Recovery in Europe The outcome of successful crisis policies?

|

|

|

- Alison Rice

- 5 years ago

- Views:

Transcription

1 Recovery in Europe The outcome of successful crisis policies? Discussion Catherine Mathieu, OFCE, Paris EUROPE AFTER THE CRISIS: WHERE IS THE ECONOMIC AND MONETARY UNION HEADED? Berlin, 12 June 2018 observatoire français des conjonctures économiques centre de recherche en économie de Sciences Po

2 Introductory remarks Peter Bofinger s presentation: Europe economic upswing after some serious policy mistakes in the immediate crisis. I agree very much with Peter Bofinger s analysis, I will not really challenge his interpretation, but rather give additional views.

3 Europe back to growth after some serious policy mistakes in the crisis EMU and Europe have had different economic outcomes after the 2007 crisis - more rapid rebound in EU non euro area countries than in euro area countries. In EMU: slow recovery - slower than elsewhere in advanced economies After the burst of the financial crisis, the euro area was unable to implement a coherent macro-economic strategy to recover the 8 percentage points of GDP lost during the crisis. Financial markets even bet on the sovereign default and euro area exit of several MS. The EU authorities and MS did not respond sufficiently rapidly and strongly. They denied to guarantee public debts, implementing limited financial solidarity only, under strict conditionality. Guaranteeing public debts would have implied to re-think and explicit the euro area framework.

4 Under the Commission s pressure, under financial markets and rating agencies threat, MS had no choice but implement restrictive policies in times of austerity. In the euro area as a whole, fiscal restriction measures amounted to 1.6% of GDP in 2011, 2.3% in 2012, 1.1% in 2013 and 0.7% in This strategy halted the nascent economic recovery in 2010 (where GDP grew by 2.2% on a y-o-y basis in the last quarter. Euro area GDP fell in 2012 and Euro area GDP per head reached its 2008 level only in Although the economic situation has improved, the scars of the crisis remain in many countries (high unemployment, large public debts, increases of income inequalities, financial instability, deindustrialization).

5 Table: some economic indicators GDP growth * Unemp. Rate ; % April 2018 Current account, % of GDP 2007 Current account, % of GDP 2017 Germany The Neths Austria Ireland Belgium Finland France Portugal Italy Spain Greece Euro area UK Denmark Sweden *Average 2017 and Forecasts Source : EUROSTAT, OECD, OFCE s forecasts

6 In 2017, the euro area current account surplus was 3.6% of GDP. For the euro area as a whole, the euro is undervalued. In an area with high unemployment and current account surplus, monetary policy should not be expansionary (as this lowers the exchange rate) but fiscal (or wage) policy should be expansionary. However, intra-area current account imbalances have declined: Germany and the Netherlands keep high current account surpluses, but except for France, no MS runs a higher than 1% of GDP surplus. This results not only from austerity policies, but also from internal devaluation strategies. Southern economies have improved their situation to some extent, but Germany maintains a substantial competitiveness advantage.

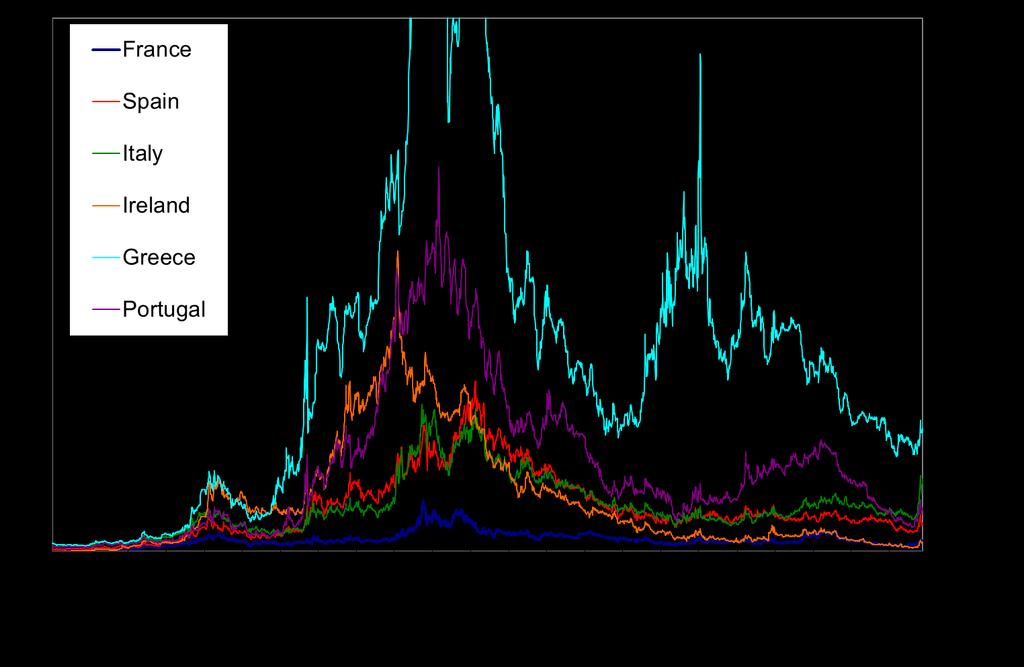

7 Unit wage costs (whole economy), 1997 = 100 Source OECD

8 Winners and losers Industrial production =100 Austria 175 Belgium 163 Germany 134 Finland 121 Netherlands 119 Sweden 114 Denmark 105 France 93 UK 93 Portugal 91 Spain 90 Italy 84 Greece 83

9 Back to growth after some serious policy mistakes in the crisis Policy mistakes during the crisis: Monetary policy: only stabilisation tool used : ZLB, QE Incapacity to reduce intra-zone imbalances, no incentive for banks to lend to productive sectors rather to speculation, no clear public debt guarantee Fiscal policies: were kept restrictive for too long - role of fiscal policy underestimated (size of multipliers, ) - Fiscal rules in place did not allow for countercyclical policies Need for economic policy coordination and differentiated policies among MS (economic contexts differ according to MS, with a single exchange rate and monetary policy, fiscal policies should differ)

