Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

|

|

|

- Caitlin Walton

- 5 years ago

- Views:

Transcription

1 3-1

2 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2

3 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry rules. 3. Identify steps in the accounting cycle. 4. Record transactions in journals, post to ledger accounts, and prepare a trial balance. 5. Explain the reasons for preparing adjusting entries. 6. Prepare financial statement from the adjusted trial balance. 7. Prepare closing entries. 3-3

4 The Accounting Information System Accounting Information System The Accounting Cycle Financial Statements For Merchandisers 3-4 Basic terminology Debits and credits Accounting equation Financial statements and ownership structure Identifying and recording Journalizing Posting Trial balance Adjusting entries Adjusted trial balance Preparing financial statements Closing Post-closing trial balance Reversing entries Summary Income statement Statement of retained earnings Statement of financial position Closing entries

5 Accounting Information System Accounting Information System (AIS) Collects and processes transaction data. Disseminates the information to interested parties. 3-5

6 Accounting Information System Helps management answer such questions as: How much and what kind of debt is outstanding? Were sales higher this period than last? What assets do we have? What were our cash inflows and outflows? Did we make a profit last period? Are any of our product lines or divisions operating at a loss? Can we safely increase our dividends to shareholders? Is our rate of return on net assets increasing? 3-6

7 Basic Terminology Event Transaction Account Real Account Nominal Account Ledger Journal Posting Trial Balance Adjusting Entries Financial Statements Closing Entries 3-7 LO 1 Understand basic accounting terminology.

8 Debits and Credits An Account shows the effect of transactions on a given asset, liability, equity, revenue, or expense account. Double-entry entry accounting system (two-sided effect). Recording done by debiting at least one account and crediting another. DEBITS must equal CREDITS. 3-8 LO 2 Explain double-entry entry rules.

9 Debits and Credits Account An Account can be illustrated in a T-Account form. An arrangement that shows the effect of transactions on an account. Debit = Left Credit = Right Account Name Debit / Dr. Credit / Cr. 3-9 LO 2 Explain double-entry entry rules.

10 Debits and Credits If Debit entries are greater than Credit entries, the account will have a debit balance. Debit / Dr. Account Name Credit / Cr. Transaction #1 Transaction #3 $10,000 $3,000 Transaction #2 8,000 Balance $15, LO 2 Explain double-entry entry rules.

11 Debits and Credits If Credit entries are greater than Debit entries, the account will have a credit balance. Account Name Debit / Dr. Credit / Cr. Transaction #1 $10,000 $3,000 Transaction #2 8,000 Transaction #3 Balance $1, LO 2 Explain double-entry entry rules.

12 Debits and Credits Summary Normal Balance Debit Normal Balance Credit Debit / Dr. Liabilities Credit / Cr. Normal Balance Debit / Dr. Assets Credit / Cr. Chapter 3-24 Equity Debit / Dr. Credit / Cr. Normal Balance Normal Balance Chapter 3-23 Debit / Dr. Expense Credit / Cr. Chapter 3-25 Debit / Dr. Revenue Credit / Cr. Normal Balance Normal Balance Chapter 3-27 Chapter LO 2 Explain double-entry entry rules.

13 Debits and Credits Summary Statement of Financial Position Income Statement Asset = Liability + Equity Revenue - Expense = Debit Credit 3-13 LO 2 Explain double-entry entry rules.

14 The Accounting Equation Relationship among the assets, liabilities and equity of a business: Illustration 3-3 The equation must be in balance after every transaction. For every Debit there must be a Credit LO 2 Explain double-entry entry rules.

15 Double-Entry System Illustration 1. Owners invest $40,000 in exchange for share capital Assets = Liabilities + Equity + 40, , LO 2 Explain double-entry entry rules.

16 Double-Entry System Illustration 2. Disburse $600 cash for secretarial wages. Assets = Liabilities + Equity (expense) 3-16 LO 2 Explain double-entry entry rules.

17 Double-Entry System Illustration 3. Purchase office equipment priced at $5,200, giving a 10 percent promissory note in exchange. Assets = Liabilities + Equity + 5, , LO 2 Explain double-entry entry rules.

18 Double-Entry System Illustration 4. Received $4,000 cash for services rendered. Assets = Liabilities + Equity + 4, ,000 (revenue) 3-18 LO 2 Explain double-entry entry rules.

19 Double-Entry System Illustration 5. Pay off a short-term term liability of $7,000. Assets = Liabilities + Equity - 7,000-7, LO 2 Explain double-entry entry rules.

20 Double-Entry System Illustration 6. Declared a cash dividend of $5,000. Assets = Liabilities + Equity + 5,000-5, LO 2 Explain double-entry entry rules.

