Casualty Actuaries of the Northwest: Strategies for Homeowners Profitability and Growth

|

|

|

- Bethany Stafford

- 6 years ago

- Views:

Transcription

1 Casualty Actuaries of the Northwest: Strategies for Homeowners Profitability and Growth Nancy Watkins, FCAS, MAAA Principal and Consulting Actuary Milliman, Inc. September 25, 2015

2 Why is Homeowners so challenging? 2

3 Strategies for integrated approach to risk Identify competitive and profitable targets Communicate with and monitor agents Use cat models and GIS data for granular pricing and underwriting Improve rate indications to clear regulatory hurdles Use new data to develop a customized view of risk Take actions outside of rates 3

4 Use the data you already have Ex-wind Loss Ratio Relativity Number of Stories 1 story 2+ stories Ex-wind Loss Ratio Relativity Policyholder Age Ex-wind Loss Ratio Relativity Coverage A per Square Foot Find new insights within company data 4

5 Use data from third party sources Buildfax Population Density Find other objective data that aligns with risk Mortgage data Census AOP Loss Ratio Relativity ZIP Average Household size or more 5

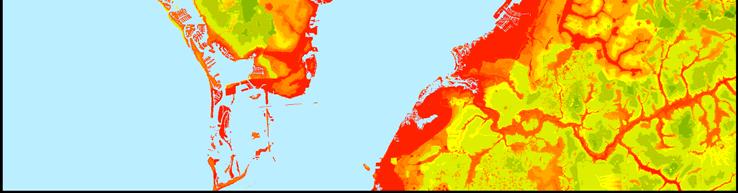

6 Use Geographic Information Systems data Example: Hurricane Land Use/Land Cover Effective Surface Roughness Start with GIS data, such as land use/land cover and a coastline Coastline Distance to Coast Use these to prepare predictor variables, such as effective surface roughness and distance to coast 6

7 Use Catastrophe Model Output For Granular Pricing Hurricane AAL / Coverage in $1000 s Combine new predictor variables with catastrophe model output to model relationships to hurricane burn rate 7

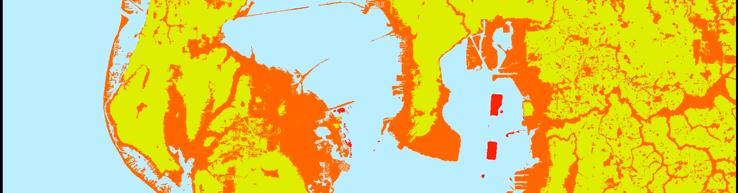

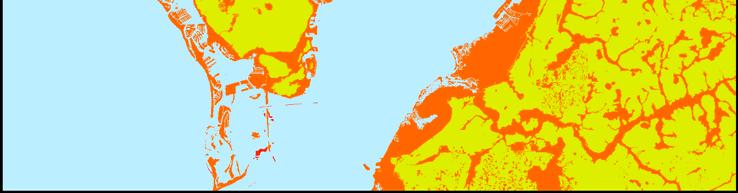

8 Example: Storm surge NOAA Shoreline Elevation Start with GIS data, such as elevation, coastline, stream/river locations Use these to prepare predictor variables 8

9 Refine storm surge risk assessment Combine with cat model output to refine underwriting rules for excessive storm surge risk, e.g. minimum permissible elevation given the distance to tidal water Example of ineligible locations 9

Hydrological Unit")

10 Example: Flood Target variables: Storm surge AAL Inland flood AAL Predictor variables: Relative Elevation Distance to Mean High Water Line Distance to River/Stream (Grouped) Hydrological Unit 10

11 Pricing Flood: the Risk is Continuous Traditional Flood Zone Rating (NFIP Flood Zones) Continuous Flood Rating 11

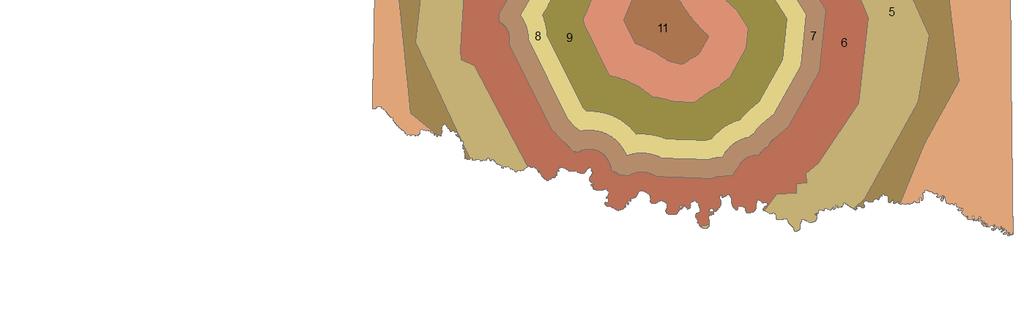

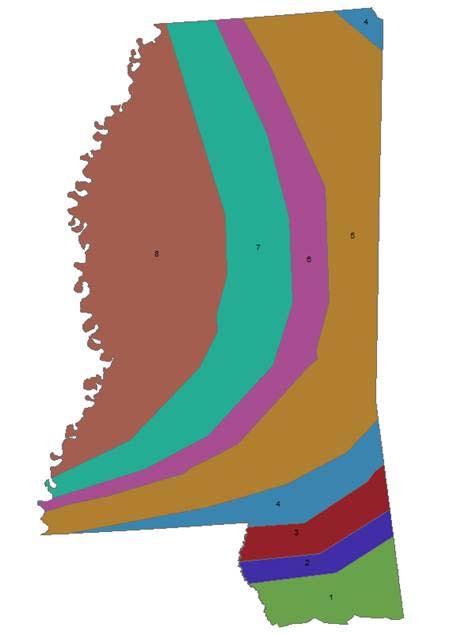

12 Example: Non-Hurricane Wind Risk Hail Days Per Year Start with Hail Days per Year Use to determine territorial definitions Then use catastrophe model output to set relativities 12

13 13 Examples of Non-Hurricane Wind Territories Based on this Approach

14 GIS Data for Other Perils Tornado Days Per Year Snow Loads Pounds Per Sq. Ft Wind Days Per Year 2/icod_ibc_2012_16_par089.htm 14

15 Example: Wildfire Risk Some predictors of fire loss: Length of road Slope Area of neighborhood Distance to edge of neighborhood Housing Density Distance-to-coast Housing Arrangement and Location Determine the Likelihood of Housing Loss Due to Wildfire (Syphard, et al.) 15

16 Example: Sinkhole Soil permeability Limestone Head difference Subsidence incident reports Start with GIS data reflecting geological characteristics that affect sinkhole risk Model against subsidence incidence reports to get sinkhole risk score Use sinkhole risk score to determine ineligible locations, and combine with insurance claim data to create rates and rating territories 16

17 Know your competition Look at competitiveness by geography and by rating variable 17

18 And then get to know them even better Find specific segments where you are consistently competitive 18

19 Identify profitable segments to target Census Only Census + Black Knight Finds good risks in a generally bad ZIP (Ocala) Use propertylevel prospect data to improve targeting (Rockledge) Finds bad risks in a generally good zip 19

20 Top Predictor Variables Black Knight 1. DwellAge 2. YearBuilt 3. Average Years Owned for ZIP 4. NoOfCars 5. EstMarketValue 6. MarkettoArea 7. EstDwellValue 8. % ZIP with Loan to Value > 100% 12. NoOfUnits 13. OutstandingLoanToMarket 18. Dwelling Value per Square Foot Census 9. NowMarried_Pct 10. SingleMaleHouseholds_Pct 11. HomesHighCostLoan_Pct 14. CrimeIndexPersonal 15. Households60To64_Pct 16. IncomeAvgHouse 17. HousesVacant_Pct 19. HousesVacation_Pct 20. PopulationDensityAge6to PopUnder18_Pct 22. FinancialAssetsAvg 20

