EUROPE LEADS FLIGHT TO QUALITY

|

|

|

- Erin Patrick

- 5 years ago

- Views:

Transcription

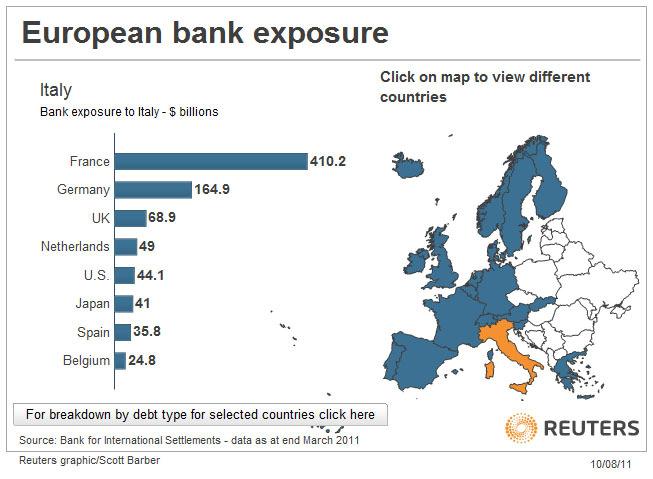

1 EUROPE LEADS FLIGHT TO QUALITY Our cautious stance has paid off this quarter as many of the risks we were concerned about have begun to play out. This has led to a flight to quality, which is where we are positioned, and has helped us to outperform. Our present situation feels like déjà vu from last year. In Q2 of last year we were introduced to the Greece and Ireland debt problems. A European short-term bailout and a Federal Reserve QE2 later, and all trouble was forgotten. However, one year later, we are back where we started. Greece is in trouble again and Portugal, Spain and Italy have been added to the mix. European banks are struggling and will need more capital due to these problems and more. In the US, QE2 has run its course and the sluggish economy is back to where it was prior to QE2. The Fed s recently announced Operation Twist seems unlikely to boost the economy out of its softness. Is this merely a pause that refreshes or should we be concerned about a 2008 redux? We look at the global landscape to gauge where earnings and stock markets may be headed. EUROPE All roads lead to Rome. Italy is too big to bailout and if the Greek crisis makes its way to Italy, we may see a 2008 redux. French banks have large exposures to Italy sovereign debt and if France is forced to step in and nationalize/recap its banks, it will lose its AAA credit rating. If that happens, then Germany will be the only sovereign of size left in Europe to bail anyone else out. If Germany were to take on a European rescue, its Debt/GDP ratio would rise to 130% and they would lose their AAA credit rating and they would lose the ability to bail anyone out. So the reason that Greece matters is its impact on contagion. That is, if Greece defaults, then investors could bid up Portugese bond yields due to worries that it defaults too. Those higher yields add to their fiscal deficit due to increased financing costs and make it more likely that Portugal will default. It can become a self fulfilling prophecy if investors are not convinced that the authorities will do something to protect investors from such losses. If Portugal defaults, then maybe Spain will. If Spain does, then maybe Italy will. The dominoes keep falling until we reach a new equilibrium. The problem is that that new equilibrium will be at much higher yields for sovereigns and banks and will mean much slower global growth if not outright contraction.

