After studying this chapter, you should be able to: adjusted account balances.

|

|

|

- Brittany McDonald

- 5 years ago

- Views:

Transcription

1 4 Completing the Accounting Cycle 1

2 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and financial statements. 2. Prepare financial statements from adjusted account balances. 3. Prepare closing entries. 2

3 After studying this chapter, you should be able to: 4. Describe the accounting cycle. 5. Illustrate the accounting cycle for one period. 6. Explain what is meant by the fiscal year and the natural business year. 3

4 4-1 Objective 1 Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and financial statements. 4

5 4-1 5

6 4-1 Spreadsheet (Work Sheet) Trial Balance Adjustments Adjusted TB Accounts Dr Cr Dr Cr Dr Cr Accounts are listed in the Trial Balance column using the ending balance found in the general ledger. 6

7 4-1 Spreadsheet (Work Sheet) Trial Balance Adjustments Adjusted TB Accounts Dr Cr Dr Cr Dr Cr Adjustments are entered here. Two possibilities: 1. Deferrals Existing balances are changed. 2. Accruals New information is entered. 7

8 4-1 Spreadsheet (Work Sheet) Trial Balance Adjustments Adjusted TB Accounts Dr Cr Dr Cr Dr Cr Adjustments are combined with the trial balance. Account balances are now adjusted. 8

9 4-1 Spreadsheet (Work Sheet) Adjusted TB Income State. Balance Sheet Accounts Dr Cr Dr Cr Dr Cr Revenue and expense balances in the Adjusted Trial Balance column are extended to the Income Statement column. 9

10 4-1 Spreadsheet (Work Sheet) Adjusted TB Income State. Balance Sheet Accounts Dr Cr Dr Cr Dr Cr Asset, liability, owner s equity, and drawing balances in the Adjusted Trial Balance column are extended to the Balance Sheet column. 10

11 4-1 Example Exercise 4-1 The balances for the accounts listed below appear in the Adjusted Trial Balance columns of the end-of-period spreadsheet (work sheet). Indicate whether each balance should be extended to (a) an Income Statement column or (b) a Balance Sheet column. 1. Amber Bablock, Drawing 2. Utilities Expense 3. Accumulated Depreciation Equipment 4. Unearned Rent 5. Fees Earned 6. Accounts Payable 7. Rent Revenue 8. Supplies 11

12 4-1 Follow My Example Balance Sheet column 2. Income Statement column 3. Balance Sheet column 4. Balance Sheet column 5. Income Statement column 6. Balance Sheet column 7. Income Statement column 8. Balance Sheet column For Practice: PE 4-1A, PE 4-1B 12

13 4-2 Objective 2 Prepare financial statements from adjusted account balances. 13

14 4-2 To balance sheet 14 14

15 (Concluded) 4-2 From statement of owner equity 15 15

16 4-2 Example Exercise 4-2 In the Balance Sheet columns of the end-of-period spreadsheet (work sheet) for Dimple Consulting Co. for the current year, the Debit column total is $678,450, and the Credit column total is $599,750 before the amount of net income or net loss has been included. In preparing the income statement from the end-of-period spreadsheet (work sheet), what is the amount of net income or net loss? 16

17 4-2 Follow My Example 4-2 A net income of $78,700 ($678,450 $599,750) would be reported. When the Debit column of the Balance Sheet columns is more than the Credit column, net income is reported. If the Credit column exceeds the Debit column, a net loss is reported. For Practice: PE 4-2A, PE 4-2B 17