10 Public debts and deficits % of GDP Public debt, Maastricht criteria Public balance (and max.) 2007 Highest deficit Germany (81) France Italy Spain (100) The Neths (68) Belgium (108) Austria (84) Greece Portugal (131) Finland Ireland (120) Euro area (94) UK USA Japan Source: Ameco

11 Back to growth after some serious policy mistakes in the crisis? Maybe the recovery is behind us. Euro area GDP slowed in the first quarter of 2018 (0.4% instead of 0.7% previous quarters), in part temporary phenomena but slowdown seems underway at least suggested by Business survey data, up to end May: +0.4 GDP would grow by 2.2% (q/q-4) instead of 2.7% at the end of 2017 More importantly: a new euro area crisis may be around the Corner: Italy and financial markets

12 Back to growth after some serious policy mistakes in the crisis Two doctrines differ over the conduct of economic policy : a Keynesian policy requests a precise coordination of national (fiscal, social, taxes and wages) policies ; a liberal one requests economic policies competition and financial markets supervision. Northern MS refuses unlimited guarantee which is indispensable for a single currency.

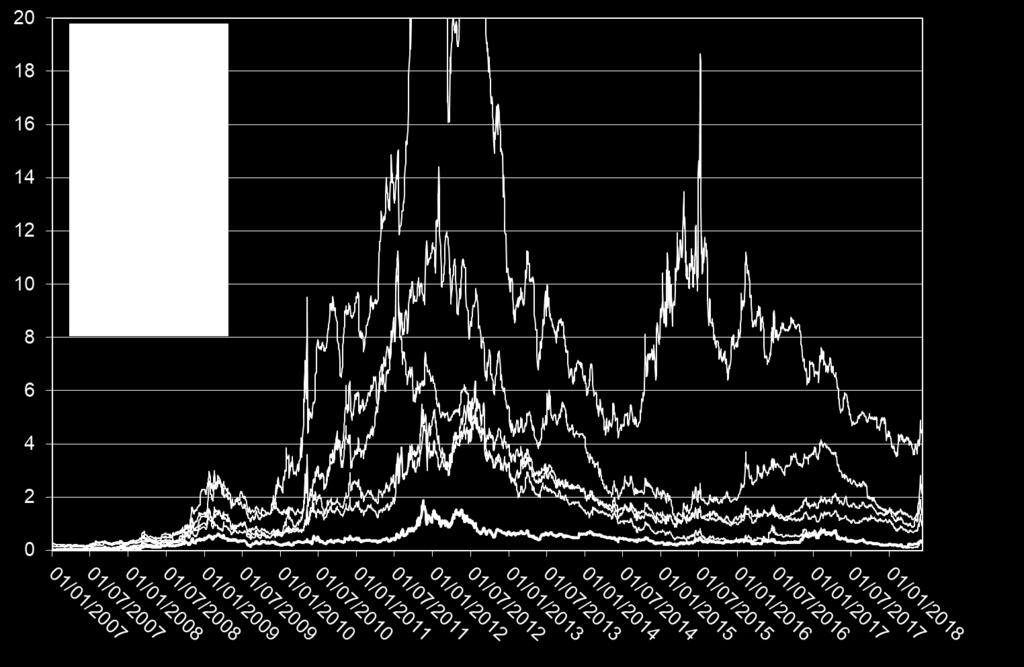

13 Fragility The euro area is fragile. If Northern countries are doing well, many countries (among them notably Italy, Greece and even France) suffer from de-industrialisation and are in trouble. Parties opposed to the current orientation of European Institutions have more and more influence in some MS. Anti-European Governments (Hungary, Poland, Italy) come to power, which may destabilize the EU or the Euro area. Financial markets are nervous. The Italy-Germany government spread rose to 2.4 percentage points. The Spain-Germany spread is 0.95 p.p. The following question remains unsolved: can the euro area functioning be improved, accounting for divergent situations, interests and views in MS?

14 10-year government interest rates February 2012 May 2016 June 2018 Greece Portugal US Spain Italy UK Ireland Sweden France Belgium Finland Austria Netherlands Germany Japan

15 Interest rates on 10-year government bonds (percent)

16 Inflation

17 Which proposals? Proposals emanating from EU institutions generally tend to increase EU authorities power. They face reluctance from MS, who wish to keep their power and some autonomy: Northern MS are against EU transfers; smaller countries wish to keep their specificity, and refuse ruling from the larger MS and from the Commission. EU institutions generally tend to place MS under surveillance, either as concerns macroeconomic management or structural reforms, which comes in contradiction with domestic democratic sovereignty, as could be seen from the Greek crisis, from Brexit, from the last election in Italy. Besides, EU institutions do not wish to question the Stability and Growth Pact and the Fiscal Compact, which constrain fiscal policy coordination, as they do not wish to undermine the absence of explicit coordination between fiscal and monetary policies.

18 to achieve the Banking Union (SRF, EIDS) To limit the domestic publics bonds owns by banks No A riskless asset No A European Minister of economy and finance which powers? The capital market Union No More MS fiscal discipline No A fiscal capacity and a stabilisation mechanism at the EU level Yes if no more constraints on MS A reform support programme No A single seat at the IMF strange The ESM become a EMF which powers? One challenge is that any major reform would require a change in the Treaties, and unanimity, and in several countries a referendum with no guarantee about the results, as European construction is not currently popular.

19 Economists view points - Some propose to oblige MS to comply with the SGP and the TSCG; - Some rely on financial markets to control domestic economic policies, - Others to change the fiscal rules. - Some suggest a Euro zone budget and a minister of finance to control MS fiscal policy and/or to put in place a fiscal capacity and/or to organise transfers between MS. - Others refuse a transfers Union or a liabilities Europe - Some push for moving towards a federal EU with increased democracy - Some claims for public investment programme for ecological transition. - Some make original suggestions to cut public debts (monetisation, fiscal money) - Some advocating economic policy coordination with Keynesian targets

20 Some hot issues Should MS try to bring public debt back to 60% of GDP (even if it implies fiscal restrictive policies during 20 years)? Our answers : No. Can we accept the ECB to change its policy because the next governor is expected to be a German? No Do we need macro-prudential measures to avoid real estate or financial bubbles? Yes Do we need un-prudential measures to encourage banks to finance innovative investment or ecological ones? Yes OG evaluations should be reviewed. Yes In order to cut public debts, combating tax avoidance, tax optimisation and tax competition should be a priority The ECB should progressively normalize interest rates and bonds purchase policy. But at the same time, public debts should remain guaranteed; coordinated fiscal, wage, and tax policies should reduce imbalances among MS. Europe has to make political choices which are impossible/difficult in a multicountry framework.

