2015 AEG Professional Landslide Forum February 26-28, 2015

|

|

|

- Sharon Mathews

- 5 years ago

- Views:

Transcription

1 2015 AEG Professional Landslide Forum February 26-28, 2015 Keynote 3: Lessons from the National Earthquake Hazards Reduction Program Can be Applied to the National Landslide Hazards Program: A Rational Approach. Richard J. Roth, Jr, Consulting Insurance Actuary, Huntington Beach, CA rjrothjr@verizon.net Jeffrey R. Keaton, Amec Foster Wheeler, Los Angeles, CA, jeff.keaton@amecfw.com 1

2 Who are we? We are an actuary and a geotechnologist seeking to bridge two very different disciplines to achieve a result of significant benefit to property owners. I am the kind of actuary who specializes in all forms of insurance other than life and health. This includes fire, automobile, workers compensation, liability, earthquake, windstorms and so on. I was the Chief Property/Casualty Actuary for the California Insurance Department (CID) for 20 years. During that time, I took a special interest in the problems of how to provide insurance for natural disasters. 2

3 The Business of Insurance Insurance is a special kind of business, in which the costs of the product are not known until AFTER the product is sold. (When Ford sells a car, Ford knows exactly the costs of making that car.) In addition, the insurance company holds your money and promises to pay if you have a covered claim. A fiduciary responsibility. An insurance company issues far more policies than it has assets, because only a few policies will have claims each year. A leveraged business. 3

4 What Do Actuaries Do? Actuaries are experts in all aspects of forming and running an insurance company, a very complicated business. They determine what rate (dollar premium) to charge for each type and location of house or automobile to be insured. They estimate the probability of catastrophic event, such as hurricanes, earthquakes, large brush fires, hail storms, and so on. Insurance claims often involve lawsuits, which are not settled for many years. Fire and earthquake claims are usually not settled for many years. An Actuary must estimate the reserves for these claims. 4

5 What Do Actuaries Need to Know? When State Farm sells homeowners insurance in California, it must know: What rate to charge for each type and location of a house. The rate is based on the past history claims from policyholders. The past history must be adjusted for building cost inflation and changes in building codes. When AAA Auto Club sells automobile insurance in California, it must know: What rate to charge for each type of car, by location, by owner s driving record. This results in a very large matrix of combinations to fit the population, all based on history. 5

6 Problems in Insuring Natural Disasters Historical claims data from past natural disasters can t be used for determining the rates for the insurance. Once an earthquake has occurred, the stress has been removed. Yet, insurance is now available for earthquakes, hurricanes, hail, and floods. Generally, there is no insurance available for landslides or subsidence (sinkholes). Earthquakes, landslides and sinkholes are part of the exclusion for earth movement in homeowners policies. Earthquake insurance must be purchased separately. The demand by property owners for this insurance is low, mainly because the public s perception of risk from most natural hazards is low and that government programs will cover their losses. 6

7 Hurricanes and Hail What do Hurricanes and Hail have in common? Answer: World War II. In 1940, there were 377 qualified weather forecasters in the US. Far fewer were professional meteorologists. During one year, 1942, the army increased that number by 2,590 through special training programs at MIT, Cal Tech, and NYU. After the war, the meteorological profession grew and the public interest in predicting the weather grew. 7

8 Weather Modeling after WW II After the war, some of the trained weather forecasters continued their interest in meteorology and took jobs in the field. One group moved to Hartford and joined the Travelers Insurance Company to develop a windstorm and hurricane model. Travelers insured hurricanes along the East Coast. Another weather forecaster, my father, moved to Chicago and founded a bureau, funded by the insurance industry, to model hail patterns for rating hail insurance. Hail only occurs in certain places and under certain conditions. This experience led him to become an actuary like myself. 8

9 The growth of natural hazard modeling Hurricane modeling is now a big business, not only along the East Coast, but around the world, for rating and catastrophe prediction. Hail insurance, which protects mainly corn and tobacco, continues to be modeled for rating purposes. Flood insurance is a federal government program, which relies mainly on special flood maps of designated hazard areas. Earthquake modeling did not develop until the 1980s, with the development of the modern PC computer. The first model was developed by Karl Steinbrugge, a professor at the University of California, Berkeley. 9

10 The Beginning of EQ Modeling I had the good fortune to work with Karl in the 1980s. After he retired, he was under contract with the California Insurance Department to work with me. He developed a Questionnaire which every insurance company in California had to submit each year. The insurers supplied the number, type and location of the homes and commercial buildings that they insured for earthquake damage. The Questionnaire contained an algorithm to estimate the Probable Maximum Loss (PML) for each EQ zone. 10

11 California was divided into EQ zones 11

12 How was this Questionnaire used? Each year, the data from the Questionnaire were compiled and summarized into a published report. From this report the CDI could determine the PML for each insurers by location. The commercial EQ exposure was greater than the residential exposure, although the residential received the most political attention. The CDI could see if an insurer had too much PML (gambling?). The Questionnaire did not set rates for EQ insurance. 12

13 After an Earthquake When an EQ occurred, the Questionnaire was especially useful for identifying insurers that would have the most claims. This happened after the 1989 Loma Prieta and the 1994 Northridge EQs. Several insurers were especially hard hit by these events. This Questionnaire was useful when insurers submitted an application to start insuring for EQ damage how much capital would be needed? After both these events, the California Legislature considered numerous legislation dealing with EQ insurance. 13

14 Growth of EQ Modeling With the introduction of the PC computer, two firms were formed to provide EQ modeling in California RMS and EQE. Staffed with seismologists and structural engineers, they could use detailed fault maps from the State Geologist and the USGS, along with ground attenuation knowledge, to estimate the PMLs. These models were much more detailed and used much more geological information than the CDI s Questionnaire. These models are particularly useful to insurers of commercial buildings and reinsurers. 14

15 The need for EQ modeling It is very difficult to get a mortgage on a large commercial building without an assessment of the earthquake exposure and PML exposure. If the exposure is high enough, earthquake insurance would be required. The same type of evaluation of the landslide exposure could be required. The commercial exposure includes damage to the building, damage to contents and business interruption (loss of sales and disruption of suppliers). 15

16 What do the EQ models need to know? The inputs to the EQ models are: The known fault zones The estimated probabilities of events by magnitude and recurrence interval. The regional soil characteristics The expected attenuation, including liquefaction potential The expected damage to building, by type of construction and inventory, called the vulnerability. The secondary damage potential, including business interruption The results are highly dependent on the assumptions in the inputs. 16

17 The federal program - NEHRP The federal National Earthquake Hazards Reduction Program (NEHRP) can be credited with funding the geological, seismological and structural engineering research necessary to the development of the earthquake computer models. NEHRP started in 1977 to promote the study of earthquakes, with a view toward promoting mitigation, sound building practices, life safety, and economic recovery. NEHRP is the work of four primary agencies: FEMA, NIST, NSF and USGS. 17

18 Can Models be Developed for Landslides? A landslide model would be more complicated than an EQ model Landslides require a trigger to cause the earth to slide, such as rainfall or an EQ. All of the geophysical and engineering knowledge is available. The software would be similar to the EQ modeling software. What is lacking is the interest from insurers. Hardly any insurers offer landslide insurance, because of the unknown risk. However, a credible model would help change this. 18