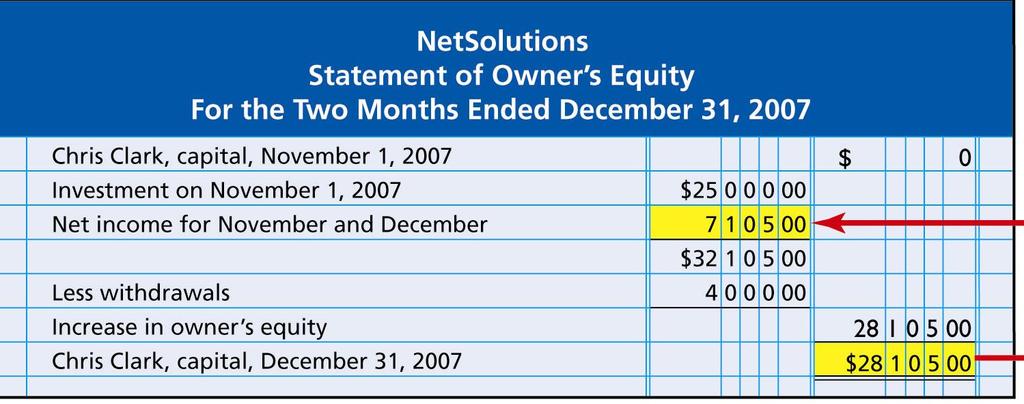

18 4-2 Example Exercise 4-3 Zack Gaddis owns and operates Gaddis Employment Services. On January 1, 2007, Zack Gaddis, Capital had a balance of $186,000. During the year, Zack invested an additional $40,000 and withdrew $25,000. For the year ended December 31, 2007, Gaddis Employment Services reported a net income of $18,750. Prepare a statement of owner s equity for the year ended December 31,

19 4-2 Follow My Example 4-3 GADDIS EMPLOYMENT SERVICES STATEMENT OF OWNER S EQUITY For the Year Ended December 31, 2007 Zack Gaddis, capital, January 1, 2007 $186,000 Additional investment during ,000 Total $226,000 Withdrawals $ 25,000 Less net income 18,750 Decrease in owner s equity 6,250 Zack Gaddis, capital, December 31, 2007 $219,750 For Practice: PE 4-3A, PE 4-3B 19

20 4-2 A classified balance sheet is a balance sheet that was expanded by adding subsections for current assets; property, plant, and equipment; and current liabilities. 20

21 4-2 Cash and other assets that are expected to be converted into cash, sold or used up usually within a year or less, through the normal operations of the business are called current assets. Cash Accounts Receivable Supplies 21

22 4-2 Notes receivable are written promises by the customer to pay the amount of the note and possibly interest at an agreed rate. 22

23 4-2 Property, plant, and equipment (also called fixed assets) include assets that depreciate over a period of time. Land is an exception as it is not subject to depreciation. Equipment Machinery Buildings Land 23

24 4-2 Liabilities that will be due within a short time (usually one year or less) and that are to be paid out of current assets are called current liabilities. Accounts payable Wages payable Interest payable Unearned fees 24

25 4-2 Liabilities not due for a long time (usually more than one year) are long-term liabilities. Notes payable Mortgage payable Bond payable 25

26 4-2 Owner s equity is the owner s right to the assets of the business. Owner s equity is added to the total liabilities, and the total must be equal to the total assets. 26

27 4-2 Example Exercise 4-4 The following accounts appear in the adjusted trial balance of Hindsight Consulting. Indicate whether each account would be reported in the (a) current asset; (b) property, plant, and equipment; (c) current liability, (d) long-term liability; or (e) owner s equity section of the December 31, 2007 balance sheet of Hindsight Consulting. 1. Jason Corbin, Capital 5. Cash 2. Notes Receivable (due 6. Unearned Rent in 6 months) months) 3. Notes Payable (due in 7. Accumulated Depr. 2009) Equipment 4. Land 8. Accounts Payable 27

28 4-2 Follow My Example Owner s equity 5. Current asset 2. Current asset 6. Current liability 3. Long-term liability 7. Property, plant, and equipment 4. Property, plant, and equip. 8. Current liability For Practice: PE 4-4A, PE 4-4B 28

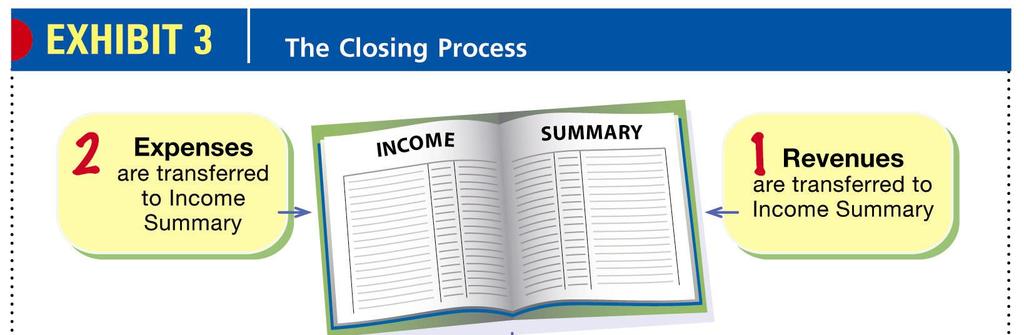

29 4-3 Objective 3 Prepare closing entries. 29

30 4-3 Accounts that are relatively permanent from year to year are called real accounts. Accounts that report amounts for only one period are called temporary accounts or nominal accounts. 30

