The Economy of Italy: Banks on the Edge

|

|

|

- Rodger Boone

- 6 years ago

- Views:

Transcription

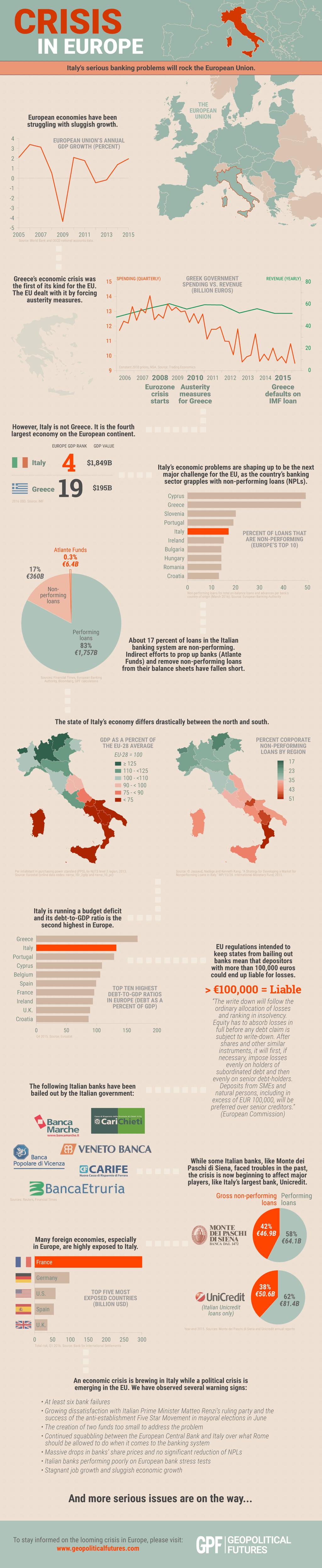

1 The Economy of Italy: Banks on the Edge Oct. 17, 2016 A visual breakdown of Italy s mounting financial crisis. 1 / 8

2 2 / 8

3 Since the 2008 global financial crisis, European economies have been struggling with sluggish growth. Mediterranean Europe in particular has faced a challenging recovery, reflected in the current staggering rates of unemployment, with some nations over 20 percent and all over 10 percent. To make matters worse, the world currently finds itself in the midst of an exporters crisis, which has been unfolding to the point where it appears that a worldwide recession is beginning. Global economic growth forecasts along with estimates for worldwide trade growth have been lowered multiple times throughout the year. The first economic crisis to test the fundamental cohesion of the eurozone was the Greek economic crisis. Germany largely dictated how this crisis was to be handled because it is the largest economy in Europe and the fourth largest economy in the world. Berlin faced a doubleedged sword when looking for solutions to the Greek crisis. On one hand, Germany cannot afford to unilaterally solve the Greek problem, as it would set a precedent Germany cannot live with. It must compel the Greeks to be primarily responsible for its own debts. On the other hand, it cannot afford to see Greece default or leave the European Union. Germany relies on the European free trade zone for nearly half of its exports, and total exports account for almost half of Germany s GDP. It is terrified of a breakdown in the eurozone. Default would lead Greece to leave the eurozone, which would then set a precedent for leaving the free trade zone. The Crisis in the South This year, Germany has been confronted with a farm more daunting challenge: the economy of Italy. Italy is a $1.8 trillion economy and the fourth largest in Europe. The size of the Greek economy pales in comparison. Italy already has a major unemployment problem in the south. It is now facing a rising rate of non-performing loans (NPLs) loans that are not being paid back. Italy s NPLs now total an estimated 360 billion euros (about $395 billion) and show no signs of significantly reducing in the near future. It should be noted that the source of Italian NPLs is overwhelmingly corporate. According to a 2015 International Monetary Fund paper, 80 percent of Italian NPLs were in the corporate sector. Moreover, the regional average for corporate NPLs is above 30 percent, and in some southern regions in Italy exceeds 50 percent. This is not a problem confined to a few individual borrowers. This is a larger issue affecting small and medium-sized enterprises that provide jobs for a large part of the economy of Italy. It is a systemic issue, and though it is far worse in southern Italy, it is not confined there. The Italian government has spent the year searching for potential ways to avoid a massive breakdown in the financial system. Failure to succeed in this endeavor means economic failure and greatly increases the risk of political failure. Unemployment in at least four of Italy s southern provinces is over 18.8 percent and in the other southern provinces is between 12 3 / 8

4 percent and 18.7 percent, according to Eurostat. Disillusionment with the Italian government is growing and the crisis has also raised the deeper question about whether Italy should stay in the European Union. These issues will likely come to a head in a Dec. 4 public referendum in which Italians will vote on constitutional changes to restructure the government in a way that is supposed to facilitate the government taking action to address the economic crisis. Prime Minister Matteo Renzi has previously said he would resign if he lost the referendum. What Are Italy s Options? The argument for staying in the EU will be that Italy can t get better without the EU. The argument for leaving the union will be that Italy will never get better if it stays. In any case, the malaise that has gripped the economy of Italy for years will continue, and it is important not to expect solutions in a matter of weeks. The question is whether this is the permanent condition of Europe. A solution to the Italian banking crisis is becoming more and more urgent. The problems are that, given Europe s track record, speed is unlikely and the Italian crisis has proved far more challenging than the Greek one. Compounding the complexity of the issue is that the solution to this crisis does not only have economic consequences, but political consequences throughout the entire eurozone. The current Italian banking crisis carries with it the possibility of bank failures. The consequences of these failures pyramid the crisis because of European Union regulations. Essentially, the position of the European Union is that the European Central Bank (ECB) and the central banks of member countries cannot bail out failing banks by recapitalizing them in other words, injecting money to keep them solvent. EU regulations go so far as to prohibit Italy from using its state funds to shield investors and shareholders of banks from losses, unless there is risk of very extraordinary systemic stress. Rather, the European Union has adopted a bail-in strategy. Making Investors Out of Depositors The bail-in strategy is in theory a mechanism for ensuring fair competition and stability in the financial sector across the eurozone. It protects countries, like Germany, from spending their money on bank failures in other countries, and keeps the ECB from printing extra money and exposing Europe to inflation that would reduce the position of creditors. The fear of inflation is remote at the moment but it still is an institutional principle of the ECB. And controlling national expenditures on banks imposes fiscal discipline on countries that seek to bail out not just banks, but the equity holdings of investors, who will lose their investment when the bank fails. The issue is this: who is considered an investor? In the view of the EU, depositors are, in cases of a bank resolution, investors in the bank. The bail-in process can potentially apply to any 4 / 8