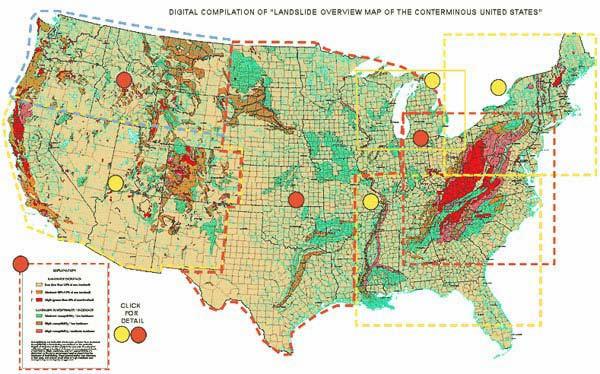

19 Landslides 101 According to the USGS National Landslide Information Center, landslides are a serious geologic hazard common to almost every State in the United States. It is estimated that in the United States, they cause in excess of $1 billion in damages and from about 25 to 50 deaths each year. Globally, landslides cause billions of dollars in damages and thousands of deaths and injuries each year, particularly in underdeveloped countries. Source: USGS website, Landslides

20 The Focus of USGS on Landslides Advancing public safety Investigating past landslides Monitoring current sites Undertaking research to make accurate landslide hazard maps, and Making forecasts of landslide occurrences. 20

21 USGS Landslide Hazards Research Program The results of this research will be particularly useful to insurance companies. This research seeks to answer the major questions: 1. When and where will landslides occur? 2. How big will they be? 3. How fast and how far will they move? 4. What areas will the landslides affect or damage? 5. How frequently do landslides occur in a given locality? 21

22 22

23 Current Landslide Modeling Efforts USGS also has a well-established program focusing on landslides, with a section on landslides on its website: landslides.usgs.gov. This is the USGS Landslide Hazards Program. USGS is developing software for landslide assessments and modeling, with names like Seismic LAndslide Movement Modeled using Earthquake Records - SLAMMMER, and TRIGRS which is a program relating slope stability to rainfall infiltration. 23

24 Homeowners Insurance The common Homeowners insurance policy excludes damage due to earth movement. The primary coverages in an Homeowners policy are fire, burglary and personal liability, all of which can be priced and happen infrequently at any particular home, but often enough that the aggregate future losses can be predicted by actuaries based on past loss statistics. With landslide coverage included, the Homeowners policy would be almost a true all-risk policy. To have complete insurance coverage for earth movement, the policy would have to include earthquake liquefaction and sinkholes as well. 24

25 Public Awareness In California, when a house is sold, the buyer must be informed if the house is near a known active fault zone. With improved landslide hazard maps, the same requirement could be made for designated landslide zones. Landslide loss models would also be of great benefit to regional and local governments, for emergency response planning, for land use planning and for maintenance programs responsible for utility water leaks that could contribute to triggering landslide movements. 25

Earthquakes Continuing Education Course No /264109

Earthquakes Continuing Education Course No. 264108/264109 No. 244778), is a Professor in the Civil Engineering Department at UCLA, a California licensed engineer, and also certified with the California

Earthquakes Continuing Education Course No. 264108/264109 No. 244778), is a Professor in the Civil Engineering Department at UCLA, a California licensed engineer, and also certified with the California

Catastrophes and the Advent of the Use of Cat Models in Ratemaking

Catastrophes and the Advent of the Use of Cat Models in Ratemaking Christopher S. Carlson, FCAS, MAAA Pinnacle Actuarial Resources, Inc. Casualty Actuarial Society Catastrophes and the Advent of the Use

Catastrophes and the Advent of the Use of Cat Models in Ratemaking Christopher S. Carlson, FCAS, MAAA Pinnacle Actuarial Resources, Inc. Casualty Actuarial Society Catastrophes and the Advent of the Use

RISK MODELING AND CALIFORNIA RESIDENTIAL EARTHQUAKE INSURANCE

RISK MODELING AND CALIFORNIA RESIDENTIAL EARTHQUAKE INSURANCE Robert Muir-Wood Chief Research Officer July 9 th 2015 1 $M CALIFORNIA EARTHQUAKE INSURANCE 1968-1993: A THRIVING AND STABLE MARKET 600 Loma

RISK MODELING AND CALIFORNIA RESIDENTIAL EARTHQUAKE INSURANCE Robert Muir-Wood Chief Research Officer July 9 th 2015 1 $M CALIFORNIA EARTHQUAKE INSURANCE 1968-1993: A THRIVING AND STABLE MARKET 600 Loma

Garfield County NHMP:

Garfield County NHMP: Introduction and Summary Hazard Identification and Risk Assessment DRAFT AUG2010 Risk assessments provide information about the geographic areas where the hazards may occur, the value

Garfield County NHMP: Introduction and Summary Hazard Identification and Risk Assessment DRAFT AUG2010 Risk assessments provide information about the geographic areas where the hazards may occur, the value

Mark Brannon, FCAS, MAAA, CPCU Sue Buehler, FCAS, MAAA

P&C Catastrophe Issues Mark Brannon, FCAS, MAAA, CPCU Sue Buehler, FCAS, MAAA Association of Insurance Compliance Professionals Gulf States Chapter Education Day July 30, 2010 Atlanta, Georgia Agenda What

P&C Catastrophe Issues Mark Brannon, FCAS, MAAA, CPCU Sue Buehler, FCAS, MAAA Association of Insurance Compliance Professionals Gulf States Chapter Education Day July 30, 2010 Atlanta, Georgia Agenda What

An Introduction to Natural Catastrophe Modelling at Twelve Capital. Dr. Jan Kleinn Head of ILS Analytics

An Introduction to Natural Catastrophe Modelling at Twelve Capital Dr. Jan Kleinn Head of ILS Analytics For professional/qualified investors use only, Q2 2015 Basic Concept Hazard Stochastic modelling

An Introduction to Natural Catastrophe Modelling at Twelve Capital Dr. Jan Kleinn Head of ILS Analytics For professional/qualified investors use only, Q2 2015 Basic Concept Hazard Stochastic modelling

Natural Hazards Risks in Kentucky. KAMM Regional Training

Natural Hazards Risks in Kentucky KAMM Regional Training Floodplain 101 Kentucky has approximately 92,000 linear miles of streams and rivers Approximately 31,000 linear miles have mapped flood hazards

Natural Hazards Risks in Kentucky KAMM Regional Training Floodplain 101 Kentucky has approximately 92,000 linear miles of streams and rivers Approximately 31,000 linear miles have mapped flood hazards

INTRODUCTION TO NATURAL HAZARD ANALYSIS

INTRODUCTION TO NATURAL HAZARD ANALYSIS November 19, 2013 Thomas A. Delorie, Jr. CSP Managing Director Natural Hazards Are Global and Include: Earthquake Flood Hurricane / Tropical Cyclone / Typhoon Landslides

INTRODUCTION TO NATURAL HAZARD ANALYSIS November 19, 2013 Thomas A. Delorie, Jr. CSP Managing Director Natural Hazards Are Global and Include: Earthquake Flood Hurricane / Tropical Cyclone / Typhoon Landslides

Q1 Do you...(check all that apply).

