Svein Gjedrem: Inflation targeting in an oil economy

|

|

|

- Alyson Benson

- 5 years ago

- Views:

Transcription

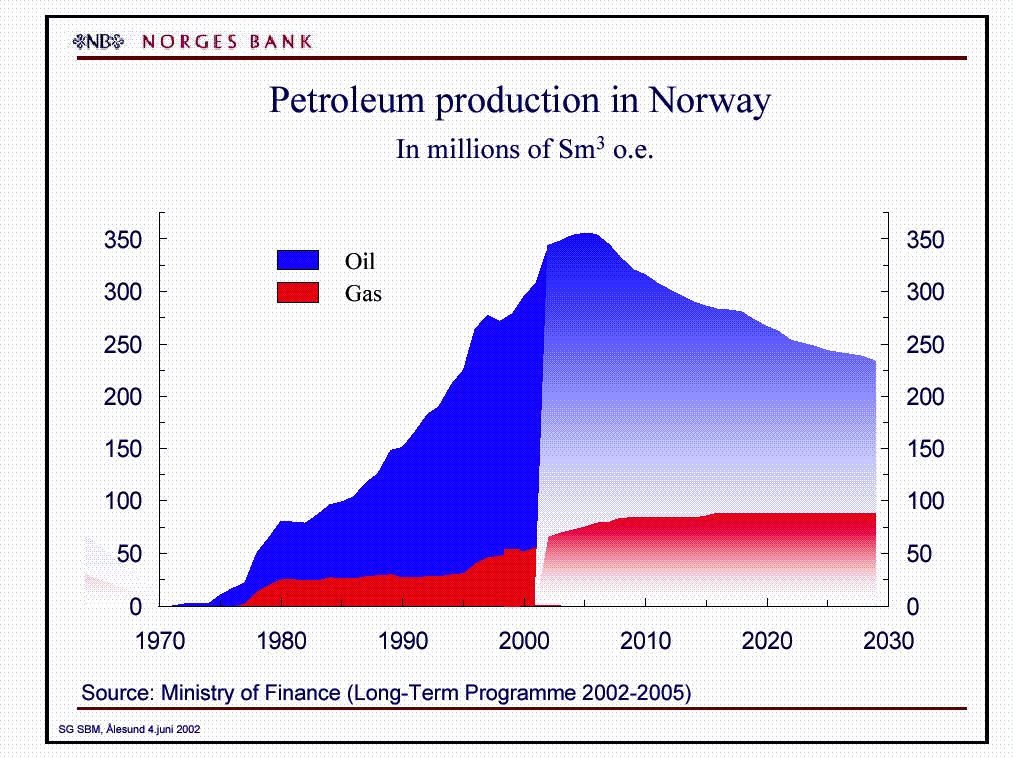

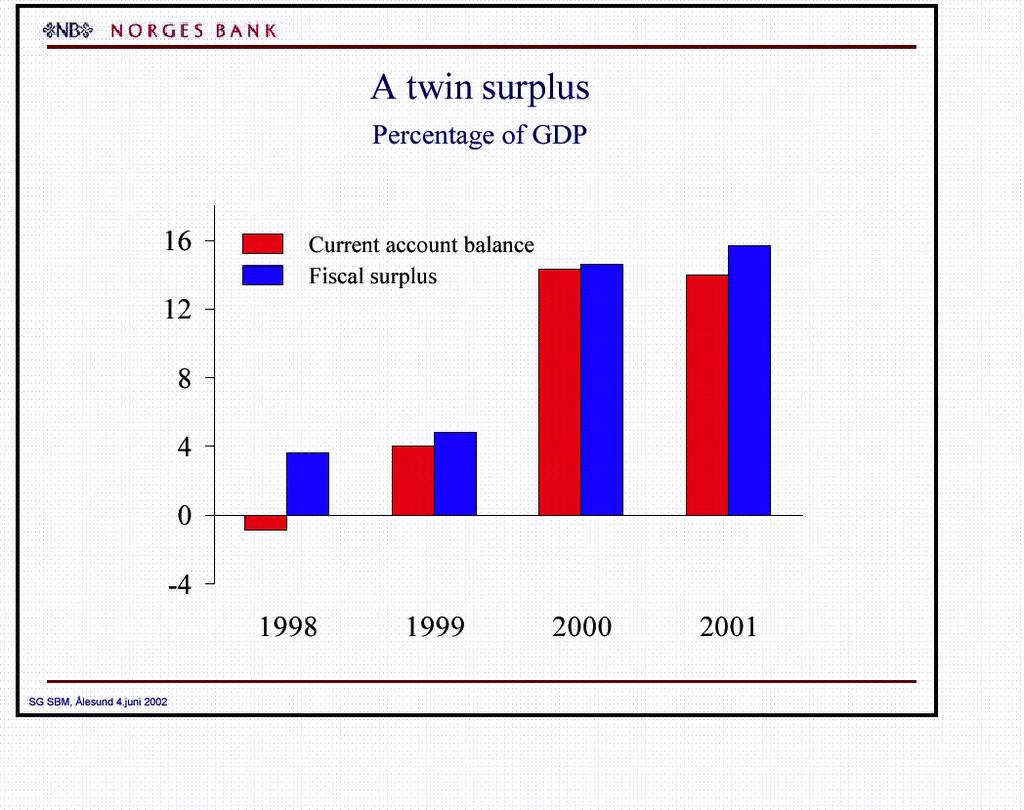

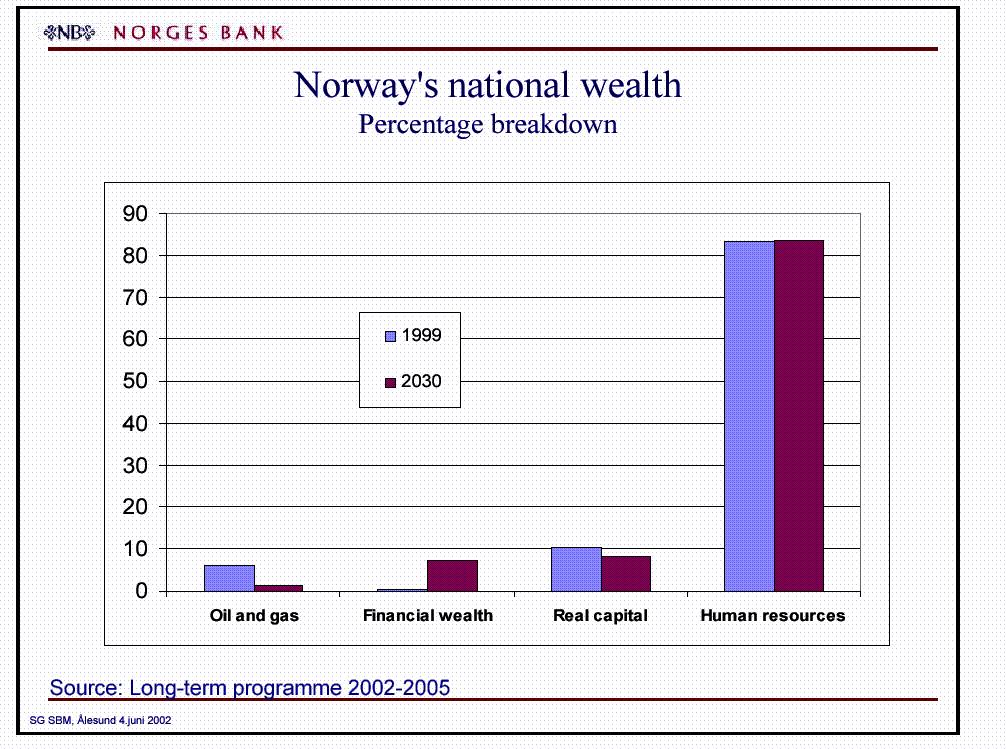

1 Svein Gjedrem: Inflation targeting in an oil economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebanken Møre, Ålesund, 4 June Please note that the text below may differ slightly from the actual presentation. * * * Norway is unique in being both a fully developed economy and a major oil exporter. Last year, Norway was the world s third largest exporter of oil. In the future, we will become an increasingly important exporter of natural gas. The present value of remaining petroleum reserves has been estimated at NOK 2 200bn, or roughly 1½ times our current GDP. The bulk of Norway s petroleum wealth will be extracted over a period of 40 years, from 1990 to New technology has had a significant impact on our future production potential. In spite of rapid production growth, the estimated present value of our petroleum wealth has increased some per cent over the last ten years, measured in real terms. As an example, the registered oil reserves in the Ekofisk field are larger today than when the field started production 30 years ago. Revenues from the petroleum sector have generated a fiscal surplus of some per cent since A similar surplus is generated on the current account, reflecting capital outflows to the Government Petroleum Fund. Even in 1998, when the oil price fell to 10 USD/barrel, Norway had a fiscal surplus of some 4 per cent of GDP. The existence of abundant natural resources can be a mixed blessing. Experience elsewhere suggests that the sudden occurrence of major income flows tends to undermine future production potential. In the long term, it is difficult to ensure an efficient distribution of wealth between and within generations without triggering rent-seeking behaviour among households and firms. In the short term, the volatility in income flows and in terms of trade poses a challenge for monetary and fiscal policy. The mixed blessing of national wealth is not a new problem. Vigilant observers were already aware of this in the 17th century. In modern economic language, the Moroccan ambassador to Spain pointed to the problem of deteriorating competitiveness 300 years ago (see Chart 2). The main long-term challenge to economic policy is how the returns on petroleum wealth can be phased into the economy without a deterioration of our future growth potential. Even with our substantial petroleum reserves, human capital is by far our most important resource. It accounts for over 80 per cent of Norway s national wealth (present value of future labour). Income from oil and gas is transferred to financial assets through the government budget. These transfers are large in terms of GDP, but still minor compared with our human capital. Oil and gas reserves account for about 7 percent of national wealth today, whereas in 2030 these reserves will be reduced to only 1-2 per cent. To meet these challenges, the Norwegian Government Petroleum Fund was established on 22 June Its main objective is to manage assets and distribute wealth between generations. It also serves as a buffer against shocks: changes in petroleum revenues are absorbed by the Fund, not by the domestic economy. This reduces the need for structural adjustments and thus promotes exchange rate stability. The Fund invests only in foreign markets. Investments are spread between equities and fixed income instruments, as well as across countries. The net annual inflow to the Fund equals the net fiscal surplus plus the return on the Fund s capital. In March 2001, a broad majority in the Norwegian parliament (the Storting) adopted a new set of guidelines for fiscal and monetary policy. According to the new guideline for fiscal policy, petroleum revenues are to be phased in approximately in pace with the expected real return on the Government Petroleum Fund.