21 Is the euro zone actually well prepared for a next crisis, maybe as a result of recent developments in Italy? No The euro area needs: A lender of last resort to avoid speculative crises - sovereign bonds should remain safe assets Scrapping the numerical stupid fiscal rules: 3% of GDP, 60% of GDP Implementing instead a golden rule for public finances, allowing to borrow to invest

22 Net public investment, % of GDP 2,0 1,5 EMU-12 Periphery Germany 1,0 0,5 0, ,5-1,0 Source: Achim Truger (calculations based on Ameco)

23 Is Draghi s whatever it takes enough to avoid a new panic? Issue of last resort (again) There is a need for solidarity beween MS

24 Do current regulations and deficit rules allow enough flexibility to avoid procyclical policies in future? NO they allow for very limited contra-cyclical policy Countries already committing with the rules cannot be constrained to run counter-cyclical policies Countries not committing with the rules cannot run countercyclical policies What is needed : golden rule for public finances (at least) Plus economic policy coordination

25 What is needed to normalize ECB s policy? So far the ECB s does not meet its own inflation target of close to two percent (this was the case in May, but due to higher energy prices, core inflation close to 1.1% only) There are no signs of accelerating domestic inflationary pressure, even in countries with low unemployment: Germany, the Netherlands There are obviously no sign of accelerating inflation is countries where unemployment is high (and higher than before the crisis) There is still a negative output gap at the EA level Still no reason for the ECB increase its interest rate

26 Is the current growth solid enough to reduce the damages caused by the crisis in terms of regionally high unemployment, reduced investment, etc Euro area countries should become able again to issue safe public debts, at an interest rate controlled by the ECB. They should be able to run a government deficit in line with their macroeconomic stabilisation needs. The mutual guarantee of public debts should be entire for countries agreeable to submit their economic policy to a coordination process.

27 Economic policy coordination cannot consist in fulfilling automatic rules (like the SGP rules). A coordination process needs to be organised between MS. Coordination should target GDP growth and full employment; it should account for all economic variables; Countries should follow an economic policy strategy allowing to meet the inflation target (at least to remain within a target of around 2%), to meet an objective in terms of wage developments (in the medium-run real wages should grow in line with labour productivity, in the short-run adjustment processes should be implemented by countries where wages have risen too rapidly, or not sufficiently).

28 As the real targets are full employment, external balance and inflation rate, a target on public balance or public debt is not useful in this framework Countries should announce and negotiate their current account balance targets; countries running high external surpluses should agree to lower them or to finance explicitly industrial projects in Southern economies. The process should always reach unanimous agreement on a coordinated but differentiated strategy.

29 It should however be recognised that our proposal is politically impossible to implement, since Germany and many Northern countries refuse to depart from the European Treaties, the SGP or the TSCG; they require that financial markets exert control on MS, and that the EU authorities can impose structural reforms to MS. If one adds the refusal of a EU of transfers and the refusal of tax harmonisation, it seems unlikely that ambitious projects, such as Emmanuel Macron s, for instance, may be implemented. Besides, three political choices need to be made. Does the EU want to maintain and develop its social model, with its specificity in terms of social and fiscal systems and labour rights or is its objective it to oblige reluctant countries to accept the constraints of a liberal globalization? Should EU MS keep different national social and tax systems, or is the objective to make them converge? Or does the EU want the national systems to converge? Which part of public spending should be done at the EU level? Can the EU make progresses without any precise agreement on these three issues?

30 One of the causes of the crisis was the rapid expansion of the financial sector, financial incomes and wealth. Taxes on financial incomes, wealth should be increased to restore public finances, instead of cutting social spending like European institutions usually recommend. At the EU level, this requires a strategy of tax harmonisation, to set minimum tax rates for firms and high incomes, to tax higher wealth, and to ensure that each country may be able to tax its firms and its residents. Euro area s survival requires that the European project becomes popular again, carrying a specific social model, an objective of convergence and solidarity among MS and turn towards a development taking fully into account the ecological constraints. It is only within this framework that institutional progresses could be made. But can all Member countries share this common project? Where are the political and social forces capable of imposing it?

Europe s Response to the Sovereign Debt Crisis. Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

How Europe is Overcoming the Euro Crisis?

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

Europe s Response to the Sovereign Debt Crisis. Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Fiscal rules in Lithuania

Fiscal rules in Lithuania Algimantas Rimkūnas Vice Minister, Ministry of Finance of Lithuania 3 June, 2016 Evolution of National and EU Fiscal Regulations Stability and Growth Pact (SGP) Maastricht Treaty

Fiscal rules in Lithuania Algimantas Rimkūnas Vice Minister, Ministry of Finance of Lithuania 3 June, 2016 Evolution of National and EU Fiscal Regulations Stability and Growth Pact (SGP) Maastricht Treaty

The Stability and Growth Pact Status in 2001

4 The Stability and Growth Pact Status in 200 Tina Winther Frandsen, International Relations INTRODUCTION The EU member states' public finances showed remarkable development during the 990s. In 993, the

4 The Stability and Growth Pact Status in 200 Tina Winther Frandsen, International Relations INTRODUCTION The EU member states' public finances showed remarkable development during the 990s. In 993, the

Europe in crisis. George Gelauff. ECU 92 Lustrum Conference Utrecht. 23 February 2012

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

Europe in crisis George Gelauff ECU 92 Lustrum Conference Utrecht Menu Costs and benefits of Europe Banks and governments Monetary Union and debts Germany Conclusion 2 Europe in crisis Europe largest export

34 th Associates Meeting - Andorra, 25 May Item 5: Evolution of economic governance in the EU