2 2

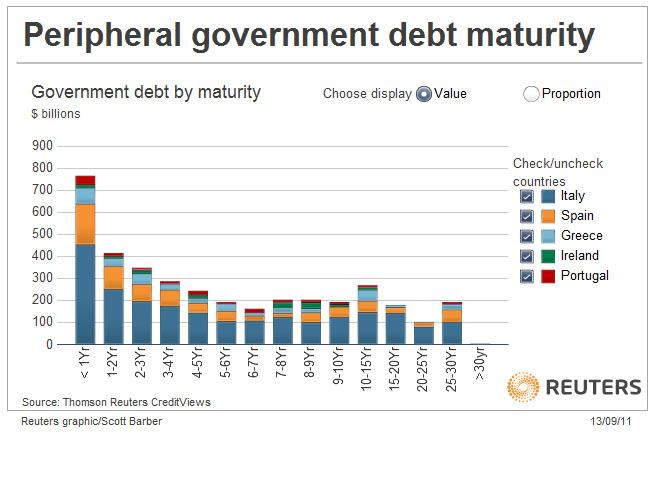

3 Also, this is not an issue that might arise in the distant future. Italy, Spain and Greece have significant debt that matures over the next year and will need to be rolled over. So that is why the lights are on at all hours of the night in European capitals. It is also why the IMF and EU institutions are getting creative to come up with ways to increase bailout funds. The idea being that if investors are convinced that the authorities have the firepower to rescue them, then said investors will continue to invest and keep yields low and perhaps a bailout will not be needed or at least will be minimized. It is the Hank Paulson bazooka approach from Will those worries come to fruition? That probably is not the most important question for us. Rather it is, will the earnings environment for the next couple of years be better or worse than it is right now. Even if contagion does not take hold, the increase in interest rates and cuts in spending could make earnings growth slow and stocks worth less. If there is a better than even chance that the earnings environment deteriorates, then we should be cautious. We currently believe that the risk is better than even and thus we are in a cautious stance presently. BANK CAPITAL Banks are instruments of a country s monetary policy and can impact the growth of a country s economy and the earnings of companies that do business in that country. As such, the health of banks, or lack thereof, have a large impact on economic and earnings growth. Bank capital growth or shrinkage impacts the ability of these banks to make new loans and grow an economy. This is why the US recapitalized its banks with TARP in 2008 because principal losses reduced bank capital and threatened to shrink loans (and therefore the economy) in the US without a capital infusion. Banks are the most leveraged sector in the market. As such they try to minimize risk by taking senior credit positions in loans with the goal that they minimize principal losses to acceptable levels. The total amount of bank assets is limited by the type of assets it has and the capital that it has. In normal times a bank has few losses so it levers up its capital to the limit to maximize earnings. Regulators set minimum capital ratios to limit the maximum leverage in the banking system. In simplistic terms a 10% capital ratio implies 10:1 leverage while a 2% capital ratio implies 50:1 leverage. So how much capital do banks have? Well it turns out that the answer is a moving target. In theory, capital is what is left over when you subtract liabilities from assets. That sounds straightforward but the trouble comes when trying to value the assets. That is why there is a footnote to balance sheets that divides assets into three levels. This tries to give the reader an insight into what portion of assets are valued based on liquid markets or a more subjective value from the company. A more subtle notion is Risk Weighted Assets (RWA). This notion tries to level the playing field for banks with different risk profiles. The idea is banks that only make nearly riskless loans need less capital than banks that make more risky loans. In theory this makes sense and is a shorthand way of using a single metric to measure the relative safety of a bank regardless of the underlying asset profile. 3

4 RWA implicitly assumes that the relative risk of the asset class remains the same and that credit ratings are timely. In the old regime where all assets were treated the same, a bank may need 10 cents of capital for every dollar of AAA US Treasuries or AAA French Euro bonds that it held as assets (note that the numbers are merely illustrative). Under a RWA regime, the bank may need only 2 cents, or less, of capital for every dollar of such bonds. Under RWA, the bank could hold 5 times as much AAA debt as before and still be considered adequately capitalized. (Technically RWA lowers the value of the asset, but conceptually lowering capital required seems easier to understand). The problem arises that over time AAA credits take on more debt and the rating agencies are slow to lower ratings. So the banks are still following the rules but the underlying assumptions have changed and the banks are really more risky than its capital ratio would imply. That is the world that we are now in. The RWA regime does not adequately reflect the true risk of underlying assets, thus leaving banks undercapitalized. The IMF was criticized for suggesting that European banks needed at least $300 billion in additional capital. That was when people were assuming a 22% haircut to Greek debt and perhaps other sovereign debt. Now a 50% number is being rumored and $1 trillion additional capital numbers are being mentioned. We met with the CEO of BNP, a large French bank, who said that they were going to be shrinking their balance sheet to help deal with their reduced capital. This will in turn reduce the credit available to BNP clients and probably the French economy as well. Some of this credit will be picked up by other banks but at the margin it makes credit harder to get and probably raises rates as there is less supply of credit. The more the contagion spreads from Greece, the more losses are incurred and the more capital is required or balance sheet shrinkage is required. If the contagion spreads to Italy, then the problem is probably too big for Europe to handle and the only recourse is a global bailout or economic shrinkage. That is why the Europeans are willing to throw so much time and resources at a seemingly insignificant Greek problem. Perhaps there will be a large enough bailout that will solve the problem and markets will soar from here. We do not assign that a high probability but it is something that we keep a close eye on. ECONOMIC HEALTH Given the issues in Europe, one would expect that their economy would be softening, and indeed it is. But what about the other global growth engines? Interestingly the Chinese Manufacturing PMI is now below 50. It last started down in mid China did an almost 30% of GDP stimulus plan back in 2009 through bank lending. This originally led to strong growth but has now morphed into inflation and bad loans which they are trying to contain. It is doubtful that China will be a strong growth engine in the near term. 4

