Trade led Growth in Times of Crisis Asia Pacific Trade Economists Conference 2 3 November 2009, Bangkok. Session 1

|

|

|

- Roland Andrews

- 6 years ago

- Views:

Transcription

1 Trade led Growth in Times of Crisis Asia Pacific Trade Economists Conference 2 3 November 2009, Bangkok Session 1 Do We Need a New Approach to Trade? Alan V. Deardorff Asia Pacific Research and Training Network on Trade

2 Do We Need a New Approach to Trade? Alan V. Deardorff University of Michigan For a Panel on Taking Stock of the Global Crisis Asia Pacific Trade Economists' Conference, Bangkok, November 2,

3 Questions Two main questions: Is growing trade (exports and imports) (still) a good thing? Are growing trade imbalances a good thing? 3

4 Questions Related questions: Has trade (or trade imbalance) increased Instability? Vulnerability? Would trade restrictions now be beneficial? Are problems made better or worse by Exchange rate movements? Exchange rate intervention? 4

5 Growth of Trade

6 Growth of Trade Countries have become more dependent on Exports for employment Imports for Consumption Investment Inputs 6

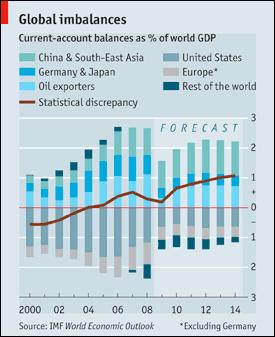

7 Source: IMF World Economic Outlook

8 Growth of Trade Thus they have become more vulnerable to Drop in demand for exports Rise in price (or reduced availability) of imports (e.g., oil, food) Do these changes hurt? Yes! Is it worth restricting trade in order to avoid this hurt? No! 8

9 Growth of Trade Why not? Need to consider two cases: Flexible exchange rate Fixed exchange rate 9

10 Growth of Trade Flexible exchange rate Drop in exports leads to Currency depreciation Offsetting rise in exports & fall in imports Net effects On aggregate demand: none On terms of trade: negative 10

11 Growth of Trade Result under flexible rate There is a loss, via the terms of trade. But what is lost is the gains from trade. Implication Don t deprive countries of the gains from trade in good times in order not to lose them in bad times Would be like avoiding a good restaurant because the excellent chef may leave 11

12 Growth of Trade Fixed exchange rate (peg or currency area) Drop in exports leads to Intervention / monetary outflow / deflation Effects On aggregate demand: negative On terms of trade: negative 12

13 Growth of Trade Result under fixed rate Country is more vulnerable to shocks from abroad But shocks at home are dampened Choice is between Little trade and own shocks only, or More trade and subject to shocks from abroad Trade is like a diversified portfolio Note: should be better ex ante but can turn out bad ex post (e.g., this year!) 13

14 Growth of Trade Imbalances

15 Growth of Trade Imbalances Some countries have run persistent current account deficits And accumulated resulting debts Most notably, U.S. Others have run persistent surpluses And accumulated resulting assets Most notably, China Thus we have growth of unbalanced trade 15

16 16

17 Growth of Trade Imbalances Are there gains from unbalanced trade? In theory, yes, if undistorted This is just trade over time Surplus countries are exporting goods now in exchange for goods later (or earlier) Deficit countries are importing goods now, paid for by goods later (or earlier) 17

18 Growth of Trade Imbalances Illustration of inter temporal trade Countries differ in abilities to produce for two periods Present Future May also differ in preferences for present and future consumption Existence of financial assets makes trade possible across time 18

19 Q future Country A Q future Country B Q present Q present 19

20 Q future Country A Q future Country B Q present Q present 20

21 Q future Country A Surplus Q future Country B Deficit Q present Q present 21

22 Growth of Trade Imbalances Inter temporal trade as drawn above Country B is growing faster than country A See future output compared to present Thus B is like China and A like U.S. But B runs the trade deficit and A the surplus To get surplus in B, we d need very different preferences B preferring future consumption even more than its future production Or perhaps it s more likely that A and/or B are distorted by policy 22

23 Growth of Trade Imbalances Inter temporal trade May be based on comparative advantage And thus be beneficial May be more likely distorted by policies And thus more questionable Figure could then look as follows Assumes A subsidizes international borrowing and/or B subsidizes international lending (Both financed by lump sum taxes that reduce expenditure below income.) 23

24 Q future Country A Q future Country B Deficit Surplus Q present Q present 24

25 Growth of Trade Imbalances Is this plausible? Can we imagine governments subsidizing international borrowing and lending? On one side, at least, China s massive purchases of US debt for its reserves seems to qualify. 25

