COMPLETING THE ACCOUNTING CYCLE

|

|

|

- Anissa Palmer

- 6 years ago

- Views:

Transcription

1 Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

2 4-2 P 1 BENEFITS OF A WORK SHEET Aids the preparation of financial statements. Reduces possibility of errors. Links accounts and their adjustments. Not a required report. Assists in planning and organizing an audit. Helps in preparing interim financial statements. Shows the effects of proposed transactions.

3 P 1 FastForward Worksheet For the Month Ended December 31,

4 P 1 FastForward Worksheet For the Month Ended December 31,

5 P 1 FastForward Worksheet For the Month Ended December 31,

6 P 1 FastForward Worksheet For the Month Ended December 31,

7 P 1 FastForward Worksheet For the Month Ended December 31,

8 4-8 P 1 PREPARING THE FINANCIAL STATEMENTS

9 4-9 P 1 PREPARING THE FINANCIAL STATEMENTS

10 4-10 C 1 RECORDING CLOSING ENTRIES 1. Resets revenue, expense and withdrawal account balances to zero at the end of the period. 2. Helps summarize a period s revenues and expenses in the Income Summary account. Identify accounts for closing. Record and post closing entries. Prepare post-closing trial balance.

11 4-11 C 1 TEMPORARY AND PERMANENT ACCOUNTS Revenues Assets Expenses Temporary Accounts Withdrawals Liabilities Permanent Accounts Owner s Capital Income Summary The closing process applies only to temporary accounts.

12 4-12 P 2 RECORDING CLOSING ENTRIES Close Credit Balances in Revenue Accounts to Income Summary. Close Debit Balances in Expense accounts to Income Summary. Close Income Summary account to Owner s Capital. Close Withdrawals to Owner s Capital. Let s see how the closing process works!

13 P FastForward Adjusted Trial Balance December 31, 2011 Debit Credit Cash $ 4,350 Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-equip. $ 375 Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 7,850 Rental revenue 300 Depreciation expense-equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals $ 47,685 $ 47,685 Using the adjusted trial balance, let s prepare the closing entries for FastForward.

14 P FastForward Adjusted Trial Balance December 31, 2011 Debit Credit Cash $ 4,350 Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-equip. $ 375 Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 7,850 Rental revenue 300 Depreciation expense-equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals $ 47,685 $ 47,685 Close Credit Balances in Revenue Accounts to Income Summary.

15 4-15 P 2 CLOSE CREDIT BALANCES IN REVENUE ACCOUNTS TO INCOME SUMMARY Dr. Cr. Dec. 31 Consulting revenue 7,850 Rental revenue 300 Income summary 8,150 Now, let s look at the ledger accounts after posting this closing entry.

16 4-16 P 2 CLOSE CREDIT BALANCES IN REVENUE ACCOUNTS TO INCOME SUMMARY Consulting Revenue 7,850 7,850 - Income Summary 8,150 Rental Revenue

17 P 2 FastForward Adjusted Trial Balance December 31, 2011 Debit Credit Cash $ 4,350 Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-equip. $ 375 Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 7,850 Rental revenue 300 Depreciation expense-equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals $ 47,685 $ 47, Close Debit Balances in Expense Accounts to Income Summary.

18 4-18 P 2 CLOSE DEBIT BALANCES IN EXPENSE ACCOUNTS TO INCOME SUMMARY Dr. Cr. Dec. 31 Income summary 4,365 Depreciation expense-equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Now, let s look at the ledger accounts after posting this closing entry.

19 4-19 P 2 CLOSE DEBIT BALANCES IN EXPENSE ACCOUNTS TO INCOME SUMMARY Depreciation Expense- Eq Rent Expense 1,000 1,000 - Salaries Expense 1,610 1,610 - Supplies Expense 1,050 1,050 - Income Summary 4,365 8,150 3,785 Insurance Expense Utilities Expense Net Income

20 P 2 FastForward Adjusted Trial Balance December 31, 2011 Debit Credit Cash $ 4,350 Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-equip. $ 375 Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 7,850 Rental revenue 300 Depreciation expense-equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals $ 47,685 $ 47, Close Income Summary to Owner s Capital.

21 P 2 CLOSE INCOME SUMMARY TO OWNER S CAPITAL 4-21 Dr. Cr. Dec. 31 Income summary 3,785 C. Taylor, Capital 3,785 Now, let s look at the ledger accounts after posting this closing entry.