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

The European Economic Crisis

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

A Two-Handed Economist s Presentation on The Treaty. Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

REPORT FROM THE COMMISSION. Denmark. Report prepared in accordance with Article 126(3) of the Treaty

of the Treaty") EUROPEAN COMMISSION Brussels, 12.05.2010 SEC(2010) 585 REPORT FROM THE COMMISSION Denmark Report prepared in accordance with Article 126(3) of the Treaty REPORT FROM THE COMMISSION Denmark Report prepared

EUROPEAN COMMISSION Brussels, 12.05.2010 SEC(2010) 585 REPORT FROM THE COMMISSION Denmark Report prepared in accordance with Article 126(3) of the Treaty REPORT FROM THE COMMISSION Denmark Report prepared

Crisis and cooperative solutions: the euro area since 2008

Crisis and cooperative solutions: the euro area since 2008 Jérôme Creel ESCP Europe, Labex Refi & Sciences Po, OFCE [special issue of Réalités Industrielles, August 2018] Abstract: Since the European integration

Crisis and cooperative solutions: the euro area since 2008 Jérôme Creel ESCP Europe, Labex Refi & Sciences Po, OFCE [special issue of Réalités Industrielles, August 2018] Abstract: Since the European integration

Nicolaie Alexandru-Chidesciuc, CFA, PhD

, CFA, PhD Associate professor Romanian-American University Vice-president AAFBR Board member CFA Romania Bucharest, April 2011 1 Summary I. Some background II. Euro area imbalances III. Lessons IV. Conclusions

, CFA, PhD Associate professor Romanian-American University Vice-president AAFBR Board member CFA Romania Bucharest, April 2011 1 Summary I. Some background II. Euro area imbalances III. Lessons IV. Conclusions

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Economic recovery and employment in the EU. Raymond Torres, Director, ILO Research Department

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Implications of the European financial crisis for fiscal policy and public financing of the health and social sectors

Implications of the European financial crisis for fiscal policy and public financing of the health and social sectors Peter S Heller Visiting Professor of Economics Williams College April 17, 2013 Principal

Implications of the European financial crisis for fiscal policy and public financing of the health and social sectors Peter S Heller Visiting Professor of Economics Williams College April 17, 2013 Principal

The Turbulent EMS in the 1990s: What Lessons for Today? Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel

The Turbulent in the 1990s: What Lessons for Today? André Sapir Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel 2 The turbulent 1990s: the incompatible trio July 1990: Full

The Turbulent in the 1990s: What Lessons for Today? André Sapir Professor of Economics, Université Libre de Bruxelles Senior Fellow, Bruegel 2 The turbulent 1990s: the incompatible trio July 1990: Full

HOW TO DEAL WITH ECONOMIC DIVERGENCES IN EMU? N May Catherine MATHIEU OFCE. Henri STERDYNIAK OFCE

HOW TO DEAL WITH ECONOMIC DIVERGENCES IN EMU? N 2007-14 May 2007 Catherine MATHIEU OFCE Henri STERDYNIAK OFCE How to deal with economic divergences in EMU? Catherine Mathieu and Henri Sterdyniak (OFCE)

HOW TO DEAL WITH ECONOMIC DIVERGENCES IN EMU? N 2007-14 May 2007 Catherine MATHIEU OFCE Henri STERDYNIAK OFCE How to deal with economic divergences in EMU? Catherine Mathieu and Henri Sterdyniak (OFCE)

The ECB and its Watchers XIII. Klaus Regling CEO of EFSF Frankfurt, 10 June 2011

The ECB and its Watchers XIII Klaus Regling CEO of EFSF Frankfurt, 10 June 2011 Is the real economy disconnected from financial market developments? 3 Real GDP per capita growth (changes in percent) 2

The ECB and its Watchers XIII Klaus Regling CEO of EFSF Frankfurt, 10 June 2011 Is the real economy disconnected from financial market developments? 3 Real GDP per capita growth (changes in percent) 2

The Economic and Monetary Union and the European Union s Competence Issues

Working Paper Series L-2016-01 The Economic and Monetary Union and the European Union s Competence Issues Yumiko Nakanishi (Hitotsubashi University) 2016 Yumiko Nakanishi. All rights reserved. Short sections

Working Paper Series L-2016-01 The Economic and Monetary Union and the European Union s Competence Issues Yumiko Nakanishi (Hitotsubashi University) 2016 Yumiko Nakanishi. All rights reserved. Short sections

Spring Forecast: slowly recovering from a protracted recession

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

The Greek crisis and the European Stability Mechanism (ESM) Abstract The financial crisis of is considered by many economists to be the

Abstract The financial crisis of is considered by many economists to be the") The Greek crisis and the European Stability Mechanism (ESM) Abstract The financial crisis of 2007 2008 is considered by many economists to be the worst financial crisis since the Great Depression of the

The Greek crisis and the European Stability Mechanism (ESM) Abstract The financial crisis of 2007 2008 is considered by many economists to be the worst financial crisis since the Great Depression of the

International Environment Economics for Business (IEEB)

") International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

The Brussels Economic Forum

The Brussels Economic Forum What kind of policies should the new Member States apply to optimise their speed of convergence? Banco de Portugal VÍTOR CONSTÂNCIO Brussels, 23d of April 24 I. INTRODUCTION

The Brussels Economic Forum What kind of policies should the new Member States apply to optimise their speed of convergence? Banco de Portugal VÍTOR CONSTÂNCIO Brussels, 23d of April 24 I. INTRODUCTION

A role for public and social investment in EU economic governance

A role for public and social investment in EU economic governance Mario Pianta Università di Urbino Intereconomics conference New growth for Europe Berlin,10 October 2016 Europe s crisis: a problem of

A role for public and social investment in EU economic governance Mario Pianta Università di Urbino Intereconomics conference New growth for Europe Berlin,10 October 2016 Europe s crisis: a problem of

Euro area economic developments from monetary policy maker s perspective

Euro area economic developments from monetary policy maker s perspective Member of Executive Board Structure of the presentation: 1. Where do we come from? ECB s monetary policy set up and main reactions