21 What is Extra AOP Profit Worth? Sample calculation targeting best 10% of risks Census only model With Black Knight model Current average expected annual AOP profit $16 $16 Average expected AOP loss cost $278 $278 Loss Ratio Relativity of best 10% 73% 36% Expected AOP loss cost of best 10% $202 $101 Decrease in loss cost/increase in annual profit $76 $177 Expected annual profit of best 10% $92 $193 Assumptions: Average AOP Premium = $427 Expected AOP percent profit = 3.7% AOP permissible loss ratio = 65% In this scenario, the Black Knight model selects prospects with $101 higher average profit 21

22 Put it all together Profitability + competiveness + market size = opportunity 22

23 Communicate with and monitor agents Use scoring to monitor portfolio by agent 23

24 Improve your rate indications Rerate historical policies Split indications by peril Calculate a separate cost of reinsurance Expected reinsurer profit = expected ceded premium less expected ceded loss and LAE Allocate to company, state, program, line, form, peril, territory Enhance trend calculation Improve the complement of credibility Map results to see if they make sense Water Relativities by ZIP 24

25 Take actions outside of rates Marketing Underwriting Claims Policy administration 25

26 Challenges for non-large companies What if you don t work for AllStateFarmers? Credibility Data availability Systems limitations In-house expertise / access to technology 26

27 Even small companies have useful data Claims to model claim severity Level of Insight Quotes to model Bind Rate Policies to model Renewal Rate Policies to model claim frequency Combine models to make analytic-based selections (also known as Price Optimization) Minimum sample size (Policies) 27

28 Quote Volume and Bind Rates Over Time 28

29 What variables correlate with bind rate? In other words, what dimensions should we look into more closely? Can include variables not used for rating, for marketing insights Or limit to variables used for rating, for pricing decision support 29

30 Example of Multivariate Segmentation Overall Bind Rate = 18% Year Built < 2004 Bind Rate = 12% 75% of quotes Year Built >= 2004 Bind Rate = 32% 25% of quotes Zone = Inland Bind Rate = 4% 16% of quotes Zone = Coastal Bind Rate = 14% 59% of quotes 30

31 Get started Get your pricing and underwriting right Split rating algorithm, at least by major peril Use GIS data and cat model output to Add new rating factors Redo your territories Get rid of misaligned discounts and rating factors Leverage competitive analysis to make selections Get the most from your marketing Develop profitability measurements to decide where to grow Identify market segments where you are competitive Pinpoint individual homes to pursue where you are profitable and competitive Share insights and target lists with agents 31

32 Questions?

NAR Brief MILLIMAN FLOOD INSURANCE STUDY

NAR Brief MILLIMAN FLOOD INSURANCE STUDY Top Line Summary Independent actuaries studied National Flood Insurance Program (NFIP) rates in 5 counties. The study finds that many property owners are overcharged

NAR Brief MILLIMAN FLOOD INSURANCE STUDY Top Line Summary Independent actuaries studied National Flood Insurance Program (NFIP) rates in 5 counties. The study finds that many property owners are overcharged

Kevin D. Burns, FCAS, MAAA The Hanover Insurance Group

Alternative Methods Kevin D. Burns, FCAS, MAAA The Hanover Insurance Group September 16, 2013 The opinions expressed in this paper (presentation) are the opinions of the author and do not necessarily reflect

Alternative Methods Kevin D. Burns, FCAS, MAAA The Hanover Insurance Group September 16, 2013 The opinions expressed in this paper (presentation) are the opinions of the author and do not necessarily reflect

INTRODUCTION TO NATURAL HAZARD ANALYSIS

INTRODUCTION TO NATURAL HAZARD ANALYSIS November 19, 2013 Thomas A. Delorie, Jr. CSP Managing Director Natural Hazards Are Global and Include: Earthquake Flood Hurricane / Tropical Cyclone / Typhoon Landslides

INTRODUCTION TO NATURAL HAZARD ANALYSIS November 19, 2013 Thomas A. Delorie, Jr. CSP Managing Director Natural Hazards Are Global and Include: Earthquake Flood Hurricane / Tropical Cyclone / Typhoon Landslides

Flood Solutions. Summer 2018

Flood Solutions Summer 2018 Flood Solutions g Summer 2018 Table of Contents Flood for Lending Life of Loan Flood Determination... 2 Multiple Structure Indicator... 2 Future Flood... 2 Natural Hazard Risk...

Flood Solutions Summer 2018 Flood Solutions g Summer 2018 Table of Contents Flood for Lending Life of Loan Flood Determination... 2 Multiple Structure Indicator... 2 Future Flood... 2 Natural Hazard Risk...

THE EVOLUTION OF CATASTROPHE MODELS AND

SERA Charleston, SC THE EVOLUTION OF CATASTROPHE MODELS AND THE REGULATORY IMPLICATIONS OFTHEIR USE April 2015 Richard Piazza Chief Actuary Louisiana Department of Insurance 1 Warning to Regulators! Don

SERA Charleston, SC THE EVOLUTION OF CATASTROPHE MODELS AND THE REGULATORY IMPLICATIONS OFTHEIR USE April 2015 Richard Piazza Chief Actuary Louisiana Department of Insurance 1 Warning to Regulators! Don

RespondTM. You can t do anything about the weather. Or can you?

RespondTM You can t do anything about the weather. Or can you? You can t do anything about the weather Or can you? How insurance firms are using sophisticated natural hazard tracking, analysis, and prediction

RespondTM You can t do anything about the weather. Or can you? You can t do anything about the weather Or can you? How insurance firms are using sophisticated natural hazard tracking, analysis, and prediction

Fundamentals of Catastrophe Modeling. CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010

Fundamentals of Catastrophe Modeling CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010 1 ANTITRUST NOTICE The Casualty Actuarial Society is committed to adhering

Fundamentals of Catastrophe Modeling CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010 1 ANTITRUST NOTICE The Casualty Actuarial Society is committed to adhering

AIR Worldwide Analysis: Exposure Data Quality

AIR Worldwide Analysis: Exposure Data Quality AIR Worldwide Corporation November 14, 2005 ipf Copyright 2005 AIR Worldwide Corporation. All rights reserved. Restrictions and Limitations This document may

AIR Worldwide Analysis: Exposure Data Quality AIR Worldwide Corporation November 14, 2005 ipf Copyright 2005 AIR Worldwide Corporation. All rights reserved. Restrictions and Limitations This document may

Homeowners Ratemaking Revisited

Why Modeling? For lines of business with catastrophe potential, we don t know how much past insurance experience is needed to represent possible future outcomes and how much weight should be assigned to

Why Modeling? For lines of business with catastrophe potential, we don t know how much past insurance experience is needed to represent possible future outcomes and how much weight should be assigned to

Catastrophes and the Advent of the Use of Cat Models in Ratemaking

Catastrophes and the Advent of the Use of Cat Models in Ratemaking Christopher S. Carlson, FCAS, MAAA Pinnacle Actuarial Resources, Inc. Casualty Actuarial Society Catastrophes and the Advent of the Use

Catastrophes and the Advent of the Use of Cat Models in Ratemaking Christopher S. Carlson, FCAS, MAAA Pinnacle Actuarial Resources, Inc. Casualty Actuarial Society Catastrophes and the Advent of the Use

Modeling Extreme Event Risk

Modeling Extreme Event Risk Both natural catastrophes earthquakes, hurricanes, tornadoes, and floods and man-made disasters, including terrorism and extreme casualty events, can jeopardize the financial