21 Double-Entry System Illustration 7. Convert a long-term liability of $80,000 into ordinary shares. Assets = Liabilities + Equity - 80, , LO 2 Explain double-entry entry rules.

22 Double-Entry System Illustration 8. Pay cash of $16,000 for a delivery van. Assets = Liabilities + Equity - 16, ,000 Note that the accounting equation equality is maintained after recording each transaction LO 2 Explain double-entry entry rules.

23 Financial Statements and Ownership Structure Ownership structure dictates the types of accounts that are part of the equity section. Proprietorship or Partnership Corporation Capital account Drawing account Share capital Share premium Dividends Retained Earnings 3-23 LO 2 Explain double-entry entry rules.

24 Financial Statements and Ownership Structure Statement of Financial Position Illustration 3-4 Equity Share Capital (Investment by shareholders) Retained Earnings (Net income retained in business) Dividends Net income or Net loss (Revenues less expenses) Income Statement Retained Earnings Statement 3-24 LO 2 Explain double-entry entry rules.

25 The Accounting Cycle Transactions Illustration Reversing entries 1. Journalization 8. Post-closing trail balance 2. Posting 7. Closing entries 3. Trial balance 6. Financial Statements Work Sheet 4. Adjustments 5. Adjusted trial balance 3-25 LO 3 Identify steps in the accounting cycle.

26 Identify and Recording Transactions What to Record? An item should be recognized in the financial statements if it is an element, is measurable, and is relevant and a faithful representation LO 3 Identify steps in the accounting cycle.

27 1. Journalizing General Journal a chronological record of transactions. Journal Entries are recorded in the journal. September 1: Shareholders invested $15,000 cash in the corporation in exchange for ordinary shares. Illustration LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

28 2. Posting Posting the process of transferring amounts from the journal to the ledger accounts. Illustration 3-7 Illustration LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

29 2. Posting Posting Transferring amounts from journal to ledger. Illustration LO 4

30 Expanded Example 2. Posting The purpose of transaction analysis is (1) to identify the type of account involved, and (2) to determine whether a debit or a credit is required. Keep in mind that every journal entry affects one or more of the following items: assets, liabilities, equity, revenues, or expense LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

31 1. October 1: Shareholders invest $100,000 cash in an advertising venture to be known as Pioneer Advertising Agency Inc. Oct Posting Cash 100,000 Illustration 3-9 Share capital - ordinary 100,000 Cash Share Capital - Ordinary Debit Credit Debit Credit 100, , LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

32 2. October 1: Pioneer Advertising purchases office equipment costing $50,000 by signing a 3-month, 12%, $50,000 note payable. Oct Posting Office equipment 50,000 Illustration 3-10 Notes payable 50,000 Office Equipment Debit Credit Debit Notes Payable Credit 50,000 50, LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

33 3. October 2: Pioneer Advertising receives a $12,000 cash advance from KC, a client, for advertising services that are expected to be completed by December 31. Oct Posting Cash 12,000 Illustration 3-11 Unearned service revenue 12,000 Cash Unearned Service Revenue Debit Credit Debit Credit 100,000 12,000 12, LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

34 2. Posting 4. October 3: Pioneer Advertising pays $9,000 office rent, in cash, for October. Illustration 3-12 Oct. 3 Rent expense 9,000 Cash 9,000 Cash Rent Expense Debit Credit Debit Credit 100,000 9,000 9,000 12, LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

35 2. Posting 5. October 4: Pioneer Advertising pays $6,000 for a one-year insurance policy that will expire next year on September 30. Oct. 4 Prepaid insurance 6,000 Illustration 3-13 Cash 6,000 Cash Prepaid Insurance Debit Credit Debit Credit 100,000 9,000 6,000 12,000 6, LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

36 6. October 5: Pioneer Advertising purchases, for $25,000 on account, an estimated 3-month supply of advertising materials from Aero Supply. Oct Posting Advertising supplies 25,000 Illustration 3-14 Accounts payable 25,000 Advertising Supplies Debit Credit Accounts Payable Debit Credit 25,000 25, LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

37 2. Posting 7. October 9: Pioneer Advertising signs a contract with a local newspaper for advertising inserts (flyers) to be distributed starting the last Sunday in November. Pioneer will start work on the content of the flyers in November. Payment of $7,000 is due following delivery of the Sunday papers containing the flyers. Illustration LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

38 2. Posting 8. October 20: Pioneer Advertising s board of directors declares and pays a $5,000 cash dividend to shareholders. Oct. 20 Dividends 5,000 Illustration 3-16 Cash 5,000 Cash Dividends Debit Credit Debit Credit 100,000 9,000 5,000 12,000 6,000 5, LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

