined. So estimating this relationship is easier said than done. (Doing so requires an instrument. Might be an interesting subject for a final paper for this course. I have the authors data set if you d like to try.)

43 Alternative is the external balance approach We have already seen how this works. You make assumptions about: By how much a 10% depreciation of the dollar will improve the U.S. CA deficit (recall: typically, economists assume by 1% of US GDP) What CA/GDP ratio is sustainable for the US Recall: typically economists assume 2.5%, since together with nominal income growth of 5% this yields a 50% debt/gdp ratio in equilibrium.

44 Reminder of the underlying arithmetic In equilibrium: n = c/g, where: n = ratio of net external debt relative to GDP 50% would be a very high ratio for a country like the United States. We have never seen a large country with a ratio that high during peacetime. c = current account deficit relative to GDP g = nominal growth rate of the economy So if g=5 (3% growth + 2% inflation), we must cut the deficit to 2 1/2% of GDP from its current 6 ½ per cent

45 Then to cut the U.S. deficit ratio by 4 points, the dollar has to fall by 40% (hopefully, only an additional 20%, since 20% has already occurred). Note that now we are talking about the dollar s value against all foreign currencies (its trade weighted value ), and not just its value against the renminbi. But for the reasons just described, it is hard to imagine that we will see a smooth adjustment without Chinese participation.

46 So what should the Chinese do? Move more quickly in the direction of greater flexibility, and let the renminbi appreciation. Realize that the financial market development they prize responds to asset market flexibility (it is not merely a precondition). That is a lesson of Japanese experience in the 1970s. And if China moves, the rest of Asia can continue moving. The entire burden will not fall, in this case on Europe. Meanwhile, China and other Asian countries can stimulate demand. And one can then at least hold out hope for the possibility of smooth rebalancing of the global economy.

Period 3 MBA Program January February MACROECONOMICS IN THE GLOBAL ECONOMY Core Course. Professor Ilian Mihov

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Lecture #8: How Scary is the US Trade Deficit?

Parsons, 2007 Lecture #8: How Scary is the US Trade Deficit? First, the facts: How big IS the US deficit? Well, if we look at the current account, whose largest component is the trade deficit, it was about

Parsons, 2007 Lecture #8: How Scary is the US Trade Deficit? First, the facts: How big IS the US deficit? Well, if we look at the current account, whose largest component is the trade deficit, it was about

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

vox Research-based policy analysis and commentary from leading economists

vox Research-based policy analysis and commentary from leading economists On the renminbi and economic convergence Helmut Reisen 17 December 2009 Must China let its exchange rate appreciate to reduce global

vox Research-based policy analysis and commentary from leading economists On the renminbi and economic convergence Helmut Reisen 17 December 2009 Must China let its exchange rate appreciate to reduce global

How Is Global Trade Financed? (EA)

") How Is Global Trade Financed? (EA) For countries to trade goods and services, they must also trade their currencies. If you have ever visited a foreign country, such as Mexico, you know that you must exchange

How Is Global Trade Financed? (EA) For countries to trade goods and services, they must also trade their currencies. If you have ever visited a foreign country, such as Mexico, you know that you must exchange

How Successful is China s Economic Rebalancing?*

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

China might NEVER become the biggest

China might NEVER become the biggest economy in the world It is often assumed that given China s remarkable growth rates over the past three decades around 10% real GDP per year China is on the way to

China might NEVER become the biggest economy in the world It is often assumed that given China s remarkable growth rates over the past three decades around 10% real GDP per year China is on the way to

Is The Market Predicting A Recession?

Is The Market Predicting A Recession? October 25, 2018 by Lance Roberts of Real Investment Advice There has been lot s of analysis lately on what message the recent gyrations in the market are sending.

Is The Market Predicting A Recession? October 25, 2018 by Lance Roberts of Real Investment Advice There has been lot s of analysis lately on what message the recent gyrations in the market are sending.

Econ 340. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Outline: Exchange Rates

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

Global Imbalances and the Financial Crisis: Products of Common Causes

179 Commentary Global Imbalances and the Financial Crisis: Products of Common Causes Jacob Frenkel As you indicated, this paper has two discussants, and I m the last one. So, when I saw what Maury presented

179 Commentary Global Imbalances and the Financial Crisis: Products of Common Causes Jacob Frenkel As you indicated, this paper has two discussants, and I m the last one. So, when I saw what Maury presented

The role of central banks and governments in the crisis

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

Preface to Global imbalances. Is the world economy really at risk?, by Anton Brender and Florence Pisani

Preface to Global imbalances. Is the world economy really at risk?, by Anton Brender and Florence Pisani Olivier Blanchard February 20, 2007 If, twenty years ago, you had asked economists whether globalization

Preface to Global imbalances. Is the world economy really at risk?, by Anton Brender and Florence Pisani Olivier Blanchard February 20, 2007 If, twenty years ago, you had asked economists whether globalization

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

The Final Round 1 Everett Rutan Xavier High School or A Note about the Notes.

