The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply

|

|

|

- Scott Neal

- 6 years ago

- Views:

Transcription

1 The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply Conference Call will begin at 10:00am CT, lines open at 10:50am CT Audio: Access Code: # You can also listen to the conference call audio using your computer speakers. To maximize the webinar viewing area, please select View Full Screen from the menu or press Alt-Enter on your keyboard. Presented by: Jeffrey F. Caughron, Managing Director & COO Ryan W. Hayhurst, Managing Director jcaughron@gobaker.com ryan@gobaker.com

2 Rate Environment: Fed Funds, 2yr T Note, and 10yr T Note 10yr Yield Driven Primarily by 1. Less Treasury Issuance 2. Strong International Demand 3. Low Inflation / Deflation Threat 2yr Yield Driven Primarily by Expectations of Fed Tightening 2

3 3

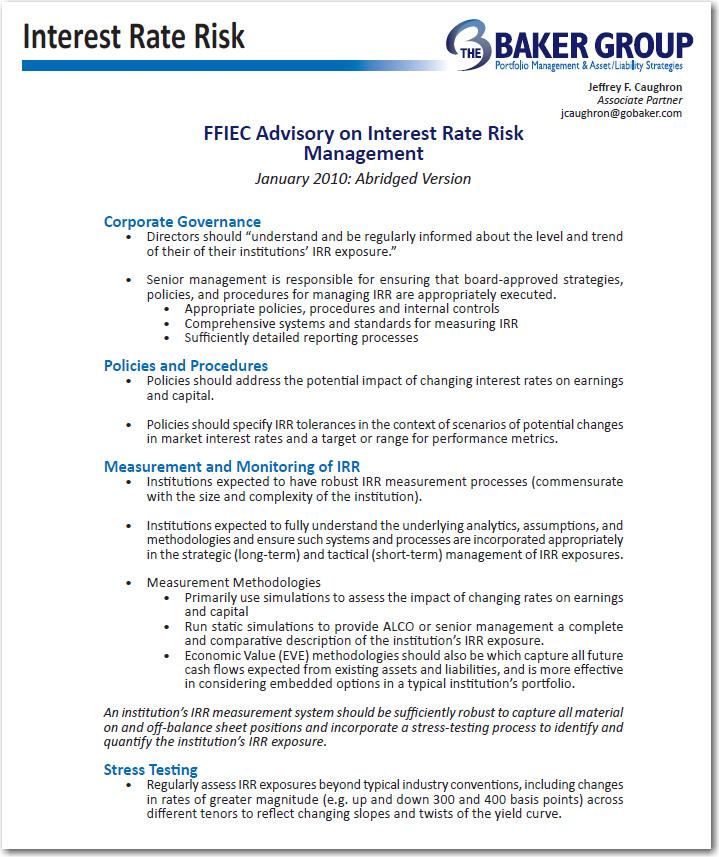

4 Effective Governance Processes Directors need a basic understanding of IRR commensurate with the institution s activities o o Policy Approval including risk limits Document participation in board and ALCO minutes Management should maintain an effective IRR measurement system which provides meaningful data to inform the directorate of exposure levels o Policies should require regular IRR measurement and meaningful risk limits. Role of ALCO is to coordinate balance sheet strategies, manage liquidity, and monitor IRR exposures. o o ALCO needs representation from major operational functions (e.g. lending, deposit gathering, investing.) One function is to help develop and review the key assumptions used in analyzing exposures Independent Review of Processes o o o Does IRR management process function according to policy guidelines? Does IRR measurement system reasonably estimate exposures based on reasonable assumptions? Overall assessment of risk management procedures (model validation, back testing, etc) Risk Mitigation Strategies: o o o Natural Hedge (adjust cash flows and/or relative durations of assets and liabilities) Complex Hedging (off balance sheet derivatives need thorough understanding of risks) Contingency Funding Plan (liquidity risk management) 4

5 Effective Governance Processes: Establishing Policy Limits Limits should not be so low as to frequently require exception approval or refinement, and they should not be set so high as to allow for an unacceptable level of IRR. Thresholds and limits should reflect current market conditions and balance sheet posture. For example, what was an achievable margin ten years ago may not be realistic in the current environment. Limits should reflect the unique characteristics of the bank, it s business model, market area, etc. 5

6 OCC Range of Practices Memo: Risk Limits 6

7 OCC Range of Practices Memo: Earnings at Risk 7

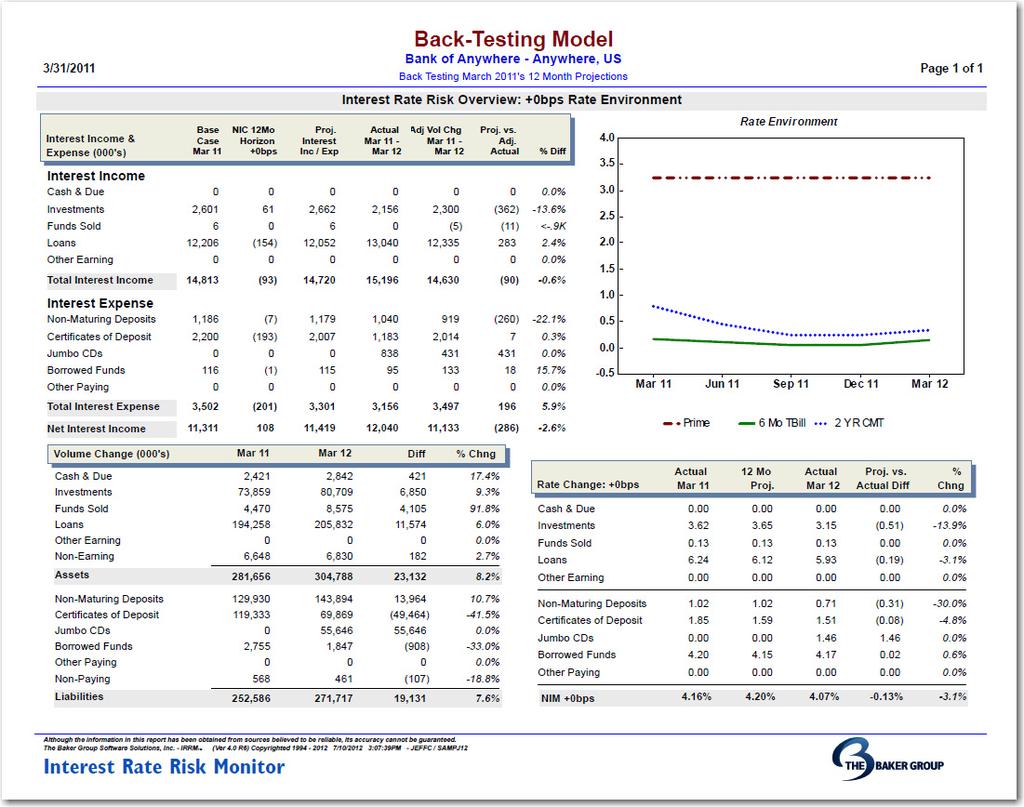

300bps in the next 12mos, the Net Interest Changes is a")