39 2. Posting 9. October 26: Employees are paid every four weeks. The total payroll is $2,000 per day. The pay period ended on Friday, October 26, with salaries of $40,000 being paid. Oct. 26 Salaries expense 40,000 Illustration 3-17 Cash 40,000 Cash Salaries Expense Debit Credit Debit Credit 100,000 9,000 40,000 12,000 6,000 5,000 40, LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

40 10. October 31: Pioneer Advertising receives $28,000 in cash and bills Copa Company $72,000 for advertising services of $100,000 provided in October. Oct Posting Illustration 3-18 Cash 28,000 Accounts receivable 72,000 Service revenue 100,000 Cash Accounts Receivable Service Revenue Debit Credit Debit Credit Debit Credit ,000 9,000 72,000 12,000 28,000 80,000 6,000 5,000 40, ,000

41 3. Trial Balance Trial Balance A list of each account and its balance; used to prove equality of debit and credit balances. Illustration LO 4 Record transactions in journals, post to ledger accounts, and prepare a trial balance.

42 4. Adjusting Entries Makes it possible to: Report on the statement of financial position the appropriate assets, liabilities, and equity at the statement date. Report on the income statement the proper revenues and expenses for the period. Revenues are recorded in the period in which they are earned. Expenses are recognized in the period in which they are incurred LO 5 Explain the reasons for preparing adjusting entries.

43 Types of Adjusting Entries Illustration 3-20 Deferrals 1. Prepaid Expenses. Expenses paid in cash and recorded as assets before they are used or consumed. Accruals 3. Accrued Revenues. Revenues earned but not yet received in cash or recorded. 2. Unearned Revenues. Revenues received in cash and recorded as liabilities before they are earned. 4. Accrued Expenses. Expenses incurred but not yet paid in cash or recorded LO 5 Explain the reasons for preparing adjusting entries.

44 Adjusting Entries for Deferrals Deferrals are either prepaid expenses or unearned revenues. Illustration LO 5 Explain the reasons for preparing adjusting entries.

45 Adjusting Entries for Prepaid Expenses Payment of cash that is recorded as an asset because service or benefit will be received in the future. Cash Payment BEFORE Expense Recorded Prepayments often occur in regard to: insurance supplies advertising rent purchasing buildings and equipment 3-45 LO 5 Explain the reasons for preparing adjusting entries.

46 Adjusting Entries for Prepaid Expenses Supplies. Pioneer purchased advertising supplies costing $25,000 on October 5. Prepare the journal entry to record the purchase of the supplies. Oct. 5 Advertising supplies 25,000 Cash 25,000 Advertising Supplies Cash Debit Credit Debit Credit 25,000 25, LO 5 Explain the reasons for preparing adjusting entries.

47 Adjusting Entries for Prepaid Expenses Supplies. An inventory count at the close of business on October 31 reveals that $10,000 of the advertising supplies are still on hand. Oct. 31 Advertising supplies expense 15,000 Advertising supplies 15,000 Advertising Supplies Debit Credit Advertising Supplies Expense Debit Credit 25,000 15,000 15,000 10, LO 5 Explain the reasons for preparing adjusting entries.

48 Adjusting Entries for Prepaid Expenses Statement Presentation: Illustration 3-35 Advertising supplies identifies that portion of the asset s cost that will provide future economic benefit LO 5 Explain the reasons for preparing adjusting entries.

49 Adjusting Entries for Prepaid Expenses Statement Presentation: Illustration 3-34 Advertising expense identifies that portion of the asset s cost that expired in October LO 5 Explain the reasons for preparing adjusting entries.

50 Adjusting Entries for Prepaid Expenses Insurance. On Oct. 4 th, Pioneer paid $6,000 for a one-year fire insurance policy, beginning October 1. Show the entry to record the purchase of the insurance. Oct. 4 Prepaid insurance 6,000 Cash 6,000 Prepaid Insurance Cash Debit Credit Debit Credit 6,000 6, LO 5 Explain the reasons for preparing adjusting entries.

51 Adjusting Entries for Prepaid Expenses Insurance. An analysis of the policy reveals that $500 ($6,000 / 12) of insurance expires each month. Thus, Pioneer makes the following adjusting entry. Oct. 31 Insurance expense 500 Prepaid insurance 500 Prepaid Insurance Debit Credit Insurance Expense Debit Credit 6, , LO 5 Explain the reasons for preparing adjusting entries.

52 Adjusting Entries for Prepaid Expenses Statement Presentation: Illustration 3-35 Prepaid Insurance identifies that portion of the asset s cost that will provide future economic benefit LO 5 Explain the reasons for preparing adjusting entries.

53 Adjusting Entries for Prepaid Expenses Statement Presentation: Illustration 3-34 Insurance expense identifies that portion of the asset s cost that expired in October LO 5 Explain the reasons for preparing adjusting entries.