5 liabilities of the institution not backed by assets or collateral. There is some insurance available, and there are EU regulations on deposit insurance, but there is no EU-wide system of deposit insurance. This is because creditor nations do not want to share the liability for bank failures in other nations. This means that while the first 100,000 euros in deposits are protected, in the sense that they cannot be seized, any money above that amount can be. The idea of the bail-in obliterates a distinction that has become fundamental to European and American banking since the massive banking failures of the 1920s and 1930s. It was understood that the purpose of a savings account was to find a safe haven for your savings or your operating capital. The depositor paid for the safe haven by accepting extremely modest interest rates. In contrast, an investor takes on greater risk and is responsible for evaluating the financials of an investment. The bank is an institution that is an alternative to riskier investments. There is one tremendous consequence in this bail-in strategy. It increases the possibility of runs on banks, particularly by large depositors. As it becomes known that depositors are investors and that their assets will be forfeited to pay debtors, the bank ceases to be a safe haven. The more aware the depositor becomes that he will be treated as an investor, the more he will behave like an investor. Realizing that his bank deposit is all risk with no upside, any indication that risks are mounting will cause a rational actor to withdraw his money, and this will increase the risk of a run and collapse. The Economy of Italy in a Downward Spiral Italy, EU regulators and eurozone countries like Germany now find themselves caught in a toxic cycle. The EU s rules have limited the Italian government s ability to provide support for struggling banks. Partly as a result, European regulators have been cautioning about the state of Italian banks. EU warnings about banks have spooked investors the same investors that the Italian government and EU had hoped would buy tranches of bad loans under an EU-approved plan to help Italy s banks. Failure to effectively implement this plan has forced the Italian government to consider alternative ways to pump money into ailing banks. Some of these plans, however, may contravene EU rules. Floating these alternative proposals is further spooking European institutions and private investors, while heightening tensions between Rome and Berlin. For example, the Italians want to run a substantial budget deficit to stimulate the economy of Italy. The EU operates under a stability pact, which requires deficits to be kept within certain limits, but allows for exceptions. One exception has been France, which has been operating outside the boundaries of the stability pact for years. Spain and Portugal were recently given exceptions as well. As German Chancellor Angela Merkel put it, The stability pact has a lot of 5 / 8

6 flexibility, which we have to apply in a smart way. In the meantime, Italy will continue to come up with homegrown solutions, knowing that the ECB may approve or reject the proposal. For example, in October 2015 the European Commission rejected an Italian plan to create a single bad bank that would have taken away all of the debts held by Italian banks. The twin goals in this plan would have been to encourage investment into Italy s banks while creating a more efficient vehicle, backed by state guarantees, for selling the bad debt on the market. Italy s broad strategy is to find a way to shift the risk from the banks to the Italian government which is precisely what new EU regulations try to prevent. That said, there is also the question of whether the Italian government could absorb the risk of all these loans failing. Italy s debt-to-gdp ratio is more than 132 percent, second in the eurozone only to Greece. The Italian budget passed last December is around 32 billion euros and is projected to run a deficit of 2.4 percent of GDP and exceed the previous target of 1.8 percent. Italy has already taken steps to safeguard its ailing banking system, but Rome s efforts have had limited impact. In November 2015, the Italian government raised 3.6 billion euros to rescue four smaller banks. It did that by getting three-year advances of 600 million euro loan installments from healthier Italian banks. The government may be able to save a few banks, such as Monte dei Paschi di Siena, which is struggling to find a buyer, but Italy doesn t have the ability to bail out the entire banking sector. Taking out loans is theoretically possible, but the premium Italy will have to pay for borrowing money is only going to increase. A second attempt was made this past April when the Italian government set up the Atlante fund, a 4.25 billion euro fund charged with purchasing shares of troubled lenders and buying bad debt in an effort to alleviate concerns over the Italian banking sector. Two months later, roughly half of these funds were already used to purchase Banca Popolare di Vicenza and Veneto Banca when both banks IPOs failed. Italy s largest bank, UniCredit, had lost 55 percent of its value as of June and needs an estimated 10 billion euros in additional capital. The bank received 3 billion euros from the initial round of targeted longer-term refinancing operations loans from the ECB. While special government funds may address some issues in the short term, it is not enough to solve the underlying problems. The Euro Problem For nearly a year now, Brussels has been trying to impose strict financial targets on Italy. For years, Germany has subscribed to the policy of austerity for southern Europe. Both sides have reasonable demands. Italy wants the EU to support it in a particularly challenging time. Germany does not want to be held responsible for what it sees as another country s profligate lending. One reason there has been such a standoff over how to solve Italy s banking crisis is because Italy and Germany have found their interests diverging despite the fact that neither country can afford to see Italy s banking system collapse. 6 / 8