8 IRRM Clients Net Interest Change: Unchanged Rate Scenario & +300bps Scenario The average IRRM client can expect slight margin compression in the next 12mos if market rates remain unchanged If rates rise (parallel) 300bps in the next 12mos, the Net Interest Changes is a positive 2.02%. 8

9 OCC Range of Practices Memo: Economic Value of Equity 9

10 IRRM Clients Economic Value of Equity (EVE): +300bps Rate Scenario For a +300bps rate shock, the average IRRM client can expect a 8.35% depreciation in the (theoretical/hypothetical) fair value of equity. One standard deviation from the mean gives us a range of 27.49% to 10.79%. 10

and decay rates, the reasonableness of asset prepayment assumptions, and key driver rates customer behavior may not reflect past behavior when market rates change in the future.")

11 Developing Key Assumptions Well supported, institution specific assumptions are necessary for good IRR analysis Management should give particular attention to non maturity deposit price sensitivity (or betas) and decay rates, the reasonableness of asset prepayment assumptions, and key driver rates customer behavior may not reflect past behavior when market rates change in the future. o o Sensitivity Testing of Key Assumptions (e.g. NMD Stress Test) Deposit Migration Simulation The IRRM model uses a Maturity Distribution Schedule instead of decay rates to determine NMD average lives. In IRRM, the driver rate can be any rate, but is most often assumed to be Fed Funds. 11

12 Common Weaknesses Found During Review of Assumptions Use of peer averages without consideration of bank specific factors Lack of differentiation between rising and falling rate scenarios Over simplification of balance sheet categories leading to potentially faulty analysis Lack of qualitative adjustment factors to historic data (e.g. not considering a higher run off factor for surge deposits) Inadequate sensitivity testing to evaluate how results would change in response to changes in critical assumptions Source: FDIC Supervisory Insights from Winter

13 NMD as a % of Total Funding Has Surged With Low Rates 13

14 Questions NMD Balances: How long lived and how stable? Will our deposits stick around for a long time? How to determine historical average life: o Open Close Study Based on historical behavior, what s the average life of our core deposits? How to determine balance stability & potential surge balances: o Surge Balance Analysis Based on historical behavior, how sticky are our depositors and how much of a surge in NMD did we experience over the past five years flow versus our peers? Regulator Concern: The future may be different 14

15 Questions about NMD Pricing: How reactive is our pricing and how quickly do we react? How aggressively will we need to price our deposits in reaction to a Fed tightening? How to determine shift sensitivities (pricing betas): o Historical Price Analysis: Sensitivities Based on observed historical behavior, what s our normal pricing reaction to changes in market rates? How to determine time lags: o Historical Pricing Analysis: Time Lags Based on observed historical behavior, how quickly do we react to changes in market rates? Regulator Concern: The future may be different 15

16 OCC Range of Practices Memo: Repricing Betas 16

17 Estimating NMD Betas Using Call Report Data 17

18 Estimating NMD Betas Using Monthly Institution Supplied Data A Non Maturity Deposit (NMD) sensitivity (beta) analysis will provide empirical evidence to support your assumptions. Focus on distinct periods of rising ( ) and falling ( & ) rates. Results should not be used rigidly since the next period of rising rates may not look like the last. Instead, use actual historical data as a starting point for determining appropriate sensitivities. 18

19 Example Open Close Study to Estimate NMD Average Lives Tracks account open date and closed date to determine an actual average life for accounts (MMDA, NOW, Savings, etc.) Query core processor for open accounts and any recently closed accounts Results will often demonstrate very long average lives (8 12yrs) 19

20 Open Close Study A Non Maturity Deposit (NMD) Open Close Study can be used to provide empirical evidence to support your assumptions. For accounts that were closed in a given time period, obtain the date opened and average balance (YTD or LTD). This data can be used to calculate the true average lives of closed accounts. Results should not be used rigidly since factors such as demographics may cause deposits to behave differently in the future. 20

21 Example NMD Analysis to Estimate Decay MMDA Deposit Balance April 13 April 12 April 11 April 10 April 09 April 08 April 07 April 06 Accounts Open on: April 06-32% 34,330,089 37,883,043 39,941,999 38,102,344 37,429,422 37,473,074 42,247,033 51,034,496 April 07 6,173,696 10,059,312 8,553,936 8,362,733 10,114,226 15,758,102 18,427,352 April ,990, ,474, ,561, ,751, ,880, ,100,676 April ,373, ,775, ,500, ,001, ,982,260 April 10-50% 533,256, ,829, ,990,838 1,078,107,545 April ,101,243 1,392,390,905 1,371,170,024 April ,804,487 1,645,297,130 April ,717,123 MMDA Number of Accounts April 13 April 12 April 11 April 10 April 09 April 08 April 07 April 06 Accounts Open on: April 06-78% ,553 1,888 2,285 April April 08 1,152 1,721 1,833 2,100 2,574 2,616 April 09 2,981 4,077 4,524 5,159 6,567 April 10-53% 5,536 8,299 9,520 11,700 April 11 6,883 10,930 13,200 April 12 6,855 12,771 April 13 1,250 21

22 NMD Analysis: Potential Surge Balances 22

23 Cost effective versus local markets or other wholesale funding alternatives. Flexible maturities: 1 mo to 30yrs. Can match funds according to your asset/liability needs. A single certificate per maturity. No collateral is required. No early withdrawal feature. Only upon death or adjudication of incompetence declared by court of law. Excellent resource for Contingency Funding Plans Through Baker Group arrangement with Financial Northeastern Companies 23