54 Adjusting Entries for Prepaid Expenses Depreciation. Pioneer Advertising estimates depreciation on its office equipment to be $400 per month. Accordingly, Pioneer recognizes depreciation for October by the following adjusting entry. Oct. 31 Depreciation expense 400 Accumulated depreciation 400 Depreciation Expense Debit Credit Accumulated Depreciation Debit Credit LO 5 Explain the reasons for preparing adjusting entries.

55 Adjusting Entries for Prepaid Expenses Statement Presentation: Illustration 3-35 Accumulated Depreciation is a contra asset account LO 5 Explain the reasons for preparing adjusting entries.

56 Adjusting Entries for Prepaid Expenses Statement Presentation: Illustration 3-34 Depreciation expense identifies that portion of the asset s cost that expired in October LO 5 Explain the reasons for preparing adjusting entries.

57 Adjusting Entries for Unearned Revenues Receipt of cash that is recorded as a liability because the revenue has not been earned. Cash Receipt BEFORE Revenue Recorded Unearned revenues often occur in regard to: rent airline tickets school tuition magazine subscriptions customer deposits 3-57 LO 5 Explain the reasons for preparing adjusting entries.

58 Adjusting Entries for Unearned Revenues Unearned Revenue. Pioneer Advertising received $12,000 on October 2 from KC for advertising services expected to be completed by December 31. Show the journal entry to record the receipt on Oct. 2 nd. Oct. 2 Cash 12,000 Unearned service revenue 12,000 Cash Unearned Service Revenue Debit Credit Debit Credit 12,000 12, LO 5 Explain the reasons for preparing adjusting entries.

59 Adjusting Entries for Unearned Revenues Unearned Revenues. Analysis reveals that Pioneer earned $4,000 of the advertising services in October. Thus, Pioneer makes the following adjusting entry. Oct. 31 Unearned service revenue 4,000 Service revenue 4,000 Service Revenue Debit Credit Unearned Service Revenue Debit Credit 100,000 4,000 12,000 4,000 8, LO 5 Explain the reasons for preparing adjusting entries.

60 Adjusting Entries for Unearned Revenues Statement Presentation: Illustration 3-35 Unearned service revenue identifies that portion of the liability that has not been earned LO 5 Explain the reasons for preparing adjusting entries.

61 Adjusting Entries for Unearned Revenues Statement Presentation: Illustration 3-34 Service revenue represents that portion of the liability that was earned in October LO 5 Explain the reasons for preparing adjusting entries.

62 Adjusting Entries for Accruals Accruals are either accrued revenues or accrued expenses. Illustration LO 5 Explain the reasons for preparing adjusting entries.

63 Adjusting Entries for Accrued Revenues Revenues earned but not yet received in cash or recorded. Adjusting entry results in: Revenue Recorded BEFORE Cash Receipt Accrued revenues often occur in regard to: rent interest services performed 3-63 LO 5 Explain the reasons for preparing adjusting entries.

64 Adjusting Entries for Accrued Revenues Accrued Revenues. In October Pioneer earned $2,000 for advertising services that it did not bill to clients before October 31. Thus, Pioneer makes the following adjusting entry. Oct. 31 Accounts receivable 2,000 Service revenue 2, Accounts Receivable Debit 72,000 2,000 74,000 Credit Service Revenue Debit Credit 100,000 4,000 2, ,000

65 Adjusting Entries for Accrued Revenues Statement Presentation Illustration Illustration 3-35 LO 5

66 Adjusting Entries for Accrued Expenses Expenses incurred but not yet paid in cash or recorded. Adjusting entry results in: Expense Recorded BEFORE Cash Payment Accrued expenses often occur in regard to: rent interest salaries taxes 3-66 LO 5 Explain the reasons for preparing adjusting entries.

67 Adjusting Entries for Accrued Expenses Accrued Interest. Pioneer signed a three-month, 12%, note payable in the amount of $50,000 on October 1. The note requires interest at an annual rate of 12 percent. Three factors determine the amount of the interest accumulation: Illustration LO 5 Explain the reasons for preparing adjusting entries.

68 Adjusting Entries for Accrued Expenses Accrued Interest. Pioneer signed a three-month, 12%, note payable in the amount of $50,000 on October 1. Prepare the adjusting entry on Oct. 31 to record the accrual of interest. Oct. 31 Interest expense 500 Interest payable 500 Interest Expense Debit Credit Interest Payable Debit Credit LO 5 Explain the reasons for preparing adjusting entries.

69 Adjusting Entries for Accrued Expenses Statement Presentation Illustration Illustration 3-35 LO 5

70 Adjusting Entries for Accrued Expenses Accrued Salaries. At October 31, the salaries for these days represent an accrued expense and a related liability to Pioneer. The employees receive total salaries of $10,000 for a five-day work week, or $2,000 per day LO 5 Explain the reasons for preparing adjusting entries.