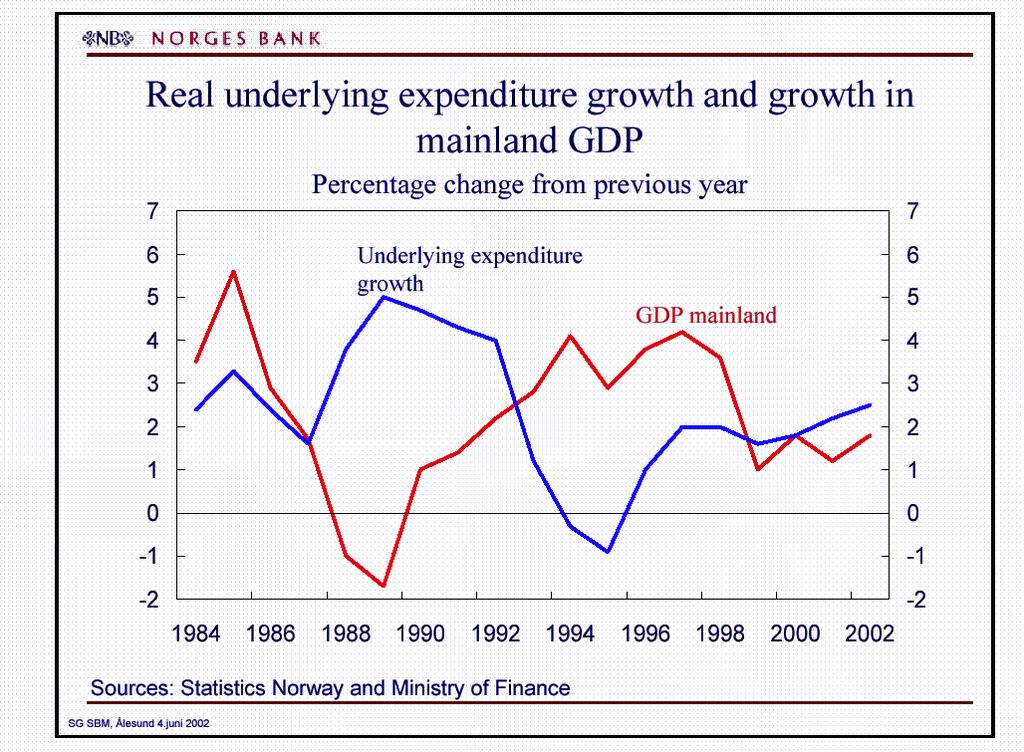

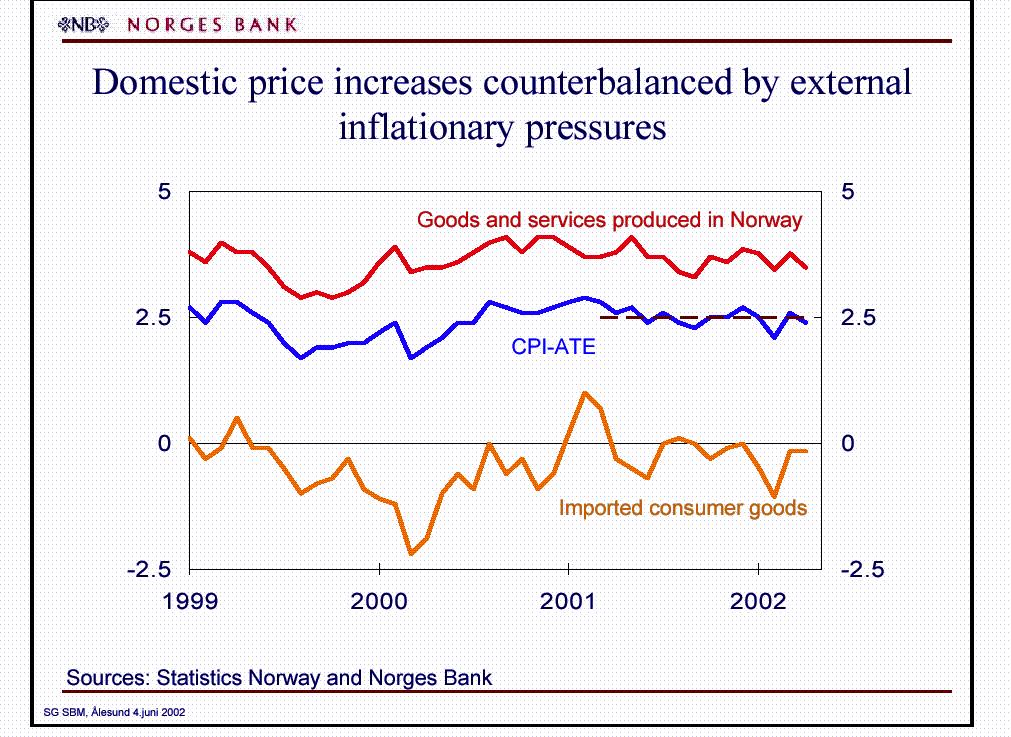

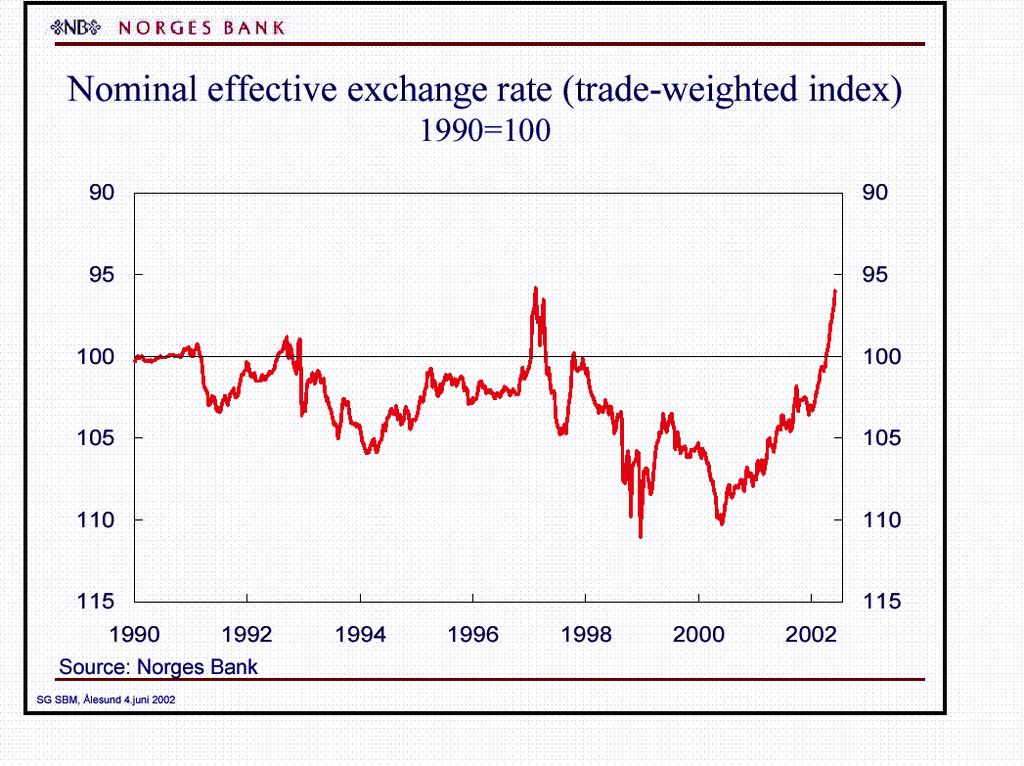

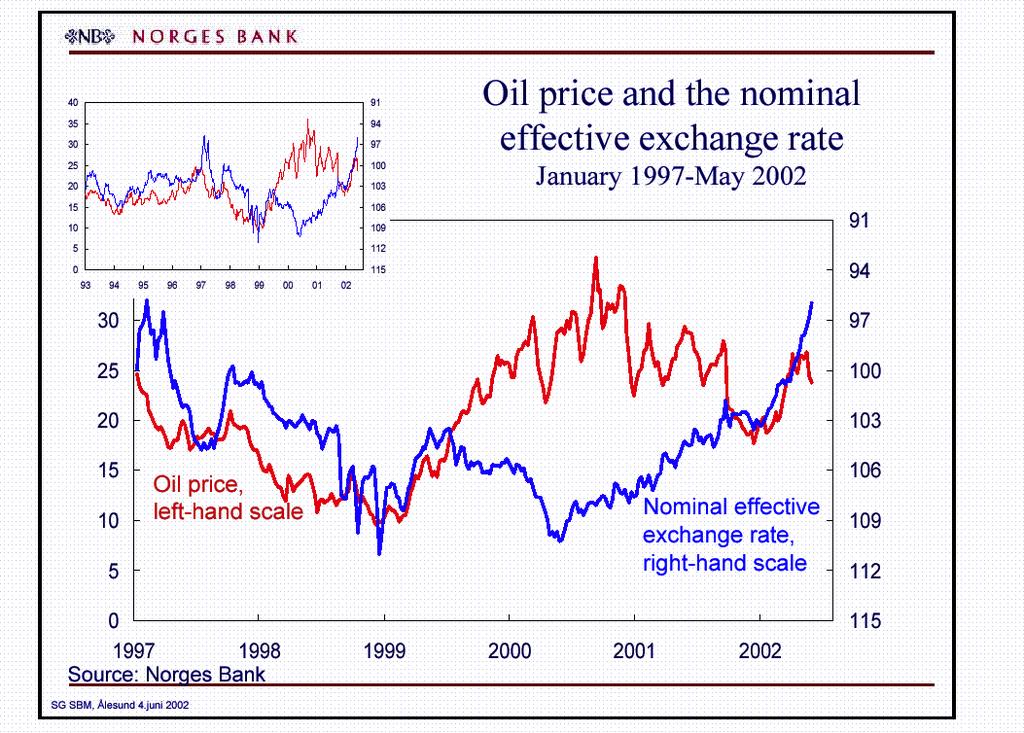

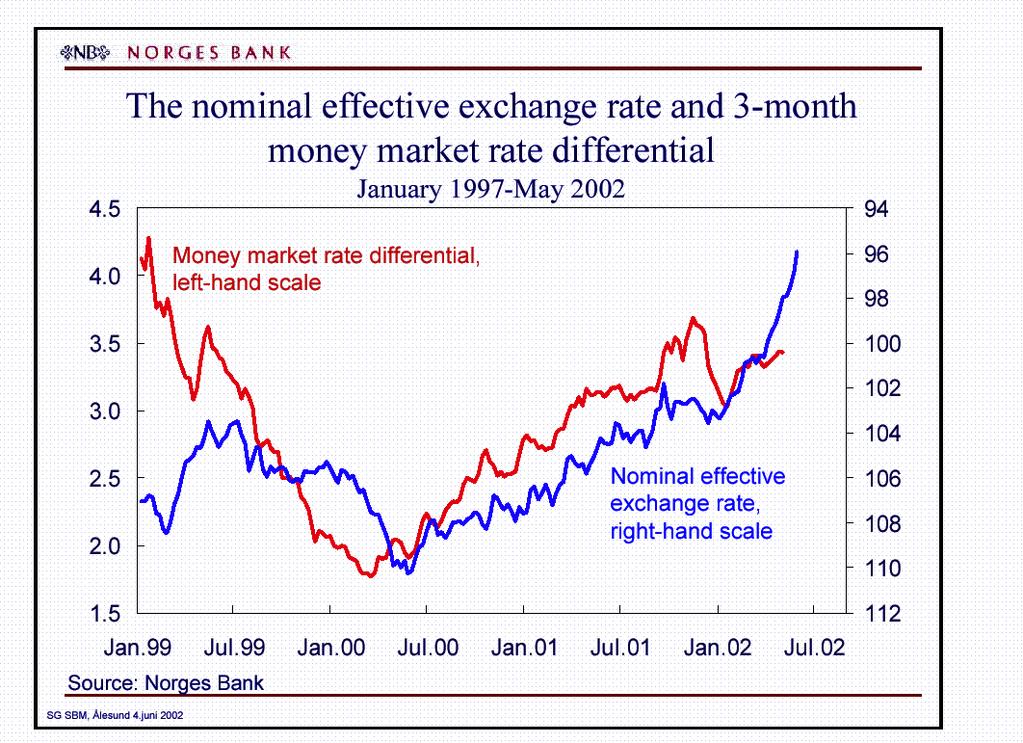

2 The guideline makes fiscal policy predictable and anchors it in a long-term strategy. It also makes policy robust to changes in oil prices and ensures that petroleum wealth will be of benefit both today and in the future. The guidelines imply that the structural non-oil budget deficit will equal 4 per cent of the total value of the Fund. The non-oil deficit is thus financed by the return on the Fund, ensuring both long-term fiscal balance and a continued phasing in of petroleum revenues. The use of petroleum revenues will accordingly increase as long as the Petroleum Fund is expanding. Fiscal policy will contribute to stimulating aggregate demand in the Norwegian economy every year. This annual expansionary fiscal impact poses a challenge to stabilisation policy in general and monetary policy in particular. Underlying real expenditure growth has exceeded mainland GDP for the last 4 years. Nominal growth in 2002 is 7 per cent. (The deflator, mainly wages, is 4½ per cent). Measured as a share of GDP, public expenditure is growing rapidly. In 2002 alone, this share will increase by some 2½ percentage points. According to the Revised National Budget, an increase in expenditure of 7 per cent this year will lead to an estimated growth in public sector consumption of only 1½ per cent. The rest will be spent on government transfers and wage growth. This is consistent with close adherence to the new fiscal guidelines. The new guidelines for fiscal and monetary policy were introduced simultaneously, and are not independent of each other. Fiscal policy is geared towards the phasing in of oil revenues; monetary policy has been given a more explicit responsibility for macroeconomic stabilisation. Monetary policy is to be oriented towards low and stable inflation. The inflation target is set at 2½ per cent. Monetary policy affects the economy with considerable and variable lags. The key rate is set on the basis of an overall assessment of the inflation outlook two years ahead. If it appears that inflation will be higher than 2½ per cent with unchanged interest rates, the interest rate will be increased. If it appears that inflation will be lower than 2½ per cent with unchanged interest rates, the interest rate will be reduced. It is just as important to avoid an inflation