Some core processors may be able to calculate historical")

24 Estimating Loan Prepayments Prepayment estimates should be differentiated by product For most accounts, some level of prepayments is better than none Generally speaking, most prepayments should decline as rates rise and increase as rates decline Mortgage prepayments could use consensus estimates (Bloomberg Median or YieldBook) Some core processors may be able to calculate historical prepayments, but many cannot 24

25 Sensitivity Testing: Non Maturity Deposits Whatever Baseline Assumptions You Use, Stress Test Them Institutions should incorporate stressed assumptions for non maturity deposits in IRR models FDIC Three Ways to Stress NMD Assumptions (Sensitivity Tests) 1. Ratchet up pricing betas (shift sensitivities) and reduce time lags in order to mimic an aggressively competitive environment for NMD 2. Reduce Average Life (and Duration) Assumptions in order to assess the EVE impact of lower duration liabilities 3. Simulate a migration of NMD balances into more rate sensitive funding (time deposits or wholesale funding) considered to be the most realistic depiction of what may happen in the next rate cycle Demographics Access to information 25

26 Case Study NMD Migration: Balance Sheet Before vs After Before After The simulation shows a 20% decline in Non Maturing Deposits, replaced by Fed Funds (Borrowed Funds Category) 26

27 Case Study NMD Migration: Earnings Simulation Before 27

28 Case Study NMD Migration: Earnings Simulation After As migration takes place, interest expense rises more rapidly and earnings feel the impact 28

29 NMD Migration Simulation Results: Eight Sample Banks from TX, KS, ND, CO, OK, KY NP = Non-Parallel Rate Scenario (+400/+100bps) NMD Migration Stress Test: 20% Bank Total Assets NMD/TDM 12mo NIC NP 12mo ROA NP EVE NP 1 70mm 37.2% mm 61.0% mm 55.0% mm 51.2% mm 57.2% mm 44.3% mm 44.7% mm 42.5% Average 287mm 49.1%

30 Developing an In House Independent Review Eleven step guide to developing an in-house independent ALCO review Banks are expected to monitor the effectiveness of their key internal controls either as a part of the internal audit process or by means of an appropriate independent review, and managing IRR is no exception. 30

31 The Iron Triangle of Regulatory Compliance Back-Test: Can be done internally or supplied by vendor Independent Review of Processes: Must assess the adequacy of all ALCO processes Board Education? A Robust Model? Stress Testing? Assumptions Reviews? Policy Limits? ALCO Minutes? Model Validation: Can be supplied by vendor the independent review should involve assessing the institution s measurement system of IRR, including the reasonableness of assumptions, the process used in determining assumptions, and the back testing of assumptions and results. FFIEC 31

32 32

33 Model Validation Validation: o Third Party o Periodically Updated o Documentation on file Institutions that use vendorsupplied models are not required to test the mechanics and mathematics of the measurement model. However the vendor should provide documentation showing a credible independent third party has performed such a function. FFIEC 33

34 What to Expect During an IRR Exam Expectations contained primarily in two documents: o 1996 Joint Agency Policy Statement on Interest Rate Risk o 2010 Interagency Advisory Effective IRR requires o Informed Directors o Capable Management o Appropriate Internal Resources Bankers should be prepared to discuss the results of their IRR measurement system and be able to describe key assumptions and assumptions development It isn t enough to simply produce reports management must demonstrate understanding Well documented board and ALCO minutes will help examiners understand the bank s risk management practices, etc. 34

35 Common Examination Findings Insufficient evidence of board and senior management discussion of IRR Policy limits unrealistic or uninformed Use of default (not bank specific) model assumptions Inadequate documentation or support of assumptions Lack of (assumption) sensitivity testing Lack of 300bp or 400bp interest rate shock scenarios Lack of nonparallel yield curve shift scenarios Lack of backtesting or backtesting over an insufficient period of time (3 mo. Vs. 12 mo.) Need for regular independent reviews Independent reviews do not cover all required areas Lack of independent review expertise Outdated or missing Model Validation Source: FDIC 35

36 Interest Rate Risk & ALCO Checklist A pre exam checklist for management review Director Education Ensure directors have a basic understanding of IRR and the bank s ALCO processes Provide directors with access to educational resources on interest rate risk Board minutes should reflect director participation in IRR discussions Regular (Quarterly) ALCO Meetings to Review & Discuss Reports ALCO minutes should reflect a demonstration of sound processes that quantify risk to earnings & capital Regular (Quarterly) Standard & Non Standard Stress Tests 100bp, +100bp, +200bp, +300bp, +400bp, Non Parallel (e.g. +400bp/+100bp Bear Flattener) Ramped Rate Shifts & Immediate Rate Shocks 12 & 24 Month Horizons Earnings at Risk & Economic Value of Equity Annual Validation Obtain most recent Validation Letter for Model (validates the math of the model) Back Test your reports over a 12 month period (validates the results) Independent Review of ALCO Process (validates the process) Annual Assumptions Review Use Back Test to determine if assumptions are generally reasonable Periodically perform analysis to ensure assumptions reflect institution s profile and activities (e.g. Loan Prepayments, NMD Sensitivities, Open Close Study, Decay Analysis, Surge Balances, etc.) Annual Sensitivity Testing (aka, assumptions stress test e.g. increase NMD betas, shorten NMD average lives by 50%, run a migration simulation from NMD to CD s, etc.) Annual Review of Investment & ALCO Policies 36

37 Resources from The Baker Group LP Resources from FDIC 37

Investment Strategies for 1 st Quarter 2015

Investment Strategies for 1 st Quarter 2015 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 929 460 526 You can also listen to the conference call audio

Investment Strategies for 1 st Quarter 2015 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 929 460 526 You can also listen to the conference call audio

Asset/Liability Management

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Investment Strategies For 1 st Quarter 2016

Investment Strategies For 1 st Quarter 2016 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855 749 4750 Access Code: 928 643 950# You can also listen to the conference call audio

Investment Strategies For 1 st Quarter 2016 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855 749 4750 Access Code: 928 643 950# You can also listen to the conference call audio

Interest Rate Risk Measurement

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

Balance Sheet Strategies For Changing Rate Environments

Balance Sheet Strategies For Changing Rate Environments Moss Adams 2017 Credit Union Conference Portland, OR June 22 nd, 2017 Ryan W. Hayhurst Managing Director ryan@gobaker.com 800 962 9468 Credit Union

Balance Sheet Strategies For Changing Rate Environments Moss Adams 2017 Credit Union Conference Portland, OR June 22 nd, 2017 Ryan W. Hayhurst Managing Director ryan@gobaker.com 800 962 9468 Credit Union

Measuring Your IRR Profile Against Peers & Regulatory Targets. February 26, 2015 Webinar

Measuring Your IRR Profile Against Peers & Regulatory Targets February 26, 2015 Webinar. PRESENTERS Tom Hauck joined Austin Associates in 1991. He works with financial institutions around the country in

Measuring Your IRR Profile Against Peers & Regulatory Targets February 26, 2015 Webinar. PRESENTERS Tom Hauck joined Austin Associates in 1991. He works with financial institutions around the country in

Your State Association Presents. Interest Rate Risk: What Does th Future Hold? Program Materials

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

ASSET/LIABILITY MANAGEMENT - YEAR 2

ASSET/LIABILITY MANAGEMENT - YEAR 2 Interest Rate Risk Measurement & Management Raleigh A. Trovillion Executive Vice President UMB Bank Investment Division St. Louis, MO raleigh.trovillion@umb.com 314-612-8039

ASSET/LIABILITY MANAGEMENT - YEAR 2 Interest Rate Risk Measurement & Management Raleigh A. Trovillion Executive Vice President UMB Bank Investment Division St. Louis, MO raleigh.trovillion@umb.com 314-612-8039

Leading Practices. Non-Maturity Deposit Modeling: June 26, :45 AM 12:45 PM. Presented by:

Non-Maturity Deposit Modeling: Leading Practices June 26, 2017 11:45 AM 12:45 PM Presented by: Thomas E Bowers, CFA Managing Director ZM Financial Systems, Inc. 1020 Southhill Drive, Ste. 200 Cary, North

Non-Maturity Deposit Modeling: Leading Practices June 26, 2017 11:45 AM 12:45 PM Presented by: Thomas E Bowers, CFA Managing Director ZM Financial Systems, Inc. 1020 Southhill Drive, Ste. 200 Cary, North

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 Raleigh A. Andy Trovillion Executive Vice President UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com 800-433-5962 August 1, 2017 INTEREST RATE

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 Raleigh A. Andy Trovillion Executive Vice President UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com 800-433-5962 August 1, 2017 INTEREST RATE

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT Scott J. Hopf, CPA Senior Manager BKD, LLP 375 North Shore Drive, Suite 501 Pittsburgh, PA 15212 shopf@bkd.com 412.364.9395 AGENDA The Basics

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT Scott J. Hopf, CPA Senior Manager BKD, LLP 375 North Shore Drive, Suite 501 Pittsburgh, PA 15212 shopf@bkd.com 412.364.9395 AGENDA The Basics

Interest Rate Risk Managing Through The Uptick in Rates

Interest Rate Risk Managing Through The Uptick in Rates Outline Asset Liability Management as Performance Management Sensitivity and the Sources of Risk History of Interest Rate Risk Management How to

Interest Rate Risk Managing Through The Uptick in Rates Outline Asset Liability Management as Performance Management Sensitivity and the Sources of Risk History of Interest Rate Risk Management How to

PNC Bank, NA. Board Report. June 30, Pittsburgh, PA. A/L BENCHMARKS Standards for Asset/Liability Management

A/L BENCHMARKS Standards for Asset/Liability Management Board Report PNC Bank, NA June 30, 2006 Olson Research Associates, Inc. 10290 Old Columbia Road, Columbia, MD 21046 Phone: 888-657-6680 Web: http://www.olsonresearch.com

A/L BENCHMARKS Standards for Asset/Liability Management Board Report PNC Bank, NA June 30, 2006 Olson Research Associates, Inc. 10290 Old Columbia Road, Columbia, MD 21046 Phone: 888-657-6680 Web: http://www.olsonresearch.com

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment

Risk Management Strategy & Solutions FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment Joseph Kennerson, Managing Director jkennerson@darlingconsulting.com Mark A. Haberland,

Risk Management Strategy & Solutions FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment Joseph Kennerson, Managing Director jkennerson@darlingconsulting.com Mark A. Haberland,

RISING Rates Are Here Again Time to Celebrate or Danger Ahead?

Risk Management Strategy & Solutions RISING Rates Are Here Again Time to Celebrate or Danger Ahead? November 9, 2017 Frank Farone, Managing Director ffarone@darlingconsulting.com 2017 Darling Consulting

Risk Management Strategy & Solutions RISING Rates Are Here Again Time to Celebrate or Danger Ahead? November 9, 2017 Frank Farone, Managing Director ffarone@darlingconsulting.com 2017 Darling Consulting

Developing Deposit Strategies for Rising Rates Session 1. Agenda

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

What is a Dynamic ALCO

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Introduction to Asset/Liability Management

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

Core Deposit Analytics Session 1

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Liquidity and Contingency Funding Strategies for Today s Market

Liquidity and Contingency Funding Strategies for Today s Market Presented by www.firstempire.com Today s Presenter Frank Santucci, Managing Director ALM Services, BSMS Frank has been working with banks

Liquidity and Contingency Funding Strategies for Today s Market Presented by www.firstempire.com Today s Presenter Frank Santucci, Managing Director ALM Services, BSMS Frank has been working with banks

Southeast Bankers Outreach Forum

Southeast Bankers Outreach Forum IRR in a Protracted Low Rate Environment Date: September 30, 2014 Presented by: Trent Cowsert Director of Capital Markets The opinions expressed are those of the presenter

Southeast Bankers Outreach Forum IRR in a Protracted Low Rate Environment Date: September 30, 2014 Presented by: Trent Cowsert Director of Capital Markets The opinions expressed are those of the presenter

Core Deposit Analytics Session 2: Beyond Basics - Applying Results

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

Developing a Funding Strategy for Rising Rates. Agenda

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Revised Interest Rate Risk Supervision Effective January 1, 2017

Revised Interest Rate Risk Supervision Effective January 1, 2017 Key Changes to NCUA s interest rate risk supervision: 1. Development of Interest Rate Risk Review Procedures Workbook 2. Updated IRR tolerance

Revised Interest Rate Risk Supervision Effective January 1, 2017 Key Changes to NCUA s interest rate risk supervision: 1. Development of Interest Rate Risk Review Procedures Workbook 2. Updated IRR tolerance

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

MAKING LIQUIDITY YOUR NEW BEST FRIEND

FHLB INDIANAPOLIS MAKING LIQUIDITY YOUR NEW BEST FRIEND David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Friends vs. Best Friends 2 3 Types of Friendship 1. Friendship of

FHLB INDIANAPOLIS MAKING LIQUIDITY YOUR NEW BEST FRIEND David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Friends vs. Best Friends 2 3 Types of Friendship 1. Friendship of

Now What? Navigating Fearlessly Through a Turbulent Environment February 2, 2016

Risk Management Strategy & Solutions Now What? Navigating Fearlessly Through a Turbulent Environment February 2, 2016 Frank L. Farone, Managing Director ffarone@darlingconsulting.com 2015 2016 Darling

Risk Management Strategy & Solutions Now What? Navigating Fearlessly Through a Turbulent Environment February 2, 2016 Frank L. Farone, Managing Director ffarone@darlingconsulting.com 2015 2016 Darling

ALCO: The Fundamentals

ALCO: The Fundamentals Presented by: Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 ext. 4210 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

ALCO: The Fundamentals Presented by: Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 ext. 4210 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

Advanced Asset/Liability Management

Advanced Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management Summary Developing Assumptions

Advanced Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management Summary Developing Assumptions

Liquidity Basics Measuring and Managing Liquidity

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Loan Pricing Deals/Relationships Session 2. Agenda

Loan Pricing Deals/Relationships Session 2 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Loan Pricing Deals/Relationships Session 2 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Financial Literacy Mastery

Financial Literacy Mastery Presented by Eileen Iles Colette Wagner Crowe Horwath LLP Session Objectives Satisfy your NCUA financial literacy requirement by taking your knowledge of financial statements

Financial Literacy Mastery Presented by Eileen Iles Colette Wagner Crowe Horwath LLP Session Objectives Satisfy your NCUA financial literacy requirement by taking your knowledge of financial statements

ASSET/LIABILITY MANAGEMENT - YEAR 2

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017 by Alpha-Numeric Consulting, LLC December 20, 2017 Introduction Financial institutions recognize the need for accurate

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017 by Alpha-Numeric Consulting, LLC December 20, 2017 Introduction Financial institutions recognize the need for accurate

Lecture Materials FUNDING. Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Balance Sheet Strategies For Changing Rate Environments Asset/Liability Management Seminar

Balance Sheet Strategies For Changing Rate Environments Asset/Liability Management Seminar Pasadena & Concord, CA April 25-26, 2017 Ryan W. Hayhurst - Managing Director ryan@gobaker.com 800-962-9468 Market

Balance Sheet Strategies For Changing Rate Environments Asset/Liability Management Seminar Pasadena & Concord, CA April 25-26, 2017 Ryan W. Hayhurst - Managing Director ryan@gobaker.com 800-962-9468 Market

Deposit Pricing in Rising Rates Session 1. Three Part Series

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Testing of the ALM Process: What Should it Really Entail?

Testing of the ALM Process: What Should it Really Entail? Tuesday, June 18, 2013 2:00 PM 3:15 PM Presented by: Bert Purdy, CPA, CTFA Senior Manager BKD, LLP 211 N. Broadway, Suite 600 St. Louis, MO 63102

Testing of the ALM Process: What Should it Really Entail? Tuesday, June 18, 2013 2:00 PM 3:15 PM Presented by: Bert Purdy, CPA, CTFA Senior Manager BKD, LLP 211 N. Broadway, Suite 600 St. Louis, MO 63102

Managing the Bank in World of Uncertainty. FMS Connecticut/Western Massachusetts Chapter May 2, 2017

Managing the Bank in World of Uncertainty FMS Connecticut/Western Massachusetts Chapter May 2, 2017 Facilitator: Jim Clarke, Ph.D. JJClarke2@aol.com Dr. Clarke lectures on Asset/Liability Management &

Managing the Bank in World of Uncertainty FMS Connecticut/Western Massachusetts Chapter May 2, 2017 Facilitator: Jim Clarke, Ph.D. JJClarke2@aol.com Dr. Clarke lectures on Asset/Liability Management &

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08)

NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08)") Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08) Dan Frilot Senior Vice President Balance Sheet Solutions, LLC Background Balance Sheet

Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08) Dan Frilot Senior Vice President Balance Sheet Solutions, LLC Background Balance Sheet

Deposit Pricing in Rising Rates Session 2

Deposit Pricing in Rising Rates Session 2 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Deposit Pricing in Rising Rates Session 2 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Federal Home Loan Bank of Des Moines. A Case for Diversifying the Right-Hand Side of the Balance Sheet

Federal Home Loan Bank of Des Moines A Case for Diversifying the Right-Hand Side of the Balance Sheet 1 Agenda 1. YIELD CURVE FUNDING STRATEGIES 2. BUILDING A CASE FOR FUNDING DIVERSIFICATION 3. BLENDED

Federal Home Loan Bank of Des Moines A Case for Diversifying the Right-Hand Side of the Balance Sheet 1 Agenda 1. YIELD CURVE FUNDING STRATEGIES 2. BUILDING A CASE FOR FUNDING DIVERSIFICATION 3. BLENDED

Asset Liability Management for CU Boards The Basics of ALM Presented by: Frank Santucci - Managing Director ALM Services

Asset Liability Management for CU Boards The Basics of ALM Presented by: Frank Santucci - Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire

Asset Liability Management for CU Boards The Basics of ALM Presented by: Frank Santucci - Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

Georgia Banking School

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management II 2017 Georgia Banking School May 10, 2017 Joel Updegraff Managing Director, ALM SunTrust Robinson Humphrey Important Disclosure

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management II 2017 Georgia Banking School May 10, 2017 Joel Updegraff Managing Director, ALM SunTrust Robinson Humphrey Important Disclosure

ALM Strategies In the Current Economic Environment Presented by: Frank Santucci Managing Director ALM Services (October 2015)

") 1 ALM Strategies In the Current Economic Environment Presented by: Frank Santucci Managing Director ALM Services (October 2015) 1 Asset Liability Management is the process of Measuring, Monitoring and

1 ALM Strategies In the Current Economic Environment Presented by: Frank Santucci Managing Director ALM Services (October 2015) 1 Asset Liability Management is the process of Measuring, Monitoring and

Interagency Advisory on Interest Rate Risk Management

Interagency Management As part of our continued efforts to help our clients navigate through these volatile times, we recently sent out the attached checklist that briefly describes how c. myers helps

Interagency Management As part of our continued efforts to help our clients navigate through these volatile times, we recently sent out the attached checklist that briefly describes how c. myers helps

Georgia Banking School

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

Liquidity Basics Measuring and Managing Liquidity. Course Agenda

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Elevate Your Credit Union s Performance Now is NOT the Time for Business as Usual!

Risk Management Strategy & Solutions Elevate Your Credit Union s Performance Now is NOT the Time for Business as Usual! 2017 Darling Consulting Group, Inc. 260 Merrimac Street Newburyport, MA 01950 Tel:

Risk Management Strategy & Solutions Elevate Your Credit Union s Performance Now is NOT the Time for Business as Usual! 2017 Darling Consulting Group, Inc. 260 Merrimac Street Newburyport, MA 01950 Tel:

Liquidity Basics Measuring and Managing Liquidity. Course Agenda

Liquidity Basics Measuring and Managing Liquidity David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Objectives. NCUA Interest Rate Risk Supervision

NCUA Interest Rate Supervision Lisa Boylen Senior ALM Analyst March 21, 2017 Objectives Understand NCUA s Revised Exam Procedures For Interest Rate Understand Exam Scope and Ratings Help You Prepare For

NCUA Interest Rate Supervision Lisa Boylen Senior ALM Analyst March 21, 2017 Objectives Understand NCUA s Revised Exam Procedures For Interest Rate Understand Exam Scope and Ratings Help You Prepare For

ALCO: The Fundamentals

ALCO: The Fundamentals Presented by: David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext. 4217 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

ALCO: The Fundamentals Presented by: David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext. 4217 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

Key ALM Assumptions for Rising Rates. Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends

CONNECT WITH US Key ALM Assumptions for Rising Rates Lisa Boylen Senior ALM Analyst February 21, 2018 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Planning

CONNECT WITH US Key ALM Assumptions for Rising Rates Lisa Boylen Senior ALM Analyst February 21, 2018 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Planning

NCUA Regulatory Update on ALM

Peter Jensen, Regional Capital Markets Specialist NCUA, Region 4, Division of Special Actions NCUA Regulatory Update on ALM University for Credit Unions September 23, 2014 Agenda Introduction Interest

Peter Jensen, Regional Capital Markets Specialist NCUA, Region 4, Division of Special Actions NCUA Regulatory Update on ALM University for Credit Unions September 23, 2014 Agenda Introduction Interest

NCUA LETTER TO CREDIT UNIONS

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA 22314 DATE: September 2003 LETTER NO: 03-CU-15 TO: SUBJ: Federally Insured Credit Unions Real Estate Concentrations

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA 22314 DATE: September 2003 LETTER NO: 03-CU-15 TO: SUBJ: Federally Insured Credit Unions Real Estate Concentrations

Southeast Bankers Outreach Forum

Southeast Bankers Outreach Forum CRE Exposures and Sound Risk Management Practices Date: September 28, 2017 Presented by: Trey Wheeler Assistant Vice President Office - 404.498.7152 trey.wheeler@atl.frb.org

Southeast Bankers Outreach Forum CRE Exposures and Sound Risk Management Practices Date: September 28, 2017 Presented by: Trey Wheeler Assistant Vice President Office - 404.498.7152 trey.wheeler@atl.frb.org

Credit Union Survival in a Challenging

Credit Union Survival in a Challenging Environment How to Make Balance Sheet Strategy Decisions with Confidence January 24, 2013 C O M P L E T E ALM SOLUTIONS Frank L. Farone Managing Director Darling

Credit Union Survival in a Challenging Environment How to Make Balance Sheet Strategy Decisions with Confidence January 24, 2013 C O M P L E T E ALM SOLUTIONS Frank L. Farone Managing Director Darling

Interest Rate Risk in the Banking Book. Taking a close look at the latest IRRBB developments

Interest Rate Risk in the Banking Book Taking a close look at the latest IRRBB developments Interest Rate Risk in the Banking Book Interest rate risk in the banking book (IRRBB) can be a significant risk

Interest Rate Risk in the Banking Book Taking a close look at the latest IRRBB developments Interest Rate Risk in the Banking Book Interest rate risk in the banking book (IRRBB) can be a significant risk

Deposit Growth Strategies and Balance Sheet Management

Deposit Growth Strategies and Balance Sheet Management Presented by: Frank Santucci Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire Securities,

Deposit Growth Strategies and Balance Sheet Management Presented by: Frank Santucci Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire Securities,

Treatment of IRRBB in Latin America

Treatment of IRRBB in Latin America Survey results Meeting on Interest Rate Risk in the Banking Book (IRRBB) and the Revised Standardised Approach (RSA) for Credit Risk Sao Paulo, Brazil 27-28 April 2016

Treatment of IRRBB in Latin America Survey results Meeting on Interest Rate Risk in the Banking Book (IRRBB) and the Revised Standardised Approach (RSA) for Credit Risk Sao Paulo, Brazil 27-28 April 2016

BCBS Standard for Interest Rate Risk in the Banking Book Objectives, Approaches and Disclosure

BCBS Standard for Interest Rate Risk in the Banking Book Objectives, Approaches and Disclosure Meeting on IRRBB and the Revised Standardised Approach for Credit Risk Sao Paulo, Brazil 27-28 April 2016

BCBS Standard for Interest Rate Risk in the Banking Book Objectives, Approaches and Disclosure Meeting on IRRBB and the Revised Standardised Approach for Credit Risk Sao Paulo, Brazil 27-28 April 2016

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Dwight R. Larsen National Bank Examiner Office of the Comptroller of the Currency Minneapolis, Minnesota dwightrlarsen@hotmail.com 202-597-1329 August

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Dwight R. Larsen National Bank Examiner Office of the Comptroller of the Currency Minneapolis, Minnesota dwightrlarsen@hotmail.com 202-597-1329 August

Liquidity Risk Basics Measuring and Managing Liquidity. Dad, What is Liquidity & Where Does it Come From?