26 Growth of Trade Imbalances Other problems with inter temporal trade May have time consistency problem: Will future generation be willing to complete the transaction begun earlier? Specifically, will U.S. pay back what it has borrowed today? 26

27 Growth of Trade Imbalances My own views, not based on much expertise or evidence: U.S. and China (and others in comparable positions) are being short sighted U.S. consumers have been living beyond their means, ignoring the need to pay their debts in the future Chinese government has been using surplus to grow production, not consumption, ignoring the likelihood that US won t pay its debts. 27

28 Growth of Trade Imbalances All are relying on inter temporal markets that lack the guarantees of intra temporal markets Witness the financial crises that demonstrate this, even within countries subject to rule of law, lender of last resort, etc. How much worse might happen when the irresponsible borrowers and lenders are countries and their governments 28

29 Growth of Trade Imbalances Efforts among heads of state in the G20 to rebalance are overdue, but not likely to succeed Need leadership that is currently absent, and probably new international institutions 29

30 Growth of Trade Imbalances Thus, I see this as a serious problem Does it require a new approach to trade? Not if that means trade restrictions These, we know, do not reduce surpluses and deficits, which arise instead from imbalance between income and expenditure What is needed: New approach to spending Not new approach to trade 30

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Class Notes. Chapter 5 Saving and Investment in the Open Economy Learning Objectives

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

Fragmentation, Comparative Advantage, and Industrial Policy

TOWARDS A RETURN OF INDUSTRIAL POLICY? ARTNeT SYMPOSIUM 25-26 JULY 2011 ESCAP, BANGKOK Fragmentation, Comparative Advantage, and Industrial Policy Alan V. Deardorff University of Michigan Fragmentation,

TOWARDS A RETURN OF INDUSTRIAL POLICY? ARTNeT SYMPOSIUM 25-26 JULY 2011 ESCAP, BANGKOK Fragmentation, Comparative Advantage, and Industrial Policy Alan V. Deardorff University of Michigan Fragmentation,

Exchange Rate Regimes and Structural Realignment of Global Economies. Comments from an Asian perspective

Exchange Rate Regimes and Structural Realignment of Global Economies Comments from an Asian perspective Yozo Nishimura Institute for International Monetary Affairs November 17, 2009 Tokyo IIMA 1 Main points

Exchange Rate Regimes and Structural Realignment of Global Economies Comments from an Asian perspective Yozo Nishimura Institute for International Monetary Affairs November 17, 2009 Tokyo IIMA 1 Main points

PubPol 201. Module 1: International Trade Policy. Class 3 Outline. Definitions. Class 3 Outline. Definitions. Definitions. Class 3

PubPol 201 Module 1: International Trade Policy Class 3 Trade Deficits; 2 3 Definitions Balance of trade = Exports minus Imports Surplus if positive Deficit if negative Reported in 2 forms Balance of trade

PubPol 201 Module 1: International Trade Policy Class 3 Trade Deficits; 2 3 Definitions Balance of trade = Exports minus Imports Surplus if positive Deficit if negative Reported in 2 forms Balance of trade

China s macroeconomic imbalances: causes and consequences. John Knight and Wang Wei

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

PubPol 201. Module 1: International Trade Policy. Class 3 Trade Deficits; Currency Manipulation

PubPol 201 Module 1: International Trade Policy Class 3 Trade Deficits; Currency Manipulation Class 3 Outline Trade Deficits; Currency Manipulation Trade deficits Definitions What they do and do not mean

PubPol 201 Module 1: International Trade Policy Class 3 Trade Deficits; Currency Manipulation Class 3 Outline Trade Deficits; Currency Manipulation Trade deficits Definitions What they do and do not mean

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

BOP Problems and Marshall Lerner condition and J-curve

BOP Problems and Marshall Lerner condition and J-curve Section 4.7 of Matt McGee s Economics In Terms of the Good, the Bad and the Economist Chapter 27, Blink and Dorton s IB Course Companion: Economics

BOP Problems and Marshall Lerner condition and J-curve Section 4.7 of Matt McGee s Economics In Terms of the Good, the Bad and the Economist Chapter 27, Blink and Dorton s IB Course Companion: Economics

Movements of goods and services across borders are often thought of as

C H A P T E R 1 4 The Link Between Trade and Capital Flows Movements of goods and services across borders are often thought of as distinct from international capital flows. For example, an individual who

C H A P T E R 1 4 The Link Between Trade and Capital Flows Movements of goods and services across borders are often thought of as distinct from international capital flows. For example, an individual who

Lecture 1: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 1: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics 1. The relationship between savings, investment and real interest rates in a closed economy (the world economy) 2. The relationship

