Imbalances in the Eurozone & the position of Germany. Wendy Carlin, UCL & CEPR April 2012

|

|

|

- Alberta Gregory

- 5 years ago

- Views:

Transcription

1 Imbalances in the Eurozone & the position of Germany Wendy Carlin, UCL & CEPR April 2012

2 Should surplus countries adjust? Standard argument in favour of balanced responsibility for adjustment Currency union is two blocs North & South South is uncompetitive with current account deficit (and in deep recession) North has a surplus and not in recession

3 Should surplus countries adjust? All adjustment is by South this has to be done via nominal wage cuts; likely to require higher unemployment & deeper recession; lowers growth for North as well, via shrinkage of aggregate demand in currency union Balanced adjustment by North and South Relieves South of some deflation of nominal wages and demand Global growth is higher Counterpart is higher inflation in North

4 Should surplus countries adjust? Policy in North Combination of Wages policy, which encourages higher wage growth Fiscal expansion Outcome Real exchange rate depreciation in South; real appreciation in North Lower current account imbalances in new equilibrium Balance sheet relative to unilateral Southern adjustment Eurozone higher growth & higher survival probability South higher growth; lower debt burden; less deflation; less unemployment: unambiguously positive North somewhat higher growth; higher inflation; possibly higher debt ratio: ambiguous

5 Dynamic and political economy considerations the Northern perspective #1 1. Germany has little fiscal space it is close to high employment; its rapidly ageing population makes transition to substantial structural surplus more urgent (e.g. than in some of South) If so, benefits to Germany are more limited & costs are higher: disutility of higher debt; higher inflation

6 Dynamic and political economy considerations the Northern perspective #2 2. Productivity growth & future of good jobs depend on export sector; if so, X sector (& not the state) must retain control of real exchange rate

7 Dynamic and political economy considerations the Northern perspective #2 2. Productivity growth & future of good jobs depend on export sector; if so, X sector (& not the state) must retain control of real exchange rate Why is real exchange rate appreciation via Southern deflation (or via forexmarket under flexible rates) any different from appreciation via domestic nominal wage growth in North? For political economy reasons the former keep the pressure on firms to innovate to retain export market share the latter undermines innovation model of a coordinated market economy

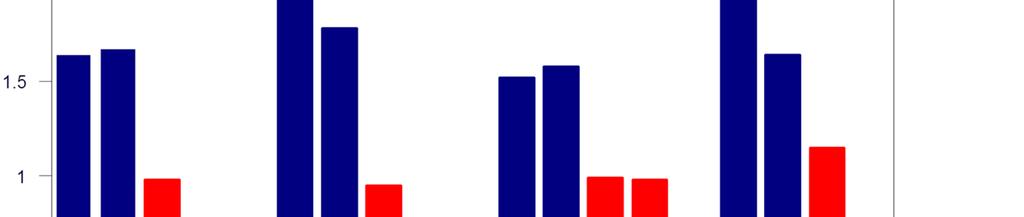

8 Germany & Italy were Europe s laggards, Growth of GDP GDP, 2005 euros (1999=100) Italy Germany

9 Growth of GDP GDP, 2005 euros (1999=100) Italy Germany 9 Source: EU Commission Growth of productivity GDP per employed (1999=100) Germany Italy Germany Italy Growth of compensation per employee (1999=100) Italy Germany

10 Dynamic and political economy considerations the Northern perspective #3 3. Asymmetric adjustment sharpens incentives for South to undertake reforms that make reckless or passive behaviour in Eurozone less likely in future Single currency: successful membership requires growth of unit labour costs at ECB target inflation rate and ability to adjust real exchange rate to shocks / structural change Coordinated economies (North) deliver this via private sector Non-coordinated ones with large wage-setters (South) do not

11 Dynamic and political economy considerations the Northern perspective #3 (cont.) In absence of delivery by private sector, policy must target the real exchange rate Fiscal policy councils Active fiscal policy not a debt brake is required (e.g. Spain s budget surpluses & tumbling debt ratio during ) Demands: Effective policy-making / governance at national level OR Major institutional reforms / change from non-coordination with large wage setters to a different variety of capitalism (? Latvia) OR Monitoring by Brussels (& other governance changes)

