Introduction to Accounting 1

|

|

|

- Ashlyn Flowers

- 5 years ago

- Views:

Transcription

1 DELTA UNIVERSITY FOR SCIENCE & TECHNOLOGY Introduction to Accounting 1 Section 7 Mr. Omar Ahmed Hashish 11/30/2017.

2 Adjusting the Accounts (Continue) Unearned Revenues: - They are those types of revenues in which Cash is received before performance of service. - On the day of cash payment the cash received is debited and the unearned revenues are credited because they are treated as liabilities. - Then on the day of adjustment the unearned revenues are debited in the amount which are really earned and an equal amount of revenues are credited. - Examples of unearned revenues: Rent Airline tickets School fees Etc.. Example 1: On February 1 st a client reserved a ticket for a flight from Egypt to France and paid the price of the ticket which was $ 3,000. The flight will be on February 22 nd. Journalize the necessary journal entries on the dates (February 1 st & February 22 nd ). - On February 1 st the client paid to us cash amount of $3,000 for a flight which will be later so the cash balance in our records increased so it will be debited and this amount of money is considered liability on us (the company) because the client didn't get his service yet and the revenues is considered not earned yet until he has his flight so an equal amount of unearned revenues will be credited so the journal entry will be as follows: February 1 st Cash 3000 Unearned Service Revenues On February 22 nd the client had his flight so the unearned revenues which were recorded on February 1 st are considered to be earned so the unearned revenues will be debited because they decrease (treated as liabilities) and the service revenues are credited so the journal entry will be as follows: February 22 nd Unearned Service Revenues 3000 Service Revenues 3000

3 Example 2: On May 1 st one of our apartments was rented for an upcoming year for a value of $24,000. Journalize the necessary journal entries on the dates (May 1 st, June 1 st & July 1 st ) - The same illustration as the previous example for the first date May 1 st Cash 24,000 Unearned Rent Revenue 24,000 - On the date June 1 st one month of the rent passed so the client is said to have service of one month so the rent of one month is considered as earned revenue which is calculated as (24,000/12=2,000) so the journal entry on this date will be as follows: June 1 st Unearned rent revenues 2,000 Rent Revenues 2,000 July 1 st Unearned Rent Revenues 2,000 Rent Revenues 2, Accruals: Accrued Expenses: - They are those types of expenses in which we receive service before we pay cash. - So on the date of having the service we record expenses as debit because they are incurred and record and equal amount of Accounts Payable as credit - Then on the date of Adjustment (payment of cash) we record the amount of cash paid as a credit and an equal amount of accounts payable as debit. Example: On October 17 th Amr Company had advertising services from an advertising company valued for $7,000, but the company didn't paid for these services until October 31 st. Journalize the necessary journal entries on the date (October 1 st & October 31 st ).

4 October 17 th Advertising Expenses 7,000 Accounts Payable 7,000 October 31 st Accounts Payable 7,000 Cash 7,000 Accrued Revenues: - They are this type of revenues when we perform service before we receive cash. - So on the date of performing service we record the value of the service as revenue in the credit side and an equal amount of accounts receivable in the debit side. - On the date of adjustment the amount of cash received is recorded in the debit side and an equal amount of accounts receivable is recorded in the credit side. Example: On April 5 th Ahmed Company performed computer services for a client valued for $800 but money was received on May 10 th. Journalize necessary journal entries on dates (April 5 th & May 10 th ). April 5 th Accounts Receivable 800 Service Revenues 800 May 10 th Cash 800 Accounts Receivable 800