Lecture 1: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics 1. The relationship between savings, investment and real interest rates in a closed economy (the world economy) 2. The relationship

Chapter 18. The International Financial System Intervention in the Foreign Exchange Market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Econ520. Spring Prof. Lutz Hendricks. March 28, 2017

Practice Problems: Trade Deficits Econ520. Spring 2017. Prof. Lutz Hendricks. March 28, 2017 Jones, Charles I. (2008). Macroeconomics (1st ed.). W. W. Norton, ch. 14, questions 1, 3-8. 1 Basics 1. Explain

Practice Problems: Trade Deficits Econ520. Spring 2017. Prof. Lutz Hendricks. March 28, 2017 Jones, Charles I. (2008). Macroeconomics (1st ed.). W. W. Norton, ch. 14, questions 1, 3-8. 1 Basics 1. Explain

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Presentation. The Boom in Capital Flows and Financial Vulnerability in Asia

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

The International Financial System

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

Intermediate Macroeconomics

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Chapter 5. Saving and Investment in the Open Economy. Copyright 2009 Pearson Education Canada

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada Balance of Payments Accounting The balance of payments accounts are the record of country s international transactions.

Chapter 5 Saving and Investment in the Open Economy Copyright 2009 Pearson Education Canada Balance of Payments Accounting The balance of payments accounts are the record of country s international transactions.

3/9/2010. Topics PP542. Macroeconomic Goals (cont.) Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History

Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History") Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Global imbalances: the perspective of the Bank of England

Global imbalances: the perspective of the Bank of England MERVYN KING Governor Bank of England In 9, demand in the world s major economies fell, relative to its pre-crisis trend, by around USD.5 trillion

Global imbalances: the perspective of the Bank of England MERVYN KING Governor Bank of England In 9, demand in the world s major economies fell, relative to its pre-crisis trend, by around USD.5 trillion

How Successful is China s Economic Rebalancing?*

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does not imply

only, and the presence of them, or of links to them, on the IMF website does not imply") 7 TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 9-10, 2006 The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does

7 TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 9-10, 2006 The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does

CRS Report for Congress

CRS Report for Congress Received through the CRS Web Order Code RS21625 Updated April 25, 2005 China s Currency Peg: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense,

CRS Report for Congress Received through the CRS Web Order Code RS21625 Updated April 25, 2005 China s Currency Peg: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense,

1. Generation One. 2. Generation Two. 3. Sudden Stops. 4. Banking Crises. 5. Fiscal Solvency

Currency Crises 1. Generation One 2. Generation Two 3. Sudden Stops 4. Banking Crises 5. Fiscal Solvency 1 Generation One 1.1 Monetary and Fiscal Policy Initial position long-run equilibrium purchasing

Currency Crises 1. Generation One 2. Generation Two 3. Sudden Stops 4. Banking Crises 5. Fiscal Solvency 1 Generation One 1.1 Monetary and Fiscal Policy Initial position long-run equilibrium purchasing

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Should China Revalue? Domingo Cavallo and Joaquín Cottani

Should China Revalue? Domingo Cavallo and Joaquín Cottani According to many G7 analysts the solution to China s macroeconomic imbalance, which manifests itself in the form of a large balance of payments

Should China Revalue? Domingo Cavallo and Joaquín Cottani According to many G7 analysts the solution to China s macroeconomic imbalance, which manifests itself in the form of a large balance of payments

The Government Deficit and the Financial Crisis

The Government Deficit and the Financial Crisis The 2008 financial crisis has resulted in a huge increase in the federal government deficit. Government spending has increased significantly, and tax revenue

The Government Deficit and the Financial Crisis The 2008 financial crisis has resulted in a huge increase in the federal government deficit. Government spending has increased significantly, and tax revenue

Unraveling the Mythology

Has the American Economy Tanked? If so, what should the U.S. do? Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno September 9, 2011 Unraveling the Mythology It ain't what you don't

Has the American Economy Tanked? If so, what should the U.S. do? Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno September 9, 2011 Unraveling the Mythology It ain't what you don't

Objectives of the lecture

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Challenges for Monetary Policy in Latin America and the Caribbean

Challenges for Monetary Policy in Latin America and the Caribbean XCVII Meeting of Central Bank Governors of the Center for Latin American Monetary Studies Brian Wynter Governor Bank of Jamaica 29 April

Challenges for Monetary Policy in Latin America and the Caribbean XCVII Meeting of Central Bank Governors of the Center for Latin American Monetary Studies Brian Wynter Governor Bank of Jamaica 29 April

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

"The Continuing Problem of China's Currency Management Policy"

"The Continuing Problem of China's Currency Management Policy" Written testimony of Dean Baker Co-Director, Center for Economic and Policy Research (CEPR) For the hearing on "Assessing the U.S. Rebalance

"The Continuing Problem of China's Currency Management Policy" Written testimony of Dean Baker Co-Director, Center for Economic and Policy Research (CEPR) For the hearing on "Assessing the U.S. Rebalance

Malaysia. Real Sector. Economic recovery is gaining momentum.