Modeling Extreme Event Risk Both natural catastrophes earthquakes, hurricanes, tornadoes, and floods and man-made disasters, including terrorism and extreme casualty events, can jeopardize the financial

National Flood Insurance Program

National Flood Insurance Program A Discussion in Three Parts: The Nature of Flood Risk An Overview of the NFIP Impact of Recent Legislation (BW-12 & HFIAA-14) Nature of Flood Risk FLOODS ARE AN ACT OF

National Flood Insurance Program A Discussion in Three Parts: The Nature of Flood Risk An Overview of the NFIP Impact of Recent Legislation (BW-12 & HFIAA-14) Nature of Flood Risk FLOODS ARE AN ACT OF

Flood Insurance Coverage in Dare County: Before and After Hurricane Floyd

Flood Insurance Coverage in Dare County: Before and After Hurricane Floyd Craig E. Landry Department of Economics Center for Natural Hazards Research East Carolina University National Flood Insurance Program

Flood Insurance Coverage in Dare County: Before and After Hurricane Floyd Craig E. Landry Department of Economics Center for Natural Hazards Research East Carolina University National Flood Insurance Program

Specialty Distribution and You

Specialty Distribution and You 1 AmWINS PROPERTY PRACTICE BY THE NUMBERS #1 Property Wholesaler Broker in the U.S. $2.4 B Annual Premium 111,193 Submissions received annually 48,187 Accounts bound annually

Specialty Distribution and You 1 AmWINS PROPERTY PRACTICE BY THE NUMBERS #1 Property Wholesaler Broker in the U.S. $2.4 B Annual Premium 111,193 Submissions received annually 48,187 Accounts bound annually

AIRCURRENTS: BLENDING SEVERE THUNDERSTORM MODEL RESULTS WITH LOSS EXPERIENCE DATA A BALANCED APPROACH TO RATEMAKING

MAY 2012 AIRCURRENTS: BLENDING SEVERE THUNDERSTORM MODEL RESULTS WITH LOSS EXPERIENCE DATA A BALANCED APPROACH TO RATEMAKING EDITOR S NOTE: The volatility in year-to-year severe thunderstorm losses means

MAY 2012 AIRCURRENTS: BLENDING SEVERE THUNDERSTORM MODEL RESULTS WITH LOSS EXPERIENCE DATA A BALANCED APPROACH TO RATEMAKING EDITOR S NOTE: The volatility in year-to-year severe thunderstorm losses means

2/28/2017. The evolution of home and auto insurance. Agenda. Home & Auto Insurance Evolution Timeline. 1. Home & Auto Insurance Evolution Timeline

The evolution of home and auto insurance Sheri Scott, FCAS, MAAA March 2016 Agenda 1. Home & Auto Insurance Evolution Timeline 2. Millennial Needs Driving Use of Technology and Shared Economy 3. Vehicle

The evolution of home and auto insurance Sheri Scott, FCAS, MAAA March 2016 Agenda 1. Home & Auto Insurance Evolution Timeline 2. Millennial Needs Driving Use of Technology and Shared Economy 3. Vehicle

CATASTROPHIC RISK AND INSURANCE Hurricane and Hydro meteorological Risks

CATASTROPHIC RISK AND INSURANCE Hurricane and Hydro meteorological Risks INTRODUCTORY REMARKS OECD IAIS ASSAL VII Conference on Insurance Regulation and Supervision in Latin America Lisboa, 24-28 April

CATASTROPHIC RISK AND INSURANCE Hurricane and Hydro meteorological Risks INTRODUCTORY REMARKS OECD IAIS ASSAL VII Conference on Insurance Regulation and Supervision in Latin America Lisboa, 24-28 April

Sea Level Rise and the NFIP

Cheryl A Johnson, PE, CFM, PMP March 26, 2014 http://www.globalchange.gov/ Sea-level rise and the likely increase in hurricane intensity and associated storm surge will be among the most serious consequences

Cheryl A Johnson, PE, CFM, PMP March 26, 2014 http://www.globalchange.gov/ Sea-level rise and the likely increase in hurricane intensity and associated storm surge will be among the most serious consequences

Accounting for Long-Term Erosion and Sea Level Rise in New England: A TMAC Recommendation

Accounting for Long-Term Erosion and Sea Level Rise in New England: A TMAC Recommendation Elena Drei-Horgan, PhD, CFM Jeremy Mull, PE Brian Caufield, PE May 2017 Establishment of TMAC, Definition, Members

Accounting for Long-Term Erosion and Sea Level Rise in New England: A TMAC Recommendation Elena Drei-Horgan, PhD, CFM Jeremy Mull, PE Brian Caufield, PE May 2017 Establishment of TMAC, Definition, Members

STATE NATIONAL INSURANCE COMPANY, INC.

INSURANCE APPLICATION STATE NATIONAL INSURANCE COMPANY, INC. APPLICATION DETAIL Effective / Expiration Date Policy Number Date [MM/DD/YYYY] [MM/DD/YYYY] 12:01 AM Standard Time at the residence premises

INSURANCE APPLICATION STATE NATIONAL INSURANCE COMPANY, INC. APPLICATION DETAIL Effective / Expiration Date Policy Number Date [MM/DD/YYYY] [MM/DD/YYYY] 12:01 AM Standard Time at the residence premises

Biggert-Waters Flood Insurance Reform and Modernization Act of 2012

Biggert-Waters Flood Insurance Reform and Modernization Act of 2012 On July 6, 2012, President Obama signed into law the Biggert-Waters Flood Insurance Reform Act of 2012, which reauthorizes and reforms

Biggert-Waters Flood Insurance Reform and Modernization Act of 2012 On July 6, 2012, President Obama signed into law the Biggert-Waters Flood Insurance Reform Act of 2012, which reauthorizes and reforms

The AIR Coastal Flood Model for Great Britain

The AIR Coastal Flood Model for Great Britain The North Sea Flood of 1953 inundated more than 100,000 hectares in eastern England. More than 24,000 properties were damaged, and 307 people lost their lives.

The AIR Coastal Flood Model for Great Britain The North Sea Flood of 1953 inundated more than 100,000 hectares in eastern England. More than 24,000 properties were damaged, and 307 people lost their lives.

Flood Insurance THE TOPIC OCTOBER 2012

Flood Insurance THE TOPIC OCTOBER 2012 Because of frequent flooding of the Mississippi River during the 1960s and the rising cost of taxpayer funded disaster relief for flood victims, in 1968 Congress

Flood Insurance THE TOPIC OCTOBER 2012 Because of frequent flooding of the Mississippi River during the 1960s and the rising cost of taxpayer funded disaster relief for flood victims, in 1968 Congress

VULNERABILITY ASSESSMENT

SOUTHSIDE HAMPTON ROADS HAZARD MITIGATION PLAN VULNERABILITY ASSESSMENT INTRODUCTION The Vulnerability Assessment section builds upon the information provided in the Hazard Identification and Analysis

SOUTHSIDE HAMPTON ROADS HAZARD MITIGATION PLAN VULNERABILITY ASSESSMENT INTRODUCTION The Vulnerability Assessment section builds upon the information provided in the Hazard Identification and Analysis

ACTUARIAL FLOOD STANDARDS

ACTUARIAL FLOOD STANDARDS AF-1 Flood Modeling Input Data and Output Reports A. Adjustments, edits, inclusions, or deletions to insurance company or other input data used by the modeling organization shall

ACTUARIAL FLOOD STANDARDS AF-1 Flood Modeling Input Data and Output Reports A. Adjustments, edits, inclusions, or deletions to insurance company or other input data used by the modeling organization shall

Potential Assessments from Florida Hurricanes

April 2, 2012 Potential Assessments from Florida Hurricanes Office of the Insurance Consumer Advocate State of Florida Prepared by: Stephen A. Alexander, FCAS, MAAA TABLE OF CONTENTS SCOPE... 3 LIMITATIONS...