Euro area economic developments from monetary policy maker s perspective Member of Executive Board Structure of the presentation: 1. Where do we come from? ECB s monetary policy set up and main reactions

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 THE DEBT CRISIS IN GREECE AND THE EURO ZONE

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 April 2010 Prepared by: Sema Gençay ÇAPANOĞLU (scapanoglu@ikv.org.tr) THE DEBT CRISIS IN GREECE AND THE EURO ZONE Greece is struggling with the most serious

ECONOMIC DEVELOPMENT FOUNDATION IKV BRIEF 2010 April 2010 Prepared by: Sema Gençay ÇAPANOĞLU (scapanoglu@ikv.org.tr) THE DEBT CRISIS IN GREECE AND THE EURO ZONE Greece is struggling with the most serious

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Back to fiscal consolidation in Europe and its dual tradeoff: now or later, through spending cuts or tax hikes

Back to fiscal consolidation in Europe and its dual tradeoff: now or later, through spending cuts or tax hikes Christophe Blot (OFCE) Jérôme Creel (OFCE & ESCP Europe) Bruno Ducoudré (OFCE) Xavier Timbeau

Back to fiscal consolidation in Europe and its dual tradeoff: now or later, through spending cuts or tax hikes Christophe Blot (OFCE) Jérôme Creel (OFCE & ESCP Europe) Bruno Ducoudré (OFCE) Xavier Timbeau

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

COMMUNICATION FROM THE COMMISSION 2014 DRAFT BUDGETARY PLANS OF THE EURO AREA: OVERALL ASSESSMENT OF THE BUDGETARY SITUATION AND PROSPECTS

EUROPEAN COMMISSION Brussels, 15.11.2013 COM(2013) 900 final COMMUNICATION FROM THE COMMISSION 2014 DRAFT BUDGETARY PLANS OF THE EURO AREA: OVERALL ASSESSMENT OF THE BUDGETARY SITUATION AND PROSPECTS EN

EUROPEAN COMMISSION Brussels, 15.11.2013 COM(2013) 900 final COMMUNICATION FROM THE COMMISSION 2014 DRAFT BUDGETARY PLANS OF THE EURO AREA: OVERALL ASSESSMENT OF THE BUDGETARY SITUATION AND PROSPECTS EN

The Economic Situation of the European Union and the Outlook for

The Economic Situation of the European Union and the Outlook for 2001-2002 A Report by the EUROFRAME group of Research Institutes for the European Parliament The Institutes involved are Wifo in Austria,

The Economic Situation of the European Union and the Outlook for 2001-2002 A Report by the EUROFRAME group of Research Institutes for the European Parliament The Institutes involved are Wifo in Austria,

PUBLIC FINANCE IN THE EU: FROM THE MAASTRICHT CONVERGENCE CRITERIA TO THE STABILITY AND GROWTH PACT

8 : FROM THE MAASTRICHT CONVERGENCE CRITERIA TO THE STABILITY AND GROWTH PACT Ing. Zora Komínková, CSc., National Bank of Slovakia With this contribution, we open up a series of articles on public finance

8 : FROM THE MAASTRICHT CONVERGENCE CRITERIA TO THE STABILITY AND GROWTH PACT Ing. Zora Komínková, CSc., National Bank of Slovakia With this contribution, we open up a series of articles on public finance

Household Balance Sheets and Debt an International Country Study

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

10: The European Monetary Union. Baldwin&Wyplosz The Economics of European Integration

10: The European Monetary Union The importance of credibility The theory OCA leaves out the issue of credibility in the conduct of monetary policy. Inflation depends on the expectations of economic agents

10: The European Monetary Union The importance of credibility The theory OCA leaves out the issue of credibility in the conduct of monetary policy. Inflation depends on the expectations of economic agents

The Euro Crisis. What happened, Why, What are They Doing to Save the Euro?

The Euro Crisis What happened, Why, What are They Doing to Save the Euro? What Happened? Why? Who has been blamed for the crisis? Greece and the other PIGS The EU (flawed economic governance of EMU) The

The Euro Crisis What happened, Why, What are They Doing to Save the Euro? What Happened? Why? Who has been blamed for the crisis? Greece and the other PIGS The EU (flawed economic governance of EMU) The

What is the global economic outlook?

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

STAT/12/ October Household saving rate fell in the euro area and remained stable in the EU27. Household saving rate (seasonally adjusted)

") STAT/12/152 30 October 2012 Quarterly Sector Accounts: second quarter of 2012 Household saving rate down to 12.9% in the euro area and stable at 11. in the EU27 Household real income per capita fell by

STAT/12/152 30 October 2012 Quarterly Sector Accounts: second quarter of 2012 Household saving rate down to 12.9% in the euro area and stable at 11. in the EU27 Household real income per capita fell by

What does Western Economic Crisis Mean for South Africa?

What does Western Economic Crisis Mean for South Africa? Seeraj Mohamed Corporate Strategy and Industrial Development Research Programme University of the Witwatersrand Context for Europe s Crisis Global

What does Western Economic Crisis Mean for South Africa? Seeraj Mohamed Corporate Strategy and Industrial Development Research Programme University of the Witwatersrand Context for Europe s Crisis Global

Managing the Fragility of the Eurozone. Paul De Grauwe London School of Economics

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Can the Euro Survive?

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Fiscal union and the need for accurate macroeconomic statistics. Guntram Wolff, Bruegel Luxembourg 26 Jan 2016

Fiscal union and the need for accurate macroeconomic statistics Guntram Wolff, Bruegel Luxembourg 26 Jan 2016 Outline The euro area crisis The new institutional setup Importance of macroeconomic statistics

Fiscal union and the need for accurate macroeconomic statistics Guntram Wolff, Bruegel Luxembourg 26 Jan 2016 Outline The euro area crisis The new institutional setup Importance of macroeconomic statistics

1. Sustainable public finances and structural reforms for growth

Over the last three years, we have taken unprecedented steps to combat the effects of the world-wide financial crisis, both in the European Union as such and within the euro area. The strategy we have

Over the last three years, we have taken unprecedented steps to combat the effects of the world-wide financial crisis, both in the European Union as such and within the euro area. The strategy we have

Divergence and Adjustment in the Euro Area

MINISTÉRIO DAS FINANÇAS Divergence and Adjustment in the Euro Area Vítor Gaspar Frankfurt June 15, 2012 MINISTÉRIO DAS FINANÇAS 1 Outline 1. Credit Boom 2. Eliminating excessive debt 3. Challenges ahead

MINISTÉRIO DAS FINANÇAS Divergence and Adjustment in the Euro Area Vítor Gaspar Frankfurt June 15, 2012 MINISTÉRIO DAS FINANÇAS 1 Outline 1. Credit Boom 2. Eliminating excessive debt 3. Challenges ahead

Check against delivery.