Malaysia Real Sector Economic recovery is gaining momentum. Malaysia s economy grew 4.7% in the first three quarters of 23, well above the year-earlier pace of 3.7%. GDP rose 5.1% in the third quarter,

Malaysia Real Sector Economic recovery is gaining momentum. Malaysia s economy grew 4.7% in the first three quarters of 23, well above the year-earlier pace of 3.7%. GDP rose 5.1% in the third quarter,

International Trade. International Trade, Exchange Rates, and Macroeconomic Policy. International Trade. International Trade. International Trade

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Global Imbalances and the U.S. Current Account Deficit. Economics 826 January 2009

Global Imbalances and the U.S. Current Account Deficit Economics 826 January 2009 1 A. What are the facts? B. Why is this trend worrying? C. What are the possible causes? D. What are the possible adjustments?

Global Imbalances and the U.S. Current Account Deficit Economics 826 January 2009 1 A. What are the facts? B. Why is this trend worrying? C. What are the possible causes? D. What are the possible adjustments?

A Two-Handed Economist s Presentation on The Treaty. Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

Investment and its Financing: A Macro Perspective

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

`Global Imbalances and the US Current Account Deficit. Economics 426 January 2016

1 `Global Imbalances and the US Current Account Deficit Economics 426 January 2016 2 A. Thoughts on Capital Flows Courtesy of David Backus, NYU Thoughts Capital Flows: Thoughts Backus (NYU) Capital Flows

1 `Global Imbalances and the US Current Account Deficit Economics 426 January 2016 2 A. Thoughts on Capital Flows Courtesy of David Backus, NYU Thoughts Capital Flows: Thoughts Backus (NYU) Capital Flows

Global Imbalances. January 23rd

Global Imbalances January 23rd Fact #1: The US deficit is big But there is little agreement on why, or on how much we should worry about it Global current account identity (CA = S-I = I*-S*) is a useful

Global Imbalances January 23rd Fact #1: The US deficit is big But there is little agreement on why, or on how much we should worry about it Global current account identity (CA = S-I = I*-S*) is a useful

Yen and Yuan. The Impact of Exchange Rate Fluctuations on the Asian Economies. C. H. Kwan RIETI

Yen and Yuan The Impact of Exchange Rate Fluctuations on the Asian Economies C. H. Kwan RIETI November 21 The Yen-dollar Rate as the Major Determinant of Asian Economic Growth -4-3 -2 Stronger Yen Yen

Yen and Yuan The Impact of Exchange Rate Fluctuations on the Asian Economies C. H. Kwan RIETI November 21 The Yen-dollar Rate as the Major Determinant of Asian Economic Growth -4-3 -2 Stronger Yen Yen

The Global Macroeconomy

The Global Macroeconomy 1 1. Foreign Exchange: Currencies and Crises 2. Globalization of Finance: Debts and Deficits 3. Government and Institutions: Policies and Performance 4. Conclusions 1 Introduction

The Global Macroeconomy 1 1. Foreign Exchange: Currencies and Crises 2. Globalization of Finance: Debts and Deficits 3. Government and Institutions: Policies and Performance 4. Conclusions 1 Introduction

Suggested Solutions to Problem Set 4

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Global Markets. CHINA AND GLOBAL MARKET VOLATILITY.

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

Discussion of Boom, Bust, Recovery: Forensics of the Latvia Crisis By Olivier Blanchard, Mark Griffiths and Bertrand Gruss 1

Discussion of Boom, Bust, Recovery: Forensics of the Latvia Crisis By Olivier Blanchard, Mark Griffiths and Bertrand Gruss 1 By Kristin J. Forbes, MIT-Sloan School of Management November 11, 2013 This

Discussion of Boom, Bust, Recovery: Forensics of the Latvia Crisis By Olivier Blanchard, Mark Griffiths and Bertrand Gruss 1 By Kristin J. Forbes, MIT-Sloan School of Management November 11, 2013 This

DEVELOPING COUNTRIES AND THE DOLLAR. C. P. Chandrasekhar and Jayati Ghosh

DEVELOPING COUNTRIES AND THE DOLLAR C. P. Chandrasekhar and Jayati Ghosh It is now generally recognised that the very large macroeconomic imbalances between the US and the rest of the world, which are

DEVELOPING COUNTRIES AND THE DOLLAR C. P. Chandrasekhar and Jayati Ghosh It is now generally recognised that the very large macroeconomic imbalances between the US and the rest of the world, which are

The Macro-economy and the Global Financial Crisis

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

International Finance

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

FIRST LOOK AT MACROECONOMICS*

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

JAPAN s CURRENT FINANCIAL & ECONOMIC CRISIS. AContrarianView?