7 However, there are now growing indications that Germany is being forced to shift its commitment to austerity. Initial indicators of this include Germany s recommendation that the EU not fine Spain and Portugal for their excessive deficits, as well as Merkel s recent call for the EU to show Italy more flexibility in terms of spending. Several key factors are contributing to this evolution. Germany s export crisis, lower interest rates, the refugee crisis and political changes across the Continent have led to a change in Germany s constraints and priorities. Germany s export crisis is one of the driving forces behind Berlin s reduced focus on austerity. The eurozone is an important destination for German exports, and austerity policies which prevented governments from adequately addressing low growth and unemployment hurt demand for German goods. Now that the country is facing an exports crisis, Berlin must now consider the possibility that stimulus in southern economies like Italy could help revive some demand for German goods. At the same time, despite austerity, German banks are currently facing the risk of contagion from southern European banks saddled with non-performing loans and suffering due to low growth and low interest rates. In late August, the European Commission approved plans for a 5 billion euro recapitalization of Portugal s Caixa Geral de Depósitos, a state-owned entity and Portugal s largest bank by assets. The plan includes a government injection of 2.7 billion euros which the EU has agreed not to consider state aid. European authorities are showing great flexibility on banking and budget rules for Portugal because they fear contagion from Portugal s ailing banking system that is still saddled with 33.7 billion euros worth of NPLs, representing 12 percent of total loans. This not only sets precedence within the eurozone but also opens the door for discussion on how more flexibility can be demonstrated towards the Italian government. Lastly, the refugee crisis has also contributed to the decline of austerity politics, as the vast majority of asylum seekers arrive in two key southern European economies Italy and Greece. While arrivals to Greece have been declining, in part due to the EU s deal with Turkey, refugees continue heading to Italy in large numbers. Thus far in 2016, 165,409 people have arrived in Greece and 129,126 in Italy. The continuation of the refugee crisis and its disproportionate impact on southern Europe are giving the region s governments ammunition in their negotiations over austerity. Southern Europe s economies, like the economy of Italy, are fragile, and the decline of austerity politics does not mean that the problem of debt is going away. Haggling between governments and Brussels over budgets will continue, and some political forces in Berlin will still prefer to see spending cuts in southern Europe. But fiscal health and spending cuts in the region are gradually taking a backseat as German leaders turn their attention to the export crisis, banking stability, refugee issues and the rise of anti-establishment parties. In the long run, this may be a risky choice, and for some countries austerity could come back with a vengeance. But as Europe fragments, EU members and Germany in particular will become more flexible on issues like austerity as they race to address pressing crises and keep the bloc together. This may ultimately 7 / 8

8 Powered by TCPDF ( Geopolitical Futures prove to be advantageous for Italy as it seeks to mitigate and solve its banking crisis. 8 / 8

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 THE DEBT CRISIS IN GREECE AND THE EURO ZONE

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 April 2010 Prepared by: Sema Gençay ÇAPANOĞLU (scapanoglu@ikv.org.tr) THE DEBT CRISIS IN GREECE AND THE EURO ZONE Greece is struggling with the most serious

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 April 2010 Prepared by: Sema Gençay ÇAPANOĞLU (scapanoglu@ikv.org.tr) THE DEBT CRISIS IN GREECE AND THE EURO ZONE Greece is struggling with the most serious

The Lurking Crisis of Bank Deposits

The Lurking Crisis of Bank Deposits Feb 01, 2016 The Italian banking crisis has moved to its next inevitable stage. European institutions have started to struggle with the question of whether and how to

The Lurking Crisis of Bank Deposits Feb 01, 2016 The Italian banking crisis has moved to its next inevitable stage. European institutions have started to struggle with the question of whether and how to

International Environment Economics for Business (IEEB)

") International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

Greece and the Eurozone: Background, Context, and Prospects

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

Can the Euro Survive?

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Italy Prometeia Brief

Executive summary Italy Prometeia Brief January 2017 No. 17/1 GDP growth forecast for 2016 revised upward to 0.9 per cent while 2017 forecast revised downward to 0.7 per cent Effects of recent downgrade

Executive summary Italy Prometeia Brief January 2017 No. 17/1 GDP growth forecast for 2016 revised upward to 0.9 per cent while 2017 forecast revised downward to 0.7 per cent Effects of recent downgrade

Greece and the Eurozone: Background, Context, and Prospects. Stergios Skaperdas Global Peace and Conflict Studies February 12, 2015

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas Global Peace and Conflict Studies February 12, 2015 Agenda Background on Greece Context: Eurozone and the EU Four scenarios:

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas Global Peace and Conflict Studies February 12, 2015 Agenda Background on Greece Context: Eurozone and the EU Four scenarios:

The Risks Facing European Banks

The Risks Facing European Banks February 29, 2016 This commentary was written by Bill Witherell, Cumberland s Chief Global Economist. He joined Cumberland after years of experience at the OECD in Paris.

The Risks Facing European Banks February 29, 2016 This commentary was written by Bill Witherell, Cumberland s Chief Global Economist. He joined Cumberland after years of experience at the OECD in Paris.