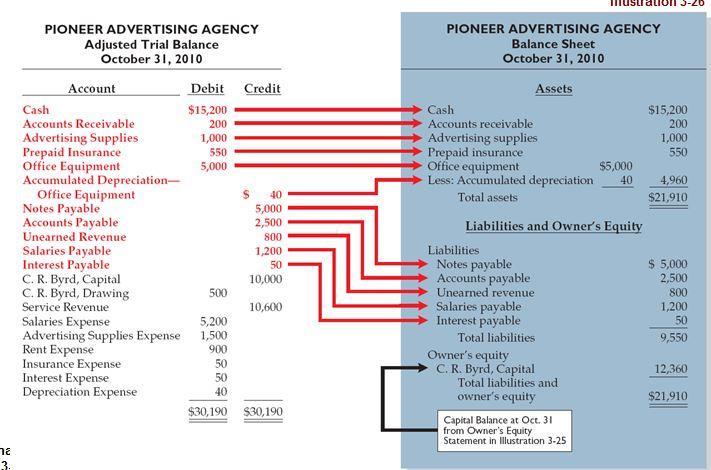

5 - After making the needed adjustments in the accounting period the company should prepare a trial balance including these adjustments in order to record correct and reliable balances for the accounts this new trial balance is called Adjusted Trial Balance. - From this adjusted trial balance the company can prepare the financial statements (Income Statement, Owner's Equity Statement & Balance Sheet) - Income Statement is prepared by moving the amounts of Revenues and expenses from the adjusted trial balance to the income statement, if revenues are more than expenses so the result is a net profit, while if expenses are more than revenues so the result is a net loss. - Then to prepare the owner's equity statement we record the beginning balance of the owner's equity as usual then in the Addition part we move the amounts of investments from the adjusted trial balance and the amount of net income from the income statement (if present) then in the deducting part we move the amounts of withdrawals from the adjusted trial balance and the amount of net loss from the income statement (if present) to calculate the ending balance of owner's equity. - Then to prepare the balance sheet we move the amounts of assets and liabilities from the adjusted trial balance each in its side and move the ending balance of the owner's equity from the owner's equity statement to the balance sheet. - These steps are performed as follows:

6 Good Luck

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

Module 3 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

The Accounting Cycle Revised Edition

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Learning Outcomes. The Basic Accounting Cycle

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Dec. 4: Paid $ 750 cash for office supplies. Date Accounts Debit Credit Dec. 4 Office Supplies 750 Cash 750

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Chapter 6 Accounting Adjustments and Working papers

Chapter 6 Accounting Adjustments and Working papers Topics 1. Cash basis vs. Accrual Basis 2. Accrued Income 3. Accrued Expenses 4. Prepaid Expenses 5. Unearned Income 6. Depreciation 7. Supply Expenses

Chapter 6 Accounting Adjustments and Working papers Topics 1. Cash basis vs. Accrual Basis 2. Accrued Income 3. Accrued Expenses 4. Prepaid Expenses 5. Unearned Income 6. Depreciation 7. Supply Expenses

REINFORCEMENT ACTIVITY 3, Part B, p. 715

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

HUM 211: Principles of Accounting Lecture 03: The Recording Process

Chapter 2 HUM 211: Principles of Accounting Lecture 03: The Recording Process Masud Jahan Department of Science and Humanities Military Institute of Science and Technology 2011 Learning Objective To identify

Chapter 2 HUM 211: Principles of Accounting Lecture 03: The Recording Process Masud Jahan Department of Science and Humanities Military Institute of Science and Technology 2011 Learning Objective To identify

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3)

") MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry.

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

CHAPTER 3 THE ADJUSTING PROCESS

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

COMSATS Institute of Information Technology Abbottabad

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

THE ACCOUNTING CYCLE: Accruals and Deferrals

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

Financial & Managerial Accounting 13th Edition Solutions Manual Warren

Financial & Managerial Accounting 13th Edition Solutions Manual Warren Completed downloadable package SOLUTIONS MANUAL for Financial & Managerial Accounting 13th Edition by Carl S Warren, James M Reeve,

Financial & Managerial Accounting 13th Edition Solutions Manual Warren Completed downloadable package SOLUTIONS MANUAL for Financial & Managerial Accounting 13th Edition by Carl S Warren, James M Reeve,

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Extra Practice for Block 1

Extra Practice for Block 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008. Print. Custom Edition. Chapter 1 p.26-27 1. Which of the following

Extra Practice for Block 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008. Print. Custom Edition. Chapter 1 p.26-27 1. Which of the following

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

COMSATS Institute of Information Technology Abbottabad

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

Chapter 3 The Adjusting Process

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Fill-in-the-Blank Equations. Exercises

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

2014 Mar. 31 Balance 30, Adjusting 26 22,500 7, Mar. 31 Balance 3, Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Demonstration Problems

Demonstration Problems Chapter 3 Problem #1: Solution A GENERAL JOURNAL J1 Date Account Title Debit Credit Oct. 31 Insurance Expense 3,600 Prepaid Expense 3,600 300 12 = $3,600 31 Supplies Expense 3,000

Demonstration Problems Chapter 3 Problem #1: Solution A GENERAL JOURNAL J1 Date Account Title Debit Credit Oct. 31 Insurance Expense 3,600 Prepaid Expense 3,600 300 12 = $3,600 31 Supplies Expense 3,000

Chapter 17 Accounting for Accruals and Deferrals

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

Accounting Principles Dr. Mishari Alfraih. Adjusting the Accounts

Accrual- vs. Cash-Basis Accounting Accrual-Basis Accounting Adjusting the Accounts Transactions recorded in the periods in which the events occur Revenues are recognized when earned, rather than when cash

Accrual- vs. Cash-Basis Accounting Accrual-Basis Accounting Adjusting the Accounts Transactions recorded in the periods in which the events occur Revenues are recognized when earned, rather than when cash