JAPAN s CURRENT FINANCIAL & ECONOMIC CRISIS AContrarianView? ORIGINS Current Crisis Successful export-led growth Emergence Bubble Economy Collapse of Bubble and extension via FDI of export-led growth to

JAPAN s CURRENT FINANCIAL & ECONOMIC CRISIS AContrarianView? ORIGINS Current Crisis Successful export-led growth Emergence Bubble Economy Collapse of Bubble and extension via FDI of export-led growth to

Appendix: Analysis of Exchange Rates Pursuant to the Act

Appendix: Analysis of Exchange Rates Pursuant to the Act Introduction Although reaching judgments about whether countries manipulate the rate of exchange between their currency and the United States dollar

Appendix: Analysis of Exchange Rates Pursuant to the Act Introduction Although reaching judgments about whether countries manipulate the rate of exchange between their currency and the United States dollar

Comments Regarding Causes of Significant Trade Deficits for 2016 Docket No. ITA

Comments Regarding Causes of Significant Trade Deficits for 2016 Docket No. ITA-2017-0003 I am William A. Jones, President and CEO of Penn United Technologies, Inc. of Cabot, Pennsylvania, north of Pittsburgh.

Comments Regarding Causes of Significant Trade Deficits for 2016 Docket No. ITA-2017-0003 I am William A. Jones, President and CEO of Penn United Technologies, Inc. of Cabot, Pennsylvania, north of Pittsburgh.

The Global Macroeconomy

1 The Global Macroeconomy 1 Foreign Exchange: Currencies and Crises ECON 322 Slides Ayse Kabukcuoglu 2 Globalization of Finance: Debts and Deficits 3 Government and Institutions: Policies and Performance

1 The Global Macroeconomy 1 Foreign Exchange: Currencies and Crises ECON 322 Slides Ayse Kabukcuoglu 2 Globalization of Finance: Debts and Deficits 3 Government and Institutions: Policies and Performance

Flows between sectors. Over a given period of time, income flows and spending flows run within each sector and between sectors.

Basic macroeconomic accounting The threesector division An economy can be divided into three sectors: (i) the domestic private sector (households, firms, and banks); (ii) the domestic government sector

Basic macroeconomic accounting The threesector division An economy can be divided into three sectors: (i) the domestic private sector (households, firms, and banks); (ii) the domestic government sector

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Protectionism. The term free-trade describes the process of lowering protectionist barriers and thereby realizing those gains from trade.

Protectionism Protectionism Protectionism: is the placement of legal restrictions on international trade and includes tariffs, quotas, subsidies, and other bureaucratic barriers Despite the obvious gains

Protectionism Protectionism Protectionism: is the placement of legal restrictions on international trade and includes tariffs, quotas, subsidies, and other bureaucratic barriers Despite the obvious gains

The International Monetary System

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

Trade deficits and the US economy Part I

Trade deficits and the US economy Part I by Michael Knetter Globalization is frequently identified as a primary force affecting the structure and development of the US economy as we enter a new millennium.

Trade deficits and the US economy Part I by Michael Knetter Globalization is frequently identified as a primary force affecting the structure and development of the US economy as we enter a new millennium.

PRESS POINTS FOR CHAPTER 3: IS IT TIME FOR AN INFRASTRUCTURE PUSH? THE MACROECONOMIC EFFECTS OF PUBLIC INVESTMENT World Economic Outlook, October 2014

PRESS POINTS FOR CHAPTER 3: IS IT TIME FOR AN INFRASTRUCTURE PUSH? THE MACROECONOMIC EFFECTS OF PUBLIC INVESTMENT World Economic Outlook, October 14 Prepared by Abdul Abiad (team leader), Aseel Almansour,

PRESS POINTS FOR CHAPTER 3: IS IT TIME FOR AN INFRASTRUCTURE PUSH? THE MACROECONOMIC EFFECTS OF PUBLIC INVESTMENT World Economic Outlook, October 14 Prepared by Abdul Abiad (team leader), Aseel Almansour,

Financial Crises: Why They Occur and What to Do about Them. E. Maskin Institute for Advanced Study

Financial Crises: Why They Occur and What to Do about Them E. Maskin Institute for Advanced Study current financial crisis only latest in long sequence history of financial crises goes back hundreds of