12 Governance standards diverged in Eurozone

13 How compelling are these arguments? More scope to increase employment rate in Germany, especially women s Thinking of good jobs only in terms of export sector is too limited & neglects costs of increasingly segmented labour market in Germany Another form of wishful thinking is to expect reforms & structural change required in South to take place under conditions of austerity-only

14 References Boltho, A. and Carlin, W. (2012) The problems of European monetary union asymmetric shocks or asymmetric behaviour? Carlin, W (2011) 10 Questions about the Eurozone crisis and how it can be resolved Carlin, W (2012), Real exchange rate adjustment, wage-setting institutions, and fiscal stabilization policy: Lessons of the Eurozone s first decade, CEPR Discussion Paper No Carlin, W (2012) The Eurozone crisis North and South INET Berlin

How to avoid a double-dip recession in the eurozone

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE. Paul De Grauwe (LSE) Yuemei Ji (Brunel University)

Yuemei Ji (Brunel University)") CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE Paul De Grauwe (LSE) Yuemei Ji (Brunel University) Stagnation in Eurozone Figure 1: Real GDP in Eurozone, EU10 and US (prices of 2010) 135 130 125

CRISIS MANAGEMENT AND ECONOMIC GROWTH IN THE EUROZONE Paul De Grauwe (LSE) Yuemei Ji (Brunel University) Stagnation in Eurozone Figure 1: Real GDP in Eurozone, EU10 and US (prices of 2010) 135 130 125

Europe s Response to the Sovereign Debt Crisis. Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

What Governance for the Eurozone? Paul De Grauwe London School of Economics

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

Europe: social regression forever?

Europe: social regression forever? Michel Husson Beograd, 1. oktobar 2013 Centar za kulturnu dekontaminaciju A three-level crisis 1. A debt crisis The true aim of fiscal austerity is to validate excessive

Europe: social regression forever? Michel Husson Beograd, 1. oktobar 2013 Centar za kulturnu dekontaminaciju A three-level crisis 1. A debt crisis The true aim of fiscal austerity is to validate excessive

Spring Forecast: slowly recovering from a protracted recession

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE. 9 May 2012 Vicky Pryce

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

Does the South of Europe have a competitiveness problem?

Does the South of Europe have a competitiveness problem? Lorenzo Codogno Economic and Financial Analysis Department of the Treasury, Italy s Ministry of Economy and Finance International Price and Cost

Does the South of Europe have a competitiveness problem? Lorenzo Codogno Economic and Financial Analysis Department of the Treasury, Italy s Ministry of Economy and Finance International Price and Cost

Macroeconomic paradigms, policy regimes and the crisis: The origins, strengths & limitations of Taylor Rule macroeconomics

Macroeconomic paradigms, policy regimes and the crisis: The origins, strengths & limitations of Taylor Rule macroeconomics Wendy Carlin UCL & CEPR December 2010 Outline 1. How should we characterize the

Macroeconomic paradigms, policy regimes and the crisis: The origins, strengths & limitations of Taylor Rule macroeconomics Wendy Carlin UCL & CEPR December 2010 Outline 1. How should we characterize the

Paris, November 19, 2013 Michel Husson

Work in times of crisis and changing employment relations Paris, November 19, 2013 Michel Husson A three-level crisis 1. A debt crisis The true aim of fiscal austerity is to validate excessive drawing

Work in times of crisis and changing employment relations Paris, November 19, 2013 Michel Husson A three-level crisis 1. A debt crisis The true aim of fiscal austerity is to validate excessive drawing

Europe in crisis. George Gelauff. ECU 92 Lustrum Conference Utrecht. 23 February 2012

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Eurozone job crisis:

UNDER EMBARGO UNTIL 22:01 GMT TUESDAY 10 JULY 2012 Eurozone job crisis: Trends and policy responses Executive Summary INTERNATIONAL LABOUR ORGANIZATION INTERNATIONAL INSTITUTE FOR LABOUR STUDIES Executive

UNDER EMBARGO UNTIL 22:01 GMT TUESDAY 10 JULY 2012 Eurozone job crisis: Trends and policy responses Executive Summary INTERNATIONAL LABOUR ORGANIZATION INTERNATIONAL INSTITUTE FOR LABOUR STUDIES Executive