71 Adjusting Entries for Accrued Expenses Accrued Salaries. Employees receive total salaries of $10,000 for a five-day work week, or $2,000 per day. Prepare the adjusting entry on Oct. 31 to record accrual for salaries. Oct. 31 Salaries expense 6,000 Salaries payable 6,000 Salaries Expense Debit Credit Salaries Payable Debit Credit 40,000 6,000 6,000 46, LO 5 Explain the reasons for preparing adjusting entries.

72 Adjusting Entries for Accrued Expenses Statement Presentation Illustration Illustration 3-35 LO 5

73 Adjusting Entries for Accrued Expenses Accrued Salaries. On November 23, Pioneer will again pay total salaries of $40,000. Prepare the entry to record the payment of salaries on November 23. Nov. 23 Salaries payable 6,000 Salaries expense 34,000 Cash 40,000 Salaries Expense Debit Credit Salaries Payable Debit Credit 34,000 6,000 6, LO 5 Explain the reasons for preparing adjusting entries.

74 Adjusting Entries for Accrued Expenses Bad Debts. Assume Pioneer reasonably estimates a bad debt expense for the month of $1,600. It makes the adjusting entry for bad debts as follows. Illustration LO 5 Explain the reasons for preparing adjusting entries.

75 5. Adjusted Trial Balance Shows the balance of all accounts, after adjusting entries, at the end of the accounting period. Illustration LO 5

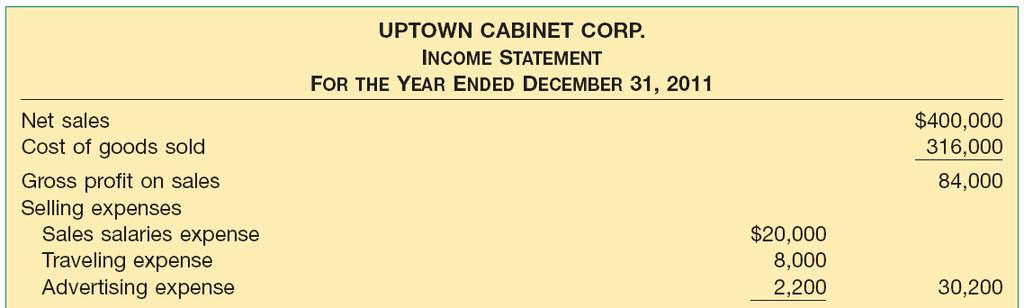

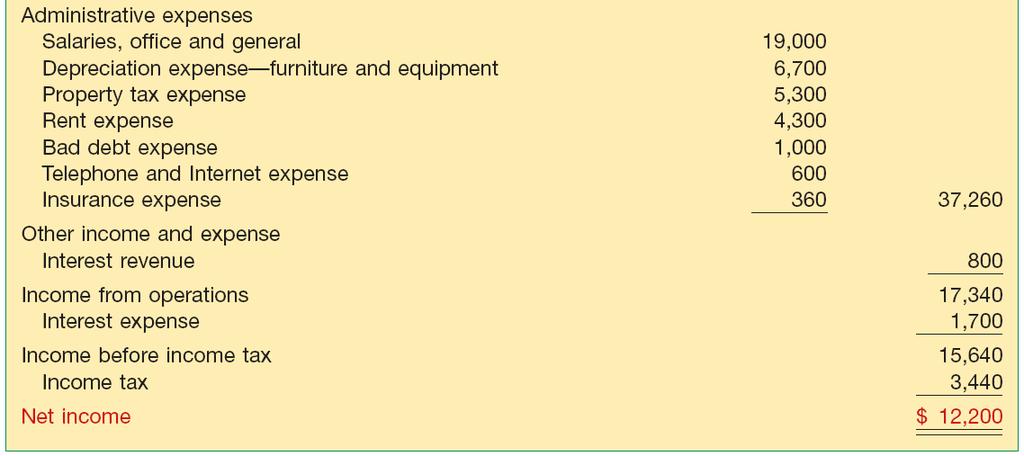

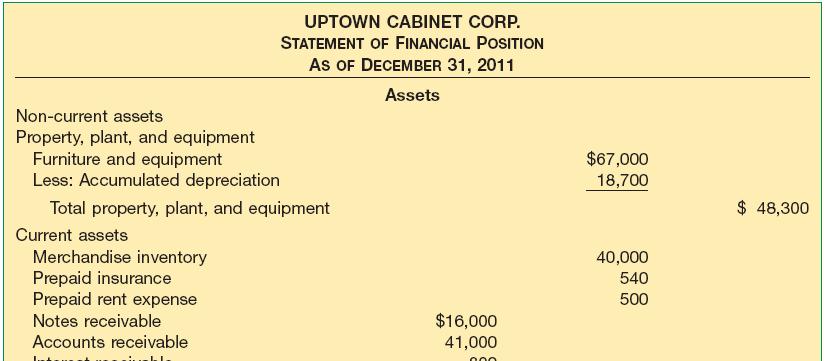

76 6. Preparing Financial Statements Financial Statements are prepared directly from the Adjusted Trial Balance. Income Statement Retained Earnings Statement Statement of Financial Position 3-76 LO 6 Prepare financial statement from the adjusted trial balance.