Financial Crises: Why They Occur and What to Do about Them E. Maskin Institute for Advanced Study current financial crisis only latest in long sequence history of financial crises goes back hundreds of

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform

Developing Countries: Growth, Crisis, and Reform") Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

SHORT-TERM ACHIEVEMENTS AND LONG-TERM PROBLEMS. by Man 9{. MeCtzer

SHORT-TERM ACHIEVEMENTS AND LONG-TERM PROBLEMS by Man 9{. MeCtzer Carnegie. Mellon University and American 'Enterprise Institute (Preparedfor the 113. Senate 'Budget Committee, January 26, 1995 It is a

SHORT-TERM ACHIEVEMENTS AND LONG-TERM PROBLEMS by Man 9{. MeCtzer Carnegie. Mellon University and American 'Enterprise Institute (Preparedfor the 113. Senate 'Budget Committee, January 26, 1995 It is a

Y669 International Political Economy. September 21, 2010

Y669 International Political Economy September 21, 2010 What is an exchange rate? The price of a currency expressed in terms of other currencies or gold. What the International Monetary System Has to Do

Y669 International Political Economy September 21, 2010 What is an exchange rate? The price of a currency expressed in terms of other currencies or gold. What the International Monetary System Has to Do

Avoiding Currency Crises * Martin Feldstein **

Avoiding Currency Crises * Martin Feldstein ** Although the Asian crisis countries are now generally experiencing economic recoveries with rising exports and strong share prices, significant damage remains

Avoiding Currency Crises * Martin Feldstein ** Although the Asian crisis countries are now generally experiencing economic recoveries with rising exports and strong share prices, significant damage remains

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.

During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.") Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Exploding fiscal deficits in the United States

Issue 6 Exploding fiscal deficits in the United States Implications for the world economy Key points A worsening of the US fiscal deficit by 4 per cent of GDP will: raise nominal long bonds by 60 basis

Issue 6 Exploding fiscal deficits in the United States Implications for the world economy Key points A worsening of the US fiscal deficit by 4 per cent of GDP will: raise nominal long bonds by 60 basis

A macroeconomic survey of Europe

A macroeconomic survey of Europe Olivier Blanchard January 2007 Nr. 1 Four themes A broad based (both across countries, across consumption, investment and exports) expansion. Not a boom. Fundamentals in

A macroeconomic survey of Europe Olivier Blanchard January 2007 Nr. 1 Four themes A broad based (both across countries, across consumption, investment and exports) expansion. Not a boom. Fundamentals in

Bruce Greenwald: The Crisis Bigger than Global Warming

Bruce Greenwald: The Crisis Bigger than Global Warming April 26, 2016 by Robert Huebscher Manufacturing is dying on a global basis, according to Bruce Greenwald, and its collapse will mean the demise of

Bruce Greenwald: The Crisis Bigger than Global Warming April 26, 2016 by Robert Huebscher Manufacturing is dying on a global basis, according to Bruce Greenwald, and its collapse will mean the demise of

GRA 6639 Topics in Macroeconomics

Lecture 9 Spring 2012 An Intertemporal Approach to the Current Account Drago Bergholt (Drago.Bergholt@bi.no) Department of Economics INTRODUCTION Our goals for these two lectures (9 & 11): - Establish

Lecture 9 Spring 2012 An Intertemporal Approach to the Current Account Drago Bergholt (Drago.Bergholt@bi.no) Department of Economics INTRODUCTION Our goals for these two lectures (9 & 11): - Establish

Economy at Risk: The Growing U.S. Trade Deficit

Economy at Risk: The Growing U.S. Trade Deficit Statement by Professor Robert A. Blecker Department of Economics American University Washington, DC 20016-8029 blecker@american.edu Presented at AFL-CIO/USBIC

Economy at Risk: The Growing U.S. Trade Deficit Statement by Professor Robert A. Blecker Department of Economics American University Washington, DC 20016-8029 blecker@american.edu Presented at AFL-CIO/USBIC

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

Christopher Balding Assistant Professor HSBC School of Business Peking University Graduate School Shenzhen

Christopher Balding Assistant Professor HSBC School of Business Peking University Graduate School Shenzhen Introduction Though potential opportunities for international institutional or policy coordination

Christopher Balding Assistant Professor HSBC School of Business Peking University Graduate School Shenzhen Introduction Though potential opportunities for international institutional or policy coordination

Title: Principle of Economics Saving and investment

Title: Principle of Economics Saving and investment Instructor: Vladimir Hlasny Institution: 이화여자대학교 Dictated: 김나정, 김민겸, 김성도, 문혜린, 박현서 [0:00] Let s recall from chapter 23 that the country s gross domestic