5 5

6 6

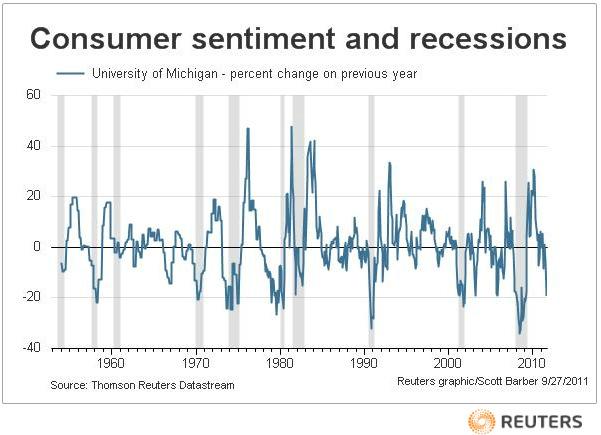

7 In the US, the Philly Fed Index is now negative, while the ISM manufacturing index is right about 50 suggesting softness in the US economy as well. The ECRI weekly leading index is also negative. The University of Michigan Consumer sentiment index is quite negative again. While all of these indices are a bit noisy and could turn around, they confirm our cautious stance. PORTFOLIO High quality performed almost twice as well this quarter as low quality. This helped our stock selection and sector selection. This quarter we took some risk off as we sold more volatile stocks and replaced them with less volatile stocks. One example is that we bought Autozone (up 8% for Q3) which is expanding into supplying local mechanics and garages. We sold Newell (down -24% for Q3) to make room for AZO. We also added to cash and puts. Cash is now up to 23%. Our stocks worked quite well this quarter as did our sector weights. Consumer staples (large overweight, -4.9% return Q3 vs S&P %) and utilities (overweight, 0.4% return Q3) were the top performing sectors. Financials (large underweight, -23.1% return Q3) lagged badly. So we were overweight the strong sectors and underweight the weak sector which added to outperformance. HIGH QUALITY STOCKS OUTPERFORM SINCE EARLY 2011 (Going up is quality outperf.) 7

8 LOOKING FORWARD We see Europe as a possible game changer. Estimates are all over the place as to how much additional capital the banks in Europe need. The IMF suggested around EU300 billion. Some brokerage firms suggested over EU1 trillion. This is uncharted territory. If Europe gets it right, we could see improved global GDP growth. If they get it wrong, slow global GDP growth could be with us for some time. We try to produce the best risk-adjusted returns available. As risks have increased, we have increased our protection. If risks subside or are priced in, we will gladly reduce our protection. One possible piece of good news is that the price of gasoline is finally dropping. This will help many consumer stocks as consumers spend their gas savings on other things. Best regards, Thomas H. Forester CIO and Portfolio Manager For more complete information on the Forester Funds, including charges and expenses, obtain a prospectus by calling or visiting The prospectus should be read carefully before investing. The foregoing does not constitute an offer of any securities for sale. Past performance is not indicative of future results. The views expressed herein are those of Thomas Forester and are not intended as investment advice. Copyright All rights reserved. 8

Can the Euro Survive?

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

The European Economic Crisis

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

A Two-Handed Economist s Presentation on The Treaty. Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

February 17, 2015 Todd Asset Management Investment Team Why Europe Why Now?

February 17, 2015 Todd Asset Management Investment Team Why Europe Why Now? We think it s time time to be more constructive on Europe. When most people think of the continent, it is usually with the thought

February 17, 2015 Todd Asset Management Investment Team Why Europe Why Now? We think it s time time to be more constructive on Europe. When most people think of the continent, it is usually with the thought

The Disconnect Continues

The Disconnect Continues Richard Bernstein June 3, 2011 Our strategies focus on finding disconnects between investor sentiment and the reality of improvement or deterioration in fundamentals. The current

The Disconnect Continues Richard Bernstein June 3, 2011 Our strategies focus on finding disconnects between investor sentiment and the reality of improvement or deterioration in fundamentals. The current

Economic Outlook 2011/ /10/2010

GOOD NEWS OUR ECONOMY IS GROWING Professor Emeritus of Economics Thomas R. Brown Professor in Economics Education WE ARE NOT IN A RECESSION WE HAVE A LONG WAY TO GO TO A FULL RECOVERY WORST RECOVERY SINCE

GOOD NEWS OUR ECONOMY IS GROWING Professor Emeritus of Economics Thomas R. Brown Professor in Economics Education WE ARE NOT IN A RECESSION WE HAVE A LONG WAY TO GO TO A FULL RECOVERY WORST RECOVERY SINCE

Interview with Klaus Regling, Managing Director, ESM. Published in Hospodárske noviny (Slovakia) on 16 September Interviewer: Tomáš Púchly

on 16 September Interviewer: Tomáš Púchly") Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.