.") Q1 Do you...(check all that apply). Live in the City of... Work in the City of... Visit the City of Hesperia... Live in the City of Hesperia Work in the City of Hesperia Visit the City of Hesperia but

Q1 Do you...(check all that apply). Live in the City of... Work in the City of... Visit the City of Hesperia... Live in the City of Hesperia Work in the City of Hesperia Visit the City of Hesperia but

Reactions to Catastrophic Events: A Look at Insurers, Consumers, and Regulators. Patricia Born, PhD

Reactions to Catastrophic Events: A Look at Insurers, Consumers, and Regulators Patricia Born, PhD Agenda Introduction Insurer Responses over 30 Years Consumer Responses Regulatory Considerations Introduction

Reactions to Catastrophic Events: A Look at Insurers, Consumers, and Regulators Patricia Born, PhD Agenda Introduction Insurer Responses over 30 Years Consumer Responses Regulatory Considerations Introduction

Pennsylvania. Senate Banking & Insurance and Senate Environmental Resources & Energy Committees. Joint Public Hearing on Flood Insurance

Pennsylvania Senate Banking & Insurance and Senate Environmental Resources & Energy Committees Joint Public Hearing on Flood Insurance January 28, 2014 Respectfully submitted by: Donald L. Griffin, CPCU,

Pennsylvania Senate Banking & Insurance and Senate Environmental Resources & Energy Committees Joint Public Hearing on Flood Insurance January 28, 2014 Respectfully submitted by: Donald L. Griffin, CPCU,

France s Funds and Insurance Schemes for Natural Disasters. Update

France s Funds and Insurance Schemes for Natural Disasters Update 1 Mandatory cover of losses arising from Natural Catastrophes in: all Physical Damage (a.k.a. Fire ) insurance policies covering risks

France s Funds and Insurance Schemes for Natural Disasters Update 1 Mandatory cover of losses arising from Natural Catastrophes in: all Physical Damage (a.k.a. Fire ) insurance policies covering risks

Getting ahead of the next Big One The future of disaster insurance in New Zealand

+ Getting ahead of the next Big One The future of disaster insurance in New Zealand Janet Lockett : Clinton Freeman : Richard Beauchamp New Zealand Society of Actuaries Conference, 21 November 2012 + Why

+ Getting ahead of the next Big One The future of disaster insurance in New Zealand Janet Lockett : Clinton Freeman : Richard Beauchamp New Zealand Society of Actuaries Conference, 21 November 2012 + Why

PREDICTING EARTHQUAKE PREPARATION: SMALL BUSINESS RESPONSES TO NISQUALLY

13 th World Conference on Earthquake Engineering Vancouver, B.C., Canada August 1-6, 2004 Paper No.0571 PREDICTING EARTHQUAKE PREPARATION: SMALL BUSINESS RESPONSES TO NISQUALLY Jacqueline Meszaros 1 and

13 th World Conference on Earthquake Engineering Vancouver, B.C., Canada August 1-6, 2004 Paper No.0571 PREDICTING EARTHQUAKE PREPARATION: SMALL BUSINESS RESPONSES TO NISQUALLY Jacqueline Meszaros 1 and

Protecting U.S. Insurance Consumers and Taxpayers From the Financial Effects of Natural Disasters

Protecting U.S. Insurance Consumers and Taxpayers From the Financial Effects of Natural Disasters 12/8/00 The Public Policy Case for Policyholder Disaster Protection Reserves (AAA Hill Staff Briefing)

Protecting U.S. Insurance Consumers and Taxpayers From the Financial Effects of Natural Disasters 12/8/00 The Public Policy Case for Policyholder Disaster Protection Reserves (AAA Hill Staff Briefing)

EExtreme weather events are becoming more frequent and more costly.

FEATURE RESPONDING TO CATASTROPHIC WEATHER, CAPTIVES ANSWER THE CALL EExtreme weather events are becoming more frequent and more costly. According to Munich Re, in 2017 insured catastrophic losses were

FEATURE RESPONDING TO CATASTROPHIC WEATHER, CAPTIVES ANSWER THE CALL EExtreme weather events are becoming more frequent and more costly. According to Munich Re, in 2017 insured catastrophic losses were

CALIFORNIA EARTHQUAKE RISK ASSESSMENT

CALIFORNIA EARTHQUAKE RISK ASSESSMENT June 14 th, 2018 1 Notice The information provided in this Presentation was developed by the Workers Compensation Insurance Rating Bureau of California (WCIRB) and

CALIFORNIA EARTHQUAKE RISK ASSESSMENT June 14 th, 2018 1 Notice The information provided in this Presentation was developed by the Workers Compensation Insurance Rating Bureau of California (WCIRB) and

Topics. Why earthquake insurance? Earthquake insurance nuts and bolts Recent challenges and Insurance Department response Where do we go from here?

Topics Why earthquake insurance? Earthquake insurance nuts and bolts Recent challenges and Insurance Department response Where do we go from here? Why Earthquake Insurance? Earthquake damage is typically

Topics Why earthquake insurance? Earthquake insurance nuts and bolts Recent challenges and Insurance Department response Where do we go from here? Why Earthquake Insurance? Earthquake damage is typically

A Multihazard Approach to Building Safety: Using FEMA Publication 452 as a Mitigation Tool

Mila Kennett Architect/Manager Risk Management Series Risk Reduction Branch FEMA/Department of Homeland Security MCEER Conference, September 18, 2007, New York City A Multihazard Approach to Building Safety:

Mila Kennett Architect/Manager Risk Management Series Risk Reduction Branch FEMA/Department of Homeland Security MCEER Conference, September 18, 2007, New York City A Multihazard Approach to Building Safety:

Catastrophe Exposures & Insurance Industry Catastrophe Management Practices. American Academy of Actuaries Catastrophe Management Work Group

Catastrophe Exposures & Insurance Industry Catastrophe Management Practices American Academy of Actuaries Catastrophe Management Work Group Overview Introduction What is a Catastrophe? Insurer Capital

Catastrophe Exposures & Insurance Industry Catastrophe Management Practices American Academy of Actuaries Catastrophe Management Work Group Overview Introduction What is a Catastrophe? Insurer Capital

A Firm Foundation The Insurance Industry & Its Contributions to Society

A Firm Foundation The Insurance Industry & Its Contributions to Society St. John s University School of Risk Management, Insurance & Actuarial Science New York, NY April 10, 2008 Robert P. Hartwig, Ph.D.,

A Firm Foundation The Insurance Industry & Its Contributions to Society St. John s University School of Risk Management, Insurance & Actuarial Science New York, NY April 10, 2008 Robert P. Hartwig, Ph.D.,

REDARS 2 Software and Methodology for Evaluating Risks from Earthquake DAmage to Roadway Systems

REDARS 2 Software and Methodology for Evaluating Risks from Earthquake DAmage to Roadway Systems by Stuart D. Werner for presentation at Eighth U.S. National Conference on Earthquake Engineering San Francisco

REDARS 2 Software and Methodology for Evaluating Risks from Earthquake DAmage to Roadway Systems by Stuart D. Werner for presentation at Eighth U.S. National Conference on Earthquake Engineering San Francisco

Disaster Recovery Planning: Preparation is Key to Survival

Adjusters International Disaster Recovery Consulting EDITOR S NOTE Making sure the right insurance program is in place to protect your organization after a disaster may not be enough to survive in today

Adjusters International Disaster Recovery Consulting EDITOR S NOTE Making sure the right insurance program is in place to protect your organization after a disaster may not be enough to survive in today

Chapter 1 NATURAL HAZARDS AND DISASTERS

Chapter 1 NATURAL HAZARDS AND DISASTERS MULTIPLE-CHOICE QUESTIONS 1. People live in dangerous areas for what reasons? a. for the views b. because of cheap land c. because the land is fertile d. for proximity

Chapter 1 NATURAL HAZARDS AND DISASTERS MULTIPLE-CHOICE QUESTIONS 1. People live in dangerous areas for what reasons? a. for the views b. because of cheap land c. because the land is fertile d. for proximity

REGIONAL CATASTROPHE RISK MODELLING, SOURCES OF COMMON UNCERTAINTIES

13 th World Conference on Earthquake Engineering Vancouver, B.C., Canada August 1-6, 2004 Paper No. 1326 REGIONAL CATASTROPHE RISK MODELLING, SOURCES OF COMMON UNCERTAINTIES Mohammad R ZOLFAGHARI 1 SUMMARY