Title: Principle of Economics Saving and investment Instructor: Vladimir Hlasny Institution: 이화여자대학교 Dictated: 김나정, 김민겸, 김성도, 문혜린, 박현서 [0:00] Let s recall from chapter 23 that the country s gross domestic

LIMIT INFLATION Country and Time- Zimbabwe, 2008 Annual Inflation Rate- 79,600,000,000% Time for Prices to Double hours

Inflation 1 Copyright LIMIT INFLATION Country and Time- Zimbabwe, 2008 Annual Inflation Rate- 79,600,000,000% Time for Prices to Double- 24.7 hours What is Inflation? Inflation is rising general level

Inflation 1 Copyright LIMIT INFLATION Country and Time- Zimbabwe, 2008 Annual Inflation Rate- 79,600,000,000% Time for Prices to Double- 24.7 hours What is Inflation? Inflation is rising general level

Unit 2: Macro Measures REVIEW ACTIVITY Name That Concept Rules: 1. Cannot use the word(s) 2. Focus on the concept not word Ex: Price Maker

2. Focus on the concept not word Ex: Price Maker") 1 Unit 2: Macro Measures 1 REVIEW ACTIVITY Name That Concept Rules: 1. Cannot use the word(s) 2. Focus on the concept not word Ex: Price Maker 2 NAME THAT CONCEPT 1.Macroeconomics 2.Inflation 3.Nominal

1 Unit 2: Macro Measures 1 REVIEW ACTIVITY Name That Concept Rules: 1. Cannot use the word(s) 2. Focus on the concept not word Ex: Price Maker 2 NAME THAT CONCEPT 1.Macroeconomics 2.Inflation 3.Nominal

12 ECB GLOBAL IMBALANCES: RECENT DEVELOPMENTS AND POLICY REQUIREMENTS

Box 1 GLOBAL IMBALANCES: RECENT DEVELOPMENTS AND POLICY REQUIREMENTS The diverging pattern of current account positions that have been observed at the global level for a number of years raises two important

Box 1 GLOBAL IMBALANCES: RECENT DEVELOPMENTS AND POLICY REQUIREMENTS The diverging pattern of current account positions that have been observed at the global level for a number of years raises two important

MANAGING CAPITAL FLOWS

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

Chapter 20 (9) Financial Globalization: Opportunity and Crisis

Financial Globalization: Opportunity and Crisis") Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Georgetown University. From the SelectedWorks of Robert C. Shelburne. Robert C. Shelburne, United Nations Economic Commission for Europe.

Georgetown University From the SelectedWorks of Robert C. Shelburne Summer 2013 Global Imbalances, Reserve Accumulation and Global Aggregate Demand when the International Reserve Currencies Are in a Liquidity

Georgetown University From the SelectedWorks of Robert C. Shelburne Summer 2013 Global Imbalances, Reserve Accumulation and Global Aggregate Demand when the International Reserve Currencies Are in a Liquidity

PART II-FINANCIAL INSTITUTIONS (INTERMEDIARIES)

") Boğaziçi University Department of Economics Money, Banking and Financial Institutions L.Yıldıran PART II-FINANCIAL INSTITUTIONS (INTERMEDIARIES) What do banks and other intermediaries do? Why do they exist?

Boğaziçi University Department of Economics Money, Banking and Financial Institutions L.Yıldıran PART II-FINANCIAL INSTITUTIONS (INTERMEDIARIES) What do banks and other intermediaries do? Why do they exist?

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Ángel Estrada and Francesca Viani (*) 14 th EMERGING MARKET WORKSHOP Madrid (*) The views expressed here do not necessarily coincide with those of Banco de España

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Ángel Estrada and Francesca Viani (*) 14 th EMERGING MARKET WORKSHOP Madrid (*) The views expressed here do not necessarily coincide with those of Banco de España

PAGE ONE Economics. Scott A. Wolla, Ph.D., Senior Economic Education Specialist -10,000. Millions of Dollars -20, , , , ,000

International Trade: Making Sense of the Trade Deficit Scott A. Wolla, Ph.D., Senior Economic Education Specialist GLOSSARY Asset: A resource with economic value that an individual, corporation, or country

International Trade: Making Sense of the Trade Deficit Scott A. Wolla, Ph.D., Senior Economic Education Specialist GLOSSARY Asset: A resource with economic value that an individual, corporation, or country

Macedonia's Balance of Payments

Macedonia's Balance of Payments Macedonia. Use the following Macedonia balance of payments data to answer questions 1 through 4. Note that the data presented in the text is insufficient to answer the question

Macedonia's Balance of Payments Macedonia. Use the following Macedonia balance of payments data to answer questions 1 through 4. Note that the data presented in the text is insufficient to answer the question