During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.") Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Investment Report The Flexible Guarantee Bond and Flexi Guarantee Plan

Investment Report 2011 The Flexible Guarantee Bond and Flexi Guarantee Plan The Flexible Guarantee Bond and Flexi Guarantee Plan Investment Report 2011 This information does not constitute investment advice

Investment Report 2011 The Flexible Guarantee Bond and Flexi Guarantee Plan The Flexible Guarantee Bond and Flexi Guarantee Plan Investment Report 2011 This information does not constitute investment advice

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Fixed Income Markets: Experiencing Historic Lows

Fixed Income Markets: Experiencing Historic Lows Prepared: June 7, 2012 Overview How low can they go? This seemed to be the question the fixed income markets tried to answer on June 1st. Ten-year yields

Fixed Income Markets: Experiencing Historic Lows Prepared: June 7, 2012 Overview How low can they go? This seemed to be the question the fixed income markets tried to answer on June 1st. Ten-year yields

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

Short-Term (next 3 to six months)

") Review: Income Portfolio For a brief discussion of the portfolio s past annual performance visit the Performance Summary section. For the quarter ending June 30, 2012, the balanced portfolio generated

Review: Income Portfolio For a brief discussion of the portfolio s past annual performance visit the Performance Summary section. For the quarter ending June 30, 2012, the balanced portfolio generated

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Overcoming the crisis

Princeton, Oct 24 th, 2011 Overcoming the crisis backwards induction approach: 1. Diagnosis how did we get there? Run-up phase Crisis phase 2. Give long-run perspective Banking landscape (ESBies, European

Princeton, Oct 24 th, 2011 Overcoming the crisis backwards induction approach: 1. Diagnosis how did we get there? Run-up phase Crisis phase 2. Give long-run perspective Banking landscape (ESBies, European

The Global Economy Modest Improvement

Title line 1 Title line 2 The Global Economy Modest Improvement Name David Katsnelson, Director Title, date RISI Macroeconomic Service 3 June, 2015 1 Agenda 1. Global Snapshot 2. China 3. External Environment

Title line 1 Title line 2 The Global Economy Modest Improvement Name David Katsnelson, Director Title, date RISI Macroeconomic Service 3 June, 2015 1 Agenda 1. Global Snapshot 2. China 3. External Environment

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

The EU is running out of choices to tame the crisis

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

History of Recession. The Last Recession

Financial Instability is it a curse or a boom? Is it like that reality check which we need to bring us back to the path of inclusive growth and development or is it a result of Greed and No fear, is it

Financial Instability is it a curse or a boom? Is it like that reality check which we need to bring us back to the path of inclusive growth and development or is it a result of Greed and No fear, is it

Eurozone. Outlook for. Ernst & Young Eurozone Forecast. Summer edition 2012

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

Eurozone Ernst & Young Eurozone Forecast Summer edition 2012 Outlook for Published in collaboration with Andy Baldwin Head of Financial Services Europe, Middle East, India and Africa With key national

The Financial Crisis of ? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The dynamic nature of risk analysis: a multi asset perspective

The dynamic nature of risk analysis: This document is for Professional Clients in the UK only and is not for consumer use. Challenges for multi asset investing Multi asset portfolios with return and volatility

The dynamic nature of risk analysis: This document is for Professional Clients in the UK only and is not for consumer use. Challenges for multi asset investing Multi asset portfolios with return and volatility

CROSSCURRENTS Part II

CROSSCURRENTS Part II Two quarters ago we noted that the two hurricanes in Houston and Florida, while tragic, would be GDP positive for the next few quarters. Last quarter we added that the tax package

CROSSCURRENTS Part II Two quarters ago we noted that the two hurricanes in Houston and Florida, while tragic, would be GDP positive for the next few quarters. Last quarter we added that the tax package

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Rakan Mosely Head of Financial Markets Phone: (0)

") Rakan Mosely Head of Financial Markets Phone: (0)20 7803 1400 rmosely@oxfordeconomics.com The ECB s TLTROs: bazooka or peashooter? Ben May Senior Eurozone Economist bmay@oxfordeconomics.com June 2014 Outline

Rakan Mosely Head of Financial Markets Phone: (0)20 7803 1400 rmosely@oxfordeconomics.com The ECB s TLTROs: bazooka or peashooter? Ben May Senior Eurozone Economist bmay@oxfordeconomics.com June 2014 Outline

Member of

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2013

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Economic Overview. Bruce McCain, Key Private Bank Chief Investment Strategist. June/July Investments are:

Economic Overview June/July 2013 Bruce McCain, Key Private Bank Chief Investment Strategist Investments are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL

Economic Overview June/July 2013 Bruce McCain, Key Private Bank Chief Investment Strategist Investments are: NOT FDIC INSURED NOT BANK GUARANTEED MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL

Supply and Demand over the Business Cycle

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

ECONOMIC RESEARCH DEPARTMENT Summary of macroeconomic forecasts GDP Growth Inflation Curr. Account / GDP Fiscal balances / GDP % 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e 216 e 217 e 218 e

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

Investment Report With Profits Fund

Investment Report 2011 With Profits Fund With Profits Fund Investment Report 2011 The information in this report should not be considered as investment advice and we recommend that you speak to a suitably

Investment Report 2011 With Profits Fund With Profits Fund Investment Report 2011 The information in this report should not be considered as investment advice and we recommend that you speak to a suitably

Effectiveness of International Bailouts in the EU during the Financial Crisis A Comparative Analysis

Effectiveness of International Bailouts in the EU during the Financial Crisis A Comparative Analysis Sara Koczkas MSc student, Shanghai University, Sydney Institute of Language Commerce Shanghai, P.R.