31 4-3 To report amounts for only one period, temporary accounts should have zero balances at the beginning of the period. At the end of the period the revenue and expense account balances are transferred to Income Summary. 31

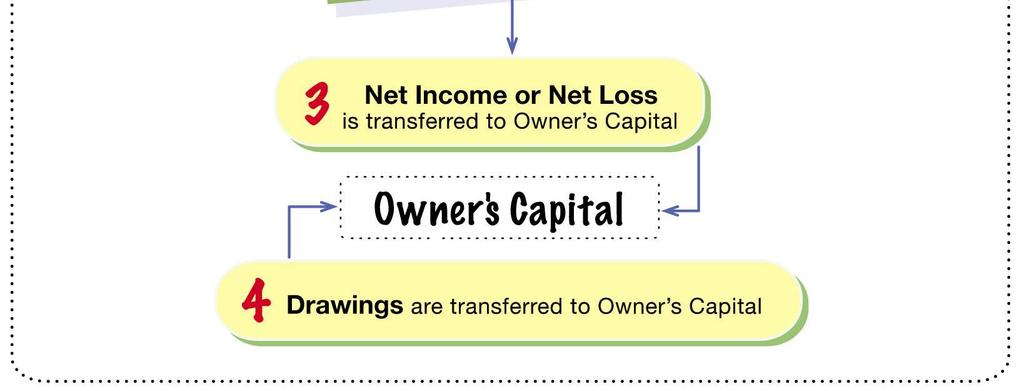

32 4-3 The balance of Income Summary is then transferred to the owner s capital account. The balance of the owner s drawing account is also transferred to the owner s capital account. The entries that transfer these balances are called closing entries. 32

33 4-3 33

34 4-3 Debit each revenue account for the amount of its balance, and credit Income Summary for the total revenue. Fees Earned Income Summary 16,840 Bal. 16,840 16,960 Rent Revenue 120 Bal

35 Wages Expense 4-3 Bal. 4,525 4,525 Income Summary Rent Expense Bal. 1,600 1,600 Depreciation Expense Bal ,855 16,960 Utilities Expense Bal Supplies Expense Bal. 2,040 2,040 Insurance Expense Bal Miscellaneous Expense Bal Debit Income Summary for the total expenses and credit each expense account for its balance. 35

36 Income Summary 9,855 7,105 16, Chris Clark, Capital Bal. 25,000 7,105 Chris Clark, Drawing Bal. 4,000 Debit Income Summary for the amount of its balance (in this case, the net income) and credit the capital account. 36

37 4-3 Chris Clark, Capital 4,000 Bal. 25,000 7,105 Chris Clark, Drawing Bal. 4,000 4,000 Debit the capital account for the balance of the drawing account, and credit drawing for the same amount. 37

38 4-3 Step 1 Step 2 Step 3 Step 4 38

39 4-3 After the closing entries are posted, all of the temporary accounts have zero balances. 39

40 4-3 Example Exercise The After following the accounts accounts have appear been adjusted in the adjusted at July 31, trial the balance end of of the fiscal Hindsight year, Consulting. the following Indicate balances whether are taken each from account the ledger would of be Cabriolet reported in Services the (a) current Co. asset; (b) property, plant, and equipment; (c) Terry current Lambert, liability, Capital (d) long-term $615,850 liability; or (e) owner s equity Terry section Lambert, of the Drawing December 31, 2007, 25,000 balance sheet of Hindsight Fees Consulting. Earned 380,450 Wages Expense 250,000 Rent Expense 65,000 Supplies Expense 18,250 Miscellaneous Expense 6,200 Journalize the four entries required to close the accounts. 40

41 Follow My Example July 31 Fees Earned 380,450 Income Summary 380, Income Summary 339,450 Wages Expense 250,000 Rent Expense 65,000 Supplies Expense 18,250 Miscellaneous Expense 6, Income Summary 41,000 Terry Lambert, Capital 41, Terry Lambert, Capital 25,000 Terry Lambert, Drawing 25,000 For Practice: PE 4-5A, PE 4-5B 41