Bullet Points for intervention delivered at the OECD-IMF Conference on structural reforms by Jürgen Stark Member of the Executive Board and the Governing Council of the European Central Bank 17 March 2008

Bullet Points for intervention delivered at the OECD-IMF Conference on structural reforms by Jürgen Stark Member of the Executive Board and the Governing Council of the European Central Bank 17 March 2008

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

Modelling the sovereign debt crisis in Europe

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

What Governance for the Eurozone? Paul De Grauwe London School of Economics

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

Kristina Budimir 1 Debt Crisis in the EU Member States and Fiscal Rules

Kristina Budimir 1 Debt Crisis in the EU Member States and Fiscal Rules The financial turmoil in September 2008 provoked an economic downturn with a sharp slump in production, followed by slow growth resulting

Kristina Budimir 1 Debt Crisis in the EU Member States and Fiscal Rules The financial turmoil in September 2008 provoked an economic downturn with a sharp slump in production, followed by slow growth resulting

How to avoid a double-dip recession in the eurozone

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

ECB LTRO Dec Greece program

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

The EU Craft and SME Barometer 2018/H2

The EU Craft and SME Barometer 2018/H2 SMEs show stability at high level; SME Climate Index stabilises at 81.7 Internal demand fosters SMEs growth, yet no further acceleration is expected The UEAPME SME

The EU Craft and SME Barometer 2018/H2 SMEs show stability at high level; SME Climate Index stabilises at 81.7 Internal demand fosters SMEs growth, yet no further acceleration is expected The UEAPME SME

Lithuania within the Economic Governance cycle of the EU

European Institute of Public Administration - Institut européen d administration publique Lithuania within the Economic Governance cycle of the EU Faculty of Economics University of Vilnius, 16 October

European Institute of Public Administration - Institut européen d administration publique Lithuania within the Economic Governance cycle of the EU Faculty of Economics University of Vilnius, 16 October

Surrogates of Fiscal Federalism

Surrogates of Fiscal Federalism Francesco Saraceno OFCE-Research Center in Economics of Sciences Po Luiss School of European Political Economy Jakarta School of Government and Public Policy Europe 2020:

Surrogates of Fiscal Federalism Francesco Saraceno OFCE-Research Center in Economics of Sciences Po Luiss School of European Political Economy Jakarta School of Government and Public Policy Europe 2020:

Overview of EU public finances

6 volume 17, 12/29B I Overview of EU public finances PRE-CRISIS DEVELOPMENTS Public finance developments in the EU up to 28 can be divided into three stages: In 1997, the Stability and Growth Pact entered

6 volume 17, 12/29B I Overview of EU public finances PRE-CRISIS DEVELOPMENTS Public finance developments in the EU up to 28 can be divided into three stages: In 1997, the Stability and Growth Pact entered

Europe in the World Economy: Economic Recovery and Europe 2020

Europe in the World Economy: Economic Recovery and Europe 2020 Rafael Doménech Economic recovery and Europe 2020: Towards smart, sustainable and inclusive growth Wilton Park, October 24, 2012 Main messages

Europe in the World Economy: Economic Recovery and Europe 2020 Rafael Doménech Economic recovery and Europe 2020: Towards smart, sustainable and inclusive growth Wilton Park, October 24, 2012 Main messages

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Economic and Financial Affairs Committee. The EMU: challenges and the way forward

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

The economic crisis and the move towards new economic governance of the EU

The economic crisis and the move towards new economic governance of the EU Fritz Breuss JSPS EU-Japan Joint Seminar wiiw Rethinking Regional Integration in the Light of the Current Crisis: East Asia and

The economic crisis and the move towards new economic governance of the EU Fritz Breuss JSPS EU-Japan Joint Seminar wiiw Rethinking Regional Integration in the Light of the Current Crisis: East Asia and

ILO World of Work Report 2013: EU Snapshot

Greece Spain Ireland Poland Belgium Portugal Eurozone France Slovenia EU-27 Cyprus Denmark Netherlands Italy Bulgaria Slovakia Romania Lithuania Latvia Czech Republic Estonia Finland United Kingdom Sweden

Greece Spain Ireland Poland Belgium Portugal Eurozone France Slovenia EU-27 Cyprus Denmark Netherlands Italy Bulgaria Slovakia Romania Lithuania Latvia Czech Republic Estonia Finland United Kingdom Sweden

THE EURO AREA AT A CROSSROADS

I N T E R N A T I O N A L M O N E T A R Y F U N D THE EURO AREA AT A CROSSROADS Jeffrey Franks Director, IMF Europe Office International Monetary Fund February 2, 2017 1 MONETARY UNION HAS IMPORTANT ACHIEVEMENTS

I N T E R N A T I O N A L M O N E T A R Y F U N D THE EURO AREA AT A CROSSROADS Jeffrey Franks Director, IMF Europe Office International Monetary Fund February 2, 2017 1 MONETARY UNION HAS IMPORTANT ACHIEVEMENTS

Prospects for the euro area.short and long term?