The Final Round 1 Everett Rutan Xavier High School everett.rutan@moodys.com or ejrutan3@acm.org Connecticut Debate Association Darien High School and Glastonbury High School March 8, 2008 Resolved: In

The Final Round 1 Everett Rutan Xavier High School everett.rutan@moodys.com or ejrutan3@acm.org Connecticut Debate Association Darien High School and Glastonbury High School March 8, 2008 Resolved: In

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

FIRST LOOK AT MACROECONOMICS*

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

The Global Recession of 2016

INTERVIEW BARRON S The Global Recession of 2016 Forecaster David Levy sees a spreading global recession intensifying and ultimately engulfing the world s economies By LAWRENCE C. STRAUSS December 19, 2015

INTERVIEW BARRON S The Global Recession of 2016 Forecaster David Levy sees a spreading global recession intensifying and ultimately engulfing the world s economies By LAWRENCE C. STRAUSS December 19, 2015

DEVELOPING COUNTRIES AND THE DOLLAR. C. P. Chandrasekhar and Jayati Ghosh

DEVELOPING COUNTRIES AND THE DOLLAR C. P. Chandrasekhar and Jayati Ghosh It is now generally recognised that the very large macroeconomic imbalances between the US and the rest of the world, which are

DEVELOPING COUNTRIES AND THE DOLLAR C. P. Chandrasekhar and Jayati Ghosh It is now generally recognised that the very large macroeconomic imbalances between the US and the rest of the world, which are

LECTURE XIII. 30 July Monday, July 30, 12

LECTURE XIII 30 July 2012 TOPIC 15 Exchange Rates BIG PICTURE How do we evaluate currency across countries? How is the exchange rate determined? What is the relationship of the foreign exchange market

LECTURE XIII 30 July 2012 TOPIC 15 Exchange Rates BIG PICTURE How do we evaluate currency across countries? How is the exchange rate determined? What is the relationship of the foreign exchange market

Lecture 7. Unemployment and Fiscal Policy

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Global Imbalances and the U.S. Current Account Deficit. Economics 826 January 2009

Global Imbalances and the U.S. Current Account Deficit Economics 826 January 2009 1 A. What are the facts? B. Why is this trend worrying? C. What are the possible causes? D. What are the possible adjustments?

Global Imbalances and the U.S. Current Account Deficit Economics 826 January 2009 1 A. What are the facts? B. Why is this trend worrying? C. What are the possible causes? D. What are the possible adjustments?

1. Inflation target policy how does it work?

Mr. Heikensten discusses recent economic and monetary policy developments in Sweden Speech by the Deputy Governor of the Bank of Sweden, Mr. Lars Heikensten, at the Local Authorities Economics Seminar

Mr. Heikensten discusses recent economic and monetary policy developments in Sweden Speech by the Deputy Governor of the Bank of Sweden, Mr. Lars Heikensten, at the Local Authorities Economics Seminar

General Discussion: Overview

General Discussion: Overview Chair: Erkki Liikanen Mr. Rajan: Mr. Feldstein, you offered an explanation for our paper. I didn t know if you thought there was a difference between your explanation and ours.

General Discussion: Overview Chair: Erkki Liikanen Mr. Rajan: Mr. Feldstein, you offered an explanation for our paper. I didn t know if you thought there was a difference between your explanation and ours.

Objectives for Chapter 24: Monetarism (Continued) Chapter 24: The Basic Theory of Monetarism (Continued) (latest revision October 2004)

Chapter 24: The Basic Theory of Monetarism (Continued) (latest revision October 2004)") 1 Objectives for Chapter 24: Monetarism (Continued) At the end of Chapter 24, you will be able to answer the following: 1. What is the short-run? 2. Use the theory of job searching in a period of unanticipated

1 Objectives for Chapter 24: Monetarism (Continued) At the end of Chapter 24, you will be able to answer the following: 1. What is the short-run? 2. Use the theory of job searching in a period of unanticipated