April 2, 2012 Potential Assessments from Florida Hurricanes Office of the Insurance Consumer Advocate State of Florida Prepared by: Stephen A. Alexander, FCAS, MAAA TABLE OF CONTENTS SCOPE... 3 LIMITATIONS...

Wildfire and Flood Hazards, Using GIS Tools to Assess Risk

Wildfire and Flood Hazards, Using GIS Tools to Assess Risk Floodplain Management Association Conference, Rancho Mirage, CA September 2015 Thoughts To Keep In Mind What advantages are there in looking at

Wildfire and Flood Hazards, Using GIS Tools to Assess Risk Floodplain Management Association Conference, Rancho Mirage, CA September 2015 Thoughts To Keep In Mind What advantages are there in looking at

THE NATIONAL FLOOD INSURANCE PROGRAM: Challenges and Solutions

THE NATIONAL FLOOD INSURANCE PROGRAM: Challenges and Solutions American Academy of Actuaries Flood Insurance Work Group Capitol Hill Briefing June 26, 2017 American Academy of Actuaries The American Academy

THE NATIONAL FLOOD INSURANCE PROGRAM: Challenges and Solutions American Academy of Actuaries Flood Insurance Work Group Capitol Hill Briefing June 26, 2017 American Academy of Actuaries The American Academy

Canada s exposure to flood risk. Who is affected, where are they located, and what is at stake

Canada s exposure to flood risk Who is affected, where are they located, and what is at stake Why a flood model for Canada? Catastrophic losses Insurance industry Federal government Average industry CAT

Canada s exposure to flood risk Who is affected, where are they located, and what is at stake Why a flood model for Canada? Catastrophic losses Insurance industry Federal government Average industry CAT

CL-3: Catastrophe Modeling for Commercial Lines

CL-3: Catastrophe Modeling for Commercial Lines David Lalonde, FCAS, FCIA, MAAA Casualty Actuarial Society, Ratemaking and Product Management Seminar March 12-13, 2013 Huntington Beach, CA 2013 AIR WORLDWIDE

CL-3: Catastrophe Modeling for Commercial Lines David Lalonde, FCAS, FCIA, MAAA Casualty Actuarial Society, Ratemaking and Product Management Seminar March 12-13, 2013 Huntington Beach, CA 2013 AIR WORLDWIDE

Risk, Mitigation, & Planning

Risk, Mitigation, & Planning Lessons from Flooding in the Houston Area Russell Blessing, Samuel Brody & Wesley Highfield CUMULATIVE FLOOD LOSS: 1972-2015 INSURED FLOOD LOSS: 1972-2015 THE HOUSTON-GALVESTON

Risk, Mitigation, & Planning Lessons from Flooding in the Houston Area Russell Blessing, Samuel Brody & Wesley Highfield CUMULATIVE FLOOD LOSS: 1972-2015 INSURED FLOOD LOSS: 1972-2015 THE HOUSTON-GALVESTON

September 8, RE: Application for Planned Unit Development and Special Exemption Permit by Bluff Point Holdings LLC

September 8, 2011 Northumberland County Board of Supervisors P.O. Box 129 Heathsville, VA 22473 RE: Application for Planned Unit Development and Special Exemption Permit by Bluff Point Holdings LLC Dear

September 8, 2011 Northumberland County Board of Supervisors P.O. Box 129 Heathsville, VA 22473 RE: Application for Planned Unit Development and Special Exemption Permit by Bluff Point Holdings LLC Dear

Homeowners ROE Outlook

Aon Benfield Homeowners ROE Outlook October 21 Risk. Reinsurance. Human Resources. Homeowners: Positive Outlook, Expanding Growth Opportunities For a nationwide, personal lines insurer the overall outlook

Aon Benfield Homeowners ROE Outlook October 21 Risk. Reinsurance. Human Resources. Homeowners: Positive Outlook, Expanding Growth Opportunities For a nationwide, personal lines insurer the overall outlook

TABLE OF CONTENTS OVERVIEW...1 BINDING AUTHORITY...1 ELIGIBILITY CRITERIA...2 COVERAGE LIMITS.3 COVERAGES.3-4 LOSS SETTLEMENT 5-7 MID-TERM CHANGES..

Commercial Hurricane Underwriting Manual 2016 TABLE OF CONTENTS OVERVIEW...1 BINDING AUTHORITY...1 ELIGIBILITY CRITERIA...2 COVERAGE LIMITS.3 COVERAGES.3-4 LOSS SETTLEMENT 5-7 MID-TERM CHANGES..8 CANCELLATIONS..8

Commercial Hurricane Underwriting Manual 2016 TABLE OF CONTENTS OVERVIEW...1 BINDING AUTHORITY...1 ELIGIBILITY CRITERIA...2 COVERAGE LIMITS.3 COVERAGES.3-4 LOSS SETTLEMENT 5-7 MID-TERM CHANGES..8 CANCELLATIONS..8

TESTIMONY. Association of State Floodplain Managers, Inc.

ASSOCIATION OF STATE FLOODPLAIN MANAGERS, INC. 2809 Fish Hatchery Road, Suite 204, Madison, Wisconsin 53713 www.floods.org Phone: 608-274-0123 Fax: 608-274-0696 Email: asfpm@floods.org TESTIMONY Association

ASSOCIATION OF STATE FLOODPLAIN MANAGERS, INC. 2809 Fish Hatchery Road, Suite 204, Madison, Wisconsin 53713 www.floods.org Phone: 608-274-0123 Fax: 608-274-0696 Email: asfpm@floods.org TESTIMONY Association

Everything You Need to Know about the PCS Catastrophe Loss Index

Everything You Need to Know about the Since 1949, the property/casualty insurance industry has relied on catastrophe loss estimates from PCS and its predecessor organizations to set catastrophe reserves

Everything You Need to Know about the Since 1949, the property/casualty insurance industry has relied on catastrophe loss estimates from PCS and its predecessor organizations to set catastrophe reserves

Fourth Quarter and Full Year Highlights

Exhibit 99.1 The Hanover Reports Fourth Quarter Net Income and Operating Income of $1.20 and $2.00 per Diluted Share, Respectively; Fourth Quarter Combined Ratio of 95.1%; Combined Ratio Excluding Catastrophes

Exhibit 99.1 The Hanover Reports Fourth Quarter Net Income and Operating Income of $1.20 and $2.00 per Diluted Share, Respectively; Fourth Quarter Combined Ratio of 95.1%; Combined Ratio Excluding Catastrophes

COASTALRISK. FLOODANDNATURALHAZARDRISKASSESSMENT Commercial Mayport Naval Station, Jacksonville, FL September 7, 2018

COASTALRISK FLOODANDNATURALHAZARDRISKASSESSMENT Commercial September 7, 2018 THISREPORTISPROVIDEDSUBJECTTOTHECOASTALRISKCONSULTING,LLC.TERMSANDCONDITIONSOFUSE,WHICHIS AVAILABLEATWWW.COASTALRISKCONSULTING.COM.THISANALYSISISFURNISHED

COASTALRISK FLOODANDNATURALHAZARDRISKASSESSMENT Commercial September 7, 2018 THISREPORTISPROVIDEDSUBJECTTOTHECOASTALRISKCONSULTING,LLC.TERMSANDCONDITIONSOFUSE,WHICHIS AVAILABLEATWWW.COASTALRISKCONSULTING.COM.THISANALYSISISFURNISHED

Catastrophe Models: Learning from Superstorm Sandy

Catastrophe Models: Learning from Superstorm Sandy January 2013 Lockton Companies Although Superstorm Sandy was only a Category 1 hurricane, it made landfall on October 29 as the largest Atlantic hurricane