42 Exhibit 7 Post-Closing Trial Balance NetSolutions Post-Closing Trial Balance December 31, 2007 Cash Accounts Receivable Supplies Prepaid Insurance Land Office Equipment Accumulated Depreciation Accounts Payable Wages Payable Unearned Rent Chris Clark, Capital

43 4-4 Objective 4 Describe the accounting cycle. 43

44 4-4 The accounting process that begins with analyzing and journalizing transactions and ends with preparing the accounting records for the next period s transactions is called the accounting cycle. There are ten steps in the accounting cycle. 44

45 The Accounting Cycle Transactions are analyzed and recorded in the journal. 2. Transactions are posted to the ledger. 3. An unadjusted trial balance is prepared. 4. Adjustment data are assembled and analyzed. 5. An optional end-of-period spreadsheet (work sheet) is prepared. Continued 45

46 6. Adjusting entries are journalized and posted to the ledger. 7. An adjusted trial balance is prepared. 8. Financial statements are prepared. 9. Closing entries are journalized and posted to the ledger. 10. A post-closing trial balance is prepared

47 Example Exercise The From following the following accounts list of appear steps in the adjusted accounting trial cycle, balance identify of what Hindsight two steps Consulting. are missing. Indicate whether each account would be a. reported Transactions in the (a) are current analyzed asset; (b) and property, recorded plant, in the and journal. b. equipment; Transactions (c) current are posted liability, to (d) the long-term ledger. liability; or (e) c. owner s Adjustment equity section data are of the assembled December and 31, analyzed. 2007, balance sheet of Hindsight Consulting. d. An optional end-of-period spreadsheet (work sheet) is prepared. e. Adjusting entries are journalized and posted to the ledger. f. Financial statements are prepared. g. Closing entries are journalized and posted to the ledger. h. A post-closing trial balance is prepared

the preparation of an unadjusted trial")

.")

48 4-4 Follow My Example 4-6 The following two steps are missing: (1) the preparation of an unadjusted trial balance and (2) the preparation of the adjusted trial balance. The unadjusted trial balance should be prepared after step (b). The adjusted trial balance should be prepared after step (e). For Practice: PE 4-6A, PE 4-6B 48

49 4-5 Objective 5 Illustrate the accounting cycle for one period. Refer to the textbook for this extended illustration. 49

50 4-6 Objective 6 Explain what is meant by the fiscal year and the natural business year. 50

51 4-6 The annual accounting period adopted by a business is known as its fiscal year. When a business adopts a fiscal year that ends when business activities have reached the lowest point in its annual operation, such a fiscal year is also called the natural year. 51

52 Financial History of a Business 4-6 The financial history of a business may be shown by a series of balance sheets and income statements, as displayed below. 52

53 Appendix End-of-Period Spreadsheet (Work Sheet) 53

54 The end-of-period spreadsheet (work sheet) shown in the following slides does not have the usual spreadsheet headings due to space constraints. 54

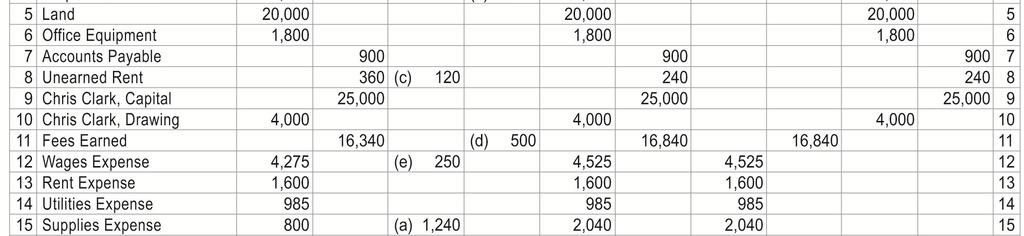

55 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 Supplies 2,000 Prepaid Insurance 2,400 Land 20,000 Office Equipment 1,800 Accounts Payable 900 The Unearned Rent 360 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 Wages Expense 4,275 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 Miscellaneous Expense ,600 42,600 unadjusted trial balance is checked for equality. 55

56 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Cost of Unearned Rent 360 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 Wages Expense 4,275 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 Miscellaneous Expense ,600 42,600 (a) 1,240 supplies on hand at end of period is $