rate that is too low as it is to avoid an inflation rate that is too high. Up to March 2001, the Bank pursued exchange rate stability against European currencies. Implicitly, this meant that inflation in Norway had to be kept at the target for the euro area. From 1999 onwards, the ECB s target was defined as an inflation rate below 2 per cent. Since the introduction of an inflation target, the underlying inflation rate has been around 2½ per cent. The rate of increase in the headline CPI has shown somewhat wider variations, but averaged 2¼ per cent in the 1990s. The use of oil revenues must be counteracted by a tight monetary policy. A tight monetary policy implies relatively high interest rates, a strong krone, or both. As fiscal policy creates demand for resources in public services and other sheltered sectors, industries exposed to foreign competition may be faced with difficulties finding labour and higher labour costs. The contest for resources is likely to lead to a real appreciation of the krone and a deterioration of competitiveness in our exposed sectors. The krone exchange rate has appreciated as a result of a wider interest rate differential between Norway and other countries. Combined with low growth abroad and increased trade with low-cost countries such as China, this has led to a fall in import prices. The relatively high price increases of Norwegian products reflect high wage growth and a tight labour market. The krone exchange rate, measured against the trade-weighted index, has appreciated around 13 per cent in the last two years. However, the krone was exceptionally weak in mid The krone is 4-5 per cent stronger today than in the early 1990s, and about as strong as the previous high in early Thus, the recent strong showing of the krone is not without precedent. Changes in the oil price have time and again been an important factor behind exchange rate movements. Empirical evidence shows that the exchange rate is affected mainly by large fluctuations in the oil price. The krone tends to depreciate if the oil price is very low, as happened during the Russian crisis in On the other hand, the krone did not appreciate accordingly when the oil price surged from 1999 onwards. Hence, the relationship between the oil price and the exchange rate has not been evident for the last two years. Since late 2001, however, our currency may have been used as a hedge against the upside risk to the oil price, and this may have contributed to its appreciation.