Effectiveness of International Bailouts in the EU during the Financial Crisis A Comparative Analysis Sara Koczkas MSc student, Shanghai University, Sydney Institute of Language Commerce Shanghai, P.R.

Quarterly Research Conference Call October 18, 2011

Quarterly Research Conference Call October 18, 2011 SEATTLE 999 Third Avenue Suite 4200 Seattle, Washington 98104 206.622.3700 tel 206.622.0548 fax LOS ANGELES 2321 Rosecrans Avenue Suite 2250 El Segundo,

Quarterly Research Conference Call October 18, 2011 SEATTLE 999 Third Avenue Suite 4200 Seattle, Washington 98104 206.622.3700 tel 206.622.0548 fax LOS ANGELES 2321 Rosecrans Avenue Suite 2250 El Segundo,

Modelling the sovereign debt crisis in Europe

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Fund Management Diary

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Normalizing Monetary Policy

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

PAGE 42 THE STERN STEWART INSTITUTE PERIODICAL #10 JAMES GORMAN: NAVIGATING THE CHANGING LANDSCAPE OF FINANCE

PAGE 42 THE STERN STEWART INSTITUTE PERIODICAL #10 THE AUTHOR James Gorman Chairman of the Board and Chief Executive Officer Morgan Stanley PAGE 43 Navigating the Changing Landscape of Finance Contrary

PAGE 42 THE STERN STEWART INSTITUTE PERIODICAL #10 THE AUTHOR James Gorman Chairman of the Board and Chief Executive Officer Morgan Stanley PAGE 43 Navigating the Changing Landscape of Finance Contrary

The Macro-economy and the Global Financial Crisis

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Twin Problems: Employment and Consumer Spending

Twin Problems: Employment and Consumer Spending September 1, 11 Asha G. Bangalore agb3@ntrs.com The elevated unemployment rate remains at the top of the Fed s worry list. Nearly as important is the recent

Twin Problems: Employment and Consumer Spending September 1, 11 Asha G. Bangalore agb3@ntrs.com The elevated unemployment rate remains at the top of the Fed s worry list. Nearly as important is the recent

Banks and sovereign debt in Europe

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Fiscal Federalism - some thoughts

Fiscal Federalism - some thoughts John Hassler Swedish Fiscal Policy Council and IIES Why federal fiscal policy? 1. Financing union-wide public goods 2. Means to foster integration 3. Insurance against

Fiscal Federalism - some thoughts John Hassler Swedish Fiscal Policy Council and IIES Why federal fiscal policy? 1. Financing union-wide public goods 2. Means to foster integration 3. Insurance against

European Integration: The Euro and the ECB

European Integration: The Euro and the ECB A view from across the pond November 29 th, 2017 The Euro in Crazy Brief historical context: World War I: 1914-1918 Treaty of Versailles: Crippling War Reparations

European Integration: The Euro and the ECB A view from across the pond November 29 th, 2017 The Euro in Crazy Brief historical context: World War I: 1914-1918 Treaty of Versailles: Crippling War Reparations

Transcript of interview with ESM Managing Director Klaus Regling. The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

Picton Mahoney Asset Management Synergy Funds

Picton Mahoney Asset Management Synergy Funds Investors emotions remain fickle. In late April, the market seemed convinced that the global economy would be on a high-growth recovery. By the end of June,

Picton Mahoney Asset Management Synergy Funds Investors emotions remain fickle. In late April, the market seemed convinced that the global economy would be on a high-growth recovery. By the end of June,

European Market Uncertainties: How Do We Respond as Investors?

European Market Uncertainties: How Do We Respond as Investors? Los Angeles Fire and Police Pension System February 2012 European Debt Crisis - Introduction Financial markets have experienced significant

European Market Uncertainties: How Do We Respond as Investors? Los Angeles Fire and Police Pension System February 2012 European Debt Crisis - Introduction Financial markets have experienced significant

Market Update. Market Update: Global Economic Themes. Overview

Market Update Late August 2013 Market Update: Global Economic Themes So far this summer, we have produced two Market Update papers covering capital market themes and geopolitical risks. In this final paper

Market Update Late August 2013 Market Update: Global Economic Themes So far this summer, we have produced two Market Update papers covering capital market themes and geopolitical risks. In this final paper

Negative Yields in the Eurozone: Rationale and Repercussions

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not

The Invesco White Paper Series Invesco Fixed Income Negative Yields in the Eurozone: Rationale and Repercussions When in 1 the European Central Bank (ECB) introduced a negative deposit rate, this was not