57 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 (b) 200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 The Unearned Rent 360 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 Wages Expense 4,275 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense ,600 42,600 Insurance Expense (b) 200 Accounts are added as needed. insurance expense for December is $200 ($2,400/12) 57

58 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 (b) 200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Rent revenue 8 Unearned Rent 360 (c) 120 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 Wages Expense 4,275 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense ,600 42, Insurance Expense (b) 200 Rent Revenue (c) 120 earned during December was $

59 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 (b) 200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Wages Unearned Rent 360 (c) 120 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 Wages Expense 4,275 (d) 250 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense ,600 42,600 Insurance Expense (b) 200 Rent Revenue (c) 120 Wages Payable (d) 250 accrued but not paid at the end of December totaled $

60 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 (e) 500 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 (b) 200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Unearned Rent 360 (c) 120 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 Wages Expense 4,275 (d) 250 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense ,600 42,600 (e) 500 Insurance Expense (b) 200 Rent Revenue (c) 120 Wages Payable (d) 250 Fees accrued at the end of December but not recorded total $

61 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 (e) 500 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 (b) 200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Unearned Rent 360 (c) 120 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 (e) 500 Wages Expense 4,275 (d) 250 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense ,600 42,600 Insurance Expense (b) 200 Rent Revenue (c) 120 Wages Payable (d) 250 Depreciation Expense (f) 50 Accum. Depreciation (f) 50 Depreciation of office equipment is $50 for December. 61

62 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 (e) 500 Supplies 2,000 (a) 1,240 To make Prepaid Insurance 2,400 (b) 200 Land 20,000 more Office Equipment 1,800 Accounts Payable 900 Unearned Rent 360 (c) 120 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 (e) 500 Wages Expense 4,275 (d) 250 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense ,600 42,600 Insurance Expense (b) 200 Rent Revenue (c) 120 Wages Payable (d) 250 Depreciation Expense (f) 50 Accum. Depreciation (f) 50 space, let s remove the heading. 62

63 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 (e) 500 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 (b) 200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Unearned Rent 360 (c) 120 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 (e) 500 Wages Expense 4,275 (d) 250 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense 455 Insurance Expense 42,600 42,600 (b) 200 Rent Revenue (c) 120 Wages Payable (d) 250 Summed and ruled Depreciation Expense (f) 50 Accum. Depreciation (f) 50 2,360 2,360 63

64 The next step is to add or subtract the adjustments from (to) the amounts found in the Unadjusted Trial Balance columns and enter the results in the Adjusted Trial Balance columns. 64

65 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,220 (e) 500 Supplies 2,000 (a) 1,240 Prepaid Insurance 2,400 (b) 200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Unearned Rent 360 (c) 120 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,340 (e) 500 Wages Expense 4,275 (d) 250 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 800 (a) 1,240 Miscellaneous Expense 455 Insurance Expense 42,600 42,600 (b) 200 Rent Revenue (c) 120 Wages Payable (d) 250 Depreciation Expense (f) 50 Accum. Depreciation (f) 50 2,360 2,

66 Unadjusted Adjusted Trial Balance Adjustments Trial Balance Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 2,065 Accounts Receivable 2,220 (e) 500 2,720 Supplies 2,000 (a) 1, Prepaid Insurance 2,400 (b) 200 2,200 Land 20,000 20,000 Office Equipment 1,800 1,800 Accounts Payable Unearned Rent 360 (c) Chris Clark, Capital 25,000 25,000 Chris Clark, Drawing 4,000 4,000 Fees Earned 16,340 (e) ,840 Wages Expense 4,275 (d) 250 4,525 Rent Expense 1,600 1,600 Utilities Expense Supplies Expense 800 (a) 1,240 2,040 Miscellaneous Expense Insurance Expense 42,600 42,600 (b) Rent Revenue (c) Wages Payable (d) Depreciation Expense (f) Accum. Depreciation (f) ,360 2,360 43,400 43,400 66

67 Because of space constraints, the Unadjusted Trial Balance and the Adjustments columns will not be shown in the following slides. 67