GETTING THE EURO ZONE OUT OF THE DOLDRUMS. Michel Aglietta Univ Paris West and Cepii

GETTING THE EURO ZONE OUT OF THE DOLDRUMS Michel Aglietta Univ Paris West and Cepii The way to stagnation: stylized facts and some theory 2 Anemic potential growth, perennial output gap and subpar real

GETTING THE EURO ZONE OUT OF THE DOLDRUMS Michel Aglietta Univ Paris West and Cepii The way to stagnation: stylized facts and some theory 2 Anemic potential growth, perennial output gap and subpar real

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

II. Underlying domestic macroeconomic imbalances fuelled current account deficits

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

What does Western Economic Crisis Mean for South Africa?

What does Western Economic Crisis Mean for South Africa? Seeraj Mohamed Corporate Strategy and Industrial Development Research Programme University of the Witwatersrand Context for Europe s Crisis Global

What does Western Economic Crisis Mean for South Africa? Seeraj Mohamed Corporate Strategy and Industrial Development Research Programme University of the Witwatersrand Context for Europe s Crisis Global

Economic Alignment and Euro Adoption in the Czech Republic: What Is New?

Economic Alignment and Euro Adoption in the Czech Republic: What Is New? Vladimir TOMSIK Vice-Governor Czech National Bank European Business Forum November 3, 2017, Prague Basic Facts Successful inflation

Economic Alignment and Euro Adoption in the Czech Republic: What Is New? Vladimir TOMSIK Vice-Governor Czech National Bank European Business Forum November 3, 2017, Prague Basic Facts Successful inflation

Surrogates of Fiscal Federalism

Surrogates of Fiscal Federalism Francesco Saraceno OFCE-Research Center in Economics of Sciences Po Luiss School of European Political Economy Jakarta School of Government and Public Policy Europe 2020:

Surrogates of Fiscal Federalism Francesco Saraceno OFCE-Research Center in Economics of Sciences Po Luiss School of European Political Economy Jakarta School of Government and Public Policy Europe 2020:

Europe s Response to the Sovereign Debt Crisis. Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Period 3 MBA Program January February MACROECONOMICS IN THE GLOBAL ECONOMY Core Course. Professor Ilian Mihov

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

PUBLIC SPENDING ON CULTURE IN EUROPE

PUBLIC SPENDING ON CULTURE IN EUROPE 2007-2015 Brussels, 21 February 2018 Requested by the Committee on Culture and Education Coordinated by Pere Almeda, Albert Sagarra and Marc Tataret. TABLE OF CONTENTS

PUBLIC SPENDING ON CULTURE IN EUROPE 2007-2015 Brussels, 21 February 2018 Requested by the Committee on Culture and Education Coordinated by Pere Almeda, Albert Sagarra and Marc Tataret. TABLE OF CONTENTS

Managing the Fragility of the Eurozone. Paul De Grauwe London School of Economics

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

The Eurozone Crisis, Greece, and the Experience of Austerity

The Eurozone Crisis, Greece, and the Experience of Austerity From Austerity to Development: The Challenges Ahead Athens, 09.11.2013 Prof. Louka T. Katseli Central Messages 1. Austerity policies have failed

The Eurozone Crisis, Greece, and the Experience of Austerity From Austerity to Development: The Challenges Ahead Athens, 09.11.2013 Prof. Louka T. Katseli Central Messages 1. Austerity policies have failed

A Fiscal Union in Europe: why is it possible/impossible?

Warsaw 18 th October 2013 A Fiscal Union in Europe: why is it possible/impossible? Daniele Franco Chiara Goretti Italian Ministry of the Economy and Finance This talk FROM non-controversial aspects General

Warsaw 18 th October 2013 A Fiscal Union in Europe: why is it possible/impossible? Daniele Franco Chiara Goretti Italian Ministry of the Economy and Finance This talk FROM non-controversial aspects General

74 ECB THE 2012 MACROECONOMIC IMBALANCE PROCEDURE

Box 7 THE 2012 MACROECONOMIC IMBALANCE PROCEDURE This year s European Semester (i.e. the framework for EU policy coordination introduced in 2011) includes, for the first time, the implementation of the

Box 7 THE 2012 MACROECONOMIC IMBALANCE PROCEDURE This year s European Semester (i.e. the framework for EU policy coordination introduced in 2011) includes, for the first time, the implementation of the