77 6. Preparing Financial Statements Illustration LO 6

78 6. Preparing Financial Statements Illustration LO 6

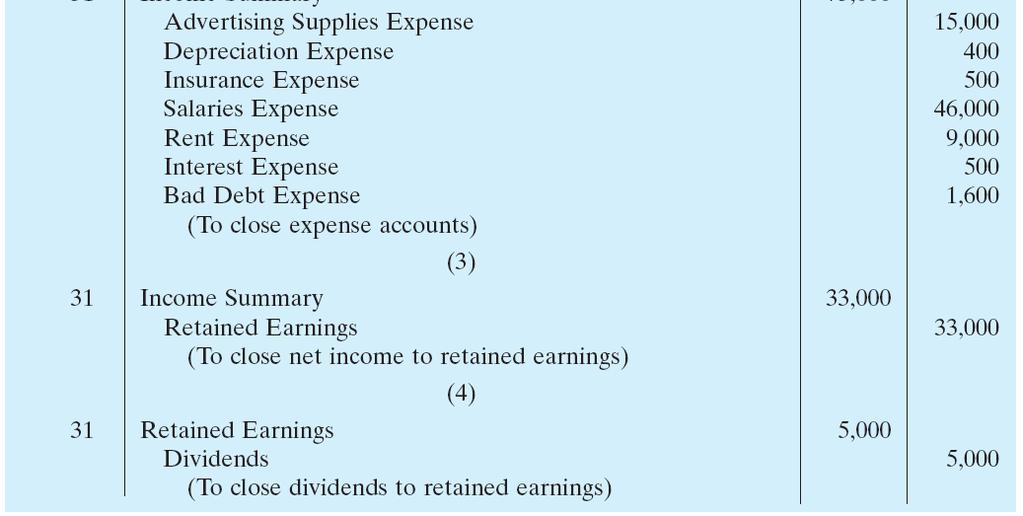

79 7. Closing Entries To reduce the balance of the income statement (revenue and expense) ) accounts to zero. To transfer net income or net loss to equity. Statement of financial position (asset, liability,, and equity) ) accounts are not closed. Dividends are closed directly to the Retained Earnings account LO 7 Prepare closing entries.

80 7. Closing Entries Illustration LO 7

81 7. Closing Entries Entries Illustration LO 7

82 8. Post-Closing Trial Balance Illustration LO 7 Prepare closing entries.

83 9. Reversing Entries After preparing the financial statements and closing the books, a company may reverse some of the adjusting entries before recording the regular transactions of the next period LO 7 Prepare closing entries.

84 Accounting Cycle Summarized 1. Enter the transactions of the period in appropriate journals. 2. Post from the journals to the ledger (or ledgers). 3. Take an unadjusted trial balance (trial balance). 4. Prepare adjusting journal entries and post to the ledger(s). 5. Take a trial balance after adjusting (adjusted trial balance). 6. Prepare the financial statements from the second trial balance. 7. Prepare closing journal entries and post to the ledger(s). 8. Take a trial balance after closing (post-closing trial balance). 9. Prepare reversing entries (optional) and post to the ledger(s) LO 7 Prepare closing entries.

85 Financial Statements for a Merchandising Company Illustration LO 7

86 Financial Statements of a Merchandising Company Illustration LO 7 Prepare closing entries.

87 Financial Statements of a Merchandising Company Illustration LO 7

88 Internal controls are a system of checks and balances designed to prevent and detect fraud and errors. Both of these actions are required under SOX. Companies find that internal control review is a costly process. One study estimates the cost for U.S. companies at over $35 billion, with audit fees doubling in the first year of compliance. The enhanced internal control standards apply only to large public companies listed on U.S. exchanges. There is continuing debate over whether foreign issuers should have to comply. 3-88

89 Most companies use accrual-basis accounting recognize revenue when it is earned and expenses in the period incurred, without regard to the time of receipt or payment of cash. Under the strict cash basis, companies record revenue only when they receive cash, and record expenses only when they disperse cash. Cash basis financial statements are not in conformity with IFRS LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

90 Illustration: Quality Contractor signs an agreement to construct a garage for $22,000. In January, Quality begins construction, incurs costs of $18,000 on credit, and by the end of January delivers a finished garage to the buyer. In February, Quality collects $22,000 cash from the customer. In March, Quality pays the $18,000 due the creditors. Illustration 3A LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