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks September 26, 2013 by Andrew Balls of PIMCO In the following interview, Andrew Balls, managing director and head of European portfolio

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks September 26, 2013 by Andrew Balls of PIMCO In the following interview, Andrew Balls, managing director and head of European portfolio

17 FAQs regarding Cyprus' bail-out/bail-in

17 FAQs regarding Cyprus' bail-out/bail-in 1. How big is Cyprus? Cyprus is an island in the Mediterranean see, located north of Israel and south of Turkey. Its size is around 9,250 square kilometres. It

17 FAQs regarding Cyprus' bail-out/bail-in 1. How big is Cyprus? Cyprus is an island in the Mediterranean see, located north of Israel and south of Turkey. Its size is around 9,250 square kilometres. It

1. Resolution of banks and investment firms

C. Recovery and resolution During the year under review, the Bank s work on recovery and resolution mainly concerned resolution in the banking sector. While the European institutional framework remained

C. Recovery and resolution During the year under review, the Bank s work on recovery and resolution mainly concerned resolution in the banking sector. While the European institutional framework remained

Interview with Klaus Regling, Managing Director, ESM. Published in Hospodárske noviny (Slovakia) on 16 September Interviewer: Tomáš Púchly

on 16 September Interviewer: Tomáš Púchly") Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Fund Management Diary

Fund Management Diary Meeting held on 19 July 2016 EU Bailout Rarely have we been through such a period when events have moved so fast that markets have inevitably been left in the wake. Critically, the

Fund Management Diary Meeting held on 19 July 2016 EU Bailout Rarely have we been through such a period when events have moved so fast that markets have inevitably been left in the wake. Critically, the

The Big Picture Hasn t Changed: Don t Get Sucked Back Into the Stock Market

The Big Picture Hasn t Changed: Don t Get Sucked Back Into the Stock Market July 22, 2016 by Justin Spittler of Casey Research Stocks are on a tear right now Today, the S&P 500 hit a new all-time high.

The Big Picture Hasn t Changed: Don t Get Sucked Back Into the Stock Market July 22, 2016 by Justin Spittler of Casey Research Stocks are on a tear right now Today, the S&P 500 hit a new all-time high.

Gains for all: A proposal for a common euro bond Paul De Grauwe Wim Moesen. University of Leuven

Gains for all: A proposal for a common euro bond Paul De Grauwe Wim Moesen University of Leuven Until the eruption of the credit crisis in August 2007 financial markets were gripped by a flight to risk.

Gains for all: A proposal for a common euro bond Paul De Grauwe Wim Moesen University of Leuven Until the eruption of the credit crisis in August 2007 financial markets were gripped by a flight to risk.

Cyprus Proposal. March 27 th, 2013, 5:00PM EST

Cyprus Proposal March 27 th, 2013, 5:00PM EST Cyprus Proposal The paramount questions remain: 1) What is the end-game solution for the Euro? 2) How will the Euro survive after the Cyprus solution? 3) What

Cyprus Proposal March 27 th, 2013, 5:00PM EST Cyprus Proposal The paramount questions remain: 1) What is the end-game solution for the Euro? 2) How will the Euro survive after the Cyprus solution? 3) What

2016 Stress Test Results. Sources: Bloomberg, EBA

August 5, 2016 Global Economic Research 50 South LaSalle Chicago, Illinois 60603 northerntrust.com Carl R. Tannenbaum Chief Economist 312.557.8820 ct92@ntrs.com Asha G. Bangalore Economist 312.444.4146

August 5, 2016 Global Economic Research 50 South LaSalle Chicago, Illinois 60603 northerntrust.com Carl R. Tannenbaum Chief Economist 312.557.8820 ct92@ntrs.com Asha G. Bangalore Economist 312.444.4146

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

Imbalances in the Eurozone & the position of Germany. Wendy Carlin, UCL & CEPR April 2012

Imbalances in the Eurozone & the position of Germany Wendy Carlin, UCL & CEPR April 2012 Should surplus countries adjust? Standard argument in favour of balanced responsibility for adjustment Currency

Imbalances in the Eurozone & the position of Germany Wendy Carlin, UCL & CEPR April 2012 Should surplus countries adjust? Standard argument in favour of balanced responsibility for adjustment Currency

Europe in crisis. George Gelauff. ECU 92 Lustrum Conference Utrecht. 23 February 2012

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Cristina Camastra Matr IL QUANTITATIVE EASING DELLA BCE. The object of my work is The BCE s Quantitative Easing discussed through three

Cristina Camastra Matr. 067972 IL QUANTITATIVE EASING DELLA BCE The object of my work is The BCE s Quantitative Easing discussed through three chapters. In the first part I will talk about quantitative

Cristina Camastra Matr. 067972 IL QUANTITATIVE EASING DELLA BCE The object of my work is The BCE s Quantitative Easing discussed through three chapters. In the first part I will talk about quantitative

Eurozone. Outlook for. Ernst & Young Eurozone Forecast. Summer edition 2012

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

Adventures in Monetary Policy: The Case of the European Monetary Union

: The Case of the European Monetary Union V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis The ECB and Its Watchers XIX March 14, 2018 Why the Discontent? The Tell-Tale

: The Case of the European Monetary Union V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis The ECB and Its Watchers XIX March 14, 2018 Why the Discontent? The Tell-Tale

Recent liquidity injections by the European Central Bank have brought relief to the banking system and sovereign bond markets.