68 Adjusted Trial Balance Income Statement Balance Sheet Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,720 Supplies 760 Prepaid Insurance 2,200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Unearned Rent 240 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,840 Wages Expense 4,525 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 2,040 Miscellaneous Expense 455 Insurance Expense 200 Rent Revenue 120 Wages Payable 250 Depreciation Expense 50 Accum. Depreciation 50 43,400 43,400 68

69 The next step is to extend amounts in the Adjusted Trial Balance columns to the Income Statement and Balance Sheet columns. 69

70 Adjusted Trial Balance Income Statement Balance Sheet Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 Accounts Receivable 2,720 Supplies 760 Prepaid Insurance 2,200 Land 20,000 Office Equipment 1,800 Accounts Payable 900 Unearned Rent 240 Chris Clark, Capital 25,000 Chris Clark, Drawing 4,000 Fees Earned 16,840 Wages Expense 4,525 Rent Expense 1,600 Utilities Expense 985 Supplies Expense 2,040 Miscellaneous Expense 455 Insurance Expense 200 Rent Revenue 120 Wages Payable 250 Depreciation Expense 50 Accum. Depreciation 50 43,400 43,

71 Adjusted Trial Balance Income Statement Balance Sheet Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 2,065 Accounts Receivable 2,720 2,720 Supplies Prepaid Insurance 2,200 2,200 Land 20,000 20,000 Office Equipment 1,800 1,800 Accounts Payable Unearned Rent Chris Clark, Capital 25,000 25,000 Chris Clark, Drawing 4,000 4,000 Fees Earned 16,840 16,840 Wages Expense 4,525 4,525 Rent Expense 1,600 1,600 Utilities Expense Supplies Expense 2,040 2,040 Miscellaneous Expense Insurance Expense Rent Revenue Wages Payable Depreciation Expense Accum. Depreciation ,400 43,400 71

72 The Income Statement and Balance Sheet columns are totaled. 72

73 Adjusted Trial Balance Income Statement Balance Sheet Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 2,065 Accounts Receivable 2,720 2,720 Supplies Prepaid Insurance 2,200 2,200 Land 20,000 20,000 Office Equipment 1,800 1,800 Accounts Payable Unearned Rent Chris Clark, Capital 25,000 25,000 Chris Clark, Drawing 4,000 4,000 Fees Earned 16,840 16,840 Wages Expense 4,525 4,525 Rent Expense 1,600 1,600 Utilities Expense Supplies Expense 2,040 2,040 Miscellaneous Expense Insurance Expense Rent Revenue Wages Payable Depreciation Expense Accum. Depreciation ,400 43,400 73

74 Adjusted Trial Balance Income Statement Balance Sheet Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 2,065 Accounts Receivable 2,720 2,720 Supplies Prepaid Insurance 2,200 2,200 Land 20,000 20,000 Office Equipment 1,800 1,800 Accounts Payable Unearned Rent Chris Clark, Capital 25,000 25,000 Chris Clark, Drawing 4,000 4,000 Fees Earned 16,840 16,840 Wages Expense 4,525 4,525 Rent Expense 1,600 1,600 Utilities Expense Supplies Expense 2,040 2,040 Miscellaneous Expense Insurance Expense Rent Revenue Wages Payable Depreciation Expense Accum. Depreciation ,400 43,400 9,855 16,960 33,545 26,440 74

75 The net income or net loss is determined. Then the Income Statement and Balance Sheet columns are totaled and double-ruled. 75

76 Adjusted Trial Balance Income Statement Balance Sheet Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 2,065 Accounts Receivable 2,720 2,720 Supplies Prepaid Insurance 2,200 2,200 Land 20,000 20,000 Office Equipment 1,800 1,800 Accounts Payable Unearned Rent Chris Clark, Capital 25,000 25,000 Chris Clark, Drawing 4,000 4,000 Fees Earned 16,840 16,840 Wages Expense 4,525 4,525 Rent Expense 1,600 1,600 Utilities Expense Supplies Expense 2,040 2,040 Miscellaneous Expense Insurance Expense Rent Revenue Wages Payable Depreciation Expense Accum. Depreciation ,400 43,400 9,855 16,960 33,545 26,440 76