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Transactions that Affect Revenue, Expenses, and Withdrawals

Chapter 5 Transactions that Affect Revenue, Expenses, and Withdrawals 5.1 Relationship of Revenue, Expenses and Withdrawals to Owner s Equity Temporary and Permanent Accounts Temporary Accounts Revenue,

Chapter 5 Transactions that Affect Revenue, Expenses, and Withdrawals 5.1 Relationship of Revenue, Expenses and Withdrawals to Owner s Equity Temporary and Permanent Accounts Temporary Accounts Revenue,

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Your gateway to the world of accounting 1

Your gateway to the world of accounting 1 Accounting 212 Explain all the lessons of Accounting 212 for the third grade of secondary Ayman Ayyad Students-BH.com 2012 1 Index No. Lesson Title Page 1 Index

Your gateway to the world of accounting 1 Accounting 212 Explain all the lessons of Accounting 212 for the third grade of secondary Ayman Ayyad Students-BH.com 2012 1 Index No. Lesson Title Page 1 Index

Record Transactions in the Journal. Copy (post) to the Ledger. Prepare the Trial Balance

to the Ledger. Prepare the Trial Balance") Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

SOLUTIONS. Learning Goal 13

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 3 Adjusting the Accounts 高立翰

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

Important Terminology

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY. Y. Chang Company COVER SHEET

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

Problem 5-3A (90 minutes) Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011

Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011") Solution Manual for Chapter 5 354 Problem 5-3A (90 minutes) Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011 Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income

Solution Manual for Chapter 5 354 Problem 5-3A (90 minutes) Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011 Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income

New Horizons Balance Sheet as at December 31, 1997

Balance Sheet as at December 31, 1997 CURRENT ASSETS: Cash $152,350 Accounts Receivable 74,000 Office Supplies 800 Total Current Assets $227,150 CAPITAL ASSETS: Office Furniture $5,000 Less: Accumulated

Balance Sheet as at December 31, 1997 CURRENT ASSETS: Cash $152,350 Accounts Receivable 74,000 Office Supplies 800 Total Current Assets $227,150 CAPITAL ASSETS: Office Furniture $5,000 Less: Accumulated

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

CHAPTER 11. Financial Reporting Concepts ANSWERS TO QUESTIONS

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

Solution to Problem 31 Adjusting entries. Solution to Problem 32 Closing entries.

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts:

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

FORENSIC ACCOUNTING VERSION

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis 2/2017 Sub Topics 1. Accounting Cycles 2. Accounting Entry Principle 3. Transaction Analysis 1 1. ACCOUNTING CYCLE Identify

Chapter 3 Accounting cycles, Accounting Entry Principle, and Transaction Analysis 2/2017 Sub Topics 1. Accounting Cycles 2. Accounting Entry Principle 3. Transaction Analysis 1 1. ACCOUNTING CYCLE Identify

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

https://testbankdata.com/download/test-bank-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattisonella-mae-matsumura/

Instant download and all chapters Test Bank Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/test-bank-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattisonella-mae-matsumura/

Instant download and all chapters Test Bank Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/test-bank-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattisonella-mae-matsumura/

Chapter 2 The Accounting Information System

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

!!!!!! Topic 2! Question 1:!

Topic 2 Question 1: Robert McPhill formed a proprietorship to provide engineering and construction work. His jobs typically involve building and designing barking lots and Drives. Robert provided the following

Topic 2 Question 1: Robert McPhill formed a proprietorship to provide engineering and construction work. His jobs typically involve building and designing barking lots and Drives. Robert provided the following

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DCC Moodle Answer Key

All Journal Entries Apr 17, 2019 to Apr 29, 2019 Account Number Account Description Debits Credits Apr 17, 2019 J1 Bank Debit Memo, Bank charges printing new cheques SN 5180 Bank Charges Expense 31.00

All Journal Entries Apr 17, 2019 to Apr 29, 2019 Account Number Account Description Debits Credits Apr 17, 2019 J1 Bank Debit Memo, Bank charges printing new cheques SN 5180 Bank Charges Expense 31.00

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

CHAPTER 2 ANALYZING TRANSACTIONS DISCUSSION QUESTIONS

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

ACCT-112 Final Exam Practice Solutions

ACCT-112 Final Exam Practice Solutions Question 1 Jan 1 Cash 200,000 H. Happee, Capital 200,000 Jan 2 Prepaid Insurance 10,000 Cash 10,000 Jan 15 Equipment 15,000 Cash 5,000 Notes Payable 10,000 Jan 30