OBSERVATION TD Economics February 29, 2 DELEVERAGING BEGETS WEAK ECONOMIES ACROSS EURO ZONE PERIPHERY Highlights Recent liquidity injections by the European Central Bank have brought relief to the banking

OBSERVATION TD Economics February 29, 2 DELEVERAGING BEGETS WEAK ECONOMIES ACROSS EURO ZONE PERIPHERY Highlights Recent liquidity injections by the European Central Bank have brought relief to the banking

Eurozone Focus The Ongoing Saga Of Sovereign Debt

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies?

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.

During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.") Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016.

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

Tria: «Government commitment to the euro. And the debt will fall» Italian version

Pagina 1 di 6 Stampa Stampa senza immagine Chiudi INTERVIEW Tria: «Government commitment to the euro. And the debt will fall» Italian version The Minister of Economics: «The position of the executive branch

Pagina 1 di 6 Stampa Stampa senza immagine Chiudi INTERVIEW Tria: «Government commitment to the euro. And the debt will fall» Italian version The Minister of Economics: «The position of the executive branch

The outlook for the global economy in 2012

The Eurozone Crisis Still Threatens Global Growth Paolo Guerrieri Professor of Economics, University of Rome Sapienza; Professor, College of Europe, Bruges The outlook for the global economy in 2012 is

The Eurozone Crisis Still Threatens Global Growth Paolo Guerrieri Professor of Economics, University of Rome Sapienza; Professor, College of Europe, Bruges The outlook for the global economy in 2012 is

The EU is running out of choices to tame the crisis

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

Italy: liquidation of Veneto Banca and Banca Popolare di Vicenza

ECONOMIC RESEARCH DEPARTMENT Italy: liquidation of Veneto Banca and Banca Popolare di Vicenza Given their modest size, Veneto Banca and Banca Popolare di Vicenza are set to undergo an insolvency procedure

ECONOMIC RESEARCH DEPARTMENT Italy: liquidation of Veneto Banca and Banca Popolare di Vicenza Given their modest size, Veneto Banca and Banca Popolare di Vicenza are set to undergo an insolvency procedure

EUROPEAN BANKS: NEITHER A BORROWER NOR LENDER BE

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY August 8 2016 EUROPEAN BANKS: NEITHER A BORROWER NOR LENDER BE Matthew Peterson Chief Wealth Strategist, LPL Financial KEY TAKEAWAYS Banks everywhere are under pressure

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY August 8 2016 EUROPEAN BANKS: NEITHER A BORROWER NOR LENDER BE Matthew Peterson Chief Wealth Strategist, LPL Financial KEY TAKEAWAYS Banks everywhere are under pressure

Comunicato Stampa DIFFUSO A CURA DEL SERVIZIO SEGRETERIA PARTICOLARE DEL DIRETTORIO E COMUNICAZIONE

Comunicato Stampa DIFFUSO A CURA DEL SERVIZIO SEGRETERIA PARTICOLARE DEL DIRETTORIO E COMUNICAZIONE Results of the Comprehensive Assessment 26 October 2014 The results have been published today of the

Comunicato Stampa DIFFUSO A CURA DEL SERVIZIO SEGRETERIA PARTICOLARE DEL DIRETTORIO E COMUNICAZIONE Results of the Comprehensive Assessment 26 October 2014 The results have been published today of the

Economics Essay Sample

Critically assess the main challenges facing the EU in 2013 and its capacity to meet them, with particular reference either to enlargement or to further integration. Introduction This brief essay aims

Critically assess the main challenges facing the EU in 2013 and its capacity to meet them, with particular reference either to enlargement or to further integration. Introduction This brief essay aims

Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015

, 8 November 2015") Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015 Politis: The main goal of the programme is to restore confidence in Cyprus. Is this mission complete?

Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015 Politis: The main goal of the programme is to restore confidence in Cyprus. Is this mission complete?

Member of

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Why ESBies won t solve the euro area s problems

https://ftalphaville.ft.com/2017/04/25/2187829/guest-post-why-esbies-wont-solve-the-euro-areas-problems/ Why ESBies won t solve the euro area s problems APRIL 25, 2017 By: Marcello Minenna The following

https://ftalphaville.ft.com/2017/04/25/2187829/guest-post-why-esbies-wont-solve-the-euro-areas-problems/ Why ESBies won t solve the euro area s problems APRIL 25, 2017 By: Marcello Minenna The following

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA Ulrich Volz, German Development Institute 8 August 2012, United Nations Economic and Social Commission for Asia

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA Ulrich Volz, German Development Institute 8 August 2012, United Nations Economic and Social Commission for Asia

Ways out of the crisis

Ways out of the crisis This contribution is part of the collaboration between FEPS and ECLM (www.eclm.dk) March 2011 Any further information can be obtained through FEPS Secretary General, Dr Ernst Stetter,

Ways out of the crisis This contribution is part of the collaboration between FEPS and ECLM (www.eclm.dk) March 2011 Any further information can be obtained through FEPS Secretary General, Dr Ernst Stetter,

Regling: Greece has to repay that loan in full. That is our expectation, nothing has changed in that regard.

Handelsblatt, 6 March 2015 Greece needs to repay its loan in full Handelsblatt: Mr. Regling, the euro rescue fund EFSF has lent around 142 billion to Greece and is thus by far Greece s largest creditor.

Handelsblatt, 6 March 2015 Greece needs to repay its loan in full Handelsblatt: Mr. Regling, the euro rescue fund EFSF has lent around 142 billion to Greece and is thus by far Greece s largest creditor.

Can the Eurozone Reform?

Can the Eurozone Reform? by Economist Conference on: Governance and regional arteries for Growth: Europe s momentum Greece s impetus, Wyndham Loutraki Poseidon Resort, Greece, May 10-11, 2018 The Greek

Can the Eurozone Reform? by Economist Conference on: Governance and regional arteries for Growth: Europe s momentum Greece s impetus, Wyndham Loutraki Poseidon Resort, Greece, May 10-11, 2018 The Greek

Policy Note A PROPOSAL TO CREATE A EUROPEAN SAFE ASSET. Levy Economics Institute of Bard College. The Problem 2019 / 1

Levy Economics Institute of Bard College Policy Note 2019 / 1 A PROPOSAL TO CREATE A EUROPEAN SAFE ASSET PAOLO SAVONA The Problem There is a consensus on the fact that the eurozone and the instruments

Levy Economics Institute of Bard College Policy Note 2019 / 1 A PROPOSAL TO CREATE A EUROPEAN SAFE ASSET PAOLO SAVONA The Problem There is a consensus on the fact that the eurozone and the instruments

Is Italy s recent support to its banks the start of a new wave of public intervention in the EU?

Is Italy s recent support to its banks the start of a new wave of public intervention in the EU? blogs.lse.ac.uk/europpblog/2017/01/16/italy-support-banks-start-of-new-wave-eu-intervention/ The banking

Is Italy s recent support to its banks the start of a new wave of public intervention in the EU? blogs.lse.ac.uk/europpblog/2017/01/16/italy-support-banks-start-of-new-wave-eu-intervention/ The banking

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2012

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2012 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2012 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

A Decade-Long Economic Crisis: Cyprus vs. Greece

A Decade-Long Economic Crisis: Cyprus vs. Greece Gikas Hardouvelis Professor of Finance & Economics University of Piraeus LSE SU Hellenic and Cypriot Societies Forum London, March 18, 17 TABLE OF CONTENTS

A Decade-Long Economic Crisis: Cyprus vs. Greece Gikas Hardouvelis Professor of Finance & Economics University of Piraeus LSE SU Hellenic and Cypriot Societies Forum London, March 18, 17 TABLE OF CONTENTS

Department of Economics ECONOMIC OVERVIEW

Department of Economics ECONOMIC OVERVIEW January 2012 EDITORIAL Will the Euro Survive? By joining the euro, Europe s peripheral countries gained access to cheap, easy financing. They spent beyond their

Department of Economics ECONOMIC OVERVIEW January 2012 EDITORIAL Will the Euro Survive? By joining the euro, Europe s peripheral countries gained access to cheap, easy financing. They spent beyond their

For the Eurozone, much hinges on self-discipline and self-interest

For the Eurozone, much hinges on self-discipline and self-interest Author: Jonathan Lemco, Ph.D. Will the Eurozone survive its severe financial challenges? Vanguard believes it is in the interests of both

For the Eurozone, much hinges on self-discipline and self-interest Author: Jonathan Lemco, Ph.D. Will the Eurozone survive its severe financial challenges? Vanguard believes it is in the interests of both

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

The Euro Zone Sovereign Debt Crisis: Testing the Limits of Solidarity. Presentation to the IA BE

IA BE The Euro Zone Sovereign Debt Crisis: Testing the Limits of Solidarity Presentation to the IA BE Jean Deboutte 14 June 2011 Table of Contents Section 1 Introduction Section 2 Diagnosis Section 3 Remedies

IA BE The Euro Zone Sovereign Debt Crisis: Testing the Limits of Solidarity Presentation to the IA BE Jean Deboutte 14 June 2011 Table of Contents Section 1 Introduction Section 2 Diagnosis Section 3 Remedies

Europe s Response to the Sovereign Debt Crisis. Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

2016 World Savings Day

ACRI Association of Italian Savings Banks 2016 World Savings Day Address by the Governor of the Bank of Italy Ignazio Visco Rome, 27 October 2016 There are mixed signals from the global economy. On the

ACRI Association of Italian Savings Banks 2016 World Savings Day Address by the Governor of the Bank of Italy Ignazio Visco Rome, 27 October 2016 There are mixed signals from the global economy. On the

Eurozone job crisis:

UNDER EMBARGO UNTIL 22:01 GMT TUESDAY 10 JULY 2012 Eurozone job crisis: Trends and policy responses Executive Summary INTERNATIONAL LABOUR ORGANIZATION INTERNATIONAL INSTITUTE FOR LABOUR STUDIES Executive

UNDER EMBARGO UNTIL 22:01 GMT TUESDAY 10 JULY 2012 Eurozone job crisis: Trends and policy responses Executive Summary INTERNATIONAL LABOUR ORGANIZATION INTERNATIONAL INSTITUTE FOR LABOUR STUDIES Executive

A Selective Focus is Key to Navigating European Banking Sector Challenges

A Selective Focus is Key to Navigating European Banking Sector Challenges March 2016 PERSPECTIVES Key Insights Andrea Brasili Senior Economist Global Asset Allocation Research Diego Franzin Head of Equities

A Selective Focus is Key to Navigating European Banking Sector Challenges March 2016 PERSPECTIVES Key Insights Andrea Brasili Senior Economist Global Asset Allocation Research Diego Franzin Head of Equities

Florida: An Economic Overview

Florida: An Economic Overview March 24, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview March 24, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Greece Rising

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Greece Rising

The Government Deficit and the Financial Crisis

The Government Deficit and the Financial Crisis The 2008 financial crisis has resulted in a huge increase in the federal government deficit. Government spending has increased significantly, and tax revenue

The Government Deficit and the Financial Crisis The 2008 financial crisis has resulted in a huge increase in the federal government deficit. Government spending has increased significantly, and tax revenue

The Lender of Last Resort in the Euro Area: Where Do We Stand?