The dynamic nature of risk analysis: a multi asset perspective

The dynamic nature of risk analysis: a multi asset perspective Whitepaper Multi asset portfolios with return and volatility targets have a dual focus: return and risk. This means that there are two important

The dynamic nature of risk analysis: a multi asset perspective Whitepaper Multi asset portfolios with return and volatility targets have a dual focus: return and risk. This means that there are two important

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

Our goal is to provide a clear perspective on the global financial markets, as well as a logical framework to discuss them, thereby enabling investors to recognize both the opportunities and risks that

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Eurozone Focus The Ongoing Saga Of Sovereign Debt

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

QUANTITATIVE EASING. 1. Point of departure 2. More on the US 3. Secular Stagnation 4. More on the Euro Area 5. Helicopter money 6.

1 Arne Jon Isachsen BI Norwegian Business School QUANTITATIVE EASING 1. Point of departure 2. More on the US 3. Secular Stagnation 4. More on the Euro Area 5. Helicopter money 6. Summing up 1. Point of

1 Arne Jon Isachsen BI Norwegian Business School QUANTITATIVE EASING 1. Point of departure 2. More on the US 3. Secular Stagnation 4. More on the Euro Area 5. Helicopter money 6. Summing up 1. Point of

Xavier Student Bond Investment Fund. Supplemental Economic Report 10/10/11-10/14/11 10/10/11. Sarkozy and Merkel Meet

Xavier Student Bond Investment Fund Supplemental Economic Report 10/10/11-10/14/11 10/10/11 Sarkozy and Merkel Meet French President Nicolas Sarkozy and German Chancellor Angela Merkel wound up their weekend

Xavier Student Bond Investment Fund Supplemental Economic Report 10/10/11-10/14/11 10/10/11 Sarkozy and Merkel Meet French President Nicolas Sarkozy and German Chancellor Angela Merkel wound up their weekend

Deposit Flight From Europe Banks Eroding Common Currency

Deposit Flight From Europe Banks Eroding Common Currency An accelerating flight of deposits from banks in four European countries is jeopardizing the renewal of economic growth and undermining a main tenet

Deposit Flight From Europe Banks Eroding Common Currency An accelerating flight of deposits from banks in four European countries is jeopardizing the renewal of economic growth and undermining a main tenet

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Miroljub Labus. Monetary and Exchange Rate Policy Part 2. Introduction into Economic System of the EU. Faculty of Law, Belgrade

Miroljub Labus Monetary and Exchange Rate Policy Part 2 Introduction into Economic System of the EU Faculty of Law, Belgrade R.Baldwin and C.Wyplosz: The Economics of European Integration, Ch.16 and 17

Miroljub Labus Monetary and Exchange Rate Policy Part 2 Introduction into Economic System of the EU Faculty of Law, Belgrade R.Baldwin and C.Wyplosz: The Economics of European Integration, Ch.16 and 17

Why U.S. Treasurys Look Like High-Yield Bonds

Boom & Bust Monthly Insight Video September 2014 Why U.S. Treasurys Look Like High-Yield Bonds Hi, I m Rodney Johnson. Welcome to the September 2014 educational video. This month we re going to talk about

Boom & Bust Monthly Insight Video September 2014 Why U.S. Treasurys Look Like High-Yield Bonds Hi, I m Rodney Johnson. Welcome to the September 2014 educational video. This month we re going to talk about

The role of central banks and governments in the crisis

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

Global Debt Crisis & Impact on India. October 2011

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011 Anthony B. Sanders Distinguished Professor of Real Estate Finance, George Mason University, and Senior Scholar, Mercatus

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011 Anthony B. Sanders Distinguished Professor of Real Estate Finance, George Mason University, and Senior Scholar, Mercatus

Global Debt and The New Neutral

Global Debt and The New Neutral May 1, 2018 by Nicola Mai of PIMCO Back in 2014, PIMCO developed the concept of The New Neutral as a secular framework for interest rates. After the financial crisis, the

Global Debt and The New Neutral May 1, 2018 by Nicola Mai of PIMCO Back in 2014, PIMCO developed the concept of The New Neutral as a secular framework for interest rates. After the financial crisis, the

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

WSJ: So when do you think they could realistically conclude these negotiations on the first review?

Transcript of interview with Klaus Regling, Managing Director, ESM Published in the Wall Street Journal, 12 April 2016 Klaus Regling, the managing director of the European Stability Mechanism, the eurozone

Transcript of interview with Klaus Regling, Managing Director, ESM Published in the Wall Street Journal, 12 April 2016 Klaus Regling, the managing director of the European Stability Mechanism, the eurozone

Are Low Rates Natural?

Are Low Rates Natural? Charles Bean London School of Economics Monetary and Financial Policy Conference London 25 September 2015 Questions and outline Questions: Why are (real safe) interest rates so low?