The Economy of Italy: Banks on the Edge

The Economy of Italy: Banks on the Edge Oct. 17, 2016 A visual breakdown of Italy s mounting financial crisis. 1 / 8 2 / 8 Since the 2008 global financial crisis, European economies have been struggling

The Economy of Italy: Banks on the Edge Oct. 17, 2016 A visual breakdown of Italy s mounting financial crisis. 1 / 8 2 / 8 Since the 2008 global financial crisis, European economies have been struggling

Greece. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

Global Imbalances, Currency Wars and the Euro

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICIES ECONOMIC AND MONETARY AFFAIRS Global Imbalances, Currency Wars and the Euro NOTE Abstract Global current

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICIES ECONOMIC AND MONETARY AFFAIRS Global Imbalances, Currency Wars and the Euro NOTE Abstract Global current

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Can the Euro Survive?

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

General Certificate of Education Advanced Level Examination January 2013

General Certificate of Education Advanced Level Examination January 2013 Economics ECON4 Unit 4 The National and International Economy Wednesday 30 January 2013 1.30 pm to 3.30 pm For this paper you must

General Certificate of Education Advanced Level Examination January 2013 Economics ECON4 Unit 4 The National and International Economy Wednesday 30 January 2013 1.30 pm to 3.30 pm For this paper you must

Intermediate Macroeconomics

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Session 11. Fiscal Policy

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

The Forex Market in March 2007

1 The Forex Market in March 2007 US Dollar : USD The US dollar in March continued to weaken from prior month compared with the euro and the yen with exchange rates averaging at US$ 1.3251 per euro and

1 The Forex Market in March 2007 US Dollar : USD The US dollar in March continued to weaken from prior month compared with the euro and the yen with exchange rates averaging at US$ 1.3251 per euro and

The Economic Situation of the European Union and the Outlook for

The Economic Situation of the European Union and the Outlook for 2001-2002 A Report by the EUROFRAME group of Research Institutes for the European Parliament The Institutes involved are Wifo in Austria,

The Economic Situation of the European Union and the Outlook for 2001-2002 A Report by the EUROFRAME group of Research Institutes for the European Parliament The Institutes involved are Wifo in Austria,

Keeping you informed matters

Keeping you informed matters Annual Investment Review January 2018 matters Page 2 of 12 Outlook Economic growth in the US and emerging economies is leading the way, with global growth falling in line.

Keeping you informed matters Annual Investment Review January 2018 matters Page 2 of 12 Outlook Economic growth in the US and emerging economies is leading the way, with global growth falling in line.

THE REAL ESTATE SECTOR AND THE FINANCIAL CRISIS: THE SPANISH EXPERIENCE

THE REAL ESTATE SECTOR AND THE FINANCIAL CRISIS: THE SPANISH EXPERIENCE Eloísa Ortega Director, Economic Analysis and Forecasting Department CONFERENCE ON EUROPEAN ECONOMIC INTEGRATION CEEI 2013 Vienna

THE REAL ESTATE SECTOR AND THE FINANCIAL CRISIS: THE SPANISH EXPERIENCE Eloísa Ortega Director, Economic Analysis and Forecasting Department CONFERENCE ON EUROPEAN ECONOMIC INTEGRATION CEEI 2013 Vienna

Macroeconomic Policies in Europe: Quo Vadis A Comment

Macroeconomic Policies in Europe: Quo Vadis A Comment February 12, 2016 Helene Schuberth Outline Staff Projection of the Euro Area Monetary Policy Investment Rebalancing in the euro area Fiscal Policy

Macroeconomic Policies in Europe: Quo Vadis A Comment February 12, 2016 Helene Schuberth Outline Staff Projection of the Euro Area Monetary Policy Investment Rebalancing in the euro area Fiscal Policy

Quarterly Spanish National Accounts. Base 2000

May 19 2010 Quarterly Spanish National Accounts. Base 2000 First quarter of 2010 Quarterly National Accounts (GDP) Latest data Year-on-year growth rate Quarter-on-quarter growth rate First quarter of 2010-1.3