The Lender of Last Resort in the Euro Area: Where Do We Stand? Karl Whelan University College Dublin Presentation at University College Cork March 9, 2018 Plan for this Talk Lender of last resort Rationale

The Lender of Last Resort in the Euro Area: Where Do We Stand? Karl Whelan University College Dublin Presentation at University College Cork March 9, 2018 Plan for this Talk Lender of last resort Rationale

EUROSTAT SUPPLEMENTARY TABLE FOR REPORTING GOVERNMENT INTERVENTIONS TO SUPPORT FINANCIAL INSTITUTIONS

EUROPEAN COMMISSION EUROSTAT Directorate D: Government Finance Statistics (GFS) and Quality Unit D1: Excessive deficit procedure and methodology Unit D2: Excessive deficit procedure (EDP) 1 Unit D3: Excessive

EUROPEAN COMMISSION EUROSTAT Directorate D: Government Finance Statistics (GFS) and Quality Unit D1: Excessive deficit procedure and methodology Unit D2: Excessive deficit procedure (EDP) 1 Unit D3: Excessive

Greece and the Euro. Harris Dellas, University of Bern. Abstract

Greece and the Euro Harris Dellas, University of Bern Abstract The recent debt crisis in the EU has revived interest in the costs and benefits of membership in a currency union for a country like Greece

Greece and the Euro Harris Dellas, University of Bern Abstract The recent debt crisis in the EU has revived interest in the costs and benefits of membership in a currency union for a country like Greece

A European Unemployment Insurance Scheme? An Interview with Sebastian Dullien

A European Unemployment Insurance Scheme? An Interview with Sebastian Dullien By Thomas Vendryes First evoked in the 1970s, the idea of a European unemployment benefit scheme has recently become a topics

A European Unemployment Insurance Scheme? An Interview with Sebastian Dullien By Thomas Vendryes First evoked in the 1970s, the idea of a European unemployment benefit scheme has recently become a topics

Florida: An Economic Overview

Florida: An Economic Overview May 1, 2012 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Mixed Economy Turned

Florida: An Economic Overview May 1, 2012 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Mixed Economy Turned

The role of ECB in relation to the modified EFSF and the future ESM. Prof. Dr. iur. Dr. rer. pol. Peter Sester

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

2Q16. Don t Be So Negative. June Uncharted territory

2Q16 TOPICS OF INTEREST Don t Be So Negative June 2016 ANDREW AKERS Analyst Following the financial crisis of 2008, slow global growth and low inflation have prompted a number of central banks to implement

2Q16 TOPICS OF INTEREST Don t Be So Negative June 2016 ANDREW AKERS Analyst Following the financial crisis of 2008, slow global growth and low inflation have prompted a number of central banks to implement

EUROPE LEADS FLIGHT TO QUALITY

EUROPE LEADS FLIGHT TO QUALITY Our cautious stance has paid off this quarter as many of the risks we were concerned about have begun to play out. This has led to a flight to quality, which is where we

EUROPE LEADS FLIGHT TO QUALITY Our cautious stance has paid off this quarter as many of the risks we were concerned about have begun to play out. This has led to a flight to quality, which is where we

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Cyprus

Eurozone EY Eurozone Forecast September 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Cyprus

In search of symmetry in the eurozone

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

The 2008 crisis and the future: Have the important lessons been learned?

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Banking union: restoring financial stability in the Eurozone

EUROPEAN COMMISSION MEMO Brussels, 15 April 2014 Banking union: restoring financial stability in the Eurozone 1. Banking union in a nutshell Since the crisis started in 2008, the European Commission has

EUROPEAN COMMISSION MEMO Brussels, 15 April 2014 Banking union: restoring financial stability in the Eurozone 1. Banking union in a nutshell Since the crisis started in 2008, the European Commission has

How the Eurozone will be resolving its crisis

How the Eurozone will be resolving its crisis Wolfgang MÜNCHAU Eurointelligence ASBL The political economy of the Eurozone is based on three pillars: lies, loopholes and fudges. Back in the 1990s, its

How the Eurozone will be resolving its crisis Wolfgang MÜNCHAU Eurointelligence ASBL The political economy of the Eurozone is based on three pillars: lies, loopholes and fudges. Back in the 1990s, its

Bernard Connolly Europe Driver or Driven? EMU and the Lust for Crisis ACI Congress, May 30, 2008

Bernard Connolly Europe Driver or Driven? EMU and the Lust for Crisis ACI Congress, May 30, 2008 0 The information contained herein is being furnished for discussion purposes only and may be subject to

Bernard Connolly Europe Driver or Driven? EMU and the Lust for Crisis ACI Congress, May 30, 2008 0 The information contained herein is being furnished for discussion purposes only and may be subject to

Briefing Note on Euro Zone Crisis and its Impact on India July 2012

Briefing Note on Euro Zone Crisis and its Impact on India July 2012 Contents Briefing Note on Euro Zone Crisis and its Impact on India Executive summary. 3 Section 1 Global economic scenario 4 Gross Domestic

Briefing Note on Euro Zone Crisis and its Impact on India July 2012 Contents Briefing Note on Euro Zone Crisis and its Impact on India Executive summary. 3 Section 1 Global economic scenario 4 Gross Domestic

Flash Note Euro area: sovereign bond yields scenario update

FLASH NOTE Flash Note Euro area: sovereign bond yields scenario update The dust settles after the Brexit vote Pictet Wealth Management - Asset Allocation & Macro Research 28 July 2016 The German 10-years