13 th World Conference on Earthquake Engineering Vancouver, B.C., Canada August 1-6, 2004 Paper No. 1326 REGIONAL CATASTROPHE RISK MODELLING, SOURCES OF COMMON UNCERTAINTIES Mohammad R ZOLFAGHARI 1 SUMMARY

Local Government Incentives for Earthquake-Resilient New Buildings

2016 Local Government Incentives for Earthquake-Resilient New Buildings Keith Porter, PE PhD University of Colorado Boulder & SPA Risk LLC January 13, 2016 1. How will a code-compliant building stock perform

2016 Local Government Incentives for Earthquake-Resilient New Buildings Keith Porter, PE PhD University of Colorado Boulder & SPA Risk LLC January 13, 2016 1. How will a code-compliant building stock perform

VULNERABILITY ASSESSMENT

SOUTHSIDE HAMPTON ROADS HAZARD MITIGATION PLAN VULNERABILITY ASSESSMENT INTRODUCTION The Vulnerability Assessment section builds upon the information provided in the Hazard Identification and Analysis

SOUTHSIDE HAMPTON ROADS HAZARD MITIGATION PLAN VULNERABILITY ASSESSMENT INTRODUCTION The Vulnerability Assessment section builds upon the information provided in the Hazard Identification and Analysis

Future Pathways. Fresh perspectives from actuaries of the future. Auckland, 9 March 2012 Wellington, 12 March 2012

Future Pathways Fresh perspectives from actuaries of the future Auckland, 9 March 2012 Wellington, 12 March 2012 Future Pathways Fresh perspectives from actuaries of the future General Insurance Clinton

Future Pathways Fresh perspectives from actuaries of the future Auckland, 9 March 2012 Wellington, 12 March 2012 Future Pathways Fresh perspectives from actuaries of the future General Insurance Clinton

Modeling Extreme Event Risk

Modeling Extreme Event Risk Both natural catastrophes earthquakes, hurricanes, tornadoes, and floods and man-made disasters, including terrorism and extreme casualty events, can jeopardize the financial

Modeling Extreme Event Risk Both natural catastrophes earthquakes, hurricanes, tornadoes, and floods and man-made disasters, including terrorism and extreme casualty events, can jeopardize the financial

According to the U.S. Geological

Estimating economic losses in the Bay Area from a magnitude-6.9 earthquake Data from the BLS Quarterly Census of Employment and Wages are used to analyze potential business and economic losses resulting

Estimating economic losses in the Bay Area from a magnitude-6.9 earthquake Data from the BLS Quarterly Census of Employment and Wages are used to analyze potential business and economic losses resulting

CATASTROPHE RISK MODELLING AND INSURANCE PENETRATION IN DEVELOPING COUNTRIES

CATASTROPHE RISK MODELLING AND INSURANCE PENETRATION IN DEVELOPING COUNTRIES M.R. Zolfaghari 1 1 Assistant Professor, Civil Engineering Department, KNT University, Tehran, Iran mzolfaghari@kntu.ac.ir ABSTRACT:

CATASTROPHE RISK MODELLING AND INSURANCE PENETRATION IN DEVELOPING COUNTRIES M.R. Zolfaghari 1 1 Assistant Professor, Civil Engineering Department, KNT University, Tehran, Iran mzolfaghari@kntu.ac.ir ABSTRACT:

Changes Coming to the National Flood Insurance Program What to Expect. Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act

Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act Flood Risk Flood risks and the costs of flooding Weather

Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act Flood Risk Flood risks and the costs of flooding Weather

Canadian Institute of Actuaries Conference CATASTROPHE MODELING 2012 AND BEYOND JUNE 21, Sherry Thomas Krista Lienau

Canadian Institute of Actuaries Conference CATASTROPHE MODELING 2012 AND BEYOND JUNE 21, 2012 Sherry Thomas Krista Lienau Catastrophe Modeling 2012 and Beyond Agenda Current landscape of Canadian catastrophe

Canadian Institute of Actuaries Conference CATASTROPHE MODELING 2012 AND BEYOND JUNE 21, 2012 Sherry Thomas Krista Lienau Catastrophe Modeling 2012 and Beyond Agenda Current landscape of Canadian catastrophe

Assessing and Managing Risk of Natural Disasters for a Workplace

Session No. 629 Assessing and Managing Risk of Natural Disasters for a Workplace William Piispanen, CIH, CSP, CEA, CMIOSH Senior Director Safety URS Corporation Boise, ID Susie Vader, STS Regulatory and

Session No. 629 Assessing and Managing Risk of Natural Disasters for a Workplace William Piispanen, CIH, CSP, CEA, CMIOSH Senior Director Safety URS Corporation Boise, ID Susie Vader, STS Regulatory and

Flood Insurance Coverage in Dare County: Before and After Hurricane Floyd

Flood Insurance Coverage in Dare County: Before and After Hurricane Floyd Craig E. Landry Department of Economics Center for Natural Hazards Research East Carolina University National Flood Insurance Program

Flood Insurance Coverage in Dare County: Before and After Hurricane Floyd Craig E. Landry Department of Economics Center for Natural Hazards Research East Carolina University National Flood Insurance Program

IVANS 2008 XCHANGE CONFERENCE Key Communications Issues Facing the Property/Casualty Insurance Industry in 2008

IVANS 2008 XCHANGE CONFERENCE Key Communications Issues Facing the Property/Casualty Insurance Industry in 2008 Tampa, Florida February 7, 2008 Jeanne. M. Salvatore Senior Vice President, Public Affairs

IVANS 2008 XCHANGE CONFERENCE Key Communications Issues Facing the Property/Casualty Insurance Industry in 2008 Tampa, Florida February 7, 2008 Jeanne. M. Salvatore Senior Vice President, Public Affairs

Guide To Homeowner s Insurance Exam Study Guide

Guide To Homeowner s Insurance Exam Study Guide This document contains all the questions that will included in the final exam, in the order that they will be asked. When you have studied the course materials,

Guide To Homeowner s Insurance Exam Study Guide This document contains all the questions that will included in the final exam, in the order that they will be asked. When you have studied the course materials,

California s Earthquake Legislation

California s Earthquake Legislation California s Earthquake Legislation Generally follows every earthquake Attempts to alleviate problem observed Legislation, Paso Robles Earthquake Associated with M6

California s Earthquake Legislation California s Earthquake Legislation Generally follows every earthquake Attempts to alleviate problem observed Legislation, Paso Robles Earthquake Associated with M6

PREPARING FOR THE NEXT BIG EARTHQUAKE

PREPARING FOR THE NEXT BIG EARTHQUAKE Rotary Club of Los Gatos Chris Nance Chief Communications Officer November 7, 2017 TOP FIVE THINGS TO KNOW about the value of earthquake insurance RISK The risk is

PREPARING FOR THE NEXT BIG EARTHQUAKE Rotary Club of Los Gatos Chris Nance Chief Communications Officer November 7, 2017 TOP FIVE THINGS TO KNOW about the value of earthquake insurance RISK The risk is

A Framework for Risk Assessment of Infrastructure in a Multi-Hazard Environment. Stephanie King, PhD, PE

A Framework for Risk Assessment of Infrastructure in a Multi-Hazard Environment Stephanie King, PhD, PE Weidlinger Associates, Inc. AEI-MCEER Symposium New York, NY September 18, 2007 www.wai.com New York

A Framework for Risk Assessment of Infrastructure in a Multi-Hazard Environment Stephanie King, PhD, PE Weidlinger Associates, Inc. AEI-MCEER Symposium New York, NY September 18, 2007 www.wai.com New York