77 Adjusted Trial Balance Income Statement Balance Sheet Account Title Debit Credit Debit Credit Debit Credit Cash 2,065 2,065 Accounts Receivable 2,720 2,720 Supplies Prepaid Insurance 2,200 2,200 Land 20,000 20,000 Office Equipment 1,800 1,800 Accounts Payable Unearned Rent Chris Clark, Capital 25,000 25,000 Chris Clark, Drawing 4,000 4,000 Fees Earned 16,840 16,840 Wages Expense 4,525 4,525 Rent Expense 1,600 1,600 Utilities Expense Supplies Expense 2,040 2,040 Miscellaneous Expense Insurance Expense Rent Revenue Wages Payable Depreciation Expense Accum. Depreciation ,400 43,400 9,855 16,960 33,545 26,440 Net income 7,105 7,105 16,960 16,960 33,545 33,545

78 Net Income Income Statement Balance Sheet 9,855 16,960 33,545 26,440 7,105 7,105 16,960 16,960 33,545 33,545 Net Income The difference between the Income Statement column totals is the net income (or net loss) for the period. 78

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Cash. Laundry Equipment. Hilda Dinero, Capital Oct. 31 Clos. 1,000 Oct. 31 Bal. 18, Clos. 12, Bal. 30,200

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

2014 Mar. 31 Balance 30, Adjusting 26 22,500 7, Mar. 31 Balance 3, Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Dec. 4: Paid $ 750 cash for office supplies. Date Accounts Debit Credit Dec. 4 Office Supplies 750 Cash 750

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Enter account titles and their unadjusted balances in the Trial Balance columns Total the amounts

Process by which companies produce their financial statements Chapter 4 Copyright 2009 Prentice Hall. All rights reserved 2 Journalize Transaction Post to Accounts Adjust Accounts Prepare an accounting

Process by which companies produce their financial statements Chapter 4 Copyright 2009 Prentice Hall. All rights reserved 2 Journalize Transaction Post to Accounts Adjust Accounts Prepare an accounting

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Learning Outcomes. The Basic Accounting Cycle

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

SOLUTIONS. Learning Goal 13

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Problem 5-3A (90 minutes) Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011

Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011") Solution Manual for Chapter 5 354 Problem 5-3A (90 minutes) Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011 Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income

Solution Manual for Chapter 5 354 Problem 5-3A (90 minutes) Part 1 CHALLENGER CONSTRUCTION Work Sheet For Year Ended September 30, 2011 Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

a) Post-closing trial balance c) Income statement d) Statement of retained earnings

Post-closing trial balance c) Income statement d) Statement of retained earnings") Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 3 The Adjusting Process 2 After studying

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 3 The Adjusting Process 2 After studying

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY. Y. Chang Company COVER SHEET

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

DE ANZA COLLEGE Accounting 1A Comprehensive Problem for Lawrence Scott Osborne's Class ONLY Y. Chang Company COVER SHEET The purpose of this project is to give you experience doing manual accounting. You

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS EXTERNAL TRANSACTIONS INTERNAL TRANSACTIONS NON-TRANSACTIONAL EVENTS Involves an

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS EXTERNAL TRANSACTIONS INTERNAL TRANSACTIONS NON-TRANSACTIONAL EVENTS Involves an

Graded Project. Lesson 1: Business Accounting and You OVERVIEW INSTRUCTIONS

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Chapter 5 Accrual Adjustments and Financial Statement Preparation. Revenue recognition Matching expenses to revenues Expenses related to periods

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

CHAPTER 3 Selected Solutions. The Accounting Information System. Brief Topics Questions Exercises Exercises Problems

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 3. Learning Objectives. Distinguish accrual accounting from cash-basis accounting. Objective 1. The Adjusting Process

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 4 Completing the Accounting Cyclt 163

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry.

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts:

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

COMPLETING THE ACCOUNTING CYCLE

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 4 Completing the Accounting Cycle Study Guide Do You Know?

Chapter 4 Completing the Accounting Cycle Study Guide Do You Know? Learning Objective 1: Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and

Chapter 4 Completing the Accounting Cycle Study Guide Do You Know? Learning Objective 1: Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and

Answer: b Rationale: Journalizing means to record a transaction in a general journal.