May 19 2010 Quarterly Spanish National Accounts. Base 2000 First quarter of 2010 Quarterly National Accounts (GDP) Latest data Year-on-year growth rate Quarter-on-quarter growth rate First quarter of 2010-1.3

L-6 The Fiscal Multiplier debate and the eurozone response to the crisis. Carlos San Juan Mesonada Jean Monnet Professor University Carlos III Madrid

L-6 The Fiscal Multiplier debate and the eurozone response to the crisis Carlos San Juan Mesonada Jean Monnet Professor University Carlos III Madrid The Fiscal Multiplier debate and the eurozone response

L-6 The Fiscal Multiplier debate and the eurozone response to the crisis Carlos San Juan Mesonada Jean Monnet Professor University Carlos III Madrid The Fiscal Multiplier debate and the eurozone response

APPENDIX: Country analyses

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

Nicolaie Alexandru-Chidesciuc, CFA, PhD

, CFA, PhD Associate professor Romanian-American University Vice-president AAFBR Board member CFA Romania Bucharest, April 2011 1 Summary I. Some background II. Euro area imbalances III. Lessons IV. Conclusions

, CFA, PhD Associate professor Romanian-American University Vice-president AAFBR Board member CFA Romania Bucharest, April 2011 1 Summary I. Some background II. Euro area imbalances III. Lessons IV. Conclusions

Economic Policy Statement of Eesti Pank 12 December 2012

Economic Policy Statement of Eesti Pank 12 December 2012 Key points of the presentation The external environment The Estonian economy until now and in the next few years Economic policy implications 12

Economic Policy Statement of Eesti Pank 12 December 2012 Key points of the presentation The external environment The Estonian economy until now and in the next few years Economic policy implications 12

Review of European Economic Governance (ETUC position)

") Review of European Economic Governance (ETUC position) Adopted at the ETUC Executive Committee on 2-3 December 2014 The European Commission will review the framework of European economic governance in

Review of European Economic Governance (ETUC position) Adopted at the ETUC Executive Committee on 2-3 December 2014 The European Commission will review the framework of European economic governance in

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

Europe in the World Economy: Economic Recovery and Europe 2020

Europe in the World Economy: Economic Recovery and Europe 2020 Rafael Doménech Economic recovery and Europe 2020: Towards smart, sustainable and inclusive growth Wilton Park, October 24, 2012 Main messages

Europe in the World Economy: Economic Recovery and Europe 2020 Rafael Doménech Economic recovery and Europe 2020: Towards smart, sustainable and inclusive growth Wilton Park, October 24, 2012 Main messages

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

A Strategy for Growth in the EU How to Boost the Economic Recovery?

A Strategy for Growth in the EU How to Boost the Economic Recovery? EU Commission and Konrad Adenauer Stiftung Berlin, November 19, 01 Lorenzo Codogno Director General, Italian Ministry of Economy and

A Strategy for Growth in the EU How to Boost the Economic Recovery? EU Commission and Konrad Adenauer Stiftung Berlin, November 19, 01 Lorenzo Codogno Director General, Italian Ministry of Economy and

Public Debt and Fiscal Rules

Public Debt and Fiscal Rules Financial Stability Seminar Madrid, April, 1 Fritz Zurbrügg Director, Federal Finance Administration Deficit International debt crisis Public Deficit and Debt In percent of

Public Debt and Fiscal Rules Financial Stability Seminar Madrid, April, 1 Fritz Zurbrügg Director, Federal Finance Administration Deficit International debt crisis Public Deficit and Debt In percent of

CONDITIONAL EUROBONDS AND EUROZONE REFORM

CONDITIONAL EUROBONDS AND EUROZONE REFORM John Muellbauer, INET at Oxford OENB workshop Towards a genuine economic and monetary union, Vienna, 10-11 September, 2015 OBJECTIVES Reduce the Euro-area policy

CONDITIONAL EUROBONDS AND EUROZONE REFORM John Muellbauer, INET at Oxford OENB workshop Towards a genuine economic and monetary union, Vienna, 10-11 September, 2015 OBJECTIVES Reduce the Euro-area policy

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

STABILITY PROGRAMME UPDATE KINGDOM OF SPAIN

STABILITY PROGRAMME UPDATE KINGDOM OF SPAIN 2017-2020 e-nipo 057-17-061-9 TABLE OF CONTENTS 1. EXECUTIVE SUMMARY... 5 2. INTRODUCTION... 7 3. MACROECONOMIC OUTLOOK... 10 3.1. Recent evolution of the Spanish