CRS Report for Congress

Order Code RS21625 Updated March 17, 2006 CRS Report for Congress Received through the CRS Web China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and

Order Code RS21625 Updated March 17, 2006 CRS Report for Congress Received through the CRS Web China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and

AN ASSESSMENT OF THE EFFECTS OF THE CURRENCY REGIME CHANGE SHOCK ON THE EXTERNAL EQUILIBRIUM OF SOME NEW EUROPEAN UNION MEMBER STATES

AN ASSESSMENT OF THE EFFECTS OF THE CURRENCY REGIME CHANGE SHOCK ON THE EXTERNAL EQUILIBRIUM OF SOME NEW EUROPEAN UNION MEMBER STATES CAMELIA MILEA Scientific Researcher III, Victor Slăvescu Centre for

AN ASSESSMENT OF THE EFFECTS OF THE CURRENCY REGIME CHANGE SHOCK ON THE EXTERNAL EQUILIBRIUM OF SOME NEW EUROPEAN UNION MEMBER STATES CAMELIA MILEA Scientific Researcher III, Victor Slăvescu Centre for

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 18 The International Monetary System, 1870-19731973 Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 18 The International Monetary System, 1870-19731973 Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Financial Crises: Why They Occur and What to Do about Them. E. Maskin Institute for Advanced Study

Financial Crises: Why They Occur and What to Do about Them E. Maskin Institute for Advanced Study current financial crisis only latest in long sequence history of financial crisis in U.S. goes back to

Financial Crises: Why They Occur and What to Do about Them E. Maskin Institute for Advanced Study current financial crisis only latest in long sequence history of financial crisis in U.S. goes back to

Alan Bollard: Easy money global liquidity and its impact on New Zealand

Alan Bollard: Easy money global liquidity and its impact on New Zealand Speech by Dr Alan Bollard, Governor of the Reserve Bank of New Zealand, to the Wellington Chamber of Commerce, Wellington, 15 March

Alan Bollard: Easy money global liquidity and its impact on New Zealand Speech by Dr Alan Bollard, Governor of the Reserve Bank of New Zealand, to the Wellington Chamber of Commerce, Wellington, 15 March

10. Fiscal Policy and the Government Budget

10. Fiscal Policy and the Government Budget 1 The Government Budget The government s budget is affected by: Government spending (outlay) Tax revenue (income) 2 Government Spending Major components of government

10. Fiscal Policy and the Government Budget 1 The Government Budget The government s budget is affected by: Government spending (outlay) Tax revenue (income) 2 Government Spending Major components of government

!!! Current account balance =!!!!!! + (!!!!!! ) Capital account balance =!!!!!!, which is also equal to current account balance when!! =!!!!

Capital account balance =!!!!!!, which is also equal to current account balance when!! =!!!!") ECON 302: Intermediate Macroeconomic Theory (Fall 2014) Discussion Section 10 December 5, 2014 KEY CONCEPTS Chapter 15 Open Economy The budget constraint for the home country is + = + + + + ( ) Current

ECON 302: Intermediate Macroeconomic Theory (Fall 2014) Discussion Section 10 December 5, 2014 KEY CONCEPTS Chapter 15 Open Economy The budget constraint for the home country is + = + + + + ( ) Current

Causes of the Trade Deficit. Written Statement of. Barry K. Rogstad, President American Business Conference. The Trade Deficit Review Commission

Causes of the Trade Deficit Written Statement of Barry K. Rogstad, President American Business Conference to The Trade Deficit Review Commission August 19, 1999 I am Barry Rogstad, President of the American

Causes of the Trade Deficit Written Statement of Barry K. Rogstad, President American Business Conference to The Trade Deficit Review Commission August 19, 1999 I am Barry Rogstad, President of the American

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

The Balance of Payments. Balance of Payments. Balance of Payments Accounts. Balance of Payments Accounts. They are composed of the following:

The Balance of Payments Chapter Objective: This chapter serves to introduce the student to the balance of payments, how it is constructed and how balance of payments data may be interpreted. Chapter Outline

The Balance of Payments Chapter Objective: This chapter serves to introduce the student to the balance of payments, how it is constructed and how balance of payments data may be interpreted. Chapter Outline

Trade and Development. Copyright 2012 Pearson Addison-Wesley. All rights reserved.

Trade and Development Copyright 2012 Pearson Addison-Wesley. All rights reserved. 1 International Trade: Some Key Issues Many developing countries rely heavily on exports of primary products for income

Trade and Development Copyright 2012 Pearson Addison-Wesley. All rights reserved. 1 International Trade: Some Key Issues Many developing countries rely heavily on exports of primary products for income