22 4-22 P 2 CLOSE INCOME SUMMARY TO OWNER S CAPITAL C. Taylor, Capital 30,000 3,785 33,785 Income Summary 4,365 8,150 3,785 -

23 P FastForward Adjusted Trial Balance December 31, 2011 Debit Credit Cash $ 4,350 Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-equip. $ 375 Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 7,850 Rental revenue 300 Depreciation expense-equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals $ 47,685 $ 47,685 Close Withdrawals Account to Owner s Capital.

24 P 2 CLOSE WITHDRAWALS ACCOUNT TO OWNER S CAPITAL 4-24 Dr. Cr. Dec. 31 C. Taylor, Capital 200 C. Taylor, Withdrawals 200 Now, let s look at the ledger accounts after posting this closing entry.

25 4-25 P 2 CLOSE WITHDRAWALS ACCOUNT TO OWNER S CAPITAL C. Taylor, Withdrawals C. Taylor, Capital ,000 3,785 33,585

26 4-26 SUMMARY OF THE CLOSING PROCESS 1. Close Credit Balances in Revenue Accounts to Income Summary. 2. Close Debit Balances in Expense Accounts to Income Summary. 3. Close Income Summary to Owner s Capital. 4. Close Withdrawals Account to Owner s Capital.

27 4-27 P 3 POST-CLOSING TRIAL BALANCE List of permanent accounts and their balances after posting closing entries. Let s look at FastForward s post-closing trial balance. Total debits and credits must be equal.

28 4-28 P 3 POST-CLOSING TRIAL BALANCE FastForward Post-Closing Trial Balance December 31, 2011 Debit Credit Cash $ 4,350 Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-equip. $ 375 Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 33,585 C. Taylor, Withdrawals - Consulting revenue - Rental revenue - Depreciation expense-equipment - Salaries expense - Insurance expense - Rent expense - Supplies expense - Utilities expense - Totals $ 43,120 $ 43,120

29 4-29 C 2 ACCOUNTING CYCLE

30 4-30 C 3 CLASSIFIED BALANCE SHEET Categories of a Classified Balance Sheet Assets Liabilities and Equity Current assets Current liabilities Noncurrent assets Noncurrent liabilities Long-term investments Equity Plant assets Intangible assets Current items are those expected to come due (both collected and owed) within the longer of one year or the company s normal operating cycle.

31 4-31 C 3 Current assets are expected to be sold, collected, or used within one year or the company s operating cycle.

32 4-32 C 3 Long-term investments are expected to be held for more than one year or the operating cycle.

33 4-33 C 3 Plant assets are tangible long-lived assets used to produce or sell products and services.

34 4-34 C 3 Intangible assets are long-term resources used to produce or sell products and services and that lack physical form.

35 4-35 C 3 Current liabilities are obligations due within the longer of one year or the company s operating cycle.

36 4-36 C 3 Long-term liabilities are obligations not due within the longer of one year or the company s operating cycle.

37 4-37 C 3 Equity is the owner s claim on the assets.

the company owns or controls")

the item can be reliably measured.")

the obligation")

38 4-38 GLOBAL VIEW The definition of an asset is similar under U.S. GAAP and IFRS and involves three basic criteria: (1)the company owns or controls the right to use the item, (2)the right arises from a past transaction or event, and (3)the item can be reliably measured. Both systems define the initial asset value as historical cost for nearly all assets. The definition of a liability is similar under U.S. GAAP and IFRS and involves three basic criteria: (1) the item is a present obligation requiring a probable future resource outlay, (2) the obligation arises from a past transaction or event, and (3) the obligation can be reliably measured.

39 4-39 A 1 CURRENT RATIO Helps assess the company s ability to pay its debts in the near future Current Ratio = Current Assets Current Liabilities Limited Brands, Inc. $ in millions Current assets $ 2,867 $ 2,919 $ 2,771 $ 2,784 Current liabilities 1,225 1,374 1,709 1,575 Current ratio Industry current ratlo