91 Illustration: Quality Contractor signs an agreement to construct a garage for $22,000. In January, Quality begins construction, incurs costs of $18,000 on credit, and by the end of January delivers a finished garage to the buyer. In February, Quality collects $22,000 cash from the customer. In March, Quality pays the $18,000 due the creditors. Illustration 3A LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

92 Conversion From Cash Basis To Accrual Basis Illustration: Dr. Diane Windsor, like many small business owners, keeps her accounting records on a cash basis. In the year 2010, Dr. Windsor received $300,000 from her patients and paid $170,000 for operating expenses, resulting in an excess of cash receipts over disbursements of $130,000 ($300,000 - $170,000). At January 1 and December 31, 2010, she has accounts receivable, unearned service revenue, accrued liabilities, and prepaid expenses as shown in Illustration 3A-5. Illustration 3A LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

93 Conversion From Cash Basis To Accrual Basis Illustration: Calculate service revenue on an accrual basis. Illustration 3A-8 Illustration 3A LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

94 Conversion From Cash Basis To Accrual Basis Illustration: Calculate operating expenses on an accrual basis. Illustration 3A-11 Illustration 3A LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

95 Conversion From Cash Basis To Accrual Basis Illustration 3A LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

96 Theoretical Weaknesses of the Cash Basis Today s economy is considerably more lubricated by credit than by cash. The accrual basis, not the cash basis, recognizes all aspects of the credit phenomenon. Investors, creditors, and other decision makers seek timely information about an enterprise s future cash flows LO 8 Differentiate the cash basis of accounting from the accrual basis of accounting.

97 Illustration of Reversing Entries Accruals Illustration 3B LO 9 Identifying adjusting entries that may be reversed.

98 Illustration of Reversing Entries Deferrals Illustration 3B LO 9 Identifying adjusting entries that may be reversed.

99 Summary of Reversing Entries 1. All accruals should be reversed. 2. All deferrals for which a company debited or credited the original cash transaction to an expense or revenue account should be reversed. 3. Adjusting entries for depreciation and bad debts are not reversed. Recognize that reversing entries do not have to be used. Therefore, some accountants avoid them entirely LO 9 Identifying adjusting entries that may be reversed.

100 A company prepares a worksheet either on columnar paper or within an electronic spreadsheet. A company uses the worksheet to adjust account balances and to prepare financial statements LO 10 Prepare a 10-column worksheet.

101 Worksheet Columns A company prepares a worksheet either on columnar paper or within an electronic spreadsheet LO 10 Prepare a 10-column worksheet.

102 Adjusted Trial Balance Illustration 3C-1 LO 10 Prepare a 10-column worksheet.

103 Preparing Financial Statements from a Worksheet The Worksheet: Provides information needed for preparation of the financial statements. Sorts data into appropriate columns, which facilitates the preparation of the statements LO 10 Prepare a 10-column worksheet.

104 Illustration LO 10

105 Illustration LO 10 Prepare a 10-column worksheet.

106 Illustration LO 10

107 Copyright Copyright 2011 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM

C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM 3-1 Intermediate Accounting IFRS Edition Presented By: Ratna Candra Sari Email: ratna_candrasari@uny.ac.id Learning Objectives 1. Understand basic accounting

C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM 3-1 Intermediate Accounting IFRS Edition Presented By: Ratna Candra Sari Email: ratna_candrasari@uny.ac.id Learning Objectives 1. Understand basic accounting

CHAPTER 3 Selected Solutions. The Accounting Information System. Brief Topics Questions Exercises Exercises Problems

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

The Recording Process

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

PREVIEW OF CHAPTER 5-2

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS. Balance Sheet and Statement of of Cash Flows. Usefulness of the Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

TH E ACCO U NTI NG LEARNING OBJECTIVES. Needed: A Reliable Information System. After studying this chapter, you should be able to:

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

The Recording Process

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Chapter 2 Review of the Accounting Process

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

Accounting for Receivables

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

Accounting for Receivables

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3)

") MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Accounting in Action. Chapter 1. Learning Objectives. After studying this chapter, you should be able to:

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

3. Balance sheet accounts are referred to as temporary accounts because their balances are always changing.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

PREVIEW OF CHAPTER 24

24-1 PREVIEW OF CHAPTER 24 24-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield Presentation and 24 Disclosure in Financial Reporting LEARNING OBJECTIVES After studying this chapter,

24-1 PREVIEW OF CHAPTER 24 24-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield Presentation and 24 Disclosure in Financial Reporting LEARNING OBJECTIVES After studying this chapter,

PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

Chapter 3 The Adjusting Process

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

CHAPTER 3. Adjusting the Accounts 6, 7 1 8, 9, 10, 11, 12, 13, 18, 19, , 18 6A 12, 13 14, 15