Implications of Fiscal Austerity for U.S. Monetary Policy

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

MEETING OF SHAREHOLDERS SCOTIABANK TRINIDAD AND TOBAGO LIMITED CROWNE PLAZA JANUARY

ADDRESS DELIVERED BY ROB PITFIELD, CHAIRMAN THE 36 th ANNUAL MEETING OF SHAREHOLDERS SCOTIABANK TRINIDAD AND TOBAGO LIMITED CROWNE PLAZA JANUARY 26 th 2006 It s a pleasure to be here today to celebrate

ADDRESS DELIVERED BY ROB PITFIELD, CHAIRMAN THE 36 th ANNUAL MEETING OF SHAREHOLDERS SCOTIABANK TRINIDAD AND TOBAGO LIMITED CROWNE PLAZA JANUARY 26 th 2006 It s a pleasure to be here today to celebrate

Ric Battellino: Recent financial developments

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

Normalizing Monetary Policy

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

CurrencyShares Japanese Yen Trust (FXY)

") 1 of 5 11/13/2008 3:23 PM CurrencyShares Japanese Yen Trust (FXY) This ETF tracks the value of the yen against the U.S. dollar. $101.85-3.33 (-3.17%) 11/13/2008 3:59 PM FXY is one of our BUY FIRST stocks!

1 of 5 11/13/2008 3:23 PM CurrencyShares Japanese Yen Trust (FXY) This ETF tracks the value of the yen against the U.S. dollar. $101.85-3.33 (-3.17%) 11/13/2008 3:59 PM FXY is one of our BUY FIRST stocks!

Final Exam: 14 Dec 2004 Econ 200 David Reiley

Your Name: Final Exam: 14 Dec 2004 Econ 200 David Reiley You have 120 minutes to take this exam. There are a total of 100 points possible, on 5 multiple-choice questions, and 2 multi-part essay questions.

Your Name: Final Exam: 14 Dec 2004 Econ 200 David Reiley You have 120 minutes to take this exam. There are a total of 100 points possible, on 5 multiple-choice questions, and 2 multi-part essay questions.

Lecture 13: The Equity Premium

Lecture 13: The Equity Premium October 27, 2016 Prof. Wyatt Brooks Types of Assets This can take many possible forms: Stocks: buy a fraction of a corporation Bonds: lend cash for repayment in the future

Lecture 13: The Equity Premium October 27, 2016 Prof. Wyatt Brooks Types of Assets This can take many possible forms: Stocks: buy a fraction of a corporation Bonds: lend cash for repayment in the future

China: Double, Double Toil and Trouble/Fire Burn, and Cauldron Bubble?

China: Double, Double Toil and Trouble/Fire Burn, and Cauldron Bubble? September 15, 2015 by Andy Rothman of Matthews Asia September 10, 2015 China s economy is seemingly in turmoil. Markets are down,

China: Double, Double Toil and Trouble/Fire Burn, and Cauldron Bubble? September 15, 2015 by Andy Rothman of Matthews Asia September 10, 2015 China s economy is seemingly in turmoil. Markets are down,

Closed vs. Open Economies

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

History and Current Situation Policies Adopted Opinions Conclusion

LOGO Group 8 The Exchange Rate Regime & International Trade in China over a long run Leith Ben Anne Luna Camille Daniel A short video =D Contents 1 History and Current Situation 2 Policies Adopted 3 Opinions

LOGO Group 8 The Exchange Rate Regime & International Trade in China over a long run Leith Ben Anne Luna Camille Daniel A short video =D Contents 1 History and Current Situation 2 Policies Adopted 3 Opinions

Global Imbalances and Latin America: A Comment on Eichengreen and Park

3 Global Imbalances and Latin America: A Comment on Eichengreen and Park Barbara Stallings I n Global Imbalances and Emerging Markets, Barry Eichengreen and Yung Chul Park make a number of important contributions

3 Global Imbalances and Latin America: A Comment on Eichengreen and Park Barbara Stallings I n Global Imbalances and Emerging Markets, Barry Eichengreen and Yung Chul Park make a number of important contributions

ECMC49S Midterm. Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100

ECMC49S Midterm Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [10 marks] (i) State the Fisher Separation Theorem

ECMC49S Midterm Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [10 marks] (i) State the Fisher Separation Theorem

Petrodollars, the Savings Bust, and the U.S. Current Account Deficit

GLOBAL PERSPECTIVES Petrodollars, the Savings Bust, and the U.S. Current Account Deficit March 2007 International finance is a fascinating but challenging subject with many moving Richard H. Clarida Global

GLOBAL PERSPECTIVES Petrodollars, the Savings Bust, and the U.S. Current Account Deficit March 2007 International finance is a fascinating but challenging subject with many moving Richard H. Clarida Global

Renminbi Internationalization in Light of Recent Turbulence. Barry Eichengreen

Renminbi Internationalization in Light of Recent Turbulence Barry Eichengreen Renminbi Internationalization Lots of talk 76,000 unique Google hits the last time I looked. But how are they doing? (Curb

Renminbi Internationalization in Light of Recent Turbulence Barry Eichengreen Renminbi Internationalization Lots of talk 76,000 unique Google hits the last time I looked. But how are they doing? (Curb

Jeremy Siegel on Dow 15,000 By Robert Huebscher December 18, 2012

Jeremy Siegel on Dow 15,000 By Robert Huebscher December 18, 2012 Jeremy Siegel is the Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania and a Senior Investment

Jeremy Siegel on Dow 15,000 By Robert Huebscher December 18, 2012 Jeremy Siegel is the Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania and a Senior Investment

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System FAN Gang National Economic Research Institute China Reform Foundation May 2006 1.China s trade balance In most of past

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System FAN Gang National Economic Research Institute China Reform Foundation May 2006 1.China s trade balance In most of past

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

(1) UIP : R = R f + Ee E

UIP : R = R f + Ee E") Christiano 362, Winter 2003 February 3 and 5 Lecture #9 and 10: Making Y Endogenous in Short Run, and Integrating Short and Long Run Up to now, we have assumed that Y is exogenous in the short and the

Christiano 362, Winter 2003 February 3 and 5 Lecture #9 and 10: Making Y Endogenous in Short Run, and Integrating Short and Long Run Up to now, we have assumed that Y is exogenous in the short and the

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies Remarks by Mr Masaaki Shirakwa, Governor of the Bank of Japan, at the Bank

Masaaki Shirakawa: The transition from high growth to stable growth Japan s experience and implications for emerging economies Remarks by Mr Masaaki Shirakwa, Governor of the Bank of Japan, at the Bank

Gauging Current Conditions:

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

Comments on Foreign Effects of Higher U.S. Interest Rates. James D. Hamilton. University of California at San Diego.

1 Comments on Foreign Effects of Higher U.S. Interest Rates James D. Hamilton University of California at San Diego December 15, 2017 This is a very interesting and ambitious paper. The authors are trying

1 Comments on Foreign Effects of Higher U.S. Interest Rates James D. Hamilton University of California at San Diego December 15, 2017 This is a very interesting and ambitious paper. The authors are trying

Growth and Value Investing: A Complementary Approach

Growth and Value Investing: A Complementary Approach March 14, 2018 by Stephen Dover, Norman Boersma of Franklin Templeton Investments Growth and value investing are often seen as competing styles, with

Growth and Value Investing: A Complementary Approach March 14, 2018 by Stephen Dover, Norman Boersma of Franklin Templeton Investments Growth and value investing are often seen as competing styles, with

Figure 0.1 US current account balance as percent of GDP,

Overview The United States has once again entered into a period of large external imbalances. This time, the current account deficit, at nearly 6 percent of GDP in 2004, is much larger than during the

Overview The United States has once again entered into a period of large external imbalances. This time, the current account deficit, at nearly 6 percent of GDP in 2004, is much larger than during the

International Finance

Terminology International Finance Chris Edmond NYU Stern Spring 2008 Trade balance balance on merchandise trade ( goods ) balance on goods and services ( net exports ) Current account balance current account

Terminology International Finance Chris Edmond NYU Stern Spring 2008 Trade balance balance on merchandise trade ( goods ) balance on goods and services ( net exports ) Current account balance current account

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Fund Management Diary

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY Annenberg Foundation & Educational Film Center

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY ECONOMICS U$A: 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY (MUSIC PLAYS) ANNOUNCER: FUNDING FOR THIS PROGRAM WAS PROVIDED BY ANNENBERG

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY ECONOMICS U$A: 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY (MUSIC PLAYS) ANNOUNCER: FUNDING FOR THIS PROGRAM WAS PROVIDED BY ANNENBERG

What Should the Fed Do?

Peterson Perspectives Interviews on Current Topics What Should the Fed Do? Joseph E. Gagnon and Michael Mussa discuss the latest steps by the Federal Reserve to help the economy and what tools might be

Peterson Perspectives Interviews on Current Topics What Should the Fed Do? Joseph E. Gagnon and Michael Mussa discuss the latest steps by the Federal Reserve to help the economy and what tools might be

Tactical Gold Allocation Within a Multi-Asset Portfolio

Tactical Gold Allocation Within a Multi-Asset Portfolio Charles Morris Head of Global Asset Management, HSBC Introduction Thank you, John, for that kind introduction. Ladies and gentlemen, my name is Charlie

Tactical Gold Allocation Within a Multi-Asset Portfolio Charles Morris Head of Global Asset Management, HSBC Introduction Thank you, John, for that kind introduction. Ladies and gentlemen, my name is Charlie

FORECAST OF OREGON S ECONOMY IN 2013: DISAPPOINTING BUT NOT DISASTROUS

FORECAST OF OREGON S ECONOMY IN 2013: DISAPPOINTING BUT NOT DISASTROUS ERIC FRUITS Editor and Adjunct Professor, Portland State University During a recent presentation that I made to the Roseburg Chamber

FORECAST OF OREGON S ECONOMY IN 2013: DISAPPOINTING BUT NOT DISASTROUS ERIC FRUITS Editor and Adjunct Professor, Portland State University During a recent presentation that I made to the Roseburg Chamber

Bruce Greenwald: The Crisis Bigger than Global Warming

Bruce Greenwald: The Crisis Bigger than Global Warming April 26, 2016 by Robert Huebscher Manufacturing is dying on a global basis, according to Bruce Greenwald, and its collapse will mean the demise of

Bruce Greenwald: The Crisis Bigger than Global Warming April 26, 2016 by Robert Huebscher Manufacturing is dying on a global basis, according to Bruce Greenwald, and its collapse will mean the demise of

Macroeconomics: Principles, Applications, and Tools

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 17 Macroeconomic Policy Debates Learning Objectives 17.1 List the benefits and the costs for a country of running a deficit. 17.2

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 17 Macroeconomic Policy Debates Learning Objectives 17.1 List the benefits and the costs for a country of running a deficit. 17.2

The Real Problem was Nominal: How the Crash of 2008 was Misdiagnosed. Scott Sumner, Bentley University

The Real Problem was Nominal: How the Crash of 2008 was Misdiagnosed Scott Sumner, Bentley University A Contrarian View The great crash of 2008 does not discredit the Efficient Markets Hypothesis; indeed

The Real Problem was Nominal: How the Crash of 2008 was Misdiagnosed Scott Sumner, Bentley University A Contrarian View The great crash of 2008 does not discredit the Efficient Markets Hypothesis; indeed

Bretton Woods II: The Reemergence of the Bretton Woods System

Bretton Woods II: The Reemergence of the Bretton Woods System by Teresa M. Foy January 28, 2005 Department of Economics, Queen s University, Kingston, Ontario, Canada, K7L 3N6. foyt@qed.econ.queensu.ca,

Bretton Woods II: The Reemergence of the Bretton Woods System by Teresa M. Foy January 28, 2005 Department of Economics, Queen s University, Kingston, Ontario, Canada, K7L 3N6. foyt@qed.econ.queensu.ca,

An interim assessment

What is the economic outlook for OECD countries? An interim assessment Paris, 5 April 2011 11h Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General 1. The news has of course been

What is the economic outlook for OECD countries? An interim assessment Paris, 5 April 2011 11h Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General 1. The news has of course been

10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapt er. Key Concepts. Aggregate Supply1

Chapt er 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Aggregate Supply1 Key Concepts The aggregate supply/aggregate demand model is used to determine how real GDP and the price level are determined and why

Chapt er 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Aggregate Supply1 Key Concepts The aggregate supply/aggregate demand model is used to determine how real GDP and the price level are determined and why

Are we on the road to recovery?

Are we on the road to recovery? Transcript Catherine Gordon: Hi, I m Catherine Gordon. We re here with Joe Davis, Vanguard s chief economist, to talk about economic trends and the outlook for the rest

Are we on the road to recovery? Transcript Catherine Gordon: Hi, I m Catherine Gordon. We re here with Joe Davis, Vanguard s chief economist, to talk about economic trends and the outlook for the rest

Trade led Growth in Times of Crisis Asia Pacific Trade Economists Conference 2 3 November 2009, Bangkok. Session 1

Trade led Growth in Times of Crisis Asia Pacific Trade Economists Conference 2 3 November 2009, Bangkok Session 1 Do We Need a New Approach to Trade? Alan V. Deardorff Asia Pacific Research and Training

Trade led Growth in Times of Crisis Asia Pacific Trade Economists Conference 2 3 November 2009, Bangkok Session 1 Do We Need a New Approach to Trade? Alan V. Deardorff Asia Pacific Research and Training

EFN REPORT. ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Autumn 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

EFN REPORT ECONOMIC OUTLOOK FOR THE EURO AREA IN 2015 and 2016 Autumn 2015 1 About the European ing Network The European ing Network (EFN) is a research group of European institutions, founded in 2001

Yen and Yuan RIETI, Tokyo

Yen and Yuan RIETI, Tokyo November 2, 21 In the first half of his talk, Dr. Kwan, senior fellow at RIETI, argued that Asian currencies should be pegged to a currency basket, with the Japanese yen comprising

Yen and Yuan RIETI, Tokyo November 2, 21 In the first half of his talk, Dr. Kwan, senior fellow at RIETI, argued that Asian currencies should be pegged to a currency basket, with the Japanese yen comprising

conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006

the BRIC economies: conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006 introduction Global Monetary Easing in 2001 3 Fuels consumer boom in West (esp. USA) Fuels investment boom

the BRIC economies: conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006 introduction Global Monetary Easing in 2001 3 Fuels consumer boom in West (esp. USA) Fuels investment boom

On Abenomics and the Japanese Economy. Motoshige Itoh Member, Council on Economic and Fiscal Policy and Professor, University of Tokyo

On Abenomics and the Japanese Economy Motoshige Itoh Member, Council on Economic and Fiscal Policy and Professor, University of Tokyo The purpose of this brief overview is to summarize some of the major

On Abenomics and the Japanese Economy Motoshige Itoh Member, Council on Economic and Fiscal Policy and Professor, University of Tokyo The purpose of this brief overview is to summarize some of the major

The Future of European and Asian Economy after the Euro-zone Crisis

The Future of European and Asian Economy after the Euro-zone Crisis 16 January 2013 John Junggun Oh Korea University ojunggun@korea.ac.kr Contents Impacts of Euro-zone Crisis and Future Prospects on the

The Future of European and Asian Economy after the Euro-zone Crisis 16 January 2013 John Junggun Oh Korea University ojunggun@korea.ac.kr Contents Impacts of Euro-zone Crisis and Future Prospects on the

The yellow highlighted areas are bear markets with NO recession.

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Econ 98- Chiu Spring 2005 Final Exam Review: Macroeconomics

Disclaimer: The review may help you prepare for the exam. The review is not comprehensive and the selected topics may not be representative of the exam. In fact, we do not know what will be on the exam.

Disclaimer: The review may help you prepare for the exam. The review is not comprehensive and the selected topics may not be representative of the exam. In fact, we do not know what will be on the exam.

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Midterm Exam I: Answer Sheet

Economics 434 Spring 1999 Dr. Ickes Midterm Exam I: Answer Sheet Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently given the price

Economics 434 Spring 1999 Dr. Ickes Midterm Exam I: Answer Sheet Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently given the price

CHINA S DIRECTION IN What is the Risk of a Debt Crisis?

Sinology by Andy Rothman January 18, 2018 a In 2018, I expect China s economy to return to the long-term trend of gradual deceleration, while remaining one of the world s fastestgrowing economies. a China

Sinology by Andy Rothman January 18, 2018 a In 2018, I expect China s economy to return to the long-term trend of gradual deceleration, while remaining one of the world s fastestgrowing economies. a China

FED TAPERING FISCAL & REVENUE DEFICITS

FED TAPERING FISCAL & REVENUE DEFICITS The Finance Minister announced a 4.8 per cent revenue deficit and 6.8 per cent fiscal deficit in the Union Budget this week! So is that good or bad? What does Fiscal

FED TAPERING FISCAL & REVENUE DEFICITS The Finance Minister announced a 4.8 per cent revenue deficit and 6.8 per cent fiscal deficit in the Union Budget this week! So is that good or bad? What does Fiscal

CRS Report for Congress

Order Code RS21625 Updated March 17, 2006 CRS Report for Congress Received through the CRS Web China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and

Order Code RS21625 Updated March 17, 2006 CRS Report for Congress Received through the CRS Web China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and

Chi on China Up or Down? The Knowns and Unknowns of the RMB New Normal

For professional investors 28 January 2015 1 Chi on China Up or Down? The Knowns and Unknowns of the RMB New Normal SUMMARY The knowns: China s renminbi (RMB) has entered a new normal environment characterised

For professional investors 28 January 2015 1 Chi on China Up or Down? The Knowns and Unknowns of the RMB New Normal SUMMARY The knowns: China s renminbi (RMB) has entered a new normal environment characterised

Chi on China RMB Undervaluation, Déjà vu

For professional investors 26 February 2014 1 Chi on China RMB Undervaluation, Déjà vu SUMMARY The fall in China s current account surplus in recent years has not resulted from a genuine change in the

For professional investors 26 February 2014 1 Chi on China RMB Undervaluation, Déjà vu SUMMARY The fall in China s current account surplus in recent years has not resulted from a genuine change in the

Game-Changers in the Era of Dissonance

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

Exchange Rate Regimes and Structural Realignment of Global Economies. Comments from an Asian perspective

Exchange Rate Regimes and Structural Realignment of Global Economies Comments from an Asian perspective Yozo Nishimura Institute for International Monetary Affairs November 17, 2009 Tokyo IIMA 1 Main points

Exchange Rate Regimes and Structural Realignment of Global Economies Comments from an Asian perspective Yozo Nishimura Institute for International Monetary Affairs November 17, 2009 Tokyo IIMA 1 Main points

China Warms to a More Flexible Yuan

Page 1 of 5 This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com. http://www.wsj.com/articles/china-warms-to-a-more-flexible-yuan-1418811977

Page 1 of 5 This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com. http://www.wsj.com/articles/china-warms-to-a-more-flexible-yuan-1418811977

Federal Budget Policy with an Aging Population and Persistently Low Interest Rates. Douglas Elmendorf and Louise Sheiner February 5, 2016

Federal Budget Policy with an Aging Population and Persistently Low Interest Rates Douglas Elmendorf and Louise Sheiner February 5, 2016 Key considerations Recent surge in debt Debt/GDP projected to rise

Federal Budget Policy with an Aging Population and Persistently Low Interest Rates Douglas Elmendorf and Louise Sheiner February 5, 2016 Key considerations Recent surge in debt Debt/GDP projected to rise

Monetary Policy and the Expanded Loanable Funds Model

Monetary Policy and the Expanded Loanable Funds Model R.J. Barbera Why were central banks created? The Bank of England, one of the first central banks, focused upon preventing financial crises. The simple

Monetary Policy and the Expanded Loanable Funds Model R.J. Barbera Why were central banks created? The Bank of England, one of the first central banks, focused upon preventing financial crises. The simple

Finance 527: Lecture 27, Market Efficiency V2

Finance 527: Lecture 27, Market Efficiency V2 [John Nofsinger]: Welcome to the second video for the efficient markets topic. This is gonna be sort of a real life demonstration about how you can kind of

Finance 527: Lecture 27, Market Efficiency V2 [John Nofsinger]: Welcome to the second video for the efficient markets topic. This is gonna be sort of a real life demonstration about how you can kind of

Speech of Professor Motoshige Itoh At the event organized by Thai-Japanese Association December 17, 2002 At the Bangkok Club, Bangkok, Thailand.

Speech of Professor Motoshige Itoh At the event organized by Thai-Japanese Association December 17, 2002 At the Bangkok Club, Bangkok, Thailand. Good afternoon ladies and gentleman. It s my great honor

Speech of Professor Motoshige Itoh At the event organized by Thai-Japanese Association December 17, 2002 At the Bangkok Club, Bangkok, Thailand. Good afternoon ladies and gentleman. It s my great honor

The Conduct of Monetary Policy

The Conduct of Monetary Policy This lecture examines the strategies and tactics central banks use to conduct monetary policy. Price Stability, a Nominal Anchor, and the Time-Inconsistency Problem A. Price

The Conduct of Monetary Policy This lecture examines the strategies and tactics central banks use to conduct monetary policy. Price Stability, a Nominal Anchor, and the Time-Inconsistency Problem A. Price

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri Name (print): Name (signature): Section Registered (circle one): T 1:30 T 6:00 W 1:30 As always, the honor code rules are in effect. You know

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri Name (print): Name (signature): Section Registered (circle one): T 1:30 T 6:00 W 1:30 As always, the honor code rules are in effect. You know

Prospects for the National and Local Economies: A Monetary Policymaker s View. I. Good afternoon. I m very pleased to be here with you today.

Presentation to Chapman University Annual Economic Forum Hyatt Regency, Huntington Beach, CA By Robert T. Parry, President and CEO of the Federal Reserve Bank of San Francisco For delivery May 29, 2003,

Presentation to Chapman University Annual Economic Forum Hyatt Regency, Huntington Beach, CA By Robert T. Parry, President and CEO of the Federal Reserve Bank of San Francisco For delivery May 29, 2003,

Weekly Market Commentary

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

Five key investment themes for 2015

Five key investment themes for 2015 Exiting QE in the US was always going to be a path of uncertainty for central bankers, globally and for markets and investors. There is simply no exact precedent for

Five key investment themes for 2015 Exiting QE in the US was always going to be a path of uncertainty for central bankers, globally and for markets and investors. There is simply no exact precedent for

Retirement Investments Insurance. Pensions. made simple TAKE CONTROL OF YOUR FUTURE

Retirement Investments Insurance Pensions made simple TAKE CONTROL OF YOUR FUTURE Contents First things first... 5 Why pensions are so important... 6 How a pension plan works... 8 A 20 year old needs to

Retirement Investments Insurance Pensions made simple TAKE CONTROL OF YOUR FUTURE Contents First things first... 5 Why pensions are so important... 6 How a pension plan works... 8 A 20 year old needs to

Incremental Steps Toward a Radical Solution

Peterson Perspectives Interviews on Current Topics Incremental Steps Toward a Radical Solution Simon Johnson observes that the Federal Reserve s policy of quantitative easing of monetary policy is a necessary

Peterson Perspectives Interviews on Current Topics Incremental Steps Toward a Radical Solution Simon Johnson observes that the Federal Reserve s policy of quantitative easing of monetary policy is a necessary

Introduction. ECON204 Notes. Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

Global Financial Crisis and China s Countermeasures

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Exchange Rate Regimes Revised: January 13, 2012

The Global Economy Class Notes Exchange Rate Regimes Revised: January 13, 2012 The term exchange rate regimes refers to the various arrangements governments around the world make about international transactions.

The Global Economy Class Notes Exchange Rate Regimes Revised: January 13, 2012 The term exchange rate regimes refers to the various arrangements governments around the world make about international transactions.

I don't understand the argument that even though inflation is not accelerating, the world nevertheless suffers from "global excess liquidity":

August 17, 2005 Global Excess Liquidity? I don't understand the argument that even though inflation is not accelerating, the world nevertheless suffers from "global excess liquidity": Economics focus A

August 17, 2005 Global Excess Liquidity? I don't understand the argument that even though inflation is not accelerating, the world nevertheless suffers from "global excess liquidity": Economics focus A

Effective Economic Growth for People: The Role of the United States 1

Effective Economic Growth for People: The Role of the United States 1 William R. Cline Center for Global Development and Institute for International Economics December, 2004 It is a pleasure to speak once

Effective Economic Growth for People: The Role of the United States 1 William R. Cline Center for Global Development and Institute for International Economics December, 2004 It is a pleasure to speak once

Modern Portfolio Theory

66 Trusts & Trustees, Vol. 15, No. 2, April 2009 Modern Portfolio Theory Ian Shipway* Abstract All investors, be they private individuals, trustees or professionals are faced with an extraordinary range

66 Trusts & Trustees, Vol. 15, No. 2, April 2009 Modern Portfolio Theory Ian Shipway* Abstract All investors, be they private individuals, trustees or professionals are faced with an extraordinary range

Sub-3% GDP Growth: A Lost Decade For The US Economy

Sub-3% GDP Growth: A Lost Decade For The US Economy February 3, 2016 by Gary Halbert of Halbert Wealth Management IN THIS ISSUE: 1. 4Q GDP Up Only 0.7% Economy Started and Ended Weak 2. A Controversy Over

Sub-3% GDP Growth: A Lost Decade For The US Economy February 3, 2016 by Gary Halbert of Halbert Wealth Management IN THIS ISSUE: 1. 4Q GDP Up Only 0.7% Economy Started and Ended Weak 2. A Controversy Over

DEFICITS AND DEBT Macroeconomics in Context (Goodwin, et al.)

") Chapter 16 DEFICITS AND DEBT Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter expands on the material from Chapter 10, from a less theoretical and more applied perspective. It

Chapter 16 DEFICITS AND DEBT Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter expands on the material from Chapter 10, from a less theoretical and more applied perspective. It

Working Paper. A fundamental interest rate explanation and forecast. July 3, Economic Research & Corporate Development. Dr.

Spezialthemen Working Paper / Nr. 114 / 21.08.2008 Economic Research & Corporate Development Working Paper 130 July 3, 2009 MAcroeconomics Financial markets economic policy sectors Dr. Rolf Schneider A

Spezialthemen Working Paper / Nr. 114 / 21.08.2008 Economic Research & Corporate Development Working Paper 130 July 3, 2009 MAcroeconomics Financial markets economic policy sectors Dr. Rolf Schneider A