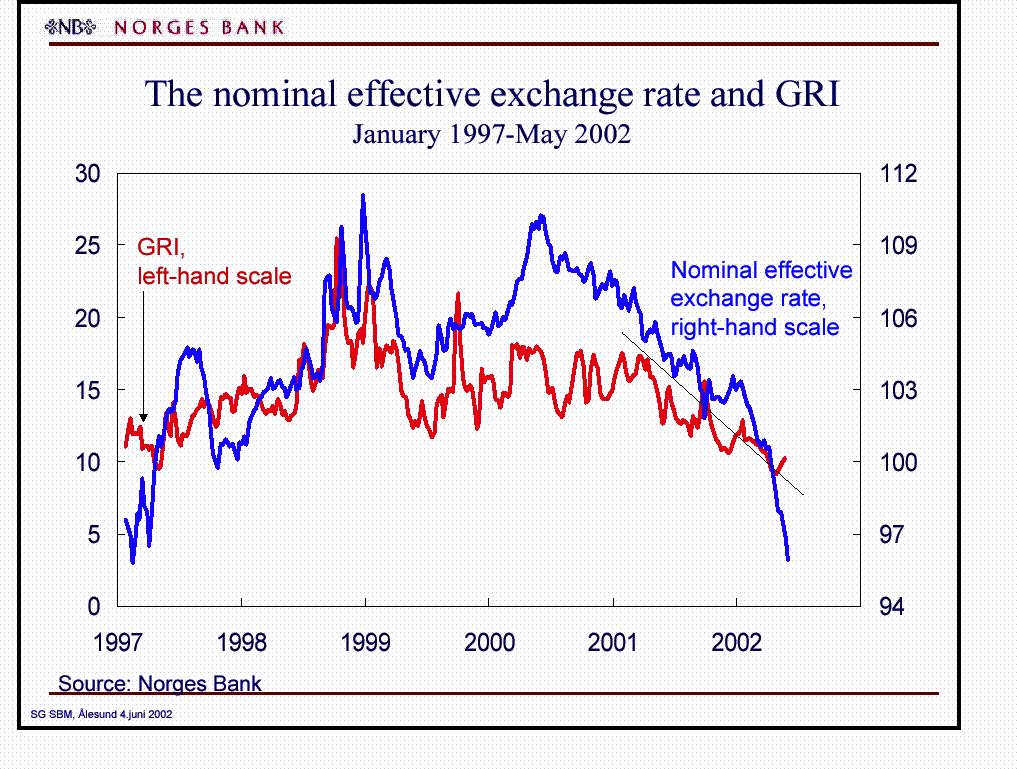

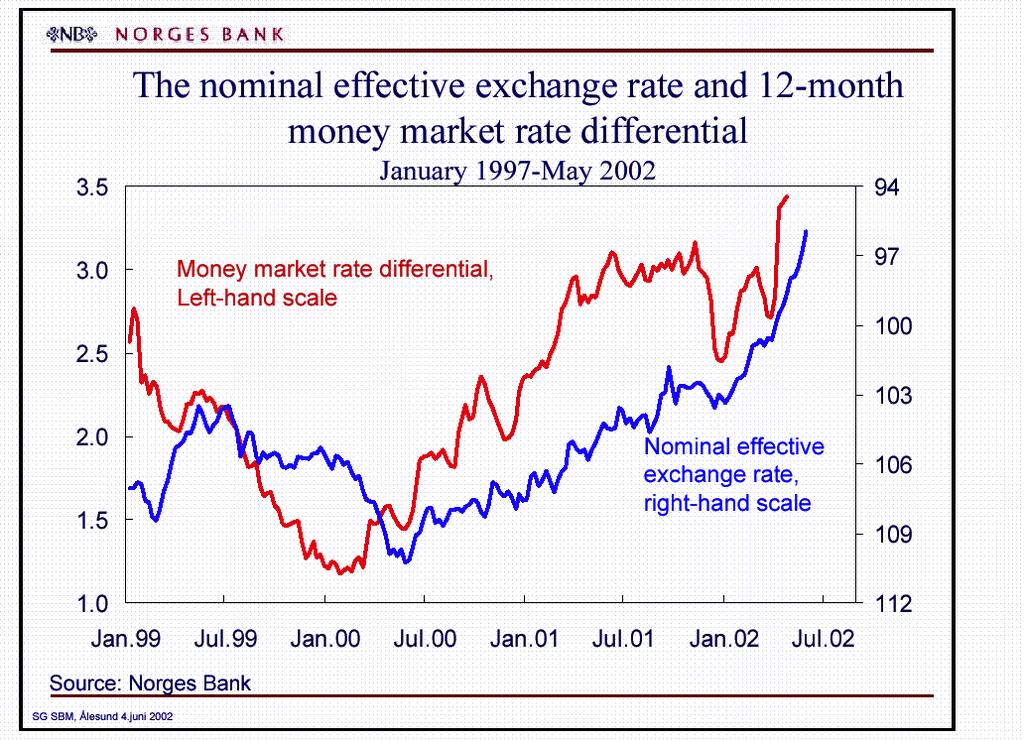

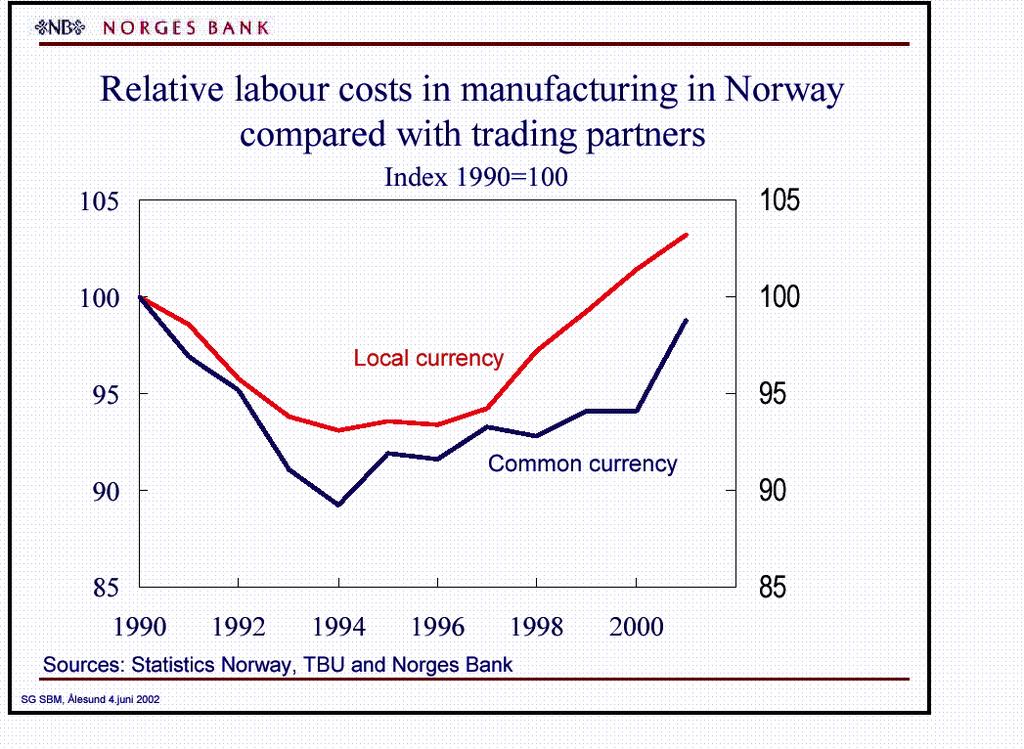

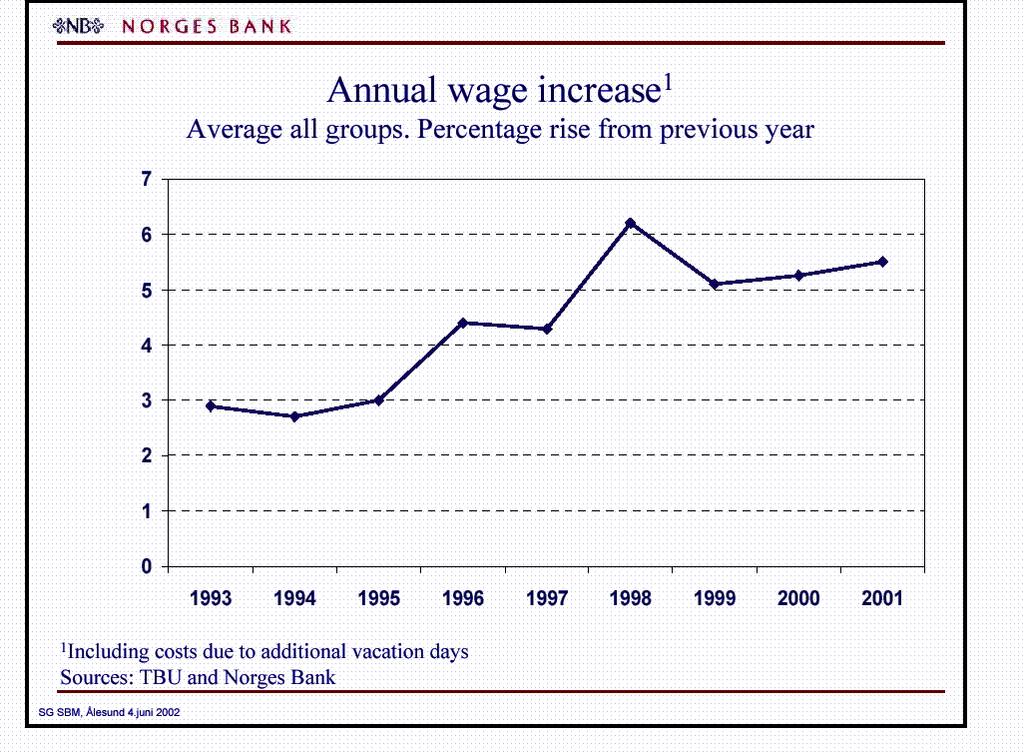

3 Another factor behind the appreciation of the krone is the current low risk premium in global currency markets (measured by a global risk index, GRI). Since the beginning of this year, lower risk premiums have accompanied a stronger krone. Developments in the GRI were also an important factor during the Russian crisis in When global risk premiums and interest rates are low, investors may turn to higher-yield currencies. There is also a tendency for more peripheral currencies to attract increased attention when volatility between the major global currencies is subdued and risk premiums are low. The interest rate differential has been an important explanation for the movements in the krone exchange rate, at least since the summer of A higher interest rate differential has accompanied a stronger krone. The krone has appreciated significantly since the beginning of this year, however, and apparently somewhat more than what can be explained by the interest rate differential alone. One explanation may be that market participants react to signs of pressure in the economy by adjusting their interest rate expectations in the longer term. This has an impact on longer-term interest rates. Thus, movements in the exchange rate may be a result of changes in forward rates, as well as current interest rates. Since early January, the 12-month money market differential appears to have followed the krone exchange rate more closely than the 3-month differential. The pressure on internal resources seems to have resulted in expectations of tight monetary conditions, which contributed to the recent appreciation of the krone. The nominal appreciation of the krone has been accompanied by a significant real appreciation of Norwegian labour. Measured in local labour costs, cost competitiveness has been deteriorating since For a time, profits in the exposed sector were not affected by the increase in labour costs, as the krone depreciated. However, this depreciation could not last, as it would have ignited domestic inflationary pressures. Tight labour market conditions warrant a relatively tight monetary policy. Norwegian interest rates are not very high, however, when our wage growth is compared with that of other countries. On the contrary, the recent appreciation of the krone will have a cushioning effect on inflation and thus on interest rates. Since 1998, the increase in labour costs has been between 5 and 7 per cent. This year s wage negotiations were no exception. It now seems evident that wage growth will be significantly higher than our previous estimate of 5 per cent this year. The carry-over to next year is also substantial, especially in retail trade and the public sector. It is evident from this year s wage negotiations that our labour market is tight. Norges Bank kept interest rates unchanged at the Executive Board meeting on Wednesday, 22 May. The Bank changed its stance on future inflation risks. The main reason was the higher-than-projected wage increases. According to the Bank s assessment of the risks associated with the inflation outlook, the appreciation of the krone cannot fully counteract stronger wage growth, faster growth in consumption, a higher oil price and a somewhat more favourable global economic outlook.

4

5

6

7

8

9

Svein Gjedrem: The conduct of monetary policy

Svein Gjedrem: The conduct of monetary policy Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee on Finance and Economic