Catastrophe Models: Learning from Superstorm Sandy January 2013 Lockton Companies Although Superstorm Sandy was only a Category 1 hurricane, it made landfall on October 29 as the largest Atlantic hurricane

Putting a price on political risk

Putting a price on political risk Telecoms Leisure Agriculture Transportation and logistics Financial Power Utilities Retail Metals and mining Oil and gas WHAT IS POLITICAL RISK? Political risk is the

Putting a price on political risk Telecoms Leisure Agriculture Transportation and logistics Financial Power Utilities Retail Metals and mining Oil and gas WHAT IS POLITICAL RISK? Political risk is the

AIRCURRENTS: NEW TOOLS TO ACCOUNT FOR NON-MODELED SOURCES OF LOSS

JANUARY 2013 AIRCURRENTS: NEW TOOLS TO ACCOUNT FOR NON-MODELED SOURCES OF LOSS EDITOR S NOTE: In light of recent catastrophes, companies are re-examining their portfolios with an increased focus on the

JANUARY 2013 AIRCURRENTS: NEW TOOLS TO ACCOUNT FOR NON-MODELED SOURCES OF LOSS EDITOR S NOTE: In light of recent catastrophes, companies are re-examining their portfolios with an increased focus on the

Homeowners' ROE Outlook. October 2018

Homeowners' ROE Outlook October 8 Homeowners: Growing, Profitable, and Continued Opportunities to Differentiate through Innovation The past several editions of this study described homeowners as a growth

Homeowners' ROE Outlook October 8 Homeowners: Growing, Profitable, and Continued Opportunities to Differentiate through Innovation The past several editions of this study described homeowners as a growth

The AIR Typhoon Model for South Korea

The AIR Typhoon Model for South Korea Every year about 30 tropical cyclones develop in the Northwest Pacific Basin. On average, at least one makes landfall in South Korea. Others pass close enough offshore

The AIR Typhoon Model for South Korea Every year about 30 tropical cyclones develop in the Northwest Pacific Basin. On average, at least one makes landfall in South Korea. Others pass close enough offshore

MULTI-LINE REINSURANCE

MULTI-LINE REINSURANCE SPECIALTY LINES PROPERTY PROPERTY CATASTROPHE FLAGSTONE RÉASSURANCE SUISSE SA - BERMUDA BRANCH Important Facts Flagstone Réassurance Suisse SA - Bermuda Branch is a wholly owned

MULTI-LINE REINSURANCE SPECIALTY LINES PROPERTY PROPERTY CATASTROPHE FLAGSTONE RÉASSURANCE SUISSE SA - BERMUDA BRANCH Important Facts Flagstone Réassurance Suisse SA - Bermuda Branch is a wholly owned

In comparison, much less modeling has been done in Homeowners

Predictive Modeling for Homeowners David Cummings VP & Chief Actuary ISO Innovative Analytics 1 Opportunities in Predictive Modeling Lessons from Personal Auto Major innovations in historically static

Predictive Modeling for Homeowners David Cummings VP & Chief Actuary ISO Innovative Analytics 1 Opportunities in Predictive Modeling Lessons from Personal Auto Major innovations in historically static

Catastrophe Risk Management

Catastrophe Risk Management Complete. Current. Connected. TOM LARSEN How will catastrophe modeling be used in the insurance enterprise of the future? Catastrophe modeling is a profound technology that

Catastrophe Risk Management Complete. Current. Connected. TOM LARSEN How will catastrophe modeling be used in the insurance enterprise of the future? Catastrophe modeling is a profound technology that

The Alabama Coastal Insurance Shopper's Guide. Are you paying too much? Do you have the right coverage?

The Alabama Coastal Insurance Shopper's Guide Are you paying too much? Do you have the right coverage? Contents Introduction... 1 Section I: The Process of Buying Homeowners Insurance... 2 Section II:

The Alabama Coastal Insurance Shopper's Guide Are you paying too much? Do you have the right coverage? Contents Introduction... 1 Section I: The Process of Buying Homeowners Insurance... 2 Section II:

Talk Components. Wharton Risk Center & Research Context TC Flood Research Approach Freshwater Flood Main Results

Dr. Jeffrey Czajkowski (jczaj@wharton.upenn.edu) Willis Research Network Autumn Seminar November 1, 2017 Talk Components Wharton Risk Center & Research Context TC Flood Research Approach Freshwater Flood

Dr. Jeffrey Czajkowski (jczaj@wharton.upenn.edu) Willis Research Network Autumn Seminar November 1, 2017 Talk Components Wharton Risk Center & Research Context TC Flood Research Approach Freshwater Flood

Natural Hazards Risks in Kentucky. KAMM Regional Training

Natural Hazards Risks in Kentucky KAMM Regional Training Floodplain 101 Kentucky has approximately 92,000 linear miles of streams and rivers Approximately 31,000 linear miles have mapped flood hazards

Natural Hazards Risks in Kentucky KAMM Regional Training Floodplain 101 Kentucky has approximately 92,000 linear miles of streams and rivers Approximately 31,000 linear miles have mapped flood hazards

Executive Summary. Annual Recommended 2019 Rate Filings

1 Page Annual Recommended 2019 Rate Filings As required by statute, Citizens has completed the annual analysis of recommended rates for 2019. The Office of Insurance Regulation uses this information as

1 Page Annual Recommended 2019 Rate Filings As required by statute, Citizens has completed the annual analysis of recommended rates for 2019. The Office of Insurance Regulation uses this information as

SOUTH CENTRAL REGION MULTI-JURISDICTION HAZARD MITIGATION PLAN. Advisory Committee Meeting September 12, 2012

SOUTH CENTRAL REGION MULTI-JURISDICTION HAZARD MITIGATION PLAN Advisory Committee Meeting September 12, 2012 AGENDA FOR TODAY Purpose of Meeting Engage All Advisory Committee Members Distribute Project

SOUTH CENTRAL REGION MULTI-JURISDICTION HAZARD MITIGATION PLAN Advisory Committee Meeting September 12, 2012 AGENDA FOR TODAY Purpose of Meeting Engage All Advisory Committee Members Distribute Project

Louisiana Legislative Auditor

Louisiana Legislative Auditor Steve J. Theriot, CPA Legislative Auditor Insurance Rate Quotes for Hurricane-Affected Areas Information Report October 2006 This report was developed to provide current information

Louisiana Legislative Auditor Steve J. Theriot, CPA Legislative Auditor Insurance Rate Quotes for Hurricane-Affected Areas Information Report October 2006 This report was developed to provide current information

FEMA FLOOD MAPS Public Works Department Stormwater Management Division March 6, 2018

FEMA FLOOD MAPS Public Works Department Stormwater Management Division March 6, 2018 Presentation Overview FEMA National Flood Insurance Program (NFIP) FEMA Community Rating System (CRS) Flood Insurance

FEMA FLOOD MAPS Public Works Department Stormwater Management Division March 6, 2018 Presentation Overview FEMA National Flood Insurance Program (NFIP) FEMA Community Rating System (CRS) Flood Insurance

CAT301 Catastrophe Management in a Time of Financial Crisis. Will Gardner Aon Re Global

CAT301 Catastrophe Management in a Time of Financial Crisis Will Gardner Aon Re Global Agenda CAT101 and CAT201 Revision The Catastrophe Control Cycle Implications of the Financial Crisis CAT101 - An Application

CAT301 Catastrophe Management in a Time of Financial Crisis Will Gardner Aon Re Global Agenda CAT101 and CAT201 Revision The Catastrophe Control Cycle Implications of the Financial Crisis CAT101 - An Application