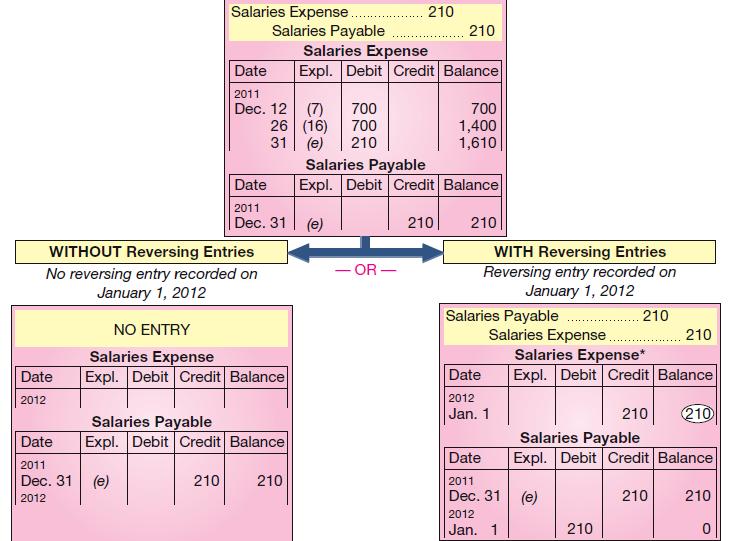

40 4-40 P 4 4A REVERSING ENTRIES Reversing entries are optional. They are recorded in response to accrued assets and accrued liabilities that were created by adjusting entries at the end of a reporting period. The purpose of reversing entries is to simplify a company s recordkeeping. Let s see how the accounting for our payroll accrual will be handled with and without reversing entries.

41 P

42 4-42 P 4 Without Reversing Entries With Reversing Entries

43 END OF CHAPTER

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

COST-VOLUME-PROFIT ANALYSIS

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

STATEMENT OF CASH FLOWS

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

INVESTMENTS AND INTERNATIONAL OPERATIONS

15-1 Chapter 15 INVESTMENTS AND INTERNATIONAL OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D.,

15-1 Chapter 15 INVESTMENTS AND INTERNATIONAL OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D.,

Income and Changes in Retained Earnings

Income and Changes in Retained Earnings Chapter 12 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney,

Income and Changes in Retained Earnings Chapter 12 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney,

Flexible Budgets and Performance Analysis

Flexible Budgets and Performance Analysis Chapter 9 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

Flexible Budgets and Performance Analysis Chapter 9 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

ACCOUNTING FOR CORPORATIONS

Chapter 13 ACCOUNTING FOR CORPORATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok,

Chapter 13 ACCOUNTING FOR CORPORATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok,

COST-VOLUME-PROFIT ANALYSIS

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2015

Chapter 22 COST-VOLUME-PROFIT ANALYSIS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2015

Capital Budgeting Decisions

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

Profit Planning. Learning Objective 1. organizations budget and the processes they

Learning Objective 1 Profit Planning Chapter 07 Understand d why organizations budget and the processes they use to create budgets. PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell,

Learning Objective 1 Profit Planning Chapter 07 Understand d why organizations budget and the processes they use to create budgets. PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell,

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Cost-Volume-Profit Relationships

Cost-Volume-Profit Relationships Chapter 05 Learning Objective 1 Explain how changes in activity affect contribution margin and net operating income. PowerPoint Authors: Susan Coomer Galbreath, Ph.D.,

Cost-Volume-Profit Relationships Chapter 05 Learning Objective 1 Explain how changes in activity affect contribution margin and net operating income. PowerPoint Authors: Susan Coomer Galbreath, Ph.D.,

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

Accounting for Business Transactions QUESTIONS

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

Financial and Managerial Accounting 7th Edition Wild Solutions Manual Full Download: http://testbanklive.com/download/financial-and-managerial-accounting-7th-edition-wild-solutions-manual/ Chapter 2 Accounting

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Chapter 6 The annual report and accounts. The closure of the accounting cycle and Accounting information disclosed to the public

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Learning Outcomes. The Basic Accounting Cycle

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

THE ACCOUNTING CYCLE: Accruals and Deferrals

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Lesson 4. Lesson 4. Cash. Beg. Balance End. Balance. 30 Liability. Accounting Cycle Part Stephen's Sweet Shop Trial Balance

Lesson 4 Financial Accounting (Information useful to investors and creditors.) The primary tool for investors and creditors are the financial statements to be prepared in accordance with generally accepted

Lesson 4 Financial Accounting (Information useful to investors and creditors.) The primary tool for investors and creditors are the financial statements to be prepared in accordance with generally accepted

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts:

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

The Accounting Cycle Revised Edition

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Chapter 4 Completing the Accounting Cyclt 163

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM. MULTIPLE CHOICE Conceptual. Test Bank Chapter 3

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

Chapter 02 Analyzing and Recording Transactions

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

Financial Accounting Information For Decisions 6th Edition Wild Chapter 02 Analyzing and Recording Transactions Student Learning Objectives and Related Assignment Materials* Student Learning Objectives

Week 5, Chap 4 Part 1

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Graded Project. Lesson 1: Business Accounting and You OVERVIEW INSTRUCTIONS

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

Accounting I. StraighterLine does not apply letter grades. Students earn a score as a percentage of 100%. A passing percentage is 70% or higher.

Accounting I Course Text Wild, John J., Kermit D. Larson, and Barbara Chiapetta. Fundamental Accounting Principles, Volume 1, 18th edition. McGraw-Hill/Irwin, 2007. ISBN 0-07-328661-3 Course Description

Accounting I Course Text Wild, John J., Kermit D. Larson, and Barbara Chiapetta. Fundamental Accounting Principles, Volume 1, 18th edition. McGraw-Hill/Irwin, 2007. ISBN 0-07-328661-3 Course Description

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Chapter 3 The Adjusting Process

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

CHAPTER 3 Selected Solutions. The Accounting Information System. Brief Topics Questions Exercises Exercises Problems

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

Text. Stay focused and keep doing what you believe in Melody Kulp (second from left; David Reinstein is on the far left)

") Stay focused and keep doing what you believe in Melody Kulp (second from left; David Reinstein is on the far left) 3 Adjusting Accounts and A Look Back Chapter 2 explained the analysis and recording of

Stay focused and keep doing what you believe in Melody Kulp (second from left; David Reinstein is on the far left) 3 Adjusting Accounts and A Look Back Chapter 2 explained the analysis and recording of

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

REPORTING AND INTERPRETING LIABILITIES

REPORTING AND INTERPRETING LIABILITIES Chapter 9 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Slide Inc. 1 UNDERSTANDING THE BUSINESS The acquisition of assets is financed from two sources: Debt -

REPORTING AND INTERPRETING LIABILITIES Chapter 9 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Slide Inc. 1 UNDERSTANDING THE BUSINESS The acquisition of assets is financed from two sources: Debt -

Heintz & Parry. 20 th Edition. College Accounting

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything!

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

The Accounting Cycle Reporting Financial i Results

51 52 The Accounting Cycle Reporting Financial i Results Chapter 5 To prepare an income statement, a statement of retained earnings, and a balance sheet. LO1 Adjusted Trial Balance Cash $ 3,925 Accounts

51 52 The Accounting Cycle Reporting Financial i Results Chapter 5 To prepare an income statement, a statement of retained earnings, and a balance sheet. LO1 Adjusted Trial Balance Cash $ 3,925 Accounts

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

10. Describe an account and its use in recording transactions.

1MODULE learning objective Accounting in Business, Analyzing Transactions, and Preparing Journal 10. Describe an account and its use in recording transactions. 1. THE ACCOUNT AND ITS ANALYSIS An account

1MODULE learning objective Accounting in Business, Analyzing Transactions, and Preparing Journal 10. Describe an account and its use in recording transactions. 1. THE ACCOUNT AND ITS ANALYSIS An account

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Total Assets 4,945,738

Web-GAAP Training School District Initial Year Governmental Fund Trial Balance For the Fiscal Year Ended June 30, 2000 Balance Sheet Debit Credit Fund: General ASSETS: Equity in Pooled Cash and Cash Equivalents

Web-GAAP Training School District Initial Year Governmental Fund Trial Balance For the Fiscal Year Ended June 30, 2000 Balance Sheet Debit Credit Fund: General ASSETS: Equity in Pooled Cash and Cash Equivalents

True / False Questions

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

CHAPTER 8 REVIEW EXERCISES (continued) Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE

Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE") Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

(Accrual and Prepayment)

") Accrual and Prepayment Longman Question 13 The following balances were extracted from the ledgers of Mr Ko at 31 March 2014: $ Telephone 12,355 Dr Rent and rates 55,000 Dr Loan to Bob 450,000 Dr Rental

Accrual and Prepayment Longman Question 13 The following balances were extracted from the ledgers of Mr Ko at 31 March 2014: $ Telephone 12,355 Dr Rent and rates 55,000 Dr Loan to Bob 450,000 Dr Rental

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

SOLUTIONS. Learning Goal 13

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

Understanding Accounting and Financial Information

Chapter Seventeen Understanding Accounting and Financial Information McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. SEAN PERICH Bakery Barn A lifelong weightlifter

Chapter Seventeen Understanding Accounting and Financial Information McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. SEAN PERICH Bakery Barn A lifelong weightlifter