ACCT-112 Final Exam Practice Solutions Question 1 Jan 1 Cash 200,000 H. Happee, Capital 200,000 Jan 2 Prepaid Insurance 10,000 Cash 10,000 Jan 15 Equipment 15,000 Cash 5,000 Notes Payable 10,000 Jan 30

MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6)

") MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Double entry accounting system includes: Accrual accounting

MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Double entry accounting system includes: Accrual accounting

Examination: Financial Accounting Mid Term, Spring 2008 Examiner: Prof. Dr. Barbara Schöndube-Pirchegger

Examination: 11052 Financial Accounting Mid Term, Spring 2008 Examiner: Prof. Barbara Schöndube-Pirchegger First name: Last name: Matriculation number: The following aid can be used: non-programmable calculator

Examination: 11052 Financial Accounting Mid Term, Spring 2008 Examiner: Prof. Barbara Schöndube-Pirchegger First name: Last name: Matriculation number: The following aid can be used: non-programmable calculator

Answer: b Rationale: Journalizing means to record a transaction in a general journal.

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

COMPLETING THE ACCOUNTING CYCLE

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

The General Ledger. The 4 th step of the accounting cycle is to post to the ledger.

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

The General Ledger 4 Post to the ledger The 4 th step of the accounting cycle is to post to the ledger. The General Ledger is a book containing a separate page for each business account. The General Ledger

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Exercise 2-1. Exercise 2-2. Exercise 2-3. Name. = Liabilitiy Acounts + Debit Credit. Asset Acounts. Stockholders Equity Acounts Debit. Credit.

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

Lesson 4. Lesson 4. Cash. Beg. Balance End. Balance. 30 Liability. Accounting Cycle Part Stephen's Sweet Shop Trial Balance

Lesson 4 Financial Accounting (Information useful to investors and creditors.) The primary tool for investors and creditors are the financial statements to be prepared in accordance with generally accepted

Lesson 4 Financial Accounting (Information useful to investors and creditors.) The primary tool for investors and creditors are the financial statements to be prepared in accordance with generally accepted

Work4Me. Algorithmic Version. Problem Six. Adjusting Entries, Closing Entries, and Financial Analysis. 1 st Web-Based Edition

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Six Adjusting Entries, Closing Entries, and Financial Analysis Page 1 Emory Legal Services, Incorporated CHART OF ACCOUNTS Problem 6 ASSETS REVENUE

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Six Adjusting Entries, Closing Entries, and Financial Analysis Page 1 Emory Legal Services, Incorporated CHART OF ACCOUNTS Problem 6 ASSETS REVENUE

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

4. A They increase retained earnings in the shareholders equity section. This is why we always credit revenues.

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

Adapted By Manik Hosen

Adapted By Manik Hosen Question: Who are the users of Accounting Information? Ans: The information that a user of accounting information needs depends upon the kinds of decisions the user makes. There

Adapted By Manik Hosen Question: Who are the users of Accounting Information? Ans: The information that a user of accounting information needs depends upon the kinds of decisions the user makes. There

Chapter 2. Ex a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit. Ex.

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

Chapter 2 Ex. 2 4 a. debit g. debit b. credit h. credit c. credit i. debit d. credit j. credit e. debit k. debit f. credit l. debit Ex. 2 5 1. debit and credit entries (c) 2. debit and credit entries (c)

CHAPTER3. Adjusting the Accounts. Apago PDF Enhancer. Study Objectives. Feature Story WHAT WAS YOUR PROFIT?

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

A. II. B. I. III. A. B.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Operating Decisions and the Income Statement

Operating Decisions and the Income Statement McGraw-Hill/Irwin Chapter 3 2009 The McGraw-Hill Companies, Inc. Understanding the Business How do business activities affect the income statement? How are

Operating Decisions and the Income Statement McGraw-Hill/Irwin Chapter 3 2009 The McGraw-Hill Companies, Inc. Understanding the Business How do business activities affect the income statement? How are

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

ACC 301 -S Extra Credit (20 points)

") ACC 301 -S1 2018 Extra Credit (20 points) Please review the ACC 213 material before completing this assignment. You can earn a total of 20 points for this assignment and these points will be counted as

ACC 301 -S1 2018 Extra Credit (20 points) Please review the ACC 213 material before completing this assignment. You can earn a total of 20 points for this assignment and these points will be counted as

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

GOLDEN RULES. 1.) The following are elements of financial statements:

The following are elements of financial statements:") GOLDEN RULES 1.) The following are elements of financial statements: Elements by which the financial position (assets = equity + liabilities) is measured: (1) Assets (2) Liabilities (3) Equity Elements

GOLDEN RULES 1.) The following are elements of financial statements: Elements by which the financial position (assets = equity + liabilities) is measured: (1) Assets (2) Liabilities (3) Equity Elements