2015 AEG Professional Landslide Forum February 26-28, 2015

2015 AEG Professional Landslide Forum February 26-28, 2015 Keynote 3: Lessons from the National Earthquake Hazards Reduction Program Can be Applied to the National Landslide Hazards Program: A Rational

2015 AEG Professional Landslide Forum February 26-28, 2015 Keynote 3: Lessons from the National Earthquake Hazards Reduction Program Can be Applied to the National Landslide Hazards Program: A Rational

Managing Data for Analytics. April 14, 2015

Managing Data for Analytics April 14, 2015 1 Importance of Predictive Analytics Predictive Analytics can help insurers be more effective in all segments of the value chain Marketing Target and acquire

Managing Data for Analytics April 14, 2015 1 Importance of Predictive Analytics Predictive Analytics can help insurers be more effective in all segments of the value chain Marketing Target and acquire

Background Info on SSIC. Filing History. What the Filing Will Achieve. Filing framework. Our Objectives in the Filing

May 17, 2012 Background Info on SSIC Filing History What the Filing Will Achieve Filing framework Our Objectives in the Filing 2 Incorporated on November 21, 1997 - one of the oldest Florida domiciled

May 17, 2012 Background Info on SSIC Filing History What the Filing Will Achieve Filing framework Our Objectives in the Filing 2 Incorporated on November 21, 1997 - one of the oldest Florida domiciled

Contents. Introduction to Catastrophe Models and Working with their Output. Natural Hazard Risk and Cat Models Applications Practical Issues

Introduction to Catastrophe Models and Working with their Output Richard Evans Andrew Ford Paul Kaye 1 Contents Natural Hazard Risk and Cat Models Applications Practical Issues 1 Natural Hazard Risk and

Introduction to Catastrophe Models and Working with their Output Richard Evans Andrew Ford Paul Kaye 1 Contents Natural Hazard Risk and Cat Models Applications Practical Issues 1 Natural Hazard Risk and

The AIR Inland Flood Model for Great Britian

The AIR Inland Flood Model for Great Britian The year 212 was the UK s second wettest since recordkeeping began only 6.6 mm shy of the record set in 2. In 27, the UK experienced its wettest summer, which

The AIR Inland Flood Model for Great Britian The year 212 was the UK s second wettest since recordkeeping began only 6.6 mm shy of the record set in 2. In 27, the UK experienced its wettest summer, which

Homeowners & Dwelling/Fire Rate Filings & Rate Collection System

2014 Industry Conference Navigating the Changing Insurance Environment Homeowners & Dwelling/Fire Rate Filings & Rate Collection System Robert Lee, Actuary, Property Casualty Product Review Kayne Smith,

2014 Industry Conference Navigating the Changing Insurance Environment Homeowners & Dwelling/Fire Rate Filings & Rate Collection System Robert Lee, Actuary, Property Casualty Product Review Kayne Smith,

The utilization and cost of reinsurance is a significant consideration in

A American DECEMBER 2008 Academy of Actuaries The American Academy of Actuaries is a national organization formed in 1965 to bring together, in a single entity, actuaries of all specializations within

A American DECEMBER 2008 Academy of Actuaries The American Academy of Actuaries is a national organization formed in 1965 to bring together, in a single entity, actuaries of all specializations within

OICONNECT Policy Administration System LIGHTNING QUOTE

OICONNECT Policy Administration System LIGHTNING QUOTE Agent User Guide OLYMPUS INSURANCE COMPANY PO Box 32879, PALM BEACH GARDENS, FL 33410 1 BEGIN A LIGHTNING QUOTE 1.1 Beginning a Lightning Quote Page

OICONNECT Policy Administration System LIGHTNING QUOTE Agent User Guide OLYMPUS INSURANCE COMPANY PO Box 32879, PALM BEACH GARDENS, FL 33410 1 BEGIN A LIGHTNING QUOTE 1.1 Beginning a Lightning Quote Page

Less Risky Business. In Catastrophe Planning, Location Intelligence Combined with Superior Data Can Mitigate Exposure and Improve Risk Management

Solutions for Customer Intelligence, Communications and Care. W HITE PAPER: insurance WHITE PAPER: insurance 2 abstract challenges: over-exposure and high risk The year 2010 marked the fifth anniversary

Solutions for Customer Intelligence, Communications and Care. W HITE PAPER: insurance WHITE PAPER: insurance 2 abstract challenges: over-exposure and high risk The year 2010 marked the fifth anniversary

QUICK GUIDE. An Introduction to COPE Data. Copyright 2017 AssetWorks Inc. All Rights Reserved. For more information visit,

QUICK GUIDE An Introduction to COPE Data An Introduction to COPE Data The collection of COPE data is important for organizations. It s four data categories construction, occupancy, protection, and exposure

QUICK GUIDE An Introduction to COPE Data An Introduction to COPE Data The collection of COPE data is important for organizations. It s four data categories construction, occupancy, protection, and exposure

Citizens Property Insurance Corporation: 2013 Rate Hearing. Thursday, September 20, 2012

Citizens Property Insurance Corporation: 2013 Rate Hearing Thursday, September 20, 2012 Citizens Mission and Vision Citizens public purpose is to serve the people of Florida by providing property and casualty

Citizens Property Insurance Corporation: 2013 Rate Hearing Thursday, September 20, 2012 Citizens Mission and Vision Citizens public purpose is to serve the people of Florida by providing property and casualty

THE NATIONAL FLOOD INSURANCE PROGRAM: CHALLENGES AND SOLUTIONS

APRIL 2017 THE NATIONAL FLOOD INSURANCE PROGRAM: CHALLENGES AND SOLUTIONS American Academy of Actuaries Flood Insurance Work Group ACTUARY.ORG Flood Insurance Work Group Rade Musulin, MAAA, ACAS, Chairperson

APRIL 2017 THE NATIONAL FLOOD INSURANCE PROGRAM: CHALLENGES AND SOLUTIONS American Academy of Actuaries Flood Insurance Work Group ACTUARY.ORG Flood Insurance Work Group Rade Musulin, MAAA, ACAS, Chairperson

Homeowners' ROE Outlook

Aon Benfield Homeowners' ROE Outlook Growth. Divergent Markets. Technological Innovation. October 7 Homeowners: Growth. Divergent Markets. Technological Innovation. The estimated prospective ROE for homeowners

Aon Benfield Homeowners' ROE Outlook Growth. Divergent Markets. Technological Innovation. October 7 Homeowners: Growth. Divergent Markets. Technological Innovation. The estimated prospective ROE for homeowners

Sensitivity Analyses: Capturing the. Introduction. Conceptualizing Uncertainty. By Kunal Joarder, PhD, and Adam Champion

Sensitivity Analyses: Capturing the Most Complete View of Risk 07.2010 Introduction Part and parcel of understanding catastrophe modeling results and hence a company s catastrophe risk profile is an understanding

Sensitivity Analyses: Capturing the Most Complete View of Risk 07.2010 Introduction Part and parcel of understanding catastrophe modeling results and hence a company s catastrophe risk profile is an understanding

Quantifying Riverine and Storm-Surge Flood Risk by Single-Family Residence: Application to Texas

CREATE Research Archive Published Articles & Papers 2013 Quantifying Riverine and Storm-Surge Flood Risk by Single-Family Residence: Application to Texas Jeffrey Czajkowski University of Pennsylvania Howard

CREATE Research Archive Published Articles & Papers 2013 Quantifying Riverine and Storm-Surge Flood Risk by Single-Family Residence: Application to Texas Jeffrey Czajkowski University of Pennsylvania Howard

Considerations When Developing Actuarially Sound Rates for Lender Placed Property Insurance

Considerations When Developing Actuarially Sound Rates for Lender Placed Property Insurance Sheri L. Scott, FCAS, MAAA Consulting Actuary, Milliman Inc. NAIC August 9, 2012 Meeting Discussion Topics 1.