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

Heintz & Parry. 20 th Edition. College Accounting

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

Heintz & Parry 20 th Edition College Accounting Chapter 3 The Double-Entry Framework 1 Define the parts of a T account. SHAPED LIKE a T Debit Credit Debit means Left Debit Credit Credit means Right Abbreviation

REINFORCEMENT ACTIVITY 3, Part B, p. 715

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

Week 5, Chap 4 Part 1

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

ACCOUNTING. The Wonder of the Worksheet

ACCOUNTING The Wonder of the Worksheet SAC 2012 P a g e 2 2012 State Group 11 Refer to the Table and to the work sheet. For questions 53 through 59, write the identifying letter of the best response on

ACCOUNTING The Wonder of the Worksheet SAC 2012 P a g e 2 2012 State Group 11 Refer to the Table and to the work sheet. For questions 53 through 59, write the identifying letter of the best response on

Recording Business Transactions

2-1 Recording Business Transactions Atanas Atanasov Assist.prof., University of Economics - Varna 2-2 Tools of The Recording Process Debits and Credits Journal Entries Ledger Accounts First, however, let

2-1 Recording Business Transactions Atanas Atanasov Assist.prof., University of Economics - Varna 2-2 Tools of The Recording Process Debits and Credits Journal Entries Ledger Accounts First, however, let

CHAPTER 3. The Adjusting Process. Chapter Overview

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

On October 1, 2010, Cody Doerr established Banyan Realty, which completed the following transaction during the month:

Pr 2-2 A page 91 On October 1, 2010, Cody Doerr established Banyan Realty, which completed the following transaction during the month: A. Cody Doerr transferred cash from a personal bank account to an

Pr 2-2 A page 91 On October 1, 2010, Cody Doerr established Banyan Realty, which completed the following transaction during the month: A. Cody Doerr transferred cash from a personal bank account to an

Annie s Animal Care Practice with Adjusting Entries

Overview One of your friends, Annie, owns a local animal kennel called Annie s Animal Care. Refer to the Chart of Accounts and Business Transactions listed below and then complete the Journal and Ledger

Overview One of your friends, Annie, owns a local animal kennel called Annie s Animal Care. Refer to the Chart of Accounts and Business Transactions listed below and then complete the Journal and Ledger

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

CPT Chapter2, Unit-3 Fundamentals of Accountancy CA.S.K.Chhabra What is a Trial balance? It is a Statement prepared to ensure the arithmetical accuracy of all the accounts before the preparation of the

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Chapter 5 Accrual Adjustments and Financial Statement Preparation. Revenue recognition Matching expenses to revenues Expenses related to periods

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Weygandt, Kieso, Kimmel, Trenholm, Kinnear, Barlow, Atkins: Principles of Financial Accounting, Canadian Edition CHAPTER 4

CHAPTER 4 Completion of the Accounting Cycle ASSIGNMENT CLASSIFICATION TABLE Study Objectives 1. Prepare closing entries and a postclosing trial balance. 2. Explain the steps in the accounting cycle including

CHAPTER 4 Completion of the Accounting Cycle ASSIGNMENT CLASSIFICATION TABLE Study Objectives 1. Prepare closing entries and a postclosing trial balance. 2. Explain the steps in the accounting cycle including

Week 3. Topic 3 Chapter 3. ACT102 Introduction to Accounting. Accounting for end of financial period adjustments 21/02/2018

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

THE ACCOUNTING CYCLE: Accruals and Deferrals

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM. MULTIPLE CHOICE Conceptual. Test Bank Chapter 3

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

Record Transactions in the Journal. Copy (post) to the Ledger. Prepare the Trial Balance

to the Ledger. Prepare the Trial Balance") Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Chapter 6 The annual report and accounts. The closure of the accounting cycle and Accounting information disclosed to the public

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176)

") NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 11 Contestant Number: Time: Rank: FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2016 CONCEPT KNOWLEDGE: True/False (20 @ 2 points each) Multiple Choice (25 @ 2 points each) APPLICATION KNOWLEDGE:

Page 1 of 11 Contestant Number: Time: Rank: FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2016 CONCEPT KNOWLEDGE: True/False (20 @ 2 points each) Multiple Choice (25 @ 2 points each) APPLICATION KNOWLEDGE:

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

The Accounting Cycle Revised Edition

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

BUS210. Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information

BUS210 Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information Connecting the Accounting Equation with Transactions: Journal Entries, T Accounts E4-9 Prepare journal entries for each cash transaction

BUS210 Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information Connecting the Accounting Equation with Transactions: Journal Entries, T Accounts E4-9 Prepare journal entries for each cash transaction

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything!

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

XI ACCOUNTING REGULAR / PRIVATE. S.Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net