Prospects for the euro area.short and long term? Peter Westaway Head of Investment Strategy and Chief Economist, Europe Vanguard Presentation to conference on The euro: Voices from the commonwealth at

Prospects for the euro area.short and long term? Peter Westaway Head of Investment Strategy and Chief Economist, Europe Vanguard Presentation to conference on The euro: Voices from the commonwealth at

In search of symmetry in the eurozone

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Greece Rising

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Greece Rising

Project Link Meeting, New York

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Outlook Overview: OECD Countries UN LINK Conference, Bangkok October, 2009

Outlook Overview: OECD Countries UN LINK Conference, Bangkok 26 28 October, 2009 Dave Turner OECD, Economics Department OECD Outlook: Outline 1. Recovery underway but will probably be slow 2. Risks and

Outlook Overview: OECD Countries UN LINK Conference, Bangkok 26 28 October, 2009 Dave Turner OECD, Economics Department OECD Outlook: Outline 1. Recovery underway but will probably be slow 2. Risks and

Shredding Europe s Safety Net: The Welfare State and the Politics of Austerity

Shredding Europe s Safety Net: The Welfare State and the Politics of Austerity Dr. Erica E. Edwards Executive Director Center for European Studies/ European Union Center of Excellence UNC Chapel Hill eedwards@email.unc.edu

Shredding Europe s Safety Net: The Welfare State and the Politics of Austerity Dr. Erica E. Edwards Executive Director Center for European Studies/ European Union Center of Excellence UNC Chapel Hill eedwards@email.unc.edu

Chapter 1. Fiscal consolidation targets, plans and measures in OECD countries

1. FISCAL CONSOLIDATION TARGETS, PLANS AND MEASURES IN OECD COUNTRIES 1 Chapter 1 Fiscal consolidation targets, plans and measures in OECD countries This chapter discusses the consolidation efforts of

1. FISCAL CONSOLIDATION TARGETS, PLANS AND MEASURES IN OECD COUNTRIES 1 Chapter 1 Fiscal consolidation targets, plans and measures in OECD countries This chapter discusses the consolidation efforts of

Lecture 15. Fiscal Policy and the Stability Pact

Lecture 15 Fiscal Policy and the Stability Pact The Fiscal Policy Instrument In a monetary union, the fiscal instrument assumes greater importance: the only macroeconomic policy instrument left at the

Lecture 15 Fiscal Policy and the Stability Pact The Fiscal Policy Instrument In a monetary union, the fiscal instrument assumes greater importance: the only macroeconomic policy instrument left at the

Chronology of European Initiatives in Response to the Crisis 1,2

Chronology of Initiatives in Response to the Crisis 1,2 Michaela Hajek-Rezaei 3 Oct. 6/7, 2008 Oct. 8, 2008 The EU finance ministers agree on a coordinated response to the financial crisis. The Ecofin

Chronology of Initiatives in Response to the Crisis 1,2 Michaela Hajek-Rezaei 3 Oct. 6/7, 2008 Oct. 8, 2008 The EU finance ministers agree on a coordinated response to the financial crisis. The Ecofin

Rules-Based Fiscal Policy in EMU: Pros and Cons

Rules-Based Fiscal Policy in EMU: Pros and Cons Presentation at the Brussels Economic Forum Richard Hemming International Monetary Fund April 22, 2004 The Case for Fiscal Rules Political economy influences

Rules-Based Fiscal Policy in EMU: Pros and Cons Presentation at the Brussels Economic Forum Richard Hemming International Monetary Fund April 22, 2004 The Case for Fiscal Rules Political economy influences

Towards a Reform of E(M)U

U") Towards a Reform of E(M)U Prof. Dr. Dr. h.c. Lars P. Feld University of Freiburg and Walter Eucken Institut.ECB Watchers, Frankfurt,14th March 2018 17 18 GCEE proposal Maastricht 2.0 : Necessary elements

Towards a Reform of E(M)U Prof. Dr. Dr. h.c. Lars P. Feld University of Freiburg and Walter Eucken Institut.ECB Watchers, Frankfurt,14th March 2018 17 18 GCEE proposal Maastricht 2.0 : Necessary elements

Document de travail / Mai 2013

Document de travail 2013-06 / Mai 2013 REDEMPTION? Catherine Mathieu and Henri Sterdyniak OFCE Redemption? Catherine MATHIEU* and Henri STERDYNIAK** Abstract The economic crisis which started in 2008

Document de travail 2013-06 / Mai 2013 REDEMPTION? Catherine Mathieu and Henri Sterdyniak OFCE Redemption? Catherine MATHIEU* and Henri STERDYNIAK** Abstract The economic crisis which started in 2008

Overview. Origins. EU Austerity Economic Causes Economic Consequences 04/03/ Single European Act Neo-liberal Assumptions National Objectives

EU Austerity Economic Causes Economic Consequences IER Conference 9 March 2016 Overview CAUSES the neo-liberal assumptions of the 1986 Single Europe Act and subsequent treaties the contradictions between

EU Austerity Economic Causes Economic Consequences IER Conference 9 March 2016 Overview CAUSES the neo-liberal assumptions of the 1986 Single Europe Act and subsequent treaties the contradictions between

Miroljub Labus. Monetary and Exchange Rate Policy Part 2. Introduction into Economic System of the EU. Faculty of Law, Belgrade

Miroljub Labus Monetary and Exchange Rate Policy Part 2 Introduction into Economic System of the EU Faculty of Law, Belgrade R.Baldwin and C.Wyplosz: The Economics of European Integration, Ch.16 and 17

Miroljub Labus Monetary and Exchange Rate Policy Part 2 Introduction into Economic System of the EU Faculty of Law, Belgrade R.Baldwin and C.Wyplosz: The Economics of European Integration, Ch.16 and 17

Monetary Integration

Monetary Integration By Michael Möhnle Table of Contents 1. 6-Stages of Economic Integration 2. International Monetary Integration - Bretton Woods 3. European Monetary Integration 4. European (Economic

Monetary Integration By Michael Möhnle Table of Contents 1. 6-Stages of Economic Integration 2. International Monetary Integration - Bretton Woods 3. European Monetary Integration 4. European (Economic

EUROPA - Press Releases - Taxation trends in the European Union EU27 tax...of GDP in 2008 Steady decline in top corporate income tax rate since 2000

DG TAXUD STAT/10/95 28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio1

DG TAXUD STAT/10/95 28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio1

Courthouse News Service

14/2009-30 January 2009 Sector Accounts: Third quarter of 2008 Household saving rate at 14.4% in the euro area and 10.7% in the EU27 Business investment rate at 23.5% in the euro area and 23.6% in the