Are Low Rates Natural? Charles Bean London School of Economics Monetary and Financial Policy Conference London 25 September 2015 Questions and outline Questions: Why are (real safe) interest rates so low?

Gundlach: I m Not Really Bullish on Bonds

Gundlach: I m Not Really Bullish on Bonds September 13, 2017 by Robert Huebscher Jeffrey Gundlach, one of the most respected bond managers in the world with over $100B in fixed-income assets under management,

Gundlach: I m Not Really Bullish on Bonds September 13, 2017 by Robert Huebscher Jeffrey Gundlach, one of the most respected bond managers in the world with over $100B in fixed-income assets under management,

Weekly Market Commentary

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY Annenberg Foundation & Educational Film Center

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY ECONOMICS U$A: 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY (MUSIC PLAYS) ANNOUNCER: FUNDING FOR THIS PROGRAM WAS PROVIDED BY ANNENBERG

ECONOMICS U$A 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY ECONOMICS U$A: 21 ST CENTURY EDITION PROGRAM #25 MONETARY POLICY (MUSIC PLAYS) ANNOUNCER: FUNDING FOR THIS PROGRAM WAS PROVIDED BY ANNENBERG

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Ireland

Eurozone EY Eurozone Forecast September 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Ireland

The Time Has Come: The European Distressed Opportunity

INSIGHTS The Time Has Come: The European Distressed Opportunity 203.621.1700 2013, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY For several years, the European debt crisis has inflicted unprecedented

INSIGHTS The Time Has Come: The European Distressed Opportunity 203.621.1700 2013, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY For several years, the European debt crisis has inflicted unprecedented

Q Economic Outlook

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

2012 Economic Outlook: Overview of U.S. Economy. Presented by: Mark Evans, CFA Director of Investment Strategies

2012 Economic Outlook: Overview of U.S. Economy Presented by: Mark Evans, CFA Director of Investment Strategies mevans@viningsparks.com A Recovery of Sorts Rates have fallen even further Economy is getting

2012 Economic Outlook: Overview of U.S. Economy Presented by: Mark Evans, CFA Director of Investment Strategies mevans@viningsparks.com A Recovery of Sorts Rates have fallen even further Economy is getting

Adventures in Monetary Policy: The Case of the European Monetary Union

: The Case of the European Monetary Union V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis The ECB and Its Watchers XIX March 14, 2018 Why the Discontent? The Tell-Tale

: The Case of the European Monetary Union V. V. Chari & Keyvan Eslami University of Minnesota & Federal Reserve Bank of Minneapolis The ECB and Its Watchers XIX March 14, 2018 Why the Discontent? The Tell-Tale

Charts for the beach. Richard Bernstein. Global Growth in Money Supply *vs. Inflation Rate. Emerging market problems are secular, not short-term.

CPI Y/Y % Charts for the beach Richard Bernstein August 9, 2013 Our basic positions are now famous (or infamous). We continue to favor US assets and to shield our portfolios from the on-going and broad

CPI Y/Y % Charts for the beach Richard Bernstein August 9, 2013 Our basic positions are now famous (or infamous). We continue to favor US assets and to shield our portfolios from the on-going and broad

Department of Economics ECONOMIC OVERVIEW

Department of Economics ECONOMIC OVERVIEW January 2012 EDITORIAL Will the Euro Survive? By joining the euro, Europe s peripheral countries gained access to cheap, easy financing. They spent beyond their

Department of Economics ECONOMIC OVERVIEW January 2012 EDITORIAL Will the Euro Survive? By joining the euro, Europe s peripheral countries gained access to cheap, easy financing. They spent beyond their

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

> Macro Investment Outlook

> Macro Investment Outlook Dr Shane Oliver Head of Investment Strategy and Chief Economist October 214 The challenge for investors how to find better yield and returns as bank deposit rates stay low 9

> Macro Investment Outlook Dr Shane Oliver Head of Investment Strategy and Chief Economist October 214 The challenge for investors how to find better yield and returns as bank deposit rates stay low 9

Global Imbalances. January 23rd

Global Imbalances January 23rd Fact #1: The US deficit is big But there is little agreement on why, or on how much we should worry about it Global current account identity (CA = S-I = I*-S*) is a useful

Global Imbalances January 23rd Fact #1: The US deficit is big But there is little agreement on why, or on how much we should worry about it Global current account identity (CA = S-I = I*-S*) is a useful

The Lure of Alternative Credit Opportunities in Global Credit Investing

The Lure of Alternative Credit Opportunities in Global Credit Investing David Snow, Privcap: Today we re joined by Glenn August of Oak Hill Advisors. Glenn, welcome to PrivCap. Thanks for being here. Glenn

The Lure of Alternative Credit Opportunities in Global Credit Investing David Snow, Privcap: Today we re joined by Glenn August of Oak Hill Advisors. Glenn, welcome to PrivCap. Thanks for being here. Glenn