Pricing Climate Risk: An Insurance Perspective

Pricing Climate Risk: An Insurance Perspective Howard Kunreuther kunreuther@wharton.upenn.edu Wharton School University of Pennsylvania Pricing Climate Risk: Refocusing the Climate Policy Debate Tempe,

Pricing Climate Risk: An Insurance Perspective Howard Kunreuther kunreuther@wharton.upenn.edu Wharton School University of Pennsylvania Pricing Climate Risk: Refocusing the Climate Policy Debate Tempe,

Risk-based Land-use Guide: Safe use of land based on hazard risk management

Risk-based Land-use Guide: Safe use of land based on hazard risk management Bert Struik, Laurie Pearce Calgary, September 29, 2015 Messages A city-focused land-use guide is available to help reduce risk

Risk-based Land-use Guide: Safe use of land based on hazard risk management Bert Struik, Laurie Pearce Calgary, September 29, 2015 Messages A city-focused land-use guide is available to help reduce risk

Your Guide to CEA Earthquake Insurance for Homeowners

California Earthquake Authority 801 K Street, Suite 1000 Sacramento, California 95814 TOLL FREE (877) 797-4300 www.earthquakeauthority.com Your Guide to CEA Earthquake Insurance for Homeowners For more

California Earthquake Authority 801 K Street, Suite 1000 Sacramento, California 95814 TOLL FREE (877) 797-4300 www.earthquakeauthority.com Your Guide to CEA Earthquake Insurance for Homeowners For more

Executive Summary. Introduction and Purpose. Scope

Executive Summary Introduction and Purpose This is the first edition of the Los Angeles Unified School District All-Hazard Mitigation Plan, and through completion of this plan the District continues many

Executive Summary Introduction and Purpose This is the first edition of the Los Angeles Unified School District All-Hazard Mitigation Plan, and through completion of this plan the District continues many

Casualty Actuaries of the Northwest: Strategies for Homeowners Profitability and Growth

Casualty Actuaries of the Northwest: Strategies for Homeowners Profitability and Growth Nancy Watkins, FCAS, MAAA Principal and Consulting Actuary Milliman, Inc. September 25, 2015 Why is Homeowners so

Casualty Actuaries of the Northwest: Strategies for Homeowners Profitability and Growth Nancy Watkins, FCAS, MAAA Principal and Consulting Actuary Milliman, Inc. September 25, 2015 Why is Homeowners so

SOUTH CENTRAL REGION MULTI-JURISDICTION HAZARD MITIGATION PLAN. Advisory Committee Meeting September 12, 2012

SOUTH CENTRAL REGION MULTI-JURISDICTION HAZARD MITIGATION PLAN Advisory Committee Meeting September 12, 2012 AGENDA FOR TODAY Purpose of Meeting Engage All Advisory Committee Members Distribute Project

SOUTH CENTRAL REGION MULTI-JURISDICTION HAZARD MITIGATION PLAN Advisory Committee Meeting September 12, 2012 AGENDA FOR TODAY Purpose of Meeting Engage All Advisory Committee Members Distribute Project

NATURAL DISASTER RESPONSE

NATURAL DISASTER RESPONSE TRENDS IN NATURAL DISASTERS 2017 RECORD RAINFALL ON TEXAS PUERTO RICO HURRICANES & LEFT WITHOUT POWER WILDFIRES IN CALIFORNIA $306 BILLION IN DAMAGE 2018 AS OF JULY 9, THERE WERE

NATURAL DISASTER RESPONSE TRENDS IN NATURAL DISASTERS 2017 RECORD RAINFALL ON TEXAS PUERTO RICO HURRICANES & LEFT WITHOUT POWER WILDFIRES IN CALIFORNIA $306 BILLION IN DAMAGE 2018 AS OF JULY 9, THERE WERE

FUTURE FLOODS: An exploration of a cross-disciplinary approach to flood risk forecasting. Brad Weir: Catastrophe Models

FUTURE FLOODS: An exploration of a cross-disciplinary approach to flood risk forecasting Brad Weir: Catastrophe Models Agenda Reinsurance & Catastrophes Catastrophe Modelling Models in Asia Limitations

FUTURE FLOODS: An exploration of a cross-disciplinary approach to flood risk forecasting Brad Weir: Catastrophe Models Agenda Reinsurance & Catastrophes Catastrophe Modelling Models in Asia Limitations

Terms of Reference (ToR) Earthquake Hazard Assessment and Mapping Specialist

Earthquake Hazard Assessment and Mapping Specialist") Terms of Reference (ToR) Earthquake Hazard Assessment and Mapping Specialist I. Introduction With the support of UNDP, the Single Project Implementation Unit (SPIU) of the Ministry of Disaster Management

Terms of Reference (ToR) Earthquake Hazard Assessment and Mapping Specialist I. Introduction With the support of UNDP, the Single Project Implementation Unit (SPIU) of the Ministry of Disaster Management

California Wildfires: The Role of Disaster Insurance

Order Code RS22747 October 25, 2007 Summary California Wildfires: The Role of Disaster Insurance Rawle O. King Analyst in Financial Economics and Risk Assessment Government and Finance Division The tragic

Order Code RS22747 October 25, 2007 Summary California Wildfires: The Role of Disaster Insurance Rawle O. King Analyst in Financial Economics and Risk Assessment Government and Finance Division The tragic

Catastrophe Risk Engineering Solutions

Catastrophe Risk Engineering Solutions Catastrophes, whether natural or man-made, can damage structures, disrupt process flows and supply chains, devastate a workforce, and financially cripple a company

Catastrophe Risk Engineering Solutions Catastrophes, whether natural or man-made, can damage structures, disrupt process flows and supply chains, devastate a workforce, and financially cripple a company

Insuring Your Quiznos Franchise

Insuring Your Quiznos Franchise Table of Contents Quiznos Franchisee...1 The Importance of Insurance...2 Quiznos Insurance Requirements...2 Marsh-Administered Quiznos Insurance Program...4 3 Steps to Obtaining

Insuring Your Quiznos Franchise Table of Contents Quiznos Franchisee...1 The Importance of Insurance...2 Quiznos Insurance Requirements...2 Marsh-Administered Quiznos Insurance Program...4 3 Steps to Obtaining

Principle-Based Reforms for Florida s Property Insurance Market

Principle-Based Reforms for Florida s Property Insurance Market Senate Banking and Insurance Committee January 16, 2013 Kevin M. McCarty, Insurance Commissioner 1 Committee Guidance* Return to a free market

Principle-Based Reforms for Florida s Property Insurance Market Senate Banking and Insurance Committee January 16, 2013 Kevin M. McCarty, Insurance Commissioner 1 Committee Guidance* Return to a free market

COMMUNITY SUMMARY LINN COUNTY MULTI-JURISDICTIONAL HAZARD MITIGATION PLAN CITY OF LISBON

COMMUNITY SUMMARY LINN COUNTY MULTI-JURISDICTIONAL HAZARD MITIGATION PLAN CITY OF LISBON This document provides a summary of the hazard mitigation planning information for the City of Lisbon that will

COMMUNITY SUMMARY LINN COUNTY MULTI-JURISDICTIONAL HAZARD MITIGATION PLAN CITY OF LISBON This document provides a summary of the hazard mitigation planning information for the City of Lisbon that will

RESOLUTION NO. WHEREAS, the Signal Hill Safety Element was last updated in 1986; and

RESOLUTION NO. A RESOLUTION OF THE PLANNING COMMISSION OF THE CITY OF SIGNAL HILL, CALIFORNIA, RECOMMENDING CITY COUNCIL APPROVAL OF GENERAL PLAN AMENDMENT 16-02 ADOPTING THE 2016 SAFETY ELEMENT UPDATE