14/2009-30 January 2009 Sector Accounts: Third quarter of 2008 Household saving rate at 14.4% in the euro area and 10.7% in the EU27 Business investment rate at 23.5% in the euro area and 23.6% in the

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

EMPLOYMENT RATE IN EU-COUNTRIES 2000 Employed/Working age population (15-64 years)

") EMPLOYMENT RATE IN EU-COUNTRIES 2 Employed/Working age population (15-64 years EU-15 Denmark Netherlands Great Britain Sweden Portugal Finland Austria Germany Ireland Luxembourg France Belgium Greece Spain

EMPLOYMENT RATE IN EU-COUNTRIES 2 Employed/Working age population (15-64 years EU-15 Denmark Netherlands Great Britain Sweden Portugal Finland Austria Germany Ireland Luxembourg France Belgium Greece Spain

74 ECB THE 2012 MACROECONOMIC IMBALANCE PROCEDURE

Box 7 THE 2012 MACROECONOMIC IMBALANCE PROCEDURE This year s European Semester (i.e. the framework for EU policy coordination introduced in 2011) includes, for the first time, the implementation of the

Box 7 THE 2012 MACROECONOMIC IMBALANCE PROCEDURE This year s European Semester (i.e. the framework for EU policy coordination introduced in 2011) includes, for the first time, the implementation of the

The current state of the Euro and its future

The current state of the Euro and its future Volker Wieland IMFS, Goethe University Frankfurt Seminar Municipal Guarantee Board, Helsinki, Finland September 12, 2013 Some of the questions raised.. Which

The current state of the Euro and its future Volker Wieland IMFS, Goethe University Frankfurt Seminar Municipal Guarantee Board, Helsinki, Finland September 12, 2013 Some of the questions raised.. Which

Institutions for EMU Economic Governance Francesco Saraceno OFCE-Research Center in Economics of Sciences Po Luiss School of European Political Economy Jakarta School of Government and Public Policy Where

Institutions for EMU Economic Governance Francesco Saraceno OFCE-Research Center in Economics of Sciences Po Luiss School of European Political Economy Jakarta School of Government and Public Policy Where

Fiscal Policy, Budget Deficits and the Economic Crisis. Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010

Fiscal Policy, Budget Deficits and the Economic Crisis Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010 Three lines of defence against the economic crisis 1. Measures to deal with the

Fiscal Policy, Budget Deficits and the Economic Crisis Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010 Three lines of defence against the economic crisis 1. Measures to deal with the

The reform of EU s fiscal rules: between centralisation and decentralisation

The reform of EU s fiscal rules: between centralisation and decentralisation Marco BUTI Director-General European Commission, DG Economic and Financial Affairs Bruegel Annual Research Seminar 2018 Brussels,

The reform of EU s fiscal rules: between centralisation and decentralisation Marco BUTI Director-General European Commission, DG Economic and Financial Affairs Bruegel Annual Research Seminar 2018 Brussels,

AIECE Spring Meeting General Report. Bologna, 12/13 May Ferdinand Fichtner, Christoph Große Steffen, Michael Hachula DIW Berlin

AIECE Spring Meeting 2016 General Report Ferdinand Fichtner, Christoph Große Steffen, Michael Hachula DIW Berlin Overview: Discussion of General Report Thursday Friday 14.30 14.45 14.45 16.00 16.20 16.35

AIECE Spring Meeting 2016 General Report Ferdinand Fichtner, Christoph Große Steffen, Michael Hachula DIW Berlin Overview: Discussion of General Report Thursday Friday 14.30 14.45 14.45 16.00 16.20 16.35

FINANCIAL STABILITY SOVEREIGN DEBT ECONOMIC GROWTH

The European sovereign debt crisis and the future of the euro Peter Bekx European Commission i Tokyo, 30 November 2012 1 A Vicious circle FINANCIAL STABILITY SOVEREIGN DEBT ECONOMIC GROWTH 2 Breaking the

The European sovereign debt crisis and the future of the euro Peter Bekx European Commission i Tokyo, 30 November 2012 1 A Vicious circle FINANCIAL STABILITY SOVEREIGN DEBT ECONOMIC GROWTH 2 Breaking the

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Ireland

Eurozone EY Eurozone Forecast September 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Ireland

Josef Bonnici: The changing nature of economic and financial governance following the euro area crisis

Josef Bonnici: The changing nature of economic and financial governance following the euro area crisis Introductory remarks by Professor Josef Bonnici, Governor of the Central Bank of Malta, at the Malta

Josef Bonnici: The changing nature of economic and financial governance following the euro area crisis Introductory remarks by Professor Josef Bonnici, Governor of the Central Bank of Malta, at the Malta

THE EU S ECONOMIC RECOVERY PICKS UP MOMENTUM

THE EU S ECONOMIC RECOVERY PICKS UP MOMENTUM ECONOMIC SITUATION The EU economy saw a pick-up in growth momentum at the beginning of this year, boosted by strong business and consumer confidence. Output

THE EU S ECONOMIC RECOVERY PICKS UP MOMENTUM ECONOMIC SITUATION The EU economy saw a pick-up in growth momentum at the beginning of this year, boosted by strong business and consumer confidence. Output

Peter Praet: The role of the central bank and euro area governments in times of crisis

Peter Praet: The role of the central bank and euro area governments in times of crisis Speech by Mr Peter Praet, Member of the Executive Board of the European Central Bank, at the German Federal Ministry

Peter Praet: The role of the central bank and euro area governments in times of crisis Speech by Mr Peter Praet, Member of the Executive Board of the European Central Bank, at the German Federal Ministry

Greece Facing an Uncertain Future

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

OECD III: EMU. Gavin Cameron Lady Margaret Hall. Michaelmas Term 2004

OECD III: EMU Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 the Trinity Free Capital Mobility USA, Japan ERM, NICs, EMU Independent domestic monetary policy Stable (Fixed) Exchange Rate Bretton

OECD III: EMU Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 the Trinity Free Capital Mobility USA, Japan ERM, NICs, EMU Independent domestic monetary policy Stable (Fixed) Exchange Rate Bretton