FLASH NOTE Flash Note Euro area: sovereign bond yields scenario update The dust settles after the Brexit vote Pictet Wealth Management - Asset Allocation & Macro Research 28 July 2016 The German 10-years

Italy: fundamentals are the compass amid political twists

Italy: fundamentals are the compass amid political twists Eric Brard Head of Fixed Income Annalisa USARDI, CFA Senior Economist With the contribution of: Giuseppina Marinotti Investment Insights Unit The

Italy: fundamentals are the compass amid political twists Eric Brard Head of Fixed Income Annalisa USARDI, CFA Senior Economist With the contribution of: Giuseppina Marinotti Investment Insights Unit The

Impact of Greece Debt Crisis on World Economy

Impact of Greece Debt Crisis on World Economy Kovid Kumar Gupta 1 kovid.gupta@gmail.com Abstract This study aims at exploring the reasons behind the Greece debt crisis that emerged in the 21 st century

Impact of Greece Debt Crisis on World Economy Kovid Kumar Gupta 1 kovid.gupta@gmail.com Abstract This study aims at exploring the reasons behind the Greece debt crisis that emerged in the 21 st century

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

Global Debt Crisis & Impact on India. October 2011

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Slovenia

Eurozone EY Eurozone Forecast June 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Slovenia

The Budget Deficit of the United States and the Current Account Deficits of the Eurozone Latin Countries

(Ackermann) Remarks at dinner honoring Joe Ackermann October 25, 2012 Martin Feldstein The Budget Deficit of the United States and the Current Account Deficits of the Eurozone Latin Countries Thank you.

(Ackermann) Remarks at dinner honoring Joe Ackermann October 25, 2012 Martin Feldstein The Budget Deficit of the United States and the Current Account Deficits of the Eurozone Latin Countries Thank you.

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Hearing on Decree Law 237/2016 Urgent measures for the protection of savings in the banking sector

Joint Session of the Sixth Committees of the Senate of the Republic (Finance and Treasury) and the Chamber of Deputies (Finance) Hearing on Decree Law 237/2016 Urgent measures for the protection of savings

Joint Session of the Sixth Committees of the Senate of the Republic (Finance and Treasury) and the Chamber of Deputies (Finance) Hearing on Decree Law 237/2016 Urgent measures for the protection of savings

Investment assets totalled EUR billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms

1/13 Investment assets totalled EUR 188.5 billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms At the end of 2016, the total net amount of assets put into funds by earnings-related

1/13 Investment assets totalled EUR 188.5 billion at the end of 2016 return for the past 20 years 4.3 per cent in real terms At the end of 2016, the total net amount of assets put into funds by earnings-related

Policy Reforms after the Crisis

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

What s Going on in Italy?

WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS What s Going on in Italy? October 16, 2018 Peter Donisanu Investment Strategy Analyst Key takeaways» Global financial markets have been rocked by concerns

WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS What s Going on in Italy? October 16, 2018 Peter Donisanu Investment Strategy Analyst Key takeaways» Global financial markets have been rocked by concerns

International Money and Banking: 8. How Central Banks Set Interest Rates

International Money and Banking: 8. How Central Banks Set Interest Rates Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Central Banks and Interest Rates Spring 2018 1 / 32 Monetary

International Money and Banking: 8. How Central Banks Set Interest Rates Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Central Banks and Interest Rates Spring 2018 1 / 32 Monetary

Italy: Beyond the point of no return or surprisingly resilient? Public Finances and the Economic and Financial Document Rome, 11 March 2017

Lorenzo Codogno LC Macro Advisors Ltd Founder and Chief Economist +44 758 3564410 lorenzo.codogno@lc-ma.com Visiting Professor at London School of Economics L.Codogno@lse.ac.uk Italy: Beyond the point

Lorenzo Codogno LC Macro Advisors Ltd Founder and Chief Economist +44 758 3564410 lorenzo.codogno@lc-ma.com Visiting Professor at London School of Economics L.Codogno@lse.ac.uk Italy: Beyond the point

EuroView: Looking beyond the shortterm

October 2016 EuroView: Looking beyond the shortterm risks Rory Bateman, Head of UK & European Equities While we are encouraged by the European equity market recovery since the UK s EU referendum, the total

October 2016 EuroView: Looking beyond the shortterm risks Rory Bateman, Head of UK & European Equities While we are encouraged by the European equity market recovery since the UK s EU referendum, the total

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

Europe s Response to the Sovereign Debt Crisis. Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Greek Debts Updates After Referendum

Market Insights Greek Debts Updates After Referendum 07/2015 What happened? Greece voted against yielding to further austerity, as demanded by creditors with 61% of voters backing up Prime Minister Alexis

Market Insights Greek Debts Updates After Referendum 07/2015 What happened? Greece voted against yielding to further austerity, as demanded by creditors with 61% of voters backing up Prime Minister Alexis

GREECE S IMPACT ON THE EUROPEAN DEBT CRISIS

1 GREECE S IMPACT ON THE EUROPEAN DEBT CRISIS Summary The European leaders had initially planned to unveil a clear action plan to their counterparts at the G20 Summit on November 3-4th in Cannes, France

1 GREECE S IMPACT ON THE EUROPEAN DEBT CRISIS Summary The European leaders had initially planned to unveil a clear action plan to their counterparts at the G20 Summit on November 3-4th in Cannes, France

Economic and Financial Affairs Committee. The EMU: challenges and the way forward

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for Modest

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for Modest

Negative Yields in the Eurozone: Rationale and Repercussions

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not