RESOLUTION NO. A RESOLUTION OF THE PLANNING COMMISSION OF THE CITY OF SIGNAL HILL, CALIFORNIA, RECOMMENDING CITY COUNCIL APPROVAL OF GENERAL PLAN AMENDMENT 16-02 ADOPTING THE 2016 SAFETY ELEMENT UPDATE

Village of Blue Mounds Annex

Village of Blue Mounds Annex Community Profile The Village of Blue Mounds is located in the southwest quadrant of the County, north of the town of Perry, west of the town of Springdale, and south of the

Village of Blue Mounds Annex Community Profile The Village of Blue Mounds is located in the southwest quadrant of the County, north of the town of Perry, west of the town of Springdale, and south of the

Disaster Risk Reduction and Management in St. Lucia

Disaster Risk Reduction and Management in St. Lucia National Circumstances Saint Lucia is a Small Island Developing State (SIDS) located at latitude 13 o N, and 61 o S within the Lesser Antilles. The

Disaster Risk Reduction and Management in St. Lucia National Circumstances Saint Lucia is a Small Island Developing State (SIDS) located at latitude 13 o N, and 61 o S within the Lesser Antilles. The

2015 Mobile County, Alabama Multi-Hazard Mitigation Plan Appendices

2015 Mobile County, Alabama Multi-Hazard Mitigation Plan A - Federal Requirements for local Mitigation Plans B - Community Mitigation Capabilities C - 2009 Plan Implementation Status D - Hazard Ratings

2015 Mobile County, Alabama Multi-Hazard Mitigation Plan A - Federal Requirements for local Mitigation Plans B - Community Mitigation Capabilities C - 2009 Plan Implementation Status D - Hazard Ratings

THE NATIONAL FLOOD INSURANCE PROGRAM:

THE NATIONAL FLOOD INSURANCE PROGRAM: Directions for Reform As Congress considers legislative changes to the debt-ridden National Flood Insurance Program, Carolyn Kousky discusses four key issues for reform.

THE NATIONAL FLOOD INSURANCE PROGRAM: Directions for Reform As Congress considers legislative changes to the debt-ridden National Flood Insurance Program, Carolyn Kousky discusses four key issues for reform.

Not IF but WHEN? A Certified Financial Planner s Guide to Earthquake Insurance for California Homeowners & Risk Management Steps to Minimize Damage

Not IF but WHEN? A Certified Financial Planner s Guide to Earthquake Insurance for California Homeowners & Risk Management Steps to Minimize Damage By: David Shaffer, ARM, CPRIA David Shaffer Insurance

Not IF but WHEN? A Certified Financial Planner s Guide to Earthquake Insurance for California Homeowners & Risk Management Steps to Minimize Damage By: David Shaffer, ARM, CPRIA David Shaffer Insurance

Urban Risk Management for Natural Disasters. Bogazici University Istanbul, Turkey. October 25-26, 20001

A Framework for Evaluating the Cost-Effectiveness of Mitigation Measures Howard Kunreuther* Patricia Grossi** Nano Seeber*** Andrew Smyth**** Paper Presented at the Bogazici University /Columbia University

A Framework for Evaluating the Cost-Effectiveness of Mitigation Measures Howard Kunreuther* Patricia Grossi** Nano Seeber*** Andrew Smyth**** Paper Presented at the Bogazici University /Columbia University

June 24, Re: Solicitation for Comment on the Study and Report to Congress on Natural Catastrophes and Insurance. Dear Director McRaith:

June 24, 2013 The Honorable Michael McRaith Director, Federal Insurance Office United States Department of the Treasury 1500 Pennsylvania Avenue, N.W. Washington D.C. 20220 Re: Solicitation for Comment

June 24, 2013 The Honorable Michael McRaith Director, Federal Insurance Office United States Department of the Treasury 1500 Pennsylvania Avenue, N.W. Washington D.C. 20220 Re: Solicitation for Comment

Disaster resilient communities: Canada s insurers promote adaptation to the growing threat of high impact weather

Disaster resilient communities: Canada s insurers promote adaptation to the growing threat of high impact weather by Paul Kovacs Executive Director, Institute for Catastrophic Loss Reduction Adjunct Research

Disaster resilient communities: Canada s insurers promote adaptation to the growing threat of high impact weather by Paul Kovacs Executive Director, Institute for Catastrophic Loss Reduction Adjunct Research

California Insurance CE

California Insurance CE How to Earn Credit for This Course ONLINE with instant exam results: BookmarkEducation.com or Complete and return this answer sheet. MAIL: Bookmark Education, 6203 W. Howard Street,

California Insurance CE How to Earn Credit for This Course ONLINE with instant exam results: BookmarkEducation.com or Complete and return this answer sheet. MAIL: Bookmark Education, 6203 W. Howard Street,

Florida Hurricane Catastrophe Fund Financing Observations and Perspective Presented to Summer Insurance Symposium June 2, 2009 Destin, Florida

Florida Hurricane Catastrophe Fund Financing Observations and Perspective Presented to 2009 Summer Insurance Symposium June 2, 2009 Destin, Florida Introduction John Forney, CFA Managing Director, Public

Florida Hurricane Catastrophe Fund Financing Observations and Perspective Presented to 2009 Summer Insurance Symposium June 2, 2009 Destin, Florida Introduction John Forney, CFA Managing Director, Public

Prerequisites for EOP Creation: Hazard Identification and Assessment

Prerequisites for EOP Creation: Hazard Identification and Assessment Presentation to: Advanced Healthcare Emergency Management Course Objectives Upon lesson completion, you should be able to: Understand

Prerequisites for EOP Creation: Hazard Identification and Assessment Presentation to: Advanced Healthcare Emergency Management Course Objectives Upon lesson completion, you should be able to: Understand

Flood Insurance THE TOPIC OCTOBER 2012

Flood Insurance THE TOPIC OCTOBER 2012 Because of frequent flooding of the Mississippi River during the 1960s and the rising cost of taxpayer funded disaster relief for flood victims, in 1968 Congress

Flood Insurance THE TOPIC OCTOBER 2012 Because of frequent flooding of the Mississippi River during the 1960s and the rising cost of taxpayer funded disaster relief for flood victims, in 1968 Congress

Our Mission OVER $13 BILLION OF PROTECTION. FIVE THINGS TO KNOW ABOUT California Earthquake Authority CEA S COMMITMENT TO LOWER RATES

CALIFORNIA EARTHQUAKE AUTHORITY: One of the world s largest providers of residential earthquake insurance HOW CEA FINANCIAL CAPACITY WOULD RESPOND TO HISTORICAL CALIFORNIA EARTHQUAKES NEW IAL $128 M CEA

CALIFORNIA EARTHQUAKE AUTHORITY: One of the world s largest providers of residential earthquake insurance HOW CEA FINANCIAL CAPACITY WOULD RESPOND TO HISTORICAL CALIFORNIA EARTHQUAKES NEW IAL $128 M CEA

CRS-2 Wildfire Data Overview On October 24, 2007, President Bush issued a federal emergency disaster declaration in response to property damage from w

Order Code RS22747 Updated January 30, 2008 Summary California Wildfires: The Role of Disaster Insurance Rawle O. King Analyst in Financial Economics and Risk Assessment Government and Finance Division

Order Code RS22747 Updated January 30, 2008 Summary California Wildfires: The Role of Disaster Insurance Rawle O. King Analyst in Financial Economics and Risk Assessment Government and Finance Division