Svein Gjedrem: The conduct of monetary policy Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee on Finance and Economic

Jan F Qvigstad: Outlook for the Norwegian economy

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Svein Gjedrem: The outlook for the Norwegian economy

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce

Øystein Olsen: The economic outlook

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based

Svein Gjedrem: Monetary policy and aspects of economic developments

Svein Gjedrem: Monetary policy and aspects of economic developments Speech by Mr Svein Gjedrem, Governor of the Central Bank of Norway, Ålesund, 12 October 2005. Please note that the text below may differ

Svein Gjedrem: Monetary policy and aspects of economic developments Speech by Mr Svein Gjedrem, Governor of the Central Bank of Norway, Ålesund, 12 October 2005. Please note that the text below may differ

Svein Gjedrem: Interest rate developments

Svein Gjedrem: Interest rate developments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the annual conference hosted by the Norwegian Federation of State Employees Unions,

Svein Gjedrem: Interest rate developments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the annual conference hosted by the Norwegian Federation of State Employees Unions,

Jarle Bergo: Monetary policy and the cyclical situation

Jarle Bergo: Monetary policy and the cyclical situation Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at a meeting with local authorities and the business community,

Jarle Bergo: Monetary policy and the cyclical situation Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at a meeting with local authorities and the business community,

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at a presentation of the Monetary Policy

Svein Gjedrem: The outlook for the Norwegian economy and monetary policy assessments Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at a presentation of the Monetary Policy

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference Commodities,

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference Commodities,

Svein Gjedrem: Norwegian experiences in balancing economic development with macroeconomic stability - a historical perspective

Svein Gjedrem: Norwegian experiences in balancing economic development with macroeconomic stability - a historical perspective Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway),

Svein Gjedrem: Norwegian experiences in balancing economic development with macroeconomic stability - a historical perspective Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway),

Svein Gjedrem: Monetary policy and the labour market

Svein Gjedrem: Monetary policy and the labour market Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference to mark the 10th anniversary of the Federation of Norwegian

Svein Gjedrem: Monetary policy and the labour market Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference to mark the 10th anniversary of the Federation of Norwegian

Svein Gjedrem: Transatlantic economic partnership - Nordic and American perspectives

Svein Gjedrem: Transatlantic economic partnership - Nordic and American perspectives Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Nordic Investment Bank Economic

Svein Gjedrem: Transatlantic economic partnership - Nordic and American perspectives Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Nordic Investment Bank Economic

Svein Gjedrem: The economic outlook in Norway

Svein Gjedrem: The economic outlook in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 22 March 2007.

Svein Gjedrem: The economic outlook in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 22 March 2007.

Svein Gjedrem: Monetary policy in an open economy

Svein Gjedrem: Monetary policy in an open economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Confederation of Higher Education Unions, Kongsberg, 13 November 2002.

Svein Gjedrem: Monetary policy in an open economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Confederation of Higher Education Unions, Kongsberg, 13 November 2002.

Economic Survey 2/2013. Norwegian economy. Economic trends

Economic trends Economic growth among Norway s trading partners remains very low. Growth in the euro area is at a complete standstill, and unemployment is generally very high and rising. Growth in the

Economic trends Economic growth among Norway s trading partners remains very low. Growth in the euro area is at a complete standstill, and unemployment is generally very high and rising. Growth in the

Mr. Bäckström explains why price stability ought to be a central bank s principle monetary policy objective

Mr. Bäckström explains why price stability ought to be a central bank s principle monetary policy objective Address by the Governor of the Bank of Sweden, Mr. Urban Bäckström, at Handelsbanken seminar

Mr. Bäckström explains why price stability ought to be a central bank s principle monetary policy objective Address by the Governor of the Bank of Sweden, Mr. Urban Bäckström, at Handelsbanken seminar

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

Svein Gjedrem: The economic outlook for Norway

Svein Gjedrem: The economic outlook for Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), for Norges Bank s regional network, Region East, 19 November 2008. Please note

Svein Gjedrem: The economic outlook for Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), for Norges Bank s regional network, Region East, 19 November 2008. Please note

Svein Gjedrem: On business cycles, monetary policy and property markets

Svein Gjedrem: On business cycles, monetary policy and property markets Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Næringseiendom conference, Bergen, 12 May 2006.

Svein Gjedrem: On business cycles, monetary policy and property markets Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Næringseiendom conference, Bergen, 12 May 2006.

Project Link Meeting, New York

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Minutes of the Monetary Policy Committee meeting, August 2016

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

Economic Projections :2

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

2 Macroeconomic Scenario

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

Antonio Fazio: Overview of global economic and financial developments in first half 2004

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Economic Projections :3

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Norwegian economy. Economic trends Economic Survey 3/2001

Economic trends Economic Survey 3/2001 Norwegian economy The fear of a demand-driven increase in inflation has so far induced Norges Bank to maintain high interest rates. Changes in figures from the quarterly

Economic trends Economic Survey 3/2001 Norwegian economy The fear of a demand-driven increase in inflation has so far induced Norges Bank to maintain high interest rates. Changes in figures from the quarterly

Egil Matsen: The equity share in the Government Pension Fund Global

Egil Matsen: The equity share in the Government Pension Fund Global Introductory statement by Mr Egil Matsen, Governor of Norges Bank (Central Bank of Norway), Oslo, 1 December 2016. Accompanying slides

Egil Matsen: The equity share in the Government Pension Fund Global Introductory statement by Mr Egil Matsen, Governor of Norges Bank (Central Bank of Norway), Oslo, 1 December 2016. Accompanying slides

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

MCCI ECONOMIC OUTLOOK. Novembre 2017

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce and Industry,

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce and Industry,

Jarle Bergo: The economic situation, global uncertainty and monetary policy

Jarle Bergo: The economic situation, global uncertainty and monetary policy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at the Annual General Meeting of ACI Norge

Jarle Bergo: The economic situation, global uncertainty and monetary policy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at the Annual General Meeting of ACI Norge

Svein Gjedrem: The role of the Central Bank

Svein Gjedrem: The role of the Central Bank Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Fafo Institute for Labour and Social Research and the Norwegian Power and

Svein Gjedrem: The role of the Central Bank Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Fafo Institute for Labour and Social Research and the Norwegian Power and

Svein Gjedrem: The central bank s instruments

Svein Gjedrem: The central bank s instruments Lecture by Mr Svein Gjedrem, Governor of the Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI Norwegian School of Management,

Svein Gjedrem: The central bank s instruments Lecture by Mr Svein Gjedrem, Governor of the Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI Norwegian School of Management,

New information since the October 2011 Monetary Policy Report (3/11) 1

1") Meeting 14 March 2012 New information since the October 2011 Monetary Policy Report (3/11) 1 International economy According to preliminary figures, GDP for Norway s main trading partners fell by 0.2 percent

Meeting 14 March 2012 New information since the October 2011 Monetary Policy Report (3/11) 1 International economy According to preliminary figures, GDP for Norway s main trading partners fell by 0.2 percent

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 24 May 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank In recent weeks,

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 24 May 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank In recent weeks,

Evaluation of Norges Bank's projections for 2004

Evaluation of Norges Bank's projections for 2004 Per Espen Lilleås, economist in the Economics Department 1 The assessments of capacity utilisation in the Norwegian economy in 2004, measured by estimates

Evaluation of Norges Bank's projections for 2004 Per Espen Lilleås, economist in the Economics Department 1 The assessments of capacity utilisation in the Norwegian economy in 2004, measured by estimates

Outlook for Economic Activity and Prices (April 2010)

") April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

The National Budget 2014

The National Budget 214 The National Budget 214 1 Contents: page 1. Introduction... 2 2. Economic outlook... 2 3. Economic policy... 7 3.1 Fiscal policy... 7 3.2 Tax policy... 16 3.3 Monetary policy...

The National Budget 214 The National Budget 214 1 Contents: page 1. Introduction... 2 2. Economic outlook... 2 3. Economic policy... 7 3.1 Fiscal policy... 7 3.2 Tax policy... 16 3.3 Monetary policy...

Svein Gjedrem: Management of the Government Pension Fund Global

Svein Gjedrem: Management of the Government Pension Fund Global Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee

Svein Gjedrem: Management of the Government Pension Fund Global Introductory statement by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the hearing before the Standing Committee

Economic outlook. Address by Central Bank Governor Svein Gjedrem to invited foreign embassy representatives. Norges Bank 18 March 2004

Economic outlook Address by Central Bank Governor Svein Gjedrem to invited foreign embassy representatives Norges Bank 1 March SG Diplomat 1.. Long-term interest rates Per cent 15 1 9 Norway US Germany

Economic outlook Address by Central Bank Governor Svein Gjedrem to invited foreign embassy representatives Norges Bank 1 March SG Diplomat 1.. Long-term interest rates Per cent 15 1 9 Norway US Germany

Lars Heikensten: The Swedish economy and monetary policy

Lars Heikensten: The Swedish economy and monetary policy Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at a seminar arranged by the Stockholm Chamber of Commerce and Veckans Affärer,

Lars Heikensten: The Swedish economy and monetary policy Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at a seminar arranged by the Stockholm Chamber of Commerce and Veckans Affärer,

Inflation targeting. Governor Svein Gjedrem Gausdal 31 January Mainland GPD and consumer prices Percentage change on previous year

Inflation targeting Governor Svein Gjedrem Gausdal January SG Gausdal.. Mainland GPD and consumer prices Percentage change on previous year Mainland GDP Consumer prices 99 99 99 99 99 99 99 997 998 999

Inflation targeting Governor Svein Gjedrem Gausdal January SG Gausdal.. Mainland GPD and consumer prices Percentage change on previous year Mainland GDP Consumer prices 99 99 99 99 99 99 99 997 998 999

Erdem Başçi: Recent economic and financial developments in Turkey

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Monetary Policy Report October

Monetary Policy Report October Reports from the Central Bank of Norway No. / Monetary Policy Report / Norges Bank Oslo Address: Bankplassen Postal address: Postboks 9 Sentrum, Oslo Phone: + Fax: + E-mail:

Monetary Policy Report October Reports from the Central Bank of Norway No. / Monetary Policy Report / Norges Bank Oslo Address: Bankplassen Postal address: Postboks 9 Sentrum, Oslo Phone: + Fax: + E-mail:

Jarle Bergo: The economic outlook

Jarle Bergo: The economic outlook Address by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 31 March 2005. The address

Jarle Bergo: The economic outlook Address by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, Oslo, 31 March 2005. The address

Gauging Current Conditions:

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

Meeting with Analysts

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

MONETARY POLICY REPORT WITH FINANCIAL STABILITY ASSESSMENT

7 DECEMBER MONETARY POLICY REPORT WITH FINANCIAL STABILITY ASSESSMENT Norges Bank Oslo 7 Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

7 DECEMBER MONETARY POLICY REPORT WITH FINANCIAL STABILITY ASSESSMENT Norges Bank Oslo 7 Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 19 July 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 19 July 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

Corporate and Household Sectors in Austria: Subdued Growth of Indebtedness

Corporate and Household Sectors in Austria: Subdued Growth of Indebtedness Stabilization of Corporate Sector Risk Indicators The Austrian Economy Slows Down Against the background of the renewed recession

Corporate and Household Sectors in Austria: Subdued Growth of Indebtedness Stabilization of Corporate Sector Risk Indicators The Austrian Economy Slows Down Against the background of the renewed recession

Structural Changes in the Maltese Economy

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

CONTENTS 1. INTRODUCTION AND SUMMARY 5 2. INFLATION TRENDS 7 3. MONETARY POLICY SINCE OCTOBER ECONOMIC PROJECTIONS TO THE END OF

APRIL 2004 APRIL 2004 2 CONTENTS 1. INTRODUCTION AND SUMMARY 5 2. INFLATION TRENDS 7 3. MONETARY POLICY SINCE OCTOBER 2003 18 4. ECONOMIC PROJECTIONS TO THE END OF 2006 27 5. MONETARY POLICY CONDUCT AND

APRIL 2004 APRIL 2004 2 CONTENTS 1. INTRODUCTION AND SUMMARY 5 2. INFLATION TRENDS 7 3. MONETARY POLICY SINCE OCTOBER 2003 18 4. ECONOMIC PROJECTIONS TO THE END OF 2006 27 5. MONETARY POLICY CONDUCT AND

Monetary Policy Report 1/09

.. Monetary Policy Report / Governor Svein Gjedrem London, March Norwegian banks equity capital ) Per cent of total assets. - Sources: Klovland (), Statistics Norway and Norges Bank ) Includes savings

.. Monetary Policy Report / Governor Svein Gjedrem London, March Norwegian banks equity capital ) Per cent of total assets. - Sources: Klovland (), Statistics Norway and Norges Bank ) Includes savings

NBIM Quarterly Performance Report Second quarter 2007

NBIM Quarterly Performance Report Second quarter 2007 Government Pension Fund Global Norges Bank s foreign exchange reserves Investment portfolio Buffer portfolio Government Petroleum Insurance Fund Norges

NBIM Quarterly Performance Report Second quarter 2007 Government Pension Fund Global Norges Bank s foreign exchange reserves Investment portfolio Buffer portfolio Government Petroleum Insurance Fund Norges

Monetary Policy Report 3/12. Charts

Monetary Policy Report / Charts Chart. Key rates and estimated forward rates as at June and October.¹) Percent. January December ²) US Euro area³) UK 9 ) Broken lines show estimated forward rates as at

Monetary Policy Report / Charts Chart. Key rates and estimated forward rates as at June and October.¹) Percent. January December ²) US Euro area³) UK 9 ) Broken lines show estimated forward rates as at

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

Economy Report - Malaysia

Economy Report - Malaysia (Extracted from 2001 Economic Outlook) REAL GROSS DOMESTIC PRODUCT Economic activity in Malaysia expanded strongly in 2000 under the stimulus of strong export growth as well as

Economy Report - Malaysia (Extracted from 2001 Economic Outlook) REAL GROSS DOMESTIC PRODUCT Economic activity in Malaysia expanded strongly in 2000 under the stimulus of strong export growth as well as

The Riksbank's monetary policy strategy

SPEECH DATE: 14 September 2006 SPEAKER: LOCALITY: Deputy Governor Lars Nyberg Foreign Banker s Association SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00 00 Fax +46 8 21 05

SPEECH DATE: 14 September 2006 SPEAKER: LOCALITY: Deputy Governor Lars Nyberg Foreign Banker s Association SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00 00 Fax +46 8 21 05

Jean-Pierre Roth: Recent economic and financial developments in Switzerland

Jean-Pierre Roth: Recent economic and financial developments in Switzerland Introductory remarks by Mr Jean-Pierre Roth, Chairman of the Governing Board of the Swiss National Bank and Chairman of the Board

Jean-Pierre Roth: Recent economic and financial developments in Switzerland Introductory remarks by Mr Jean-Pierre Roth, Chairman of the Governing Board of the Swiss National Bank and Chairman of the Board

Consumption, Income and Wealth

59 Consumption, Income and Wealth Jens Bang-Andersen, Tina Saaby Hvolbøl, Paul Lassenius Kramp and Casper Ristorp Thomsen, Economics INTRODUCTION AND SUMMARY In Denmark, private consumption accounts for

59 Consumption, Income and Wealth Jens Bang-Andersen, Tina Saaby Hvolbøl, Paul Lassenius Kramp and Casper Ristorp Thomsen, Economics INTRODUCTION AND SUMMARY In Denmark, private consumption accounts for

Haruhiko Kuroda: Japan s economy and monetary policy

Haruhiko Kuroda: Japan s economy and monetary policy Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a meeting with business leaders, Osaka, 28 September 2015. Introduction * * * It is

Haruhiko Kuroda: Japan s economy and monetary policy Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a meeting with business leaders, Osaka, 28 September 2015. Introduction * * * It is

Deepak Mohanty: Inflation dynamics in India issues and concerns

Deepak Mohanty: Inflation dynamics in India issues and concerns Speech by Mr Deepak Mohanty, Executive Director of the Reserve Bank of India, to the Bombay Chamber of Commerce and Industry, Mumbai, 4 March

Deepak Mohanty: Inflation dynamics in India issues and concerns Speech by Mr Deepak Mohanty, Executive Director of the Reserve Bank of India, to the Bombay Chamber of Commerce and Industry, Mumbai, 4 March

Developments in inflation and its determinants

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

Monetary Policy Report 3/11. Charts

Monetary Policy Report / Charts Chart. Projected output gap¹) for Norway's trading partners. Per cent. Q Q - - - - MPR / MPR / - - - - - 7 9 ) The output gap measures the percentage deviation between GDP

Monetary Policy Report / Charts Chart. Projected output gap¹) for Norway's trading partners. Per cent. Q Q - - - - MPR / MPR / - - - - - 7 9 ) The output gap measures the percentage deviation between GDP

Potential Output in Denmark

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

Svein Gjedrem: The krone exchange rate and competitiveness in the business sector

Svein Gjedrem: The krone exchange rate and competitiveness in the business sector Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Federation of Norwegian Process Industries,

Svein Gjedrem: The krone exchange rate and competitiveness in the business sector Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Federation of Norwegian Process Industries,

Monthly policy monetary report November monetary policy monthly report

Monthly policy monetary report 2006 Bank of Albania monetary policy monthly report NOVEMBER 2006 Bank of Albania 2006 Monthly policy monetary report I Main highlights Annual inflation rate in 2006 recorded

Monthly policy monetary report 2006 Bank of Albania monetary policy monthly report NOVEMBER 2006 Bank of Albania 2006 Monthly policy monetary report I Main highlights Annual inflation rate in 2006 recorded

Monetary Policy Report 1/12. Charts

Monetary Policy Report / Charts Chart. Projected output gap¹) for Norway's trading partners. Percent. Q Q - - - - MPR / MPR / - - - - - 8 ) The output gap measures the percentage deviation between GDP

Monetary Policy Report / Charts Chart. Projected output gap¹) for Norway's trading partners. Percent. Q Q - - - - MPR / MPR / - - - - - 8 ) The output gap measures the percentage deviation between GDP

INFLATION REPORT / III

INFLATION REPORT / III 11 INFLATION REPORT / III FOREWORD 3 In 1998, the Czech National Bank switched to inflation targeting. In the inflation targeting regime, the central bank s communication with

INFLATION REPORT / III 11 INFLATION REPORT / III FOREWORD 3 In 1998, the Czech National Bank switched to inflation targeting. In the inflation targeting regime, the central bank s communication with

Lars Heikensten: Monetary policy and the economic situation

Lars Heikensten: Monetary policy and the economic situation Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at Handelsbanken, Karlstad, 26 January 2004. * * * It is nice to meet a group

Lars Heikensten: Monetary policy and the economic situation Speech by Mr Lars Heikensten, Governor of the Sveriges Riksbank, at Handelsbanken, Karlstad, 26 January 2004. * * * It is nice to meet a group

Øystein Olsen: The purpose and scope of monetary policy

Øystein Olsen: The purpose and scope of monetary policy Speech by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME) / BI Norwegian Business

Øystein Olsen: The purpose and scope of monetary policy Speech by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME) / BI Norwegian Business