Considerations When Developing Actuarially Sound Rates for Lender Placed Property Insurance Sheri L. Scott, FCAS, MAAA Consulting Actuary, Milliman Inc. NAIC August 9, 2012 Meeting Discussion Topics 1.

Q: Did the Subcommittee consider a contingency provision?

Based on Dr. Appel s analysis, this 9% underwriting profit provision would generate a statutory return on net worth of 6.8%. That return is significantly below Dr. Vander Weide s lower bound of 9.0%. It

Based on Dr. Appel s analysis, this 9% underwriting profit provision would generate a statutory return on net worth of 6.8%. That return is significantly below Dr. Vander Weide s lower bound of 9.0%. It

An Approach to Pricing Natural Perils

17th An Approach to Pricing Natural Perils Tim Andrews David McNab Ada Lui Finity Consulting Pty Ltd 2010 Why is everyone talking about the weather? The Melbourne and Perth storms were further evidence

17th An Approach to Pricing Natural Perils Tim Andrews David McNab Ada Lui Finity Consulting Pty Ltd 2010 Why is everyone talking about the weather? The Melbourne and Perth storms were further evidence

Presented by: Brian T. Ford, CPCU, MBA of Insurance Resources and Ashley Tharp of Wright Flood

Presented by: Brian T. Ford, CPCU, MBA of Insurance Resources and Ashley Tharp of Wright Flood National Flood Insurance Program 1/28/69 Goals Prevent future loss of life & property Reduce public monies

Presented by: Brian T. Ford, CPCU, MBA of Insurance Resources and Ashley Tharp of Wright Flood National Flood Insurance Program 1/28/69 Goals Prevent future loss of life & property Reduce public monies

Third Quarter Highlights

Exhibit 99.1 The Hanover Reports Third Quarter Net Income and Operating Income of $2.33 and $1.97 per Diluted Share, Respectively; Third Quarter Combined Ratio of 95.1%; Combined Ratio, Excluding Catastrophes,

Exhibit 99.1 The Hanover Reports Third Quarter Net Income and Operating Income of $2.33 and $1.97 per Diluted Share, Respectively; Third Quarter Combined Ratio of 95.1%; Combined Ratio, Excluding Catastrophes,

Data Sources. Rob Curry Roosevelt Mosley National Association of Insurance Commissioners

Data Sources Rob Curry Roosevelt Mosley 2017 National Association of Insurance Commissioners DATA SOURCES Rob Curry, MAAA, FCAS Roosevelt Mosley, MAAA, FCAS Learning Objectives At the end of this presentation,

Data Sources Rob Curry Roosevelt Mosley 2017 National Association of Insurance Commissioners DATA SOURCES Rob Curry, MAAA, FCAS Roosevelt Mosley, MAAA, FCAS Learning Objectives At the end of this presentation,

Reactions to Catastrophic Events: A Look at Insurers, Consumers, and Regulators. Patricia Born, PhD

Reactions to Catastrophic Events: A Look at Insurers, Consumers, and Regulators Patricia Born, PhD Agenda Introduction Insurer Responses over 30 Years Consumer Responses Regulatory Considerations Introduction

Reactions to Catastrophic Events: A Look at Insurers, Consumers, and Regulators Patricia Born, PhD Agenda Introduction Insurer Responses over 30 Years Consumer Responses Regulatory Considerations Introduction

Citizens Property Insurance Corporation Financial Overview

Citizens Property Insurance Corporation Financial Overview Barry Gilway President, CEO and Executive Director Financial Overview YTD Change Change Financial Summary (in billions) Q3-2016 2015 2014 Accounts

Citizens Property Insurance Corporation Financial Overview Barry Gilway President, CEO and Executive Director Financial Overview YTD Change Change Financial Summary (in billions) Q3-2016 2015 2014 Accounts

Helping to Avert Catastrophe

Insurance White Paper Helping to Avert Catastrophe How Real-Time Location Intelligence Can Mitigate Exposure and Better Manage Risk Challenges: Over-Exposure and High Risk Location, location, location

Insurance White Paper Helping to Avert Catastrophe How Real-Time Location Intelligence Can Mitigate Exposure and Better Manage Risk Challenges: Over-Exposure and High Risk Location, location, location

2015 Mobile County, Alabama Multi-Hazard Mitigation Plan Appendices

2015 Mobile County, Alabama Multi-Hazard Mitigation Plan A - Federal Requirements for local Mitigation Plans B - Community Mitigation Capabilities C - 2009 Plan Implementation Status D - Hazard Ratings

2015 Mobile County, Alabama Multi-Hazard Mitigation Plan A - Federal Requirements for local Mitigation Plans B - Community Mitigation Capabilities C - 2009 Plan Implementation Status D - Hazard Ratings

Key Fundamentals of Flood Insurance in the NFIP!

a Welcome to Key Fundamentals of Flood Insurance in the NFIP! A Before and After approach for Housing Counselors Presented by: 1 Before the Flood Presenter Melanie Graham After the Flood Presenter Erin

a Welcome to Key Fundamentals of Flood Insurance in the NFIP! A Before and After approach for Housing Counselors Presented by: 1 Before the Flood Presenter Melanie Graham After the Flood Presenter Erin

June 21, Department of the Treasury Federal Insurance Office, Room 1319 MT 1500 Pennsylvania Avenue, N.W. Washington, DC 20220

June 21, 2013 Department of the Treasury Federal Insurance Office, Room 1319 MT 1500 Pennsylvania Avenue, N.W. Washington, DC 20220 Re: Study on Natural Catastrophes and Insurance Dear Director McRaith:

June 21, 2013 Department of the Treasury Federal Insurance Office, Room 1319 MT 1500 Pennsylvania Avenue, N.W. Washington, DC 20220 Re: Study on Natural Catastrophes and Insurance Dear Director McRaith:

Account History and Characteristics Citizens Property Insurance Corporation. March 2016

History and Characteristics Citizens Property Insurance Corporation March 2016 Timeline of Citizens s FWUA FPCJUA FPCJUA merges with Citizens Property Insurance Corporation High-Risk Lines Lines PCJUA

History and Characteristics Citizens Property Insurance Corporation March 2016 Timeline of Citizens s FWUA FPCJUA FPCJUA merges with Citizens Property Insurance Corporation High-Risk Lines Lines PCJUA

Federal Flood Insurance Changes (National Flood Insurance Program NFIP)

") Federal Flood Insurance Changes (National Flood Insurance Program NFIP) Biggert-Waters (BW-12) Flood Insurance Reform Act 2012 HR 4348 Signed by the President on July 6, 2012 Public Works, Engineering

Federal Flood Insurance Changes (National Flood Insurance Program NFIP) Biggert-Waters (BW-12) Flood Insurance Reform Act 2012 HR 4348 Signed by the President on July 6, 2012 Public Works, Engineering

The Role of ERM in Reinsurance Decisions

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

Property & Casualty Insurance: Getting Risk Right

Property & Casualty Insurance: Getting Risk Right Underwriting and location intelligence. A WHITEPAPER BY CANADIAN UNDERWRITER Sponsored by: Written by Canadian Underwriter Sponsored by DMTI Spatial INTRODUCTION

Property & Casualty Insurance: Getting Risk Right Underwriting and location intelligence. A WHITEPAPER BY CANADIAN UNDERWRITER Sponsored by: Written by Canadian Underwriter Sponsored by DMTI Spatial INTRODUCTION

RISK MANAGEMENT NEXT GENERATION

RISK MANAGEMENT NEXT GENERATION STATE UPDATE July 2014 Marc Stanard / John Dorman Risk Management Key Components and National Status Risk Monitoring No digital tracking Big Elephant to Track Not Tied to

RISK MANAGEMENT NEXT GENERATION STATE UPDATE July 2014 Marc Stanard / John Dorman Risk Management Key Components and National Status Risk Monitoring No digital tracking Big Elephant to Track Not Tied to

All-Hazards Homeowners Insurance: A Possibility for the United States?