Name Category Web Site Address Description Army Corps of Engineers Federal

Version 4.0 Page 12-1 SECTION 12. ANNEX A: RESOURCES The following resources were used in the development and update of the Las Virgenes-Malibu Council of Governments. In addition to the resources listed,

Version 4.0 Page 12-1 SECTION 12. ANNEX A: RESOURCES The following resources were used in the development and update of the Las Virgenes-Malibu Council of Governments. In addition to the resources listed,

Why insurers fail. Natural disasters and catastrophes 2016 UPDATE. Grant Kelly

Property and Casualty Insurance Compensation Corporation Société d indemnisation en matière d assurances IARD 2016 UPDATE Why insurers fail Natural disasters and catastrophes Winter Storm Hurricane Tornado

Property and Casualty Insurance Compensation Corporation Société d indemnisation en matière d assurances IARD 2016 UPDATE Why insurers fail Natural disasters and catastrophes Winter Storm Hurricane Tornado

Northern Kentucky University 2018 Hazard Mitigation Plan. Public Kick-Off Meeting March 20, 2018

Northern Kentucky University 2018 Hazard Mitigation Plan Public Kick-Off Meeting March 20, 2018 Agenda Welcome Hazard Mitigation Planning 101 Hazard Identification Exercises Next Steps Jeff Baker, NKU

Northern Kentucky University 2018 Hazard Mitigation Plan Public Kick-Off Meeting March 20, 2018 Agenda Welcome Hazard Mitigation Planning 101 Hazard Identification Exercises Next Steps Jeff Baker, NKU

Fundamentals of Catastrophe Modeling. CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010

Fundamentals of Catastrophe Modeling CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010 1 ANTITRUST NOTICE The Casualty Actuarial Society is committed to adhering

Fundamentals of Catastrophe Modeling CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010 1 ANTITRUST NOTICE The Casualty Actuarial Society is committed to adhering

EDUCATIONAL NOTE EARTHQUAKE EXPOSURE COMMITTEE ON PROPERTY AND CASUALTY INSURANCE FINANCIAL REPORTING

EDUCATIONAL NOTE Educational notes do not constitute standards of practice. They are intended to assist actuaries in applying standards of practice in specific matters. Responsibility for the manner of

EDUCATIONAL NOTE Educational notes do not constitute standards of practice. They are intended to assist actuaries in applying standards of practice in specific matters. Responsibility for the manner of

EARTHQUAKE ARE YOU READY TO RUMBLE?

PROPERTY BULLETIN May 2015 www.willis.com EARTHQUAKE ARE YOU READY TO RUMBLE? If you have not been paying attention recently, you may have not noticed, but lately, California has been rumbling. Last year,

PROPERTY BULLETIN May 2015 www.willis.com EARTHQUAKE ARE YOU READY TO RUMBLE? If you have not been paying attention recently, you may have not noticed, but lately, California has been rumbling. Last year,

Seismic Benefit Cost Analysis

Seismic Benefit Cost Analysis Presented by: Paul Ransom Hazard Mitigation Branch Overview of BCA Generally required for all FEMA mitigation programs: HMGP (404) and PA (406) FMA PDM Overview for BCA The

Seismic Benefit Cost Analysis Presented by: Paul Ransom Hazard Mitigation Branch Overview of BCA Generally required for all FEMA mitigation programs: HMGP (404) and PA (406) FMA PDM Overview for BCA The

Launch a Vulnerability Assessment. Building Regional Disaster Resilience

Launch a Vulnerability Assessment Building Regional Disaster Resilience Overall Process Building Regional Disaster Resilience How is this process different? Goals and values-driven rather than checklist-driven

Launch a Vulnerability Assessment Building Regional Disaster Resilience Overall Process Building Regional Disaster Resilience How is this process different? Goals and values-driven rather than checklist-driven

Multi-Jurisdictional Hazard Mitigation Plan. Data Collection Questionnaire. For School Districts and Educational Institutions

Multi-Jurisdictional Hazard Mitigation Plan Data Collection Questionnaire For School Districts and Educational Institutions County: School District / Educational Institution Name: Return by: Please complete

Multi-Jurisdictional Hazard Mitigation Plan Data Collection Questionnaire For School Districts and Educational Institutions County: School District / Educational Institution Name: Return by: Please complete

Flood Insurance Reform Act of 2012

Flood Insurance Reform Act of 2012 Impact of changes to the NFIP Note: This Fact Sheet deals specifically with Sections 205 and 207 of the Act. In 2012, the U.S. Congress passed the Flood Insurance Reform

Flood Insurance Reform Act of 2012 Impact of changes to the NFIP Note: This Fact Sheet deals specifically with Sections 205 and 207 of the Act. In 2012, the U.S. Congress passed the Flood Insurance Reform

Mortgage Servicing: Flood Insurance Administration after Biggert-Waters

NAIC Examination Oversight (E) Task Force Climate Change and Global Warming (E) Working Group Testimony of J. Kevin A. McKechnie, Senior Vice President & Director ABA Office of Insurance Advocacy, to be

NAIC Examination Oversight (E) Task Force Climate Change and Global Warming (E) Working Group Testimony of J. Kevin A. McKechnie, Senior Vice President & Director ABA Office of Insurance Advocacy, to be

Pre-Earthquake, Emergency and Contingency Planning August 2015

RiskTopics Pre-Earthquake, Emergency and Contingency Planning August 2015 Regions that are regularly exposed to seismic events are well-known, e.g. Japan, New Zealand, Turkey, Western USA, Chile, etc.

RiskTopics Pre-Earthquake, Emergency and Contingency Planning August 2015 Regions that are regularly exposed to seismic events are well-known, e.g. Japan, New Zealand, Turkey, Western USA, Chile, etc.

The Florida Senate AVAILABILITY AND COST OF RESIDENTIAL HURRICANE COVERAGE. Revised Interim Project Summary September 1999 SUMMARY

Committee on Banking and Insurance The Florida Senate Revised Interim Project Summary 2000-03 September 1999 Senator James A. Scott, Chairman AVAILABILITY AND COST OF RESIDENTIAL HURRICANE COVERAGE SUMMARY

Committee on Banking and Insurance The Florida Senate Revised Interim Project Summary 2000-03 September 1999 Senator James A. Scott, Chairman AVAILABILITY AND COST OF RESIDENTIAL HURRICANE COVERAGE SUMMARY

PHASE 2 HAZARD IDENTIFICATION AND RISK ASSESSMENT

Prioritize Hazards PHASE 2 HAZARD IDENTIFICATION AND After you have developed a full list of potential hazards affecting your campus, prioritize them based on their likelihood of occurrence. This step

Prioritize Hazards PHASE 2 HAZARD IDENTIFICATION AND After you have developed a full list of potential hazards affecting your campus, prioritize them based on their likelihood of occurrence. This step

INSURANCE MARKET UPDATE

INSURANCE MARKET UPDATE NEW ZEALAND January 2010 CONTENTS Introduction 1 Summary of the 1 January 2010 Willis RE 1st View Global Insurance Market Report 1 The main loss events affecting the global property

INSURANCE MARKET UPDATE NEW ZEALAND January 2010 CONTENTS Introduction 1 Summary of the 1 January 2010 Willis RE 1st View Global Insurance Market Report 1 The main loss events affecting the global property

Multi-Jurisdictional Hazard Mitigation Plan. Data Collection Questionnaire. For Local Governments

Multi-Jurisdictional Hazard Mitigation Plan Data Collection Questionnaire County: For Local Governments Jurisdiction: Return to: Marcus Norden, Regional Planner BRP&EC Please complete this data collection