STABILITY PROGRAMME UPDATE KINGDOM OF SPAIN 2017-2020 e-nipo 057-17-061-9 TABLE OF CONTENTS 1. EXECUTIVE SUMMARY... 5 2. INTRODUCTION... 7 3. MACROECONOMIC OUTLOOK... 10 3.1. Recent evolution of the Spanish

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

Crisis and cooperative solutions: the euro area since 2008

Crisis and cooperative solutions: the euro area since 2008 Jérôme Creel ESCP Europe, Labex Refi & Sciences Po, OFCE [special issue of Réalités Industrielles, August 2018] Abstract: Since the European integration

Crisis and cooperative solutions: the euro area since 2008 Jérôme Creel ESCP Europe, Labex Refi & Sciences Po, OFCE [special issue of Réalités Industrielles, August 2018] Abstract: Since the European integration

Croatia and the European Union: an Opportunity, not a Guarantee

and the European Union: an Opportunity, not a Guarantee Europe has invented a Convergence Machine. Much as the United States takes in poor people and transforms them into high income households, the EU

and the European Union: an Opportunity, not a Guarantee Europe has invented a Convergence Machine. Much as the United States takes in poor people and transforms them into high income households, the EU

Economics Essay Sample

Critically assess the main challenges facing the EU in 2013 and its capacity to meet them, with particular reference either to enlargement or to further integration. Introduction This brief essay aims

Critically assess the main challenges facing the EU in 2013 and its capacity to meet them, with particular reference either to enlargement or to further integration. Introduction This brief essay aims

Spring 2013 forecast: The EU economy slowly recovering from a protracted recession

EUROPEAN COMMISSION PRESS RELEASE Brussels, 3 May 2013 Spring 2013 forecast: The EU economy slowly recovering from a protracted recession Following the recession that marked 2012, the EU economy is expected

EUROPEAN COMMISSION PRESS RELEASE Brussels, 3 May 2013 Spring 2013 forecast: The EU economy slowly recovering from a protracted recession Following the recession that marked 2012, the EU economy is expected

Recovery in Europe The outcome of successful crisis policies?

Recovery in Europe The outcome of successful crisis policies? Discussion Catherine Mathieu, OFCE, Paris EUROPE AFTER THE CRISIS: WHERE IS THE ECONOMIC AND MONETARY UNION HEADED? Berlin, 12 June 2018 observatoire

Recovery in Europe The outcome of successful crisis policies? Discussion Catherine Mathieu, OFCE, Paris EUROPE AFTER THE CRISIS: WHERE IS THE ECONOMIC AND MONETARY UNION HEADED? Berlin, 12 June 2018 observatoire

Svein Gjedrem: Inflation targeting in an oil economy

Svein Gjedrem: Inflation targeting in an oil economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebanken Møre, Ålesund, 4 June 2002. Please note that the text

Svein Gjedrem: Inflation targeting in an oil economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebanken Møre, Ålesund, 4 June 2002. Please note that the text

STAT/12/ October Household saving rate fell in the euro area and remained stable in the EU27. Household saving rate (seasonally adjusted)

") STAT/12/152 30 October 2012 Quarterly Sector Accounts: second quarter of 2012 Household saving rate down to 12.9% in the euro area and stable at 11. in the EU27 Household real income per capita fell by

STAT/12/152 30 October 2012 Quarterly Sector Accounts: second quarter of 2012 Household saving rate down to 12.9% in the euro area and stable at 11. in the EU27 Household real income per capita fell by

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

34 th Associates Meeting - Andorra, 25 May Item 5: Evolution of economic governance in the EU

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Will the Troika Adjustment Program of Internal Devaluation Work? Dr. Aidan Regan Blog: Euro-Irish Public Policy

The Origins and Impact of the Eurozone Crisis Will the Troika Adjustment Program of Internal Devaluation Work? Dr. Aidan Regan Blog: Euro-Irish Public Policy Outline Introduction The Origins of the Eurozone

The Origins and Impact of the Eurozone Crisis Will the Troika Adjustment Program of Internal Devaluation Work? Dr. Aidan Regan Blog: Euro-Irish Public Policy Outline Introduction The Origins of the Eurozone

Managing Social Imbalances: competitiveness at the price of more working poverty?