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

Enterprise Risk Management and the ALCO Process

Enterprise Risk Management and the ALCO Process Session 1: Gathering the Parts David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext 4217 Agenda Session 1 Overview of ERM Evolution of ERM

Enterprise Risk Management and the ALCO Process Session 1: Gathering the Parts David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext 4217 Agenda Session 1 Overview of ERM Evolution of ERM

INDUSTRY REPORT. Exposure To Falling Rates - 3Q All Banks Banks < Banks $1B -

A/L BENCHMARKS Standards for Asset/Liability Management TM INDUSTRY REPORT Interest Margin at Risk How do you measure exposure in a dynamic rate environment? What will happen to the bank s margin if interest

A/L BENCHMARKS Standards for Asset/Liability Management TM INDUSTRY REPORT Interest Margin at Risk How do you measure exposure in a dynamic rate environment? What will happen to the bank s margin if interest

Improving Usefulness of PPNR CCAR Stress Test Models: Adding 30+ Years of Rate Data to Deposit Balance Models

Improving Usefulness of PPNR CCAR Stress Test Models: Adding 30+ Years of Rate Data to Deposit Balance Models PETE GILCHRIST, WES WEST, RYAN SCHULZ, JANE LIM We welcome your feedback and are happy to continue

Improving Usefulness of PPNR CCAR Stress Test Models: Adding 30+ Years of Rate Data to Deposit Balance Models PETE GILCHRIST, WES WEST, RYAN SCHULZ, JANE LIM We welcome your feedback and are happy to continue

What Is Asset/Liability Management?

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

Lecture Materials FUNDING

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 & Darryl Mataya SVP & Chief Development Officer FARIN

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 & Darryl Mataya SVP & Chief Development Officer FARIN

Core Deposit Analytics Session 1: Determining Core The Basics

Core Deposit Analytics Session 1: Determining Core The Basics Thomas A. Farin Chairman of the Board tfarin@farin.com 1 Building Blocks for Deposit Analysis Pricing Betas Decay Rates Surge Balance Identification

Core Deposit Analytics Session 1: Determining Core The Basics Thomas A. Farin Chairman of the Board tfarin@farin.com 1 Building Blocks for Deposit Analysis Pricing Betas Decay Rates Surge Balance Identification

Managing Volatility in Liability Driven Investing A Three-Factor Framework

Jeff Passmore, CFA, FSA, EA April 2018 LDI Portfolio Manager LDI Strategist jpassmore@barrowhanley.com Overview Liability Driven Investing (LDI) has become a mainstream approach to managing pension financial

Jeff Passmore, CFA, FSA, EA April 2018 LDI Portfolio Manager LDI Strategist jpassmore@barrowhanley.com Overview Liability Driven Investing (LDI) has become a mainstream approach to managing pension financial

Asset Liability Management: The Fundamentals

Asset Liability Management: The Fundamentals By Toby Lawrence, Principal Financial Institution Advisory Services CLAconnect.com Disclaimers To ensure compliance imposed by IRS Circular 230, any U. S. federal

Asset Liability Management: The Fundamentals By Toby Lawrence, Principal Financial Institution Advisory Services CLAconnect.com Disclaimers To ensure compliance imposed by IRS Circular 230, any U. S. federal

Liquidity Management. 158 Route 206 Gladstone, NJ P: (908) Home FinPro, Inc.

Home FinPro, Inc.") Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

2015 BOK Financial Corporation and BOKF, NA DFAST Public Disclosure

2015 BOK Financial Corporation and BOKF, NA DFAST Public Disclosure BOK Financial Corporation and BOKF, NA are required to perform annual company-run capital stress testing pursuant to the Dodd-Frank Wall

2015 BOK Financial Corporation and BOKF, NA DFAST Public Disclosure BOK Financial Corporation and BOKF, NA are required to perform annual company-run capital stress testing pursuant to the Dodd-Frank Wall

Market and Liquidity Risk Assessment Overview. Federal Reserve System

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

ALM Process & Strategies

ALM Process & Strategies Requirements for a Solid Foundation Chad McKeithen, Managing Director Duncan-Williams Inc. Al Forrester, CEO FiCast Data Corp Outline History of Interest Rate Risk Management How

ALM Process & Strategies Requirements for a Solid Foundation Chad McKeithen, Managing Director Duncan-Williams Inc. Al Forrester, CEO FiCast Data Corp Outline History of Interest Rate Risk Management How

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT. AMIfs Institute July 18, 2016 Monday Afternoon Session

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT AMIfs Institute July 18, 2016 Monday Afternoon Session 1 Agenda - Introduction to ALM Monday, July 18 Afternoon Best Practices in ALM Structuring the ALCO Process

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT AMIfs Institute July 18, 2016 Monday Afternoon Session 1 Agenda - Introduction to ALM Monday, July 18 Afternoon Best Practices in ALM Structuring the ALCO Process

Balance Sheet Strategies for 2018: A Roadmap to Outperform Your Peers Jim Reber, President August 13, 2018

51 st ANNUAL CONVENTION Balance Sheet Strategies for 2018: A Roadmap to Outperform Your Peers Jim Reber, President August 13, 2018 Yield Curve August 6 2 What is Normal? 25yr Avg 25yr Average 10yr Average

51 st ANNUAL CONVENTION Balance Sheet Strategies for 2018: A Roadmap to Outperform Your Peers Jim Reber, President August 13, 2018 Yield Curve August 6 2 What is Normal? 25yr Avg 25yr Average 10yr Average

Deposit Pricing in Rising Rates Session 1. Three Part Series

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Effective Process Deposit Analysis Tools Betas Decay Rates

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Effective Process Deposit Analysis Tools Betas Decay Rates

OFFICE OF INSPECTOR GENERALoFF

OFFICE OF INSPECTOR GENERALoFF REVIEW OF NCUA S INTEREST RATE RISK PROGRAM Report #OIG-15-11 November 13, 2015 TABLE OF CONTENTS Section Page EXECUTIVE SUMMARY...1 BACKGROUND...2 RESULTS IN DETAIL...7

OFFICE OF INSPECTOR GENERALoFF REVIEW OF NCUA S INTEREST RATE RISK PROGRAM Report #OIG-15-11 November 13, 2015 TABLE OF CONTENTS Section Page EXECUTIVE SUMMARY...1 BACKGROUND...2 RESULTS IN DETAIL...7