2. International developments

2. International developments (6) During the period, global economic developments were generally positive. The economy grew faster in the second quarter, mainly driven by the favourable financing conditions

2. International developments (6) During the period, global economic developments were generally positive. The economy grew faster in the second quarter, mainly driven by the favourable financing conditions

Monetary Policy Update December 2007

Monetary Policy Update December 7 At its meeting on 8 December, the Executive Board of the Riksbank decided to hold the repo rate unchanged at per cent. During the first half of 8 it is expected that the

Monetary Policy Update December 7 At its meeting on 8 December, the Executive Board of the Riksbank decided to hold the repo rate unchanged at per cent. During the first half of 8 it is expected that the

NATIONAL BANK OF SERBIA. Speech at the presentation of the Inflation Report November 2018

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November 8 Savo Jakovljević, Acting General Manager of the Economic Research and Statistics Department Belgrade, November 8 Ladies

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November 8 Savo Jakovljević, Acting General Manager of the Economic Research and Statistics Department Belgrade, November 8 Ladies

Editor: Felix Ewert. The Week Ahead Key Events 6 12 Nov, 2017

Editor: Felix Ewert The Week Ahead Key Events 6 12 Nov, 2017 Monday 6, 09.30 SWE: Industrial production & orders (Sep) % mom/yoy SEB Cons. Prev. Production 2.5/4.1 --- -1.7/7.3 New orders --- --- -1.8/6.3

Editor: Felix Ewert The Week Ahead Key Events 6 12 Nov, 2017 Monday 6, 09.30 SWE: Industrial production & orders (Sep) % mom/yoy SEB Cons. Prev. Production 2.5/4.1 --- -1.7/7.3 New orders --- --- -1.8/6.3

Svein Gjedrem: Economic perspectives

Svein Gjedrem: Economic perspectives Annual address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the meeting of the Supervisory Council of Norges Bank, Oslo, February * * *

Svein Gjedrem: Economic perspectives Annual address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the meeting of the Supervisory Council of Norges Bank, Oslo, February * * *

Structural changes in the Maltese economy

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the

SME Monitor Q aldermore.co.uk

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

December. Monetary Policy Report. with financial stability assessment

December Monetary Policy Report with financial stability assessment Norges Bank Oslo Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

December Monetary Policy Report with financial stability assessment Norges Bank Oslo Address: Bankplassen Postal address: Postboks 79 Sentrum, 7 Oslo Phone: +7 Fax: +7 E-mail: central.bank@norges-bank.no

Implementation of the EU fiscal governance framework: Assessment of the fiscal stance appropriate for the euro area

European Fiscal Board Implementation of the EU fiscal governance framework: Assessment of the fiscal stance appropriate for the euro area Prof. Niels THYGESEN Chair of the European Fiscal Board Interparliamentary

European Fiscal Board Implementation of the EU fiscal governance framework: Assessment of the fiscal stance appropriate for the euro area Prof. Niels THYGESEN Chair of the European Fiscal Board Interparliamentary

Financial Stability 2

Reports from the Central Bank of Norway No. 6/3 Financial Stability 3 N o v e m b e r Financial Stability is published twice a year and this report and the Inflation Report together comprise Norges Bank

Reports from the Central Bank of Norway No. 6/3 Financial Stability 3 N o v e m b e r Financial Stability is published twice a year and this report and the Inflation Report together comprise Norges Bank

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Executive Directors welcomed the continued

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

Irma Rosenberg: Assessment of monetary policy

Irma Rosenberg: Assessment of monetary policy Speech by Ms Irma Rosenberg, Deputy Governor of the Sveriges Riksbank, at Norges Bank s conference on monetary policy 2006, Oslo, 30 March 2006. * * * Let

Irma Rosenberg: Assessment of monetary policy Speech by Ms Irma Rosenberg, Deputy Governor of the Sveriges Riksbank, at Norges Bank s conference on monetary policy 2006, Oslo, 30 March 2006. * * * Let

The Exchange Rate and Canadian Inflation Targeting

The Exchange Rate and Canadian Inflation Targeting Christopher Ragan* An essential part of the Bank of Canada s inflation-control strategy is a flexible exchange rate that is free to adjust to various

The Exchange Rate and Canadian Inflation Targeting Christopher Ragan* An essential part of the Bank of Canada s inflation-control strategy is a flexible exchange rate that is free to adjust to various

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2018) Meeting with Analysts Petr Král Prague, 4 May 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report II/2018) Meeting with Analysts Petr Král Prague, 4 May 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

2018 World Savings Day

ACRI Association of Italian Savings Banks 2018 World Savings Day Address by the Governor of the Bank of Italy Ignazio Visco Rome, 31 October 2018 The protection of savings calls, in the first place, for

ACRI Association of Italian Savings Banks 2018 World Savings Day Address by the Governor of the Bank of Italy Ignazio Visco Rome, 31 October 2018 The protection of savings calls, in the first place, for

OIL-EXPORTING COUNTRIES: KEY STRUCTURAL FEATURES, ECONOMIC DEVELOPMENTS AND OIL REVENUE RECYCLING

OIL-EXPORTING COUNTRIES: KEY STRUCTURAL FEATURES, ECONOMIC DEVELOPMENTS AND OIL REVENUE RECYCLING This article reviews key structural features and recent economic developments in ten major oilexporting

OIL-EXPORTING COUNTRIES: KEY STRUCTURAL FEATURES, ECONOMIC DEVELOPMENTS AND OIL REVENUE RECYCLING This article reviews key structural features and recent economic developments in ten major oilexporting

DETERMINANTS OF INFLATION INFLATION REPORT 2004/1. Inflation Report 1/ April 2004

Inflation Report REPORT / / April REPORT / Contents FOREWORD 5 REPORT / SUMMARY 7 Inflation assessment 9 DETARMINANTS OF The financial markets International economic activity and inflation Economic activity

Inflation Report REPORT / / April REPORT / Contents FOREWORD 5 REPORT / SUMMARY 7 Inflation assessment 9 DETARMINANTS OF The financial markets International economic activity and inflation Economic activity

Economic projections

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Economic Projections for

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Minutes of the Monetary Policy Committee meeting, November 2018

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, November 2018 Published 21 November 2018 The Act on the Central Bank of Iceland stipulates

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, November 2018 Published 21 November 2018 The Act on the Central Bank of Iceland stipulates

Outlook for Economic Activity and Prices (July 2018)

") Outlook for Economic Activity and Prices (July 2018) July 31, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue growing at a pace above its potential in fiscal 2018, mainly

Outlook for Economic Activity and Prices (July 2018) July 31, 2018 Bank of Japan The Bank's View 1 Summary Japan's economy is likely to continue growing at a pace above its potential in fiscal 2018, mainly

OUTLOOK FOR THE HOUSING MARKET AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN

OUTLOOK FOR THE HOUSING MARKET AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN Oslo, 7 November 217 Topics Outlook for the Norwegian economy The housing market Monetary policy 2 Topics Outlook for the

OUTLOOK FOR THE HOUSING MARKET AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN Oslo, 7 November 217 Topics Outlook for the Norwegian economy The housing market Monetary policy 2 Topics Outlook for the

Updated macroeconomic forecast

Prepare for landing: Updated macroeconomic forecast 217-219 26 January 218 Íslandsbanki Research Executive summary The Icelandic economy has been buoyant in the past few years, after the deep recession

Prepare for landing: Updated macroeconomic forecast 217-219 26 January 218 Íslandsbanki Research Executive summary The Icelandic economy has been buoyant in the past few years, after the deep recession

Daniel Mminele: Thoughts on South Africa s monetary policy

Daniel Mminele: Thoughts on South Africa s monetary policy Address by Mr Daniel Mminele, Deputy Governor of the South African Reserve Bank, at the JP Morgan Investor Conference, Washington DC, 16 April

Daniel Mminele: Thoughts on South Africa s monetary policy Address by Mr Daniel Mminele, Deputy Governor of the South African Reserve Bank, at the JP Morgan Investor Conference, Washington DC, 16 April

Economic Survey. Economic developments in Norway Forecasts

Economic Survey Economic developments in Norway Forecasts 2017-2020 3/2017 Economic Survey 3/2017 Norwegian economy Economic developments in Norway After being in a cyclical downturn for almost three

Economic Survey Economic developments in Norway Forecasts 2017-2020 3/2017 Economic Survey 3/2017 Norwegian economy Economic developments in Norway After being in a cyclical downturn for almost three