Managing Social Imbalances: competitiveness at the price of more working poverty? Bea Cantillon Herman Deleeck Centre for Social Policy, University of Antwerp London, 17 April 2012 B.Cantillon, F. Vandenbroucke,

Managing Social Imbalances: competitiveness at the price of more working poverty? Bea Cantillon Herman Deleeck Centre for Social Policy, University of Antwerp London, 17 April 2012 B.Cantillon, F. Vandenbroucke,

Impact of the Great Recession and the Role of Assistance Programmes in EMU Countries

UNIVERSIDADE DE TRÁS-OS-MONTES E ALTO DOURO Impact of the Great Recession and the Role of Assistance Programmes in EMU Countries Leonida Correia and Patrícia Martins Centre for Transdisciplinary Development

UNIVERSIDADE DE TRÁS-OS-MONTES E ALTO DOURO Impact of the Great Recession and the Role of Assistance Programmes in EMU Countries Leonida Correia and Patrícia Martins Centre for Transdisciplinary Development

University of Leipzig Institute for Economic Policy

University of Leipzig Institute for Economic Policy Prof. Dr. Gunther Schnabl Experiences with the Current EU Economic Governance Framework European Parliament Committee on Economic and Monetary Affairs

University of Leipzig Institute for Economic Policy Prof. Dr. Gunther Schnabl Experiences with the Current EU Economic Governance Framework European Parliament Committee on Economic and Monetary Affairs

Lecture 7: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 7: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 EMU Economic and Monetary Union An old idea in the European Union 1989: Delors report 1991: Maastricht treaty 1997: Stability pact Eleven

Lecture 7: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 EMU Economic and Monetary Union An old idea in the European Union 1989: Delors report 1991: Maastricht treaty 1997: Stability pact Eleven

Italy: fundamentals are the compass amid political twists

Italy: fundamentals are the compass amid political twists Eric Brard Head of Fixed Income Annalisa USARDI, CFA Senior Economist With the contribution of: Giuseppina Marinotti Investment Insights Unit The

Italy: fundamentals are the compass amid political twists Eric Brard Head of Fixed Income Annalisa USARDI, CFA Senior Economist With the contribution of: Giuseppina Marinotti Investment Insights Unit The

Study Questions. Lecture 15 International Macroeconomics

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Fiscal Policy, Budget Deficits and the Economic Crisis. Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010

Fiscal Policy, Budget Deficits and the Economic Crisis Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010 Three lines of defence against the economic crisis 1. Measures to deal with the

Fiscal Policy, Budget Deficits and the Economic Crisis Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010 Three lines of defence against the economic crisis 1. Measures to deal with the

Intermediate Macroeconomics, 7.5 ECTS

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

The future of the euro zone

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

Study Questions (with Answers) Lecture 15 International Macroeconomics

Lecture 15 International Macroeconomics") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

The Stability and Growth Pact Status in 2001

4 The Stability and Growth Pact Status in 200 Tina Winther Frandsen, International Relations INTRODUCTION The EU member states' public finances showed remarkable development during the 990s. In 993, the

4 The Stability and Growth Pact Status in 200 Tina Winther Frandsen, International Relations INTRODUCTION The EU member states' public finances showed remarkable development during the 990s. In 993, the

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

Economic and Financial Affairs Committee. The EMU: challenges and the way forward

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

remain the same until the end of 2018.

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

Macroeconomic Imbalances in the Euro Area: Symptom or cause of the crisis?