All-Hazards Homeowners Insurance: A Possibility for the United States? Howard Kunreuther Key Points In the United States, standard homeowners insurance policies do not include coverage for earthquakes

All-Hazards Homeowners Insurance: A Possibility for the United States? Howard Kunreuther Key Points In the United States, standard homeowners insurance policies do not include coverage for earthquakes

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016 Boston Catherine Eska The Hanover Insurance Group Paul Silberbush Guy Carpenter & Co. Ronald Wilkins - PartnerRe Economic Capital Modeling Safe Harbor Notice

ECONOMIC CAPITAL MODELING CARe Seminar JUNE 2016 Boston Catherine Eska The Hanover Insurance Group Paul Silberbush Guy Carpenter & Co. Ronald Wilkins - PartnerRe Economic Capital Modeling Safe Harbor Notice

Sandy + BW-12: Changing the Equation for Building Safer, More Resilient Communities

Sandy + BW-12: Changing the Equation for Building Safer, More Resilient Communities Grant Smith Jerry Sparks Jean Huang Ken Logsdon Stephanie Routh Session Agenda Moderators: Grant Smith & Jerry Sparks

Sandy + BW-12: Changing the Equation for Building Safer, More Resilient Communities Grant Smith Jerry Sparks Jean Huang Ken Logsdon Stephanie Routh Session Agenda Moderators: Grant Smith & Jerry Sparks

AGENDA RISK MANAGEMENT CONSIDERATIONS REINSURANCE IMPLICATIONS CATASTROPHE MODELING OVERVIEW GUY CARPENTER

AGENDA! CATASTROPHE MODELING OVERVIEW RISK MANAGEMENT CONSIDERATIONS REINSURANCE IMPLICATIONS CATASTROPHE MODELING OVERVIEW 2 What is Catastrophe or Cat Modeling? 3 What is Catastrophe or Cat Modeling?

AGENDA! CATASTROPHE MODELING OVERVIEW RISK MANAGEMENT CONSIDERATIONS REINSURANCE IMPLICATIONS CATASTROPHE MODELING OVERVIEW 2 What is Catastrophe or Cat Modeling? 3 What is Catastrophe or Cat Modeling?

Canadian Institute of Actuaries Conference CATASTROPHE MODELING 2012 AND BEYOND JUNE 21, Sherry Thomas Krista Lienau

Canadian Institute of Actuaries Conference CATASTROPHE MODELING 2012 AND BEYOND JUNE 21, 2012 Sherry Thomas Krista Lienau Catastrophe Modeling 2012 and Beyond Agenda Current landscape of Canadian catastrophe

Canadian Institute of Actuaries Conference CATASTROPHE MODELING 2012 AND BEYOND JUNE 21, 2012 Sherry Thomas Krista Lienau Catastrophe Modeling 2012 and Beyond Agenda Current landscape of Canadian catastrophe

Southwest Florida Healthcare Coalition

Southwest Florida Healthcare Coalition Hazards Vulnerability Assessment 2018 1 Table of Contents Summary 3 EmPower Maps and Data 5 Social Vulnerability Index Maps 19 Suncoast Disaster Healthcare Coalition

Southwest Florida Healthcare Coalition Hazards Vulnerability Assessment 2018 1 Table of Contents Summary 3 EmPower Maps and Data 5 Social Vulnerability Index Maps 19 Suncoast Disaster Healthcare Coalition

Data Analytics Tuesday, September 29, 2015

Data Analytics Tuesday, September 29, 2015 Jeff Kucera, FCAS, MAAA Actuary and Consultant e2value, Inc. Hawthorn Woods, Ill. Jeff Kucera is an actuary and consultant for e2value, the leading provider of

Data Analytics Tuesday, September 29, 2015 Jeff Kucera, FCAS, MAAA Actuary and Consultant e2value, Inc. Hawthorn Woods, Ill. Jeff Kucera is an actuary and consultant for e2value, the leading provider of

An Introduction to Natural Catastrophe Modelling at Twelve Capital. Dr. Jan Kleinn Head of ILS Analytics

An Introduction to Natural Catastrophe Modelling at Twelve Capital Dr. Jan Kleinn Head of ILS Analytics For professional/qualified investors use only, Q2 2015 Basic Concept Hazard Stochastic modelling

An Introduction to Natural Catastrophe Modelling at Twelve Capital Dr. Jan Kleinn Head of ILS Analytics For professional/qualified investors use only, Q2 2015 Basic Concept Hazard Stochastic modelling

NCOIL Summer Meeting. Flood Insurance: What s Holding Back the Private Market?

NCOIL Summer Meeting Flood Insurance: What s Holding Back the Private Market? July 11, 2014 Michael Angelina, MAAA, ACAS, CERA Vice President, Casualty Practice Council All Rights Reserved. 1 About the

NCOIL Summer Meeting Flood Insurance: What s Holding Back the Private Market? July 11, 2014 Michael Angelina, MAAA, ACAS, CERA Vice President, Casualty Practice Council All Rights Reserved. 1 About the

A Perfect Storm for P&C Analytics

A Perfect Storm for P&C Analytics Karthik Balakrishnan, Ph.D. ISO Innovative Analytics CAS Spring Meeting 24 May 2010 San Diego, CA THE PERFECT STORM Infrastructure Data Algorithms & Tools I. Infrastructure

A Perfect Storm for P&C Analytics Karthik Balakrishnan, Ph.D. ISO Innovative Analytics CAS Spring Meeting 24 May 2010 San Diego, CA THE PERFECT STORM Infrastructure Data Algorithms & Tools I. Infrastructure

IVANS 2008 XCHANGE CONFERENCE Key Communications Issues Facing the Property/Casualty Insurance Industry in 2008

IVANS 2008 XCHANGE CONFERENCE Key Communications Issues Facing the Property/Casualty Insurance Industry in 2008 Tampa, Florida February 7, 2008 Jeanne. M. Salvatore Senior Vice President, Public Affairs

IVANS 2008 XCHANGE CONFERENCE Key Communications Issues Facing the Property/Casualty Insurance Industry in 2008 Tampa, Florida February 7, 2008 Jeanne. M. Salvatore Senior Vice President, Public Affairs

Village of Blue Mounds Annex

Village of Blue Mounds Annex Community Profile The Village of Blue Mounds is located in the southwest quadrant of the County, north of the town of Perry, west of the town of Springdale, and south of the

Village of Blue Mounds Annex Community Profile The Village of Blue Mounds is located in the southwest quadrant of the County, north of the town of Perry, west of the town of Springdale, and south of the

Pioneer ILS Interval Fund

Pioneer ILS Interval Fund COMMENTARY Performance Analysis & Commentary March 2016 Fund Ticker Symbol: XILSX us.pioneerinvestments.com First Quarter Review The Fund returned 1.35%, net of fees, in the first

Pioneer ILS Interval Fund COMMENTARY Performance Analysis & Commentary March 2016 Fund Ticker Symbol: XILSX us.pioneerinvestments.com First Quarter Review The Fund returned 1.35%, net of fees, in the first

The Hanover Insurance Group, Inc.

The Hanover Insurance Group, Inc. Third Quarter 2017 Results November 2, 2017 To be read in conjunction with the press release dated November 1, 2017 and conference call scheduled for November 2, 2017

The Hanover Insurance Group, Inc. Third Quarter 2017 Results November 2, 2017 To be read in conjunction with the press release dated November 1, 2017 and conference call scheduled for November 2, 2017