Global Economic Outlook Brittle Strength

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

CIOUPDATE. Chris Hyzy. Bank of America 05/30/18 9:30 am ET. All information is as of 5/30/2018 and subject to change based on market movements

Page 1 CIOUPDATE Operator: All information is as of 5/30/2018 and subject to change based on market movements : Hello, this is with the latest CIO market update. Global equity market weakness led by Europe

Page 1 CIOUPDATE Operator: All information is as of 5/30/2018 and subject to change based on market movements : Hello, this is with the latest CIO market update. Global equity market weakness led by Europe

JANUARY 2012 THE BEST AND WORST OF TIMES

JANUARY 2012 THE BEST AND WORST OF TIMES It was the best of times. It was the worst of times. So goes the opening line in Charles Dickens classic novel, A Tale of Two Cities. It has become a cliché due

JANUARY 2012 THE BEST AND WORST OF TIMES It was the best of times. It was the worst of times. So goes the opening line in Charles Dickens classic novel, A Tale of Two Cities. It has become a cliché due

Equity Market Comment 6 May 2010

Summary Equity markets caught between cyclical recovery and structural concerns Equity markets have been moving in a yo-yo pattern in recent days, rising on strong economic data and good corporate earnings

Summary Equity markets caught between cyclical recovery and structural concerns Equity markets have been moving in a yo-yo pattern in recent days, rising on strong economic data and good corporate earnings

What Should the Fed Do?

Peterson Perspectives Interviews on Current Topics What Should the Fed Do? Joseph E. Gagnon and Michael Mussa discuss the latest steps by the Federal Reserve to help the economy and what tools might be

Peterson Perspectives Interviews on Current Topics What Should the Fed Do? Joseph E. Gagnon and Michael Mussa discuss the latest steps by the Federal Reserve to help the economy and what tools might be

June 19, 2012 OUTLOOK

OUTLOOK June 19, 2012 The poor May U.S. jobs report helped crystallize the slowdown in the global economy in the second quarter. Global manufacturing slowed in May, led by weakness in the eurozone. Helpfully,

OUTLOOK June 19, 2012 The poor May U.S. jobs report helped crystallize the slowdown in the global economy in the second quarter. Global manufacturing slowed in May, led by weakness in the eurozone. Helpfully,

Management Report. Banco Espírito Santo do Oriente, S.A.

Management Report Banco Espírito Santo do Oriente, S.A. Summary of Management Report International Economic Framework The year under review was marked by a slowdown in global economic activity and GDP

Management Report Banco Espírito Santo do Oriente, S.A. Summary of Management Report International Economic Framework The year under review was marked by a slowdown in global economic activity and GDP

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE. 9 May 2012 Vicky Pryce

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

Keeping you informed matters

Keeping you informed matters Annual Investment Review January 2018 matters Page 2 of 12 Outlook Economic growth in the US and emerging economies is leading the way, with global growth falling in line.

Keeping you informed matters Annual Investment Review January 2018 matters Page 2 of 12 Outlook Economic growth in the US and emerging economies is leading the way, with global growth falling in line.

Financial Crises. Benjamin Graham. Videos in this lecture are from Kahn Academy

Financial Crises Videos in this lecture are from Kahn Academy Today s Plan An updated syllabus is posted Today s topics: Kahn Academy Videos on foreign currency reserves and speculative attacks The Asian

Financial Crises Videos in this lecture are from Kahn Academy Today s Plan An updated syllabus is posted Today s topics: Kahn Academy Videos on foreign currency reserves and speculative attacks The Asian

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

The U.S. and Michigan Economies

The U.S. and Michigan Economies Christopher Douglas, Ph.D. Assistant Professor of Economics University of Michigan-Flint Email: ccdougla@umflint.edu Twitter: @ChrisCDouglas August 18, 2011 Michigan Family

The U.S. and Michigan Economies Christopher Douglas, Ph.D. Assistant Professor of Economics University of Michigan-Flint Email: ccdougla@umflint.edu Twitter: @ChrisCDouglas August 18, 2011 Michigan Family

The Long Hard Slog BY JASON M. THOMAS

Economic Outlook August 26, 2011 The Long Hard Slog BY JASON M. THOMAS Economic data received since the end of July point to an economy that is substantially weaker than most observers would have anticipated

Economic Outlook August 26, 2011 The Long Hard Slog BY JASON M. THOMAS Economic data received since the end of July point to an economy that is substantially weaker than most observers would have anticipated

Parallel News and Events Q22012

August 2012 Q2 2012 Investment & Planning Newsletter Parallel News and Events Q22012 In the second quarter we remained focused on helping clients navigate a volatile market while at the same time developing

August 2012 Q2 2012 Investment & Planning Newsletter Parallel News and Events Q22012 In the second quarter we remained focused on helping clients navigate a volatile market while at the same time developing