Developing Deposit Strategies for Rising Rates Session 2. Agenda

Developing Deposit Strategies for Rising Rates Session 2 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Developing Deposit Strategies for Rising Rates Session 2 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

CREDIT UNION INVESTMENT PRICE RISK

A CU*ANSWERS/CALLAHAN & ASSOCIATES WHITEPAPER OCTOBER 24, 2013 CREDIT UNION INVESTMENT PRICE RISK Jim Vilker Patrick Sickels and Chip Filson Expect NCUA and state examiners to stress credit union investment

A CU*ANSWERS/CALLAHAN & ASSOCIATES WHITEPAPER OCTOBER 24, 2013 CREDIT UNION INVESTMENT PRICE RISK Jim Vilker Patrick Sickels and Chip Filson Expect NCUA and state examiners to stress credit union investment

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Back Testing ALM Models April 17, Back Testing ALM Models: Concepts, Practice, and Compliant Business Solutions

Back Testing ALM Models: Concepts, Practice, and Compliant Business Solutions Presented by: William J. McGuire Chairman Emeritus McGuire Performance Solutions, Inc. 16435 N. Scottsdale Rd, Ste 290 Scottsdale,

Back Testing ALM Models: Concepts, Practice, and Compliant Business Solutions Presented by: William J. McGuire Chairman Emeritus McGuire Performance Solutions, Inc. 16435 N. Scottsdale Rd, Ste 290 Scottsdale,

ALM Strategy in the Current Rate Environment. Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends

ALM Strategy in the Current Rate Environment Lisa Boylen Senior ALM Analyst December 12, 2018 1 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Lessons Learned

ALM Strategy in the Current Rate Environment Lisa Boylen Senior ALM Analyst December 12, 2018 1 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Lessons Learned

Dodd-Frank Act Company-Run Stress Test Disclosures

Dodd-Frank Act Company-Run Stress Test Disclosures June 21, 2018 Table of Contents The PNC Financial Services Group, Inc. Table of Contents INTRODUCTION... 3 BACKGROUND... 3 2018 SUPERVISORY SEVERELY ADVERSE

Dodd-Frank Act Company-Run Stress Test Disclosures June 21, 2018 Table of Contents The PNC Financial Services Group, Inc. Table of Contents INTRODUCTION... 3 BACKGROUND... 3 2018 SUPERVISORY SEVERELY ADVERSE

A N N U A L R E P O R T

First Niles Financial, Inc. 2015 ANNUAL REPORT TABLE OF CONTENTS Page No. President s Message... 1 Management s Discussion and Analysis of Financial Condition and Results of Operations... 2 Report of

First Niles Financial, Inc. 2015 ANNUAL REPORT TABLE OF CONTENTS Page No. President s Message... 1 Management s Discussion and Analysis of Financial Condition and Results of Operations... 2 Report of

Balance Sheet Strategies in Today's Economic Environment May 2018

Balance Sheet Strategies in Today's Economic Environment May 2018 Scott Hildenbrand Principal/Chief Balance Sheet Strategist (212) 466-7865 shildenbrand@sandleroneill.com Current Balance Sheet Management

Balance Sheet Strategies in Today's Economic Environment May 2018 Scott Hildenbrand Principal/Chief Balance Sheet Strategist (212) 466-7865 shildenbrand@sandleroneill.com Current Balance Sheet Management

ALCO BEST PRACTICES. Police Officers Credit Union Conference May 6, Presented By Stacey Wilkerson Financial Advisor

ALCO BEST PRACTICES Police Officers Credit Union Conference May 6, 2014 Presented By Stacey Wilkerson Financial Advisor Agenda Risk vs. reward The inherent conflict between earnings and risk Strategic

ALCO BEST PRACTICES Police Officers Credit Union Conference May 6, 2014 Presented By Stacey Wilkerson Financial Advisor Agenda Risk vs. reward The inherent conflict between earnings and risk Strategic

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch. President\CEO FARIN & Associates, Inc.

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

Wells Fargo & Company. Basel III Pillar 3 Regulatory Capital Disclosures

Wells Fargo & Company Basel III Pillar 3 Regulatory Disclosures For the quarter ended March 31, 2018 1 Table of Contents Disclosure Map Introduction Executive Summary Company Overview Basel III Overview

Wells Fargo & Company Basel III Pillar 3 Regulatory Disclosures For the quarter ended March 31, 2018 1 Table of Contents Disclosure Map Introduction Executive Summary Company Overview Basel III Overview

RiskGPS. Interest Rate Risk Measurement and Control for Community Banks & Thrifts

RiskGPS Interest Rate Risk Measurement and Control for Community Banks & Thrifts User s Guide 2017 Table of Contents Introduction. 2 Logging In.. 4 Interest Rate Risk, Report Calculation Methodology..

RiskGPS Interest Rate Risk Measurement and Control for Community Banks & Thrifts User s Guide 2017 Table of Contents Introduction. 2 Logging In.. 4 Interest Rate Risk, Report Calculation Methodology..

Doing More with Your Balance Sheet

Doing More with Your Balance Sheet John P. Biestman, CFA - VP/Senior Relationship Manager Brett L.A. Manning, CFA - VP/Director, Member Strategies October 27, 2015 Who is FHLB Des Moines? Current Balance

Doing More with Your Balance Sheet John P. Biestman, CFA - VP/Senior Relationship Manager Brett L.A. Manning, CFA - VP/Director, Member Strategies October 27, 2015 Who is FHLB Des Moines? Current Balance

Loan Pricing Deals & Relationships Session 1. Agenda

Loan Pricing Deals & Relationships Session 1 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Loan Pricing Deals & Relationships Session 1 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

LIQUIDITY AND FUNDS MANAGEMENT

LIQUIDITY AND FUNDS MANAGEMENT STRATEGIC TOPIC INTERSESSION PROJECT by: Brian Heim LIQUIDITY AND FUNDS MANAGEMENT TABLE OF CONTENTS INTRODUCTION 1 PART I: LIQUIDITY GUIDANCE AND TRENDS 2 PART II: FUNDS

LIQUIDITY AND FUNDS MANAGEMENT STRATEGIC TOPIC INTERSESSION PROJECT by: Brian Heim LIQUIDITY AND FUNDS MANAGEMENT TABLE OF CONTENTS INTRODUCTION 1 PART I: LIQUIDITY GUIDANCE AND TRENDS 2 PART II: FUNDS