Multi-Jurisdictional Hazard Mitigation Plan Data Collection Questionnaire County: For Local Governments Jurisdiction: Return to: Marcus Norden, Regional Planner BRP&EC Please complete this data collection

Private property insurance data on losses

38 Universities Council on Water Resources Issue 138, Pages 38-44, April 2008 Assessment of Flood Losses in the United States Stanley A. Changnon University of Illinois: Chief Emeritus, Illinois State

38 Universities Council on Water Resources Issue 138, Pages 38-44, April 2008 Assessment of Flood Losses in the United States Stanley A. Changnon University of Illinois: Chief Emeritus, Illinois State

The AIR. Earthquake Model for Canada

The AIR Earthquake Model for Canada Magnitude 3.0 to 3.9 4.0 to 4.9 5.0 to 5.9 6.0 to 6.9 > 7.0 Vancouver Quebec City Ottawa 250 Historical earthquakes (Source: AIR Worldwide and Geological Survey of Canada)

The AIR Earthquake Model for Canada Magnitude 3.0 to 3.9 4.0 to 4.9 5.0 to 5.9 6.0 to 6.9 > 7.0 Vancouver Quebec City Ottawa 250 Historical earthquakes (Source: AIR Worldwide and Geological Survey of Canada)

Deciphering Flood: A Familiar and Misunderstood Risk

Special Report Deciphering Flood: A Familiar and Misunderstood Risk May 2017 Deciphering Flood: A Familiar and Misunderstood Risk Among natural disasters, floods are the most common, 1 but from an insurance

Special Report Deciphering Flood: A Familiar and Misunderstood Risk May 2017 Deciphering Flood: A Familiar and Misunderstood Risk Among natural disasters, floods are the most common, 1 but from an insurance

WORKING TOGETHER. An update from Quebec s home, car and business insurers

WORKING TOGETHER An update from Quebec s home, car and business insurers Canada s property and casualty (P&C) insurance industry helps people manage the everyday risks that come with owning a home, business

WORKING TOGETHER An update from Quebec s home, car and business insurers Canada s property and casualty (P&C) insurance industry helps people manage the everyday risks that come with owning a home, business

COMMUNITY SUMMARY LINN COUNTY MULTI-JURISDICTIONAL HAZARD MITIGATION PLAN CITY OF CENTRAL CITY

COMMUNITY SUMMARY LINN COUNTY MULTI-JURISDICTIONAL HAZARD MITIGATION PLAN CITY OF CENTRAL CITY This document provides a summary of the hazard mitigation planning information for the City of Central City

COMMUNITY SUMMARY LINN COUNTY MULTI-JURISDICTIONAL HAZARD MITIGATION PLAN CITY OF CENTRAL CITY This document provides a summary of the hazard mitigation planning information for the City of Central City

An Approach to Pricing Natural Perils

17th An Approach to Pricing Natural Perils Tim Andrews David McNab Ada Lui Finity Consulting Pty Ltd 2010 Why is everyone talking about the weather? The Melbourne and Perth storms were further evidence

17th An Approach to Pricing Natural Perils Tim Andrews David McNab Ada Lui Finity Consulting Pty Ltd 2010 Why is everyone talking about the weather? The Melbourne and Perth storms were further evidence

APPENDIX H TOWN OF FARMVILLE. Hazard Rankings. Status of Mitigation Actions. Building Permit Data. Future Land Use Map. Critical Facilities Map

APPENDIX H TOWN OF FARMVILLE Hazard Rankings Status of Mitigation Actions Building Permit Data Future Land Use Map Critical Facilities Map Zone Maps Hazard Rankings (From Qualitative Assessment and Local

APPENDIX H TOWN OF FARMVILLE Hazard Rankings Status of Mitigation Actions Building Permit Data Future Land Use Map Critical Facilities Map Zone Maps Hazard Rankings (From Qualitative Assessment and Local

Section 19: Basin-Wide Mitigation Action Plans

Section 19: Basin-Wide Mitigation Action Plans Contents Introduction...19-1 Texas Colorado River Floodplain Coalition Mitigation Actions...19-2 Mitigation Actions...19-9 Introduction This Mitigation Plan,

Section 19: Basin-Wide Mitigation Action Plans Contents Introduction...19-1 Texas Colorado River Floodplain Coalition Mitigation Actions...19-2 Mitigation Actions...19-9 Introduction This Mitigation Plan,

All-Hazards Homeowners Insurance: A Possibility for the United States?

All-Hazards Homeowners Insurance: A Possibility for the United States? Howard Kunreuther Key Points In the United States, standard homeowners insurance policies do not include coverage for earthquakes

All-Hazards Homeowners Insurance: A Possibility for the United States? Howard Kunreuther Key Points In the United States, standard homeowners insurance policies do not include coverage for earthquakes

Catastrophe Insurance System in France

The Geneva Papers on Risk and Insurance, 20 (No. 77 October 1995) 474-480 Catastrophe Insurance System in France by Serge Magnan * 1. Introduction Since the beginning of the fifties, French insurance companies

The Geneva Papers on Risk and Insurance, 20 (No. 77 October 1995) 474-480 Catastrophe Insurance System in France by Serge Magnan * 1. Introduction Since the beginning of the fifties, French insurance companies

Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality

Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality First Regional Europa Re Insurance Conference October 2011 Aleksandra Nakeva Ruzin, MPPM Executive Director

Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality First Regional Europa Re Insurance Conference October 2011 Aleksandra Nakeva Ruzin, MPPM Executive Director

Town of Montrose Annex

Town of Montrose Annex Community Profile The Town of Montrose is located in the Southwest quadrant of the County, east of the Town of Primrose, south of the Town of Verona, and west of the Town of Oregon.

Town of Montrose Annex Community Profile The Town of Montrose is located in the Southwest quadrant of the County, east of the Town of Primrose, south of the Town of Verona, and west of the Town of Oregon.

HAZUS -MH Risk Assessment and User Group Series HAZUS-MH and DMA Pilot Project Portland, Oregon. March 2004 FEMA FEMA 436

HAZUS -MH Risk Assessment and User Group Series HAZUS-MH and DMA 2000 Pilot Project Portland, Oregon March 2004 FEMA FEMA 436 Page intentionally left blank. Risk Assessment Pilot Project Results for DMA

HAZUS -MH Risk Assessment and User Group Series HAZUS-MH and DMA 2000 Pilot Project Portland, Oregon March 2004 FEMA FEMA 436 Page intentionally left blank. Risk Assessment Pilot Project Results for DMA

Catastrophe Risk Modeling and Application- Risk Assessment for Taiwan Residential Earthquake Insurance Pool

5.00% 4.50% 4.00% 3.50% 3.00% 2.50% 2.00% 1.50% 1.00% 0.50% 0.00% 0 100 200 300 400 500 600 700 800 900 1000 Return Period (yr) OEP20050930 Catastrophe Risk Modeling and Application Risk Assessment for

5.00% 4.50% 4.00% 3.50% 3.00% 2.50% 2.00% 1.50% 1.00% 0.50% 0.00% 0 100 200 300 400 500 600 700 800 900 1000 Return Period (yr) OEP20050930 Catastrophe Risk Modeling and Application Risk Assessment for

Flood Solutions. Summer 2018

Flood Solutions Summer 2018 Flood Solutions g Summer 2018 Table of Contents Flood for Lending Life of Loan Flood Determination... 2 Multiple Structure Indicator... 2 Future Flood... 2 Natural Hazard Risk...

Flood Solutions Summer 2018 Flood Solutions g Summer 2018 Table of Contents Flood for Lending Life of Loan Flood Determination... 2 Multiple Structure Indicator... 2 Future Flood... 2 Natural Hazard Risk...