Macroeconomic Imbalances in the Euro Area: Symptom or cause of the crisis? Daniel Gros No. 266, April 2012 Abstract. Lax financial conditions can foster credit booms. The global credit boom of the last

Macroeconomic Imbalances in the Euro Area: Symptom or cause of the crisis? Daniel Gros No. 266, April 2012 Abstract. Lax financial conditions can foster credit booms. The global credit boom of the last

The Euro. J. E. Stiglitz Tsinghua University Beijing, China March 21 st 2018

The Euro J. E. Stiglitz Tsinghua University Beijing, China March 21 st 2018 The Euro-crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro-crisis

The Euro J. E. Stiglitz Tsinghua University Beijing, China March 21 st 2018 The Euro-crisis The fact that Europe is no longer in decline is not a sign that the austerity policies worked or that the euro-crisis

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Can the euro still be saved? Morning session: the threats

Can the euro still be saved? Morning session: the threats Anton Brender and Florence Pisani Berlin, June 17 1 Fiscal and monetary policies: some problems have not yet been fully fixed! Budget balance Budget

Can the euro still be saved? Morning session: the threats Anton Brender and Florence Pisani Berlin, June 17 1 Fiscal and monetary policies: some problems have not yet been fully fixed! Budget balance Budget

SCOTLAND S ECONOMIC FUTURE POST-2014 SUBMISSION FROM PROFESSOR ANTON MUSCATELLI

SCOTLAND S ECONOMIC FUTURE POST-2014 SUBMISSION FROM PROFESSOR ANTON MUSCATELLI Introduction I thank the Committee for the invitation to appear in connection with this inquiry. I would like to point out

SCOTLAND S ECONOMIC FUTURE POST-2014 SUBMISSION FROM PROFESSOR ANTON MUSCATELLI Introduction I thank the Committee for the invitation to appear in connection with this inquiry. I would like to point out

Progress Towards Strong, Sustainable, and Balanced Growth. Figure 1: Recovery From Financial Crisis (100 = First Quarter of Real GDP contraction)

") Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

The Brussels Economic Forum

The Brussels Economic Forum What kind of policies should the new Member States apply to optimise their speed of convergence? Banco de Portugal VÍTOR CONSTÂNCIO Brussels, 23d of April 24 I. INTRODUCTION

The Brussels Economic Forum What kind of policies should the new Member States apply to optimise their speed of convergence? Banco de Portugal VÍTOR CONSTÂNCIO Brussels, 23d of April 24 I. INTRODUCTION

The European Economic Crisis

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

ANNEX 1 CMES: TRADE INDICATORS FOR FIVE MOST IMPORTANT EXPORT SECTORS

ANNEX 1 CMES: TRADE INDICATORS FOR FIVE MOST IMPORTANT EXPORT SECTORS AND VEHICLES (87), MACHINERY (84) AND ELECTRONIC PRODUCTS (85) Germany Austria The Editor(s) (if applicable) and The Author(s) 2016

ANNEX 1 CMES: TRADE INDICATORS FOR FIVE MOST IMPORTANT EXPORT SECTORS AND VEHICLES (87), MACHINERY (84) AND ELECTRONIC PRODUCTS (85) Germany Austria The Editor(s) (if applicable) and The Author(s) 2016

Lecture 1: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 1: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics 1. The relationship between savings, investment and real interest rates in a closed economy (the world economy) 2. The relationship

Lecture 1: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics 1. The relationship between savings, investment and real interest rates in a closed economy (the world economy) 2. The relationship

DBRS Confirms Republic of Portugal s Rating at BBB (low), Stable Trend

, Stable Trend") Date of Release: November 21, 2014 DBRS Confirms Republic of Portugal s at BBB (low), Stable Trend Industry: Public Finance--Sovereigns DBRS s Limited (DBRS) has confirmed the Republic of Portugal s long-term

Date of Release: November 21, 2014 DBRS Confirms Republic of Portugal s at BBB (low), Stable Trend Industry: Public Finance--Sovereigns DBRS s Limited (DBRS) has confirmed the Republic of Portugal s long-term

The Macroeconomics of Financial Integration: A European Per

The Macroeconomics of Financial Integration: A European Perspective Prepared for the DG ECFIN Annual Research Conference Philip R. Lane Trinity College Dublin October 2008 Introduction European experience

The Macroeconomics of Financial Integration: A European Perspective Prepared for the DG ECFIN Annual Research Conference Philip R. Lane Trinity College Dublin October 2008 Introduction European experience

Suggested answers to Problem Set 5

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

Structural Changes in the Maltese Economy

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS Summary Spain has significantly increased its trade openness in the last two decades Despite the global crisis and increased competition from

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS Summary Spain has significantly increased its trade openness in the last two decades Despite the global crisis and increased competition from

Structural changes in the Maltese economy

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the