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Explain the time period assumption. *2. Explain

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Explain the time period assumption. *2. Explain

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Week 3. Topic 3 Chapter 3. ACT102 Introduction to Accounting. Accounting for end of financial period adjustments 21/02/2018

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

1. Paid rent for the next three months. 2. Paid property taxes that have already been accrued. 3. Declared cash dividends on commonshares

02 Student: 1. Paid rent for the next three months. 2. Paid property taxes that have already been accrued. 3. Declared cash dividends on commonshares 4. Closed the income summary account, assuming there

02 Student: 1. Paid rent for the next three months. 2. Paid property taxes that have already been accrued. 3. Declared cash dividends on commonshares 4. Closed the income summary account, assuming there

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

Chapter 6 Accounting Adjustments and Working papers

Chapter 6 Accounting Adjustments and Working papers Topics 1. Cash basis vs. Accrual Basis 2. Accrued Income 3. Accrued Expenses 4. Prepaid Expenses 5. Unearned Income 6. Depreciation 7. Supply Expenses

Chapter 6 Accounting Adjustments and Working papers Topics 1. Cash basis vs. Accrual Basis 2. Accrued Income 3. Accrued Expenses 4. Prepaid Expenses 5. Unearned Income 6. Depreciation 7. Supply Expenses

Liabilities. Chapter 10. Learning Objectives. After studying this chapter, you should be able to:

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

PREVIEW OF CHAPTER 14-2

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

CHAPTER 3 Adjusting the Accounts

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

Investments. 1. Discuss why corporations invest in debt and share securities.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

CHAPTER3. Adjusting the Accounts. Apago PDF Enhancer. Study Objectives. Feature Story WHAT WAS YOUR PROFIT?

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

PREVIEW OF CHAPTER 20-2

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 3 Adjusting the Accounts 高立翰

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

Chapter 17 Accounting for Accruals and Deferrals

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

Learning Outcomes. The Basic Accounting Cycle

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

download from https://testbankgo.eu/p/

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION

FINAL EXAMINATION") Canadian International Matriculation Programme Sunway College FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION Date : 5 December 2017 Time Length Lecturer : 8:30 a.m. 10:30 a.m. : 2 hours : Ms

Canadian International Matriculation Programme Sunway College FINANCIAL ACCOUNTING PRINCIPLES (BAT4M) FINAL EXAMINATION Date : 5 December 2017 Time Length Lecturer : 8:30 a.m. 10:30 a.m. : 2 hours : Ms

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Seminar on Bookkeeping Basics

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Fin621 Online Quizzes & Papers GURU

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

Introduction to Fund Accounting

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

PREVIEW OF CHAPTER Slide 4-2

4-1 PREVIEW OF CHAPTER 4 4-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 4 Related Information Income Statement and LEARNING OBJECTIVES After studying this chapter, you should

4-1 PREVIEW OF CHAPTER 4 4-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 4 Related Information Income Statement and LEARNING OBJECTIVES After studying this chapter, you should

Accounting I Class Schedule

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Chapter 11. Notes, Bonds, and Leases

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Composed & Solved Hafiz Salman Majeed

FINALTERM EXAMINATION Fall 2008 MGT101- Financial Accounting (Session - 4) Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset

FINALTERM EXAMINATION Fall 2008 MGT101- Financial Accounting (Session - 4) Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

Twin Valley School District. What is the purpose and importance of accounting? Who are the users of accounting information?

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

ACCOUNTING 201. PRACTICE MIDTERM - (Covering Chapters 1-5)

") Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 11. Corporations: Organization, Share Transactions, Dividends, and Retained Earnings. Learning Objectives

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

1-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

Chapter

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Class: XI Subject: ACCOUNTANCY. NO OF PERIOD Unit-1 (25 periods) LEARNING OUTCOMES

LEARNING OUTCOMES") Unit-1 (25 CH-1. Introduction to Accounting - Project on Accounting: objectives, advantages and International limitations, types of accounting information; Accounting users of accounting information and

Unit-1 (25 CH-1. Introduction to Accounting - Project on Accounting: objectives, advantages and International limitations, types of accounting information; Accounting users of accounting information and

Instructions Identify each statement as true or false. If false, indicate how to correct the statement.

CHAPTER 3 EXERCISES: SET B E3-1B Maria Diaz has prepared the following list of statements about the time period assumption. 1. Adjusting entries are necessary only if a company has made accounting errors.

CHAPTER 3 EXERCISES: SET B E3-1B Maria Diaz has prepared the following list of statements about the time period assumption. 1. Adjusting entries are necessary only if a company has made accounting errors.

PREVIEW OF CHAPTER 2-2

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

Full file at

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete